Q4 2019 QUARTERLY LETTER - JANUARY 2020 - Keebeck Wealth ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

KEEBECK QUARTERLY LETTER

Q4 2019

Q4 2019 QUARTERLY LETTER – JANUARY 2020

Are You Sure Hank Done it this Way?

Happy New Year,

I hope that 2019 treated you and your families well and that the

next year brings you much prosperity and peace.

Speaking of peace, my wife and I recently had a baby. After

much thought, we named him Caius Pax, meaning “man of

peace.” This name isn’t quite apropos just yet. In between early

dawn feedings and cleaning spit-up off my dress pants, I

managed to cobble together this quarterly letter. In this one we

have a little fun, touching on everything from Hank Williams and

Waylon Jennings to Mister Rogers.

Enjoy the read,

Mathew Klody, CIO

1

KEEBECK QUARTERLY LETTER

Q4 2019

Are You Sure Hank Done It This Way?

Lord it's the same old tune, fiddle and guitar

Where do we take it from here?

Rhinestone suits and new shiny cars

It's been the same way for years

We need a change

Somebody told me, when I came to Nashville

Son you finally got it made

Old Hank made it here, and we're all sure that you will

But I don't think Hank done it this way

No, I don't think Hank done it this way

Ten years on the road, makin' one-night stands

Speedin' my young life away

Tell me one more time just so's I'll understand

Are your sure Hank done it this way?

Did ol' Hank really do it this way?

Lord I've seen the world, with a five piece band

Looking at the back side of me

Singing my songs, and one of his now and then

But I don't think Hank done 'em this way

I don't think Hank done 'em this way.

Take it home

Waylon Jennings - Are You Sure Hank Done It This Way (1975) from Dreaming My Dreams

2

KEEBECK QUARTERLY LETTER

Q4 2019

In Are You Sure Hank Done It This Way, Jennings pays

homage to the influence and impact of country legend Hank

Williams Sr. on country music. He contrasts that to what had

evolved into a clown show of glitz and glamor characterizing

top-selling country artists in the 1970s. “Rhinestone suits" and

"new shiny cars" and a rigid dictum of “success” from the

Grand Ole Opry largely void of true country roots dominated

the scene at the time. The song came to mark one of the

launching points for the rebellion that came to revolutionize

country music known as Outlaw Country. Artists such as Willie

Nelson, Waylon Jennings, Merle Haggard and Hank Williams,

Jr. shed the formulaic Nashville sound, grew long hair, and

replaced rhinestone-studded suits with leather jackets. Fiercely

independent, the "outlaws" abandoned lush orchestrations and stripped the music to its country core.

Source: https://en.wikipedia.org/wiki/Outlaw_country

After enormous volatility in late 2018, markets went straight up in 2019, accelerating with the launch of “not

QE.” I couldn’t help but reflect upon those lyrics, because this has become the “same old tune….it’s been

the same way for years”, one that we have seen for over a decade. Policymakers respond to any

semblance of market volatility with enormous stimulus which rockets markets to even higher levels. It’s kind

of like using a full electric defibrillator shock for a random, minor heart palpitation. U.S. unemployment is at

3.5%, the lowest level I can find in my chart going back a half century. It’s overkill, as central bank policy

just looks to have evolved into raw greed or worse at this point. That’s growing increasingly dangerous in

the current political environment.

“Did old Hank really do it this way?” In any event, with the current market so dependent and behaving

this way, we ask the question: did the U.S. economy and market grow to be the most creative and

formidable in the world by endless streams of printing money? Or has this recent era become more or less

the same clown show analogy as the “rhinestone suits” and “new shiny cars” that the outlaws rebelled

against?

Further, looking back to historical examples of great investors, we ask the question: “did old Warren

(Buffett), George (Soros) or Julian (Robertson)” really do it this way?” Meaning, was there simply no

thought behind their tremendous investment success other than buying each minor dip because assets

always go up on based upon government QE?

To both questions… no, I don’t think they “done ‘em this way.”

3

KEEBECK QUARTERLY LETTER

Q4 2019

Well, “we need a change” or, more accurately, something must change as this is unsustainable. After

putting some scale behind the Fed’s recent moves driving markets higher, we take a look ahead to 2020

and beyond, outline some street views, some non-consensus views, and potential investment opportunities.

“Not QE” Propelling Markets Higher

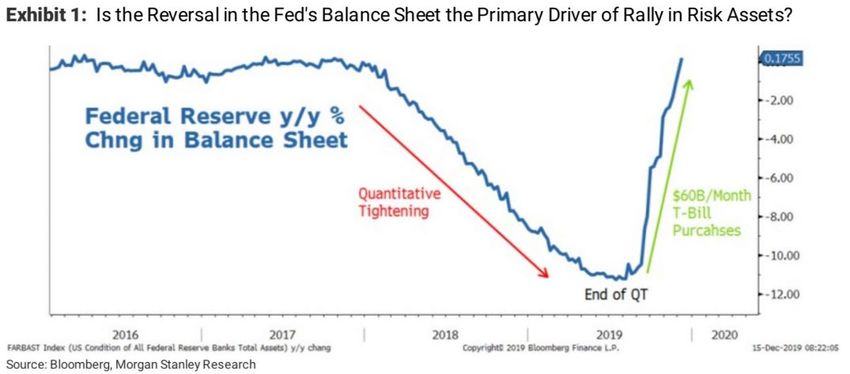

“This is not QE. In no sense is this QE. This is nothing like it all.” - Fed Chair Jerome Powell, October 2019

Let’s begin with the longer-term perspective by noting that from 2009-2015, the Fed’s balance sheet

expanded from roughly 5% to over 25% of GDP.

Federal Reserve Balance Sheet as a % of GDP (last 30 years)

As a starting point, the Fed’s recent easing came from a very accommodative level to begin with. However,

in response to disruptions in the repo market, they began to purchase an enormous sum of assets in a very

compressed time period. While the Federal Reserve was careful to go out of their way and explicitly state

this is “not QE”, the amount of “not QE” has been astounding. In the past few months, almost $400BN has

been printed, completely reversing the quantitative tightening done in 2019, and this is likely to continue

through at least the first few months of 2020.

4

KEEBECK QUARTERLY LETTER

Q4 2019

Federal Reserve Balance Sheet Y/Y change

NOT QE?

Federal Reserve Balance Sheet as a % of GDP (2019)

NOT QE?

Not QE + Emerging Signs of Inflation

Consensus opinion calls for inflation to remain muted. However, over the next few years, we see the

potential for emerging inflation to accelerate significantly. This trend could be particularly exacerbated

should the dollar begin to finally depreciate and energy prices begin to accelerate upward (See Energy

Section).

5

KEEBECK QUARTERLY LETTER

Q4 2019

As you can see, the core consumer price index is accelerating, and businesses anticipate the largest wage

increases in thirty years. The following charts all demonstrate that there has been a recent acceleration in

inflation.

Core “Official” CPI Accelerating

6

KEEBECK QUARTERLY LETTER

Q4 2019

Small Businesses Intent to Raise Wages at 30 Year Highs

Source: Paychex

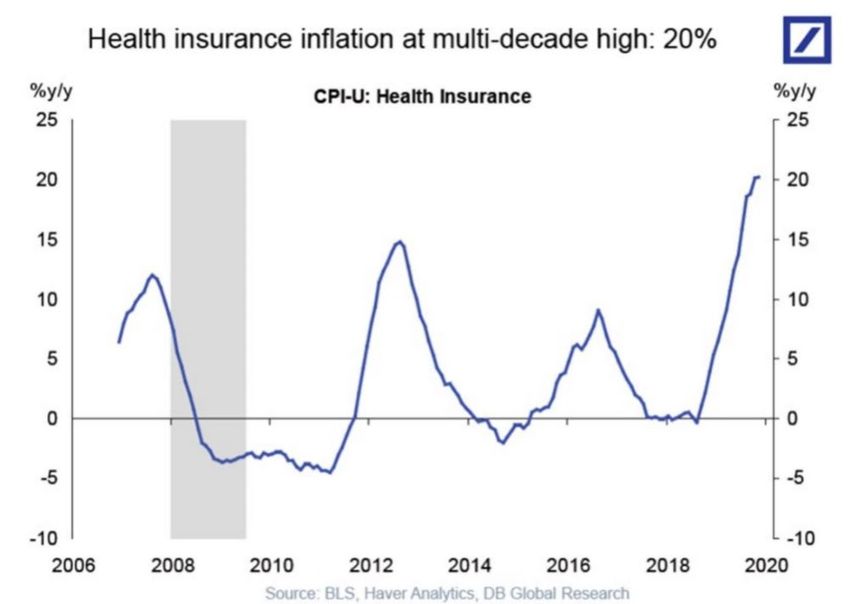

Major components of GDP, such as healthcare, are running at significant double-digit inflation.

7

KEEBECK QUARTERLY LETTER

Q4 2019

Healthcare Insurance Inflating at 20%

Core CPI Accelerating

Source: @RBAdvisor

Richard Bernstein of RBA Advisors recently wrote: “The core CPI is in its most pronounced uptrend in more

than 30 years and consensus is it’s good the Fed just eased three times…. Hmmm.” “Despite consensus

that inflation is dead and gone, monetary policy is clearly pro-inflation”

8

KEEBECK QUARTERLY LETTER

Q4 2019

What has kept a lid on inflation during the QE infinity era has been a very strong dollar coupled with weak

energy and other commodity prices. We are seeing reasons for both of these factors to reverse over the

next few years, not a market expectation, but potentially a seismic shift. We touch on energy below.

Reminder: The Long Run Trend is Currency Debasement

Opportunities in Energy

We upgraded energy to an overweight recommendation last quarter and wanted to elaborate on that theme.

At the time of writing this, consensus view is that energy, which has underperformed over the past decade,

is not an attractive investment. The charts below show the underperformance:

9

KEEBECK QUARTERLY LETTER

Q4 2019

S&P 500 vs. XLE (Energy ETF) – 10 Year History

From these charts alone, one would have assumed that oil has been displaced by alternatives. Yet, global

daily oil consumption is at the highest level in human history at over 101 million barrels per day. This has

grown steadily over time driven by global growth, particularly in developing markets.

World Oil Demand

10KEEBECK QUARTERLY LETTER

Q4 2019

Ironically, those who were calling for peak oil

during the mid-2000s can’t be found anywhere

these days. It has been our experience in

commodity cycles that they are eventually self-

correcting, as supply is curtailed when

producers (or more likely their capital

providers) dramatically reduce investment that

can no longer be justified at current low

commodity prices.

We believe signs are emerging that we are

nearing one of the bottoms of those cycles, as

the oil and gas patch has felt the pain and is

beginning to respond by cutting capital

expenditures. Source: Credit Suisse

World’s Growing Dependence on “Endless”, Cheap US Shale

Source: Bloomberg/Schwab

11KEEBECK QUARTERLY LETTER

Q4 2019

The bull case is that there is an endless, cheap supply of US shale oil and gas that can be turned on any

time prices move up. This has caused a massive collapse in spending on global exploration and

conventional discoveries.

Spending is Falling

“The last three years have been the worst stretch of time in seventy years for new conventional oil

discoveries.” Oilprice.com, October 2, 2019

12KEEBECK QUARTERLY LETTER

Q4 2019

But what if US shale isn’t infinite (at least at current prices?) What if US producers high-graded their

inventory when prices collapsed five years ago and are at the point where productivity growth is declining to

the point where the marginal cost is about to increase materially?

Not an everyday thesis, but one I came across this fall from Goehring and Rozencwajg, specialists in the

energy space. The recent letter detailing this can be found at:

http://gorozen.com/research/commentaries

13KEEBECK QUARTERLY LETTER

Q4 2019

Their research points to a compelling case that the market has it wrong when it comes to US shale

production. The best fruit (fields) was picked first and now productivity gains are diminishing while base

production is declining more quickly than anticipated.

They write in their third quarter letter: “Conventional wisdom held that productivity gains were the result of

operators drilling and completing larger and better wells (longer laterals, larger proppant loadings, and

greater fluid volumes). However, our research pointed us in an entirely different direction. We believe the

surge in drilling productivity over the last five years is largely the result of where operators drilled their

wells. In particular, we believe the improved drilling productivity was the result of a practice known as

“high-grading.” High-grading is an age-old practice used in both the oil and gas industry as well as the

mining industry which simply consists of selecting and drilling your most productive prospects first. Over the

last five years, the E&P industry has shifted significantly away from drilling their less productive Tier 2

acreage in favor of drilling their more productive Tier 1 acreage. Since drilling a Tier 1 well is nearly 100%

more productive than a Tier 2 well, the industry has created the illusion of ever-improving productivity

growth by narrowing their focus to only their best prospects. If our research is correct, then future

increases in shale drilling productivity will be more a function of continued “high-grading” and less a

function of ever-changing drilling and completion techniques.

“For the first eight months of 2019 shale production grew by 57,000 b/d per month on average. This

represented a slow-down of 60% compared with the eight months ending August 2018, during which

production grew by 132,000 b/d per month on average. Remarkably, this slowdown occurred even though

the industry completed 10% more wells during the first eight months of 2019 than in the same period last

year. In aggregate, production from all new wells actually accelerated between the two periods--from

571,000 b/d per month to 640,000 b/d per month due mainly to the higher number of wells completed.

However, drilling productivity, although still growing slightly, has now slowed dramatically. For the eight

months ending August 2018, a new well flowed 460 barrels of oil on average during its first full month of

production compared with 470 barrels this year—a rise of only 2% and a dramatic slowdown from the 10%

drilling productivity growth experienced in the first eight months of 2018 versus the first eight months of

2017.” “Also strongly contributing to the slowdown has been the dramatic increase in the underlying base

declines. For the eight-month period ending August 2018, production from existing wells declined by

440,000 b/d per month on average. By August 2019, this figure had accelerated to 590,000 b/d per month

– an increase of 150,000 b/d. The acceleration in the base decline overwhelmed all other factors and net

production growth ground to a halt.”

14KEEBECK QUARTERLY LETTER

Q4 2019

Then there is always this wildcard, “On my first day as president, I will sign an executive order that puts a

total moratorium on all new fossil fuel leases for drilling offshore and on public lands. And I will ban

fracking—everywhere.” - Elizabeth Warren, September 6, 2019.

On current depressed energy prices, the energy sector (as measured by the XLE) trades at just over 7x

forward ebitda compared to over 12x for the S&P 500 and 14x for the Nasdaq…. just sayin’…

International Opportunities

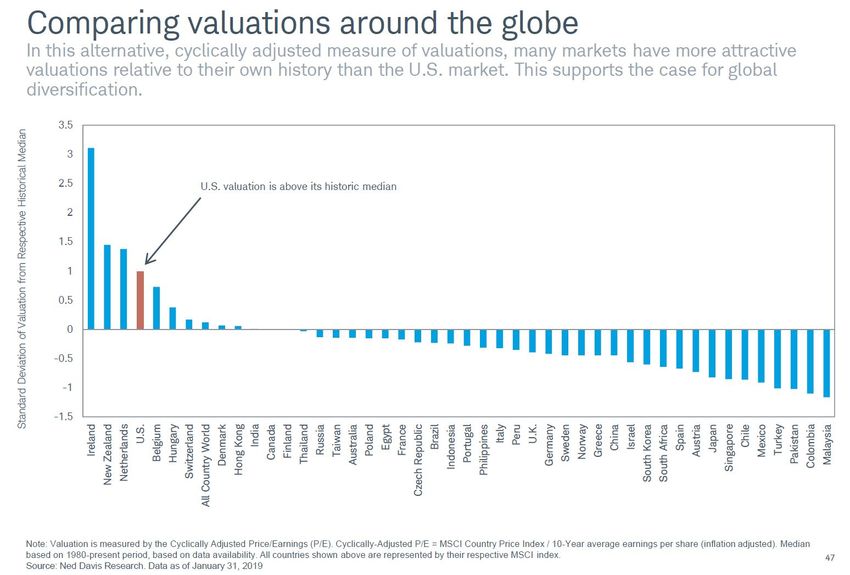

As shown in the following charts, the S&P 500 Total Return Index increased 252% vs. just 61% for the rest

of the world over the past decade. Looking ahead to the next decade, it is highly improbable that this level

of outperformance continues, particularly as the nature of the global economy continues to shift more to

international markets. This calls

for greater international

exposure. Most US investors

have international exposure far

below the international global

share of GDP. In the vein of

buying low and selling high,

shifting a portion of exposure

from the winner of the past

decade (US) to the loser makes a

great deal of sense to us,

particularly with the dollar so

strong at the moment.

Source: Bespoke

15KEEBECK QUARTERLY LETTER

Q4 2019

Source: Bespoke

16KEEBECK QUARTERLY LETTER

Q4 2019

Underweight Corporate Credit & Long Duration

We are consistently asked for high income ideas without a lot of risk. As the chart below shows, that largely

doesn’t exist in the current environment, at least not at the asset class level.

17KEEBECK QUARTERLY LETTER

Q4 2019

Global interest rates are artificially suppressed by central banks and that has reverberated across all asset

classes, including suppressing the rates earned on traditional fixed income.

18KEEBECK QUARTERLY LETTER

Q4 2019

In addition, it has spurred a credit boom (see our 3q19 letter on our website here) where excesses are

clearly building.

Generally speaking, we see the up/down skewed to the downside - particularly if higher inflation, a weaker

dollar, and higher energy prices come to pass.

Holiday Reminders from Mr. Rogers

Just over fifty years ago, an unknown Presbyterian minister named Fred Rogers began filming a children’s

program at WQED in Pittsburgh. Soon, Mister Rogers' Neighborhood was being broadcast nationally on the

predecessor to the Public Broadcasting Service. Fred went on to write, produce, and star in nine hundred

episodes over the next three decades shown across millions of homes. The show’s basic premise was a

simple one…to teach young children their inherent worth and how to be good people and good neighbors.

These very simple, basic nurturing concepts have timeless value, and recent films Won’t You Be My

Neighbor (2018) by Morgan Neville and just released A Beautiful Day in the Neighborhood starring Tom

Hanks, serve as an indicator of that value.

As we move into a new year, many of us make New Year’s resolutions on how we can improve ourselves,

be it physically, professionally, personally and spiritually. With 2020 being an election year, we will

unfortunately be reminded more than normal of the partisan divide in our country and how “un-neighborly”

our dialogue has become. I recently came across many quotes from Mister Rogers and wanted to share

those with you below to both remind myself and anyone else interested what is truly important in the long

run. At the end of the day, the whole civilization begins to break down if we aren’t decent, good neighbors

at the most basic level.

19KEEBECK QUARTERLY LETTER

Q4 2019

1. “All of us, at some time or other, need help. Whether we're giving or

receiving help, each one of us has something valuable to bring to this

world. That's one of the things that connects us as neighbors--in our

own way, each one of us is a giver and a receiver."

2. "Anyone who does anything to help a child in his life is a hero. "

3. "As human beings, our job in life is to help people realize how rare and

valuable each one of us really is, that each of us has something that no

one else has- or ever will have- something inside that is unique to all

time. It's our job to encourage each other to discover that uniqueness

and to provide ways of developing its expression."

4. "Discovering the truth about ourselves is a lifetime's work, but it's worth

the effort."

5. "Forgiveness is a strange thing. It can sometimes be easier to forgive our enemies than our friends.

It can be hardest of all to forgive people we love. Like all of life's important coping skills, the ability to

forgive and the capacity to let go of resentments most likely take root very early in our lives."

6. "How many times have you noticed that it's the little quiet moments in the midst of life that seem to

give the rest extra-special meaning?"

7. "I don't think anyone can grow unless he's loved exactly as he is now, appreciated for what he is

rather than what he will be."

8. "I hope you're proud of yourself for the times you've said "yes," when all it meant was extra work for

you and was seemingly helpful only to someone else."

9. "If you could only sense how important you are to the lives of those you meet; how important you

can be to the people you may never even dream of. There is something of yourself that you leave at

every meeting with another person."

10. "In times of stress, the best thing we can do for each other is to listen with our ears and our hearts

and to be assured that our questions are just as important as our answers."

11. "It's not the honors and the prizes and the fancy outsides of life which ultimately nourish our souls.

It's the knowing that we can be trusted, that we never have to fear the truth, that the bedrock of our

very being is good stuff."

12. "It's really easy to fall into the trap of believing that what we do is more important than what we are.

Of course, it's the opposite that's true: What we are ultimately determines what we do!"

20KEEBECK QUARTERLY LETTER

Q4 2019

13. "Knowing that we can be loved exactly as we are gives us all the best opportunity for growing into

the healthiest of people."

14. "Listening is where love begins: listening to ourselves and then to our neighbors."

15. "Little by little we human beings are confronted with situations that give us more and more clues that

we are not perfect. "

16. "Love and success, always in that order. It's that simple AND that difficult."

17. "Love is like infinity: You can't have more or less infinity, and you can't compare two things to see if

they're 'equally infinite.' Infinity just is, and that's the way I think love is, too."

18. "Love isn't a state of perfect caring. It is an active noun like struggle. To love someone is to strive to

accept that person exactly the way he or she is, right here and now."

19. "Mutual caring relationships require kindness and patience, tolerance, optimism, joy in the other's

achievements, confidence in oneself, and the ability to give without undue thought of gain."

20. "Often out of periods of losing come the greatest strivings toward a new winning streak."

21. "Often when you think you're at the end of something, you're at the beginning of something else."

22. "Our society is much more interested in information than wonder, in noise rather than silence...And I

feel that we need a lot more wonder and a lot more silence in our lives"

23. "Real strength has to do with helping others."

24. "Some days, doing 'the best we can' may still fall short of what we would like to be able to do, but life

isn't perfect on any front-and doing what we can with what we have is the most we should expect of

ourselves or anyone else."

25. "There's a world of difference between insisting on someone's doing something and establishing an

atmosphere in which that person can grow into wanting to do it."

26. "The connections we make in the course of a life--maybe that's what heaven is."

27. "The greatest gift you ever give is your honest self."

28. "The kingdom of God is for the broken hearted"

29. "The media shows the tiniest percentage of what people do. There are millions and millions of

people doing wonderful things all over the world, and they're generally not the ones being touted in

the news."

30. "The only thing evil can't stand is forgiveness."

21KEEBECK QUARTERLY LETTER

Q4 2019

31. "The thing I remember best about successful people I've met all through the years is their obvious

delight in what they're doing, and it seems to have very little to do with worldly success. They just

love what they're doing, and they love it in front of others."

32. "The world needs a sense of worth, and it will achieve it only by its people feeling that they are

worthwhile." "Try your best to make goodness attractive. That's one of the toughest assignments

you'll ever be given."

33. "There are three ways to ultimate success: The first way is to be kind. The second way is to be kind.

The third way is to be kind."

34. "There are times when explanations, no matter how reasonable, just don't seem to help."

35. "There is no normal life that is free of pain. It's the very wrestling with our problems that can be the

impetus for our growth."

36. "There's a part of all of us that longs to know that even what's weakest about us is still redeemable

and can ultimately count for something good."

37. "We all have different gifts, so we all have different ways of saying to the world who we are."

38. "We get so wrapped up in numbers in our society. The most important thing is that we are able to be

one-to-one, you and I with each other at the moment. If we can be present to the moment with the

person that we happen to be with, that's what's important."

39. "We speak with more than our mouths. We listen with more than our ears."

40. "Whatever we choose to imagine can be as private as we want it to be. Nobody knows what you're

thinking or feeling unless you share it."

41. "Who you are inside is what helps you make and do everything in life."

42. "You can think about things and make believe. All you have to do is think and they'll grow."

43. "You can't really love someone else unless you really love yourself first."

44. "You rarely have time for everything you want in this life, so you need to make choices. And

hopefully your choices can come from a deep sense of who you are."

Source: https://www.inc.com/geoffrey-james/45-quotes-from-mr-rogers-that-we-all-need-today.html

22KEEBECK QUARTERLY LETTER

Q4 2019

Keebeck Viewpoints

• Overweight international and emerging markets and non-dollar securities

• Underweight corporate debt and heavily leveraged securities

• Underweight private equity

• Overweight value vs growth

• Overweight short duration vs long duration

• Overweight domestic housing

• Overweight energy

Conclusion

In conclusion, 2019 was a very strong comeback to the weak performance seen in the second half of 2018.

Going forward, the outlook grows more complex and potentially more volatile. We continue to favor areas

which, in our opinion, demonstrate greater fundamental value and a more favorable risk/reward over the

long-term.

Sincerely,

Mathew T. Klody, CFA

Chief Investment Officer

Keebeck Wealth Management, LLC

mklody@keebeck.com

* As this newsletter is for informational purposes, the strategies and opinions included herein may not be reflected in

the management of your specific investment account(s). We manage accounts on an individualized basis, taking into

consideration each client’s unique financial situation. If you have any questions regarding your investment accounts or

our specific investment strategies, please contact us.

23KEEBECK QUARTERLY LETTER

Q4 2019

Biography

Mathew T. Klody, CFA is the Chief Investment Officer at Keebeck Wealth

Management, LLC.

Mathew is also an adjunct professor of finance at the University of Notre Dame.

Prior to joining Keebeck, Mathew was the Founder, Managing Partner and Portfolio

Manager of MCN Capital Management, LLC, the advisor to a private long short

investment partnership.

Mathew was the Senior Vice President and Analyst at Chicago-based Sheffield

Asset Management, a long/short equity hedge fund from 2007-2012. From 2003-2007, Mathew was an

Investment Analyst at the holding company of Alleghany Corporation (ticker "Y") covering the equity

portfolio, corporate development and the reinsurance portfolio. Mr. Klody began his career as a credit

analyst at the Global Corporate and Investment Bank at Bank of America.

Mathew has been selected to speak at a number of industry events, including the Spring 2017 Grant’s

Interest Rate Observer conference, Invest for Kids - Chicago (Fall of 2017), and the MOI Global - Best Ideas

Conference (2018). He has served as a guest lecturer to the Notre Dame Institute for Global Investing, the

Behavioral Finance and Applied Investment Management programs at the Mendoza College of Business. He

serves as a member of the Parish Council at St. Joan of Arc Church in Lisle, IL.

Mathew graduated summa cum laude from the University of Notre Dame with a degree in finance and

business economics. Mr. Klody is a Chartered Financial Analyst.

DISCLOSURES

Content should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors

on the date of publication and are subject to change. Content should not be viewed as personalized investment advice or as an offer to buy or

sell, or a solicitation of any offer to buy or sell the securities mentioned herein.

Past performance may not be indicative of future investment results. Different types of investments involve varying degrees of risk, and there

can be no assurance that any specific investment or strategy will be suitable or profitable for your investment portfolio. All investment

strategies have the potential for profit or loss.

Charts and graphs do not represent the performance of our firm or any of our advisory clients. All information is based on sources deemed

reliable, but no warranty or guarantee is made as to its accuracy or completeness. Projections and estimates are based on assumptions that

may not come to pass. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the

performance of your portfolio.

24You can also read