RETAIL CREDIT OUTLOOK - Anticipating and preparing for the COVID-19 impact on retail credit market - TransUnion CIBIL

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RETAIL CREDIT OUTLOOK

Anticipating and preparing for the

COVID-19 impact on retail credit market

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 1

Key questions that the market is asking, and what we hope to

cover in this presentation

How might the operating

1 Key implications for lenders

environment change for lenders?

What can be the potential impact Future Readiness

2

on retail credit growth?

Lending Strategy

What may be the likely impact on

3 Risk Management

asset quality?

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 2

Operating Environment

How COVID-19 and ensuing containment and relief measures might change

the lending ecosystem?

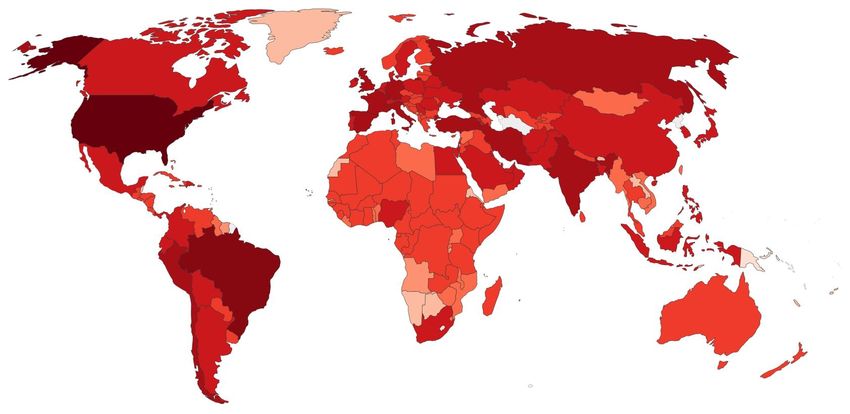

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 3COVID-19 has affected more than 6 million people across 210

countries around the world

COVID-19 Confirmed Cases

As on 2nd June 2020

Source: Our World in Data

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 4Spread of COVID-19 in India has been relatively slower

compared to other major countries affected by the pandemic

Number of Confirmed COVID-19 cases

1,000,000 USA

# Confirmed Cases

Brazil

Russia

UK

(Log scale)

India Spain

100,000

10,000

1,000

1 11 21 31 41 51 61 71 81

Days since the 1000th confirmed case

As on 2nd June 2020

Source: Our World in Data

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 5The phased lockdown implemented to curb the spread of

COVID-19 has social, financial and economic implications

• Loss of job for daily wage earners and migrant workers

Social • Migration of labor leaving them struggling to make ends meet

• Anxiety as a result of social distancing, uncertainty, fear of economic recession

• Impact on consumers’ financial position on account of pay cuts / layoffs

• Revenue reduction for companies leading to potential liquidity challenges for

Financial businesses and solvency crises

• Falling stock prices and widening of credit spreads

• Hit on consumption demand – Decrease in consumption, reduction in

discretionary spending, postponement of new investments

Economic

• Impact on supply side – Decrease in labor supply, curtailment of production, hit

on distribution of goods and services

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 6Labor market conditions have been impacted severely

Labor Participation and Unemployment

Labor Participation Rate Unemployment Rate

50%

40% 42.8% 43.0%

Percentage

42.3% 42.6%

38.2%

30%

23.5%

20%

7.0% 8.2% 7.2% 7.8%

10%

0%

May-19

May-20

Jun-19

Jan-20

Aug-19

Sep-19

Nov-19

Dec-19

Apr-20

Mar-20

Jul-19

Oct-19

Feb-20

Source: CMIE

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 7Consumer sentiment has taken a hit as a result of worsening

economic conditions

Consumer Sentiment Index

120

100 108.3 105.7 105.9 105.3

Index Value

80

60

40

20 30.9

0

May-19

May-20

Jun-19

Jan-20

Apr-20

Aug-19

Sep-19

Nov-19

Dec-19

Mar-20

Oct-19

Jul-19

Feb-20

Source: CMIE

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 8The pandemic has brought nearly all activity to a standstill,

with the effect more pronounced in the services sector

Purchasing Managers’ Index (PMI)

Manufacturing PMI Services PMI

70

57.5

60 52.7 52.4 52.7

Index Value

50 54.5

50.2 51.4 51.2

40 30.8

30

20

10

12.6

0

May-20

May-19

Nov-19

Feb-20

Jun-19

Aug-19

Jan-20

Apr-20

Sep-19

Dec-19

Mar-20

Oct-19

Jul-19

Source: CMIE

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 9Revenue of most businesses has seen a drop and may fall

further in the short term

GST Collections

1,200

1,000

800

INR Bn

600

400

200

0

May-19

Jan-20

Apr-19

Jun-19

Aug-19

Sep-19

Nov-19

Dec-19

Mar-19

Mar-20

Oct-19

Jul-19

Feb-20

Source: Government of India

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 10Consequently, India’s economic growth is expected to contract

in 2020

Growth in Real GDP

GDP Actual GDP Forecast (pre COVID-19) GDP Forecast (post COVID-19)

12%

8.7%

YoY Growth Rate

7.5% 6.2%

8% 5.6%

4.1%

4% 1.1%

~INR 24

0% trillion

(current

-4% prices)

-8%

-12%

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2016 2017 2017 2017 2017 2018 2018 2018 2018 2019 2019 2019 2019 2020 2020 2020 2020

India’s GDP estimates have been revised for FY18, FY19 and FY20

Source: Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 11The Indian government has announced an economic relief

package of INR 20 trillion under “Atmanirbhar Bharat Abhiyan”

Liquidity Infrastructure Helping Stressed

Reforms Infra

Infusion Push Businesses

• New definition of • Reduction in CRR • Affordable rental • Relaxation in

MSMEs • Collateral free loans / housing for migrants insolvency law

• Agri marketing reforms subordinate debt / • Extension of middle • Expediting tax

• Coal, minerals equity for MSMEs income housing refunds

liberalization • Special liquidity and scheme • Funds for stressed

• Higher FDI in defense partial guarantee for • Agri infrastructure NBFCs

production NBFCs fund • Moratorium on loan

• Airport, DISCOM • Funds for DISCOM • Higher VGF for social repayments

privatization • EPF support infrastructure

• New policy for PSUs • INR 2.3 trillion extra

credit to farmers

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 12India's economic relief package, intended to help spur near

term growth and spending, is amongst the largest in the world

Economic Relief Packages by G20 Countries

25%

20%

15%

% of GDP

10%

5%

0%

Australia

Brazil

Korea

Germany

India

Italy

Argentina

US

Canada

UK

France

Turkey

Japan

Indonesia

China

Mexico

South

Russia

Arabia

Africa

South

Saudi

Source: IFC, CSIS, VOX

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 13The pandemic has created operational challenges for lenders

to re-consider and potentially change their operating model

• Realigning branches and loan centres to support social distancing guidelines

• Adjusting working hours, staffing mix and times to avoid contamination

Distribution

• Encouraging customers to use digital channels

• Automating routine service requests (chatbots, etc.)

• Providing temporary relief to customers without impact on credit history

Customer • Creating customer awareness on support and relief measures

Management • Addressing evolving needs of customers

• Segmenting customers based on their credit behavior

• Automating regular tasks and processes

Internal • Rebalancing workload across operational sites

Operations • Enabling online sanction and disbursement of loans

• Reviewing financial health and BCP plans of third-party service providers

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 14To summarize:

• The lockdowns implemented to curb the spread of COVID-19, and the virus itself, would have

far reaching implications on Indian economy

• Consumers’ financial positions are likely to change dramatically and many companies may

see a reduction in revenue

• Drop in consumer sentiment, significant hit on consumption demand and spending will have a

bearing on the future trajectory of the retail credit market

• Lenders will need to innovate and redesign their operating model to transact with confidence

and better support consumers during these unprecedented times

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 15Credit Growth

What can be the potential impact on demand for major products and the

ability and willingness of lenders to extend credit?

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 16Retail credit growth, which is a reflection of wider economic

activity, has contracted in the last two years

Growth in Retail Credit Balances and Real GDP

Retail Credit GDP

Balances Growth Rate

40% 12%

YoY GDP Growth Rate

YoY Retail Credit

30% 9%

20% 6%

10% 3%

0% 0%

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2015 2015 2016 2016 2017 2017 2018 2018 2019 2019 2020

Q1 2020 retail credit growth number is as of February 2020

Products considered: home loan, LAP, auto loan, two-wheeler loan, commercial

vehicle loan, construction equipment loan, personal loan, credit card, business loan,

Source: TransUnion CIBIL consumer database,

consumer durable loan, education loan and gold loan

Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 17Lending activity has been impacted severely, with some

revival seen in May

Inquiry and Origination Volumes

Inquiry Originations

250

Indexed Volumes

200

150

100

50

0

May-19

May-18

Jun-18

Jan-19

Jun-19

Nov-19

Jan-20

May-20

Apr-18

Apr-19

Apr-20

Jul-18

Aug-18

Sep-18

Nov-18

Dec-18

Oct-18

Jul-19

Aug-19

Sep-19

Dec-19

Feb-19

Mar-19

Oct-19

Feb-20

Mar-20

Index: April-18 = 100

Products considered: home loan, LAP, auto loan, two-wheeler loan, commercial

vehicle loan, construction equipment loan, personal loan, credit card, business loan,

consumer durable loan, education loan and gold loan

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 18Credit growth is a function of demand and supply factors

Analyzed data pertaining

to previous crisis

Demand for Credit Relationship between macro-

economic variables and

(Inquiries) inquiries for key products

Credit Growth

Ability to Lend

Money Supply in the economy

(Liquidity)

Supply of Credit

(Originations)

Willingness to Lend

Changes in approval rates

(Risk aversion)

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 19The previous crisis represents an economic downturn scenario

that may help guide our direction during the current crisis

Growth in Real GDP

14%

12%

YoY Growth Rate

10%

8%

6%

4%

2%

0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010

Source: Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 20Inquiry and origination volumes declined by almost 50% YoY

during the crisis period

Growth in Inquiry and Origination Volumes

Inquiry Originations

200

Indexed Volumes

150

100

50

0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2007 2007 2008 2008 2009 2009 2010 2010 2011 2011 2012 2012

Index: Q1 2007 = 100

Products considered: home loan, LAP, auto loan, personal loan and credit card

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 21Demand for housing is closely associated with wealth creation

through the equity market

Growth in Home Loan (HL) Inquiries and Share Price Index

HL Inquiries Share Price Index

120%

Correlation = 0.89

YoY Growth Rate

90%

60%

30%

0%

-30%

-60%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010

Share price index is the average value of BSE SENSEX

Source: TransUnion CIBIL consumer database,

Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 22There is a linkage between overall industrial activity and

demand for loans against property (LAP)

Growth in LAP Inquiries and Index of Industrial Production (IIP)

LAP Inquiries IIP

100% 25%

IIP YoY Growth Rate

YoY Growth Rate

80% Correlation = 0.75 20%

LAP Inquiries

60% 15%

40% 10%

20% 5%

0% 0%

-20% -5%

-40% -10%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010

The index of industrial production measures the output of the industrial sector of the

economy, which includes manufacturing, utilities, mining and quarrying Source: TransUnion CIBIL consumer database,

Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 23Private consumption and demand for auto loans move together

Growth in Auto Loan (AL) Inquiries and Private Consumption (PC)

AL Inquiries Private Consumption

250% 12%

PC YoY Growth Rate

YoY Growth Rate

200% Correlation = 0.78

10%

AL Inquiries

150%

8%

100%

6%

50%

0% 4%

-50% 2%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010

Private Consumption is the value of goods and services consumed by households

and non-profit institutions serving households expressed in local currency Source: TransUnion CIBIL consumer database,

Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 24Household financial liabilities and demand for personal loans

are closely associated

Growth in Personal Loan (PL) Inquiries and

Household Financial Liabilities (HFL)

PL Inquiries Household financial libilities

500% 30%

HFL YoY Growth Rate

YoY Growth Rate

400% Correlation = 0.97

25%

PL Inquiries

300%

200%

20%

100%

0% 15%

-100%

-200% 10%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010

Household financial liabilities is defined as the combined liabilities of all people

in a household. It includes loans and borrowings from banks, housing finance

companies (HFCs) and nonbanking financial corporations (NBFCs). Source: TransUnion CIBIL consumer database,

Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 25Demand for credit cards, being a lifestyle payment product, is

connected with household wealth

Growth in Credit Card (CC) Inquiries and Gross Household Wealth (GHW)

CC Inquiries Gross Household wealth

200% 20%

GHW YoY Growth Rate

YoY Growth Rate

Correlation = 0.87

150%

CC Inquiries

18%

100%

50% 16%

0%

14%

-50%

-100% 12%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010

Gross household wealth represents the total value of assets (financial

as well as non-financial) minus the total value of outstanding liabilities

of households (including non-profit institutions serving households) Source: TransUnion CIBIL consumer database,

Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 26The ability of financial institutions to lend can be determined

by money supply (M2) in the economy

Growth in Origination Balances and Money Supply (M2)

Origination Balances Money Supply (M2)

120% 25%

Money Supply (M2)

Origination Balances

YoY Growth Rate

100%

YoY Growth Rate

20%

80%

60% 15%

40%

20% 10%

0%

5%

-20% Correlation = 0.70

-40% 0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010

Products considered: home loan, LAP, auto loan, personal loan and credit card

Money supply (M2) includes cash in circulation, current account deposits as well as all

Source: TransUnion CIBIL consumer database,

time-related deposits, savings deposits, and non-institutional money-market funds

Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 27Approval rates declined for all key products during the crisis

period indicating increased risk aversion

Approval Rates during Crisis Period

60%

-22%

2007 Q2 to

Approval Rate %

-16% 2008 Q1

40% -11%

-30% 2008 Q2 to

-28% 2009 Q1

20%

2009 Q2 to

2010 Q1

0%

Home Loan LAP Auto Loan Personal Loan Credit Card

Products

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 28Secured lending products are expected to see more pronounced

decline in demand

Macro YoY 2020 Outlook for

Product Key Dynamics

Variable Forecast Demand

[Oxford Economics]

• Reduction in affordability

Home Share Price

-11.0% • Postponement of home purchases

Loans Index

Low High • Drop in home prices / attractive offers by builders

• Lower manufacturing / services output

LAP IIP -2.9% • Drop in real estate prices

Low High • Need of finance to revive business

• Reduction in discretionary spending

Private

Auto Loans -1.7% • Impact on travel and tour business

Consumption

Low High • Diminished ability and need to travel

• Need of funds to bridge personal finance gap

Personal Household

+15.1% • Flexible product structure

Loans Liabilities

Low High • Greater access via digital channels

• Increase in the need for digital payments

Credit Household

+9.6% • Reduction in discretionary spending

Cards Wealth

Low High • Postponement of lifestyle purchases

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 29Liquidity may not be a challenge consequent to rate cuts and

other fiscal measures initiated by the regulator

Money Supply (M2)

25%

YoY Growth Rate

20%

15%

10%

5%

0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2018 2018 2018 2018 2019 2019 2019 2019 2020 2020 2020 2020

Source: Oxford Economics

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 30Lenders are likely to tighten their credit policy and customer

selection norms to manage and mitigate risk

Product Willingness Key Dynamics

• Backed by security, lower default probability

Home Loans

• Lower interest rates, reduced margins

Low High

• Higher risk of default in smaller businesses

LAP

• Irregular cash flows may present assessment challenges

Low High

• Avoiding exposure to tour / travel segment

Auto Loans

• Challenges in repossession and resale of vehicles

Low High

• Unsecured in nature, increased risk of default

Personal Loans • Key product offering for many lenders especially FinTechs

Low High • Higher margins, increased profitability

• Revolving credit line which can be periodically managed

Credit Cards • Spending and behavior can be monitored

Low High • Leveraging CASA / internal database for acquisition

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 31To summarize:

• Demand for products like credit cards and personal loans will remain moderate as consumers

look to secure funds to bridge any personal finance gap

• Decline in discretionary spends and reduced affordability will impact demand for asset finance

products

• Given the inherent risk of products like LAP and personal loans, we anticipate a greater

decline in approval rates for these products

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 32Asset Quality

What may be the likely impact on stress levels for major products?

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 33Portfolio delinquency rates have remained largely steady in

the last three years, with the exception of LAP

Balance-level 90+ Delinquency Rate by Product

5%

% Balance in 90+ DPD

LAP

4%

Auto Loan

3%

Home Loans

2%

Credit Card

1%

Personal Loan

0%

Jun-17

Jun-18

Jun-19

Sep-17

Sep-18

Sep-19

Mar-17

Dec-17

Mar-18

Dec-18

Mar-19

Dec-19

Feb-20

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 34Impact on asset quality can be determined by analyzing

consumer scores, collection roll rates and payment hierarchy

Asset Quality

Consumer Risk Collection Roll Payment

Scores Rates Hierarchy

Shifts in borrower risk tiers Number of accounts The order in which

across product portfolios and becoming newly delinquent consumers prioritize

delinquency rates associated and flowing into subsequent payments during times of

with each tier delinquency buckets financial hardship

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 35We looked at 6-month risk tier movement for non delinquent

consumers and their delinquency rates thereof

90+ Balance DPD rate

Risk Tier (t+6)

(t+6)

Product-level Above Above

Subprime Subprime

Balance Subprime Subprime

No

Subprime Upgrade High Risk Low Risk

Risk Tier

upgrade

(t = 0)

Above No Very High Very Low

Downgrade

Subprime downgrade Risk Risk

Risk tier movements and DPD

rates can be simulated to

Subprime segment constitute a CV score of =681 delinquency rates

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 36Share of portfolio in very high risk segment has increased for

credit cards and personal loans in the last one year

Share of Portfolio in Very High Risk Segment

8%

Auto Loan

% of Balance

Credit Card

6%

Personal Loan

4% LAP

Home Loans

2%

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2016 2016 2016 2017 2017 2017 2017 2018 2018 2018 2018 2019 2019

Very High Risk segment refers to those consumers who have moved

from above subprime segment to subprime segment in next 6 months

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 37During the same time period, share of portfolio in low risk

segment has decreased for credit cards

Share of Portfolio in Low Risk Segment

5%

Auto Loan

% of Balance

4% Personal Loan

LAP

3%

Credit Card

2%

Home Loans

1%

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2016 2016 2016 2017 2017 2017 2017 2018 2018 2018 2018 2019 2019

Low Risk segment refers to those consumers who have moved from

subprime segment to above subprime segment in next 6 months

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 38Delinquency rate in very high risk segment has moved up for

home loans and LAP in the last one year

Delinquency Rate for Very High Risk Segment

16%

% Balance in 90+ DPD

Credit Card

12% LAP

Personal Loan

8%

Home Loans

4%

Auto Loan

0%

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2016 2016 2016 2017 2017 2017 2017 2018 2018 2018 2018 2019 2019

Very High Risk segment refers to those consumers who have moved

from above subprime segment to subprime segment in next 6 months

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 39Analyzing bucket net flow rates and lagged flow to 90+ would

also help gauge the impact on 90+ delinquency rate

[Illustration]

Outstanding Balance (value) Net Flow Rates

Bucket

T T+1 T+2 T+3 T+4 T+1 T+2 T+3 T+4

3

Current 100.0 102.0 105.0 107.0 110.0

Bucket net

1-29 4.0 5.0 5.0 6.0 6.0 5% 5% 6% 6%

flow rates

30-59 2.0 3.0 3.0 4.0 5.0 75% 60% 80% 83% can be

60-89 1.6 1.8 2.2 2.5 3.0 90% 74% 83% 75% simulated to

get lagged

90+ 1.3 1.5 1.8 2.1 2.4 94% 100% 95% 96%

flow to 90+

Total 108.9 113.3 117.0 121.6 126.4 Lagged flow to 90+ is the

2 product of diagonal bucket

90+ DPD 1.90% net flow rates 2.40%

Balance in next delinquency bucket 4

(eg: 30-59) on time T+1

Bucket net Impact on DPD can

1

flow rate =

Balance in previous delinquency be calculated basis

bucket (eg: 1-29) on time T lagged flow to 90+

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 40Delinquency rate and lagged flow to 90+ move in same direction

which enables us to use one to predict the other

Home Loan and Personal Loan Delinquency and Lagged Flow Rate

2.5%

HL lagged flow

2.0%

Rate (%)

1.5% HL 90+ delq

1.0% PL lagged flow

0.5% PL 90+ delq

0.0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2017 2017 2017 2017 2018 2018 2018 2018 2019 2019 2019 2019

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 41Lagged flow to 90+ has deteriorated for LAP and credit cards

in the last one year

Lagged Flow to 90+ DPD

6%

LAP

5%

Auto Loan

Percentage

4%

3% Credit Card

2% Home Loans

1% Personal Loan

0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2017 2017 2017 2017 2018 2018 2018 2018 2019 2019 2019 2019

Source: TransUnion CIBIL consumer database

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 42We studied payment hierarchy for two separate product

combinations, which represent different consumer groups

Study 1 Study 2

Home Significantly Consumer

loan different durable loan

populations

Auto Credit Personal Credit

card loan card

• More affluent • Lower income

• Higher income • Higher risk

• Lower risk

• Tighter lending criteria

Source: 2019 TransUnion CIBIL Payment Hierarchy Study

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 43The study on payment hierarchy revealed that home loans

generally have the highest payment priority

Account-level 90+ Delinquency Rate

% Accounts in 90+ DPD

1.0%

0.8% Credit Cards

0.6%

Auto Loans

0.4%

0.2% Home Loans

0.0%

Jan-14

May-14

Jan-15

May-15

Jan-16

May-16

Jan-17

May-17

Mar-14

Sep-14

Mar-15

Mar-16

Sep-16

Mar-17

Sep-17

Nov-14

Jul-15

Sep-15

Nov-15

Nov-16

Jul-14

Jul-16

Jul-17

Study Cohorts

Study cohort is the month for which the sample of consumers holding the

above products was picked (~300K per cohort)

Source: 2019 TransUnion CIBIL Payment Hierarchy Study

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 44Amongst unsecured lending products, personal loans generally

have the highest payment priority

Account-level 90+ Delinquency Rate

2.0%

% Accounts in 90+ DPD

Credit

Cards

1.5%

Consumer

1.0% Durable

Loans

0.5% Personal

Loans

0.0%

Jun-14

Aug-14

Jun-15

Jun-17

Apr-15

Apr-16

Jun-16

Apr-17

Aug-15

Aug-16

Aug-17

Dec-14

Dec-15

Dec-16

Dec-17

Oct-14

Feb-15

Oct-15

Feb-16

Oct-16

Feb-17

Oct-17

Feb-18

Study Cohorts

Study cohort is the month for which the sample of consumers holding the

above products was picked (~300K per cohort)

Source: 2019 TransUnion CIBIL Payment Hierarchy Study

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 45We simulated these risk related factors to determine the likely

impact on asset quality

Historic Base Worst

Risk Factors

Ranges case Case

Increase in share of portfolio moving from above

0.5% - 0.8% +1% +2%

subprime to subprime (Very High Risk Segment)

Increase in delinquency rate of Very High Risk

1.04X - 1.07X 1.1X 1.2X

Segment

Increase in share of subprime portfolio remaining in

0.3% - 0.6% +1% +2%

same risk tier (High Risk segment)

Increase in delinquency rate of High Risk Segment 1.03X - 1.06X 1.1X 1.2X

Deterioration in net flow rates for all delinquency

4% - 7% 10% 20%

buckets

Above simulations carried out individually for home loan, LAP, auto loan, personal loan and credit card

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 46Asset quality for unsecured products is likely to be impacted

more severely than asset backed products

Product Impact Key Dynamics

• Adverse impact on consumers financial situation

Home Loans • Possibility of non-payment for under-construction home loans

Low High • Highest payment priority

• Shutdown of businesses / Slowdown of orders

LAP • Irregular cash flows / poor churning

Low High • Emergency credit line / sub-ordinate debt to small businesses

• Slowdown of cab services and car rental businesses

Auto Loans

• Migration of drivers to their hometown

Low High

• Job losses / Lay-offs / Pay-cuts

Personal Loans • Recent acquisition by NBFCs / FinTechs from high risk customers

Low High • Increase in loan stacking behavior

• Job losses / Lay-offs / Pay-cuts

Credit Cards • Least payment priority

Low High • Alternate and convenient payment option

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 47The impact on individual lender’s portfolio will also depend on

the risk management practices adopted by that lender

Origination growth

Slower pace of growth may lead to

increase in delinquency levels –

“denominator effect”

Collection practices Profile of existing consumers

Collection prioritization models and Acquisition of high risk consumers

cohesive treatment strategies in past, age profile, income, etc.

Asset Quality

Portfolio monitoring Current portfolio mix

Use of behavior scorecards and Open market acquisitions, sourcing

early warning systems from DSA, collateral coverage

Credit models

Use of risk models and data

analytics in credit underwriting

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 48To summarize:

• Ascertaining the impact of COVID-19 on asset quality is a complex picture dependent on

number of interlocking factors like consumer credit scores, collection roll rates and payment

hierarchy

• A wider analysis of these factors predicts that asset quality will likely be impacted most for

personal loans and credit cards with home loans and auto loans experiencing less of a shift

• In these difficult times, lenders need to actively monitor their portfolio and implement analytics

driven risk and collection management practices to minimize impact of any potential risk

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 49Key implications from findings for lenders to consider

Future Readiness Lending Strategy Infra

Risk Management

• Innovate and redesign • Decide on the choice of • Use of risk models and data

distribution channels customers (open market / analytics in credit underwriting

• Reconsider the customer existing) • Segment customers basis

management framework • Evaluate partnership models their credit behavior

• Facilitate seamless customer (co-lending / co-origination) • Monitor portfolio using

onboarding • Leverage on digital sourcing behavior scorecards and early

• Digitize and automate internal channels earning tools

operations • Decide on the right product • Implement collection

mix (secured versus prioritization models to

unsecured) maximize recoveries

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 50Thank

Thank You!

vDisclaimer

This Presentation is prepared by TransUnion CIBIL Limited (TU CIBIL). This Presentation is based on

collation of information, substantially, provided by credit institutions who are members with TU CIBIL.

While TU CIBIL takes reasonable care in preparing the Presentation , TU CIBIL shall not be responsible

for errors and/or omissions caused by inaccurate or inadequate information submitted to it by credit

institutions. Further, TU CIBIL does not guarantee the adequacy or completeness of the information in

the Presentation and/or its suitability for any specific purpose nor is TU CIBIL responsible for any access

or reliance on the Presentation and that TU CIBIL expressly disclaims all such liability. This Presentation

is not a recommendation for rejection / denial or acceptance of any application nor any recommendation

by TU CIBIL to (i) lend or not to lend; (ii) enter into or not to enter into any financial transaction with the

concerned individual/entity. The user should carry out all the necessary analysis that is prudent in its

opinion before making any decisions based on the Information contained in this Presentation. The use of

the Presentation is governed by the provisions of the Credit Information Companies (Regulation) Act,

2005, the Credit Information Companies Regulations, 2006, Credit Information Companies Rules, 2006.

No part of this presentation should be copied, circulated, published without prior approvals.

© 2020 TransUnion CIBIL Ltd. All Rights Reserved | 52You can also read