JSE - GARP presentation - Stock exchange developments - Leila Fourie

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

JSE – GARP presentation

Stock exchange developments – Leila Fourie

www.jse.co.za

www.jse.co.za

Copyright© JSE Limited 2009

1

Top 20 WFE exchanges

Domestic market capitalisation (equities), July 2013

Taiwan SE Corp.

Singapore Exchange

Johannesburg SE $825,9 billion (18th largest)

BME Spanish Exchanges

National Stock Exchange India

BM&FBOVESPA

BSE India The JSE is a world class, liquid exchange. It

Korea Exchange is by far the biggest on the continent and

NASDAQ OMX Nordic Exchange

Shenzhen SE

one of only 4 African exchanges that are

Australian SE members of the WFE. It is the 4th largest

SIX Swiss Exchange bond market by value traded

Deutsche Börse

TMX Group

Shanghai SE

Hong Kong Exchanges

London SE Group

Japan Exchange Group - Tokyo

NASDAQ OMX

NYSE Euronext $m

0 5 000 000 10 000 000 15 000 000 20 000 000 25 000 000

www.jse.co.za

Sources: WFE

2

Finance is a Key Sector of the Domestic Economy

• South Africa has a world class financial

sector which accounts for around 20% of

GDP and provides employment for 12%

of the formal sector’s (non-agri)

employed

• In value terms, the stock market is

greater than the country’s total economy,

reflecting a high degree of financialisation

• The GFC of 2008-2009 has ushered in a

massive overhaul of financial regulation,

affecting banks, exchanges, CCPs,

CSDPs etc.

www.jse.co.za

Source: World Bank

3

Annual Stock Market Trends

USD Indices (2000=100) Indices (2000=100)

350 600 0

300 500 30

250

400 60

200 Divergence

300 90

150

200 120

100 ZAR depreciation

50 100 150

0 0 180

Developing Countries South Africa

JSE ALSI (LHS) USD/ZAR (RHS)

UK Germany

• South Africa’s stock market performance from 2002 up to the start of the GFC was more impressive

than that of its peers and some of the more developed markets

• It has also fared better post the GFC and has diverged from the currency’s performance since 2010

www.jse.co.za

Sources: World Bank; I-Net

4

JSE and Exchange Rate trends

Indices (Jan 2005=100)

350 50

Stocks continue to

Global financial crisis diverge from

economic reality;

300 bonds lose some 75

appeal as sovereign

indebtedness grows

and global LT rates

250 start to rise 100

200 125

150 150

Development of asset

100 price bubble

Strong portfolio capital Deteriorating domestic 175

inflows, aided by US factors; imminent end

and EU quantitative of QE measures

easing leading to capital

50 outflows 200

2005 2006 2007 2008 2009 2010 2011 2012 2013

JSE ALSI (LHS) USD/ZAR (RHS)

www.jse.co.za

Source: I-Net

5

Bond Market Trends

Sovereign spreads over USTs • From 2001 to 2007, positive domestic

(basis points) factors helped narrow the spread: GDP

1200

growth averaged 4.3% over this period;

interest rates declined from mid-2003 to

900

Aug 2006, fuelling spending and growth

600

• RSA’s sovereign credit rating also

improved between 2003 and 2007

300 • The GFC led to a blow-out of EMs

spreads in 2009

0 • Subsequently, however, a re-assessment

of “risk” led to a narrowing in spreads

Developing Countries Developing Asia

Latin America & Caribbean South Africa

www.jse.co.za

Sources: World Bank

6

Best Investment View of SA Asset Managers

Effective asset allocation

100%

9.0 12.5 14.2 17.3 14.0 14.9

90% 17.2 18.0 20.12 18.77

80% 17.2

13.4

12.7

9.6 8.5 12.7 13.6

70% 17.9 17.1 15.8

60%

50%

40% 72.4 71.7 69.5 68.9 69.4 67.0 66.7

30% 61.7 59.0 60.4

20%

10%

0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 Q2/2013

SA Equities SA Bonds SA Listed Property

SA Real Estate SA Cash SA Other

SA Commodities

www.jse.co.za

Source: Alexander Forbes

7

Uncertainty Heightens Volatility

Net inflows/outflows (Rm) Capital flows to developing countries

25000

20000

15000

10000

5000

0

-5000

-10000

-15000

-20000

2010 2011 2012 2013

Shares Bonds

• Foreign investors’ appetite for EM bonds after the GFC has been reflected on the JSE by strong net inflows into this

market. However, recently, these flows have wavered and there has been a moderate shift towards a preference for

shares.

• Portfolio inflows are at risk in the short-term for as long as speculation of an easing in QE continues to drive market

sentiment. www.jse.co.za

Sources: JSE; World Bank

8

The crisis changed our approach

www.jse.co.za

9

CCP purpose - providing settlement assurance

• Reduce systemic risk

• Ensure efficient, fair markets

• Protect investors

• Ensure orderly markets

• Promote transparency

www.jse.co.za

10But what is a CCP?

Counterparty Counterparty

A B

Should one of the counterparties to the trade default the other faces losses

(credit risk)

Central

Counterparty Counterparty

Counterparty

A B

(CCP)

A central counterparty (CCP) stands between two parties of a financial trade and absorbs

the credit risk each party faces by becoming the counterparty to each trade

www.jse.co.za

11CCPs in the spotlight

CCPs are seen as systemically important and if ineffective, they could be a source for

contagion, financial shocks and default

• 2008 Global Financial Crisis highlighted gaps in financial institutions risk management

• However, it also highlighted the important role that CCPs play in reducing trading risks:

Lehman Brothers’ entire derivative book that was cleared through LCH

Clearnet (a CCP) was successfully unwound and any losses absorbed by

the clearing house’s risk management controls

• Financial regulators focus widened from banks (e.g. Basel 2/3) to include CCPs

(CPSS-IOSCO, ESMA)

• CPSS-IOSCO requires a CCP to have sufficient financial resources to cover credit

exposures in extreme yet plausible market conditions

www.jse.co.za

12Nothing new...CCP failures prior to the 2008 crisis

CCP COUNTRY DATE DESCRIPTION

Caisse de Liquidation France 1974 • Steep rise in sugar prices attracted speculative investors, who were caught out by a

sharp correction, leading to inability to meet margin calls

• CCP failed to increase margin in response to greater market volatility

• Lack of coordination between clearing house and exchange

• Allocation of losses among GCMs were not transparent

Kuala Lumpur Malaysia 1983 • Crash in palm oil prices led to the default of six brokers

Commodity Clearing • CCP slow to respond to market conditions – 12 day delay between market crash and

House broker default

• Lack of management experience and coordination among market participants

Hong Kong Futures Hong Kong 1987 • Trading suspended for four days in the wake of “Black Monday”

Exchange • Bailed out by consortium of banks supported by government once it was clear the

guarantee fund would be insufficient

• Guarantee fund separate from clearing house and exchange – clearing house

responsible for risk management, but was not exposed to losses

• CCP did not increase margin despite sharp growth in trading volumes

• No position limits and high concentration of brokers

BM&F Brazil 1999 • Sudden $/Real devaluation caused two small clearing banks to default

• Margin and default funds insufficient as banks were beyond BM&F operational

limits, and margin stress tests were inadequate for major move

• Central bank intervened and bailed out the banks

Actual CCP failure Near CCP failure

www.jse.co.za

Source: Oliver Wyman 2011

13South African CCP: Safcom

• In South Africa, all exchange-traded derivative

trades are cleared through Safcom, a wholly

owned subsidiary of the JSE

• Safcom thereby mitigates systemic risk in the

South African exchange-traded derivatives

market, as it reduces the risk of a single default

impacting other counterparties and thereby

contaminating the market

• Imperative that Safcom’s risk management

practices are of the highest standards and its

financial safeguards quantified as accurately as

possible

• Equities are cleared by the JSE – potential exists to move to CCP model

www.jse.co.za

14Safcom growth – initial margin at an all time high

Initial Margin Date

1 20,141,569,086 27-Aug-13

2 19,935,505,763 26-Aug-13

3 19,892,281,931 01-Jul-08

4 19,852,376,156 02-Jul-08

5 19,838,111,897 22-Aug-13

6 19,830,893,646 15-Jul-08

7 19,807,451,439 23-Aug-13

8 19,755,821,585 18-Jun-08

9 19,753,674,514 08-Jul-08

10 19,747,127,668 14-Jul-08

www.jse.co.za

15Creditworthiness of the CCP: Safcom

Safcom mitigates its risk through the following measures:

1. Entry requirements to becoming a clearing member (financial and capital adequacy

requirements)

2. Collateral for each trade that is cleared – initial and variation margin

3. A default fund, to which all clearing members must contribute, that can be accessed

to cover losses suffered as the result of one clearing member defaulting

4. Fidelity fund – for isolated and limited circumstances

In addition:

• Back testing

• Stress testing

• Default ‘fire drills’

• Safcom risk waterfall

• Risk tolerance

• Liquidity lines

www.jse.co.za

16Main trends - CCPs

www.jse.co.za

171

Re-regulation

and extra -

territorial reach

www.jse.co.za

18Re-regulation and extra-territorial reach

The G-20 reform was a catalyst for a coordinated global regulatory response

US Dodd-Frank Act • SWAP dealers and participants must register

• Central reporting in a depository

• Central clearing of standardised OTC derivatives

• Mandatory margin for cleared trades

• Central trading of standardised derivatives

• Restriction of activities

EMIR • Operational risk monitoring measures

• Central reporting

• Central clearing of standardised OTC derivatives

• Regulation of CCPs as ‘systemically important’

BIS / Basle III • Lower capital for centrally cleared derivatives and structured products

• Capital for default fund contributions

• Margin for non-centrally cleared transactions

CPSS IOSCO • Global standard for CCPs and financial market infrastructures

www.jse.co.za

192 Product

expansion . . .

OTC clearing

www.jse.co.za

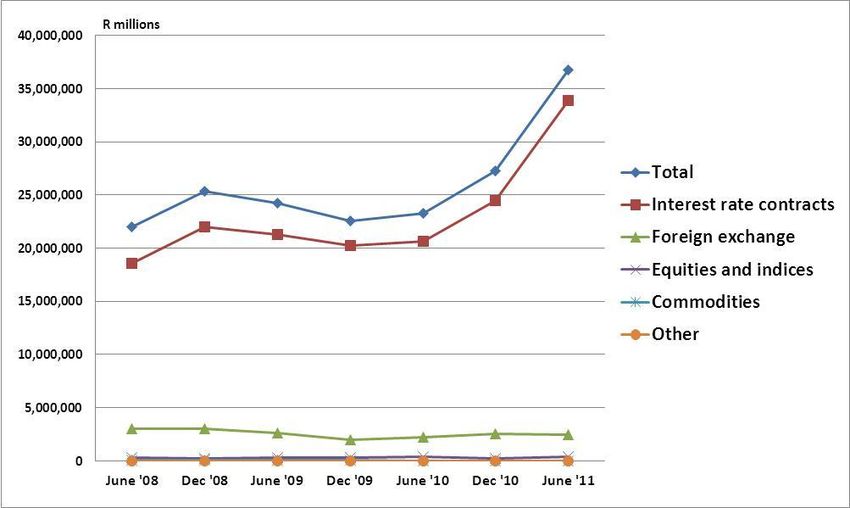

20OTC Derivatives Clearing : Market size

According to BIS, 85% of all derivative transactions are traded OTC

• In June 2008, the global OTC derivatives market

gross notional outstanding peak trading volumes

were more than $680 trillion

• OTC trading increased by 535% over 7 years to

2008

• OTC market subsequently contracted to $615

trillion to date

• 2010: ZAR OTC derivatives ZAR24 trillion,

ZAR800 billion traded on exchange

www.jse.co.za

Source: BIS, ISDA, SARB

213 Default funds –

more science

required

www.jse.co.za

22CCP risk waterfall

• A CCP’s risk waterfall defines how risk mitigants will be used in the case of a default

• A typical CCP (and Safcom’s) risk waterfall follows a defaulter-pays model

In the case of a default, losses are funded as follows:

Initial margin of the defaulting clearing member

The defaulting clearing member’s contribution to the default

fund

CCP’s contribution to the default fund

Non-defaulting member’s contribution to the default fund

www.jse.co.za

23CCP default fund quantification

Possible alternatives to quantifying a default fund:

• CPSS-IOSCO requires a CCP to have sufficient financial resources to cover credit

exposures in extreme yet plausible market conditions

• Default fund must cover losses under extreme market conditions

• Therefore need measures of extreme losses, or tail-end losses

• Conditional VaR (CVaR) = the expected loss given that VaR is exceeded

• Extreme VaR (EVaR) = employ EVT for modelling losses within the tail end of a

distribution of returns

• Stress Testing = possible losses on today’s portfolio should historic stress events

repeat

www.jse.co.za

2425

4

Capital

adequacy

requirements

for CCPS?

www.jse.co.za

25Capital

Capital is now a focus for CCPs

• Economic capital in a CCP refers to all levels of prefunded resources to protect

the market and the structure thereof

• Twin Peaks regulation – trend: CCP capital adequacy to be regulated

• Safcom economic capital approach:

• Operational risk

• Counterparty risk

• Legal risk

• Liquidity risk

www.jse.co.za

264 The search

for margin

efficiency

www.jse.co.za

27The search for margin efficiency

• Growing demand for collateral puts margin efficiencies in the limelight.

• Growing number of CCPs are offering initial margin offsets between OTC and

ET derivatives.

• Margin Methodology:

• CCPs have traditionally made use of portfolio scanning methodologies when

determining initial margins for ET derivatives.

• Portfolio scanning typically fails to adequately recognise the benefits of

diversification.

• CCPs are looking to migrate towards VaR type portfolio margining methodologies

(Eurex call’s theirs Prisma).

www.jse.co.za

28Unknown unkowns

• How many CCPs is right?

• Capital markets are global, regulators are national – how do we reconcile

these?

• How do small countries manage systemic risk when much of the flows are

offshore?

• How to align global regulatory trends to the national agenda?

• How much capital should a CCP hold?

www.jse.co.za

29Thank you

www.jse.co.za

30Contact the JSE & join us on social media

Email: Leilaf@jse.co.za

www.jse.co.za

Copyright© JSE Limited 2011

31You can also read