Canadian Banks Midyear 2018 Outlook: Bail-In, Mortgage Tightening, Tax Reform, And IFRS Affecting The Canadian Banks - S&P Global Ratings

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Canadian Banks Midyear 2018 Outlook:

Bail-In, Mortgage Tightening, Tax Reform, And IFRS Affecting The Canadian Banks

August 17, 2018

AUTHORS

Lidia Parfeniuk Shameer Bandeally

Nikola Swann Michael Leizerovich

Amit Tiwari Michael ForbesContents

Key Takeaways 3

BICRA 4

Ratings Snapshot 6

Bail-In And Impact On Ratings 7

Domestic Net Interest Margins 9

Uninsured Mortgages 12

Outlook 14

Related Research 15

Analytical Contacts 16

August 17, 2018 2Canadian Banks: Key Takeaways

Key Expectations

We expect our stable outlooks on most rated Canadian banks to remain unchanged for the balance of 2018 and leading into 2019.

Operating performance is likely to continue on a positive trajectory, with strong contributions from the banks’ domestic, U.S., and

international businesses.

We expect asset quality metrics to remain stable and operating leverage to be positive.

Key Assumptions

A favorable domestic environment will continue to promote positive revenue and earnings growth.

Rising interest rates will benefit operating performance, though mortgage growth will slow further. A neutral to positive global macro

environment will add to the banks’ international operations.

A benign credit environment will benefit earnings, and revenue growth will continue to outpace expense growth due to disciplined

cost management.

Key Risks

A sudden and precipitous decline in home prices and a rise in unemployment would lead to higher loan losses.

Evolving changes to the North American Free Trade Agreement (NAFTA) could negatively affect a number of industries to which the

Canadian banks lend.

Global macroeconomic instability could affect the Canadian banks given market interconnectedness.

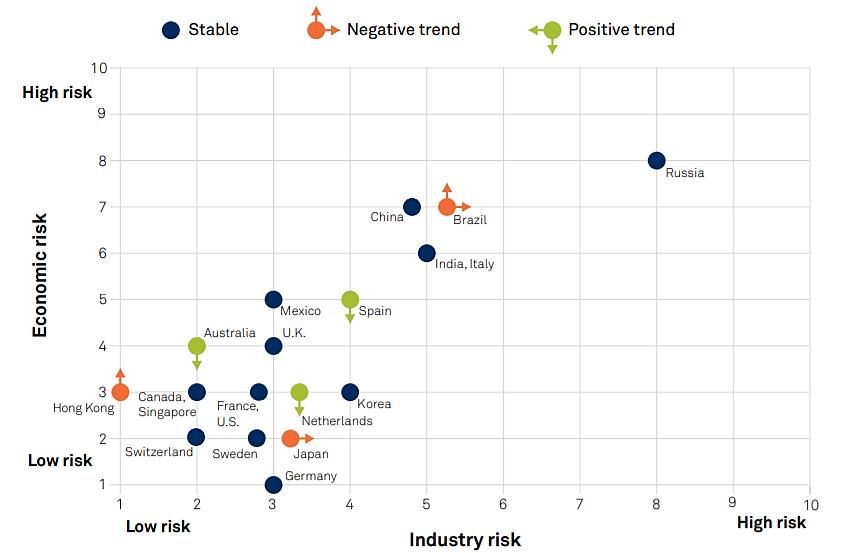

August 17, 2018 3BICRA Snapshot: Canada

BICRA Brief: Canada

BICRA group: ‘2’

Economic risk/trend: 3/stable

Industry risk/trend: 2/stable

What’s Changed In 2018:

Economic risk lowered to ‘3’ from ‘2’

Economic risk trend revised to stable

from negative

Looking Ahead:

We expect economic and industry risk

trends to remain stable over the

course of 2018 and leading into 2019.

The downgrade of the

economic risk score reflects

our concerns over high

consumer indebtedness and

elevated house prices leaving

the Canadian banks more

vulnerable to downside risks.

A BICRA (Banking Industry Country Risk Assessment) is scored on a scale from ‘1’ to ’10’, ranging

from the lowest-risk banking systems (group ‘1’) to the highest-risk (group ‘10’).

Source: S&P Global Ratings.

August 17, 2018 4Economic Backdrop: Canada

House Price Index

300

280

260

240

220

200

180

160

140

120

100

Composite Vancouver Toronto Montreal

S&P Global Ratings’ Economic Outlook – Select Economic Indicators

2013 2014 2015 2016 2017 2018F

Heavy consumer debt burdens could constrain credit growth

Real GDP (%) 2.5 2.9 1.0 1.4 3.0 2.0 and consumer spending.

CPI (%) 0.9 1.9 1.1 1.4 1.6 2.2

Rising rates and new mortgage stress tests should further

slow residential investment.

Unemployment (%) 7.1 6.6 6.9 7.0 6.3 5.9 NAFTA renegotiations may pick up in the third quarter; the

Short-Term Rate 1.2 1.2 0.8 0.8 1.1 1.8 application of auto tariffs may see as much as 15% of CAN-

U.S. exports affected.

Long-Term Rate 2.3 2.2 1.5 1.3 1.8 2.3

Note: Composite index includes 11 of the 15 largest metropolitan areas in Canada.

Sources: S&P Global Ratings, Teranet, and Bank of Canada.

August 17, 2018 5Ratings Snapshot: Canada

Business Capital & Risk Funding & Group Sovereign ICR &

Anchor SACP

Position Earnings Position Liquidity Support Support Outlook

Bank of Montreal a- Adequate Adequate Strong Adequate a Mod. High A+/Stable

Bank of Nova Scotia bbb+ Strong Adequate Strong Adequate a Mod. High A+/Stable

Canadian Imperial

a- Adequate Adequate Adequate Adequate a- Mod. High A+/Stable

Bank of Commerce

Central 1 a- Weak Very Strong Moderate Strong a- A-/Stable

Desjardins Group a- Adequate Strong Adequate Adequate a Moderate A+/Stable

Home Trust Company a- Very Weak Strong Weak Moderate b+ B+/Positive

HSBC Bank Canada a- Moderate Adequate Adequate Adequate bbb+ Core AA-/Stable

Laurentian Bank of

a- Weak Adequate Adequate Adequate bbb BBB/Negative

Canada

Manulife Bank of

a- Weak Very Strong Moderate Adequate bbb+ Strategic A+/Stable

Canada

National Bank of Canada a- Adequate Adequate Adequate Adequate a- Moderate A/Stable

Royal Bank of Canada a- Strong Adequate Strong Adequate a+ Mod. High AA-/Stable

Toronto-Dominion Bank a- Strong Adequate Strong Adequate a+ Mod. High AA-/Stable

Movements From The Anchor: What’s Changed In 2018:

Very Weak (-5)

Weak (-2) Laurentian Bank ratings removed from CreditWatch negative; outlook is negative

Moderate (-1)

Adequate (0) Royal Bank of Canada’s outlook revised to stable from negative

Strong (+1) BMO’s risk position assessment revised to strong from adequate, resulting in a

Very Strong (+2) revised stand-alone credit profile (SACP) to ‘a’ from ‘a-‘, with no change to the issuer

credit rating

Source: S&P Global Ratings.

August 17, 2018 6Bail-In Regime: Ratings Neutral…For Now

Key Takeaways From Resolution Regime Review

Canadian Systemically Bail-in applies to the six DSIBs (below) and takes effect Sept. 23, 2018.

Important Banks Ratings And No changes to issuer credit ratings or outlooks on DSIBs.

Outlooks Are Unchanged No change in our government support assessment on Canada (“supportive”).

Following Release Of Draft Bail-

In Regulations, June 19, 2017

No resolution counterparty ratings assigned to DSIBs.

We view Canada’s resolution regime as “effective,” defined in our ALAC criteria.1

The only DSIB that could obtain more ALAC uplift than the uplift it receives today is NA,

but we do not expect the bank to reach the 8% threshold required.

A Closer Look At How

Proposed Bail-in Regulations

May Affect Canadian Bank We expect to assign issue-level ratings on bail-in-eligible senior

Ratings, July 14, 2017 debt, upon issuance, at a level one notch below the SACPs.

BMO BNS CM NA RY TD

Anchor a- bbb+ a- a- a- a-

Canadian Systemically

Important Banks Ratings And SACP a a a- a- a+ a+

Outlooks Are Unchanged On

Release Of Final Bail-In Systemic Importance +1 +1 +2 +1 +1 +1

Regulations, April 20, 2018 ICR A+ A+ A+ A AA- AA-

TLAC / RRWA2 21.5% 21.5% 21.5% 21.5% 21.5% 21.5%

ALAC / SPRWA 6.4% 6.1% 5.7% 5.1% 7.1% 7.0%

Review Of Canadian Bank TLAC WB / RRWA3 24.5% 24.5% 24.5% 24.5% 24.5% 24.5%

Resolution Regime Completed;

ALAC WB / SPRWA 8.3% 8.0% 7.5% 6.8% 9.0% 8.9%

Ratings And Outlooks On

Systemically Important Banks 1 ”Bank

Rating Methodology And Assumptions: Additional Loss-Absorbing Capacity,” April 27, 2015.

Unchanged, Aug. 16, 2018 2 Regulatoryrequirement from Nov. 21, 2021.

3 WB--With buffer; assumes DSIBs maintain a 300 bps buffer over the regulatory minimum.

Sources: S&P Global Ratings.

7Regulatory And Other Changes Affected Capital, Earnings, And Asset Quality

Δ Basel I

Q218 The elimination of the Basel I Floor in first-quarter 2018 had a positive impact on the

Floor

CET1 large Canadian banks’ common equity Tier 1 (CET1) ratios.

Removal

BMO +45 bps 11.3% Despite early hits to earnings due to deferred tax asset (DTA) revaluations, the U.S. tax

reform is expected to overall benefit the Canadian banks’ U.S. businesses’ operating

BNS +50 bps 12.0% performance in 2018.

CM +16 bps 11.2% The transition from IAS 39 to IFRS 9 in first-quarter 2018 led to higher reserving levels

and lower nonperforming assets (NPAs). Some volatility in earnings is expected as a

result of IFRS 9.

RY +5 bps 10.9%

DSIBs – Loan Loss Reserves / NPAs

TD +120 bps 11.8%

120%

100%

Effective Tax Effective Tax

Rate Q417 Rate Q1 2018 80%

BMO Financial 63.7% 24.6% 60%

40%

CIBC Bank USA 86.6% 32.6%

20%

RBC USA Holdco 34.9% 22.3% 0%

2011 2012 2013 2014 2015 2016 2017 2018

Q2

TD Bank US Holdings 24.2% 6.8%

The U.S. tax reform is expected to result in an

average tax rate of 22% on the Canadian banks’

U.S. operations.

Sources: S&P Global Ratings and company filings.

August 17, 2018 8Rising Interest Rates Are Pushing NIMs Higher

DSIBs - Average Domestic NIMs

The Bank of Canada has enacted four

2.60%

increases to the overnight rate over the

past 12 months, which has benefited the

Canadian banks’ net interest margins

(NIMs), though funding costs are rising.

2.55%

2.50% S&P Global Ratings expects a

further increase in interest rates

in 2018, with the Bank of

Canada policy rate likely to

2.45% reach 1.75% from 1.5%.

2.40%

Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18

Source: S&P Global Ratings.

August 17, 2018 9Wealth Management Continues To Grow In Importance

Revenues By Business Line

For the fifth straight year, the proportion

100% 4% of wealth management to total revenues

6% 10%

14% 10% grew.

80% 30% 31% 24% Wealth management has increased in

17% 27% revenue contribution to 25.4% in 2018

from 20.5% in 2014.

60% 20%

17% 25% Recent bank acquisitions, such as TD

21% and Scottrade and CIBC and Private

92% Bancorp, are adding to the banks’ wealth

40% management positions in the U.S.

71%

We expect wealth management

58% 48% 44% 42% revenues to gain further importance in

20% revenue contribution.

Conversely, we expect capital markets

0% revenues (average for the big six banks

-8% -1% -2% is 18.3% of total revenues) to decline as

wealth management and retail and

commercial businesses grow at a faster

-20% pace.

BMO BNS CM NA RY TD

Commercial & Retail Trading & Sales Wealth Management Other

Note: TD includes wealth management within commercial and retail revenues; “other” refers to corporate and

technology segments of the banks; BMO “other” includes insurance CCPB.

Sources: S&P Global Ratings and company filings.

August 17, 2018 10Capitalization Is Expected To Remain Neutral To Bank Ratings

S&P Global Ratings’ Risk-Adjusted Capital (RAC) Ratio Before

Diversification The big six banks’ risk-adjusted capital

Q4 2016 Q2 2017 Q4 2017 (RAC) ratios averaged 8.6% in fourth-

quarter 2017.

The downgrade of the economic risk

10.2

score to ‘3’ from ‘2’ in 2018 has had a 40

9.7

bps-50 bps negative impact on the

9.3

banks’ RAC ratios, bringing the average

8.8

8.7

8.6

8.6

8.6

8.6

8.4

8.4

8.3

8.2

8.1

down to 8.2% in second-quarter 2018.

8.0

7.9

7.9

7.7

Decent internal capital generation could

outstrip loan growth adding to capital.

We expect banks to continue modest

dividend increases and opportunistic

share repurchases consistent with their

current capital and earnings

assessments.

We expect the Canadian DSIBs to

maintain their RAC ratios within our

adequate range of 7%-10%.

BMO BNS CIBC NBC RBC TD

Source: S&P Global Ratings.

August 17, 2018 11Banks Are Originating Uninsured Mortgages…

With stricter mortgage lending and approval rules, including

Insured Mortgages / Total Mortgages (%) the requirement of stress tests for borrowers, mortgage

80% origination volumes have declined.

The proportion of insured mortgages continues to decline as

portfolio insurance falls away, which is resulting in higher

originations of uninsured mortgages, slowly elevating the

70%

banks’ credit risk.

Banks’ LTVs on uninsured mortgages, however, remain

conservative at around 55%, somewhat mitigating the

60% growing risk.

DSIB Quarterly Mortgage Volume Δ

(Bil. C$)

50%

25.00

20.00

40% 15.00

10.00

5.00

30%

2013 2014 2015 2016 2017 2018 Q2

0.00

BMO BNS CM NA RY TD Q117 Q217 Q317 Q417 Q118 Q218

Source: Company filings.

August 17, 2018 12…But Asset Quality Remains Strong

NPAs & NCOs: Canadian Banks

1.60%

1.40%

Adj. NPAs / Customer Loans +

OREO (%)

1.20%

Net Charge-Offs / Average

Customer Loans

1.00%

0.80%

0.60%

A benign credit

environment is keeping

credit quality issues at

0.40% bay. But if

unemployment begins

0.20%

to rise, losses would

start to creep up.

0.00%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Q2

Sources: S&P Global Ratings and company filings.

August 17, 2018 13The Outlook For Canadian Banks Is Stable

Improving Neutral Worsening

We expect mid-single-digit revenue growth, in part reflecting slower mortgage origination, with about 50% of the

Revenues banks’ loan portfolios representing mortgages, but overall domestic retail and commercial franchises to continue their

steady revenue contributions, in addition to good revenue growth from the banks’ wealth management operations.

We expect expense control to remain a key focus, given slower revenue growth, and to produce overall positive

Expenses operating leverage.

We expect profitability to benefit slightly from rising interest rates and a benign credit environment and the banks’

Profitability U.S. and international operations to continue to produce strong results given neutral to positive global economic

conditions.

We expect asset quality metrics to remain strong and stable, though a sharp decline in home prices and rising

Asset Quality unemployment would lead to higher loan losses in the banks’ consumer loan portfolios.

We expect the large Canadian banks (DSIBs) to build toward OSFI’s minimum total loss-absorbing capacity (TLAC)

Capital and leverage ratios, beginning in September. We believe that capital management will remain a priority with a low

probability of large M&A activity.

We expect funding requirements to align with the banks’ needs with ease of access to global markets and the banks

Funding &

to begin issuing bail-in-able securities in fourth-quarter 2018. We expect the banks to continue to build liquidity on

Liquidity strong core deposit growth.

August 17, 2018 14Related Research

Review Of Canadian Bank Resolution Regime Completed; Ratings And Outlooks On Systemically Important Banks Unchanged, Aug.

16, 2018

Bank of Montreal, BMO Financial Corp. 'A+/A-1' Issuer Credit Ratings Affirmed; SACPs Raised On Stronger Risk Profile, Aug. 14,

2018

Americas Economic Snapshots, July 25, 2018

Royal Bank of Canada Outlook Revised To Stable From Negative On Maintenance Of Strong Credit Quality Metrics, June 27, 2018

Laurentian Bank of Canada Ratings Affirmed; Off CreditWatch; Outlook Negative On Concentrated Mortgage Exposure, April 27,

2018

Canada Economic Risk Higher On Elevated House Prices And Household Debt And Mortgage Fraud; No Ratings Affected, Feb. 23,

2018

Canadian Bank 2018 Outlook: Elevated Housing Prices And Consumer Leverage Are The Downside Risks To Mostly Stable

Operating Performance, Dec. 19, 2017

How IFRS 9's Expected Credit Loss Framework Will Affect Canadian Banks' Loss Provisioning In 2018 And Beyond, Dec. 18, 2017

August 17, 2018 15Analytical Contacts

Lidia Parfeniuk Nikola Swann

Toronto Toronto

+1 416 507 2517 +1 416 507 2582

lidia.parfeniuk@spglobal.com nikola.swann@spglobal.com

Amit Tiwari Shameer Bandeally

Toronto Toronto

+1 416 507 3224 +1 416 507 3230

amit.tiwari@spglobal.com shameer.bandeally@spglobal.com

Devi Aurora

New York

+1 212 438 3055

devi.aurora@spglobal.com

August 17, 2018 16Copyright © 2018 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof

(Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system,

without the prior written permission of Standard & Poor’s Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for

any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents

(collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for

any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or

maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR

IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR

PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE

UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P

Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs,

expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in

connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not

statements of fact. S&P’s opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or

sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the

Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of

the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary

or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not

perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgement at any time and in its sole discretion. S&P Parties

disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damage

alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the

independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other

S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received in

connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves

the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com

(free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other means, including via

S&P publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

Australia: Standard & Poor's (Australia) Pty. Ltd. holds Australian financial services license number 337565 under the Corporations Act 2001. Standard

& Poor’s credit ratings and related research are not intended for and must not be distributed to any person in Australia other than a wholesale client (as

defined in Chapter 7 of the Corporations Act). STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s

Financial Services LLC

August 17, 2018 17You can also read