Daily Grain / Livestock Marketing Outlook 7/6/2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Daily Grain / Livestock Marketing Outlook

Written by: Jim Gerlach

7/6/2021

Early Call 8:45am EDT: Corn down 5-10, soybeans down 10-15, wheat down 5-10.

Dow Jones futures are down modestly early Tuesday, trading close to unchanged with

European markets slightly lower to start the week. Other than a Markit PMI reading,

there are few economic reports early on Tuesday, with Wednesday looking at jobs

openings and the Federal Open Market Committee (FOMC) minutes. OPEC and major

oil producing countries failed to reach an agreement on the possible increase in

production, with an impasse between Saudi Arabia and the United Arab Emirates

(UAE). As a result, August crude oil was trading around $76 per barrel. Grain futures

are set for a hard open (no overnight trade) coming out of the 3-day weekend, with more

rain forecast for the drier areas of the Midwest and northern Plains than was indicated

on Friday.

Grains: Wheat for September delivery fell 1.9% to $6.52 ¾ on the Chicago Board of

Trade on Friday, in anticipation of rainfall arriving in the northern Plains over the

course of the holiday weekend. Corn for December delivery fell 1.6% to $5.79 ¾, while

soybeans for November delivery rose 0.3% at $13.99. Weather forecasts predict more

rainfall in parched northern Plains growing areas, where wheat is the primary crop being

hurt by drought conditions. The weather forecasts on a Friday before a weekend are

usually ignored, even more so when it is in front of long weekend, but the GFS Friday

morning put rains back in the forecast for Minnesota and eastern North Dakota.

However, this rain may be too late to salvage a crop that was assessed nationally at 20%

good-or-excellent condition last week. Outside of U.S. weather forecasts, grain traders

found other reasons to step away from corn futures. Among them was a decision by the

D.C. Court of Appeals to vacate a Trump administration-era rule lifting restrictions on

selling E15 gasoline in the summer, as well as frost hitting Brazilian crops coming to an

end. Hot and dry conditions are expected by the grain markets in the latter half of July,

but grain traders are questioning if the weather will be enough to send prices back to

near-record levels. Can a rally be sustained after the extended 4th of July weekend? I

continue to remain in the camp that believes we have already seen our summer highs,

but one has to suspect, bulls will try their best to prove that wrong in the weeks yet

1

ahead and we could see new highs post-harvest. Rainfall is expected in many areas over

the long weekend, but soil moisture in the northern Plains remains dangerously low.

Showers were limited to the southern Delta for much of the weekend but scattered into

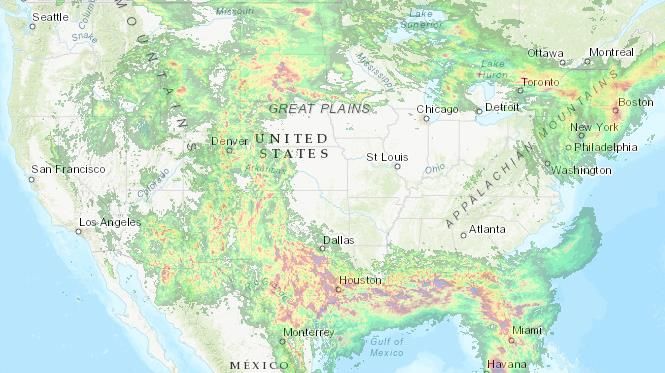

southern/northeast ND and SD the past day (see left map). Rains mainly focus on the far

northern Midwest the next 2 days but expand by Friday and remain active into next

week (see 7-day NOAA forecast map right). Drier patches will be limited to 10-15% of

the Corn Belt mainly near the NE/IA border and ND, with even wetter model risks the

next 10 days. Showers through Friday and early next week also limit short-term stress to

about ½ of the northern Plains and Canadian Prairies wheat/canola belt the next 10 days.

Mid 90s in parts of the northwest Midwest occurred over the weekend, with 100s in the

northern Plains and Saskatchewan. Heat now stays west of the corn belt. Recent wetness

in the southern Plains moderates the next 2 weeks, easing quality concerns and late

winter wheat harvest delays. Only minor Southeast flooding occurs at mid-week from

Tropical Storm Elsa, while earlier wetness slows drying in the lower MS Valley.

A third day of frost in Sao Paulo corn fields led to some private Brazilian firms citing a

6mmt production loss. Analytical firm Ag Rural dropped Brazil's total corn crop to just

85.3mmt, the lowest we have seen and 13.2mmt below the riduculous June USDA

production number of 98.5mmt. Analytical firm Rural Clima pegged the national 2nd

crop at less than 60mmt from their previous 62-65mmt expectations. CONAB had their

June estimate at 69.96mmt for Brazil’s 2nd crop and 96.4mmt for 2020/21’s total output.

Stone X figures Brazilian corn output will total 87.93mmt. That is down by 1.75mmt

from their previous estimate. The USDA ag attache to China sees this year’s corn crop

at 272mmt, above USDA at 268mmt and up from 261mmt last year, citing a 5.2 million

acre (6.2%) increase in planted area due to high price and government mandates to

increase corn acreage. The attache sees imports at 20.0mmt vs. USDA at 26.0mmt, with

old crop imports at 28.0mmt vs. USDA at 26.0mmt. China currently has 10.7mmt of

new crop U.S. corn on the books and an unknown amount of Ukrainian corn. The

attache sees new crop feed usage at 211mmt, in line with USDA and up from this year’s

2

196mmt (USDA 206mmt) with restocking of hogs contributing to demand while citing

about 40mmt of corn feed demand displaced in 2020/21 with alternative products. The

attache sees industrial demand remaining fairly weak given high prices as both the

ethanol and starch industries have suffered. Total FSI usage is estimated at 87mmt,

unchanged from this year but 4mmt higher than USDA in both years. The attache sees

2021/22 Chinese soybean imports at 102mmt vs. USDA at 103mmt, rising only slightly

from this year’s 100.0mmt. This year’s soybean crop is estimated at 17.5mmt by the

attache vs. USDA at 19.0mmt with area down due to higher corn acreage. I think the

attache is 2-4mmt too low for soybean imports.

This afternoon’s 6th national corn rating is expected to clock in at 65% good/excellent

vs. 64% last week and 68.6% average. The 5th national soy rating is expected to clock in

at 61% good/excellent vs. 60% last week and 66.6% average. The HRS rating is

expected at 23% good/excellent vs. 25% last week and 66% average. Following the late

week swoon in corn prices last week related to some talk of a Supreme Court ruling in

favor of a renewal of exemptions for some small oil refiners, corn is expected to again

open lower. Some weekend rains fell in the Canadian Prairies, and some storms are

rolling across the drought-stricken northern Plains early on Tuesday. The 10-day

weather forecast appears to show the potential for another two to three inches of rain

across the northern Corn Belt and Canadian Prairies. Some would argue it's much too

little and much too late. In the absence of Sunday or Monday night trade, futures are

expected to open lower Tuesday morning. Brazil has now harvested 12% of their

safrinha corn crop compared to 23% a year ago. However, after last week's freeze event,

production estimates for Brazil's safrinha (winter) corn crop continues to plunge. In the

U.S., any moisture is likely to help with the drought monitor now showing 100% of the

Dakotas in some form of drought, with Minnesota at 97%, and even Iowa now 75%

covered in drought. Nebraska and Iowa continue to trend drier. Nebraska has been the

highest rated of the major corn states, but that is likely to change on Tuesday's crop

progress report.

Soybean futures are likewise expected to open a bit lower to start Tuesday trade, but

finished modestly higher to end last week. After closing higher for five straight days and

up nearly 8% last week, palm oil futures are trading lower to begin the week. Canadian

canola futures on Monday fell C$29.50 and are down over C$20 early on Tuesday

following ten consecutive higher closes as weekend rains and the promise of more could

help that crop, which has suffered from high heat and dryness. Soybean oil futures had

rallied late last week but are also expected to be down to start, although the surging

crude oil market could limit any losses. Subsoil reserves remain extremely short in the

Dakotas, Minnesota, and now 50% of Iowa. While rumors of new crop China demand

for beans have circulated, we have seen no confirmation of that yet. Brazil's exports are

3

slowing down with the basis rising, and U.S. soybeans are becoming much more

competitive in August than several weeks ago, when the price spread was over $1.00

per bushel. November soybeans are coming off a week where futures rose by nearly

$1.30 per bushel on tightening stocks, solid demand and big gains in world veg oil

markets.

Last week saw the biggest weekly gain in corn prices in a decade based on the 2-4mmt

estimated Brazilian corn crop loss due to a hard freeze and the lower-than-expected rise

in U.S. corn acreage. The market is aware that nearly all the gain in corn seeding

occurred in the northern Plains and Minnesota (1.2 million of the 1.5 million gain),

where the crop is a growing risk of drought losses due to acute stress. As we move past

the 4th of July, it’s important to reiterate why it’s so hard to break drought as we move

later into summer. Remember that corn moisture needs increase dramatically heading

into and beyond pollination with the weekly draw at nearly 1.75”. Last week’s U.S.

Drought Monitor map showed topsoil short-very short across 90% of SD, 66% of ND

and 75% of MN, which is less than required for normal plant development. USDA

reported that 38% of U.S. corn is experiencing drought, which is down from 41% last

week but still up from 24% on June 1st. Thus, when you see a forecast for scattered .25-

.75” rainfall, you’re still going backwards regarding available moisture to corn crops.

Crop condition ratings will likely continue to drop across the northern Plains and WCB

in this afternoon’s weekly condition report as rainfall in the past week has been limited.

The below normal rainfall and warming temperature trend will stress corn/soybeans in

the drought areas of the northern Plains and the WCB where top and subsoil moisture is

short to very short.

The seasonal pattern for corn futures typically results in prices eroding into the fall

harvest period and with the rainfall over the weekend and forecasts for more in the drier

areas of the northern Corn Belt and northern Plains, I’m starting to think more and more

that we’ve reached a summer peak. Post-harvest, if demand isn’t being rationed or if

U.S. yields don’t live up to expectations, we could see prices push to new highs. The

current strength in grains and oilseeds may have started with weather-related crop issues

last year, which affected corn, soybeans, wheat, barley, palm oil, sun seed and rapeseed

in important growing areas in the U.S., South America, Europe and Asia. But it is

unrelenting demand that has sustained the drive, with growing interest in biodiesel in

Malaysia, Indonesia, Europe and the U.S and China’s unprecedented feed grain imports.

China’s corn stock-to-use ratio fell from an estimated 99% to 36% in five years as the

government shrank its temporary reserves. Rapid recovery of commercial hog

production following the African Swine fever outbreak promises continued strong feed

demand. As the hog recovery is a multi-year process and China’s grain production is

difficult to scale quickly, high feed grain imports, as well as continued rising soybean

4imports, over the next years are to be expected. Globally, corn is in its fourth year of

deficit and won’t replenish much in 2021 as of mid-June, 35-40% of U.S. corn acreage

was in regions affected by some level of drought. We now have multi-year low

inventories of multiple commodities in key export countries, including the U.S., with

U.S. inventories of corn, wheat and soybeans are at seven-year lows. Add production

risk, difficult-to-ration demand and fund interest in these commodities and we can

expect elevated and volatile, prices well into 2022. Recent high-price periods lasted one

to two years (2004 and 2008) or three to four years (2011-14). Should crops disappoint

in 2021, prices likely would soar to all-time highs and remain elevated for three to four

years. Normal global crops in 2021 would provide cooling off of prices, but concern

would carry over into 2022. Perfect global production this year would pressure prices,

but even then, not to the levels seen in 2015-19. Time will tell.

On the demand front, palm oil prices fell 0.8% in late trading. While demand for the oil

could remain supported thanks to its wide price discount to rival soy oil, this could be

offset by concerns of weaker demand from Covid-19-hit countries, CGS-CIMB says.

The brokerage also expects Malaysia's palm oil inventory to have risen 3% on month in

June, bucking historical trends. Malaysia's supply of palm oil has declined by an

average of 2.2% in the past 10 years, it notes. On China's Dalian exchange, September

corn is down 0.2%, September soybeans are down 1%, September soybean meal is

down 1% and September soybean oil was up 0.5%. China’s planned auction of

156,000mt of imported U.S./Ukrainian corn from state reserves only saw 28,000mt sold

as interest is low due to competing feed grain supplies. Overall demand for corn was

said to be weak at the moment, with end users able to wait for cheaper new crop

domestic supplies to become available. Amid reports that China has almost completed

its rebuild of its hog herd to pre-ASF levels, the USDA's Foreign Agricultural Service

says that the U.S. will export more corn to China in the current marketing year than

previously expected totaling 28mmt (USDA at 26mmt). Meanwhile, earlier last week,

the FAS reported that U.S. soybean exports sold to China hit $7.7 billion in the first

quarter, nearly a record. Looking ahead, China likely aims to import less U.S. grains,

but the cut looks to be mild. It's a reasonable assumption that increased wheat feeding

and high global prices will slow Chinese corn acquisitions in the year ahead, although it

will still face a longer-term problem of balancing supply and demand. For the first time

in 11 trading sessions, November canola futures closed lower on Monday, finishing

down nearly $30/mt and are lower again Tuesday. Egypt's state grain buyer purchased

180,000mt of Romanian wheat and 60,000mt of Russian wheat at an international

tender Monday for shipment between Sep 1-15. A D.C. Circuit Court of Appeals

reversed a 2019 EPA ruling that removed the restrictions on E15 sales. With the court’s

reversal decision, the RVP waivers will no longer apply to year-round sales of E15

blend. E15 fuel can still be sold during the summer but will require special waivers.

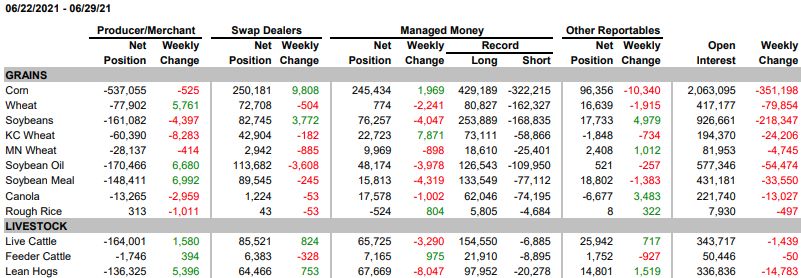

5Friday’s CFTC report showed

that funds were seen at 254,434

contracts net long as of Tuesday

the 29th. CFTC data suggests

that came via a week of pre

report buying, with 4,177 new

longs opened and 2,208 new

shorts. Commercial open interest dropped 11.9% through the week. The report showed

soybean spec traders reduced their net short by 4,047 contracts through the week that

ended 6/29. That was brought about by a week of net new selling ahead of the report,

though the group was still 76,257 contracts net long going in. CFTC data showed the

commercials reduced exposure going into the report, as open interest dropped 123,345

contracts. Commercials were still 161,082 contracts net short as of 6/29. The

Commitment of Traders data release had managed money at 774 contracts net long in

SRW as of 6/29. That was 2,241 contracts less net long from the prior week. For HRW,

the weekly update showed managed money was covering shorts, driving their net long

7,871 contracts stronger to 22,723. The CFTC report showed spec traders were 9,969

contracts net long in spring wheat as of 6/29. That was a weekly drop of 898 contracts.

The combined 5 market ag long was down 13,000 contracts to 386,000, the lowest since

mid-Sept 2020. Soybean oil was less long than expected.

Livestock: Cash hogs are called higher. As the market dives into this week's trade

coming off the hype of the long holiday weekend, one would assume that packers would

be aggressive in their purchases as coolers need restocked. USDA’s National Average

base hog price for Friday was $108.21, down by $1.18. The CME Lean Hog Index for

6/29 was another $0.82 lower at $112.18. The weekly Commitment of Traders report

showed lean hog spec traders were 8,047 contracts less net long to 67,669 contracts as

of 6/29. That was mainly long liquidation with a 7,763 fund open interest. Pork cutout

futures fell triple digits past July. July contracts themselves were $1.92 stronger to

$115.20. USDA’s National Pork Carcass Cutout Value for Friday afternoon was $.44

weaker at $115.19 on low movement of 253 loads. Weekly kill was down 3.26% vs. last

week but up 11.92% vs. last year.

For the week, July lean hogs were up $6.70 and August lean hogs were up $0.45. Lean

hog contracts rounded out the week mostly higher, except for the August and October

2021 contracts. July lean hogs closed $1.35 higher at $108.65, August lean hogs closed

$0.07 lower at $100.22 and October lean hogs closed $0.17 lower at $84.70. Hog

futures tried to rally last week, but only the July contract was able to post a sold gain

and hold it. The reason is that July has only about a week remaining to trade and it need

6to converge and remain close to cash, and that is where it is. Traders may be cautious to

begin the week as they may wait and see how the cash market will develop before they

become more active. The market could find some support this week as packers will need

to procure hogs and coolers will need replenished after the holiday festivities. Packers

have slowed their processing levels as margins become less and less favorable but

gauging where they intend to run will become clearer next week as the market settles

down into a normal schedule again. While it is becoming quite clear that Chinese

demand for U.S. pork is waning, I believe this will be more of a temporary blip as

Chinese herd liquidation appears to have run its course now that the government is

buying pork to refill freezers. China has a long history of major peaks/valleys of herd

expansion/liquidation and this bout of liquidation will likely mean pork shortages again

by late 2021/early 2022. China’s national average spot pig price Friday was down

0.89% but finished up a whopping 23.44% for the week but remains down 53.6% year

to date. Dalian live hog futures lost 3.5% on Friday. While China was not very active in

last week’s U.S. export sales (5th largest buyer), cumulative sales of 2021 have reached

1.163mmt, down from 1.214mmt last year but still the second strongest in history vs.

the 5-year average of 880,934mt.

For the week, August live cattle were down $0.80, October live cattle were down $0.33,

August feeder cattle were down $2.50 and September feeder cattle were down $1.82.

The live cattle contracts couldn't find any last-minute support from traders before

Friday's whistle blew. But even more disappointing was to see another day of thin

movement of cash cattle trade this week. August live cattle closed $1.57 lower at

$122.00, October live cattle closed $1.17 lower at $128.07 and December live cattle

closed $0.42 lower at $132.77. Based on Friday's afternoon sales, the week's movement

of cash cattle only totaled 60,537 head. On a holiday week that's not terrible, but when

last week's trade only amounted to a measly 48,965 head, the market was hoping to see

better demand last week to make up for the prior week's disappointment. Looking to this

week's trade, the market will see total kill numbers very similar to this week's estimates

as Monday will be reduced significantly. With the Fourth of July landing on a Sunday

this year, the market doesn't have just one week of holiday oddity to deal with, but

rather two weeks where trade could be compromised. Packers could be enticed to run

vigorous kill speeds next week, though, as retailers look to restock their coolers and

replenish inventory. Friday's slaughter is estimated at 113,000 head, 3,000 head fewer

than a week ago and 6,000 head more than a year ago. Saturday's kill is projected to be

around 33,000 head. Last week's total slaughter is estimated at 623,000 head, 42,000

head more than the same week a year ago. Boxed beef prices closed lower, with choice

down $2.21 ($285.44) and select down $2.52 ($264.41) with a movement of 103 loads.

Throughout the week, choice cuts averaged $290.83 (down $21.84 from last week's

average), and select cuts averaged $268.99 (down $8.80 from last week's average). The

7week's total movement of cuts, grinds and trim totaled 648 loads. Cash is called higher.

After two weeks of light cash cattle trade, the market should see more interest from

packers. The feeder cattle contracts jumped with joy and saw an opportunity in Friday's

thin market as the corn complex waned lower once again. It was especially refreshing

for the market to see the spot July contract trade lower even though it’s set to expire in

less than two weeks. The other corn contracts are all trading below $6 a bushel, but the

spot July contract is continuing to dance close to the $7 line. August feeders closed

$0.72 higher at $157.05, September feeders closed $0.35 higher at $159.42 and October

feeders closed $0.40 higher at $161.47.

Noted livestock analyst Dennis Smith, who correctly called for a summer hog top of

$120 back in February, is suggesting hog producers hedge up and I strongly concur. The

top in lean hog futures occurred roughly in tandem with the expiration of the June lean

hog contract in the middle of June. While the bullish fundamental of tight hog supplies

and sharply lower hog weights remains intact, bearish forces have emerged and

encouraged the selling. Bearish forces at play include the expectation that exports are

beginning to slow, pushback by consumers and retailers to rapidly rising prices, the

competition of food service re-stocking and the recent court ruling that allows the new

inspection rules to go into effect forcing packers to slow the chain speed. Another

bearish force at work is Prop 12 out of California dictating that only pork raised under

“their specified conditions” be allowed to enter the state. As ridiculous as this seems,

the weak lobby effort on behalf of the nation’s pork producers has allowed this to

become law. Worse yet, the industry has failed to comply to the specs. So, starting

January 1, 2022, the state of California will be mostly without any pork available to

residents of the state and the rest of the nation will have 15% more pork to absorb.

Painfully, the U.S. producer will bear the burden. The victory by the trade unions in

forcing the slowing of the chain speed, in effect, reduces the capacity of the industry by

around 3-5%. Producers should all work together and keep contraction of the herd

intact, reducing total tonnage and preventing the supply of hogs from ever exceeding

capacity. Let the U.S. consumer pay the bill of the union victory. The trade union deal is

totally out of the control of all U.S. hog producers. The Prop 12 rule is not totally out of

the producer’s control. The industry could confirm and meet the standards. Thus far,

however, I’m not aware of any concentrated effort to do so. The rise and fall of exports

is also completely out of control of hog producers. The weather is also out of anyone’s

control. Did you ever get the sick feeling that you have very little control of your future?

So, now that the spaceship ride is complete, it’s time to make a concerted effort at

controlling those variables which you can control. Have you locked in feed costs for a

large portion of your needs for the rest of 2021? Assuming the board is profitable, are

you preparing to lock in profits for a portion of your production for the remainder of the

8year? How about other input costs such as propane, fuel, etc. Lock them up. I’m

anticipating a seasonal high timing into the middle of July. The tops are likely already

in place. However, a secondary rally may occur into the high timing, allowing the

educated producer to lock in profits. Finally, the situation around the world remains

highly uncertain. African swine fever continues to spread in China. However, according

to the Chinese, they’ve been highly successful in re-building, very rapidly, their hog

herd. Lower hog and pork prices would tend to confirm this information provided by the

Chinese government. However, things are not always as they appear, especially when

dealing with the Chinese. What are the odds that they’ve mastered this disease in as

little as two years? While not in the news recently, be aware that ASF continues to

spread in Europe. This situation is not finished; it’s not run its course. If it’s ever

detected in a commercial herd in Germany, a major disruption will occur. On Thursday,

July 1, rumors surfaced of a possible case of ASF on U.S. soil. It was never confirmed.

Extreme uncertainty merits hedging. Let someone else assume the risk.

Dr. Dave Pyburn, Chief Veterinarian with the National Pork Board, discussed the spread

of African Swine Fever (ASF) at World Pork Expo. He wants U.S. producers to know

that ASF is still a high risk. Transmission of ASF may have lessened over the last year,

but that is because international travel has been reduced significantly, not because of a

lessened amount of virus. ASF is still on the advance in parts of Europe and Asia.

“We've seen recently an outbreak on a large new farm in Poland, in the northern part of

the country,” said Pyburn. “It’s along the river that borders Germany, so it’s a threat to

new areas within Germany, where they continue to find feral swine positives. ASF is

also still on the advance in the Philippines and China.” The National Pork Board has

consulted with veterinarians who are traveling into China or are stationed in China long-

term, and they’ve been told that ASF continues to kill many pigs there. Some in China

have created vaccines to prevent the spread of ASF. These vaccines are known to still

transmit ASF but prevent pig death which is perhaps exacerbating the situation. These

vaccines allow the pigs to survive ASF, they also pass the disease even farther to

different populations, making the situation significantly worse. The National Pork

Board has also learned that there’s more than one variant strain in China. “I've talked to

one veterinarian in China who runs his own lab, and he's isolating the virus to detect

variants,” said Pyburn. “He has clients come in and say, ‘I know I've got ASF because

of what I see in the pigs, now tell me is it the original or is it a variant? And then which

variant is it?’ He’s doing those virus isolations in his own lab, and he told me there's at

least seven variants over there.”

The virus continues to spread throughout the rest of the world. ASF has spread slowly in

Germany, mostly in the Eastern region, but producers continue to routinely find feral

swine carcasses that are already dead. These producers can isolate the virus to determine

9the cause of death. It’s important for producers to remember that the spread of ASF is

all about pig-to-pig contact. So far, Germany hasn’t seen any ASF spread in production

facilities. They have done heavy surveillance in areas with many feral positives, but no

spread has been detected in commercial systems. “The good thing is a lot of their major

production is not located in this Eastern part of the country,” said Pyburn. “It's not there,

it's up towards Denmark where they bring the pigs in from, coming into Germany from

Denmark. There’s not a lot of domestic pigs there. ASF is not found in the domestic

pigs.” The disease has not been discovered in North or South America yet, and

producers hope to keep it that way. The U.S. has a surveillance system that is run by the

USDA, and the National Pork Board has discussed strengthening the surveillance

program because of the high importance of finding ASF quickly to eradicate it. Borders

cannot stop domestic disease, so it’s very important that ASF can be detected quickly to

prevent further spread of the disease. “In China, their systems are set up such that they

haul pigs long distance for slaughter, so it ended up that they were hauling ASF virus

from one area of the country to another, seeding that new area, and then it took off from

there,” said Pyburn.

Weather: There is a ridge over the western U.S., a trough off the British Columbia-

Pacific Northwest U.S. coast, short-wave troughs in eastern Canada and the central

northern U.S., and Elsa is off the southwest coast of Florida. Elsa will track from

western Florida tonight to and through the Carolinas Wednesday night and Thursday. A

front associated with the central northern U.S. trough will progress southward and

eastward the rest of this week. The trough near the North American west coast will

move eastward and become cut-off as it moves into central Canada/U.S. areas later this

week. The U.S. and European models are in general agreement. For the outlook period,

temperatures on Sunday will be near to below normal from the southern Plains to above

normal over the Northwest, with near to above normal temperatures elsewhere. This

will be the general idea through the period. Weak frontal systems associated with zonal

flow may sustain scattered showers and storms across parts of the central and eastern

U.S. next week.

North American Weather Highlights: Some areas of the northern Plains received

showers over the holiday weekend, but warm temperatures continued to stress

developing crops. Though stress returns mainly in western areas between rain systems,

more widespread showers today and again later this week may keep crop conditions

from worsening and some areas could see improvement. Mainly warm and dry

conditions in the central/southern Plains over the holiday weekend allowed wet areas in

the east to drain, but continued stress in the north. Showers in the west the past few days

may have paused wheat harvest in places. Fronts this week will give a chance for

showers and storms for many places. Mainly dry conditions in the Midwest over the

10holiday weekend gave the wet areas a chance to drain but continued the stress for areas

that missed on the rain last week. Fronts this week will give a chance for showers and

storms for many places. Showers continued in the Delta over the far south over the

Independence Day weekend, but elsewhere dry conditions returned. This dry north

showers south pattern will continue today, but after tomorrow the north will see

scattered shower chances as well. Developing cotton and soybeans should continue to

benefit. Except for the far south, dry conditions returned to the Southeast over the

holiday weekend. Tropical system shower activity from Elsa, or the remnants, will

progress from south to north this week. Frontal system shower activity will take over

late in the week and for the upcoming weekend. Overall, conditions are favorable for

developing cotton. The wave of extreme heat passed early last weekend in the Canadian

Prairies and there has been isolated showers the past few days. A cut-off system will

bring scattered showers this week and may be able to briefly pause the worsening of

drought.

Global Weather Highlights: Drought continues to plague corn across Brazil with this

week also remaining dry. Above average and mostly above freezing temperatures in

Argentina for the past few days and for the rest of the week will be beneficial for wheat

growth. Strips of areas that see isolated showers this week get a bit of a moisture bonus,

but widespread showers are not expected. Another system keeps providing scattered

showers in Europe this week, maintaining beneficial soil moisture for developing crops.

It is possible the active pattern carries into early next week. Showers occurred the past

few days for Ukraine and western Russia which will benefit developing crops.

However, the latter part of the week will see showers mostly stopping and temperatures

gradually becoming above normal. Scattered showers may return next week. Scattered

showers will continue to move through the FSU spring wheat region this week, favoring

Kazakhstan. As this week ends and we head into the weekend and next week, frontal

systems provide additional chances for showers and cooler temperatures. While periods

of showers continue for southwest Australia, maintaining beneficial conditions for

vegetative winter crops, the next couple of days will remain dry in eastern Australia.

Showers then return to eastern Australia for the latter part of this week. Over the

weekend and into next week, southwestern Australia and Victoria see additional shower

chances, but Queensland and New South Wales look to be on the drier side. Periods of

showers and relatively stable temperatures continue favoring developing corn and

soybeans in China. Monsoon showers in India should continue to be consistent this

week, maintaining good soil moisture for developing crops.

Macros: The macro markets were mixed as of 8:30am EDT, with Dow futures down

0.1%, the U.S. dollar index is down 0.1%, crude oil is up 1.2% and gold is up 1.5%. The

S&P 500 on Friday posted a new record high and closed 0.74% higher. The DJIA

11gained 0.44%, while the Nasdaq 100

gained 1.15%. Bullish factors include

the 0.1 point increase in the June U.S.

unemployment rate, which the market

considered dovish for Fed policy, the

slightly stronger than expected U.S.

factory orders report, and a rally of

around 2% in mega-cap tech stocks such

as Alphabet, Amazon, Microsoft, and

Apple. The U.S. markets this week will

focus on oil prices after Monday's rally

of about 1.60% on the inability of

OPEC+ to reach a production hike agreement, tech stocks after China over the weekend

cracked down on more Chinese tech stocks, Fed policy after the markets viewed last

Friday's U.S. June unemployment report as neutral for Fed policy, any developments in

Washington on an infrastructure bill, although Congress is on recess this week,

anticipation of next week's start of the Q2 earnings season, the global pandemic

statistics as the delta variant causes a new Covid infection surge in many parts of the

world, and the impact of the weekend news of a massive ransomware attack on

thousands of businesses worldwide. Oil prices on Monday rallied by around 1.6% after

OPEC+ concluded its monthly meeting without an agreement to raise production. Oil

prices are rallying since OPEC+ now plans to leave its production unchanged in August.

The UAE wanted a higher production quota and refused to agree to the OPEC+

preliminary agreement, which involved a 400,000 bpd production hike in each month

from August through December.

The next FOMC meeting on July 27-28 is still another three weeks away. Fed officials

over the next three weeks are not likely to shift their themes, simply reiterating their

recent comments and waiting to engage in more discussion on QE tapering at its July

27-28 meeting. However, the market consensus is that the earning warning of QE

tapering will not come until the August Jackson Hole conference or the following

FOMC meeting on September 21-22. In a survey taken by Bloomberg in early June,

33% of the respondents said they expect the formal announcement of QE tapering in

September, 10% in October or November, and 33% in December. The markets are

expecting the Fed's first 25 bp rate hike in late 2022, according to the federal funds

futures market. The markets are then expecting two more 25 bp rate hikes in 2023. Last

Friday's 0.1 point increase in the U.S. June unemployment rate to 5.9% was interpreted

by the markets as a sign that the labor market is not yet strong enough for the Fed to

officially announce QE tapering. Payrolls rose by 850,000, which was stronger than

market expectations of 711,000. However, the 850,000 payroll report was not a blow-

12out number that caused the markets to believe that the Fed has concluded that the labor

market has made "substantial further progress," which is the benchmark the Fed is using

for its policy decisions. Rather, the labor market continues to just slowly improve as

more people come back into the labor market and as the pandemic drags on in many

parts of the country. The U.S. economy must still create another 6.7 million jobs before

getting back to the pre-pandemic record high.

Global shares were mostly lower Tuesday as oil prices surged after a meeting of oil

producing nations was postponed, with little else guiding trading after the U.S.

Independence Day holiday. France's CAC 40 dropped 0.5% in early trading to 6,534.23,

while Germany's DAX lost 0.6% to 15,561.04. Britain's FTSE 100 edged down 0.2% to

7,153.81. The future for the Dow industrials inching less than 0.1% lower to 34,663.00.

The S&P 500 future lost 0.1% to 4,339.88. Talks among members of the OPEC cartel

and allied oil producing countries have broken off in the midst of a standoff with the

United Arab Emirates over production levels. No debt has been set for the next meeting.

U.S. benchmark crude rose $1.28 to $76.43 a barrel. Brent crude, the international

standard, added 24 cents to $77.40 per barrel. In Asian trading, Japan's benchmark

Nikkei 225 edged up 0.2% to 28,643.21. South Korea's Kospi added 0.4% to 3,305.21.

Australia's S&P/ASX 200 fell 0.7% to 7,261.80. Hong Kong's Hang Seng lost 0.3% to

28,072.86, while the Shanghai Composite slipped 0.1% to 3,530.26. In currency trading,

the U.S. dollar slipped to 110.82 Japanese yen from 110.95 yen. The euro slipped to

$1.1851 from $1.1865.

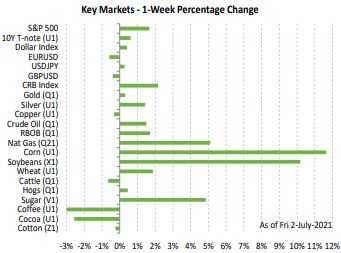

Summary: For the week, September corn was up $.61 ¾, December corn was up $.60

½, August soybeans closed up $1.30 ½, November soybeans were up $1.29 ¼,

September KC wheat closed up $.10 ¼, September Chicago wheat was up $.12 and

September Minneapolis wheat was up $.30 ¾. December corn closed down $.09 ¼ at

$5.79 ¾ Friday, hit in part by bearish news from several media sources reporting the

D.C. Circuit Court of Appeals overturned a 2019 ruling by the Environmental

Protection Agency that had allowed the sale of E15 fuels throughout the year. The

court's new ruling put a cloud over the outlook for ethanol demand, an important source

of corn demand, which has been doing very well lately as the economy recovers. The

ruling also revived previous concerns the White House is being lobbied to ease

renewable fuels mandates for refiners. From a practical point, Friday's ruling should not

impact E15 sales until June 2022. Aside from Friday's ruling, December corn continues

to show firm support after USDA estimated plantings at a lower-than-expected 92.7

million acres this week and adverse weather remains a threat to yield potential in

northwestern corn states. Friday's weather map was mostly dry across the Corn Belt

with light to moderate rain chances the next seven days and hot temperatures in the

northwestern Corn Belt through Monday. The extended forecast has another chance for

13rain in the ECB while the WCB remains generally dry with above-normal temperatures.

On the demand side, the U.S. Census Bureau said 70.4 million gallons of U.S. ethanol

were exported in May, slightly less than a year ago. Exports of distillers grains,

however, totaled 1.044mmt in May, up 68% from a year ago. Meanwhile, central

Brazil's second crop remains in poor shape with no rain in the forecast after southern

crop areas were hit with subfreezing temperatures earlier this week. Fundamentally,

domestic demand for corn remains strong and there have been no deliveries of July corn

yet. Technically, the trends remain up for both September and December corn with

December corn close to important support at $5.24.

November soybeans ended up $.03 ½ at $13.99 Friday, helped by another day of

support from higher canola and soybean oil prices. It has been an uncommonly hot week

in the western Canadian Prairies with triple-digit Fahrenheit temperatures, a condition

that is damaging to canola production and supportive for vegetable oil prices. The good-

to-excellent crop rating for canola in Saskatchewan fell from 64% to 38% as of June 28

and temperatures stayed hot after June 28. Thursday's Fats and Oils report from USDA's

NASS showed 173.5mb of soybeans crushed in May, up from 169.8mb in April, but

down 3% from a year ago. Soybean oil stocks fell from 1.81 billion pounds to 1.72

billion pounds at the end of May, down 16% from a year ago. Earlier Friday, USDA

reported U.S. exports of biodiesel increased in May to 82,320mt, 18% higher than a

year ago. December soybean oil closed up 0.79 cent at 62.28 cents. November soybeans

finished the week with a gain of $1.29 ¼, largely due to USDA's low planting estimate

of 87.6 million acres. As described above, the seven-day forecast remains mostly dry for

the western Midwest with hot temperatures coming to the northwestern Plains over the

weekend and into Monday. Even if soybeans could average 50bpa nationally, it still

would not be enough to meet USDA's anticipated demand of 4.42 billion bushels (bb).

Fundamentally, U.S. soybean supplies are expected to remain historically tight in 2021-

22 and China's demand will be a big factor again. Brazil FOB soybean prices ended the

week $.29 cheaper than comparable prices at the U.S. Gulf, a bullish sign that supplies

in Brazil are eroding. Technically, the trend is down for August soybeans, but up for

November soybeans.

September KC wheat fell $.19 to $6.09 Friday, erasing Wednesday's $.32 gain in two

days. Wheat was largely riding corn's coattails Wednesday and didn't have much in

USDA's reports to brag about. USDA's 33.7 million acre planting estimate for winter

wheat is up 11% from last year and harvest should make better progress in the week

ahead with a drier seven-day forecast for the southwestern U.S. Plains north of the

Texas Panhandle. SRW wheat is also likely to have better harvest conditions in the

week ahead with only light rains expected for much of the region. Wheat's problem

areas continue to be white wheat in the Pacific Northwest and spring wheat crops on

14both sides of the U.S.-Canadian border. Eastern North Dakota and Minnesota have

chances for moderate rain the next seven days, but the rest of the northwestern Plains

remains dry with hot temperatures into Monday. September Minneapolis wheat ended

up $.02 Friday, still showing plenty of bullish support for a crop in trouble. In contrast,

most of the world's major wheat areas outside of North America appear to be doing well

and that does not bode well for U.S. wheat exports in 2021-22. From a technical view,

the trends are sideways for September contracts of KC and Chicago wheat and up for

September Minneapolis wheat.

Please note: for monthly subscribers, we are changing our credit card merchant to

PayPal (you can still use your same credit card) as our prior merchant was no

longer close to price competitive. Please take the time to update your credit card

information on the update credit card page the next time you log in. Thank you!

A/C Trading Co. does not accept orders to buy or sell by e-mail, text or any other form of social media. This material has been

prepared by a sales or trading employee or agent of A/C Trading Co. and is, or is in the nature of, a solicitation. By accepting this

communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and

agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME

JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION

INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO

THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE

PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS

COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is

substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or

indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from

trades and statistical services and other sources that A/C Trading Co. believes are reliable. We do not guarantee that such information is

accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is

subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

15You can also read