Making headway in Japanese offshore wind - bidder scrutiny of auction rules continues - MARCH 2021 - Ashurst

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Making headway in Japanese offshore wind – bidder scrutiny of auction rules continues MARCH 2021

Auction guidelines face continued bidder scrutiny

In our latest briefing on the Japan offshore wind market,

we discuss the key themes and issues arising out of the

latest public consultation between the government and

potential bidders for the first round of fixed-bottom

offshore wind farms in Japan

Background

On 27 November 2020, the Ministry of Economy, Trade and Industry ("METI") and the Ministry of

Land, Infrastructure, Transport and Tourism ("MLIT") (together, the "government") released the

finalised auction guidelines for the first round of fixed-bottom offshore wind projects in Japan. Bids will

be accepted by the government until 27 May 2021 (5pm).1

Alongside the publication of the finalised auction guidelines, the government released a first set of Q&A

in respect of the public consultation regarding the previously published draft auction guidelines

("Q&A#1").2 There were 1,324 submissions by 43 participants, demonstrating a high level of

engagement by the market. Please click here for our detailed briefing note on these submissions.

On 1 March 2021, the government released a second set of Q&A in respect of the auction guidelines

("Q&A#2"). 3 There were 272 submissions answered by the government in Q&A#2, which also

included questions by bidders on the form of port lease contract (released by MLIT on its website in late

December 2020).4 This briefing note focusses on the key themes and issues from Q&A#2 on which

bidders appear to be focussed at this stage of the bidding process.

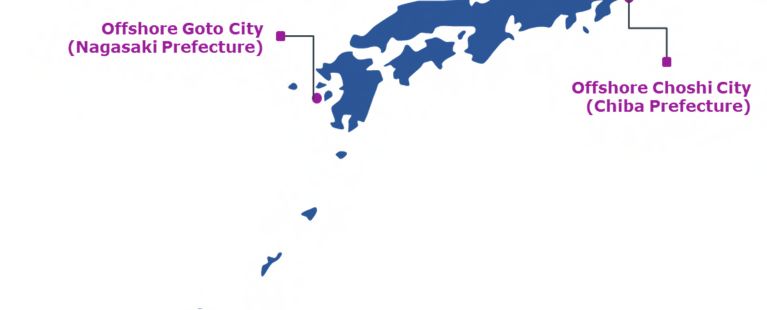

Japan's offshore wind "Round 1" projects

1

https://www.enecho.meti.go.jp/category/saving_and_new/saiene/yojo_furyoku/dl/sentei/koubo_20201127.pdf

2

https://public-comment.e-gov.go.jp/servlet/Public?CLASSNAME=PCM1040&id=155201106&Mode=1

3

https://www.enecho.meti.go.jp/category/saving_and_new/saiene/yojo_furyoku/dl/sentei/kouboFAQ_20210301.pdf

4

https://www.mlit.go.jp/kowan/kowan_tk6_000068.html

1FIT TERM

By way of summary, the FIT term is 20 years from the scheduled operation date

("SCOD"), and the SCOD must be a date that is no longer than 8 years after the

successful bidder notice is provided. The FIT term will be reduced to the extent that the

actual commercial operation date ("COD") is delayed beyond the SCOD set out in the

Occupancy Plan submitted by the bidder as part of its bid.

In Q&A#2, bidders continue to focus on the limited circumstances in which the

government may entertain an extension to SCOD, demonstrating that a shortening

of the FIT term remains a key risk factor for bidders. On this point, and in Q&A#1, the

government has generally conveyed the message that any risk of delay to COD would be

a risk for the successful bidder to manage.

In response to this position, question 5 in Q&A#2 raises the issue of delay in grid works

undertaken by the local utility. This question focusses on the circumstances in which a

local utility rejects the inclusion of any delay damages liability concept in its construction

contract. The bidder points out that in this scenario, the risk would no longer be

capable of being managed by the preferred bidder and accordingly asks whether

the government would order the local utility to agree to the inclusion of delay damages

in its contracts, or whether a delay to COD would otherwise be approved by METI for grid

delay attributable to the utility (without a shortening of the FIT term).

The bidder comments that if neither of these options is available, the successful bidder

would be responsible for a risk it cannot manage and, accordingly, SCOD would

need to be set at the maximum 8 years, with this particular bidder seemingly being of

the view that it would not be possible to propose an earlier SCOD due to this risk. In

addition, it would not be possible to offer the lowest possible FIT (resulting in an

increased burden on consumers).

The government's succinct response was that it refrains from commenting on

contracts between enterprises, confirming that it considers grid delay to be a

bidder risk.

Other related questions in Q&A#2 focus on the determination of the start date of the

occupancy period, evidencing how focussed bidders are on timeline, presumably in no

small part due to the very limited circumstances in which an extension to the SCOD will

be granted.

PORT USE ISSUES AND THE PORT LEASE CONTRACT

Approximately 1/4 of the submissions of Q&A#2 concerned port use, evidencing

how port availability, suitability, restrictions and fees are a key focus for bidders at this

point in time, with a particular focus on issues surrounding "overlapping use" of the ports.

It is worth reiterating that delays caused by overlapping use of the port by a separate

successful bidder (in respect of a "renewable energy complex") remains the one possible

avenue for a SCOD extension, so it is perhaps not surprising that there have been

renewed bidder questions in this area.

Bidders in particular focussed on the content of the "required discussions between

the business operator and the government" that would take place in the event of

such aforementioned delay, and how long such discussions would be expected to take.

The government replied that the length of discussions would depend on the

2circumstances, and that it would consider required changes to the occupancy

plan in line with the auction guidelines.

It is worth noting that some of the port related issues raised by bidders are addressed in

the draft form of port lease ("Port Lease"), published on the MLIT website in late

December of last year. Article 44 of the Port Lease is of particular note, as it would

appear to be the government's response to requests from the industry to ensure that

port related contracts cater for project financing (and, in particular, associated direct

agreements).

A number of questions in Q&A#2 concerned the Port Lease.5 One participant

queried whether delays to the project which were due to the unforeseeable state of the

leased property would result in an extension of the FIT term.6 The government simply

responded that disputes between the parties would be resolved in accordance

with the dispute resolution mechanisms in the Port Lease (reinforcing how limited

the circumstances are in which an extension to the SCOD will be considered by the

government).

As mentioned above, several questions also concerned the issue of overlapping use and

the way this is addressed in the Port Lease. Generally, the government's view is that the

contract concluded first in time will prevail, but if the holder of the earlier lease changes

its period of lease subsequently, the later contract would prevail. 7 A number of questions

also concerned the calculation and payment of fees.

Bidders also focussed on the content of the direct agreement envisaged by

Article 44, which seems to require a direct agreement only when parties A and B (i.e.

MLIT and the port manager) deem the same to be "necessary", with a follow up query

concerning whether or not parties A and B would agree to the inclusion of certain

"market standard" project finance direct agreement provisions.8

In line with the government's favoured approach of giving itself leeway to consider

each issue on merit at a future point, it simply reiterated that whether a direct

agreement was necessary (and the form of the same) would need to be

discussed with parties A and B at the appropriate time. However, the

government does stress that the provisions of any direct agreement should not

override the contents of the lease contract itself, and should not impose one-sided

obligations on the government entities. What this means in practice is unclear for

now, and we would expect follow-up questions to be raised in relation to this issue.

5

See questions 193 to 231.

6

See question 199.

7

See, for example, questions 206 and 207.

8

See question 230.

3EVALUATION CRITERIA

A key area of focus of bidders in Q&A#2 relats to how the government will implement

the project implementation and local community / economic impact scoring

system of the evaluation criteria, with roughly half of the submissions related

to this theme. The number of questions in this area perhaps displays a level of unease

amongst the bidders with regard to the qualitative nature of Japan's offshore wind

auction scoring system.

Many questions related to which entities making up the SPC / consortium (and which

entities within the general corporate structure of applicants and members of the SPC or

consortium) would be evaluated for the purposes of the scoring criteria.

For instance, given that the previous experience of entities which hold voting rights in

the SPC will be the object of evaluation for the purposes of scoring the occupancy plan,

one bidder asked to what extent the proportion of voting rights in the SPC would

be accounted for in the score. The government replied that the occupancy plan should

clearly indicate which entity plays which role in the project. 9 The government also

reiterated that where the experience of several entities is put forward for the same role

at the same time, the lowest experience score achieved by any of the relevant entities

will generally be taken into account. 10

However, the government also went on to say that if the bid submission makes it

clear in what way the joint role will be organised in terms of implementation,

human resources and sharing of information, this organisational setup between

the entities will be taken into account for the score. 11

As will not be surprising to any follower of the Japan offshore wind industry, the

government is therefore seemingly giving itself a not insignificant level of flexibility to

score the SPC/consortium members as it sees fit, on a case by case basis.

Other questions focussed on how parent company experience would be

evaluated – the short answer being that if there is evidence that parent company

experience is also the experience of the relevant entity (for example because of the way

the parent and the subsidiary are organised and share information), then the experience

of the parent company may be taken into account, but whether this scenario applies

would (unsurprisingly) be judged on a case-by-case basis. 12

Bidders have attempted to procure clearer guidance from the government in terms of

the exact criteria that would be used to determine when experience of other group

members within the corporate structure would be taken into account, but the

government is reserving its room for deciding each case on its own merits.

Bidders are obviously keen to understand where they might be able to use the

previous experience of parents and subsidiaries to achieve an improved score,

and wish to avoid a scenario where the lowest score of several entities put forward for a

particular role is adopted in the final assessment. However, it seems that the government

9

See question 33.

10

See, for example, questions 108 and 154.

11

See, for instance, questions 86, 92, 94 and 98.

12

See questions 94 and 102.

4is again keen to not limit its ability to decide the score of each submission on its particular

merits.

Separately, it is interesting to note that, compared to Q&A#1, there are now fewer

questions 13 around the sell-down categories of equity which the government had

previously singled out as not generally being permissible, which suggests market

participants are now to some extent comfortable with the restrictions around the sell-

down of equity, or have otherwise decided that they are able to structure based on the

government advice to date and the auction rules.

FIT TARIFF AND FIT APPROVAL

In comparison to Q&A#1 there were notably fewer questions on the FIT ceiling

price of 29 JPY/kWh, suggesting that bidders are becoming more familiar with how

this price was calculated (with some bidders perhaps retaining their objections to the

level of the ceiling price itself).

However, a number of FIT related questions did enquire about a scenario where a

selected bidder has entered into several connection agreements, and whether a different

SCOD could be set for each of these connection agreements (a possibility the government

had previously confirmed as acceptable to bidders). In response to these queries, the

government confirmed that the FIT approval process would be carried out separately

for each connection agreement (and that each would be the subject of a separate 20-

year FIT term). 14

In addition, there are several questions about the requirements for the FIT approval

application procedure, which remains to be published.15

The government plans to publish this information on the website of the

Agency for Natural Resources and Energy as soon as possible, although no

specific time frame was given for such publication.

INCUMBENT DEVELOPERS

We highlighted in our previous Japan offshore wind update that the auction rules do

not contain any clear protections for incumbent developers, or address their

position (with the exception of the transfer mechanism in the rules concerning grid

connection rights). This topic emerges once again in Q&A#2.

Bidders are seemingly attempting to ascertain to what extent an incumbent developer,

who would have already invested significant time and resources into stakeholder

relationships, would have an advantage due to its longer established connections to the

region.

During Q&A#1, the government had previously stated that it might also take into account

the time invested. A bidder picked up on these previous responses by the government in

Q&A#1, and stressed that efforts by incumbent developers and the understanding such

developers already have with (for example) the fishery community must form part of

13

Questions 33, 34,63, 84, 86, 123, 124, 125, 140.

14

See questions 6 and 8.

15

Questions 18 and 126.

5their score in the bidding process. 16 The government replied that if the occupancy plan

aligns with the opinion of the local council (set up in each promotion zone), then it

would be possible that this is taken into account for the score in relation to the

degree to which the occupancy plan is realistic.

This general reference to the provisions of the auction guidelines highlights once again

that the government does not want to restrict itself and will consider each submission on

a case-by-case basis.

In its responses in Q&A#2, the government also encouraged bidders to include any items

demonstrating the ability to create long-term and well-coordinated relationships with the

local government bodies. It also stressed that only the experience of the auction applicant

itself (and, if an SPC or consortium, the experience of the members) will count in this

area. It seems that this is the furthest the government is prepared to go in

terms of recognising the efforts made by incumbent developers at this stage,

and incumbent developers will largely have to wait and see whether their efforts to date

will be rewarded by a higher qualitative score when compared to bidders who may not

be as well known to the local community for example. For context on this point, it is

perhaps worth mentioning as a reminder that the auction rules provide for a

maximum of 40 points in respect of local community / economic impact, out of

an overall score of 240 points.

LOCAL COMMUNITY AND FISHERIES

Relationships with the local community, and the local fishery bodies in

particular, formed the basis of a large number of questions in Q&A#2.17

Government responses, as a general theme, emphasised the importance of

establishing good relationships with the local community to ensure the long-

term implementation of the project (and that any evidence of efforts made in relation

to this should be included in the bid submission where bidders believe they have had

relevant achievements in this area). Bidders also asked how widely "region" would be

defined in terms of assessment of the impact on the local economy of the region. The

government replied that while it did not intend to impose a limiting definition, the

opinion of the prefectural governor would be taken into account as representative of

the relevant region.

Bidders also queried the requirement for obtaining the understanding of the local

fisheries (which are part of the relevant local council set up for each zone) prior to the

application for the occupancy permit. The government reiterated that this is at the

discretion of the relevant fishermen.

A number of questions then related to the contributions to the fund for the

benefit of the local region and fishery industry – an ongoing concern of many

bidders it would seem. The government clarified that, given the exact amounts etc will

be discussed with the local council following selection, at bid submission stage a

reasonable estimate of contributions will be sufficient.

There were several questions on this topic in relation to the individual promotion

zones.18 For example, regarding Noshiro, a bidder queried how the position of wind

16

See question 78.

17

Question 61, 62, 65, 66, 70, 71, 72, 78, 81, 82, 83, 101, 128, 129, 131 and 133.

18

Question 236 and following.

6turbines could be determined, following an explanatory meeting of the local council

during which it had been stressed that before installing the turbines, the location of the

turbines should be discussed with fishery personnel (which would seem to contradict

the rule that contact between bidders and local officials at this stage is not permitted).19

The government reiterated that, in line with the summary of the opinion of the local

council attached to the auction rules, the placement of turbines would need to

reflect that the local fisheries have been taken into account and sufficient

explanation to the fisheries carried out. However, contact with the relevant fishery

personnel during the auction process would not be envisaged. Whether or not this

response satisfied the bidder who raised the question is open for debate.

There were also participant concerns as to the level of contribution to the

fisheries and local community fund – an ongoing theme of the auction rules

for some time now.

For Noshiro20, bidders generally queried whether the amount contributed (which the

auction guidelines had estimated 0.5% of the income from the sale of electricity over

20 years) might exceed the 0.5% mark annually as a result of the deliberations of the

local council. Bidders also queried whether operations would have to be stopped if

agreement could not be reached.

The government replied that given the estimate was 0.5% of sales over the 20

year period, the contribution would not necessarily be exactly the same each

year. In addition, the government highlighted that the selected bidder itself would

become a member of the council. There were also numerous queries concerning how

the amount of contribution was to be estimated at bidding stage and consequences if

the actual amount of contribution were to exceed the estimate at bidding stage (or the

actual income from sales to differ from the estimate).

The government reiterated that details of the fund contributions would be settled

after discussion with the council following selection of the successful bidder.

Similar concerns were raised by participants regarding Yurihonjo21 and Choshi22.

Uncertainties around the level of contribution to the fund therefore seem set

to continue for the foreseeable future.

DECOMMISSIONING

Decommissioning costs and associated security continue to attract many

questions from bidders.23

The government reaffirmed that the detailed methods and detailed costs of

decommissioning would not need to be included for the bid submissions (and indicating

whether a bidder planned to remove all equipment or only part of the plant would

suffice), and would be covered in amendments to the occupation plan prior to

beginning of construction.

19

See question 251.

20

See questions 243 – 248, 250 ,253.

21

See questions 257 – 263.

22

See question 268.

23

See questions 19 – 25, 55, 57, 104, 105, 132.

7The cost of decommissioning should be assumed to be 70% of the offshore

construction costs for the purposes of bid submissions. However, the

government stressed that this only applies to the offshore renewable energy generation

facilities: the cost of removal of any other facilities will form part of the assessment as

part of the income and expenditure plan (and, depending on the individual case, the

economic effect on the region and the country).24

There were also several questions about the technicalities surrounding the

decommissioning security (or reserves, as applicable). The government also confirmed

that the letter of interest for any decommissioning LC or guarantee would not need to

state the exact amount. Decommissioning method and costs will need to be assessed in

detail (and corresponding changes made to the occupancy plan) prior to the start of

construction.

ADDITIONAL POINTS OF INTEREST

We also note the following points raised in Q&A#2, which may be of interest to market

participants:

The government has clarified that electricity can only be sold to the relevant

local utility.25

A very low FIT put forward may count against the bidder if the government

considers that, in reality, it would be difficult for the bidder to achieve a profit.26

Pre-COD generation:27 it seems that it will not be possible for selected bidders to

sell any electricity generated during trial runs prior to COD. This attracted

some unhappiness from bidders, who highlighted that pre-COD generation can be

sold for onshore wind and solar, but the government referred back to the previous

relevant committee determinations on this point.

Several participants raised questions on the security.28 In particular, due to the bid

configurations possible for Yurihonjo (North, South and both zones together), one

bidder asked whether (if bidding for both zones at once as well as the North zone

separately) separate guarantees would be required. The government confirmed

that if a guarantee for both zones is submitted, no separate guarantee for

the North zone would be required. There were also several questions

surrounding the detailed forms and procedure for the guarantees.

With regard to bids that have been prepared using the bidder's own original data

(rather than the data offered by the government), the government was asked

whether there was a risk that it would view the bidder's own data as

unreliable in the event of there being a material discrepancy between the

bidder's own data and the government's data, and whether this might then

result in a lower score. In response, the government stated that there may be

cases where a low score is given if the occupancy plan is clearly unrealistic

on the basis of the government's survey results.

24

See question 21.

25

Question 1.

26

Question 2.

27

Questions 3 and 4.

28

Questions 35 – 44.

8 We also note that several participants asked how subcontracts for implementation

would be assessed, suggesting that multi-contract procurement models may

be adopted by particular bidders.29

The version of Q&A#2 published on the METI website contains an introductory note

which states that METI is "unable to answer questions about the provision of

information obtained through national surveys, as this information is subject to

confidentiality. Please contact us separately via the applicant of the confidential

information". Bidders should therefore bear this in mind if it had particular

questions or concerns with regard to national surveys.

The government affirmed that changes to the occupancy plan might be

permitted to reflect both a change to the model as well as to the maker of

the wind turbine (as long as the conditions for a change to the occupancy plan as

set are fulfilled).

29

Questions 48 – 50, 75, 89, 90, 110.

9Concluding remarks

The focus of bidders in Q&A#2 has moved away from material

concerns with the FIT ceiling price of 29 JPY/kWh and the

restrictions on the sell-down of equity. While bidders may of course Bidder attention now

retain a degree of concern in relation to these two key areas, they seems to be firmly placed

are not (at least through the formal Q&A public consultation on key practical issues

process) seeking on a material level to raise further objections with such as the scheduled

the government on these topics. date for completion,

However, the lack of protection with regard to any delay to adequacy and availability

the commercial operation date that is outside of bidder of port facilities, and

control evidently remains a key concern of the bidding interaction with the local

community. The government has been steadfast in its responses community

to the high volume of bidder questioning in this area - no extension

to the FIT term will be afforded in the event COD is delayed beyond SCOD (other than the limited

exception discussed above with regard to any overlapping use of the applicable port by another

successful bidder). Presumably the government considers that the competitive tension present in the

market will be sufficient to mitigate the risk of all bidders simply (a) specifying a SCOD that is the

maximum length allowed under the auction rules (i.e. 8 years from the date of the successful bidder

notice), and/or (b) bidding the ceiling price of 29 JPY/kWh, in order to mitigate the risk of delay which

is outside of its control. It will be interesting to see whether bidders are prepared to

bid a shorter COD or not.

In addition to the key concern around the SCOD,

bidder attention seems to now be increasingly

Bidders are focusing on how the focussed on the use and adequacy of the

government will interpret the qualitative applicable port. Publication of the draft lease port

aspects of the auction scoring system contract has gone someway to answering a number

of bidder questions in this area, but it is clear from

the number of submissions in Q&A#2 that bidders' concerns in relation to port use and development

remain. Such concerns would seemingly need to be taken into account in the determination

of each bidder's SCOD.

Following on from Q&A#1, the number of submissions in Q&A#2 relating to the fishing industry

and fund demonstrate that this topic remains a key area of focus for the bidding community.

It would seem however from the government responses to these submissions that it will be sometime

before we see clarity emerge with regard to issues such as fishing fund contributions.

Lastly, and as a general comment, it is clear from a review of the submissions in Q&A#2 that particular

bidders are focusing intently on how the government will interpret the qualitative aspects of

the auction scoring system. In general, the government's position is that it will be assessing

occupancy plans on a case by case basis, and it notably stayed away from providing bidders with any

clear cut position on the specific queries raised in this area. This is not surprising, and fits in with the

theme of the government consistently giving itself broad discretion to consider the merits of

each point in question on a case by case basis.

With bid submissions due in May of this year, exciting times lie ahead for the industry in Japan. If you

would like to discuss any point raised in this briefing note in further detail (or any of our other previous

briefing notes on offshore wind in Japan30), please do not hesitate to get in touch with any of the

Ashurst Japan offshore wind team (details below). We would be delighted to hear from you.

30

"Making headway in Japanese offshore wind - Japanese parliament passes Offshore Wind legislation" ; "Making headway in

Japanese offshore wind - one year on"; "Making headway in Japanese offshore wind - Auction guidelines face bidder scrutiny"; and

"Offshore Wind in Asia: Recent Developments and Future Opportunities"

10ASHURST KEY CONTACTS FOR OFFSHORE WIND IN JAPAN

David Wadham Frédéric Draps

Managing Partner, Tokyo Partner, Jakarta

T +81 3 5405 6203 T +62 212 996 9250

M +81 90 4828 5191 M +62 811 962 05060

david.wadham@ashurst.com frederic.draps@ashurst.com

Kensuke Inoue Peter Grayson

Partner, Tokyo Senior Associate, Tokyo

T +81 3 5405 6223 T +81 3 5405 6088

M +81 90 5190 0360 M +81 80 8053 9933

kensuke.inoue@ashurst.com peter.grayson@ashurst.com

Chiharu Takatori Eva Zimmermann

Associate, Tokyo Associate, Tokyo

T +81 3 5405 6217

T +81 3 5405 6082 M +81 80 2561 6218

chiharu.takatori@ashurst.com eva.zimmermann@ashurst.com

www.ashurst.com

This publication is not intended to be a comprehensive review of all developments in the law and practice, or to cover all aspects

of those referred to. Readers should take legal advice before applying the information contained in this publication to specific

issues or transactions. For more information please contact us at Shiroyama Trust Tower, 30th Floor, 4-3-1 Toranomon, Minato-

ku, Tokyo 105-6030 T: +81 3 5405 6200 F: +81 3 5405 6222 www.ashurst.com.

Ashurst Horitsu Jimusho Gaikokuho Kyodo Jigyo is part of the Ashurst Group. Further details about Ashurst can be found at

www.ashurst.com.

© Ashurst LLP 2021. Ref:369029823 8 March 2021

11www.ashurst.com

You can also read