VT Tyndall Real Income Fund - Tyndall Investment Management

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

VT Tyndall Real Income Fund

Weekly Commentary | 30th April 2021

Are we nearly there yet?

Stock markets, as we know, are forward looking in nature and frequently move to price in events yet

to happen. The phrase ‘travelling and arriving’ is a common one in relation to share price

movements, essentially saying that by the time much anticipated ‘news’ hits the screen the share

price has already factored it in ahead of time.

With this in mind, we are having more and more discussions lately concerning whether or not the

market has already fully priced the ‘reopening’ of the UK economy post lockdown. We will, of

course, only know the answer for sure as time goes by. As it stands today though, our inclination is

to think that is not currently the case and there is still plenty to go for in UK reopening opportunities,

particularly consumer exposed stocks.

There are several issues to think about when framing this debate and it starts with the scale of the

economic hit the UK suffered in 2020. As we have mentioned previously, GDP growth of -9.9% was

the worst yearly outturn for over 300 years. As such, the potential for an equally vigorous upside

surprise to economic activity clearly exists as we exit our third and, hopefully, final national

lockdown.

Whilst the economic contraction was incredibly sharp in 2020 it was also extremely unusual, being

driven as it was, by the enforced closure of much of the economy. The quid pro quo for enforced

closure was truly unprecedented support from the government for businesses and individuals alike,

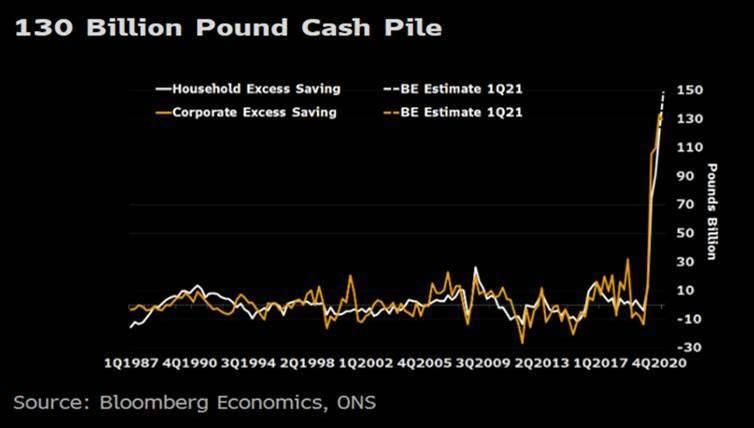

and one of the consequences of this support has been a quite exceptional build-up of corporate and

household excess savings, as the chart below clearly demonstrates.

Those excess savings, particularly on the household side, are a key reason why we think there is still

plenty more scope for UK consumer related stocks to perform strongly as we emerge from

lockdown. There are numerous anecdotal signs of significant ‘pent up’ demand after over a year of

rolling lockdowns and households, generally, have the financial capacity to fulfil that demand.

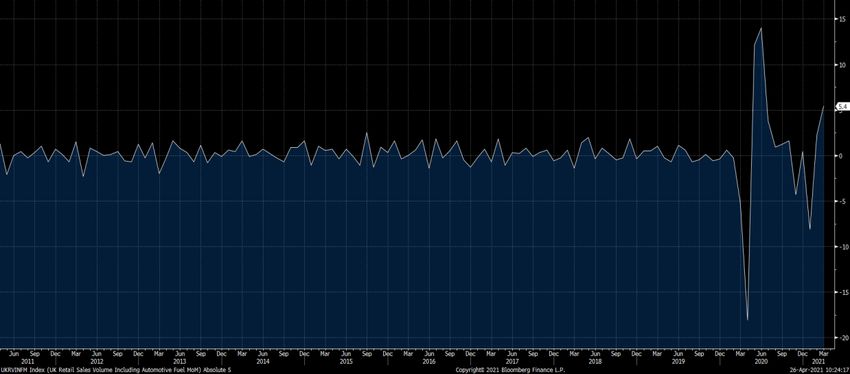

Another reason we remain so optimistic is the underlying strength of the UK housing market, a key indicator if ever there was one, for the financial health of UK consumers. Not only did UK housing surprise positively with its resilience in 2020 but, as the chart below from Rightmove of month-on- month national asking price changes demonstrates, the market appears to be accelerating strongly in early 2021. Finally, the actual evidence on the ground also appears highly encouraging, as the latest UK retail sales volume data from the Office for National Statistics (below) indicates. Very strong +5.4% volume growth was seen in March, before non-essential physical stores had even reopened on 12th April. So, we feel pretty optimistic that a sustained period of consumer strength, probably surpassing current positive expectations, is likely still to come in the UK. Furthermore, when we drill down into individual stocks in the area, we still find plenty of valuation appeal. Three of our favourite stocks in the consumer space are JD Wetherspoon (pubs), DFS Furniture (sofas) and Next (clothing and homeware). All three have incredibly strong franchises and all, in our opinion, will emerge from the pandemic in a stronger position relative to their competition than when they went in. DFS, for example, estimate they have taken an additional 2% market share nationally over the last year as weaker players have exited the industry. They now have an estimated 34% market share, over 3 times bigger than their nearest competitor.

The charts below, from Redburn Ideas, show all 3 companies’ profiles in terms of relative estimates momentum (left chart) and return on capital (right chart). From an estimate perspective both DFS and Next have already been surprising positively, reflecting the strength of their online propositions during lockdown. JD Wetherspoon, clearly, has not yet started surprising positively as their pubs have remained largely closed along with the rest of the hospitality industry. What’s most interesting to us though, in each case, is the far right column of the right hand chart. For each company the market is not yet, in our opinion, pricing future returns on capital in any way excessively optimistically. In fact, we fully expect those return on capital ‘blue bars’ to continue rising back towards levels more akin to historical performance in due course. On that basis there would appear to be plenty of scope for further substantial share price recovery from here. Our answer therefore is that, no, we aren’t nearly there yet. The UK consumer space still offers plenty of alpha opportunities as the economy reopens, and our fund is really well positioned to take full advantage. Simon Murphy, Fund Manager, VT Tyndall Real Income Fund, 30th April 2021 Data source (unless otherwise stated): Bloomberg Contact Details: Fund Manager – smurphy@tyndallim.co.uk Sales Director - hnolan@tyndallim.co.uk

Disclaimer WARNING: All information about the VT Tyndall Real Income Fund (‘The Fund’) is available in The Fund’s prospectus and Key Investor Information Document which are available free of charge (in English) from Valu-Trac Investment Management Limited (www.valu-trac.com). Any investment in the fund should be made on the basis of the terms governing the fund and not on the basis of any information provided herein. The information in this Report is presented using all reasonable skill, care and diligence and has been obtained from or is based on third party sources believed to be reliable but is not guaranteed as to its accuracy, completeness or timeliness, nor is it a complete statement or summary of any securities, markets or developments referred to. The information within this Report should not be regarded by recipients as a substitute for the exercise of their own judgement. The information in this Report has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient and is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. In the absence of detailed information about you, your circumstances or your investment portfolio, the information does not in any way constitute investment advice. If you have any doubt about any of the information presented, please consult your stockbroker, accountant, bank manager or other independent financial advisor. Value of investments can fall as well as rise and you may not get back the amount you have invested. Income from an investment may fluctuate in money terms. If the investment involves exposure to a currency other than that in which acquisitions of the investments are invited, changes in the rates of exchange may cause the value of the investment to go up or down. Past performance is not necessarily a guide to future performance. Any opinions expressed in this Report are subject to change without notice and Tyndall Investment Management is not under any obligation to update or keep current the information contained herein. Sources for all tables and graphs herein are Valu-Trac Investment Management Limited unless otherwise indicated. The information provided is "as is" without any express or implied warranty of any kind including warranties of merchantability, non-infringement of intellectual property, or fitness for any purpose. Because some jurisdictions prohibit the exclusion or limitation of liability for consequential or incidental damages, the above limitation may not apply to you. Users are therefore warned not to rely exclusively on the comments or conclusions within the Report but to carry out their own due diligence before making their own decisions. Employees of Tyndall Investment Management, or individuals connected to them, may have or have had interests of long or short positions in, and may at any time make purchases and/or sales as principal or agent in, the relevant securities or related financial instruments discussed in this Report. © 2021 Tyndall Investment Management. Tyndall Investment Management is a trading name of Odd Asset Management. Authorised and regulated by the Financial Conduct Authority (UK), registration number 660915. This status can be checked with the FCA on 0845 730 0104 or on the FCA website (UK). All rights reserved. No part of this Report may be reproduced or distributed in any manner without the written permission of Tyndall Investment Management. Investment Manager: 5-8 The Sanctuary, London, SW1P 3JP.

You can also read