Better Regulation COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre 7 July 2021 - Customer Owned Banking ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Australia as a Technology and Financial Centre

Submission 47

Better

Regulation

COBA submission to

Senate Select Committee on

Australia as a

Technology & Financial Centre

7 July 2021

Australia as a Technology and Financial Centre

Submission 47

Contents

Introduction 3

COBA Recommendations 4

Neobanks and customer owned banking sector have a lot in common 5

Banking market policy & operating environment 7

Regulatory compliance burden is imposing a python squeeze on competition 8

Better regulation & better regulatory policymaking 11

COBA’s Principles of Proportionate Regulation 11

Case study: No RIS for DDO expansion to consumer credit 12

Case study: Implementation of Royal Commission measures 14

Case study: APRA & software investment 15

Case study: Responsible Lending Obligations 16

Case study: Dual network debit cards 17

Case study: Implementation of the Consumer Data Right 18

Case study: Licensing neobanks 19

Appendix 20

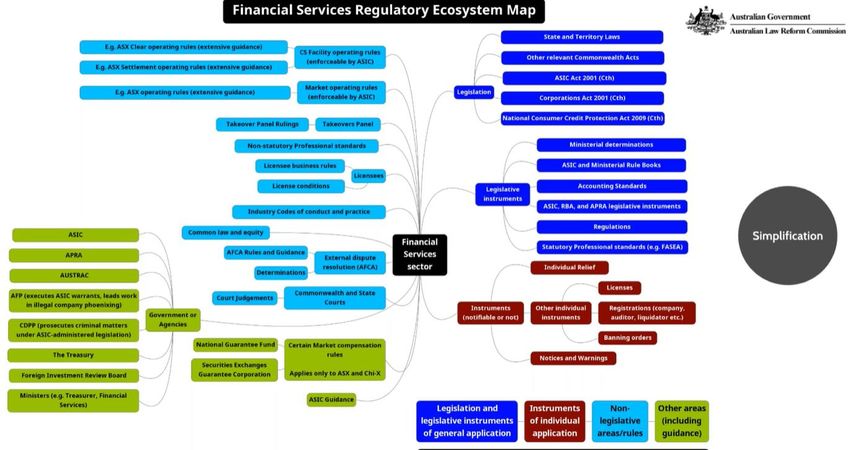

Figure 1: The complicated web of Financial Services regulation – ALRC 20

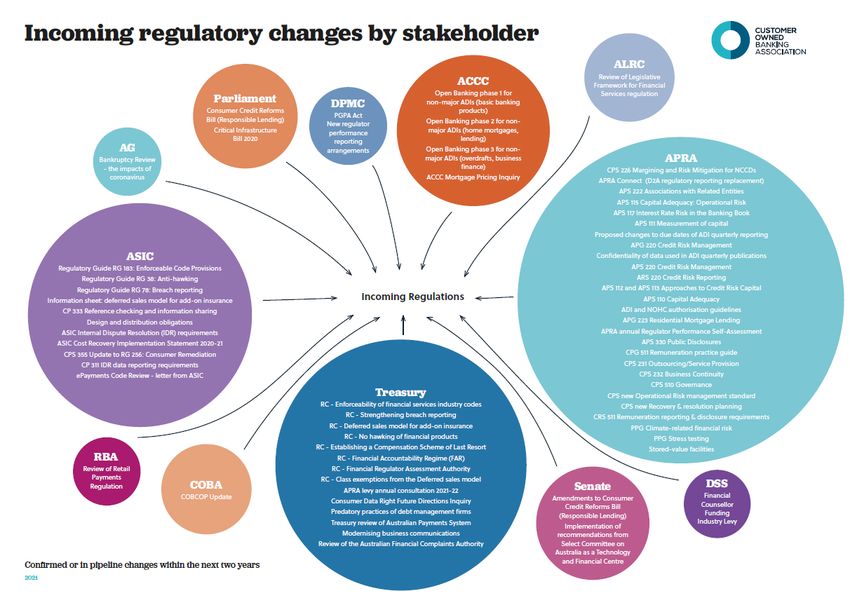

Figure 2: The incoming tsunami of regulatory change – COBA external product 21

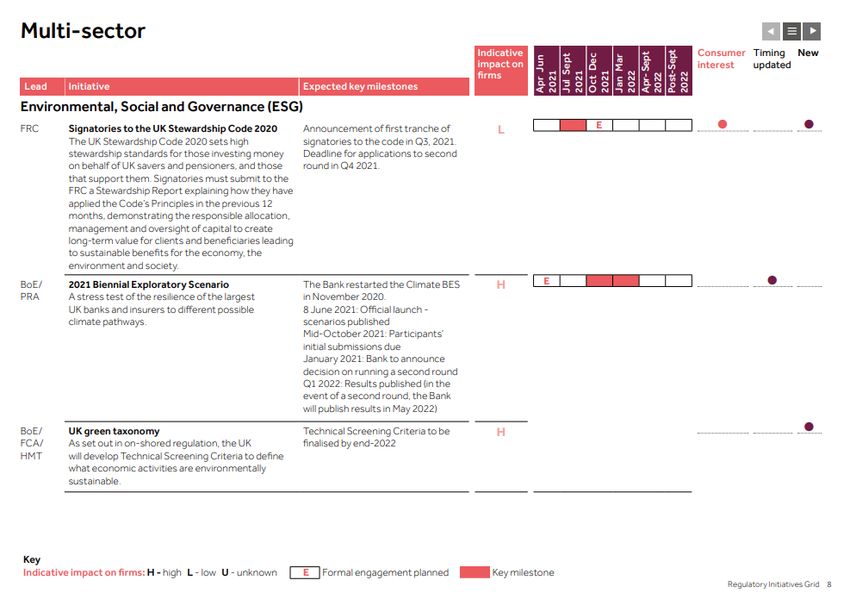

Figure 3: UK Regulatory Initiatives Grid Example – better practice regulator product 22

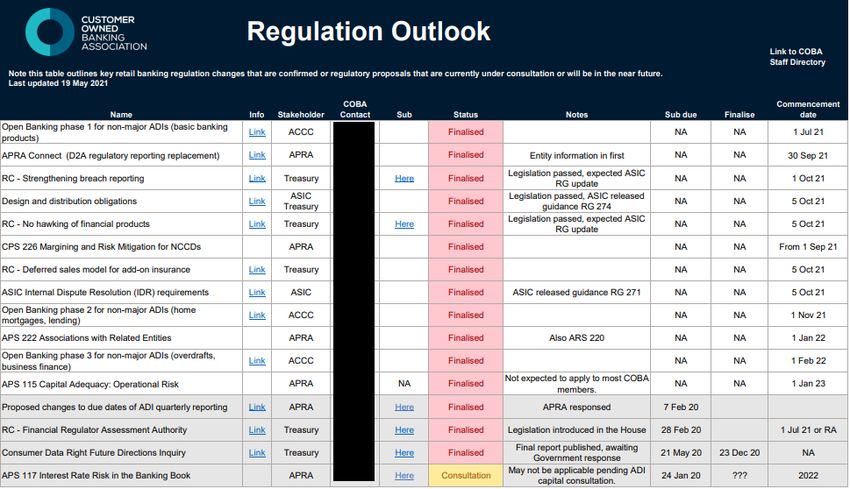

Figure 4: COBA Regulation Outlook – internal COBA member product 23

Customer Owned Banking Association Limited ABN 98 137 780 897

Customerownedbanking.asn.au

Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Introduction

The Customer Owned Banking Association (COBA) welcomes the opportunity to contribute to the

Committee’s inquiry, particularly addressing the policy environment facing neobanks and barriers to

the uptake of new technologies in the financial sector.

We support the Committee’s objective of enhancing competition in the banking sector. 1

COBA is the industry association for Australia’s customer owned banking institutions (mutual banks,

credit unions and building societies). Collectively, our sector has $147 billion in assets, around 10 per

cent of the household deposits market and more than 4.5 million customers. Customer owned banking

institutions deliver competition, choice and market leading levels of customer satisfaction in the retail

banking market.

Our sector’s main point of difference is our ownership model – our customers are also the owners of

our institutions. This model removes the motive to undertake the ‘profit before people’ behaviour

examined in the recent Banking Royal Commission. Our model better aligns the incentives of

customers and their bank and reduces the risk that the bank’s purpose will create issues that drive the

need for more regulation.

Key Points

New entrants to retail banking, such as neobanks, and existing challenger banks, such as customer

owned banks, are critical to applying competitive pressure to the major banks.

Neobanks and COBA members face the same regulatory and operating environment, i.e. an

established oligopoly, intensifying and expanding regulatory regimes, technology-driven shifts that are

fundamentally changing business models, consumer preferences and risks, and a margin squeeze

imposed by very low interest rates.

Policymakers and regulators need to recognise and respond to the impact on competition, innovation

and consumer choice of constantly ratcheting up regulatory compliance costs.

The increasing diversion of scarce resources away from customer service and innovation to meet new

compliance obligations hits challenger banks hardest and gifts a competitive advantage to major

banks. The ultimate losers from this entrenched trend are all banking customers who need a vibrant,

dynamic and innovative retail banking market.

The regulatory compliance burden is applying a python squeeze to competition in retail banking.

Policymakers and regulators must urgently change course, to deliver better regulation and better

regulatory policymaking.

____

1 Senate Select Committee Third Issues Paper

Customer Owned Banking Association Limited ABN 98 137 780 897 3

Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

We have provided a set of recommendations below that will improve the policy environment facing the

financial services sector, but particularly for neobanks and customer-owned banks given the burden of

regulation is much more acute for these institutions than their major bank peers.

Yours sincerely,

Michael Lawrence

Chief Executive Officer

COBA Recommendations

Recommendation 1

Pilot a regulatory initiatives grid like that seen in the United Kingdom to assist regulators and

policymakers to coordinate regulatory change and assist industry to plan and map out

responses for regulatory change. This would be developed in consultation with the financial

services sector.

Recommendation 2

Increase the coordination of regulatory initiatives at Council of Financial Regulators level to

minimise burden on industry.

Recommendation 3

Demonstrate a stronger commitment to adequately assess the impact of proposed regulatory

measures by consistent and rigorous application of Regulation Impact Statement (RIS)

processes.

Recommendation 4

Implement a program to systematically evaluate existing legislation and regulatory settings to

respond to changes in the regulatory environment and to reduce regulatory burden. Build in

post-implementation reviews for all major regulatory changes.

Recommendation 5

Address the cumulative burden of adding new layers of regulation by introducing a ‘one in, one

out’ approach, whereby any newly introduced burdens are offset by removing equivalent

burdens in the same policy areas.

Customer Owned Banking Association Limited ABN 98 137 780 897 4Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Neobanks and customer owned banking

sector have a lot in common

Critical point: Neobanks and customer owned banks have a lot in common as

challengers in a market dominated by major banks.

While there are many reasons customer owned banks are different to neobanks, neobanks and customer

owned banks have much in common as smaller scale challengers in a market dominated by major banks.

We exist in the same regulatory environment and generally share the same smaller size that limits our

access to economies of scale which makes regulatory compliance more acute than with our major bank

peers. However, like neobanks, this smaller size and challenger attitude makes us more agile in our ability

to deploy technology, evolve our business models and partner with fintech providers.

A neobank born of customer-owned banking

One of the first successful neobanks in the Australian market, 86 400, was created by key services

providers to the customer owned banking sector.

Neobank 86 400 was built by Cuscal2 and its core banking system was provided by Data Action 3. Cuscal

and Data Action were originally established to provide services exclusively to the customer owned banking

sector and their role in creating 86 400 reinforces the sector’s record of innovation. Both providers remain

connected to our sector as service providers and through our members’ ownership stakes in these

providers.

NAB’s acquisition of 86 400, announced in January 2021, is intended to “accelerate growth of NAB’s digital

bank UBank by combining its established customer base, brand and colleagues with 86 400’s experience

and technology platform.”4

A customer-owned bank creates a neobank

COBA member Teachers Mutual Bank Limited recently launched a new digital bank, Hiver, which it

describes as a new category of bank that combines digital banking technology and responsible investing

with the sustainable funds of a strong and respected industry player.

Hiver is targeted at essential workers, e.g. nurses, firefighters, paramedics and teachers.

“The introduction of Hiver to the banking landscape represents an exciting development in

customer-focused service delivery,” said Teachers Mutual Bank CEO Steve James. “As the first

digital mutual bank to hit the market, we are combining the best of new banking technology with the

financial security of a nine-billion-dollar balance sheet and a proven, ethical business model.”5

A customer-owned bank examines how to create more partnerships

COBA member Regional Australia Bank (RAB) is developing a strategy to compete in the Banking as a

Service (BaaS) space. A BaaS partnership allows a fintech to focus on its business strategy without having

to devote time and money to obtain a banking licence.

“The BaaS platform structure can prove incredibly useful for non-bank companies aspiring to

provide banking services,” RAB says. “The main benefit for a bank entering the BaaS ecosystem, is

____

2 Formerly the Credit Union Services Corporation (Australia) Limited

3 DA congratulates 86 400 on joining forces with UBank

4 NAB announces agreement to acquire 86 400 to accelerate UBank growth

5 Ethical, Digital, Mutual: New digital bank, “Hiver”, launches to meet the needs of Australia’s essential workers

Customer Owned Banking Association Limited ABN 98 137 780 897 Page 5 of 23Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

that it can establish solid relationships with fintech companies, fostering collaboration rather than

competition with the fintech sector.”6

RAB has a partnership agreement with a fintech firm - Douugh, run by SocietyOne co-founder Andy Taylor

- that is “developing a radically new banking model, centred around software that helps you achieve your

goals, live a happier life and achieve financial freedom.”7

"It's been very difficult and time consuming to find the right partner in Australia. We wanted to find someone

who respected our independence, shared our values and capable of supporting our ambitious product and

growth plans," Mr Taylor said.8

____

6 Regional Australia Bank statement provided to COBA.

7 Douugh website

8 Neobank Douugh wants to take HENRYs from the big four after Regional Australia Bank deal

Customer Owned Banking Association Limited ABN 98 137 780 897 6Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Banking market policy & operating

environment

Critical point: There is an opportunity for nimble customer owned banks to combine

the advantages of technology with their in-built, unmatched customer focus and

long-term perspective to enhance retail banking competition and innovation in a

digital environment.

The most recent major inquiry into competition in the financial system 9 described the banking market as an

“established oligopoly” where the four major banks hold substantial market power over their competitors

and consumers.

The market dominance of major banks, their sheer scale and brand recognition, coupled with significant

customer inertia, is difficult for smaller banks to overcome. This is despite the fact that, in many cases,

smaller bank product offerings are superior in pricing to the big four. 10

The current environment of very low interest rates not only hurts savers, it is harmful to banking

competition. The margin compression caused by very low rates hits smaller banks harder than the major

banks. This is due to smaller banks’ reliance on deposit funding.

Customer owned banking institutions gain access to economies of scale by outsourcing in areas such as

transaction, product and switching services, data processing, network and hosting services and core

banking and digital services.

In terms of investment in technology, regulator-driven investment requirements include cyber-security,

reporting and data analysis capacity, anti-money laundering and counter-terrorism finance (AML/CTF)

vigilance and Consumer Data Right (CDR) obligations, including expanding the CDR into payments. Market

and consumer-driven investment requirements include the need to update and replace legacy systems,

cost reduction, risk management, partnering capacity, application programming interfaces (APIs) and

robotics and meeting changing customer needs and expectations.

All banks are competing for scarce expertise in the information technology skills market. Australia’s biggest

bank, CBA, recently announced a major push “to hire hundreds of top-level software engineers as part of a

strategy to operate more like leading global tech companies and accelerate internal and customer-facing

digital transformation.”11

As APRA has recently observed, the customer owned sector has increased its market share over the

decade to 2020, while executing a “remarkable” degree of consolidation and delivering a significant

reduction in the sector’s cost to assets ratio. In terms of customer focus, the sector’s non-performing

housing loans ratio is less than half that of the major banks – 0.4 per cent compared to 0.9 per cent. This

reflects “the depth of understanding that mutuals have of their customers, and their ability to adhere to

sound lending practices.” 12

____

9 Competition in the Australian Financial System, Productivity Commission, 2018

10 APRA Chair Wayne Byres - Speech to COBA 2019, the Customer Owned Banking Convention

11 AFR: CBA hiring two engineers a day in digital transformation push

12Deputy Chair John Lonsdale - speech to Customer Owned Banking Association (COBA) 2021 CEO & Directors

Forum

Customer Owned Banking Association Limited ABN 98 137 780 897 7Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Regulatory compliance burden is imposing a

python squeeze on competition

Critical point: The increasing diversion of scarce resources away from customer

service and innovation to meet new compliance obligations hits challenger banks

hardest and gifts a competitive advantage to major banks. The ultimate losers from

this entrenched trend are all banking customers who need a vibrant, dynamic and

innovative retail banking market.

The growing regulatory compliance burden is imposing a python squeeze on competition.

Retail banking is highly regulated by multiple regulators with varying and sometimes overlapping mandates.

The customer owned banking sector is regulated by the same financial regulators as the major banks,

including but not limited to:

• APRA as banking regulator

• ASIC as consumer protection and conduct regulator

• RBA as payments system regulator

• Treasury as chief financial sector policy adviser

• AUSTRAC as financial money laundering and terrorism financing regulator, and

• ACCC as competition and CDR regulator.

The Financial Services Royal Commission observed that:

• given the existing breadth and complexity of the regulation of the financial services industry, adding

any new layer of law or regulation will add a new layer of compliance cost and complexity

• the existing law has rightly been described, in at least some respects, as labyrinthine and overly

detailed, and

• although regulatory complexity imposes burdens on business, the largest entities are very

sophisticated and well-resourced [and] are well able to find out what the law requires of them.

Regulation intended to benefit consumers can have the opposite effect by dampening competition,

dynamism and innovation.

The exponentially growing thicket of regulation creates so many tripwires for regulated entities, e.g.

procedural requirements and record-keeping obligations, that the risk of breaching these requirements is

more likely than actual consumer detriment from regulated entity conduct.

The existing breadth and complexity of the regulation of financial services has reached the point where it

has become necessary for the Government to create a ‘regulatory sandbox’ exemptions regime to

encourage and support the design and delivery of new financial and credit services that will benefit

consumers and businesses. “The regulatory sandbox will help overcome regulatory burdens and costs that

may hinder businesses in developing innovative offerings,” says the Explanatory Statement to the FinTech

Sandbox Regulations.13

The sheer scope of regulatory compliance is a challenge for all banking institutions. However, smaller

lenders are subject to relatively higher regulatory costs due to the fixed cost factor and this hampers their

capacity to grow and expand into new markets.

This view is not controversial. For example, the Explanatory Memorandum for a Bill currently before

Parliament, notes the impact of distorting resource allocation: “This one-size-fits-all process approach

____

13 Corporations (FinTech Sandbox Australian Financial Services Licence Exemption) Regulations 2020

Customer Owned Banking Association Limited ABN 98 137 780 897 8Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

further compounds competition issues, where large lenders have the economies of scale to more easily

overcome the costs of investing in systems to meet the process requirements.” 14

High regulatory costs hurt consumers because resources are diverted away from investment in product

innovation, better service and better pricing.

There is also the broader deadening effect on the economy’s dynamism of too much regulation. As noted

by the Reserve Bank Governor15, over the past 20 years as a society we have gone too far in the direction

of regulation as the solution to problems.

“We stop the downside through regulation, but the culture that's coming together with that

regulation is limiting the upside and the dynamism in the economy.

“I fear that over time we've erred too far in the direction of regulation.

“We want firms who are prepared to grow, to invest and to hire people—that's what I'm really

talking about—and to develop new products and new ways of doing things and to grow the

economy, because ultimately the economic growth delivers jobs and incomes to people, which is

what is important.”

It is critically important to acknowledge the opportunity cost of imposing new regulatory requirements that

force banks to divert scarce funds away from other priorities that are more relevant to their customers.

A decade ago, financial services regulation, while complex, did not have the same pace and volume of

regulatory change. While banking was subject to increasing consumer and prudential regulation, since then

a global financial crisis, various inquiries, a Royal Commission, exponential technological change and a

global pandemic have created wave after wave of regulatory change.

The depth and breadth of financial regulator mandates are relentlessly expanding. The expectations on

banks by regulators and other stakeholders only continue to grow.

While APRA is putting the finishing touches on its credit risk capital framework, i.e. ‘traditional’ banking

regulation, it is now also consulting on climate change guidance, increasing supervisory intensity on

cybersecurity, piloting new data collection methods and expanding its GCRA 16 work.

ASIC’s mandate is also expanding with continually increasing consumer protection regulation, piloting new

data reporting requirements and activity in the GCRA space as well. It is also expected to assume new

responsibilities under the upcoming Financial Accountability Regime.

The ACCC is now the regulator of Australia’s complex, new and continuously evolving CDR regime.

Regulators such as the RBA, ATO and AUSTRAC are also increasing their activity. The significant

community interest in financial services has led to a deluge of inquiries, each with their own set of potential

improvements to the system. Regulator mandates are increasingly starting to overlap into each other’s

jurisdiction such as in the GCRA and lending space.

____

14

National Consumer Credit Protection Amendment (Supporting Economic Recovery) Bill 2020, Explanatory

Memorandum, part 2.27

15 RBA Governor Philip Lowe, Hansard, Senate Select Committee on COVID-19, 28 May 2020

16 Governance, Culture, Remuneration and Accountability

Customer Owned Banking Association Limited ABN 98 137 780 897 9Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Increasing regulator resourcing – a proxy for regulatory change17

1,100

1,000

Average Staffing Level

900

800

700

600

500

APRA APRA ex-PHIAC Trend

Regulator staffing growth matches this ‘on paper’ growth in regulation. Regulators are getting more

resources and, consequently, regulated firms are spending more time interacting with regulators. The

information collected by regulators is increasing and will continue to increase with new technology. This

tsunami of regulatory change is increasing operational risk in financial services and regulatory change

programs now comprise a significant proportion of regulated entity’s investment budgets.

This sentiment is not just limited to smaller banks such as customer-owned banks. UK Finance states that:

“Even the best-resourced firms have only so much financial, technical and strategic capacity to deliver and

oversee change while managing the resilience of the system.”18 UK Finance represents the UK financial

services sector and counts globally significant banks amongst its membership – banks that dwarf

Australia’s major banks.

As noted above, this compulsory investment is crowding out funds that could also be used for customer

innovation, digital and growth initiatives. The ‘drop-dead dates’ for regulatory projects are pushing higher

value projects aside.

____

17Data from Treasury Portfolio Budget Statements. Note post-2016 adjusts for APRA’s acquisition of private health

insurance supervision (estimated 20 ASL)

18

UK Finance represents the UK financial services sector and counts globally significant banks amongst its

membership – banks that dwarf Australia’s major banks

Customer Owned Banking Association Limited ABN 98 137 780 897 10Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Better regulation & better regulatory

policymaking

Critical point: Policymakers and regulators must urgently change course, to deliver

better regulation and better regulatory policymaking.

The solution to addressing the regulatory compliance burden is ensuring there is better regulation and

better regulatory policymaking.

COBA welcomes measures that increase individual regulator accountability such as the revamped

Regulator Performance Guide. COBA applauds the passage of Government legislation to establish the

Financial Regulator Assessment Authority which will oversee the efficiency and effectiveness of APRA and

ASIC.19

While regulators are improving in their individual consideration of the impacts on regulated communities

and markets of their regulatory decisions, there is no big picture assessment of the impact of the cumulative

regulatory burden.

While improving regulator performance can increase efficiency and lower costs, ultimately it is the

legislative regimes that regulators must enforce that matter most. Suboptimal regulatory regimes bring

inefficiency and unnecessary costs. Shortcuts and haste in designing and legislating policy cannot be fixed

by improving regulator performance. The key is adequate assessment of the impact of proposed measures

and this requires consistent and rigorous application of Regulation Impact Statement (RIS) processes

informed by principles such as COBA’s Principles of Proportionate Regulation (see below).

COBA’s Principles of Proportionate Regulation

Our eight principles of Proportionate Regulation are:

1. Recognise that regulatory costs can affect competition and are ultimately borne by customers.

2. Avoid a one-size-fits-all approach to regulation.

3 Ensure regulation is tightly targeted at a clearly defined problem or regulatory objective and seek to

minimise regulatory costs.

4. Recognise the impact of the cumulative regulatory cost burden, particularly on smaller banking

institutions.

5. Positively consider banking institutions’ size, risk profile and complexity when designing and

implementing new regulation.

6. Allow smaller banking institutions at least 12 months extra time to comply with significant new

measures.

7. Recognise that for the same regulatory proposal, economies of scale could potentially result in

costs outweighing benefits for smaller banks but the benefits outweighing costs for larger banks.

8. Accommodate different models, such as the customer-owned model, particularly where the model

itself can mitigate risks that are otherwise addressed by regulation.

____

19 COBA Media Release - Regulator accountability back in focus but whole-of-system approach needed

Customer Owned Banking Association Limited ABN 98 137 780 897 11Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Various measures recommended by the Financial Services Royal Commission have been legislated

without a RIS. The Financial Sector Reform (Hayne Royal Commission Response) Bill 2020’s Explanatory

Memorandum states that: “The Financial Services Royal Commission Final Report has been certified as

being informed by a process and analysis equivalent to a Regulation Impact Statement for the purposes of

the Government decision to implement this reform.”

COBA does not agree that the Royal Commission report can be a substitute for a RIS. The legislation

introduced significant new obligations on banks in relation to breach reporting and new restrictions on

product sales and interactions with customers among other measures. The impact of these measures was

not subject to a RIS and the very substantial Bill, with its multiple schedules, was not even referred to a

Senate Committee for review.

The Government failed to provide a RIS for the extension of the design and distribution obligations (DDO)

to consumer credit. This was a massive expansion of the DDO regime that was not subject to a

consultation process. (See case study below: No RIS for DDO expansion to consumer credit.)

Case study: No RIS for DDO expansion to consumer credit

There was no public assessment or regulation impact statement done on expanding the DDO regime

at the last minute to cover home loans and other consumer credit products.

The amendments to expand the regime to include credit were rushed through under a guillotine –

debate in the Lower House on the amendments lasted about nine minutes, while debate in the

Senate lasted for about one minute. Despite the significant expansion in the scope of the DDO

regime effected by the amendments, no public consultation or cost-benefit analysis was undertaken.

It appears many MPs held the view that the amendments would operate to implement

recommendations made by the Financial Services Royal Commission. It is important to clarify that

Commissioner Hayne did not recommend this policy.

The Royal Commission Final Report noted: “The design and distribution powers do not now extend

to credit products. More significantly for present purposes, those powers do not extend to financial

products that are not regulated by the Corporations Act, but are regulated by Division 2 of Part 2 of

the ASIC Act. The product intervention powers have a broader reach, but nonetheless do not extend

to all ASIC Act products. It is not apparent why the powers should not extend, as ASIC has

requested, to all financial products and credit products within ASIC’s regulatory responsibility.”

Commissioner Hayne asked a question about whether there was a case to extend the DDO but did

not recommend that extension.

The Commissioner’s question is answered, in our view, by considering the genesis of the DDO, i.e.

the Financial System Inquiry (FSI) final report. The FSI, in supporting a DDO proposal, focussed on

addressing detrimental consumer outcomes from large scale financial investment failures, and poor

advice associated with complex financial products. There was absolutely no focus on credit products

or basic banking products.

Existing regulation of financial services is labyrinthine and complex (Figure 1 in Appendix) and there is a

high volume of new regulation scheduled for implementation or under development (Figure 2 in Appendix).

A whole-of-system approach to financial sector regulatory change is needed to ensure that any regulatory

change is proportionate, orderly and coordinated. This will reduce the impact that any necessary regulatory

change has on financial system competition and efficiency and on customers in terms of cost and

opportunity cost.

Regulators and policymakers as a collective must work together to ensure that this change is proportionate,

orderly and coordinated.

In the UK, this problem has been tackled through the introduction of the Financial Services Regulatory

Initiatives Forum and the Regulatory Initiatives Grid.

Customer Owned Banking Association Limited ABN 98 137 780 897 12Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

The forum brings together government and regulators, to provide industry with a forward-look of upcoming

regulatory initiatives. This forum comprises the Bank of England, Prudential Regulation Authority, Financial

Conduct Authority, Payment Systems Regulator and Competition and Markets Authority, with HM Treasury

as an observer member.20

Australia’s CFR already plays a similar role to the Forum. The CFR is the coordinating body for Australia's

main financial regulatory agencies. Our proposed whole of system approach to regulation clearly fits into

the CFR’s “effective and efficient regulation” objective. The most recent CFR quarterly statement outlines

that regulatory coordination is now an issue on the agenda. 21

As part of the Forum’s work, it has successfully piloted a Regulatory Initiatives Grid (“the Grid”) over the

COVID year (see Figure 3 in Appendix). The Grid sets out financial services regulators’ planned regulatory

workplan over the next two years in one document. The grid outlines key milestones for various financial

services regulation, supervisory and data initiatives. It also classifies them according to perceived

operational impact on firms and flags any that may be of interest to consumers. The Grid allows regulators

to better consider the cumulative impact and timing of regulation.

The Grid’s development has been an iterative process with financial sector stakeholders and continual calls

for feedback. For example, “In response to the feedback received in the Call for Evidence that

consultations, data requests and new requirements all contribute to the administrative burden on firms, the

Grid will include all publicly announced supervisory or policy initiatives that will, or may, have a significant

operational impact on firms.”

While COBA greatly appreciates recent moves by regulators and policymakers to increase transparency of

their workplans22, these individual workplans without demonstrated consideration of broader regulatory

change do not deliver the most efficient outcomes. COBA accepts that regulators do endeavour to

coordinate this change, e.g. via discussion at the CFR of big ticket items, but industry needs transparency

about this coordination.

COBA produces a Regulation Outlook document as an internal member product to assist our members to

navigate this change, particularly with respect to contributing to upcoming regulatory consultations (see

Figure 4 in Appendix), and many professional services firms and industry associations do the same.

However, while these products address the industry ‘roadmap’ need from a visibility perspective, they do

not address the need for greater regulatory and policymaker coordination. More broadly, the need for

greater regulatory coordination is not just an issue that impacts the entire financial services sector (see

ABA23 and ICA24 submissions on the Regulator Performance Guide).

Banks need adequate time to prepare to comply with new requirements and this time period starts at the

point the regime is finalised, i.e. once all legislated requirements, regulations, rules, standards and

guidance from regulators are settled and published. (See case study below: Implementation of Royal

Commission measures.)

____

20 UK 2020 Budget: Delivering on our promises for the British People, Page 100

21 Quarterly Statement by the Council of Financial Regulators – June 2021

22Example: see APRA’s Policy and Supervisory Priorities, ASIC’s Corporate Plan and Treasury’s Royal Commission

roadmap

23 ABA submission on Regulator Performance Guide

24 ICA submission on Regulator Performance Guide

Customer Owned Banking Association Limited ABN 98 137 780 897 13Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Case study: Implementation of Royal Commission measures

A number of new regulatory requirements flowing from Financial Services Royal Commission

recommendations commence in October 2021.

These measures were legislated in December 2020 but significant aspects of the regime have not

been settled as of late June 2021, i.e. only three months from the October 2021 commencement.

There is uncertainty about the scope and operation of the deferred sales model for add-on insurance,

the new anti-hawking regime and the new breach reporting regime. Regulations are needed to

deliver certainty.

Compliance obligations arising from these new regulatory requirements include changes to systems

and processes, policies and procedures, documentation, record-keeping and staff training.

Understanding and resourcing this compliance task requires budgeting and planning and this

requires adequate time.

Appearing before the House Economics Committee on 25 June 2021, the Insurance Council of

Australia noted that providers are at a “critical point” in preparing for the deferred sales model and

anti-hawking changes.25

“We are awaiting guidance and instructions from Treasury around how a number of these regulations

will finally be formulated. Once insurers have that information, members will be adjusting their

business operations accordingly to comply with the new rules…

“…it would be wise to have a review of these regulations in a fairly quick time period after their

implementation.”

Also appearing before the House Committee, IAG CEO Nick Hawkins said:

“We're making changes to how we offer insurance in line with a deferred sales model and anti-

hawking reforms, which will enable customers and potential customers to have the appropriate

information and sufficient time when deciding to buy insurance. We want to make sure, though, that

these reforms don't inadvertently intensify issues around underinsurance or non-insurance, and we're

working closely with Treasury, ASIC and the industry to ensure that that doesn't occur.”

In making regulatory decisions, policymakers and regulators often have to choose between objectives

which may not be perfectly aligned and may even compete.

Examples of this are APRA’s treatment of software investment in its regulatory capital framework and the

RBA’s approach to single-network debit cards versus dual-network debit cards.

COBA sought a change to APRA’s treatment of capitalised software expenses as a way to reduce barriers

to invest in software. Essentially, every dollar in software investment needs to be funded by an additional

dollar in regulatory capital (equity). This is a disincentive to invest in these types of assets given that capital

is a limited resource. Capital is critical for ADIs in today’s environment as it is needed to underpin the

additional loan growth to reach scale efficiencies or offset declines in the net interest margin.

In response, APRA said it agrees that investment in technology can support an ADI’s long-term resilience.

“However, APRA does not consider it appropriate to revise its requirement that intangible assets should be

deducted from CET1 capital.”26

COBA is asking APRA to keep this issue under review, given developments in Europe where banking

regulators are taking a less punitive approach. (See case study below: APRA & software investment)

____

25 Transcript - Australia's four major banks and other financial institutions: Insurance sector Proof

26 APRA Response to Submissions: APS 111 Capital Adequacy: Measurement of Capital

Customer Owned Banking Association Limited ABN 98 137 780 897 14Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

This is an example of the need for regulators to systematically evaluate regulatory settings to respond to

changes in the operating environment.

The European Commission’s Better Regulation agenda includes a Regulatory Fitness and Performance

Programme (REFIT)27 to strive for simplification and burden reduction by systematically evaluating existing

legislation.

The responsible lending obligations (RLOs) in the Credit Act provide a case study (see case study below:

Responsible Lending Obligations) of a regulatory regime that is obviously flawed but the Government’s

proposed approach to reforming the regime is opposed by various stakeholders because they fear a

reduction in consumer protection.

Case study: APRA & software investment

Investment in technology can improve resilience (e.g. managing cyber risk), efficiency and

competition in banking. The punitive capital treatment of software investment in the prudential

regulatory framework is a barrier to such investment.

Requiring ADIs to deduct software assets from Common Equity Tier 1 (CET1) suggests that such

assets hold no value when they could be the ADI’s most valuable assets. Currently, a piece of

furniture is given more value than critical software.

In order to reduce barriers to invest in software, COBA proposed that APRA should commit to

implementing a less punitive capital treatment for capitalised software expenses.

Essentially, every dollar in software investment needs to be funded by an additional dollar in

regulatory capital (equity). This is a disincentive to invest in these types of assets given that capital is

a limited resource. Capital is critical for ADIs in today’s environment as it is needed to underpin the

additional loan growth to reach scale efficiencies or offset declines in the net interest margin.

In the European Union, this problem has been recognised by banking regulatory policymakers. The

EU is working on new rules acknowledging that due to the evolution of the banking sector in the

digital environment, software is becoming a more important type of asset. The EU is proposing that

certain prudently valued software assets should not be subject to the deduction of intangible assets

from CET1 items.

COBA believes that a risk-weighted approach for software assets is more appropriate than

deduction. A more favourable treatment would act as a carrot to invest in these areas. COBA

members have noted that the current treatment limits their pace of investment in this area. It is in the

common interests of APRA, consumers and ADIs for ADIs to have competitive digital offerings and

up-to-date systems. A failure to provide more favourable treatment will also continue to give non-

ADIs a competitive advantage over ADIs.

Our submission suggested some options, should APRA wish to proceed cautiously.

In response28, APRA said:

“The submission noted that investment in technology can improve resilience, efficiency and

competition. The submission suggested that APRA should consider a threshold deduction approach

for capitalised software expenses, whereby the deduction only applies above a specified level.

“APRA agrees that investment in technology can support an ADI’s long-term resilience. However,

APRA does not consider it appropriate to revise its requirement that intangible assets should be

deducted from CET1 capital. Intangible assets, such as capitalised software expenses, can

automatically lose value as a result of the threat of or actual insolvency of an ADI. APRA does not

____

27 The European Union’s efforts to simplify legislation 2019: Annual Burden Survey

28 APRA Response to Submissions: APS 111 Capital Adequacy: Measurement of Capital

Customer Owned Banking Association Limited ABN 98 137 780 897 15Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

consider it prudent to include these assets within CET1 capital. A deduction approach to intangible

assets provides a prudent reflection of the capital that would be available in stressed conditions.”

Case study: Responsible Lending Obligations

The current responsible lending obligations (RLOs) in the National Consumer Credit Protection Act

(Credit Act) are not well drafted and have created a burdensome regime for lenders and borrowers.

As noted in the Explanatory Memorandum to the Government’s RLO reform Bill, the ASIC v Westpac

(Wagyu and Shiraz) case and the Financial Services Royal Commission created significant

uncertainty among credit providers around how to interpret and comply with RLO legislation and

regulation.”29

The scale of the regulatory risk posed to lenders (with consequent impacts on borrowers in terms of

cost and customer experience) by the RLOs was highlighted by ASIC’s September 2018

announcement that it had reached agreement with Westpac on a $35 million civil penalty for

breaching the RLOs. This agreement was rejected by the Federal Court and the subsequent court

action by ASIC against Westpac culminated in judgement against ASIC on 26 June 2020

Observations by the judges30 reinforce why there is such a strong case to simplify the consumer

credit regulatory regime. These observations include:

• the requirements are specific and detailed and contraventions are subject to very significant

penalties

• the regime imposes “prescriptive procedural obligations” on the credit provider

• “[If] Parliament intended to make it pellucid exactly what licensees needed to do before entering

into a credit contract, that effort miscarried”

• it is an “elaborate statutory regime”, and

• identifying the proper construction of key provision “is not straightforward” and “civil penalty

provisions should be interpreted on the basis that it is to be expected that an obligation imposed

would have been identified clearly and unambiguously.”

In ASIC’s September 2018 announcement of the $35 million civil penalty, ASIC Chair James Shipton

described it as a “very positive outcome and sends a strong regulatory message to industry that non-

compliance with the responsible lending obligations will not be tolerated.”

Since then, ASIC lost its case against Westpac on 26 June 2020 and later announced it would not

appeal.

A survey of COBA members in 201831 found that “responsible lending” requirements were ranked as

the most burdensome area of compliance, with participants concerned about the increasing depth of

information required before they can lend to customers.

Unnecessarily complex regulation can affect consumers directly, by creating inconvenience and

delay in lending decisions, but it also indirectly affects consumers by raising costs for all lenders and

these costs are ultimately borne by borrowers. A poor customer experience in obtaining credit may

deter the customer from switching in future, reducing competition and overall consumer benefit.

____

29

National Consumer Credit Protection Amendment (Supporting Economic Recovery) Bill 2020, Explanatory

Memorandum, part 2.13

30 Australian Securities and Investments Commission v Westpac Banking Corporation [2020] FCAFC 111

31 Grant Thornton, A case for proportionate regulation: The cost of compliance

Customer Owned Banking Association Limited ABN 98 137 780 897 16Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

In fact, since the introduction of RLOs into the Credit Act over ten years ago, a range of consumer

protection measures have been created or enhanced. New layers of consumer protection have been added

and regulatory compliance burden on lenders has increased without any consideration of the cumulative

impact of these new layers.

A solution to this problem would be to introduce a ‘one in, one out’ approach, whereby any newly

introduced burdens are offset by removing equivalent burdens in the same policy area.

Identifying regulation that is failing to meet objectives, that is creating unintended consequences or is

otherwise not fit for purpose could be achieved by more consistent use of post-implementation reviews.

Post implementation reviews will also lead to improvements in policymaking design and delivery.

As noted above, the RBA’s current review of retail payments regulation requires the regulator to decide

between competing objectives. Retail groups are demanding that the RBA should intervene in the market

by forcing all banks to issue dual network debit cards with the objective of improving the capacity of

retailers to lower their debit card payment transaction costs.

If the RBA did make such a regulatory intervention, it would remove choice and impose actual and

opportunity costs on banks, particularly small banks. Such an intervention would mean that small banks

would be offering a product based on factors other than their own commercial considerations and the needs

of their customers. (See case study below: Dual network debit cards.)

Case study: Dual network debit cards

The RBA is currently consulting on whether to make it mandatory for at least some ADIs to issue

dual network debit cards (DNDCs) rather than single network debit cards (SNDCs).

Retailer lobby groups are demanding “urgent regulatory action” to make issuance of DNDCs

“mandatory as part of every bank’s social obligations to promote competition in Australia.” 32

COBA members have expressed a strong desire for the issuance of DNDCs to remain a choice,

based on commercial considerations of the individual issuers and the needs of their customers.

The additional costs of supporting two networks can make it harder for small institutions to remain

competitive. While a majority of our members offer DNDCs and may choose to continue to do so, the

duplication in systems and compliance costs does impose a considerable burden on issuers with

relatively small portfolios. This applies to all COBA members, including our largest members.

Feedback from some members has suggested that while costs associated with dual network debit

cards are high, they still have appetite to issue these products based on the needs of their customer

base and the value to their business.

Importantly, if the RBA were to mandate issuance of DNDCs by all ADIs, this would reduce

incentives for schemes to innovate and improve their offering to attract new issuers and keep existing

issuers.

Better coordination among policymakers and regulators would improve decision-making in such cases

where competing objectives are in play.

As noted by APRA’s UK counterpart, prudential regulation can exhibit a ‘complexity problem’ when the

same requirements are applied to all firms.33

“This problem exists if the costs of understanding, interpreting, and operationalising prudential

requirements are higher relative to the associated public policy benefits for smaller firms than for

larger firms. Public policy benefits here means the contributions that prudential requirements make

to the safety and soundness of PRA-regulated firms. The complexity problem arises because there

are economies of scale to understanding, interpreting, and operationalising prudential

requirements, or because the factors driving smaller and larger firm distress are different, but the

____

32 Open Letter from Business Organisations Seeking Urgent Action on Debit Payments

33 PRA, A strong and simple prudential framework for non-systemic banks and building societies

Customer Owned Banking Association Limited ABN 98 137 780 897 17Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

requirements have been designed with larger firms in mind. This problem could have adverse

effects on PRA objectives because it could both reduce the resilience of small firms and diminish

effective competition.”

COBA supports action by APRA to tackle this problem in the Australian regulatory framework. APRA is

developing a simplified framework for smaller ADIs that is designed to deliver a material reduction in

regulatory burden.34

However, the complexity problem is not limited to prudential regulation. One of the most challenging

regulatory compliance projects for small ADIs has been implementing the CDR regime. This is a regulatory

change which at the same time is a significant technology transformation project.

Implementation of this project has been occurring against a backdrop of a global pandemic and many other

non-CDR regulatory change projects. This has proved challenging to all stakeholders, including banking

institutions, their key technology suppliers and the ACCC. (See case study below: Implementation of

Consumer Data Right.)

Case study: Implementation of the Consumer Data Right

The Consumer Data Right regime is novel, highly-technical, complex and elaborate, with multiple

regulators and multiple layers of requirements: legislation, rules and regulations, standards and

testing and onboarding processes. The sequencing and timing of the rules and standards has not

been optimal and late changes have been made to rules.

The three regulators (ACCC, OAIC and a Data Standards Body) administer:

• 110 pages of legislation, with a 92-page explanatory memorandum

• 127 pages of CDR rules, with a 69-page explanatory statement

• 203 pages of OAIC privacy safeguard guidelines

• data standards and customer experience standards and associated guidelines, and

• the Conformance Test Suite.

Banking institutions also must manage the interplay of their CDR obligations with their obligations

under APRA’s prudential standards, as AFSL and ACL holders, as reporting entities under AML/CTF,

as subscribers to the ePayments Code and as trusted providers of essential services to their

customers.

In March 2021, the Government shifted responsibility for CDR rule making and overall leadership of

the CDR program from the ACCC to Treasury. One of the objectives of this change was to support a

streamlined and unified approach to the development and implementation of CDR policy, rules and

standards.

____

34Deputy Chair John Lonsdale - speech to Customer Owned Banking Association (COBA) 2021 CEO & Directors

Forum

Customer Owned Banking Association Limited ABN 98 137 780 897 18Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Case study: Licensing neobanks

New entrants, alongside the growth of other challenger institutions such as customer owned banks,

are critical to applying competitive pressure in retail banking.

However, the likelihood of failure of a bank is higher during the early years of a bank’s development.

As noted by the UK Prudential Regulation Authority, factors which may lead new and growing banks

to fail include failure to obtain the required loss absorbing capacity or an inability to realise their

business model35.

“Many new and growing banks operate in highly competitive markets and many have novel and

untested business plans; this facilitates innovation and competition but not all may prove to be viable.

Coupled with this, new and growing banks may have fewer recovery options available to them than

established banks, meaning it is crucial they have the ability to exit the market in an orderly way, if

required.”

APRA has noted that there is no sign that the community is willing to accept a higher risk with their

deposits from new entrants.

“The community expects all banks to be very safe.”

“There are industries where start-ups can make a noticeable impact without having lots of capital or a

large balance sheet. To date, banking hasn’t been one of them. In simple terms: impact requires

growth, growth requires a balance sheet, a balance sheet requires capital, and depositor protection

requires plenty of capital. The mathematics of this are inescapable.” 36

APRA recently consulted on proposed revisions to its approach to licensing new entrant ADIs.

COBA supports APRA’s approach.

ADI licensing requirements should ensure the stability of the financial services industry through the

economic cycle. APRA’s Discussion Paper 37 adequately recognises this by stating that: “Sustainable

new entrants will provide more effective competition to incumbents than those which are perpetually

reliant on additional capital raises simply to meet ongoing prudential capital requirements.”

New entrants should be put in the best position to succeed, by becoming profitable institutions,

without having an undue regulatory advantage on established and proven business models. If a

neobank is unable to succeed, which recent evidence has shown happens, it needs to be able to

leave the industry in an orderly manner as to not impact other entities. The need to exit in an orderly

fashion means these ADIs must have sufficient recovery options that are tailored to the unique

circumstances of new ADIs. APRA has outlined improving recovery and resolution capabilities as

one of its key supervisory priorities 38 on APRA-regulated institutions. Given these requirements apply

to established ADIs, this must also apply to new entrants.

____

35Supervisory Statement - SS3/21 Non-systemic UK banks: The Prudential Regulation Authority’s approach to new

and growing banks April 2021

36

APRA General Manager, Regulatory Affairs and Licensing Melisande Waterford - Speech to the Future Banking

Forum 2019

37 Discussion Paper: APRA’s approach to new entrant authorised deposit-taking institutions

38 Information paper: APRA’s supervision priorities

Customer Owned Banking Association Limited ABN 98 137 780 897 19Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Appendix

Figure 1: The complicated web of Financial Services regulation – ALRC

Customer Owned Banking Association Limited ABN 98 137 780 897Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Figure 2: The incoming tsunami of regulatory change – COBA external product

Customer Owned Banking Association Limited ABN 98 137 780 897 21Australia as a Technology and Financial Centre

Submission 47

COBA submission to Senate Select Committee on Australia as a Technology & Financial Centre, 7 July 2021

Figure 3: UK Regulatory Initiatives Grid Example – better practice regulator product

Customer Owned Banking Association Limited ABN 98 137 780 897 22You can also read