FINANCIAL DIRECTOR BUYER PERSONA EXAMPLE: FD FRANK & STARLING BANK - F&G Funnel Mechanics

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FINANCIAL DIRECTOR BUYER PERSONA EXAMPLE: FD FRANK & STARLING BANK

+ GOALS + CHALLENGES

- Always, without fail, ensure the - Will the new banking ‘fintech’ actually

company finances run like clockwork be reliable and accurate?

(his legacy intact & retirement safe)

- Loathed to part with his beloved, and

- He has to somehow marry that with numerous Excel spreadsheets and

making finance at his company more existing ‘systems’ / ways of operating

tech-savvy and centred (plus data

accessible by mobile & web) - What role does the traditional person /

bank manager have to play in the

- Modern, flexible & real-time finance world of ‘fin-tech’?

FD FRANK + OBJECTIONS + CUSTOMER DATA

- Fear of incorrect, flawed data, and at Length of time they’ve been a

BACKGROUND the mercy of digital issues customer

(0

Frank is the FD for a Bristol-SME, years)

Average purchase frequency

having worked in finance all his life - Fear of increased costs with new tech, (Insert info for current customers only)

for many different UK companies. or it not being covered by the Average

He’s very much from the old-school necessary financial authorities or being spend

(Insert info for current customers only)

traditional banking brigade. easily hackable

Average CSAT score

DEMOGRAPHICS

- Fear of no human interaction and (Insert info for current customers only)

faceless tech. Fear of the unknown / Customer Lifetime

Frank is in his late-60s, with a wife new value

(Insert info for current customers only)

and 3 grown up children. He earns

£100k, has a nice savings stash, and is

looking to retire in the not-too-distant.

+ QUOTES

ATTITUDE

He’s time-poor, but also does

“

Ok my spreadsheets may seem numerous and complex, but they work -

and have done for decades. I’m very nervous about killing them off and “

everything absolutely by the book, moving to something that was only set up a few years ago. The business

and very thoroughly (which possibly bank accounts of these places only started last year!

feeds into the time-poor aspect).

COMMUNICATION PREFERENCES + ASPIRATIONS

Short, concise content ideally, but also - Short / medium term - try and find a fintech solution that overcomes

doesn’t mind lots of words (loves all his objections so he looks to be taking his old finance into the new

books, papers and reports). Uses his decade

phone and loves it for emails and - Longer term - not really applicable for him personally, he wants to

several apps seem useful thus far. retire after this project is complete with both old and new artfully and

professionally combinedWHO WANTS TO SELL TO FRANK?

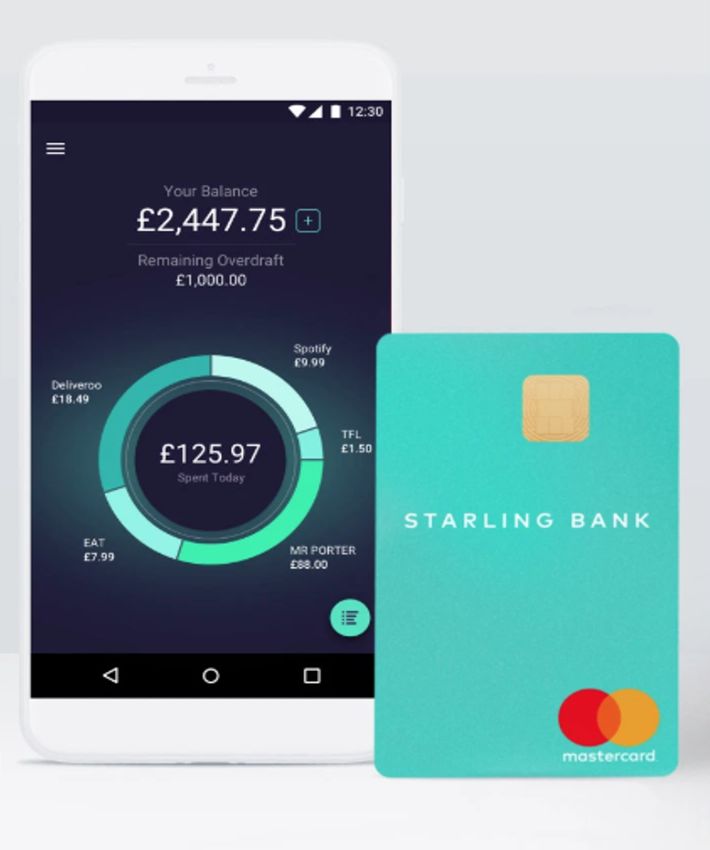

Starling Bank was the brain-child of ex-Allied Irish Banks COO (also RBS, ABN AMRO and

UBS) Anne Bode. It’s a digital, mobile-only UK “challenger bank” established in 2014.

Challenger banks are small, recently-created (i.e. in the last 4-5 years) UK retail banks

which compete directly with the well-established banks and are differentiated from them

by the fact that they are tech and digital-led or ‘Fintech’.

In 2016 Starling received its banking licence and the largest Fintech funding round of £48

million. In March 2018 Starling launched its business accounts, followed by several rounds

of additional funding.

This year it launched its first ever TV advertising campaign, and Anne Boden released her

book ‘The Money Revolution: Easy Ways to Manage Your Finances In A Digital World’. She

is regarded as a “disruptive banker” who wants to help account holders take better control

of their finances to transform their bank balance.

Starling’s vision is to appeal to any type of customer-buyer, consumer or business,

although in reality they will appeal first to the digitally-savvy and receptive, i.e. those willing

and able to manage their finances predominantly via the mobile app and embracing this

new form technology-led banking.

So how will our persona Finance Frank fare with the prospect of this new world of business

bank accounting so different to that he’s known and revered all his life?PERSONA NAME: FRANK SECTION ONE: WHO

BACKGROUND Frank is the Finance Director of a Bristol-based SME, having worked in Finance for all his life (many decades now) and for many different

Job, career path, companies both in Bristol and elsewhere in the UK, including London. His world is very much that of the old-school traditional banking, whereby

family you set up your business bank account with a reputable and well-established bank of many decades (if not centuries), and then cultivate a close

relationship with a particular bank manager there. For many years now he’s flown under the radar at his company, as he does a great and

consistent job of fastidiously managing the accounts and providing financial information to the company CEO and senior managers. However,

he’s now feeling a lot more pressure, ironically just as he’s looking to scale things back and start to look towards retirement. Recently, some of the

younger managers (and then in turn the CEO) have requested more real-time information on exactly how much money is in the business bank

account, and what recent banking transactions and working capital projections look like. They’ve started talking about phenomena such as

“Fintech” and “real-time banking”. The CEO gets annoyed when she asks for the right-this-instant bank balance and cash-flow state of affairs

(there’s a lot of pressure on sales because of Brexit), and he has to say he’ll come back with the information in a few hours, or by the end of the

day. He set up a series of amazing, but also fantastically complex, Excel-based spreadsheets to crunch the numbers. And although they’re iron-

clad in terms of accuracy, they’ve also worryingly started to freeze on occasion - and nobody else in the business has any idea how they work, so

only he can answer anyone’s questions (which keeps him working late).

DEMOGRAPHICS Frank is in his late 60s and looking to retire soon. He earns £100,000 has a wife and 3 children called Emma, Frank Junior, and John. He’s happily

Identity, age, settled now in Bristol, in a rather expensive house in Redland. He’s a consummate professional; has always worked hard, and late into the night

income,

whenever necessary (quite a lot of the time), crunching the numbers and delivering what’s required. You’ll frequently get emails from him at 2 or

geography

3am. He’s aware that technology is changing everything though, and probably for the better in that it will ultimately make things easier and

quicker for him (real-time information sounds interesting), and will possibly reduce the number of early morning missives he needs to send, as

well as the time it takes him to calculate and extract key data.

IDENTIFIERS Frank is time-poor and therefore all comms need to be short, and to-the-point. He’s only on Facebook to see pictures of his daughter living now in

Attitudes, the US, and other than that only uses LinkedIn which is useful from a business perspective. He reads the FT and broadsheets religiously everyday,

communication and also always watches the news at 9pm every night with his wife. He’s embraced technology in terms of his mobile phone and apps, so is keen

preferences to get information delivered directly into his pocket. He also reads loads of books, and has a membership for a local old boys society where he

dines and listens to talks.PERSONA NAME: FRANK SECTION TWO: WHAT

GOALS 1. The most important thing for Frank is that the business continues to run like clockwork, as that’s what his reputation

(rank) and legacy has been to-date.

2. Ultimately Frank wants to do a great job and continue to impress the CEO and senior managers and ‘retire well’.

3. He wants to demonstrate that he’s not a finance dinosaur and is ready and willing to ‘move with the times’ and

embrace new ways of banking and managing financial information. He knows these new technologies tend to impress

those he works with, and is keen to know more and leave behind a strong but also forward-thinking legacy.

4. He’s also genuinely interested in what new tech can do in terms of real-time information, flexibility and alerts. Getting

the right information at any particular moment in time is alluring. Ultimately he’d love to set up alerts that he needs and

have them sent to his mobile and also email address (he likes to have things sent to multiple places for security).

5. It would also be useful for the CEO and bank managers to be able to access the financial information themselves on

an ongoing basis (and indeed any successor of his), as although he regards himself as fundamental to the business, he

also wants to leave it behind and not have to work quite so long and hard.

CHALLENGES 1. He’s suspicious of how accurate the information he will be given is… he’s used to his beloved spreadsheets and tried-

(rank) and-tested financial categories and ways of doing things, so for him to make the leap to a completely new technology

(and potentially integrated accounting systems, such as Xero etc.) is a huge leap of faith.

2. He’d like to know what scope there is to develop a relationship with a human being bank manager, as this has been

important and necessary in the past. On occasion, the business has hit hard times and his sweet talking has led to the

bank manager affording him / the company some extra lending or time to get things in order - how would this work

with a new digital bank?

3. In moving to a new bank the whole legacy of the banking relationship with the former institution and bank manager is

lost… therefore what sort of support can he and the business receive moving forward, and how easy will the account

actually be to set up in the precise way Frank wants it to look and work?PERSONA NAME: FRANK SECTION THREE: WHY

QUOTES “I’m interested in all this so-called ‘fin-tech’ stuff everyone’s telling me about. But is it actually more about fancy branding and

Real words from the colours?”

buyer about

“Ok my spreadsheets may seem numerous and complex, but they work - and have done for decades. I’m very nervous about

aspirations, killing them off and moving to something that was only set up a few years ago. The business bank accounts of these places only

objectives, started last year!”

challenges

“If anything goes wrong and any numbers are incorrect, that will damage everything I’ve build up for decades: every number I’ve

ever provided has been double and triple checked, and that’s my entire reputation. Ok it may have taken a while to provide the

numbers, but at least I could give my word they were right.”

OBJECTIONS

Why wouldn’t they - Fear that the numbers will be incorrect and the data will be flawed, or digital issues will mean the information gets skewed

in some way.

buy?

- Fear that there will be no human interaction available with the new account, particularly access to an actual bank manager

with whom Frank can build a personal relationship and who may afford him some special dispensations.

- Fear that costs of using the account may increase in the future, as although they’re low right now, is that just to hook new

people into getting an account and then the fees could change and it will have a material impact on my business?

- Fear that if anything were to happen to the bank because it’s new and green, all my business’s funds will disappear and

not be guaranteed by the necessary authorities.

- Fear that because the account is digital, evil hackers can get into the account and steal everything or commit fraud. Or that

lots of people could access the account and cause havoc. Where are the controls and approvals in all this… they’re so

important in finance.

- What happens if someone steal mine, or my colleague’s phone, with access to the account?!

- Feeling nostalgia for killing off his beloved spreadsheets… they have a special name and everything after all…FINANCIAL DIRECTOR BUYER PERSONA & CONTENT PLAN EXAMPLE (STARLING BANK)

THE FLIPPED FUNNEL

AWARENESS The customer’s aware

they’ve got a problem &

they’re trying to define it

CONSIDERATION They’re researching all

possible ways to solve their

problem

DECISION The customer has decided

how to fix the problem & is

looking for confirmation &

reassurance that they’ve

made the right choiceMAPPING TOPICS TO FUNNEL STAGES

AWARENESS: Content here needs to help the buyer to define their problem. It

needs to reflects the buyer and their interests and concerns back to them.

This content needs to shows we understand them, their industry, their

environment, context and issues. Gives useful perspectives and ideas.

Demonstrates we know their world and their problem

CONSIDERATION: This content is about defining solutions. This is content that

shows ways to fix the issues our buyers face and how others have fixed this

stuff. We can start to show how we address these issues and concerns here

DECISION: This is about ensuring the buyer has all the information they need

to confirm they’ve made the right decision to go with us. Technical ‘how to’

stuff, what our products are and how we deliver them, case studies, reviews,

testimonials

ACTION: Sales support stuff – pitch and proposal documents, products in

detail, pricingPERSONA NAME: FD FRANK CONTENT PLAN

AWARENESS: — Frank’s question at this stage is top-level: ‘Is fin-tech for me’? Content here should speak to Frank’s

The customer’s aware they have a fears and anxiety. It should be about demystifying fin-tech. Starling needs to emphasise that

although it’s a new and shiny brand, it is trustworthy. Like traditional banks, it's subject to stringent

problem & are trying to define it

compliance, experience and security requirements . So lots hasn’t actually changed - just the tools

and tech, and for the better.

— In the evening, Frank has more time. He'll want to delve into more detail about fin-tech. Starling

should aim for PR coverage in the FT, Accountancy Now and Finance Officer Weekly. Whitepapers

and books would also be useful. Which is handy since Starling’s CEO Anne Boden has written a book:

‘The Money Revolution'.

— During the working day, Frank will need shorter and more accessible content. The focus should be on

creating / sharing podcasts, blogs, case studies and interviews. Reflect 'people like me' back to

Frank to build his confidence in the brand. Profiles of other FDs who took the leap, never looked back

then retired in a blaze of glory. Make a feature of putting faces to names of the executives in the

new bank. Particularly those with a serious banking pedigree, like Anne Boden. Showing the credible

people in key roles in the bank will address his faceless fin-tech fear. There's scope here too for

educational pieces such as:

'The Basics of Real-Time Reporting’,

'The Finance Director’s Guide to Fin-Tech’

'A Guide to Digital Transformation’

'The Art of the Possible with Fin-tech' (covering futurology, myth busting and expectation setting)PERSONA NAME: FD FRANK CONTENT PLAN

CONSIDERATION — Frank’s question now becomes: ‘Which fin-tech bank account is right for me?’

They’re researching all possible ways to — Starling needs to continue reassuring Frank. But this is when to introduce more detail about the

accounts. A 'Guide to Fin-Tech Bank Accounts' to make it easy for him to compare everything. This

fix their problem

guide needs to be thorough. Share content to show how Starling Bank offers the features and

functionality that Frank needs from his business banking. Share links to forums to show how FDs like

Frank are using digital services. Create sharable videos, posts and snapshots of reporting, data

visuals, alerts functionality. How Starling integrates with accounting softwares (without risk of

implosion).

— Creative and messaging needs to reflect Frank and people like Frank. Demonstrate your credibility

by appearing in the channels that Frank trusts. That could mean broadsheet and TV advertising. Or

even more traditional: sponsoring events at Henley, or hosting a talk at Frank’s London Club. But

don't fall into the cliche trap. He'll be active online. LinkedIn will be useful.

DECISION — Frank’s final question: ‘Am I right to choose Starling in particular?’

They’ve decided how to fix their problem — Send Frank some physical merch (the Anne Boden book, related books from the FT’s business and

finance books of the year, a leather card holder), arrange for a bank manager to meet with him.

& looking for confirmation & reassurance

— And more of the activities that took place at Consideration. So he sees a TV ad that evening, he and

they’ve made the right choice his wife (or the company’s CEO as well!) are invited to Henley, the next morning he sees a full-page

of Starling in the FT.F&G Funnel Mechanics is a marketing and business growth agency We help progressive companies grow through inbound & outbound marketing SARAH GREEN SARAH@WEAREFANDG.COM – 07932 212505 SARAH BRADBURY SARAHB@WEAREFANDG.COM – 07792 296099 JANE FRANKLIN JANE@WEAREFANDG.COM – 07775 660010

You can also read