Asia's automotive market updates and outlook

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Asia’s automotive market updates and outlook Dr. Marco H. Hecker | Chief Strategy Officer Deloitte China Automechanika, July 6th 2020

Global light vehicle sales headed for double-digit declines this year. Some Governments

have released major stimulus measures in an effort to boost vehicle demand.

Sales forecasts • Global light vehicle sales expected to be down by 22% in 2020

due to the spread of the COVID-19 virus, lockdown measures,

and a resulting slowdown in the global economy.

• Significantly higher decline than - 8% during 2008/09 fin. crisis

Global light vehicle sales

and growth (2019-2021F) Varying government stimulus packages :

Global sales % change •

Vehicle Units (Millions)

China: NEV subsidy; 0% NEV purchase tax are extended beyond

100 15% 2020; Delay of “China 6” until Jan 2021; lower auto finance

Annual % change

11.3% 10% down payment, lower interest rate as well as extended auto loan

90 5% terms; Encouragement to scrap 1 mil “China 3” (and older)

89.7 0% diesel trucks

80 -5%

-4.0% -10%

• Japan: USD1trn general stimulus- policies directed towards

78.0 businesses/ employment security. Earmarked $2.2 bn to help

70 -21.9% -15%

OEMs shift production from CN to stabilize supply chains

-20%

70.1

60 -25% • India: No direct Stimuli for Auto Sector. Gov. announced

2019 2020F 2021F packages for Micro, Small and Medium Enterprises. Tier2 and

some Tier 1 suppliers will benefit from the gov. soft loans. Also

EMI moratorium from March’20 till Aug’20 with “6 months

interest payment holiday”*)

Source: IHS Markit, Reuters *) interest will continue to accumulate

Copyright © 2020 Deloitte Development LLC. All rights reserved. Deloitte State of the Consumer Tracker 2

COVID-19 wreaks havoc on Asia’s automotive industry; the high uncertainty of

the pandemic signals demand will be slow to recover

2020 Monthly Vehicle1 Sales by Markets in k units Light Vehicles Sales Forecast (2018-2023) in mn units

-13%

Jan Feb Mar Apr May

27.1 24.8 25.9

China 1,927 2,070 2,194 21.5 23.4 24.7

1,430

310

2018 2019 2020E 2021E 2022E 2023E

-18%

581

Japan 360 430 5.2 5.1 4.2 4.5 4.6 4.6

270 218

2018 2019 2020E 2021E 2022E 2023E

India 338 310 278 -37%

156 4.0 3.5 3.1 3.4

2.7

0 2.2

2018 2019 2020E 2021E 2022E 2023E

AUS 56 62 61 -20%

27 42

1.1 1.0 0.8 0.9 0.9 1.0

2018 2019 2020E 2021E 2022E 2023E

349 338 292 -32%

SEA 134 154 3.4 3.4 3.0 3.3

2.3 2.7

Source: IHS Markit, Reuters *) interest will continue to accumulate. Note1: All types of vehicles;

IHS, CAAM, JAMA, FCAI, TAIA, TAIAI, MAA, LTA, VAMA, CAMPI, Deloitte research & analysis

2018 2019 2020E 2021E 2022E 2023E

Copyright © 2020 Deloitte Development LLC. All rights reserved. Deloitte State of the Consumer Tracker 3

Collective anxiety has started to ease in a majority of

global markets, but navigating the re-opening is critical. State of the Consumer Tracker

“I’m more anxious than I was last week” (Net Anxiety*)

India 31%

• Net consumer anxiety has receded across many

countries compared to the mid-April timeframe.

Chile* 20% One of the likely reasons is the cautious

Mexico* 5% reopening of economies .

Spain -2%

US -2%

• Some countries like India which have seen the

pandemic hit later than other countries continue

China -3% to show higher levels of net anxiety while

UK -4% countries that have relaxed their stay-at-home

Italy -5%

orders more widely have seen some reduction in

the overall level of consumer anxiety.

South Korea -5%

Poland* -5% • However, it remains to be seen whether this

Ireland* -7% trend will continue given a growing number of

Australia

medical officials pointing to the looming specter

-7%

of a second wave of virus.

France -11%

Canada -12%

Belgium* -13%

Japan -27%

Netherlands -30%

Germany -37%

-50% -40% -30% -20% -10% 0% 10% 20% 30% 40% 50%

Note: * Net anxiety = (% agree) – (% disagree); ** countries were not part of wave 1 fielding period.

Q3: To what extent do you agree or disagree with the following statements?

Copyright © 2020 Deloitte Development LLC. All rights reserved. Deloitte State of the Consumer Tracker 4Demand recovery in several markets may be stunted by

a consumer intention to keep existing vehicles longer. State of the Consumer Tracker

100%

90%

• Health concerns have largely

“I’m planning to keep my current vehicle longer kept consumers out of the

80% than I was originally expecting” (% agree) auto retail market for several

weeks.

70% =

• But, the prolonged global

economic shutdown is also

60% = starting to weigh on consumer

finances, causing many people

50%

to reconsider large purchases

going forward.

40%

30%

• At least half of the vehicle

owners in most countries are

planning to keep their current

20%

car longer than expected,

representing a significant

10%

challenge for automotive

manufacturers looking to

0%

IN CL PL CN MX IE ES KR JP AU IT FR US CA UK BE DE NL kickstart demand.

Wave 4 79% 64% 67% 61% 57% 56% 61% 55% 57% 56% 49% 48% 53% 44% 47% 39% 34%

• Also, when consumers return

Wave 5 82% 70% 65% 65% 63% 58% 56% 63% 48% 54% 56% 51% 47% 53% 45% 44% 40% 36% to the market, questions

Wave 6 76% 71% 68% 67% 62% 61% 60% 59% 55% 54% 53% 50% 50% 50% 49% 46% 45% 32% remain regarding the type of

vehicles people will buy (given

expected affordability

Note: Percentage of respondents who said “agree” or “strongly agree” have been added together. concerns).

Q3: To what extent do you agree or disagree with the following statements?

Copyright © 2020 Deloitte Development LLC. All rights reserved. Deloitte State of the Consumer Tracker 5Intent to delay vehicle maintenance is mixed as some

consumers divert spending to more immediate needs. State of the Consumer Tracker

100% • Along with concerns for their

long-term financial

90% “I’m putting off regular maintenance wellbeing, consumers are

80% for my vehicle” (% agree) also somewhat hesitant

regarding near-term

spending.

70%

60%

• Along with core questions

= around forward-looking

demand, this represents

50%

another key challenge facing

the automotive value chain,

40%

particularly dealers that rely

on their aftersales business

30%

for profitability.

20%

= • Having said that, there are

10% positive signals coming from

consumers in Europe,

0% Canada, Japan, and South

IN CN CL MX UK AU IT IE US ES FR CA DE KR PL BE NL JP Korea who are perhaps

Wave 4 63% 51% acknowledging the need to

42% 28% 32% 30% 33% 26% 30% 27% 28% 19% 20% 19% 18% 15% 12%

maintain their current vehicle

Wave 5 79% 43% 45% 41% 25% 30% 26% 29% 25% 28% 25% 26% 17% 22% 17% 17% 13% 13% (especially if they intend to

Wave 6 67% 50% 50% 41% 28% 28% 28% 27% 25% 25% 24% 23% 19% 18% 17% 17% 14% 12% keep it longer than

expected).

Note: Percentage of respondents who said “agree” or “strongly agree” have been added together.

Q3: To what extent do you agree or disagree with the following statements?

Copyright © 2020 Deloitte Development LLC. All rights reserved. Deloitte State of the Consumer Tracker 6Over the next 6 to 24 months, we can expect sectors to be impacted by COVID-19 and

experience the stages of the crisis cycle at different lengths and severity

Emerging perspectives on the Auto Sector in Asia Pacific

2020 2021

Apr May June Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May June Jul Aug

CN Resp

Recover Thrive

ond

KR Resp

Recover Thrive

ond

AU Respond Recover Thrive

NZ Respond Recover Thrive

IN Respond Recover Thrive

JP Respond Recover Thrive

SEA – Respond Recover Thrive

VN

SEA-

Respond Recover Thrive

IND

SEA-

Respond Recover Thrive

MY

SEA- Respond Recover Thrive

TH

SEA- Respond Recover Thrive

SG

Copyright © 2020 Deloitte Development LLC. All rights reserved. Deloitte State of the Consumer Tracker 7Highly capital/ labor intensive businesses with highly complex& globalized supply

chains are hindering OEMs to transform fast.

Domains:

Sample actions to address the emerging issues

1. Crisis

Accelerate growth opportunity

Workforce & Transf response &

Restructuring & Integration

Cost Control ormat Scaling Digital integrated

Business Marketing &

performance Supply Chain & Financial Management ion infrastructure planning

Customer & eCommerce

Workforce safety, wellbeing, policies & 2. Workforce &

communications Accelerated Cloud talent

migration

Adjusting customer 3. Liquidity &

Enabling the experience in a

business

Virtual Workforce COVID-19 world Review& upgrade continuity

Tech & digital

roadmap 4. Customer

Rapid Cost &

Supply Chain

interactions &

Working Capital

Control Visibility service mgmt.

Structural cost

Agile analytics & 5. End-to-end

Rapid Supplier Risk review supply chain

decision support

Assessment & Mobilisation

6. Technology &

digital

Strategic & Capital

Workforce scenario enablement

modelling & redesign Portfolio Review

7. Strategic

response,

RESPOND RECOVER REINVENT to THRIVE

Actions to address immediate & Actions to enable organisational recovery & adjust to Actions to position the organisation for post crisis scenarios &

short-term challenges scenarios demand & the ‘new normal

policy

Copyright © 2020 Deloitte Development LLC. All rights reserved. Deloitte State of the Consumer Tracker 8Due to changing customer requirements, growing competition& increasing availability

of data, OEMs are re-evaluating their business models to drive long-term growth

Double-click on retail trends

Observation on trends Sample opportunities

• High discount leading to 0% RoS • Adopt agency-based direct sales model

Sales, channel,

• Online offline integration trend • Seamlessly integrate online and offline

format strategy

• Separation of sales and aftersales • Develop new and innovative formats

• No differentiating experience/ service • Engage customers effectively across lifecycle

Customer journey

• Dealer organization not customer-centric • Re-organize dealer to enable “one-face”

& process

• Unable to obtain customer data • Re-design sales process

• Optimization opportunities brought by online • Phase out underperforming dealers

Network

• Changing consumption pattern • Re-structure network based on intra-city geo-analytics

restructure

• Inefficient network and sociodemographic analysis

• Competition from IAM • Centralize B&P services to improve efficiency

Aftersales • Revenue impact caused by BEV • Offer simple aftersales services in city center

• New network requirements due to sales innovation • Crate aftersales packages to lock-in customers

• UC market to grow at CAGR of 20% • Expand trade-in volume

Used Car & fleet • UC penetration lower by ~2x vs. mature countries • Re-design dealer KPIs to encourage UC business

• Mobility segment to grow ~16% p.a • Tailor products and services for 2B customers

• Market downturn leads to intense risk level

Dealer risk • Design risk identification model and classification rules

• Decreasing dealer profitability

management • Develop response strategy and mechanism

• Inadequate protocols to manage dealer risks

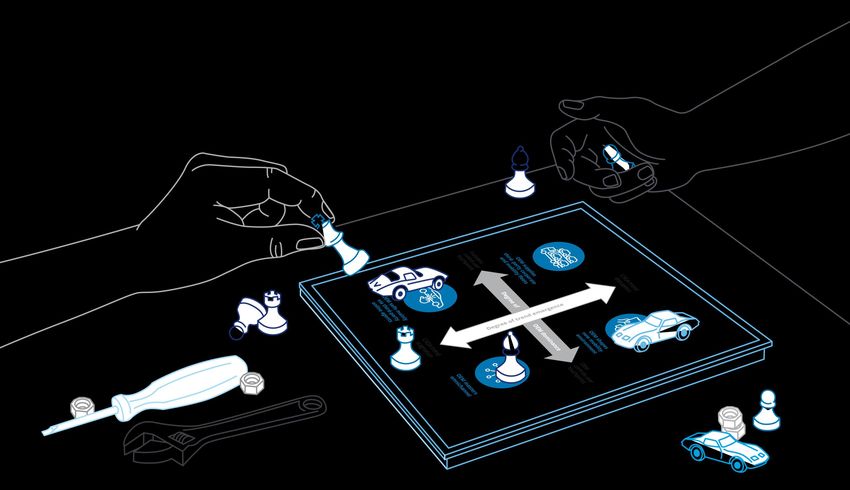

Copyright © 2020 Deloitte Development LLC. All rights reserved. Deloitte State of the Consumer Tracker 9Different future scenarios, require the modelling of specific strategic option spaces for

all players in the automotive value chain

Deloitte Study- Future of

Automotive Sales &

Aftersales | Impact of

current trends on OEM

revenues and profits until

2035

We present a differentiated

perspective of future industry

effects based on two scenarios

of trend emergence.

Beyond that, we distinguish

between two degrees of future

OEM dominance over the

competitive landscape, resulting

in four possible future states in

2035.

Future of Automotive Sales and Aftersales | Impact of current industry trends on OEM revenues and profits until 2035 10For any questions, or if you would like Scan the QR code to visit the

the link to the interactive Consumer global automotive thought

Tracker Dashboard, leadership collection on

Deloitte Insights:

please reach out to me directly:

Marco H. Hecker

Chief Strategy Officer Deloitte China

mhecker@Deloitte.com.hk

+852 616 99901

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and

their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not

provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the

“Deloitte” name in the United States and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of

public accounting. Please see www.deloitte.com/about to learn more about our global network of member firms.

Copyright © 2020 Deloitte Development LLC. All rights reserved.You can also read