CAPITAL MARKETS DAY 2019 - Netcompany

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

NETCOMPANY CAPITAL MARKETS DAY 2019

Presenters

.

Status on strategy Netcompany’s business model Update on the Danish market

André Rogaczewski, CEO Claus Jørgensen, COO Gustaf Löfberg, Country Managing Partner, DK

Update on the UK market Behind the quarterly numbers

Kevin Barrett, Partner, UK Thomas Johansen, CFO

Page 2

Agenda of today

.

Time Page

1 Status on strategy 10:30 – 11:00 5

2 Netcompany´s business model 11:00 – 11:30 15

3 Update on the Danish market 12:30 – 13:15 32

4 Update on the UK market 13:15 – 13:45 47

5 Behind the quarterly numbers 15:00 – 15:30 58

Page 3

Agenda

.

Time Page

1 Status on strategy 10:30 – 11:00 5

2 Netcompany´s business model 11:00 – 11:30 15

3 Update on the Danish market 12:30 – 13:15 32

4 Update on the UK market 13:15 – 13:45 47

5 Behind the quarterly numbers 15:00 – 15:30 58

Page 4

Investment highlights

.

Satisfied and recurring

customer base

Unique scalable business Unique financial

model with proven ability profile and multiple growth

to deliver levers

19 years track record of Only IT services company in Europe

sustainable profitable growth and North America with +EUR 200m

Establish Netcompany revenue, +20% growth, +25% EBITA

based on continued focus to

always deliver as the Northern margin over the last +10 years,

European market strong free cashflow and pay-out

ratio of above 80%

leader in IT services

Founder driven Ability to attract

with strong vision the best IT talents

High growth markets driven by

technological shift to strategic

IT solutions

Core market CAGR 2016-2022 of 10-12%

Page 5

Track record of industry-leading growth and sustainable profitability

.

Revenue growth

Reported financials (DKKm)

CAGR: 21% CAGR: 23% CAGR: 39%

(‘06-’11) (‘11-’15) (‘15-’18)

Significant investments in

Strong growth and margin despite

technology, infrastructure and

economic downturn 2.053

public sector expansion

1.416

41% 629 758 900

32% 33% 400 36% 28% 37%

27% 32% 32% 461 26%

24% 27%

35% 205 222 261 18%

127 179 8% 327 28% 25%

25% 22% 24% 21% 17%

15% 18% 15%

'06A '07A '08A '09A '10A '11A '12A '13A '14A '15A '16A '17A '18A

Revenue (DK)1 NO UK Adjusted EBITA-margin Organic Growth

Challenger National champion Northern EU challenger

Page 6

Netcompany today – 10 offices with +2000 IT people in six countries

.

Vietnam

Ho Chi

Minh, VN

5 (Emp. 92)

Oslo, NO

4

(Emp. 184)

Aalborg, DK 3 Copenhagen, DK

Leeds, UK Aarhus, DK 3 1 (Emp. 1.235)

5

Derby, UK 5

2 Warsaw, PL

5 2 (Emp. 224)

London, UK Delft, NL

(Emp. 363) (Emp. 105)

Proven capability of scaling Netcompany from ~250 in 2010 to +2,000 employees globally in 2019

Note 1: Average number of employees in Q1 2019, including freelancers and contractors

Page 7

Netcompany’s core offering is to develop and deliver innovative and

differentiated IT solutions

.

Gartner’s pace layered approach reflects the shift in spending focus from Innovation

records to innovation and differentiation • Experimental solutions with continuous short iterations to

test new ideas

• At the forefront of each new technological wave

15-20%

Innovation ‘16-’22 CAGR 1

Differentiation

• Differentiating systems to give organisations competitive

Differentiation

8-12% strategic advantage with tailored solutions

‘16-’22 CAGR 1 • Added complexity and governance compared to innovative

solutions due to strategic importance, but still with need

for agility to keep in front

0-4% Records

Records ‘16-’22 CAGR 1 • Commodity (one size fits all)

• Processes such as accounting that do not provide a

competitive advantage and should be bought as

standardised, not tailored solutions

2016 2022

Note 1: Based on company market study, core market growth in Denmark

Source: Netcompany, Gartner, company market study Page 8

Netcompany directly impacts the life of Danish citizens across their lifecycle

.

- SELECTED EXAMPLES -

From the birth of over everyone’s first day in ensuring the financing

to people’s everyday life until the golden age

the digital citizen school of the Danish welfare society

Family benefits AULA Student Platform BORGER.DK Social Pension ICI

- ATP - - KOMBIT - - Agency for Digitisation - - ATP - - Ministry of Taxation -

Paying out DKK17bn yearly in child Giving teachers and parents the Single access point for all Paying out DKK120bn yearly in Collecting public debt to the

and youth benefits tools to develop government self services for all state pension to one million society including income taxes,

children's education Danish citizens Danish citizens fees and fines

Page 9

Our core market is large and fast growing with ample room to grow

.

Records Differentiation Innovation

~8-10% CAGR1 ~9-11% CAGR1 ~7-9% CAGR1 ~8-10% CAGR1

Core market (’16-’22E) Core market (’16-’22E) Core market (’16-’22E) Core market (’16-’22E)

’16 - ’22 ’16 - ’22 ’16 - ’22 ’16 - ’22

CAGR CAGR CAGR

~ DKK119bn CAGR

~ DKK21bn ~ DKK13bn ~ DKK63bn

14-20%

15-20% 15-20% ~ DKK77bn 15-20%

~ DKK12bn ~ DKK7bn ~ DKK36bn

7-11%

8-12% 8-12% 8-12%

0-4%

0-4% 1-5% 0-4%

'16A '22F '16A '22F '16A '22F '16A '22F

Market ~ 10% Market ~ 2% Market < 1% Market < 1%

share2 share2 share2 share3

Note 1: Core market: Public Sector: Central Government, KOMBIT and larger municipals; Private Sector: Medium and large companies with strategic focus on digitisation and complex

projects that require sophisticated IT capabilities; 2: Based on core market definition and Gartner approach, as of 2016

Page 10Strategy 2022: Establish Netcompany as an emerging Northern European

market leader

.

Set the standard for IT services

and establish Netcompany as the

Mission & ambition Northern European market leader in IT services

Gain market share Export business model Utilise synergies and cross selling

• Deliver on time, on budget and in agreed • Continue export of business model in • Exploit sector specific knowledge across

quality Vietnam, the Netherlands and the UK (fully borders

• Focus on complex projects requiring implemented in Norway) • Optimise staffing of projects independent of

sophisticated IT capabilities • Expand into other Northern European geographical presence by focusing on

• Grow faster than the market in all countries, e.g. Sweden and Finland outcome based projects

geographies • Explore greenfield possibilities in selected

markets

Strategic initiatives

Outstanding talent Differentiated management model Unique, agile, deliverable-driven

& career development model & integrated sales approach methodology & toolkit

Preserve the Netcompany culture

How we win

Continue advancing Continue to contribute to Continue attracting and retaining

Top imperatives the digitalisation agenda enhancement of the talent pool the best IT people

Page 11European expansion based on disciplined M&A strategy

.

Strategic market prioritisation

• Adequate digitalisation level with

high growth segments

• Public digitalisation strategy

• Private sector with strategic focus on

digitalisation

• Attractive competitor landscape

360 degree target screening and due

Sweden diligence

Finland • Strong IT competencies

• Cultural fit

Norway

• Innovative and strategic mindset

• Fundamentally sound business

performance

UK • Proven track record of winning

Denmark tender bids

• Founder driven

Netherlands • Motivated local leadership

Tactical flexibility

• Greenfield startup in selected

markets

• Bolt-on acquisitions in large, existing

Netcompany market Strategic priority market markets

Page 12

Source: NetcompanyQDelft – the perfect match

.

QDelft – a perfect key to the Dutch market with demonstrated ability to The Dutch market is highly attractive with key characteristics similar

win and deliver large public projects to the Danish market but significantly larger

• Delivering complex and business critical IT solutions

• IT people leading IT people with strong talent pool

• Strategic public project portfolio

• Sound business culture

• Founder driven

• Office on Technical University Delft campus facilitating easy access to

talent pool Market size approx. three

times the Danish market

Key facts

Amsterdam, NL

5

• DKK +50m revenue 1 Haag, NL

5

Delft, NL 5 Large public sector with

• +20% revenue growth2 focus on digitalisation

•

+/- +/- 0 EBITA in 2019 1

Strong IT talent pool

• Based in Delft

• 105 employees

Note 1: Expected performance in 2019, source: Netcompany

Note 2: Revenue growth from 2017 to 2018, reported numbers

Page 13Agenda

.

Time Page

1 Status on the strategy 10:30 – 11:00 5

2 Netcompany´s business model 11:00 – 11:30 15

3 Update on the Danish market 12:30 – 13:15 32

4 Update on the UK market 13:15 – 13:45 47

5 Behind the quarterly numbers 15:00 – 15:30 58

Page 14Netcompany operates its own institutionalised, repeatable and scalable

business model

.

Disruptive management model Outstanding talent &

& integrated sales approach career development model

SALES &

PEOPLE

DELIVERY Young workforce with

Combined sales & delivery

outstanding talent

Decentralised management

Delivering Merit-based career path

digital

transformation

Effective, lean pyramid

IT-people leading IT-people

structure

EXECUTION

Unique, agile, deliverable-driven methodology & toolkit

Scalable in-house Truly agile delivery model Execution on time and

developed methodology in budget

Page 15Sales & delivery

IT People leading IT people - the core of the Netcompany delivery model

.

1 2

Accurate pre-selection of Unrivalled understanding of

projects assures less resources requirements, ability to

being wasted in low communicate solutions and estimate

win rates resources needed

IT-people leading

IT-people

~67% FULL

Average win rate Accuracy in

over the last 5 years1 Project Setup

3

Delivery on time and on budget with the same team that sold the project (bid team)

100% GREEN

Delivery Track Record2

Note 1: Average of 2015-2018. Total value of contracts won as a percentage of total potential value of contracts tendered for in each year; 2: Each project delivered on budget, on time

(defined as including up to one month of delay) and within scope (defined as delivery of 12 more than 95% of expected project net present value)

Page 16Sales & delivery

Above 90% of senior management are IT professionals – leading IT people

.

11% 13%

24%

31%

100%

89% 87%

76%

69%

Consultants Senior consultants Managers Principals Partners

IT background 1 Other background

Note 1: As of Dec-2018: Employees with IT background or significant IT experience

Page 17Sales & delivery

Next-gen IT – from specialists to holistic profiles

.

Old school Next-gen IT skills

Holistic consultants with strong IT skills as well as

understanding of business and solutions

Developer Business Analyst

Project Manager: Same profile but more experienced and

proven ability to lead

Narrow focus specialists No IT skills

Code Deploy

Plan Operate

Project Manager Operation Build Monitor

Test Release

Through true DevOps

Administrator Infrastructure focus

Page 18Sales & delivery

IT people leading IT people unlocks unique accuracy and commitment in

resource estimation before signing of contract

.

Resource Estimation Delivery

Bottom - Up Approach Top - Down Approach Full accountability, as the same

manager is responsible for scoping,

resource estimation and delivery

Identify and estimate hourly budget Benchmark project team structures

of all components of the solution to actual realised similar projects

Verify component estimates & Consolidate teams into optimal

Fully integrated consolidate into resource estimate organisation and resource estimate Delivery on time

bottom-up & top- and on budget

down approach

Two-way verified solid and committed resource estimate

KEY Developers trained in Managers are IT people able to

DELIVERY DRIVEN FULL TARGET MARGIN ACHIEVED

PRICING ENABLER accurate estimation technically verify all estimates

Estimates only done by developers Bottom-up or only done by Managers Top-down will set projects of on unrealistic terms

Integrated approach requires special skills with both developers and managers

Page 19Sales & delivery

Sourcing model provides flexibility and scalability to support high growth

.

Access to huge, international resource pool of talented IT

…working together across the solution life-cycle

people…

Resource flexibility through global sourcing

A

centres

Project team setup with local and global delivery

B

Denmark 1

Vietnam 1 resources

1,235 employees 92 employees

86%

>5% freelancers No freelancers

UK 1 Poland 1 C All employees covering full life-cycle

363 employees 224 employees

4%

65% contractors No freelancers

Norway 1

Sourcing type

184 employees

10%

>5% freelancers 3 1 1) Sales

2 2) Project management

Netherlands2 3) Delivery

0% 105 employees

0% freelancers Revenue share (Q1 2019)

Note 1: Q1 2019 figures

Note 2: QDelft, Netherlands. Acquired 13 May 2019

Page 20People

Proven recruitment platform attracting the best IT talents

.

Netcompany is the employer of choice for talented IT

... supported by strong employer branding

graduates...

• Netcompany is the #7 choice in the minds of students and improving in • Number of events and related initiatives at or aimed at

ranking target universities in 2018

#1 among Danish

Student rankings, DK¹ companies

(Universum rank, 2015 – 2018

0 7

10 20 15 12

20 35 34 24 19 16 9 15 15

30

2015 2016 2017 2018

Huge available target pool in Denmark 2... ... complemented with global footprint

Total students

Clear strategy to address key talent Netcompany talent pool

available p.a.

Master, Diploma ~5,700

and Bachelor IT Total 2.900

Resource pool graduates

Experienced ~1,800

IT hires Total

1.300 50,000+

IT graduates annually in

Total Danish ~7,500 other core geographies

4.200

Resources Total

Note 1: Source; Universumglobal.com/rakings/denmark

Note 2: Netcompany, Universum Research

Page 21People

Effective recruitment conducted by delivery focused managers or partners

.

ATTRACT DEVELOP SUSTAIN

Stringent hiring criteria defined Fast time-to-hire process Superior offer win rates

30

Top performers in IT or science related degree Dedicated talent screening

1 resources (DK, UK, NO, PL,

HIGHEST TECHNICAL STANDARDS VN and NL)

~800

Assessment via case-based interviews conducted by Candidates interviewed in

IT people / project managers to assess fit into the 2018 in Denmark

2 model of integrated sales and delivery

75-80%

BUSINESS ACCUMEN COMBINED WITH IT SKILLS

48 HOURS Successful offers

From interview

to offer

Personal fit with Netcompany’s performance

culture

3 7 DAYS

From interview

AMBITION TO GROW

to contract signing

Page 22People

Onboarding process – new hires on project and fully productive from day 1

.

ATTRACT DEVELOP SUSTAIN

Pre start Month 2-6 Month 2-6 Month 2-6 Month 7-12

Introduction mail/Code of Assignment of Buddy and All new employees are

Info Conduct/other intro Mentor welcomed at NC Update

Participation in Code of Participation in the first

Academy Pluralsight for Non-IT-Profiles

Conduct relevant Academy Seminar

First project evaluation and Second project evaluation and

Development First mentor meeting

second mentor meeting third mentor meeting

Breakfast with CEO and COO.

Management Meeting with Project manager

Lunch with Area Director

Employer Participation in potential Opportunity to participate in

Branding Netcompany events Employer Branding events

Survey – Your first week in

Survey Survey – Recruitment process Survey – Code of Conduct Netcompany/Your first month

in Netcompany

Page 23People

Institutionalised career model accelerates development and attracts best IT

people

.

ATTRACT DEVELOP SUSTAIN

Netcompany’s career development program offers a

With specialisation after initial new-starter level

structured career path

Consulting Consulting Generalist Consulting Career

Architect Specialist

Description

tracks

Partner Consultants

Principal Master ▪ New hires start as generalists before specialisation into

Architect Specialists 1 & Test

either Specialist, Generalist, or Architect consultants

Specialists

Managing Principal

Architect ▪ Technical expertise in the management of technical

Manager A Architects

architecture and software development

B Senior Consultant ▪ Project management, sales, relations, management of

B Generalists

A C client expectation

Senior Architect Senior Specialist

1 C

▪ Development of domain expertise, acquire profound

Specialists

Consultant & Test Specialist practical knowledge and be a technical programmer

Others (not

Accelerated career path with large progression visibility ▪ Analysts, Interface or System consultants, etc.

illustrated)

attracting top performing IT talent

Page 24People

High performance culture instilled by continuous feedback from all

managers

.

ATTRACT DEVELOP SUSTAIN

Institutionalised and management driven performance review

Bi-annual performance scoring of employees

based on 5-step banding rank

Band Criteria

High

1 Top-performers

Performance vs.

HR

2+ Ahead of expected performance vs. peers

peers

Cycle

2 On-track performance towards promotion

2- Behind expected performance vs. peers

3s are put on performance watch for 9-12m

3 Consistent 3s result in termination

Low

100% of employees are provided with performance feedback Up-or-out culture enhanced within the organisation

Note 1: Employees in Denmark, Poland and Norway

Page 25People

High employee satisfaction to retain the best people

.

ATTRACT DEVELOP SUSTAIN

Young and highly satisfied

Employee NPS score outperforms

Attrition rate 1

the tech sector and Europe 2

32 workforce initiates a virtuous

AVG. AGE

cycle

36% 3

Young and highly satisfied employees are strong

promoters amongst top grads

19%

18%

17% 6%

Employees are continuously developed by

-1% experienced IT people, which accelerates

2016A 2017A 2018A progression and attracts top grads

-26% -26%

Top performers work within a superior delivery

model for complex projects that are highly

Technology Telco Europe Global appealing to the top IT grads

Note 1: Attrition rate adjusted for the close down of the Hanoi office in Vietnam

Note 2: Source; Management Consultancy IP 2014 (out sample of 15,015); Netcompany; Glassdoor; Statista; Company information

Page 26

Note 3: 2019 figure. Source; NetcompanyExecution

Agile delivery methodology based on scalable project cell structure

.

IT people leading IT people ...within an agile and collaborative team structure

One language across the organisation Deliver large complex projects in sub-projects with small teams developing in sprints

• Full accountability and technical ability of each developer

• Development in close collaboration with all stakeholders

• Resources take holistic view and are retained over the project

life-time minimising handovers and ensuring commitment

DELIVERY Interdisciplinary • Scaling of projects through additional teams or resources that hit

TEAM Teams the ground running with the same background and training

• Fully scalable across the organisations at constant quality as all

Project projects follow codified methodology that allows managers to

example deep-dive and focus on essence rather than style

CODIFIED

METHODOLOGY

DEVELOPMENT model combining Collaborative model with focus Best practice

agility and control on TRANSPARENCY TOOLKIT LIBRARY

Page 27Execution

Execution approach combining agility and control to deliver on time and

budget

.

DEVELOPMENT

Traditional Waterfall Netcompany Agile Development

Approach Approach Approach

Iterations

Define Foundation through Analysis

Analysis

Build in sprints

Design Breaking into releases

Test

Build in sprints & gather feedback Gather

feedback

Deploy

Test & Deploy to create speed to market

Long time to market Agile and collaborative Agile and collaborative

Limited agility Continues focus on target Lack of defined solutions

No accountability Controlled change process to fulfil customer needs Lack of end focus

Lack of budget and scope

Late collaboration with client Strong focus on quality and progress monitoring commitment focus

Preferred method over last decades – Recent years alternative approach – adopted

now generally considered old fashioned but

Netcompany combines agility and control, the by many with major issues around lack of

still in use at many peers best of two worlds focus and control

Page 28Execution

Focus on full internal and external transparency

.

TRANSPARENCY

Very accurate updated project reporting based on real-time Netcompany Client

Netcompany Project View

developed methodology used throughout the organisation Project View

RESOURCE ALLOCATION INTERFACE PROJECT STATUS

Consistent and Early review and

thorough reporting approval of

allows early deliverables

detection of ensures alignment

deviations and between

possibility to adjust Netcompany and

before problems AUTOMATED TESTING TRACKING the client

arise

Real-time data feed 24/7 unfiltered

of project status access to project

status

Page 29Execution

Uniform project documentation in toolkit provides predefined templates and

work packages shared between customers and developers

.

TOOLKIT LIBRARY

Deliverables Visualisation Prototypes

• Identical set of deliverables driving the Netcompany • Visualisation of the solution is key deliverable, providing easy

methodology across all projects access into projects and replacing more complicated design

• Clear structure of deliverables to be produced at each stage of a documentation

project with approved examples of best project executions • Prototypes start with early sketches of the screens of the system,

attached and are then implemented in clickable prototypes that act like

• Set of deliverables drive processes ensuring continuous client the end system

feedback and serve as end documentation of the process

Deliverables:

Documents describing different aspects of the system, including design,

programming guidelines, test scripts and operations manual

Page 30Agenda

.

Time Page

1 Status on strategy 10:30 – 11:00 5

2 Netcompany´s business model 11:00 – 11:30 15

3 Update on the Danish market 12:30 – 13:15 32

4 Update on the UK market 13:15 – 13:45 47

5 Behind the quarterly numbers 15:00 – 15:30 58

Page 31Denmark at a glance

.

Overview of key people and organisation Key financials 2018 2017

Gustaf Löfberg Country MP

Age: 48 NC since inception

Revenue 1,544m 1,220m

(DKK)

Adjusted

EBITA

461m 359m

17 ((DKK)¹

partners

Share of

Aalborg group

(Est. ‘10) revenue

1,235 Aarhus

FTEs2 (Est. ‘06) Copenhagen

(Est. ‘00) 75% 86%

Note 1: Adjusted EBITA adjusted for special items (non-IFRS)

Note 2: Average number of employees in Q1 2019

Page 32Denmark – a highly digitised and mature market

.

Key market characteristics 1

One of the most digitised countries

and developed IT markets

Public focus on modern IT and

modernisation of municipalities

Fragmented private market with

medium/large companies focusing

on digitalisation Netcompany is well positioned to continue delivering

innovative complex solutions from a position

with superior NPS and in a market

with plenty of room to grow

Incumbents with low NPS 2

Note 1: Source: Leading consulting firm, Netcompany, I-DESI (International Digital Economy and Society Index) 2015 Main Ranking

Note 2: Net Promoter Score

Page 33Public core market size and outlook

.

Netcompany public core market Growth drivers

Digitalisation will form the basis for the efficient

welfare state

Public shift towards modernisation and replacement

Public IT service of legacy systems

market 2016

DKK ~ 11bn Focus will be innovation combined with robust

delivery as current solutions needs to be safely

replaced by modern and efficient solutions

✓ IT service market where Netcompany

offers solutions IT public core market spend (DKKbn)

Addressable × Excludes dedicated IT

market 2016 hardware/software; infrastructure CAGR 16-22

DKK ~ 7bn ~8

8-10%

✓ Central government, centralised joint

Core ~5

projects for all municipalities, select

CAGR market larger municipalities

‘16-’22 2016

✓ Regions targeting selected projects

8-10% DKK

~5bn × Small individual municipalities withNetcompany has high historical win rates on public tenders

and is taking market share from incumbents

.

Track record of ~67% win rate in recent years… … with several high-profile tenders won since 2015

Total

Totalvalue

valueof

ofparticipated

participatedDK

DKpublic

publictenders

tenders(in(inDKKbn,

DKKbn,potential contract

potential value)

contract value) Relative size for illustrative purposes

44% 72% 87% 53% Other

Rammeaftale (SKAT)

~67% average win rate driven by differentiated sales & delivery model with integrated sales

DUBU (KOMBIT)

and delivery teams

FLIS (KOMBIT)

3.5 Nyt SIS (Ministry of Education)

0.5 Rammeaftale ATIS (Working Environment Authority)

KY (KOMBIT)

2.1 1.8

1.9

0.6 0.9 Social Pension (ATP)

1.1 3.0

1.5 1.0 Rammeaftale ICI

0.8 (Tax Ministry)

2015A 2016A 2017A 2018A AULA – samarbejdsplatformen

(KOMBIT)

Netcompany won Lost/not pre-qualified Netcompany win rate as % of est. total1 By project

Note 1: Total value of contracts won as a percentage of tendered value for each year

Page 35Public market provides high degree of transparency

.

Tender visibility

Total value of known public tenders (typically multi-year contract value) Market (avg. tender contract)

Renewal of

more than +200 core • Most large public tender contracts have an average

systems at the Danish duration of ~7 years

Danish tax

tax authorities

authorities

+10 DKKbn1 • Development phase typically first 12-18 months followed

by 48-72 months of maintenance & operations

• Re-tenders of maintenance & operations contracts will

Customs

authorities ~2 DKKbn 2 typically have higher win rates to original contract holder

due to existing knowledge, unless customer satisfaction is

low which is often the case with incumbents

From already

known new and

re-tenders 10 DKKbn 2

+10-15 years

‘19-’22

Note 1: Source; Danish tax authorities

Note 2: Source; Netcompany

Page 36Incumbents being challenged by agile players in public sector

.

Adapting incumbents and

Incumbents Pure play next-gen IT disruptor

agile at-scale players

Example

companies

• International players with • Regional, agile players with • Citizen focused complex projects,

established relationship through scale/scope that drive modernisation of and

Description

legacy systems to compete with incumbents on increased efficiency in the public

and scale large-scale projects sector

Avg. market

share per

player ~15 – 40% ~3 – 10% ~10%

Source: Company market analysis, market analysis made by leading consulting firm in 2016

Page 37Public market focus

.

Continue focus on core customers and agencies

• Continue to disrupt the public IT market

• Go for the largest complex projects (Central Government, largest municipalities, KOMBIT, ATP )

Serve already won tenders

• Execute on tenders won over the last years

• Positioning for winning of future re-tenders

Acquire new tender contracts

• Target the carefully selected “right” tenders

• Leverage track record and positive customer momentum

Page 38Private core market size and outlook

.

Netcompany private core market Growth drivers

Differentiation and innovation categories driven

by customer innovation and competitive pressure

Private IT service

market 2016

Robust agile delivery is vital to customers as time-

DKK ~ 27bn

to-market is crucial

✓ IT service market where Netcompany

offers solutions IT private core market spend (DKKbn)

Addressable × Excludes IT hardware and support

market 2016 functions CAGR 16-22

DKK ~ 16bn ~13

16-22%

✓ Medium and large companies with

Core significant annual IT budget ~7

CAGR market ✓ Strategic focus on differentiation

‘16-’22 2016 ✓ “Non-vanilla” projects

10-12% DKK

~7bn × Excludes 70% of “records” segment

× ExcludesThe competitive landscape in the Danish private market

is highly fragmented

.

Incumbents Adapting incumbents Pure play next-gen IT disruptor

Example

players

• Typically been in the market 20+ • Legacy from incumbents but focused • Driving change in the IT industry by

years on closing gap between ‘running’ delivering strategic IT solutions that

Description • Focus on large, more simple projects and ‘growing’ make customers future digital

• High share of revenue from • Mostly active in more simple winners

maintenance and operations solutions given legacy

Avg. market

share per

player

~5-10% ~2-5% ~10%

Source: Company market analysis, market analysis made by leading consulting firm in 2016

Page 40Private market focus

.

Develop core customers and capture market growth

• Grow large customers with ambitious digital budget

• Benefit from tailwind following increased private spend on innovation/differentiation

Win large accounts and increase scope of work

• Gain foothold and build scale with few large customer accounts per year

• Increase scope of work with current accounts

Take end-to-end ownership with large cap companies

• Win “full scope” contracts with large cap companies (full ownership of digital journey)

Page 41Delivery model inherently support synergies and cross-selling

.

Netcompany’s Delivery model provides maximum flexibility and synergies independent of segment and sector

PUBLIC PRIVATE

• Tenders for new projects is strictly regulated by EU • Demonstration of knowledge and insight

• Every aspect of tender has to be formally documented • Long-term dialogue

Sales

• Dedicated team of 30 employees assigned to studying the dynamics of • Most sales activities are initiated in close cooperation with existing

Process

the segment and the requirements of tender responses customers through referrals

• Significant scope for selling/cross-selling

• Development of typically 12 to 18 months followed by 48 to 72 months • On average, large private sector engagements have a duration of

Services

of maintenance and operations approximately 12 – 18 months, and are of high strategic value to customers

Project • Multi-year contracts of 6 – 7 years • Shorter contracts of 12 – 18 months

Length • Increasingly multi-year contracts

• High degree of visibility on upcoming tenders • Continued focus on complex projects with customers having ambitious

Outlook • Converge to more maintenance contracts digital budgets

• Focus on larger projects that tend to have a higher strategic value

• Proven ability to deliver large, complex and transformational projects

• Private segment increasingly looking towards Public segment for references of transformations at scale

Why We • Platform agnostic approach with long track record of delivery and ability to envision innovative solutions that creates

Win trustworthiness

• Integrated Sales and Delivery organisation provides required technical knowledge and insight in sales and marketing efforts

• Strong public profile and ownership structure provides credibility

Page 42

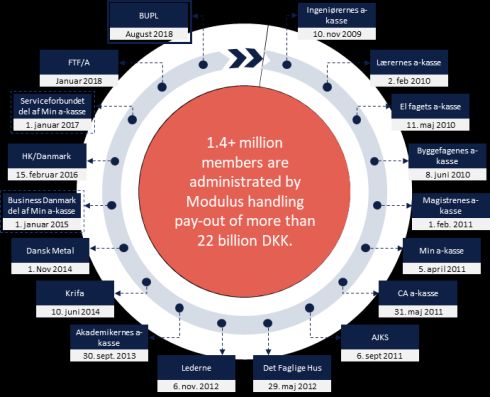

Source: NetcompanyCASE: Trade unions (1/3)

.

Ingeniørernes a-

Netcompany trade unions projects BUPL

kasse

August 2018 10. nov 2009

Common core with streamlined processes for payments FTF/A Lærernes a-kasse

and case handling Januar 2018 2. feb 2010

Serviceforbundet

Agile front-end systems with the customer in center – del af Min a-kasse

El fagets a-kasse

1. januar 2017 11. maj 2010

based on a standard CRM platform

1.4+ million Byggefagenes a-

HK/Danmark

Innovative solutions e.g. utilising AI to customize offers members are kasse

15. februar 2016 8. juni 2010

to customers, giving significant business benefits administrated by

Business Danmark

del af Min a-kasse

Modulus handling Magistrenes a-

kasse

Effective handling of compliance and legislative changes 1. januar 2015 pay-out of more than 1. feb. 2011

Dansk Metal

DKK 22bn. Min a-kasse

1. Nov 2014 5. april 2011

Parallel roll-out to several trade unions

Krifa CA a-kasse

10. juni 2014 31. maj 2011

Replaces stiff legacy systems with focus on keeping

Akademikernes a-

records, not differentiation and innovation kasse

AJKS

30. sept. 2013 6. sept 2011

Development organisation of approximately 90 Lederne Det Faglige Hus

6. nov. 2012 29. maj 2012

employees

Page 43CASE: Trade unions (2/3)

.

The new IT The experiences from

infrastructure for the the trade unions

Danish trade unions customers have also

has subsequently been been used for similar Finance

used as an entrance to solutions in e.g. banks,

large payment systems where a customer-

for the large municipal focused differentiating

service systems and and innovative

thereby creates a solution is built as a

bridge between layer around the

Private and Public product’s centric old

projects banking systems

Page 44CASE: Trade unions (3/3)

.

Examples of recent new projects

Payments User recommendations through AI Apps

GDPR safe communications

Booking

Page 45Agenda

.

Time Page

1 Status on strategy 10:30 – 11:00 5

2 Netcompany´s business model 11:00 – 11:30 15

3 Update on the Danish market 12:30 – 13:15 32

4 Update on the UK market 13:15 – 13:45 47

5 Behind the quarterly numbers 15:00 – 15:30 58

Page 46UK at a glance

.

Overview of key people and organisation Key financials 2018

Mark Ward Country Managing Partner

Age: 45 Founder: (Hunter Macdonald)

Revenue (DKK) Adj. EBITA (DKK)2

338m 29m

7

partners

363 Leeds

FTEs¹

Derby

London London Leeds Derby

Note 1: Average number of employees including independent contractors in Q1 2019

Note 2: EBITA adjusted for special items (non-IFRS) and Group HQ costs

Page 47UK – a huge market with significant potential

.

Market characteristics Huge core market with expected CAGR ‘16-22 ‘of ~10%

Largest market in EU – lower digital maturity than Nordics

but steps taken to increase rate of digitalisation

Total IT Services

Market

DKK 330bn per annum ✓ Central government, large

municipalities,

large/medium sized

Large Government Departments with significant IT Budgets,

companies

completing transformation activities similar to those in the

Addressable

Nordics

market

✓ Large, complex projects,

DKK 171bn per

annum requiring dedicated teams

over longer time period

Core

Services, finance, production, technology, media and Market

telecoms companies with major budgets are the largest DKK

segments within fragmented private market 77bn per

annum

Source: Market analysis made by leading consulting firm in 2016

Page 48Despite small size, Netcompany UK has a strong

customer portfolio

.

10 private customers Public

Services/

Telecoms/

Retail

Energy

4 private customers

Production

Technology/

Media

2 private customers

Logistics

5 private customers

3 private customers

Netcompany UK has a prestigious list of customers and in May 2019 invoiced 36 companies or Government departments, 19

of which have greater than DKK +8 billion revenue or yearly Government funding

Page 49Supporting the citizens of the UK

.

Netcompany UK is starting to influence IT delivery and UK citizens across the UK both the public and private sector

Public Private

We are working with We are working with We are assisting We are working with We are working as We are supporting

Home Office to Highways England to Government major organisations part of a programme many major

protect the UK keep the UK departments with to support UK to install smart organisations to

borders roadways safe Brexit preparation manufacturing meters into every embrace new

UK home technology and to

innovate

Page 50UK public market trends fit perfectly to Netcompany focus

.

Government Transformation Strategy

UK is not yet as advanced in digitalisation as some other countries, including Denmark. UK Government strategy has ambitious

plans and has earmarked significant funds to digitalise and optimise the relationship between citizens and the state

Increasing focus on differentiation and innovation

UK Government is increasingly buying in layers and expanding their focus on procuring more differentiation and innovation based

services

Brexit will create opportunities

It is expected, that a significant number of UK IT systems will need to be implemented and updated to support Brexit

Challenges to deliver public projects

Some of UK government’s major projects have challenges, which makes an ability to consistently deliver a key differentiator

Page 51Public market spend entails huge untapped opportunities

.

Estimated annual DKK 150bn total ICT spend in Government sectors

- If only 20% of total spend is Netcompany core market, it still amounts to DKK 30bn

DKK billion

Kr 50.0

Kr 40.0

Kr 30.0

Kr 20.0

Kr 10.0

0.3% 0% 0% 0% 0.1% 0.2% 0.3%

Kr 0

Central Local Education Health National Security Criminal Justice Transport

(DKK) Total ICT annual spend Netcompany’s share of annual spend

• Netcompany is less than 0.5% of spend in the government sector with our largest involvements

• Public market penetration in initial phase, penetrating multiple sectors

Page 52Private market opportunities

.

Global organisations

Many major UK private sector companies are global organisations with major budgets with decision makers based in the UK

Legacy systems

Many UK private sector organisations are long established and have major legacy systems that need modernisation

Resistance to traditional players

There is a resistance to traditional players based on previous delivery issues, buyers want viable alternatives who can deliver

Integration

There is strong demand for integrators who can control an organisations vendors and secure delivery

Agility

The need is for organisations that can be agile in ethos and delivery approach, which promotes a move away from the large

traditional player

Page 53Private market – ample room to grow

.

Estimated annual, global ICT spend for 7 key customers totaling DKK ~35bn, shows significant potential

DKK billion

Kr 10.0

Kr 7.5

Kr 5.0

Kr 2.5

0.6% 1.7% 0.8% 0.2% 1.9% 0.1% 0.6%

Kr 0.0

Production #1 Services #1 Production #2 Production #3 Services #2 Retail #1 Logistics #1

Total ICT annual spend by customer, anonymized Netcompany share of annual spend

Page 54Integration of Netcompany business model on track

.

Sales & delivery

✓ Integrated sales and delivery model implemented

✓ Bidding and winning of large tenders

People

✓ Recruitment, onboarding and feedback processes in place for permanent work force

✓ Reduction of use of contractors ongoing

✓ Office setup optimised

Execution

✓ Netcompany finance and staffing tools fully implemented

✓ Netcompany Academy operating for the UK to create consistent delivery performance

The integration of Netcompany UK is progressing as planned - still 3 ½ years to go in the integration plan

Page 55Key steps to full integration and financial performance on

par with group level

20-25% organic

revenue

.

growth and 20-

25% adjusted

EBITA-margin

Revenue

growth of 15-

20% and

8-10% Strategic switch to Strengthen Principal Sell the correct Closer working across Strengthen

Exploit sector specific

adjusted permanent work force and Manager level outcome-based countries between relationships in

knowledge across

EBITA-margin aligned to to support the contracts that drive management, team existing customers to

borders to share

Netcompany ethos pyramid structure experience, long term transfers to optimise grow existing

and further strengthen and support strengthen bids and profitability and staffing model, shared accounts, ample room

the career model incoming talents customer growth commercial support to grow

propositions

Acquisition, 25 October 2017 December 2022

Page 56Agenda

.

Time Page

1 Status on strategy 10:30 – 11:00 5

2 Netcompany´s business model 11:00 – 11:30 15

3 Update on the Danish market 12:30 – 13:15 32

4 Update on the UK market 13:15 – 13:45 47

5 Behind the quarterly numbers 15:00 – 15:30 58

Page 57Financial highlights

.

Revenue growth

Reported financials (DKKm) Revenue (DK) Revenue (NO) Revenue (UK)

1 1 1

Adj. EBITA-margin (DK) Adj. EBITA-margin (NO) Adj. EBITA-margin (UK)

500 45%

37% 36%

400 30% 29% 29% 31% 35%

27% 29% 29%

300 26% 25%

26% 26% 19%

22% 17% 14%

22% 20%

200 17% 9% 15%

10% 5%

100 9% 3% 5%

0 -5%

0%

Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019

Acquisition

25 October 2017

Note 1: Adjusted EBITA-margin before special items (non-IFRS)

Page 58Financial highlights

.

Quarterly trends DK

Q1 Q2 Q3 Q4

• Adjustment of • Largest intake of • Full effect of new

seniority level new employees recruits from Q3

→ higher rates • Quarter with most

working days

• Salary increase • Public holidays • Danish summer • ’17: High level of

• Easter ‘18 • Easter ‘ 17- ‘ 19 vacation (typically costs to new ERP

July) and additional

FTE´s (CFO, legal

and finance)

Page 59Financial highlights

.

Quarterly trends NO & UK

Both entities new to Netcompany, so difficult to see solid trendlines for now

Margin will typically decrease in Q3 in NO due to new recruits – impact will be reduced as

entity grows

In the UK we will be seeing gradually increasing margins through the year

Page 60Working capital development

.

Revenue growth

Reported financials (DKKm) Revenue Total Change in working capital

700

500

300

100

-100

Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019

Page 61Working capital

.

Quarterly trends - Working capital Group

Generally negative working capital in Q1, Q2 and Q3

On account taxes paid in Q1 and Q4 – normally

Q2 and Q3 have had the highest negative impact on working capital

Driven by a large proportion sales in public, which have more back-end loaded payment plans

for fixed fee projects

Page 62Revenue criteria – “POC” accounting for fixed fee projects

.

Business

Netcompany project Netcompany meets milestone Netcompany invoice

activity

WIP &

WIP TR

revenue

Accounting

implications Resources (people and hours) Trade receivables increased An invoice is created and sent to

allocated to project reflecting the milestone the customer

Revenue and balance sheet

Balance sheet “WIP” reduced Trade receivables reflect

“WIP” increased reflecting the

reflecting the milestone remaining unpaid invoices

allocated hours

Page 63Work in progress and revenue – NET reduction in WIP in 2019

.

WIP DKKm Revenue DKKm

255.1 Reduced ~2,5002

145% 22.5%

5-10% NET1

2,053.2

45%

1,416.1

102.9

2017 2018 2019 2017 2018 2019

Note 1: Based on payment plans for current fixed fee projects

Note 2: Assuming ~22.5% revenue growth

Page 64Work in progress and revenue

.

Build up of WIP-balance as Netcompany has more large public fixed fee projects

Reported financials (DKKm) Revenue WIP Percentage of revenue

3000

~2,500 1

2500

2,053.2

2000

1,416.1

1500

1000 899.6

758.1

500 255.1 ~235

53.7 83 102.9

7% 9% 7% 12% ~9%

0

2015 2016 2017 2018 2019

Note 1: Assuming ~22.5% revenue growth

Page 65Provision

.

Provision development DKKm

Provision Percentage of revenue As we continue to deliver large complex projects

the need for general provision decline

36.1

30.3

26.41 Provision relative to revenue declines, as risk

profile decreases

Covers general uncertainty in the portfolio

2.1% 1.8% 1.1%

All projects are individually addressed for “POC”

2017 2018 2019 performance on a quarterly basis

Note 1: As per Q1 2019 – annualised

Page 66You can also read