Pandemic Borrowing With the EU member states agreeing to borrow together to combat the impact of the COVID-19 pandemic, the issue of sovereign ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Questions of Power

Pandemic

Borrowing

With the EU member states agreeing to borrow

together to combat the impact of the COVID-19

pandemic, the issue of sovereign debt has reared its

ugly head once again―and with it the unresolved

tensions between the eurozone and the EU.

By Helen Thompson

T

he coronavirus pandemic has forced the vio Berlusconi’s last weeks in office in the autumn

European Union to confront again the long of 2011. Now, Italy’s 10-year bonds have fallen to

troublesome issue of sovereign debt in the eu- all-time lows.

rozone, as governments borrow to fund stimulus But Lagarde’s slip and the fury in Rome at her

programs needed to stave off the worst economic remark did draw attention to the crucial importance

effects of the pandemic. While the agreement on a of both what the ECB does and how the ECB is per-

Recovery Fund in July 2020 seems to have shown a ceived in making a number of eurozone members’

move toward more European solidarity, navigating debt serviceable, starting with Italy’s. The eurozone

a way through the difficulties national debt caus- crisis ended in 2012 because the then ECB president,

es in a transnational monetary union continues to Mario Draghi, found a way of establishing an asset

create existential questions for the EU. purchase program in Outright Monetary Transac-

In immediate terms, the situation is not nearly tions (OMT) acceptable to the German government

as bad as it was a decade ago, during the global that investors believed could be used, even if in

financial crisis of 2009-12, because for now no eu- fact it never has been. In January 2015, when the

rozone state faces being shut out of international far-left Syriza party won the Greek general elec-

capital markets. Even when European Central Bank tion and there appeared a serious risk of a second

president Christine Lagarde told a press conference all-encompassing eurozone crisis, Draghi took the

on March 12 that it was not the job of the ECB to opportunity of a setback for those challenging OMT

reduce the spreads, the spike on Italian bonds was in the German Constitutional Court, the Bundesver-

extremely modest compared to the borrowing rates fassungsgericht, to announce the ECB’s first Quan-

confronting Italy during former Prime Minister Sil- titative Easing (QE) program. Without question, this

20 | IP Special • 2 /2021Pandemic Borrowing

move prevented “contagion” from Greece relied on taking advantage of the Europe-

to the rest of southern Europe before the an Commission suspending the EU’s state

third Greek bailout. As his term of office aid legal regime to provide support for cor-

came to an end last year, Draghi also gave porations like Lufthansa also opened the

the Italian government a parting gift by prospect of borrowing inequalities making

resuming that QE program. Any sugges- themselves manifest in the Single Market.

tion that the ECB doubts the wisdom of Even before the decision from Karls

buying Italian debt still risks disaster, a ruhe, French President Emmanuel Macron

reality effectively acknowledged when, a had seen the pandemic as an opportunity

few weeks after Lagarde’s statement, the to revisit the issue of joint eurozone debt.

ECB announced its pandemic QE program, But without a real risk that the ECB would

with fewer rules constraining bond pur- be stopped in its tracks tempting investors

chase from individual member states. to push Italian yields back toward crisis

It was in this context that the Bundes- levels, he could not shift German Chan-

verfassungsgericht’s ruling in May that the cellor Angela Merkel’s position. Only

ECB had acted outside its competences by when the German Constitutional Court

failing to conduct an adequate proportion- pushed back did the calculus confront-

ality assessment took on the significance ing the chancellor change. If the original

it did. If the court had ruled between De- QE program fell short of the ECB’s legal

cember 2018 and October 2019 when QE authority, then pandemic QE would have

appeared to have come to a definitive end, no chance of satisfying the court. The ex-

then its decision would have mattered isting alternatives to the ECB commitment

rather less. But coming as it did with one were unpropitious. Although the Europe-

QE program in operation and another more an Stability Mechanism (ESM) provided

ambitious one―to deal with the COVID-19 an institutional mechanism for a bailout,

pandemic―having just begun, the court’s it was abundantly clear in the spring of

decision threatened the ECB’s ability to act 2020 that any Italian government would

as a lender of last resort to Italy. regard the prospect of utilizing the ESM

In any normal circumstances, this as unacceptable.

would have constituted a trial for the eu-

rozone. But again, the pandemic magni- No Hamiltonian Moment

fied the problem several times over. Until But in moving toward Macron’s starting

March 2020 Italy’s new borrowing had position that there must be some common

been to service old debt. But Italy has since eurozone debt, if only to strengthen na-

then also needed to borrow to finance its tional fiscal capacity, Merkel only exposed

stimulus program. Moreover, once the Ger- the predicaments that the EU as a polit-

man government quickly moved to scrap ical and legal entity now creates for the

the debt brake prescribing a balanced eurozone and, in turn, the eurozone as a

budget in order to pursue its own fiscal subset of EU member states poses for the

stimulus to combat the effects of the pan- EU. These problems begin with the rela-

demic, Italy faced being left behind in the tionship between debt and tax in the Re-

recovery stakes because its space for new covery Fund first proposed by the German Helen Thompson

is Professor of

borrowing was much smaller than that and French leaders and then agreed to in

Political Economy

enjoyed by many other eurozone states. slightly different form by the EU heads of at Cambridge

The part of the German recovery plan that government in July. University.

IP Special • 2 /2021 | 21Questions of Power

Since the Recovery Fund will allow representing the Hamiltonian moment,

the European Commission to borrow relying on member states pledging taxes

in the EU’s name and since some of the from their national tax-raising authority to

funds raised will then be distributed as service shared debt risks running into the

grants, some EU observers heralded the exact same problem that in its disastrous

move as a transformative moment for the consequences finally led to the Hamilton

eurozone, comparable to Alexander Ham- moment in the United States. It was be-

ilton’s first efforts to make the debts of the cause investors lost confidence in the debt

13 original American states the debt of the issued by the US Continental Congress―

federal American union. But Hamilton’s when the individual states were reluctant

move to create the federal assumption of to make the requisite fiscal transfers to the

individual state debt in 1790 required the treasury―that the American federal gov-

prior ratification of the American federal ernment acquired tax-raising powers. It

constitution in 1788, giving the American was because state governments’ struggles

to service state debt undermined federal

creditworthiness that Hamilton proposed

the federal government take responsibility

for all state debts.

However, the eurozone’s difficulties

Merkel gave the here go well beyond those that afflicted

the American republic. The early Amer-

ican republic was not a monetary union

non-eurozone and, consequently, did not have issues

around a single currency. That the EU is

member states

a multi-currency union in which a majority

of states nonetheless share a currency has

long been a particular burden for the EU.

an effective veto But the EU Recovery Fund turns it into a

direct problem for the eurozone, too.

In insisting that grants and loans from

the Recovery Fund be funnelled through

the Multiannual Financial Framework,

Merkel gave the non-eurozone member

states an effective veto over what is now

federal government the authority to im- the means by which Italy’s fiscal latitude

pose taxes. Nothing proposed by Merkel can be enhanced. Moreover, the very fact

and Macron or agreed at the EU summit in that the allocation structure decidedly

July approaches such a political change. benefits two non-euro members, Hungary

In the short term the EU is looking no fur- and Poland, under Article 7 proceedings,

ther than to place a new common tax on gives the governments keenest to disci-

plastic bags. pline these two eastern European states

Without much in the way of revenue (among them the non-euro members

constituting the EU’s own resources, the Sweden and Denmark) an opportunity to

common debt must rely on taxes com- demand more on rule of law compliance.

ing from the member states. Rather than This then increases the incentive for the

22 | IP Special • 2 /2021Pandemic Borrowing

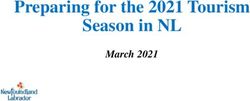

Angela Merkel’s rejection of new eurozone institutions of the kind Emmanuel Macron has advocated arises from an ingrained

political realism: the French president and the German chancellor face-to-face at the EU summit in Brussels in July 2020

Hungarian and Polish governments to use in practice required to maintain access to

their effective veto power. These dynamics the ECB’s asset purchase programs. Now

caused the drawn-out tangle between the demanding strong provisions on rule of

European Council and European Parlia- law conditionality that cannot be accepted

ment and veto threats by Budapest and by Hungary and Poland is an opportunity

Warsaw that risk delaying the Fund’s to recontest the July agreement, especially

planned start in January 2021. when there are genuine difficulties ahead

for some in procuring parliamentary rati-

Recontesting the Agreement fication for whatever Council-Parliament

This difficult process underlined the fact compromise eventually emerges.

that political consent to the Recovery Fund Yet Merkel’s rejection of new eurozone

from the governments of some eurozone institutions of the kind Macron has advo-

members has been weak from the start. cated arises from an ingrained political

To reach any agreement at all in July, the realism. The Commission will acquire

southern Europeans had to concede that the right under existing legal authority

individual eurozone member states could to borrow in the EU’s name to deal with

increase surveillance powers over their the COVID-19 pandemic and the recovery

budgets on top of those already formally from that emergency. Any eurozone fiscal

given to the European Commission and authority or a eurozone parliament would,

IP Special • 2 /2021 | 23Questions of Power

by contrast, require a new treaty. Treaty and no other non-eurozone member state

change is a long and arduous process, are was experiencing the same problem. On

there are no guarantees that all member the other hand, any significant change

states would agree to a ratification. to freedom of movement that could have

The fact that utilizing the Multiannual been contemplated would have required

Financial Framework can be accommodat- revisions to the EU treaties. That the EU-

ed within existing treaties does not, how- 27 could not move after Cameron formally

ever, ensure that national democratic pol- asked that they did, served to demonstrate

itics can be kept at bay. The very fact that to British voters that the Single Market is a

governments with a working parliamenta- protected constitutional order, unrespon-

ry majority should be able to push through sive to national democratic politics.

an EU agreement that in net terms will use

future taxes from some member states to Demarcations Breaking Down

repay debt acquired to finance expendi- Now similar dynamics generated around

ture in other member states is prompting the EU’s internal politics as a multi-curren-

some opposition parties to make an issue cy bloc with a single currency center are in

of democratic consent to the agreement. play. But this time the difficulties concern

This impulse appears to be most conse- more than one non-euro member. As after

quential in Finland, where activists from 2010, demarcations that kept issues from

the Finns Party have secured enough sig- spilling between the eurozone and the

natures in a citizens’ initiative to demand EU’s legal order are breaking down, and

a referendum, so that the process by which this is happening just as the demands―

ratification should proceed must now be tax-wise―that EU governments must ask

debated in the Finnish Parliament. of electorates as citizens of national states,

The cumulative political difficulties and not as citizens of the EU, is growing.

generated by the moves to strengthen the There have always been paths down

emergency fiscal capacity of the weaker which the EU can muddle through its ap-

eurozone states strike at the heart of the parently centrifugal contradictions. The

very issues that complicate the EU-euro- great advantage of confederations—if, with

zone relationship. After 2010 the United some crucial caveats, that is what the EU

Kingdom’s position inside the EU was is—is the issues they can leave unresolved

structurally weakened because the euro- because there is no sovereign that can im-

zone crisis politicized London’s position pose supposed remedies. But one of those

as the eurozone’s offshore financial center, caveats is the ECB’s authority, and the ECB

and then, when the British economy began cannot leave individual member states to

to recover as southern Europe remained their own devices where debt is concerned

mired in recession, the Single Market at the same time that its pandemic purchas-

turned the United Kingdom into an em- ing program is subject to a constitutional

ployer of last resort for a monetary union challenge in Germany. In Berlin, the point

to which it did not belong. of the Recovery Fund was to take the pres-

Once these dynamics were in play there sure off the ECB. But thus far it has only

was little former Prime Minister David ended up demonstrating just why the ECB

Cameron could do to minimize them. On is the only part of the EU equipped to deal

the one hand, eurozone matters had to with the predicaments sovereign debt cre-

have priority for eurozone member states ates for the eurozone.

24 | IP Special • 2 /2021You can also read