Algeria Marocco Tunisia - Confindustria Vicenza - 27 febbraio 2018 www.pwc-tls.it

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

www.pwc-tls.it

www.pwc.com

Algeria Marocco Tunisia

Confindustria Vicenza - 27 febbraio 2018

Strictly private

and confidential

Sommario

Sezione Titolo Page

1 Aspetti Fiscali 3

1.1 Società residenti 5

1.2 Società non residenti 8

1.3 Ritenute di imposta 10

1.4 Altri aspetti 15

2 Aspetti Societari 24

3 I nostri riferimenti 31

1 Aspetti Fiscali Aspetti Fiscali Algeria Marocco Tunisia 3

1 Aspetti Fiscali

Premessa

Altre fonti

PwC

Alger - PwC Worldwide Tax Summaries

05 Rue Mohamed Saadi (Ex Rue Raoul Payen) Hydra

Alger, 16035 https://www.pwc.com/gx/en/services/tax/worldwide-tax-

Algeria summaries.html

Casablanca - International Bureau of Fiscal Documentation

35 rue Aziz Bellal http://www.ibfd.org/

Mâarif - Repubblica Alerina – Direzione Generale delle Imposte

Casablanca, 20 330

https://www.mfdgi.gov.dz/

Morocco

- Repubblica Tunisina – Ministero delle Finanze

Tunis

Imm. PwC Rue du Lac d'Annecy http://www.finances.gov.tn/index.php?lang=fr

Les Berges du Lac - Marocco – General Tax Administration

1053 Tunis

https://portail.tax.gov.ma/wps/portal/DGI-Ang/Dgi-Internet-

Tunisia

Ang/Home/

Algeria Marocco Tunisia 4

PwC TLS | Avvocati e Commercialisti

1.1 Società residenti Società residenti Algeria Marocco Tunisia 5

Local authority tax (LAT): LAT is payable by entities subject to corporate tax, except

entities operating in the tourism sector.

The LAT is paid to the local authority monthly, at the rate of:

1.1 Società residenti

- 0.2% of the total turnover of the entity, with a minimum calculated on the basis of the

number of square metres of construction used by the entity.

Società residenti (1/2) - 0.1% of the turnover deriving from exportation as defined by the legislation in force.

Algeria Morocco T unisia

T ax Feature

Last reviewed: 1 February 2018 Last reviewed: 31 January 2018 Last reviewed: 1 January 2018

Residence Residence is based on incorporation A company is deemed to be resident A company is resident in Tunisian if it

in Morocco if it has its legal seat is incorporated in Tunisia

there

T ax base Territorial (active income) Territorial (active income) Territorial (active income)

Worldwide (passive income) Worldwide (passive income) Worldwide (passive income)

Corporate tax rates 19% for manufacturing activities Proportional rates: 10%, 20%, and 25% standard rate

31% (over MAD 1 million)

23% for construction, public works 35% for financial institutions,

and hydraulic activities in addition to 37% (credit institutions, leasing, telecommunication and hydrocarbon

IBS tourism and spa activities except insurance/reinsurance companies, companies

Impôt sur le Bénéfice travel agencies Deposit Bank and Bank Al Maghreb)

des Sociétés 35% for large retail companies and

26% for other activities (including 17,5% (companies exporting companies exploiting a foreign brand

trade and services) products or services) (as of 1 January 2019)

Tax on business activity (TAP) at the rate 10% (regional headquarters and 20% for small and medium size

of 1% for manufacturing activities, without representative offices of multinational companies

any reduction. However, this tax is fixed companies with Casablanca Finance

at 2% for all other activities, with a City status; offshore banks) 15% for newly listed companies (for

reduction of 25% for some activities and a 5-year period)

locations, and computed based on the 8.75% (companies operating in

invoiced turnover. export free zones; for products sold 10% for export companies (as of 1

to enterprises located outside export January 2014)

free zones; financial institutions,

professional services providers, and In addition, a 1% social solidarity

holding companies with the contribution is applicable as of 1

Casablanca Finance City status) January 2018

Algeria Marocco Tunisia 6

PwC TLS | Avvocati e Commercialisti1.1 Società residenti

Società residenti (2/2)

Algeria Morocco

Tunisia

Tax Feature Last reviewed: 1 February Last reviewed: 31 January

Last reviewed: 1 January 2018

2018 2018

Alternative minimum tax Minimum tax of DZD 10,000 Payable at the rate of 0.5% on 0.2% of revenues, but not lower

applies on a yearly basis turnover than TND 500

A special 0.25% rate is 0.1% of revenues from exports

applicable in the following activities, but not lower than TND

sectors: oil products, gas, butter, 300

oil, sugar, water, flour and

electricity

The minimum levy may not be

lower than MAD 3,000

Capital gains Yes, part of business income Yes, part of business income; Yes, part of business income

Exemption for listed shares and Exempt for venture capital funds 0% on disposal of shares listed

intra-group share transfers and UCITS on the Tunis Stock Exchange

under certain conditions

Loss carry-forward Yes, for 4 years Yes, 4 years Yes, for 5 years

Depreciation relating to a loss- Indefinitely for deferred

making period may be carried depreciation

forward for an unlimited period

Loss carry-back No No No

Unilateral double taxation relief

No No No

Algeria Marocco Tunisia 7

PwC TLS | Avvocati e Commercialisti1.2 Società non residenti Società non residenti Algeria Marocco Tunisia 8

1.2 Società non residenti

Società non residenti

In assenza di DTT.

Solitamente trattasi di ritenute per società non

residenti e senza stabile organizzazione in loco,

con riferimento a redditi di fonte locale

Algeria Morocco

Tunisia

Tax Feature Last rev iewed: 1 February Last rev iewed: 31 January

Last rev iewed: 1 January 2018

2018 2018

Corporate tax rates 19% for manufacturing activities Proportional rates: 10%, 20%, 25% standard rate (or 15% final

and 31% (over MAD 1 million) withholding tax on gross

23% for construction, public payments if carrying on activities

works and hydraulic activities in 8% (on gross contract value for in Tunisia through a non-

addition to tourism and spa certain foreign contractors) registered PE)

activities except travel agencies

35% for financial institutions,

26% for other activities (including telecommunication and

trade and services) hydrocarbon companies

In addition, a 1% social solidarity

contribution is applicable as of 1

January 2018

Capital gains on sale of shares 20% Yes, 0% for gains on securities 25% capped at 5% of the

in resident companies listed on the Moroccan stock transfer price

exchange

Some exemptions apply under

certain conditions

Capital gains on sale of Taxed as business income Yes, non-resident companies are A withholding tax of 15% of the

immov able property liable to corporate tax in respect selling price is applicable to the

of any capital gains arising from gains. Non-resident companies

immovable property or from the can opt to treat the withholding

disposal of shares of real estate tax either as a final tax or as a

companies situated in Morocco: credit against the corporate tax

such gains are subject to liability in respect of these capital

corporate tax at the standard rate gains

of 30%

Algeria Marocco Tunisia 9

PwC TLS | Avvocati e Commercialisti1.3 Ritenute di imposta Ritenute di imposta Algeria Marocco Tunisia 10

1.3 Ritenute di imposta

Branch tax set at the rate of 15% calculated on net profits after IBS.

Ritenute di imposta

Under this scenario, a 15% tax rate applies on the deemed distribution

(cash position usually) of profits after tax, which may be reduced or

removed by the applicable DTT provisions

Algeria Morocco

Tunisia

Tax Feature Last reviewed: 1 February Last reviewed: 31 January

Last reviewed: 1 January 2018

2018 2018

Branch profits 15% 15% (on remittance basis) 10%

25% if the non-resident company

is based in a tax haven

Dividends 15% 15%; 10% (as of 1 January 2015) on

profits realized from 1 January

0% on distributions by companies 2014

operating in export free zones

(EFZ) 25% if recipient is resident in a

tax haven

Interest 10% (debts, deposits, 10% 20%

guarantees)

10% for interest paid to non-

40% (bearer securities) resident banks

25% if recipient is resident in a

tax haven

Royalties 4.8% (use of computer software) 10% 15%

24% (other royalties) 25% if recipient is resident in a

tax haven

Fees (technical) 24% 10% 15%

Fees (management) 20% 15% 15%

Algeria Marocco Tunisia 11

PwC TLS | Avvocati e Commercialisti1.3 Ritenute di imposta

Algeria – Ritenute da trattati contro le doppie imposizioni

≥ 25%

Dividends Interest Royalties

Individuals, companies Qualifying companies

(%) (%) (%) (%)

Domestic Rates - Companies 15 15 10/40 4.8/24

Treaty Rates:

Country Individuals, companies Qualifying companies . ..

Austria 15 5 0/10 10

Belgium 15 15 0/15 5/15

China (People's Rep.) 10 5[2] 7 10

Egypt 10 10 5 10

France 15 5 10/12 5/10/12

Germany 15 5 10 10

Italy 15 15 15 5/15

Jordan 15 15 0/15 15

Russia 15 5 15 15

Spain 15 5 5 7/14

Switzerland 15 5 0/10 10

Turkey 12 12 10 10

United Kingdom 15 5 7 10

Algeria Marocco Tunisia 12

PwC TLS | Avvocati e Commercialisti1.3 Ritenute di imposta

Marocco - Ritenute da trattati contro le doppie imposizioni Copyright

letterari

Esenzione per

interessi pagati da/a

autorità statali Dividends Interest Royalties

Companies Qualifying companies [2]

(%) (%) (%) (%)

Domestic Rates - Companies 15 0 10 10

Treaty Rates:

Country 2 3 4

Austria 10 5 0/10 10

Belgium 10 6.5 0/10 10

China (People's Rep.) 10 10 0/10 10

Finland 10 7 0/10 10

France 15 15 10/15[6] 5/10[5]

Germany 15 5 0/10 10

Ireland 10 6 0/10 10

Italy 15 10 0/10 5/10[5]

Malta 10 6.5 0/10 10

Netherlands 25 10 10/25[8] 10

Poland 15 7 10 10

Russia 10 5 0/10 10

Spain 15 10 10 5/10[5]

Switzerland 15 7 10 10

Turkey 10 7 0/10 10

United Kingdom 25 10 10 10

United States 15 10 0/15 10

Algeria Marocco Tunisia 13

PwC TLS | Avvocati e Commercialisti16% trade mark, to cinematograph and television films, to industrial, commercial or scientific equipment

5%literary, artistic or scientific work

1.3 Ritenute di imposta

12% in other cases

Tunisia - Ritenute da trattati contro le doppie imposizioni

Dividends Interest Royalties

Qualifying

Companies

companies

(%) (%) (%) (%)

Domestic Rates - Companies 5/25 5/25 0/5/20/25 0/15/25

Treaty Rates:

Country 2 3 4

Austria 20 10 10 10/15

[3] [4]

Belgium 15 5 5/10 11

China (People's Rep.) 8 8 10 5/10

France No Limitation No Limitation 12 5/10/15/20

Germany 15 10 10 10/15

Italy 15 15 12 5/12/16

Malta 10 10 0/12 12

Netherlands 20 0 0/7.5[8] 7.5/11[8]

Norway 20 20 12 5/15/20

Oman 0 0 10 5

Spain 15 5 5/10 10

Switzerland 10 10 10 10

Turkey 15 12 10 10

United Kingdom 20 12 10/12 15

United States 20 14 15 10/15

Algeria Marocco Tunisia 14

PwC TLS | Avvocati e Commercialisti1.4 Altri aspetti Altri aspetti Algeria Marocco Tunisia 15

1.4 Altri aspetti

Norme anti abuso Increasing from 500,000 Algerian dinars (DZD) to

DZD 2 million the penalty amount relating to a failure

to provide or an incomplete production of transfer

pricing documentation

Algeria Morocco Tunisia

Tax Feature Last reviewed: 1 February Last reviewed: 31 January Last reviewed: 1 January

2018 2018 2018

Transfer pricing Yes (and transfer pricing Yes Yes, only a general principle

legislation documentation requirements for

companies under the Large

Taxpayers Unit)

Thin capitalization No No No

legislation

Controlled foreign No No No

company legislation

General anti-avoidance Yes (based on the abuse of law No No

rule (GAAR) concept)

Other anti-avoidance No No Yes, anti-tax havens rules in the

legislation form of higher withholding tax

rates if recipient is resident in a

tax haven. In addition, the

expenses paid to such persons

are not deductible

Algeria Marocco Tunisia 16

PwC TLS | Avvocati e Commercialisti1.4 Altri aspetti

Indirette

Algeria Morocco Tunisia

Tax Feature Last reviewed: 1 Last reviewed: 31 Last reviewed: 1

February 2018 January 2018 January 2018

Taxable events Supply of goods Sales and deliveries of Supply of goods (including

goods (also of imported importation) and services

Supply of services goods);

Supply of services

VAT (standard) 19% 20% 19%

VAT (reduced) 9% 0%, 7%, 10%, 14% 0%, 7%, 13%

VAT (increased) No No No

Registration/deregis DZD 100,000 MAD 2 million (for TND 100,000 (retailers)

tration threshold wholesalers and retailers)

VAT group No No No

Algeria Marocco Tunisia 17

PwC TLS | Avvocati e Commercialisti1.4 Altri aspetti

Altro

Algeria Morocco

Tunisia

Tax Feature Last reviewed: 1 February Last reviewed: 31 January

Last reviewed: 1 January 2018

2018 2018

Currency Algerian dinar (DZD) Moroccan dirham (MAD) Tunisian dinar (TND)

International financial transactions

are subject to the control of the

Moroccan Exchange Office ( Office

des Changes )

Remittances of capital to non-

Yes, foreign exchange control Yes, a request for a pre-approval

residents are guaranteed

Foreign exchange control approval is required for certain must be filed with the Tunisian

types of payments Central Bank

No limitations are imposed on the

time or amount of profit remitted

Loans, however, must be

authorized by the Office of

Exchange

Algeria Marocco Tunisia 18

PwC TLS | Avvocati e Commercialisti1.4 Altri aspetti

Consolidato fiscale e incentivi

Algeria Morocco Tunisia

Tax Feature Last reviewed: 1 February Last reviewed: 31 January Last reviewed: 1 January

2018 2018 2018

Consolidato fiscale Yes No Yes

Export companies

Export free zones Investment in certain regions

Regional development areas

Tourism Investment banks and companies

Oil and gas activities

Agriculture sector Small and medium-sized

Incentivi companies

CIT reduction for listed

Hydrocarbons sector

companies

Agriculture and fishing sectors

Investment in certain regions

Employment creation incentives

Technology and energy-saving

Special offshore regime activities

Islamic financial instruments

Algeria Marocco Tunisia 19

PwC TLS | Avvocati e Commercialisti1.4 Altri aspetti

Incentivi per gli investimenti - Algeria

Algeria Industrial Park

ANDI – National Agency of Investment Development

http://www.andi.dz/index.php/en/regimes-d-avantages

The investment projects may enjoy from tax exemptions

and reductions, depending on the project location and

impact on the economic and social development

Three levels of advantages are provided:

- Common advantages to all eligible investments (dazi,

IVA, 3/10 anni esenzione CIT…)

- Additional advantages to privileged / or job creating

activities (5 anni esenzione tasse e altro)

- Exceptional advantages to investments bringing a

particular interest for the national economy

Algeria Marocco Tunisia 20

PwC TLS | Avvocati e Commercialisti1.4 Altri aspetti

Incentivi per gli investimenti - Marocco

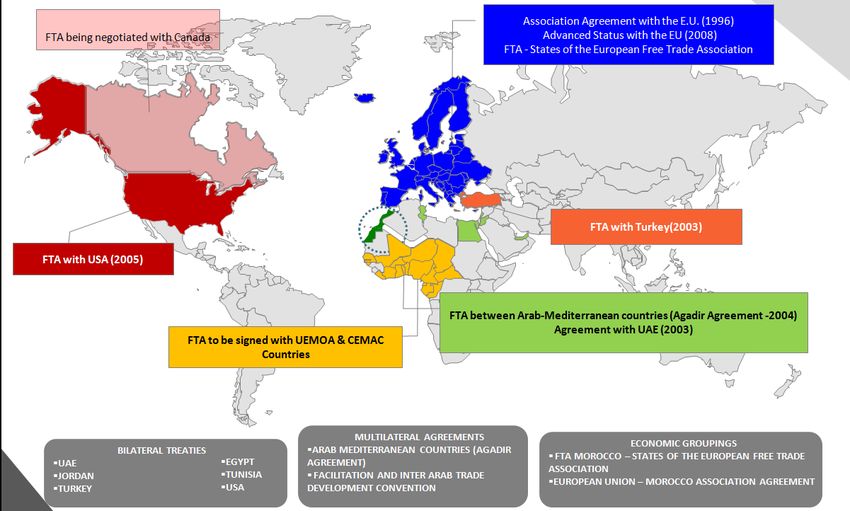

Marocco Free Trade Agreements (FTA)

Invest in Morocco

http://www.invest.gov.ma/?Id=1&lang=en

- Investment and industrial development fund

- Hassan II Fund

- Import Duty Exemption (Businesses that commit to making an

investment of an amount equal to or greater than one hundred (100) million dirhams

can benefit, as part of agreements to be concluded with the government, from

exemption from import duty and the value added tax applicable to goods, materials

and tools needed for their project and imported directly by the companies or on their

behalf. This exemption is also granted to the parts, spare parts and accessories

imported at the same time as capital goods, machinery and equipment for which

they are intended. The investment must be made within thirty-six (36) months from

the date of the signature of the abovementioned agreement.)

- VAT Exemption (Equipment goods, materials and tools needed to achieve

investment projects involving an amount higher than or equal to MAD 100 million are

exempt from VAT on imports within the framework of an agreement concluded with

the State, in favor for the beneficiaries during a period of thirty six (36) months from

the start of business).

Algeria Marocco Tunisia 21

PwC TLS | Avvocati e Commercialisti1.4 Altri aspetti Zone di Sviluppo Regionale (ZSR)

Incentivi per gli investimenti - Tunisia Primo gruppo

Secondo gruppo

Tunisia

Invest in Tunisia Zone di sviluppo Zone di sviluppo

regionale del regionale del

http://www.investintunisia.tn/It/accoglienza_46_33 secondo gruppo primo gruppo

Contributi, fino 10 % del costo

Nuova legge sull’investimento, entrata in vigore l’1 aprile 2017. del progetto

30% max 3 MTND 15 % max 1,5 MTND

Incentivi fiscali e finanziari: 100 % durante i primi 5

- Imposte ridotte al 10% per le società totalmente esportatrici; 100 % durante i primi 10

Esenzioni fiscali anni di attività e 10%

anni di attività e 10% dopo

- Esenzione IVA e dei diritti di dogana per i prodotti da dopo

riesportare; Sovvenzione per i contributi

- Vantaggi fino a 10 anni per le società sistemate nelle zone di previdenziali a carico 100 % per 10 anni 100 % per 5 anni

dell’azienda

sviluppo regionale;

- Contributi d’investimento specifici per le zone di sviluppo Contributo per le spese in

infrastrutture nel settore

regionale, fino al 30% del costo d’investimento, limitato a 3 dell’industria, fino al 10% del

85 % max 1 MTND 65 % max 1 MTND

MTND; costo del progetto

- premi d’investimento per i settori prioritari e le filiere

Contributo ai Fondi di

economiche; Promozione dell’Alloggio per i Esonero illimitato nel tempo Nessun vantaggio

- Incentivi per investimenti in asset intangibili e spese di ricerca e Salariati (FOPROLOS)

di sviluppo; Le imprese beneficiarie dei vantaggi di sviluppo

TFP (Tassa sulla Formazione

- Contributi per la formazione. Professionale)

regionale conformemente alla legislazione in vigore sono

esenti dalla TFP.

Algeria Marocco Tunisia 22

PwC TLS | Avvocati e Commercialisti1.4 Altri aspetti

Principali aspetti di fiscalità italiana da considerare

Le principali norme da considerare:

- Residenza fiscale (Esterovestizione. Vedere anche DTT – Art. 4. In particolare sede

direzione effettiva/place of effective management)

ITco

- Transfer Pricing (beni, servizi, flussi finanziari intercompany)

- CFC (tassazione in Italia delle controllate – Art 167 TUIR)

- Eventuali limitazioni all’applicabilità dei trattati contro le doppie imposizioni

DZco MAco TNco

Livello nominale di Regime fiscale Tassazione per A determinate

tassazione considerato trasparenza (i condizioni,

inferiore al 50 per privilegiato redditi conseguiti possibilità di

cento di quello dal soggetto estero disapplicare la

applicabile in Italia controllato sono norma CFC

imputati alla verificare

società italiana)

Algeria Marocco Tunisia 23

PwC TLS | Avvocati e Commercialisti2 Aspetti Societari Aspetti Societari Algeria Marocco Tunisia 24

2 Aspetti Societari Algeria (1/2) Forme societarie principali: Società per Azioni (SPA) / Società a Responsabilità Limitata (Sarl) [ Normativa simile alle società europee (in particolare a quella francese) Principali caratteristiche: Società per Azioni (SPA) - 7 azionisti (numero minimo) - capitale minimo: 1.000.000 dinari algerini (circa 7.000 euro) ovvero 5.000.000 dinari se la società fa appello al pubblico risparmio - i soci rispondono per i debiti della società solo fino a concorrenza del valore delle loro partecipazioni - organo amministrativo: consiglio di amministrazione o un direttorio assistito da un consiglio di controllo - nomina di un revisore dei conti obbligatoria Società a Reponsabilità Limitata (Sarl) - 2 soci numero minimo (50 numero massimo) - capitale minimo non previsto - cessione quote sociali a terzi solo con accordo dei soci rappresentanti i 3/4 del capitale sociale - nomina di un revisore dei conti obbligatoria Algeria Marocco Tunisia 25 PwC TLS | Avvocati e Commercialisti

2 Aspetti Societari

Algeria (2/2)

Elementi comuni:

[

- Socio straniero: partecipazione consentita ad un socio straniero in misura diversa in funzione del tipo di attività svolta dalla società.

- Regola generale: partecipazione massima socio straniero 49%

- Società algerina che esercita attività di commercio estero: partecipazione massima socio straniero 30%

Per investimenti esteri superiori a 2 miliardi di dinari (circa 15.000.000 euro) approvazione del National Board of Investement.

- Conferimenti: in denaro o in natura (beni immobili, beni mobile, diritti IP, etc) con perizia di soggetto terzo per determinazione valore

- Patti parasociali: riconosciuti a condizione che siano conformi alla normativa locale

Algeria Marocco Tunisia 26

PwC TLS | Avvocati e Commercialisti2 Aspetti Societari

Marocco (1/2)

Forme societarie principali:

[

Società per Azioni (Société Anonyme, SA) / Società a Responsabilità Limitata

Principali caratteristiche:

Società per Azioni (Société anonyme, SA)

- 5 azionisti numero minimo

- capitale minimo 300.000 dirham (circa 27.000 euro) ovvero 3.000.000 dirham se la società fa appello al pubblico risparmio

- i soci rispondono per i debiti della società solo fino a concorrenza del valore delle partecipazioni

- organo amministrativo: consiglio di amministrazione composto da 3 a 12 membri

- obbligatoria la nomina di un revisore dei conti

Società a Reponsabilità Limitata

- 1 socio numero minimo (50 numero massimo). In caso di socio unico, lo stesso non può costituire un’ altra Sarl a socio unico

- non è previsto un capitale sociale minimo

- cessione quote sociali a terzi solo con accordo dei soci rappresentanti i 3/4 del capitale sociale

Algeria Marocco Tunisia 27

PwC TLS | Avvocati e Commercialisti2 Aspetti Societari

Marocco (2/2)

Elementi comuni:

[

- Socio straniero: possibile possedere il 100% di una società marochina

- Legale rappresentante: anche straniero.

- Conferimenti: in denaro o in natura (beni immobili, beni mobili, diritti IP, etc.) con perizia di un esperio per la determinazione valore

- Patti parasociali: riconosciuti a condizione che siano conformi alla normativa locale

Algeria Marocco Tunisia 28

PwC TLS | Avvocati e Commercialisti2 Aspetti Societari

Tunisia (1/2)

Forme societarie principali:

[

Società per Azioni (Société anonyme, SA) / Società a Responsabilità Limitata

Normativa simile alle società europee (in particolare a quella francese)

Principali caratteristiche:

Società per Azioni (Société anonyme, SA)

- capitale minimo 5.000 dinari tunisini (circa 1.700 euro) ovvero 50.000 dinari se la società fa appello al pubblico risparmio

- i soci rispondono per i debiti della società solo fino a concorrenza del valore delle loro partecipazioni

- nomina di un revisore dei conti obbligatoria (iscritto all’albo ufficiale tunisino)

Società a Reponsabilità Limitata

- non è previsto un capitale sociale minimo (neanche in caso di socio unico)

- cessione quote sociali a terzi solo con accordo dei soci rappresentanti i 3/4 del capitale sociale

Algeria Marocco Tunisia 29

PwC TLS | Avvocati e Commercialisti2 Aspetti Societari

Tunisia (2/2)

Elementi comuni:

[

- Socio straniero: partecipazione consentita ad un socio straniero in misura diversa in funzione del tipo di attività svolta dalla società.

- Società tunisina che esercita attività commerciale in Tunisia: socio straniero partecipazione massima 49% oltre ad autorizzazione

speciale rilasciata dalla Tunisian Central Bank.

- Società tunisina settore industriale o servizi finanziari: socio straniero anche partecipazione di maggioranza o 100%

- Legale rappresentante: anche persona straniera

- Conferimenti: in denaro o in natura (beni immobili, beni mobile, diritti IP, etc) con perizia di un terzo per la determinazione valore

- Patti parasociali: riconosciuti a condizione che siano conformi alla normativa locale

Algeria Marocco Tunisia 30

PwC TLS | Avvocati e Commercialisti3 I nostri riferimenti I nostri riferimenti Algeria Marocco Tunisia 31

Section 3 – I nostri riferimenti

I professionisti

Photo

Giovanni Marano Davide Frau

Dottore Commercialista Avvocato

phone 0039 049 873421 phone 0039 049 873421

giovanni.marano@pwc.com davide.frau@pwc.com

Algeria Marocco Tunisia • Confindustria Vicenza - 27 febbraio 2018 32

PwC TLS | Avvocati e Commercialisti© 2017 TLS Associazione Professionale di Avvocati e Commercialisti. All rights reserved. PwC refers to the Italian member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see http://www.pwc.com/structure for further details.

You can also read