2022 2024 OSC Business Plan - Ontario ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

For the fiscal years ending

2022 – 2024

OSC

Business Plan

2022 – 2024 OSC BUSINESS PLAN TABLE OF CONTENTS INTRODUCTION............................................................................................................... 1 Background Vision, Mandate and Goals THE ENVIRONMENT ......................................................................................................... 4 Scan and Impact Securtites Regulation OSC Consultative Comittees GOVERNANCE ................................................................................................................ 13 The Commission OPERATIONS ................................................................................................................. 16 Organization, Structure and Resources to Meet Objectives STRATEGIC DIRECTION ................................................................................................. 21 OSC Statement of Priorities Current and Future Programs and Activities RISKS ............................................................................................................................ 31 Key Risks and Mitigation Strategies HUMAN RESOURCES ...................................................................................................... 36 Human Resources Plan COMMUNICATIONS ....................................................................................................... 38 Communicaiotins and Public Affairs Plan METRICS ....................................................................................................................... 40 Performance Measurement BUDGET ......................................................................................................................... 42 Financial Summary APPENDIX ..................................................................................................................... 46 Service Commitments

2022 – 2024 OSC BUSINESS PLAN

INTRODUCTION

Background

The Ontario Securities Commission (“OSC” or be anticipated in response to emerging

“Commission”) is a regulatory agency of the issues and changing market conditions,

Ontario government that operates on a cost particularly in light of the COVID-19

recovery basis. The OSC is required under pandemic and the recommendations by the

the Agencies and Appointments Directive Capital Markets Modernization Taskforce

(which is the key government directive (“the Taskforce”) that are adopted by the

setting out agency governance and government.

accountability) to annually provide a multi-

year Business Plan (the “Plan”) to the The information about the OSC included in

Minister of Finance. This Business Plan sets the Business Plan is reflective of the

out the OSC’s core strategy for the fiscal organization as at February 1, 2021.

years 2021-2022, 2022-2023 and 2023-2024

including the initiatives for the upcoming Primary Enabling Legislation –

year that will be undertaken toward this Securities Act (Ontario)

strategy.

The OSC is accountable to the Minister of

The OSC has overall accountability for the Finance. The Minister, in turn, is accountable

effective administration of the Securities Act to the Legislature for the Commission’s

(Ontario) (the “Act”) as well as the fulfilment of its mandate and its compliance

Commodity Futures Act (Ontario) (together, with government policies, and for reporting

the “Acts”). While the OSC oversees to the Legislature on the affairs of the

securities regulation for Ontario, capital Commission.

markets in Canada are highly integrated.

Accordingly, much of the OSC’s activity is The OSC annually provides the Minister with

often coordinated with the activities of other the following key reports:

provincial and territorial securities regulators, • Audited Financial Statements

primarily through the Canadian Securities

Administrators (CSA). Coordinating with the • Multi-year Business Plan

CSA helps to reduce regulatory complexity • Annual Statement of Priorities (SoP)

and burden faced by market participants.

• SoP Report Card (a progress report

Since financial services in general, and against the prior year SoP)

securities markets in particular, are • Annual Report.

increasingly global in their conduct, influence

and evolution, developments outside Canada In addition, the Ministry of Finance is

also affect operational activities of the OSC informed on operational matters through

as well as the ability to achieve its mandate. ongoing scheduled work-in-progress

meetings.

The financial summary in this Plan outlines

forecasted costs and revenues over a three- The OSC is required to affirm or sign a new

year period. Other aspects of this Plan focus Memorandum of Understanding (MOU) with

on current period initiatives. the new Minister of Finance within six

months of the Minister’s appointment. The

Business planning is not a discrete one-time OSC will be required to affirm or sign a new

exercise. Modification to various aspects of MOU with the new Minister of Finance.

the OSC Business Plan and priorities should

1 | Page2022 – 2024 OSC BUSINESS PLAN

INTRODUCTION

Vision, Mandate and Goals

Our Vision

To be an effective and responsive securities regulator –

fostering a culture of integrity and compliance and instilling investor

confidence in the capital markets.

Our Mandate

To provide protection to investors from unfair, improper or fraudulent practices,

to foster fair and efficient capital markets and confidence in capital markets and

to contribute to the stability of the financial system and the reduction of

systemic risk.

2 | PageMandate and Operating Principles The OSC is committed to fostering

confidence in Ontario's capital markets,

The mandate of the OSC as set out in the Act supporting an environment where capital is

is to provide protection to investors from available on competitive terms, streamlining

unfair, improper or fraudulent practices; to regulation with a strengthened focus on

foster fair and efficient capital markets and reducing regulatory burden and maintaining

confidence in capital markets; and to Ontario’s financial services sector as a world

contribute to the stability of the financial leader and significant contributor to the

system and the reduction of systemic risk. province’s economy.

The principal means for achieving this

mandate consist of: The OSC will continue to monitor financial

stability risks, improve market resilience, and

• Setting/defining requirements for reduce the potential risks arising from

accurate and timely disclosure of domestic and global systemic events.

information necessary for investors to

make informed decisions The OSC will also continue to seek

• Establishing restrictions on fraudulent opportunities to make its interface with

and unfair market practices and market participants easier and less costly.

procedures Efforts to streamline regulation, improve

operational efficiencies and lower regulatory

• Fostering of fair, efficient, and burden are expected to have a significant

transparent markets impact on reducing compliance costs,

• Establishing requirements for the including for development-stage and

maintenance of high standards of fitness innovative businesses.

and business conduct for market

participants As these changes are made, individuals and

businesses regulated by the OSC can expect

• Dedicated focus on reducing unnecessary to see enhanced service levels, less

regulatory burden on market participants duplication, and a more tailored regulatory

while upholding investor protection approach.

• Timely, open and efficient administration

of enforcement, compliance and Response to Expectations Set Out in

adjudication activities the Agency Mandate Letter

• Delegation of specific functions to Self- The OSC will continue to work closely with

Regulatory Organizations (SROs) (subject the Ministry of Finance pursuant to the

to appropriate OSC supervision) December 2020 mandate letter from the

• Responsible harmonization and Minister of Finance to the Acting Chair of the

coordination of regulatory practices with OSC and will coordinate with stakeholders as

other jurisdictions (e.g. through the appropriate to deliver on expectations.

Canadian Securities Administrators

(CSA), Heads of Regulatory Agencies

(HoA) and the International Organization

of Securities Commissions (IOSCO))

• Facilitating innovation in Ontario’s capital

markets.

3 | Page2022 – 2024 OSC BUSINESS PLAN

THE ENVIRONMENT

Scan and Impact

As the world emerges from an extraordinary Despite the start of a recovery in the

year, two environmental factors will influence summer of 2020, the recent resurgence of

OSC’s operations and policy agenda for years the coronavirus in Canada and elsewhere has

to come: the coronavirus pandemic and contributed to a slowing pace of recovery.

recommendations from the Ontario Capital Recent news about vaccine availability is

Markets Modernization Taskforce. Other key positive for those industries most impacted

challenges that may influence the OSC’s by social distancing. However, widespread

policy agenda, its operations and the way it vaccine availability is not expected until mid-

uses its resources are described below. 2021 and so COVID-19’s economic

consequences will remain a concern.

Effects of COVID-19

Households with constrained income are

Since the outbreak of the COVID-19 likely to prioritize non-discretionary spending

pandemic in early 2020, the world’s and could reduce their investing. The

economies and financial markets have experience of the economic shutdown may

experienced unprecedented conditions. The encourage other households to pay down

economic consequences of putting large their debt and build up contingency savings

parts of the economy into lockdown during in case of future waves of the virus and

the first wave of COVID-19 were significant. associated lockdowns. This too may impact

Economic growth declined significantly, and investing behaviour.

millions of Canadians experienced

employment disruptions and businesses At the time of writing, forecasters anticipate

struggled to meet financial commitments, that interest rates will be maintained at very

such as payments to suppliers and rent. low levels until at least 2023. Continued low

interest rates will impact capital markets

Governments provided large-scale fiscal and activity including capital raising and

monetary support for the economy and investment portfolio decisions.

financial markets. At the same time, we have

seen unprecedented levels of Central Bank Low rates may encourage firms to maintain

intervention in markets to support liquidity. current levels of debt or increase their

These supports provide the foundation for borrowing if they are creditworthy. This

the economic recovery. would result in stable or even increased

volumes of prospectus filings from corporate

Financial markets proved to be largely issuers and growing levels of corporate debt.

resilient to the conditions experienced.

Markets recovered from the initial stresses Low interest rates will challenge investors to

experienced in March and April 2020; find returns that match their needs and

however, there remains a long and plans. Increased efforts by investors to

challenging path to full recovery. The OSC, search for yield could increase their exposure

along with our CSA colleagues, took a variety to risk. This may take the form of leveraged

of steps to support industry participants and investing or moves into more risky asset

investors. Regulators will continue their classes and individual investments.

efforts to identify and implement support

measures where appropriate.

4 | PageRegulators will need to remain vigilant about The breadth and pace of innovation in the

products promising higher returns and that financial sector could result in gaps in

investors have the necessary tools to make regulation or become a source of non-

informed decisions. Other risks to investors compliance. For example, the potential

could include issues around the quality of applications and impacts of Artificial

financial information, forward-looking Intelligence (AI) are significant but are not

information and debt servicing costs as well yet well understood.

as concerns about further growth in the level

of corporate debt. Investor Needs and Education

Capital Markets Modernization Investor needs and challenges – key drivers

of regulatory concerns – are changing

Taskforce

quickly. Demographics are shifting, the

The Ontario government announced the financial industry is evolving, technology is

formation of the Taskforce, which began disrupting, and the implications of the

work in February 2020. The Taskforce ongoing global pandemic for people’s future

published a consultation report in July 2020 financial security are only beginning to be

and published its final report on January 22, understood. One way to respond to these

2021. The final Taskforce report includes challenges is through investor education,

significant recommendations to modernize something diverse stakeholders in the capital

the capital markets regulatory framework. markets widely agree on.

The OSC will review and consider the As the responsibility for investing shifts to

recommendations of the Taskforce and will individuals, they are challenged to achieve

adjust its priorities to accommodate any the returns needed to finance future needs.

changes recommended by the Taskforce as There are wide gaps in the levels of

adopted by the Ontario government. investment experience and financial literacy

among investors. Investor education has the

Technology and Innovation potential to contribute to improved financial

outcomes for investors and is an important

The pace of technological evolution and component of investor protection.

innovation creates challenges to develop and

maintain a responsive and aligned regulatory Protecting investors is a key element of the

framework. Market participants continue to OSC’s mandate. The OSC protects investors

expand their product and service offerings. by actively enforcing securities laws to hold

Fintech (technology facilitated financial offenders accountable and deter future

services) and Regtech (technology facilitated misconduct. The OSC Investor Office

regulatory compliance services) innovation provides impartial information to help

continues to advance and is a key disruptive investors evaluate their choices, invest

force in the financial services industry. wisely, and protect themselves against fraud.

Complexity driven by financial innovation The OSC is focused on improving the

offers many potential benefits and risks to investor experience, including by enhancing

the market. Fintech is leveraging new education, outreach and engagement and

technology and creating new business improving the information provided to

models such as providing new product investors or other interactions that investors

offerings (e.g. blockchain-based crypto have with issuers and registrants.

assets) and disrupting service channels (e.g.

online advisors). Financial services firms are Demographics are critical to understanding

using technological innovation, digitalization investor needs and are a key driver of most

and distributed ledger technology to reduce investor-focused issues. Different investor

operational costs and improve efficiency. segments (e.g. seniors and millennials) have

5 | Pageunique characteristics and present different Digital Transformation

challenges in terms of investment objectives

and horizons. Their preferences can vary in Ever increasing market complexity is

terms of products (ETFs versus mutual generating greater availability and reliance

funds) and service channels. on data. The OSC is adding new tools and

processes to support staff in delivering on

Growing interest in environmental, social and their responsibilities. A key element will be

governance (ESG) factors also means that addressing challenges in managing growing

regulators need to consider how best to volumes of data, including information

support investors in getting the information security.

they reasonably need to make informed

investment and voting decisions. The OSC is investing in technology and

Automated financial advice is redefining the infrastructure to support a digital

delivery of client wealth management transformation program that will improve

services and the fees charged for advice. access to data and information to identify

trends and risks to support analysis and

Due to the impacts of the COVID-19 decision-making.

pandemic, there is an even greater need for

the OSC to provide resources and support for Workforce Strategy

investors and financial consumers. The OSC

The OSC’s ability to meet the identified goals

will seek new and innovative ways to deliver

and strategic objectives is dependent upon it

investor education and support retail

having both sufficient and appropriate

investors in today's complex and uncertain

resources. The COVID-19 pandemic has

investing environment.

changed the way we work, with the majority

of OSC employees working from home offices

Cybersecurity Resilience but without reduction in operational

Cyber-attacks that have the potential to effectiveness.

disrupt our markets and market participants

are likely to occur. Growing dependence on While attracting, motivating and retaining

digital connectivity is raising the potential for top talent in a competitive market

digital disruption in our financial services and environment continues to be challenging, the

capital markets and creating a strong OSC continues to build its capabilities and

imperative to raise awareness about cyber- skills by recruiting staff across a range of

attacks and strengthen cybersecurity disciplines, and by developing the skills and

resilience. This is a growing challenge as experience of our internal talent.

more businesses, services and transactions

span national and international borders. The

OSC, working with other regulatory partners,

has an important role to play in assessing

and promoting readiness and supporting

cybersecurity coordination and resilience

within the financial services industry and

raising awareness of cybersecurity risks.

6 | Page2022 – 2024 OSC BUSINESS PLAN

THE ENVIRONMENT

Securities Regulation

Securities regulation is a provincial member of the passport system but in many

responsibility, but provincial decisions can cases, it relies on other jurisdictions’

affect the capital markets across Canada as decisions.

well as Ontario’s capital markets. The other

CSA members have similar mandates to Self-Regulatory Organizations

protect investors and foster fair and efficient (SROs)

capital markets. All Canadian securities

regulatory authorities currently work The CSA has developed a coordinated

together through the CSA. The CSA is not a approach to the regulation of SROs.

legal entity but a cooperative association. Recognized SROs play a significant role in

promoting investor protection and market

Canadian Securities Administrators integrity. They have prescriptive rules,

(CSA) compliance staff and an enforcement

function which includes the authority to

The CSA’s key objective is to coordinate and impose sanctions on their dealer members

harmonize regulation of the Canadian capital and their individual representatives and

markets. CSA members work cooperatively approved persons – i.e. fines, reprimands,

to develop and implement harmonized suspensions and permanent membership

securities laws, and to administer, monitor bans. The Securities Act provides SROs with

and enforce laws in a consistent and the ability to pursue the collection of

coordinated manner to minimize regulatory disciplinary fines directly through the courts.

duplication. As front-line regulators, SROs discharge their

responsibilities, subject to oversight by the

Harmonized Policies and Processes applicable provincial securities regulatory

The CSA has achieved a significant level of authorities known as “recognizing

harmonization and uniformity in securities regulators”.

laws and the implementation of those laws

across Canada. Currently most regulatory There are two recognized and industry-

requirements are set out in national funded SROs in Canada: the Mutual Fund

instruments and multilateral instruments and Dealers Association of Canada (MFDA) for

policies that are adopted with virtually registered mutual fund dealers and the

uniform wording in all jurisdictions. In Investment Industry Regulatory Organization

addition to harmonized instruments, the of Canada (IIROC), for investment dealers

passport system and accompanying interface and market members. Most CSA

with the OSC provides a streamlined filing jurisdictions rely on the applicable SRO to

and review procedure for prospectuses and conduct the day-to-day regulation of mutual

exemptive relief applications among multiple fund dealers and investment dealers, with

securities regulators across Canada resulting IIROC also responsible for registering

in reduced regulatory burden on market individuals and monitoring trading on equity

participants. The system is designed to and debt marketplaces in Canada. Each SRO

enable one CSA jurisdiction to rely on the is the sole sponsor of an investor protection

analysis and review undertaken by the staff fund (IPF) which protects client assets in the

of another CSA jurisdiction. The OSC is not a event of an SRO member insolvency.

7 | PageThe approved funds are the Canadian The OSC is the lead regulator for TSX Inc.,

Investor Protection Fund (CIPF) for IIROC Alpha, NEO, and Nasdaq, and is co-lead

members and the MFDA Investor Protection regulator of CSE with the BCSC. The Alberta

Corporation (MFDA IPC) for MFDA members. Securities Commission (ASC) and the BCSC

are joint lead regulators for the TSX Venture

The recognizing regulators have formal Exchange. On the derivatives side, the AMF

oversight programs, consisting of regular is the lead regulator for the Bourse de

reporting on activities, oversight reviews, Montréal and the ASC for NGX.

processes to review proposed rule and by-

law amendments and regular meetings with Clearing Agencies

the SROs to discuss issues and emerging

trends. Similar programs are in place for the Since March 1, 2011, clearing agencies

IPFs. Since multiple jurisdictions are carrying on business in Ontario are required

involved in SRO / IPF oversight, the to be recognized by the OSC or to have

programs are coordinated. A principal obtained an exemption from the requirement

regulator model is used for this purpose; to be recognized as clearing agencies in

each recognizing jurisdiction is actively Ontario.

involved in oversight, but a single regulator

(i.e. the principal regulator) coordinates the Trade Repositories

process. The OSC is the principal regulator

As part of Canada’s commitment to the G20

for IIROC, CIPF and the MFDA IPC; and the

initiative to reform the practices in the OTC

British Columbia Securities Commission

derivatives markets, the OSC has

(BCSC) is the principal regulator for the

implemented a Trade Repository Rule (TR

MFDA.

Rule) to improve transparency in the OTC

derivatives market by requiring participants

The CSA SRO Oversight Standing Committee

in the market to report certain trade

is responsible for dealing with issues and

information to a designated TR and to

initiatives that affect the SROs. The day-to-

impose certain minimum standards on

day oversight of SRO/ IPFs is performed by

designated TRs to ensure that they operate

sub-committees set up for each SRO / IPF.

in a manner that promotes the public

These sub-committees also act as forums for

interest. Market participants began reporting

the discussion of issues related to each

under the TR Rule in October 2014.

regulated entity.

Regulation of Issuers – Offerings

Exchanges

and Continuous Disclosure

Exchanges that have been recognized in

various jurisdictions in Canada are the TMX Disclosure of complete, accurate and timely

Group Inc. (and TSX Inc. that operates the information is the cornerstone of investor

exchange), TSX Venture Exchange, Canadian protection and efficient capital markets.

Securities Exchange (CSE), TSX Alpha Subject to certain specified exemptions,

Exchange (Alpha), Neo Exchange Inc. (NEO), issuers are required to prepare and file a

Nasdaq CXC Limited (Nasdaq), Natural Gas preliminary and final prospectus prior to any

Exchange (NGX) and the Bourse de Montréal. distribution of securities to the public. The

These exchanges offer services in multiple prospectus must contain full, true and plain

provinces and territories and are subject to disclosure of all material facts relating to the

regulation by the securities regulatory securities offered under the prospectus and

authorities in the jurisdictions in which they must be receipted by the Commission.

operate. The CSA relies on a “lead” regulator

model for the oversight of each recognized Public companies (referred to as reporting

exchange, whereby one jurisdiction issuers) must comply with periodic and

recognizes the exchange while the others timely continuous disclosure obligations.

exempt the exchange from recognition based Those obligations include periodic financial

on principles of reliance. reporting (annual and interim), material

8 | Pagechange reports, and business acquisition investment funds must also comply with

reports. Requirements that contribute to fair product regulations that contribute to

and efficient markets, such as insider trade investor protection, including investment

reporting, corporate governance restrictions, asset custody requirements and

requirements, and minority shareholder security holder voting requirements. Investor

protection requirements also form part of protection is further promoted by requiring

public company regulation. every publicly offered investment fund to

have a fully independent body, an

Issuers that rely on a prospectus exemption Independent Review Committee (IRC),

must comply with the applicable conditions. whose role is to consider all decisions

Depending on the exemption, conditions referred to the IRC by the fund manager

relate to the nature of the purchasers, limits involving an actual or perceived conflict of

on the amounts that may be distributed, interest faced by the fund manager in the

prescribed disclosure, and limited ongoing operation of the fund.

reporting.

The OSC also regulates structured products

Oversight reviews of reporting issuers that are securities and sold to retail

offering documents are conducted using a investors. These structured products are also

risk-based approach, both when a company known as linked notes. Linked notes

initially offers its securities to the public and generally provide investment exposure to

on an ongoing basis as it continues to give public indices and can have various degrees

information to the marketplace, to assess of downside protection and pay-out. Linked

compliance with securities law requirements. note issuers file base-shelf prospectuses and

prospectus supplements to distribute these

Prospectus-exempt distributions do not notes. Any novel linked note is subject to the

require prior approval or staff review. OSC’s review before distribution of the note.

Compliance and oversight of issuers in the

exempt market is focused on creating Registration of Dealers, Advisers and

awareness of our requirements, monitoring Investment Fund Managers

the use of the prospectus exemptions and

identifying material non-compliance that may The underlying principle of regulation for

require regulatory intervention. dealers, advisers and investment fund

managers is based on registration and

Investment funds that offer securities to the ongoing registrant obligations. Registration

public must prepare and file a preliminary entails demonstrating that the person or

and final prospectus before distributing their company meets the fit-and-proper

securities. In addition, conventional mutual requirements of proficiency, integrity and

funds must prepare a Fund Facts document financial solvency. Once registered, a dealer,

that is required to be delivered to a adviser or investment fund manager must

purchaser prior to the purchase of mutual meet ongoing registrant obligations. For

fund securities. The document provides key example, registered firms must meet certain

information about a fund in plain language business conduct requirements (including

and cannot exceed two pages in length. know-your-client (KYC), know-your-product

Similarly, exchange-traded funds (ETFs) are (KYP), suitability, conflict management and

required to deliver an ETF Facts document to client relationship requirements), and

investors who purchase ETF securities on an financial reporting, working capital, insurance

exchange. and bonding requirements.

Publicly offered investment funds are subject

to continuous disclosure obligations similar to

those applicable to public companies. These

9 | PageUnless an exemption exists, or a behalf of a registered dealer or adviser, or

discretionary exemption is granted, firms act as the ultimate designated person or

must register in each jurisdiction where they chief compliance officer of a registered firm.

are:

The OSC has delegated to IIROC the

• In the business of trading

registration of their member firm dealing

• In the business of advising representatives. To facilitate registration and

filing in multiple jurisdictions, the CSA

• Holding themselves out as being in the

developed the National Registration Database

business of trading or advising

and has harmonized the registration regime.

• Acting as an underwriter Oversight reviews of registrants and

derivatives market participants are

• Acting as an investment fund manager.

conducted to assess compliance with

applicable securities legislation and rules.

The OSC registers firms in all categories of

Registrants are selected for reviews using a

registration (this function is not delegated to

risk-based approach for issue-specific

SROs in Ontario).

compliance reviews, or when registrant-

specific concerns are identified.

Individuals must become registered with the

OSC if they trade, underwrite or advise on

10 | P a g e2022 – 2024 OSC BUSINESS PLAN

THE ENVIRONMENT

OSC Consultative Committees

The Executive and staff of the OSC operating SBAC also provides feedback on the

branches are supported by various third- effectiveness of Corporate Finance policies

party consultative committees that have and initiatives as they relate to small

been established for one or more of the business.

following purposes:

Investment Funds Technical Advisory

• To provide a broad range of ideas and

Committee (IFTAC) – advises OSC staff on

expertise as new policy initiatives are

technical compliance challenges in the

developed

investment funds product regulatory regime,

• To help the OSC understand how a and opportunities for improving alignment

specific, recently implemented policy is between investor, industry and regulatory

affecting capital market participants goals.

• To improve the OSC’s understanding of

Continuous Disclosure Advisory

the concerns and issues faced by a

Committee (CDAC) – advises OSC staff on

stakeholder group on an ongoing basis.

the development, implementation and review

of continuous disclosure policies and

A list of the key consultative committees

practices.

includes:

Mining Technical Advisory and

The Investor Advisory Panel (IAP) – is

Monitoring Committee (MTAMC) –

an independent advisory panel to the

provides advice to the CSA on technical

Commission. The IAP provides comments in

issues relating to disclosure requirements for

response to public requests for comment by

the mining industry. The committee also

the Commission on proposed rules, policies,

serves as a forum for continuing

concept papers and discussion drafts. The

communication between the CSA and the

Panel also provides comments on the OSC’s

mining industry.

proposed annual Statement of Priorities,

brings forward policy issues for consideration

Securities Advisory Committee (SAC) –

and advises on the effectiveness of the OSC’s

provides advice to the OSC on legislative and

investor protection initiatives.

policy initiatives, and capital market trends.

Market Structure Advisory Committee

Registrant Advisory Committee (RAC) –

(MSAC) – serves as a forum to discuss

serves as a forum to discuss issues and

issues and policy-and rule-making initiatives

challenges faced by registrants in

associated with market structure and

interpreting and complying with Ontario

marketplace operations in the Canadian and

securities law, including registration and

global capital markets.

compliance-related matters.

Small Business Advisory Committee Securities Proceedings Advisory

(SBAC) – advises the OSC’s Corporate Committee (SPAC) – provides comments

Finance Branch staff on current business and advice to the Office of the Secretary on

practices and emerging trends affecting small policy and procedural initiatives relating to

businesses in both the public and private the Commission’s administrative tribunal

markets. proceedings.

11 | P a g eSeniors Expert Advisory Committee International Harmonization

(SEAC) – serves as a forum to discuss

issues and challenges faced by seniors. The The OSC is actively engaged at the

Committee provides OSC staff with expert international level, promoting cooperation,

opinions and input on securities-related information sharing and the development of

policy, operational, educational and outreach principles, standards and best practices in

activities that are designed to meet the securities regulation. The OSC Acting Chair

needs of older investors. is a member of the governing Board of

IOSCO, which is the leading international

Financial Reporting Advisory Committee policy forum for over 100 securities

– provides advice to the CSA’s Chief regulators and is recognized as the global

Accountants Committee on relevant policy standard setter for the securities sector.

initiatives and various technical accounting OSC staff routinely take leadership roles on

and auditing issues that relate to financial IOSCO policy committees and actively

reporting requirements and guidance in cooperate with other regulators under

securities legislation in Canada. The IOSCO’s multilateral MOUs to facilitate cross

committee also serves as a forum to discuss border investigations and enforcement

financial reporting practices and trends in the matters.

Canadian and global capital markets.

12 | P a g e2022 – 2024 OSC BUSINESS PLAN

GOVERNANCE

The Commission

The Commission, as the regulatory body Candidates for appointment are

responsible for overseeing the capital recommended to the Minister by the Chair

markets in Ontario, administers and enforces following a recruitment process led by the

the Acts. The Securities Act (Ontario) Governance and Nominating Committee of

establishes the Commission as a corporation the Board. The Committee regularly reviews

without share capital with a Board of the qualifications, attributes, skills and

Directors consisting of the members of the experience of the Members to ensure that

Commission (Members). The Commission is Members, individually and collectively, meet

composed of at least nine and not more than the standards necessary to exercise their

sixteen Members, each of whom is appointed responsibilities effectively. The Committee

by the Lieutenant Governor in Council. If applies a competency matrix to identify any

there are fewer than nine but at least two gaps in attributes, skills and qualifications

Members in office, the Act deems the that may arise due to an upcoming vacancy

Commission to be properly constituted for up on the Commission.

to 90 days.

Appointments and reappointments to the

Members are appointed for a fixed term by Commission are made in accordance with the

the Lieutenant Governor in Council upon the Agencies and Appointments Directive, the

recommendation of the Minister of Finance Memorandum of Understanding with the

and Cabinet. The Lieutenant Governor in Minister of Finance and the procedures of the

Council also designates one Member as Public Appointments Secretariat of Ontario.

Chair & CEO of the Commission and may In accordance with the Agencies and

designate up to three Members as Vice Appointments Directive, government

Chairs of the Commission. The Chair & CEO appointments will respect the needs of the

and the Vice-Chairs are full-time Members entity to which they have been appointed but

and devote their full time to the work of the will also respect the diversity of the people in

Commission. The other Members, including Ontario and the need to deliver services and

the Lead Director, are part-time Members, decisions in a professional, ethical and

are independent of management, and devote competent manner.

as much time as necessary to perform their

duties. The Agencies and Appointments Directive

provides that a person appointed to a

As of February 1, 2021, the Commission is regulatory agency, such as the Commission,

composed of twelve Members, three full-time will serve an initial appointment for a period

and nine part-time. The full-time Members of up to two years, and may be eligible for

are D. Grant Vingoe, Acting Chair & CEO, and reappointment for a second term of up to

Wendy Berman and Timothy Moseley, Vice- three years and a third term of up to five

Chairs. The part-time Members are Mary years. The Commission has adopted a policy

Anne De Monte-Whelan, Garnet W. Fenn, to recommend the reappointment of an

Lawrence P. Haber, Craig Hayman, Raymond eligible part-time Member for up to two

Kindiak, Frances Kordyback, Cathy Singer, additional terms of two years each, resulting

M. Cecilia Williams and Heather Zordel. in a possible overall term of six years.

13 | P a g eGovernance Framework Commission. As adjudicators, Members

(other than the Chair & CEO, who does not

Although structured as a corporation, the adjudicate) act independently of their other

Commission is a regulatory body and its roles and preside over administrative

purpose is mandated by statute. The Act proceedings brought before the

establishes the Commission’s role in Commission’s Tribunal – the administrative

regulating capital markets, sets out the tribunal that is assigned the power to

fundamental principles that the Commission conduct hearings under the Acts. A brief

shall have regard to in overseeing the outline of these three primary roles follows.

administration and enforcement of the Act,

and outlines the basic governance and The Role of Members in Policy and

accountability structure for the Commission. Rule-making

The Commission, unlike a business The Commission regulates Ontario’s capital

corporation, does not have shareholders to markets by making rules that have the force

whom the Board of Directors reports. of law and by adopting policies that influence

Instead, the Commission is accountable to the behaviour of capital market participants.

the Minister of Finance and, through the The Commission exercises its regulatory

Minister, to the Ontario Legislature. The Act oversight function through enforcement of

requires the Commission to enter into a the Acts and administration of certain

Memorandum of Understanding with the provisions of the Ontario Business

Minister of Finance every five years and to Corporations Act.

provide the Minister with any information

about its activities, operations and financial Members attend regular policy and rule-

affairs that the Minister requests, including making meetings with staff to review and

an Annual Report. approve regulatory initiatives, priorities,

policies and rules and to discuss general

The Memorandum of Understanding sets out oversight of the capital markets.

the accountability relationship between the

Ontario Securities Commission and the The policy and rule-making function of

Minister. When there is a change in the Members includes:

Minister or the Chair and CEO, both parties • Setting the regulatory strategic priorities

must agree to either affirm the current that guide ongoing operations through

Memorandum of Understanding or to revise it the annual Statement of Priorities

and sign a new Memorandum of published by the Ontario Securities

Understanding. The current Memorandum of Commission

Understanding can be found on the

Commission’s website. • Providing input to staff with respect to

policy and rule-making and other

The Role of Members regulatory initiatives, including initiatives

with other securities regulators

Overview

• Assessing progress in implementing

Members of the Commission perform three priorities and initiatives

distinct functions in support of the

• Guiding staff on emerging trends and

Commission’s mandate – making policies and

issues in the capital markets.

rules, serving as a board of directors and

adjudicating. As policy and rule-makers, Meetings of two Members are held twice

Members approve and oversee the weekly to consider applications for exemptive

implementation of the Commission’s relief from Ontario securities law. In addition,

regulatory initiatives and priorities. As the the Vice-Chairs consider novel exemptive

Board, Members oversee the management of relief applications.

the financial and other affairs of the

14 | P a g eThe Role of Members as the Board of independently of their other roles and

Directors of the Commission preside over administrative proceedings

brought before the Commission’s Tribunal.

The Members act as the Board of Directors of

the Commission. The Board is responsible for

Proceedings before the Tribunal are governed

the overall stewardship of the Ontario

by the Ontario Statutory Powers Procedure

Securities Commission, including strategic

Act, the Commission’s Rules of Procedure

planning and annual budgets, financial

and Forms, the Commission’s Practice

review, reporting and disclosure, risk

Guideline, and principles of law applicable to

assessment and internal controls and board

administrative tribunals.

governance.

The Commission adopted an Adjudication

The Board exercises its corporate oversight

Guideline to enhance the transparency of the

through regular and special meetings of the

Commission’s adjudicative processes and

full Board and its four standing committees.

provide guidance to Members and employees

Board meetings are held at least quarterly

on the professional and ethical standards

and special meetings are held as required.

expected of them in the exercise of their

The Board also conducts strategic planning

responsibilities. The Commission established

and priorities setting meetings with senior

the Adjudicative Committee as a standing

management.

advisory committee to assist Members in

fulfilling their adjudicative responsibilities

The Board has delegated certain oversight

and to promote tribunal excellence.

responsibilities to its standing committees

while retaining decision-making authority.

Secretary to the Commission

The Board’s four standing committees are

the Audit and Finance Committee, The Board appoints the Secretary to the

Governance and Nominating Committee, Commission, who is an officer of the

Human Resources and Compensation corporation and reports directly to the Chair

Committee, and Risk Committee. & CEO. The Secretary to the Commission is

responsible for the oversight and leadership

The Commission adopted the Ontario of the governance framework and Tribunal.

Securities Commission Charter of The Secretary provides strategic governance

Governance to promote transparent, advice, guidance and support to the

accountable and informed governance. The Members, advances communications

Commission’s commitment to excellence in between the Board and management,

its governance practices is supported by records the corporate minutes, safeguards

clear roles and responsibilities, effective tribunal integrity and procedural fairness and

processes and reporting, and extensive provides governance and tribunal education

strategic planning and stakeholder to Members and other stakeholders.

engagement.

The Role of Members as the Tribunal of

the Commission

As adjudicators, Members (other than the

Chair & CEO, who does not adjudicate due to

involvement with enforcement activity) act

15 | P a g e2022 – 2024 OSC BUSINESS PLAN

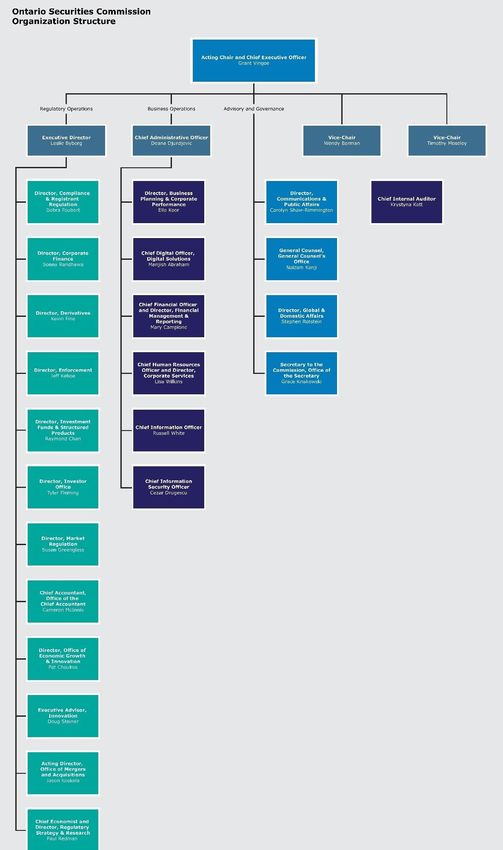

OPERATIONS

Organization, Structure and Resources to Meet Objectives

In 2019, the OSC announced a new • Investor Office

management structure to modernize and

• Market Regulation

support its capacity to keep pace with

changes in the capital markets and to deliver • Office of the Chief Accountant

on its mandate. Through 2020, the

• Office of Economic Growth and

announced organizational structure

Innovation

continued to be implemented, including the

publication of the Charter for the Office of • Office of Mergers and Acquisitions

Economic Growth and Innovation, which sets

• Regulatory Strategy and Research

out its vision, role and strategic objectives.

Business Operations Branches, reporting

In 2020, the OSC also announced the

to the Chief Administrative Officer (CAO)

creation of a Digital Solutions Branch,

including the new Executive position of Chief Business Operations Branches include:

Digital Officer. This branch is intended to

• Business Planning and Corporate

support the OSC in becoming more strategic

Performance

and proactive in leveraging and adapting to

digital trends. Centralizing digital and data • Digital Solutions

solution design, by way of creation of this

• Financial Management and Reporting

branch, will also result in more effective use

of resources, greater integration of branch • Human Resources and Corporate Services

operations, and alignment to a common

• Information Security

digital vision. The Digital Solutions Branch is

accountable to the Chief Administrative • Information Services

Officer (CAO).

Advisory and Governance Branches,

The OSC is structured into three main areas:

reporting to the Chair and CEO

Regulatory Operations Branches, Advisory and Governance Branches include:

reporting to the Executive Director (ED)

• Communications and Public Affairs

Regulatory Operations Branches include:

• General Counsel’s Office

• Compliance and Registrant Registration

• Global and Domestic Affairs

• Corporate Finance

• Office of the Secretary

• Derivatives

• Enforcement Internal Audit reports to the Chair and CEO.

• Investment Funds and Structured

Products

16 | P a g eNote: The above represents the OSC organizational structure as at February 1, 2021. The most current OSC organizational

structure, can be found at https://www.osc.gov.on.ca/en/About_our-structure_index.htm

17 | P a g eRegulatory Operations Branches and systems, self-regulatory organizations,

Offices clearing agencies and trade repositories) in

Ontario and for developing policy relating to

Compliance and Registrant Regulation – market structure, trading, clearing and

responsible for regulating firms and settlement.

individuals who are in the business of

advising or trading in securities or Office of the Chief Accountant – supports

commodity futures, and firms that manage the OSC in creating and promoting a high-

investment funds in Ontario, as well as quality framework for financial reporting by

developing policy relating to registrants and market participants.

their obligations.

Office of Economic Growth and

Corporate Finance – responsible for Innovation – responsible for leading the

regulating issuers (other than investment OSC’s efforts to support innovation and

funds) in the public and exempt markets. economic growth in Ontario’s capital

The branch reviews public distributions of markets. The Innovation Office will focus its

securities, exempt market activities and efforts on initiatives that promote innovation

continuous disclosure of reporting issuers, and capital formation, modernize regulation

and leads issuer-related policy initiatives. and reduce burden, and strengthen outreach

The branch is also responsible for supervising and engagement, including collaborating with

insider reporting, regulating credit rating businesses and other regulators to support

agencies and overseeing the listed issuer innovation, through OSC LaunchPad, and

function for OSC recognized exchanges. promoting the implementation of technology

to reduce costs and accelerate innovation in

Derivatives – responsible for developing a financial services.

regulatory framework for over-the-counter

derivatives trading in Ontario, implementing Office of Mergers and Acquisitions –

and reviewing compliance with that responsible for matters relating to take-over

framework and contributing to systemic risk bids, issuer bids, business combinations,

monitoring of the Ontario capital markets. related party transactions and significant

acquisitions of securities of reporting issuers.

Enforcement – responsible for investigating

and litigating breaches of the Acts and Regulatory Strategy and Research –

seeking orders in the public interest before responsible for the delivery of economic,

the Commission and the courts. regulatory and financial research and

analysis that supports the development of

Investment Funds and Structured OSC regulatory strategy and policy

Products – responsible for regulating recommendations. The Branch advises on

investment products that offer securities for and informs the OSC’s strategy, priorities,

sale to the public in Ontario, including mutual regulatory operations decisions and

funds, exchange-traded funds, structured discussions with other regulatory bodies and

products and scholarship plans. agencies concerned with financial stability.

The branch also supports both investors and

Investor Office – sets the strategic market participants through the Inquiries

direction and leads the OSC’s efforts in and Contact Centre.

investor engagement, education, outreach

and research. The Office also has a policy Business Operations

function, plays a key role in the oversight of

the OBSI, and provides leadership at the Business Planning and Corporate

OSC in the area of behavioural insights and Performance – responsible for the delivery

improving the investor experience. of corporate-wide processes which result in

an OSC Strategic Plan, an annual Statement

Market Regulation – responsible for of Priorities and OSC Business Plan; the

regulating market infrastructure entities identification and mitigation of current and

(including exchanges, alternative trading emerging enterprise-wide risks; quarterly

18 | P a g ebusiness reporting; measures for public and Executive, Governance and

internal reporting on OSC performance; and Regulatory Advisory Branches and

the development and ongoing management Offices

of OSC enterprise data governance.

Communications and Public Affairs –

Digital Solutions – leads the digital provides strategic advice and services to

transformation of OSC business: developing ensure timely and effective communication of

data driven business solutions leveraging OSC priorities, policies and actions to

novel technologies; modernization of external and internal stakeholders.

business platforms and processes;

digitization of business operations and General Counsel’s Office – an in-house

development of user-centric service models; legal, policy, strategy and risk-management

establishing service analytics and supporting resource to the OSC, is also responsible for

reporting needs across branches; and the collection of unpaid monetary sanctions

ensuring data accessibility, quality and and leads the defence of proceedings

standardization with fit-for-purpose data brought against the Commission. GCO also

governance supports the OSC Ethics Executive in the

oversight of organizational integrity and

Financial Management and Reporting – ethical conduct. Provides advice and support

provides financial management and analysis, to the OSC in its dealings with the Ministry of

reporting and treasury services to allow the Finance, other regulators and governments.

OSC to continue carrying out its regulatory

responsibilities. Assurance over financial Global and Domestic Affairs – responsible

reporting is provided through the design and for advising the Commission in connection

maintenance of effective controls. with its relationship and engagement with

government, regulators and other

Human Resources and Corporate organizations in Canada and internationally.

Services – this branch includes the following The Branch supports the participation of the

functions: Human Resources, Organizational Chair and Commission staff in CSA, HoA and

Development, Administration (Facilities, IOSCO, and manages the Commission’s

Procurement, Office Services), Knowledge accountability to the Minister of Finance and

Services, Records and Information day-to-day relationship with the Ministry of

Management, and Business Continuity. The Finance.

Branch provides procurement and

stewardship of OSC resources to support the Office of the Secretary – supports the

achievement of OSC priorities, ensures Members of the Commission in their

compliant program and service delivery and statutory mandate as policy and rule-

leads the design and implementation of a makers, adjudicators for the Commission’s

positive employee experience. Tribunal and as the Board of Directors by

providing administrative law and corporate

Information Services (IS) – is responsible governance advice and professional support.

for establishing, monitoring and maintaining

the information technology systems and Internal Auditor – conducts risk-based

services for the OSC in support of its internal audits to evaluate the quality and

mandate. The group includes Client effectiveness of OSC processes and systems,

Services, Application Services, Technology including compliance with policies and

Services, Enterprise Architecture and IS procedures.

Project Management.

Information Security – responsible for the

design, implementation and ongoing

maintenance of the OSC’s information

security program to achieve and sustain the

organization’s security posture.

19 | P a g eTotal Approved Permanent Positions for Fiscal Year Starting April 1,

2021

Branches and Offices # of Staff

Regulatory Operations Branches / Offices

Compliance and Registrant Regulation 90

Corporate Finance 56

Derivatives 11

Enforcement 159

Investment Funds and Structured Products 34

Investor Office 17

Market Regulation 30

Office of the Chief Accountant 5

Office of Economic Growth and Innovation 13

Office of Mergers and Acquisitions 6

Regulatory Strategy and Research 20

Business Operations Branches / Offices

Business Planning and Corporate Performance 8

Digital Solutions 19

Financial Management and Reporting 11

Human Resources & Corporate Services 40

Information Services 38

Chief Information Security Office 2

Executive, Governance & Regulatory Advisory Branches / Offices

Communications and Public Affairs 16

General Counsel’s Office 18

Global and Domestic Affairs 8

Office of the Secretary 15

Executive Offices

Offices of the Chair, Executive Director, Internal Auditor, Chief Administrative Officer 10

Strategic Workforce Positions

Strategic Workforce Positions 2

Total Approved Permanent Positions 628

20 | P a g e2022 – 2024 OSC BUSINESS PLAN

STRATEGIC DIRECTION

OSC Statement of Priorities

Our 2021-2022 SoP sets out the four • Bring Timely and Impactful Enforcement

strategic goals on which the OSC intends to Actions

focus its resources and actions in 2021-2022.

• Continue Consultation on the Current

It also lays out the priority initiatives that the

Self-Regulatory Organization (SRO)

OSC will pursue in support of each of these

Framework

strategic goals.

• Strengthen Investor Redress through the

The 2021-2022 SoP and this corresponding Ombudsman for Banking Services and

Business Plan outline the items the OSC will Investments (OBSI), through Policy and

continue to prioritize, alongside any Oversight Activities.

recommendations from the Taskforce

endorsed by the Government of Ontario, and GOAL 2: Reduce Regulatory Burden

any additional fallouts from the COVID-19

pandemic. Enhance access for businesses and financial

services providers to Ontario’s capital

The OSC recognizes that it may need to markets

update its priorities to reflect the impacts • Complete Actions Identified in the OSC

and lessons learned from the COVID-19 Burden Reduction Report.

pandemic. Additionally, the Commission

anticipates adjusting its priorities to

GOAL 3: Facilitate Financial

accommodate any changes due to the

Innovation

recommendations from the Taskforce

following their consideration by the Cultivate an environment that supports

Government of Ontario. development of innovative financial business

models

GOAL 1: Promote Confidence in

• Implement Multi-Year Plan for the Office

Ontario’s Capital Markets of Economic Growth and Innovation

Promote confidence in Ontario’s capital • Engage with Fintech and Support

markets among market participants and Innovation in Capital Markets.

investors

• Support Implementation of Client GOAL 4: Strengthen Our

Focused Reforms (CFR) Organizational Foundation

• Implement Mutual Fund Embedded People, Technology and Information

Commissions Policies and Ontario

Regulatory Response to Deferred Sales • Redevelopment of CSA National Systems

Charges (DSC) • Modernize OSC Technology Platform

• Improve the Retail Investor Experience • Foster Inclusion and Diversity

and Protection

• Continue to Monitor and Adapt to the

• Continue to Expand Systemic Risk Impacts of the COVID-19 Pandemic.

Oversight

21 | P a g eYou can also read