Anthony Marchese of Texas Rare Earth presents at the Technology Metals Summit - InvestorIntel

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Anthony Marchese of Texas

Rare Earth presents at the

Technology Metals Summit

Watch Anthony Marchese, Chairman of Texas Rare Earth Resources

Corp. (OTCQX: TRER) present being one of the lowest cost

technology metal projects in the world during the

InvestorIntel Technology Metals Summit on October 14, 2015 in

Toronto. Explaining how the Texas Rare Earth Resources’ model

is profitable “even today”, using internal Chinese prices, he

explains how the project risk is mitigated by non-REE by-

product opportunities. Probably of greatest interest to our

audience, Anthony describes how the DLA contract both

validates the project and provides potential major offtake

potential.

Anthony Marchese: First

of all, thank you Tracy

for putting on the

conference and allowing

me to step in at the

last second and

describe Texas Rare

Earth Resources. I’m

going to go through

this very quickly. It’s

a much longer

presentation than 10

minutes, but in any case the story of Texas Rare Earth

Resources is quite simple. We are a massive low-grade deposit,

highly economic, multi polymetallic rather, about 80 miles

southeast of El Paso, Texas. We are near a major metropolitan

area. Easy extraction, I think, even at today’s China

economics. We’re still a very profitable, potentially

profitable enterprise. We have 41 million shares outstanding, market cap ridiculously low at $9.1 million. We have a lot of skin in the game, insider ownership about 38%. Institutional ownership about 12% and a fair amount of float so there are plenty of shares to trade. Our PEA from several years ago, that will come down as a result of our association with K- Technologies and I’ll let them talk about what they do. They’ll be presenting I guess later on. Originally we thought about $290 million, incredible economics; IRR of 67%. That was based at the time on China internal prices. Substituting China internal prices today, that number probably is in the mid- teens. It shows you how much it’s dropped, but still if you’re showing positive economics, I believe, in today’s environment then you have a reasonable chance of doing fairly well if you get into production. Enormous — That was based on a 20-year mine life. Realistically we have about 105-year mine life and that’s only the first of three mountains in the area, I’ll talk about that a little bit more, primarily heavy rare earths about 72%, in addition to a number of byproducts, which I’ll describe in a moment. Board of directors, Amanda probably knows Eric Noyrez, former CEO of Lynas, is on our board. Jack Lifton who is one of the featured moderators joined our board a couple of years ago. I don’t think there’s a day that goes by that I don’t speak to or email Jack several times a day. We have a working board. We are very active in managing the company. We have a lot of experience. Our project, again, 80 miles southeast of El Paso, Texas. I’ll describe. This is the deposit. This is the mountain. There’s no overburden. You come in, dig it out, we’ll be heap leaching it. And I’ll just talk about our contract with the Department of Defense in a moment, but we can sell our output 100 times over just to the defense industry. This is a very interesting study that no one ever mentions…to access the full presentation, click here

Argentina Unshackled Observers from outside Argentina have gone on a frenzied romp of self-congratulation hailing the change in the Argentine Presidency in last week’s elections as something akin to a Revolution. Once again though we find that simplistic formulas are being used and the nuances of what has happened being ignored. The situation still has the potential to be a wild ride for investors.

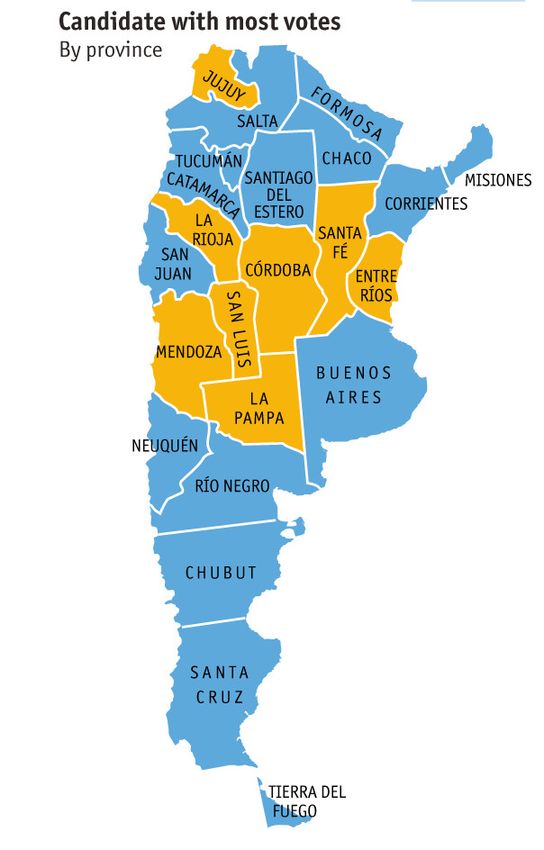

For a start the victory of Mauricio Macri is being hailed as a “right-wing” victory. To put that in context, firstly he leads a Rainbow Coalition that stretches from the Left across to the Right and the party he beat, the Frente Para la Victoria, is in fact the old Peronist Party, which was a fascist/corporatist construct in its original roots. So to claim that a wealthy businessman (in fact I would venture one of the five wealthiest in the country) that leads a Coalition including the Left is a “Right-wing” victory is stretching it a bit. Secondly we would note that the victory was surprisingly narrow. While the first votes in showed a 9% lead for Macri, as the night wore on the margin slipped and it ended up being 51.4% for Macri and 48.6% for his Kirchnerite opponent, Daniel Scioli. It should also be noted that the first round of elections last month delivered stinging losses to the Kirchnerites but they just barely hung onto control of the Senate meaning that, if they stay cohesive, they still have potential to block reforms. That said, with their patroness gone, the rats tend to disperse into the woodwork to regroup. We may end up seeing the phenomenon apparent under the De La Rua government in the late 1990s of Bribes for Votes when a hostile majority in the Senate had to be paid off, literally. The New Lay of the Land As we have repeated endlessly mining is controlled in Argentina by the provinces, in much the same way as it is in Canada or Australia. The national government in Argentina has NO approval or denial power over mining projects. So everything you have heard of “Cristina Kirchner blocked our project” is a load of codswallop. In all cases blockages occurred because of ornery provincial governments. It is interesting therefore to look at the map of the electoral results. The blue areas are provinces that voted for the Kirchnerite candidate. The yellow are those that voted for

the winning Macri-led ticket. Oops, for those who know the only province with mining of note (Silver Standrad’s Pirquitas mine) that voted for Macri was Jujuy. La Rioja has been an on- again, off-again mining favorable area and La Pampa and Mendoza have been graveyards for miners.

The provinces where mining is currently active are Catamarca,

Santa Cruz (the Kirchnerite province par excellence now run by the outgoing president’s daughter), Salta and San Juan. If there is anything to be read from this map it is that the marginalized distant provinces with the smallest populations (excepting Buenos Aires which was only won marginally by Scioli and that was because of the sprawling urban slums voting for him) supported the Kirchnerite program which gave them a greater share of the goodies. The provinces that trended for Macri where those with the largest populations (and strong agricultural export economies) that were actively persecuted and discriminated against for the last 12 years. Implications for Mining Having said that mine approvals are in provincial hands, some matters are still in the Federal purview. Amongst these that have relevance are foreign exchange allocations. Miners have been griping for years now that they could not bring in the capex items they wanted in an unrestricted way due to import restrictions and could not remit profits or dividends as and when they wished. These restrictions were part of the increasingly draconian and bizarre forex rules that the Kirchnerite regime was imposing as Argentines tried to head for the exits and buy dollars to protect themselves against the rapidly deflating peso. Moreover to say the forex regime was complex was an understatement. Here is the table of exchange rates for today for a leading Buenos Aires newspaper, La Nacion: So on the left we have the official rate, on the far right is

the so-called Dolar Blue which is the back-alley rate. In the

middle are various official rates administered by the Central

Bank for different purposes. Dolar Ahorro is a savings rate,

Dolar Tarjeta/Turista is the rate that locals can use credit

cards for (when travelling abroad) and that bona fide tourists

within the country can use to change money. The Dolar Soja is

the very prohibitive rate forced upon farmers selling their

crops (effectively a 30% tax on the official rate and a 150%

tax on the unofficial rate). Finally the Dolar Bolsa is a

conversion rate for transactions in the Stock Exchange.

Byzantine is obviously not too strong a word to describe this

bizarre system. Miners will be hoping that this system loosens

up, though the new government will be wary of letting this go

too soon or there will be a dollar buying spree that will

decimate Central Bank reserves. One suspects that Dolar

Turista and Dolar Soja will be the first to go. The government

will then aim to draw the Dolar Blue and the official rate

together somewhere in the middle. Who knows? Maybe the

wonderful Convertibility regime of the 1990s might be

revived.. Certainly Argentina had never experienced such good

times since the 1920s as under that arrangement.

Despite the mining provinces largely being of the Kirchnerite

ilk, they are the provinces that have shown themselves to be

most pro-mining. With less subsidies coming from the Federal

government more of the provinces will have to look to mining

to keep their local economies buoyant.

If one wants to muse with some names in Argentine mining those

to consider are:

Patagonia Gold Plc (AIM: PGD)

Hochschild Mining (LON: HOC)

McEwen Mining Inc. (NYSE: MUX | TSX: MUX)

U3O8 Corp. (TSX: UWE | OTCQX: UWEFF)

Pan American Silver Corp. (NASDAQ: PAAS | TSX: PAA)

Silver Standard Resources Inc. (TSE: SSO)Yamana Gold Inc. (TSX: YRI | NYSE: AUY)

Argentex Mining Corporation (TSXV: ATX | OTCQB: AGXMF)

Orocobre Limited (ASX: ORE | TSX: ORL)

Western Lithium USA Corporation (TSX: WLC | OTCQX:

WLCDF)

Galaxy Resources Limited (ASX: GXY)

One might also see those who have downplayed their Argentine

prospects dusting them off or racing back to restake them.

What Next

After exchange rates there are a vast swathes of regulations

constraining all aspects of economic life that could be cast

into the dustbin of history. Some of these measures being

rescinded should help miners. One that might not though is the

bizarre fuel subsidies. These were introduced after the

collapse of 2000/1 and the spike in inflation. To “protect the

poor” massive subsidies were introduced which have bled the

Treasury dry. They have been reduced and some have been made

to pay world parity prices for oil but many have not. This

could be the big budget winner but also a tough policy to bite

on first.

One could see a strong inflow of FDI though and this might

actually reverse the exchange rate so delays in freeing

remittances might actually work out better for miners when

they are eventually freed.

The whole construct of Kirchnerism was so bizarre and

distortive that untangling it is akin to unraveling the

Gordian Knot. Like Alexander the Great, sometimes it’s better

to just draw one’s sword and chop the knot in one fell swoop

than spend years testing one’s Boy Scout skills trying to

untie it..

Conclusion

After 12 years of Kirchnerite “policies” (more like populistbootstrapping) the Argentine economy is emerging from a long

dark tunnel into the glare of daylight. Frankly it’s better

out of the tunnel rather than being in it and foreign miners

for better or worse face a brave new world. We can say with

confidence that the rules will NOT be more onerous and the

forex regime WILL be more flexible. Growth should kick up and

frankly Argentina looks like a better bet than the deeply

troubled Brazil these days.

As a New Yorker would say “What’s not to like?”

Technology Metals: Can they

boost the wider economy?

There is talk in the

British newspapers about

the manufacturing sector

growing again, albeit

slowly. But then you read

that two steel plants, one

employing more than 2,000

people, are closing (due

to the collapse of the

steel price, thanks partly

to China exporting its

growing steel surplus).

For Western economies,

from Europe to North America, some more dramatic solution is

required.

Meanwhile, the latest issue of the magazine New Statesman has

a special section on industry (one headline reading“Manufacturing Matters”, as if anyone said it did not). Then London’s Sunday Telegraph devotes a full page to how Elon Musk and Tesla are taking on the Japanese car manufacturers – who are betting big on hydrogen as the fuel of the future – but with Musk sticking by batteries as his power source. And then there is the growing trend of acceptance that batteries, particularly lithium-ion ones, are the key to the future of renewable energy, the importance of storage being shown by news from Britain today that the country’s wind farms have a total capacity of 13,000 megawatts but the lack of wind recently has seen them generating only about 400MW. (Incidentally, I am writing this from Paris, after having travelled from Tokyo aboard a Boeing 787 Dreamliner, itself employing lithium-ion batteries in its power system.) When it comes to technology metals, we might (or should) be talking about the downstream, too. In fact, these metals may be a story far bigger than finding them, mining them, refining them: they could hold the key to a kick-start for Western economies, which badly need to reverse the export of their industries to low cost jurisdictions. We have seen an example of what possibilities might be with the Australian graphite company Talga, which started out by planning to process its Swedish graphite into graphene in Germany and has, more recently, joined the €1 billion European Union Graphene Flagship program. When we look back at the rare earth industry at the height of its market appeal (in 2011) one recalls that there was much talk of the downstream end of the business. Companies were quick to boast if they had plans for a manufacturing arm as well as a mining one; others argued this was a mistake, that finding and mining rare earths involved skills a million miles from those required for the processing of those same rare earth metals into finished items. Today, we see emerging REE producers sticking to their knitting, and letting someone else

do the value-adding. In graphite (as well as other technology metals) we see a similar trend. Oh, but that’s the market, people will argue. Japan and China have the established manufacturing infrastructure. This is not a view proposed in the New Statesman (a left- leaning but venerable magazine) by Vince Cable, who was Britain’s Secretary of State for Business, Innovation and Skills until he lost his seat in the general election earlier this year. He makes the point that manufacturing is the main generator of research and development, including the creation of intellectual property; the sector contributes disproportionately to productivity growth and standard of living; and is a major contributor to export income where it exists. He allows that the market must work in its own way. But he also argues that governments must not be passive (as shown by Japan and South Korea where business and government work in tandem). Cable is talking generally in terms of the manufacturing sector. But Musk, if he succeeds with his gigafactory, will have shown that it is possible for Western economies to re-establish manufacturing growth by harnessing the potential of technology metals, just as Talga is seeking to do in Germany. Technology metals are helping transform the mining sector: just 10 years ago there was scant talk (other than in specialty publications) about rare earths; even less about graphite which was then seen as mainly an industrial material. This has changed: now investors are quite savvy about these issues.

But perhaps it’s time to take this all a step further: to go

beyond the discovery and mining, and see how these metals

might restore and transform our industrial base.

Commodities in the “Year of

the Booby Trap”

Looking at the headlines

today of news items covering

the resources industry, I

was struck by how many

unexpected, or unwelcome,

developments are coming out

of the woodwork. Yet, just a

few hours earlier, I had

been reading yet another

analyst note saying that we

are at the bottom of the commodity cycle, and things are about

to pick up. Indeed, this is a line that I have begun running

with in recent weeks; after all, the cutbacks in production

(especially zinc) seemed in the past week or two to have put a

floor under prices.

Just last week a early stage graphite explorer, Ardiden

(ASX:ADV) had seen a capital raising oversubscribed (it has

its project in Canada). This was just one of many examples

occurring in recent weeks where exploration announcements had

seen investors piling into certain stocks. This was, I

reasoned, not at all like the gloomy time in 1999 or the post-

GFC period when you couldn’t sell a story – any story – to try

to get get some interest in the market.But then, again and today, there came another avalanche of gloom. How to explain this commodity dichotomy? Then I picked up this morning’s newspaper, turned to the business section, and there it was: 2015 is the Year of the Booby Trap. This insight came from an interview in the newspaper with Ashok Jacob, who runs the A$4 billion Ellerston Capital fund. And the booby traps? Well, there was the devaluation of the Swiss franc, the collapse of the oil price, the Volkswagen scandal and most importantly the devaluation of the Chinese yuan. I would add the European refugee crisis which could impede that continent’s economy recovery if the alliance fractures; the battle of the behemoths as the big iron ore makers ramp up production to try and crush the smaller players. And how’s that shale oil and gas revolution going? Oh, and then there was Molycorp. And now here is today’s news, which underlines Jacob’s predictions there will be further booby traps sprung on a fragile global economy before the year is out. Item # 1: China’s GDP growth slowed to 6.9%. While this reflects the transformation from industrial growth to widening of the services economy (a natural progression as economies mature) it is terrible news for commodities. This undoubtedly signals a weaker commodity demand environment in China – and that means everything from iron ore to technology metals. The impact was immediate: after the Chinese figures came out, aluminium fell 1.7%, copper was down 1.8%, lead down 1.3%, nickel by 2% and zinc was off 0.5%. Only tin defied the mood, rising 0.2% to $15,987/tonne, still not nearly enough to tempt any new producers to start up a mine. Item # 2: The normal economic response to low prices and oversupply is for mining (and oil) companies to cut back production, at which point prices can begin rising again as

supply starts to lag supply. But this is not happening, and most spectacularly in the case of the iron ore companies. Today we read that Brazil’s Vale had a record output in the September quarter of 82.2 million tonnes. This comes as Australian mines run by BHP Billiton and Rio Tinto continue to ramp up production, too. The iron ore price has fallen to $52/tonne from a 2011 high of nearly 2011. Also, it is estimated by London-based Wood Mackenzie that 55% of the world’s nickel is now being produced at a loss, but no one wants to cut back: so far, only 30,000 tonnes of capacity has been idled. The economic mechanisms are simply not working. (And, on the iron ore front, the Indian state of Goa has resumed shipments to China after the local mining ban was lifted.) Item # 3: News agency reports say Saudi Arabia is delaying payments to government contractors as the slump in oil prices pushes the country into a deficit for the first time since 2009. Companies working on infrastructure projects have been waiting for six months or more for payments as the government seeks to preserve cash. Did anyone expect the Saudis to have a cash flow problem? Item # 4: Iran is planning to add to the commodity glut. Bloomberg reports that President Hassan Rouhani will visit France and Italy in November to find foreign bidders for 15 projects. The country wants to boost its output of gold, iron ore, steel, chromite, aluminium, bauxite, copper and zinc. Just what the world needs! Ashok Jacob makes the point that all the money printing we have seen from the Fed and European, Chinese and other central banks was meant to have removed the risk of booby traps, but it hasn’t; and I would add that it was also meant to restore the globe’s appetite for commodities, which it has patently failed to do. Its main legacy has been to encourage the raising of trillions more dollars of debt.

OK, so QE hasn’t worked. Anyone got any other ideas before we trip over another booby trap? Blue Jays, Lithium, Uranium and Pot Back in April, the smart money picked the Washington Nationals to win the World Series, and with good reason, but as the season played out and Jonathon Papelbon reverted to old school choking, the Nats failed to make the post-season. No playoffs for you! The “experts” were wrong. There were also pre-season picks like St. Louis and the Dodgers, who did in fact have very good seasons. The experts were right. No one picked the Blue Jays to be a team verging on greatness. Mid-season changes and players having career-years propelled the organization to an expectedly giddy post-season. The

experts couldn’t have been expected to see that one coming. Making calls on public companies is similar to picking teams in the pre-season. Some calls look easy, but they don’t pan out. Others do. Some surprise everyone. And against that background we’re going to re-visit some of our 2015 picks. We started the year with Integra Gold – we call that one a win. Our first article of 2015 said Integra was a likely takeover target. It had just released its Preliminary Economic Analysis on its Lamaque properties in Quebec, form which we observed, “…Integra cut its cash needs, reduced the lead time to production by 25%, crammed down its all-in sustaining costs and provided visibility on the key metrics for success. They significantly de-risked the company and as a result made it very attractive to larger companies with stronger balance sheets.” In August, 2015 Eldorado Gold Corporation (“Eldorado”) invested $14.6 million into Integra by way of a non-brokered private placement of common shares, resulting in Eldorado holding 15% of Integra’s voting common shares. In a widely held company like Integra (and despite it being under the 20% threshold), that gives Eldorado control. Integra continues to report strong results and is running a $1M Gold Rush challenge aimed at crowd-sourcing brainpower to find the next gold prospect on its property. We expect more good news from Integra over the next several months. Copper Mountain Mining – unfortunately, we were right here, too. The full story of Copper Mountain’s shame can be found here, and the links in that article can be tracked backwards to the sorry beginning. In July we called it a “slow-motion disaster movie”. We have been highly critical of the board and management, not only for the poor operational results but mainly for the non-compliance with disclosure obligations. Copper Mountain misled the market

for over a decade, seriously harming the holders of the NSR on the property. Copper Mountain continues to disappoint. From a year high of over $2.30 down to its current price of roughly $0.55 a share, CUM shows what leverage does to a producer on the way down. With copper treading around $2.40 a pound, it’s unclear whether Copper Mountain will be able to continue as a viable operation. If it can hang on for another year or so, a supply- demand imbalance in copper might get leverage working upwards for the shareholders. In April we looked at two companies exploring in Brazil. Since then, one (Cancana Resources – manganese) has established a strong path to success while the other (DNI Metals – graphite) is still trying to find a way. Back then we said, “Cancana’s business model is to start with the known knowns. Develop the known manganese fields, consolidate title to the local boulder fields, and bring processing into one central plant. This should result in short term revenue, high plant usage, low downtime, and higher margins. Combining this with organic growth through the drill bit (scheduled to commence in May, 2015), Cancana has the opportunity to supply the global steel market while maintaining its premium charges.” Cancana has delivered on these goals. It has expanded its footprint, reported good exploration results, made progress with mining engineers Ausenco on centralizing the processing, begun selling product, and increased efficiencies. We like this narrative and expect more positive news from Cancana over the next 18 months. DNI Metals is still trying to execute on its business plan. It had a hard time closing on its announced private placement, and eventually had to change the terms of the offering to get the minimum amounts in the door. But close they did, and

management deserves credit for that. They have put the funds to work in Brazil and in Madagascar. The stock has drifted down significantly from its opening and finance price – time will tell if management can deliver. DNI’s season had a rough beginning but isn’t over yet. In a somewhat confusing move, DNI also recently announced it is acquiring a lab in the Greater Toronto Area to carry out testing and metallurgic work for itself and for third parties. We don’t like this acquisition. A junior exploration company needs focus to survive, and this acquisition is an unneeded deviation from the business plan. A company that is sticking to its business plan is Carube Copper, who is exploring assets in Jamaica. We’ve looked at them twice, once briefly and once in greater detail. We recently met with management for an update and are enthusiastic about its chances for success. Carube, in addition to the Jamaican assets, holds the British Columbia gold-copper assets puppied out of Wallbridge Mining in 2010. Carube has had considerable success staying on path. This is a strong deal with considerable upside offered by the assets themselves, the high quality management team and the partnership with OZ Mining, an Australian mining company with a billion dollar market cap. So far, Carube is having a good season and we expect that to continue. Another company we looked at who has ties to a much larger company was Contagious Gaming. At the time Contagious was operationalizing its English gaming assets and earning revenue in North America from its software platforms. Since then, Contagious has announced two large deals, made a serious disclosure gaffe, and is generally a puzzling company. The board and management have not done a good job engaging the shareholder base, but closing on either of the large announced

deals on accretive terms would be similar to the Blue Jays roster makeover halfway through the season. A failure to close on either deal would likely see the management team get demoted. Watch the news flow to judge management’s success. Also on the high tech front, in July we looked at Seair Inc. and its SWEET technology, aimed at oil / water separation in the oil patch. SWEET’s passive technology creates microbubbles in the oil, which lowers the cost of operation. Seair can separate more oil at a lower cost than any competing process. Customer payback ranges from only 3 – 6 months, an astounding short period of time. At that time we referred to Seair’s formal exclusive strategic partnership with Renewable Fluid Services (RFS), a U.S. based process and product development company. Seair will provide SWEET to RFS to use in RFS’ oil recovery process. This relationship has borne fruit. In late September Seair announced it had signed a confidentiality agreement with Petroleum Development Oman (PDO) with the intent to run a SWEET major field trial in a large polymer flood operation. Seair’s new management team is clearly focussed on taking what had been benched technology and commercializing it. We expect more good news as SWEET undergoes more field trials. Also in July we looked at the Fission – Denison proposed merger. At the time we liked the combined uranium portfolio of exploration and development properties, the cash flow from toll-milling at the Cigar Lake Mine and management fees from Uranium Participation Corporation, and the strength of the proposed leadership team. We also acknowledged weaknesses in the deal, which goes to Fission’s shareholders for approval next Wednesday, October 14. Some of those shareholders are strongly opposed to the deal. At a town-hall style held by Fission in Toronto on Oct 6, those shareholders made their voice heard. It’s going to be a

close call whether the deal is approved. Expect major consequences if the shareholders vote down the merger. And speaking of voting, we’re still waiting on the Allard decision and on the federal election before we make any medium term call on the marijuana industry. The Conservatives have made their anti-marijuana stance very clear – if you have any financial interest in the Canadian cannabis industry then a vote for the BigC is a self-inflicted wound. Purely from a cannabis viewpoint, the best result would be a Liberal government with the NDP having enough seats to make a difference. Cast your ballot accordingly. Last, we closed the season with a short piece that asked, given its poor energy density ratio, how did lithium become the metal of choice in the battery industry? How did this minor leaguer come to play in the big leagues? That simple question sparked an incredible amount of debate. My inbox was filled with conflicting commentary, opinions and science as to lithium’s properties when compared to other metals. Lithium’s continued use by electric vehicles and power tool manufacturers could be increased by better technologies for extraction and processing (see our piece on Pure Energy), but is at risk by commercialized research that empowers other metals to economically take lithium’s place. We will be moderating a panel at the Technology Metals conference in Toronto on Oct 13 and 14 at the King Edward Hotel. Chris Reed of Neometals Ltd. will lead a separate panel looking at lithium’s role and future – we intend to be there. Play ball!

Post Nuclear Germany – a Green Myth? In the wake of the Fukushima nuclear disaster in Japan, Angela Merkel managed to transition from being a Centre Right politician loathed by the European Left to being a darling of the Green Movement. The deed that achieved this transformation in sentiment was the precipitate announcement that Germany would phase out all its nuclear power plant fleet by 2022. It would be replaced by alternative energy sources such as solar, wind and tidal power, combined with energy consumption savings, under an initiative known as the Energiewende, or energy transformation. This sudden decision to phase out the nuclear plants also involved adherence to the pre-existing goal of reducing national CO2 emissions to 4% below 1990 levels by 2020, and by 80-90% by 2050. Easily said by a politician who won’t be around in 2050 to face the music on non-compliance!

All this sounds like, as they would say in the US, a “mom and apple pie” issue. Who wants to complain about all this good stuff going on? Well, the slight wrinkle in this plan is that to achieve this Quixotic goal, Germany is now burning more lignite coal than before Merkel made her shock announcement. Yes, in the age of reducing carbon emissions and after the acid rain scares of the 1980s (largely created by East German lignite being burned by power-generators) we now have Germany pumping out more of this stuff to reduce its dependence on nuclear. While those of Green sympathies in Germany may be cognizant (and acquiescent) of this fact, more of the environmentally- aware in other places are environmentally-unaware that the price they pay for less of the clean energy of nuclear is more of the same old, same old carbon pollution that the EU has been hot and heavy for decades against. In any case, the potential removal of German demand from the Uranium market has been one of the things weighing upon the price of the metal. The return to production of Japanese generators has helped change the mood for the better, but Germany is still a key part of demand and so I shall look here at how this situation evolved and how Germany’s renunciation of nuclear is a blow for clean-tech. The German Nuclear Scene In her first flurry of panic, Angela Merkel shuttered eight reactors, reducing the country’s capacity to nine reactors with 12,003 MWe capacity, and then to eight reactors with 10,728 MWe. The country’s 17 nuclear power reactors, comprising 15% of installed capacity, formerly supplied more than one quarter of the electricity (133 billion kWh net in 2010). Many of the units are large (they total 20,339 MWe), and the last came into commercial operation in 1989. Six units are boiling water reactors (BWR), 11 are pressurised water reactors (PWR).

According to the Frauenhofer Institute, German generating

capacity in April 2014 was 169.6 GWe comprising:

1 GWe nuclear

6 GWe hydro

7 GWe wind (0.6 offshore)

9 GWe solar, 28.2 GWe gas

2 GWe lignite

3 GWe hard coal

6 GWe biomass

In the first half of 2014 wind and solar PV had capacity

factors of 18% and 11% respectively, compared with 85% for

nuclear. In 2011 Russia provided almost 40% of the natural

gas, followed by Norway, Netherlands and UK, while only 14%

was produced domestically.

Some outside Germany perceive that the actions were taken due

to some legacy issue with Soviet-era facilities, but when

Germany was reunited in 1990, all the Soviet-designed reactors

in the East were shut down for safety reasons and are beingdecommissioned.

The Coal Splurge

Lignite is the cheapest source of electricity from fossil

fuels, and Germany has the world’s largest reserves of it. But

lignite causes the highest CO2 emissions per ton when burned,

one-third more than hard coal and three times as much as

natural gas. The three German coal-fired power plants are

among the largest point-sources of CO2 emissions in the world.

Germany’s CO 2 emissions have started to show a retrograde

trend:

1,051m metric tons in 1990

813m tons in 2011

841 m tons in 2012 and 2013

As a result, Germany could very well fall short of its 2020 CO2

target by five to eight percentage points.

Perversely for industrial users, Germany has become a source

of cheap electricity, but not for private consumers in

Germany, who have had to foot the bill for the renewable power

sources putsch, as a result of German feed-in tariffs.

In 2014, the German government parties passed the Climate

Action Program 2020, a rather idealistic strategy to reduce

emissions by around 70m tons annually by 2020, in light of the

fact that they are increasing, rather than decreasing the

burning of coal! The hefty cost of this policy: US$2.2bn to

$3.3bn per year, will be divided half and half between the

federal government and private consumers who have to pay more

for their electricity.

The overall share of coal in German electricity production has

shrunk from 56% in 1990 to 43% in 2014. During the same

period, the share of renewables in electricity production has

risen from 4% to 26%.Conclusion It is ironic that Germany comes across to the outside world as one of the most “green-conscious” nations in Europe, if not the world, but few seem to have realized that its precipitate disavowal of nuclear energy has plunged many neighbouring countries into a zone of heavier carbon emissions than would otherwise be the case, while making a mockery of global warming and lower emissions concerns. While Germany continues to expand solar and wind power, the government’s decision to phase out nuclear energy means it must now rely heavily on the dirtiest form of coal, lignite, to generate electricity. The result is that after two decades of progress, the country’s CO2 emissions are rising. The Merkel administration seems to have been given a “free-pass” by the environmentalists because the quid pro quo for this move has been the eventual removal of nuclear power from the country. This is a Faustian bargain indeed. With Japan reopening its nuclear plants and most other nations unfazed by nuclear power, Germany is the odd man out in eschewing an energy source that is carbon-neutral. There are limits to how much solar or wind power that can be installed and some nations are starting to run into the buffers, particularly with regards to offshore wind farms. The remarkable consensus from both sides of the German political fence towards the self-defeating retreat from nuclear energy, makes most think that the 2022 shutdown is inevitable. Frankly the pressure should be coming from EU partners baulking at the emissions raining down on them. That, plus a failure of alternative energy sources to reach the sufficient level of participation to replace nuclear, might just prompt a rethink. The share that coal possesses even now is massive compared to that of nuclear. Remove the nuclear and do not reduce the coal-fired and you have actually seen a deterioration of the share from clean-tech.

Bromby: Let’s give China

credit for its rare earth

dominance

(And, while we’re at it, let us

also allow some kudos for the

Carter administration over its

strategy for acquiring Chinese

strategic metals.)

The bottom line is that China did something that laissez-faire

Western governments cannot seem to manage: setting an economic

target and getting there.

This post is, to some extent, a follow-up to Jack Lifton’s

yesterday on China and rare earths, in which he remarked that

“I think that a specter is haunting global capitalism: the

specter of the success of a uniquely malleable capitalism with

Chinese characteristics”.

I recently re-read a 2010 paper by a U.S. Army analyst Cindy

Hurst published by the Institute for the Analysis of Global

Security. The paper, China’s Rare Earth Elements Industry:

What Can the West Learn? shows how the West lost the plot. She

says that in its early years Mountain Pass in California was

the largest rare earth mine in the world. During that time

American students and professors were greatly interested in

learning about the properties of the REE. Then, as China began

to gain a foothold in the industry, interest seems to have

waned. Why? According to one professor she quoted, studentstend to move to what is “hot” at the time, as there they can make the most impact both as students and later in their careers. In this case, advanced biofuels seemed the new “hot” thing. In China, as Hurst pointed out, things were quite different. Nearly 50% of graduate students who were coming to study at the Department of Energy’s Ames National Laboratory were from China; and each time a visiting student returned to China, he or she was replaced with another Chinese visiting student. In 1986 the Beijing government approved the National High Technology Research and Development Program, known as Program 863. A good deal of the money for the program went to rare earths technologies. Eleven years later, in March 1997, Hurst describes how China announced Program 973, then the largest basic research program in China, which also covered rare earths. And, talking of students, Xu Guangxian attended Columbia University from 1946 (when Chiang Kai-shek’s Kuomintang was still in power) until 1951 and he received a Ph.D in chemistry. Hurst tells how he returned to take up a post at Peking University and he was later caught up in the Cultural Revolution and went to a labour camp. After his release in 1972, Xu began the study of praseodymium, then in the 1990s launched several rare earth programs, many of which were vital to China gaining dominance in this industry. But, as Hurst points out, since the 1960s China had been deploying teams of scientists to research more efficient methods of extracting rare earths (although, as Baotou attests, there is still someway to go). Between 1978 and 1989 China managed to increase rare earth output on an average of 40% a year, according to Hurst. The end result, as we know, was that China started exporting (comparatively) large quantities of REE, causing global prices

to plunge. And, in more recent times, China has moved to become the dominant force in magnet technology. As Harry Lime (played so memorably by Orson Welles) said in that classic movie, The Third Man, “in Italy for 30 years under the Borgias they had warfare, terror, murder, and bloodshed, but they produced Michelangelo, Leonardo da Vinci, and the Renaissance. In Switzerland they had brotherly love − they had 500 years of democracy and peace, and what did that produce? The cuckoo clock”. Likewise with rare earths, it seems − and which takes us full circle back to Jack Lifton’s point about how Chinese capitalism has evolved. The West has known since (at least 2009) that China was going to restrict rare earth exports, by one means or another. Six years on, what has the West achieved to secure its own sources (as opposed to the rare earth explorers who have persevered without the back-up their Chinese competitors received)? Meanwhile, it seems the much-maligned (at the time and even now) Carter administration had a few clues about how to manage to the strategic metal needs of the United States. In 1981 the Los Angeles Times reported that the U.S. was the main buyer of the increasing tonnages of strategic metals (tungsten, uranium, molybdenum, vanadium and germanium) being exported by China. The newspaper quoted Chinese officials saying, in the 1979 when the U.S. agreed to sell China technology with both civilian and military uses, the Carter administration talked the Chinese (in return) into increasing their exports of the rare metals needed by American industry.

You can also read