Financial institutions - the impact of Scottish Independence - Law Society of Scotland 21st August 2014 Simon Morris CMS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Financial institutions – the impact of Scottish Independence Law Society of Scotland 21st August 2014 Simon Morris CMS footer date

Looking at …

1. Central bank

a) Payment systems

b) Currency union

c) Banknotes

2. Regulation

a) The requirement

b) Prudential regulation

c) Conduct regulation

3. Membership of the EU

4. Impact on firms & their clients

footer text | footer date 2

Robert Burns … lines written on a banknote

Wae worth thy power, thou cursed leaf,

Fell source o’ a’ my woe an’ grief … For

lack o’ thee, I leave this much-lov’d shore,

Never, perhaps, to greet old Scotland more.

footer text | footer date 3

What are we taking about?

Scotland

− Population 5.3m

− Employed in financial sector 148,600 (8% of Scottish workforce)

− GDP contribution from financial sector 8%

− 90% of Scottish financial sector clients are based England WNI

− 94% of Scottish insurance products are sold to England WNI

− 84% of Scottish mortgage products are sold to England WNI

footer text | footer date 4And also ...

Timing

• 18 September 2014: vote on independence referendum

• May 2015 UK general election

• 24 March 2016: Scottish Government suggestion for Independence Day

• Transitioning?

• EU negotiations?

footer text | footer date 5And meanwhile …

Poll on 11 August 2014 (YouGov) 35% yes v 55% no

Business reaction

• Societe Generale: Scotland would have an "immense" task ahead of it; currency union "looks

like a pipedream" and delusional to think it could both keep the pound "but also become master

of its own fiscal affairs". (The Telegraph, 5 August)

• RBS: "uncertainties resulting from an affirmative vote in favour of independence would be likely

to significantly impact the group's credit ratings”. (BBC News, 1 August)

• Standard Life thought to be in talks to buy potential new headquarters in London (The

Telegraph, 29 July)

• Barclays: independence could have a "modestly negative impact on the UK stock market", but

might spark an "adverse reaction" in some companies’ share prices, and “material

consequences” for RBS and Lloyds. (The Telegraph, 28 July)

• UBS: if "even a possibility" of no currency union "aversion on the part of depositors may lead to

savings shifting rapidly". UK Gov’t stake in RBS and Lloyds means “not feasible” “politically” for

them to remain Scottish. (The Scotsman, 9 July)

• Scottish Financial Executive report: “Compared with the business environment as it stands,

greater cost and complexity are certain. Uncertainty is extensive and likely to continue for some

footer text | footer time

date after such a vote.” (BBC News, March) 61. The central bank

Functions of a central bank …

1. Monetary stability – stable prices, confidence in the currency

a) Issue or facilitate issue of banknotes

2. Financial stability – stable financial system

a) Provide liquidity

b) Lender of last resort

c) Resolution authority

d) Macroprudential oversight

e) Oversight of clearing, settlement & payment infrastructure

footer text | footer date 7The proposals

Currency union with England WNI or a Scottish Central Bank

… financial stability policy will be conducted on a consistent basis across the

Sterling Area … the Bank of England Financial Policy Committee will continue

to set macroprudential policy … There could be a shared Sterling Area

prudential regulatory authority for deposit takers, insurance companies and

investment firms …

… The Bank of England … will continue to provide lender of last resort

facilities and [deal] with financial institutions which posed a systemic risk.

Scotland's Future

footer text | footer date 8In other words …

Currency union No currency union

Bank of England remains central bank Scotland may require a central bank in

and Lender of Last Resort order to join EU and for many other

reasons)

Macroprudential supervision carried Macroprudential supervision carried

across sterling area as a whole by Bank out by Scottish Monetary Institute?

Payment systems same as at present New payment systems would be

required

footer text | footer date 9The issues

Union politically rejected by UK government. And if it were acceptable:

− Central bank – Bank of England will set monetary policy

− Lender of last resort – England WNI responsibility committing public

funds to Scottish institution

− Disparities of macroprudential regulation – differing tax and

economic policy

− Infrastructure – payment & settlement done from London – but

BACS, CHAPS & LINK are private, UK & £ only

footer text | footer date 10− Scottish central bank – Need for clear responsibilities in a crisis with

x/b firms (old/new tripartite).

− Resolution – Scottish banking sector 12x GDP – would Scottish

backing would be available?

− And also

• Does not sit easily with possible € decision

• Difficulty in borrowing on ICM without central bank/novice bank

− Replicated for individual institutions => customer consequences

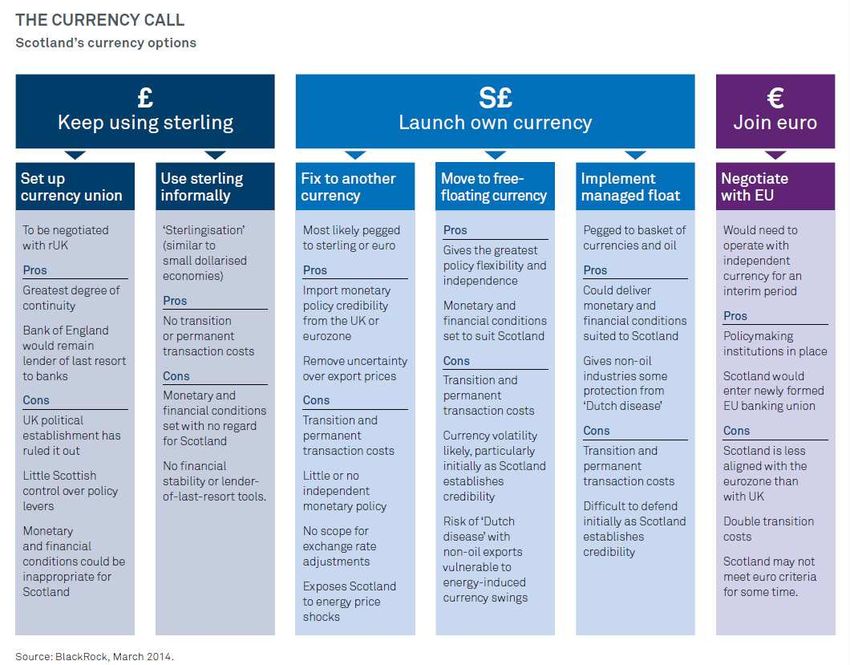

footer text | footer date 11And what about the currency?

Sterling monetary union with Bank of England as the central bank –

two assumptions

1. Sterling Area

2. Shared institutions & systems

UK government has rejected. If acceptable …

a) Non-sovereignty over monetary policy or financial stability (levers)

b) Dependency on another’s macroprudential policy

c) Non-control over financial infrastructure

d) Two economies one currency = risk of mini-€ crisis as no fiscal union

footer text | footer date 12Or a new currency or €

1. New currency

a) Sovereign central bank with all necessary competencies

i. Availability of funds for lender of last resort and resolution?

b) Paper/e clearing/ settlement system required – cost

2. € - complete currency conversion

a) Meeting the €zone convergence criteria

b) Only after sterling, dollarization or own currency for several years

c) Single € payments area legislation => major upgrade

3. And also the economic impact …

footer text | footer date 13footer date

14How does a country switch currencies?

“A country, such as Greece, contemplating leaving the euro would have

to …

1. Keep its plans secret until the last minute

2. Introduce capital controls

3. Start printing a new currency only after formal exit

4. Seek a large depreciation

5. Default on its debts

6. Recapitalise bust banks and

7. Seek close co-operation with remaining euro members”.

2012 Wolfson Economics 2012 Prizewinner on Grexit

footer text | footer dateBut also …

1. UK is non-federal currency area

2. The UK financial services economy is integrated and indivisible

3. Scottish banks would need new central bank settlement accounts

4. Redenomination depends upon sovereign law … but many

Scottish contracts are governed by English law or depend on

residence

footer text | footer date 16And Scottish banknotes?

Part 6 Banking Act 2009 – Scottish banks currently authorised may

continue to issue provided they do not stop.

footer text | footer date2. Regulation

At present

1. Bank of England

a) FPC

b) Infrastructure

2. PRA

3. FCA

4. Satellites

a) FOS

b) FSCS

footer text | footer date 18Will Scotland need its own regulators?

Some Directives assume a competent authority, others require one.

− CRD 4 – Member States shall designate competent authorities that

carry out the functions and duties provided for in this Directive and

… shall inform the Commission and EBA thereof, indicating any

division of functions and duties (Art 4)

− IMD – Member States shall designate the competent authorities

empowered to ensure implementation of this Directive [which] shall

be either public authorities or bodies … expressly empowered for

that purpose by national law (Art 7)

− PSD – Member States shall designate as the competent authorities

responsible for the authorisation and prudential supervision of

payment institutions … either public authorities, or … national

central banks (Art 20)

footer text | footer date 19− MAD – Without prejudice to the competences of the judicial

authorities, each Member State shall designate a single

administrative authority competent to ensure that the provisions

adopted pursuant to this Directive are applied (Art 11)

− MiFID – Each Member State shall designate the competent

authorities which are to carry out each of the duties provided for

under the different provisions of this Directive … (Art 48)

− AIFMD – Member States shall designate the competent authorities

which are to carry out the duties provided for in this Directive (Art

44)

− 3AML – Each Member State shall establish an FIU in order

effectively to combat money laundering and terrorist financing (Art

21)

footer text | footer date 20Scotland’s regulator(s)

What is a competent authority?

− Competent to supervise and enforce directive & regulation;

− Authority – empowered by national law;

MS can be challenged by Commission if CA fails to perform.

So what would an independent Scotland require?

a) A central bank for macroprudential regulation; and

b) A unitary regulator (an SFSA) or a prudential and a conduct

supervisor (a SPRA and a SFCA); or

c) Scotland could outsource to the FCA and the PRA.

footer text | footer date 21The proposals

− A shared PRA or a Scottish prudential regulator

“a shared Sterling Area prudential regulation authority for deposit takers, insurance

companies, and investment firms. Alternatively this could be undertaken by the

regulatory arm of a Scottish Monetary Institute working alongside the equivalent

UK authority on a consistent and harmonised basis”.

• And the Bank of England FPC and infrastructure oversight

• With England WNI sharing £zone bank recapitalisation

− A Scottish FCA

“A Scottish regulator which will assume the key responsibilities of the UK Financial

Conduct Authority in Scotland. It will work on a closely harmonised basis with the

UK regulators, delivering an aligned conduct regulatory framework, to retain a

broadly integrated market across the Sterling Area. The regulatory approach will

include the application of single rulebooks and supervisory handbooks.”

But wants a “far more efficient and effective consumer protection system”

footer text | footer date 22The issues

The EU requires a financial sector regulator, a resolution authority plus

satellites. Scottish proposals partly fulfil this but …

a) Sharing an England WNI prudential regulator may be unacceptable to

the EU & the UK government has rejected this proposal

b) The PRA may not accept an outsourced remit

c) England WNI may not find it acceptable to refinance a Scottish-

headquartered bank

d) There are difficulties in conducting unitary prudential regulation in two

sovereign states. Sharing PRA, Bank of England & FPC may not work

a) They are exclusively accountable to the UK/England WNI government

b) Plus divergence of law, tax & economic policy

c) Potential result of two significantly different regimes

footer text | footer date 23So Scotland may need new regulators …

a) A key prudential issue is funding a lending, liquidity & resolution

authority

b) Can you run unified prudential regulation with a separate central bank?

c) The cost of running new Scottish regulators would be substantial

There is an issue of supervisory jurisdiction (assuming EU membership) over

fully integrated passported firms

a) Most major Scottish firms predominantly xb into England WNI so a

Scottish regulator would have home but not host jurisdiction

b) PRA and FCA would remain home supervisors of England WNI firms xb

into Scotland

footer text | footer date 24And FOS & the FSCS

Deposit Guarantee Scheme Directive Each Member State shall

ensure that within its territory one or more deposit-guarantee schemes

are introduced and officially recognized ... (Art 3)

− Proposal – a Scottish FSCS (presumably including insurance)

funded by industry levy but would prefer to seek shared scheme

across monetary union

− Issues – would this be EU compliant? And would England WNI

agree to accept responsibility for Scottish-supervised firms’ failure?

− A Scottish non pre-funded non-UK backed guarantor affect

depositor/investor confidence

Ombudsman – Scotland would establish its own FOS

footer text | footer date 253. EU membership

The proposal

Following a vote for independence the Scottish Government will immediately seek

discussions with the Westminster Government, with member states and with the

institutions of the EU to agree the process whereby a smooth transition to

independent EU membership can take place on the day Scotland becomes an

independent country.

Scotland’s Future

The requirement

Any European State which respects the values referred to in Article 2 and is

committed to promoting them may apply to become a member of the Union … The

applicant State shall address its application to the Council, which shall act

unanimously after consulting the Commission and after receiving the consent of the

European Parliament, which shall act by a majority of its component members.

Treaty Art 49 (also on re-admission)

footer text | footer date 26Process requires the following – will it apply?

1. Candidacy

2. Scoping negotiations

3. Formal negotiations by chapter

4. Conclusions

5. Put for approval

Or can it rely on Art 48 – amendment to the Treaty?

footer text | footer date 27What do the EU politicians say?

In case there is a new country … coming out of a current member state it will

have to apply [and] accession to the European Union will have to be approved

by all other member states …Of course it will be extremely difficult to get the

approval of all the other member states to have a new member coming from

one member state (Barroso – President Commission)

A new independent state would, by the fact of its independence, become a

third country with respect to the Union and the treaties would, from the day of

its independence, not apply anymore on its territory (Van Rompuy President -

Council)

“Yo respeto todas las decisiones de los británicos, pero tengo muy claro que

una región que obtuviera la independencia quedaría fuera de la UE. Es bueno

que lo sepan los escoceses”. (Mariano Rajoy – Spanish Prime Minister)

footer text | footer date 28And if Scotland is an EU member state

− It will not be a €zone member – so does not need to meet

convergence criteria

• Inflation ≤ 1.5% above three lowest MS

• Annual deficitAnd if it isn’t immediately an EU member …

1. Scotland retains domestic market

2. No passporting in (although Scotland may permit)

3. No passporting out

1. England WNI may allow

2. Other MS may not

3. Consequent need to subsidiarise

footer text | footer date 304. The impact on firms

Forced restructuring under Post-BCCI directive unlikely

− Head office & registered office must be in same country. “Head office” is

undefined, but the UK regulators view it as the workplace of the firm’s

directors and senior managers who decide the firm’s central direction and

also make the material day-to-day decisions; and where central

administrative functions such as Compliance and internal audit are based.

Voluntary transfer of domicile possible

− If England WNI legislation allows, but not affect taxation or asset transfers

− Part VII with parallel authorisation

− Must be capable of effective supervision.

footer text | footer date 31Raising equity capital not problematical

• Can still access LSE

• But will cease to be UK companies so mandate issues

• CREST cannot effect DMZ transfer of foreign stock

Raising debt more problematical

• ratings on sovereign & private debt

Change of currency impacting contracts possibly an issue

• A pound is a pound – only entitled to nominal amount

• If a pound/pound differential, no revalorisation without contractual or

statutory provision

• If a different currency

footer text | footer date 32Differential taxation probably an issue

• Need for double tax treaty

• Possible loss of group treatment

• Recoverability of VAT

• Impact on costs

footer text | footer date 33Cross-border costs certainly an issue

• Dual authorisation if subsidiaries

• Twin rulebooks if passport

• Dual taxation regimes (double tax treaty needed)

• Dual approval of individuals

• Duplicated costs

− Compliance

− Regulation

− Marketing

− Legal

How different is different? NI/Ireland – Czech Republic/Slovakia

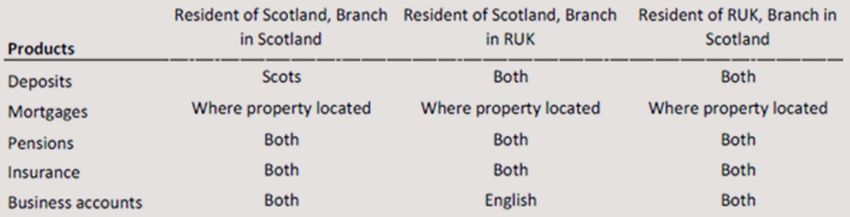

footer text | footer date 34And the impact on products …

Divergent tax regimes may make common products unsustainable

England WNI consumer confidence required in Scottish providers

• Costs

• Protection & disputes

• Impact of taxation & inflation

And looking at specific products …

footer text | footer date 35Tax incentivised savings Insurance & pensions

− UK ISAs no longer available − tax sensitivity

Mortgages − at risk from divergence

− rarely xb; Bank accounts

− Xb can increase costs

− may be dearer in Scotland;

− Different currency challenges

− FX risk on non-£ England WNI

− depositor confidence in

mortgages

England WNI;

− Scottish loans may be a

different rate even in sterling

zone

footer text | footer date 36So moving towards a conclusion … footer text | footer date 37

Day 1 issues

Complexity on Day 1 Some key uncertainties

− Unprecedented 1. When will Scotland be an EU

member?

− Constitutional issues

2. What will the currency be?

− Regulatory issues

3. Who will perform central

− EU issues bank functions?

− Taxation issues 4. And its economic impact?

− Currency issues 5. Who will be the regulators?

Unclear timetable 6. How will xb regulation work?

Lack of objective information

footer text | footer date 38Day 2 issues

Complexities on Day 2 Impacts

− Divergent policies − Firms as providers

− Divergent fiscal stance − Products in xb hands

− Divergent taxation impact

Dearer borrowing if credit ratings

− Divergent debt

change

− Divergent inflation

Heightened sovereign risk

• Scotland v Bund as a %

=> Higher consumer costs

footer text | footer date 39Days 1 + 2 issues =>

Consequent uncertainty

− Ongoing business

− Customer confidence

− Inward or new investment

All resolvable with

− Time

− Ingenuity

− Goodwill & cooperation

− Resources

footer text | footer date 40An overall scorecard

Benefits may be Drawbacks could be

1. Better consumer outcomes 1. Complexity

2. Scotland alone makes € 2. Uncertainty

choice 3. Cost

3. Lower business taxes 4. Impact on providers

4. Smaller = nimbler & more 5. Impact on customers

competitive

5. More public spending

footer text | footer date 41You can also read