IRELAND, THE ANGLOSPHERE AND THE EU - A PRIMARY SPOTLIGHT ON POLITICAL RISK - primaryaccess.co.uk

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A PRIMARY SPOTLIGHT ON POLITICAL RISK

IRELAND, THE ANGLOSPHERE

AND THE EU

14TH MAY 2019

The purpose of this note is to offer some insights into the realities of Ireland’s political and economic relationships and

attendant risks following the UK’s decision to leave the EU. It suggests the possibility of non- consensus outcomes as part of

the analysis and examines what events could trigger these.

Ireland joined the EEC in 1973-the same year as the UK. Right from the start, Ireland viewed its membership as a once-in-

several-generations opportunity to upgrade a hopelessly underfunded infrastructure and diversify its economy away from

over-reliance on the agricultural sector, through attracting foreign direct investment. As a strategy it was largely successful

on both fronts, with the EU making significant transfer payments over an extended period.

The extent of Ireland’s plundering of EU resources was captured vividly on an episode of Scrap Saturday, a satirical sketch

show which ran on Irish State broadcaster RTÉ’s Radio 1 from 1989 until 1991. In one episode, the character of the then-

Minister for Foreign Affairs says: “We are a member of the EEC, we are Europeans and committed to the give and take

of Europe; we take the CAP and the farm subsidies, and the structural funds and the free trips to Brussels and the big

expenses and we give them guff in exchange”. This funny and revealing insight accurately reflected the views of many in

Europe at the time, notably within the UK, regarding Ireland’s persistent and successful ‘panhandling’ of the EU, especially

in the matter of regional and structural infrastructure spending.

Ireland has always liked to portray itself as a good, if not a model, European citizen and dependable partner; its taxpayers did

indeed ‘take one for the team’ when the financial crisis of 2008/09 obliterated its over- leveraged domestic banking system

and led to a painful EU bailout. But on a number of occasions the Irish electorate has caused the EU major constitutional

anguish. Referenda to ratify the Treaties of Nice (in June 2001), and that of Lisbon (June 2008), were initially rejected. And

though both were overturned when re-offered, these events indicate that the people of Ireland are not averse to asserting

their sovereignty when self-interest and circumstance dictate.

This occasionally ‘sulky schoolchild’ version of Ireland is one of a number of reasons why it is well worth watching post-

Brexit (should that ever happen) because the country’s geographic position, with the use of the UK as a land bridge to

other EU states, and reliance on UK suppliers and markets (in addition to the land border with Northern Ireland), means it is

uniquely exposed to the cost, complexities and disruptions associated with applying and administering a customs border.

The economic implications are potentially enormous.

Data on Ireland’s trade in goods and services, sourced from the Irish Central Statistics Office, gives a pretty clear picture

which shows that while the EU states do feature as relatively important partners, the relationships with the UK and the US

are significantly more so, and particularly in goods trade.

14 Old Queen Street, London SW1H 9HP

Ireland’s top ten trading partners in goods and services, Irish Central Statistics Office, 2018©

IRE Services Exports 2017, IRE Services Imports 2017,

% USA % USA

UK UK

Netherlands Netherlands

2.5 2.3 1.51.3

0.1

2.3

11.5 Germany 1.8 Germany

3.6 1.7

2.3 France 2.8 France

4.0 Italy 27 Italy

4.0 Switzerland 12.4 Switzerland

16.4 Japan Japan

7.5

3.0

China 9.2

China

Spain Spain

IRE Goods Exports 2017, IRE Goods Imports 2017,

% USA % USA

UK UK

Belgium Belgium

2 2 2 2

4 Germany 22 Germany

4 3

24

5 27 Switzerland 6 Switzerland

Netherlands Netherlands

5

9

France France

8

China China

12 13

Italy 21

11 Italy

Japan Japan

Under the heading ‘For Ireland Brexit may prove to be another moment of psychological liberation’ written by Liam Kennedy,

Professor of American Studies at University College Dublin, and published on the The Conversation website, the author notes:

“Ireland entered the EEC as an agrarian backwater in need of aid—it now more confidently maintains EU membership

as a modern hi-tech, open economy. In 2014, it went from being a net beneficiary to a net contributor to the EU budget.

With such growth comes responsibilities and, with the EU demonstrating strong support for Ireland during Brexit, there

may have to be payback—or at least some tough decisions to be made regarding such issues as corporate taxation and

contributions to European defence.”

“Ireland’s globalised economy is highly dependent on investment by US multinationals. At present, approximately 700

US companies have investment in Ireland, employing around 150,000 people. In 2017 they paid €4.25bn into the Irish

exchequer. In 2016 Ireland accounted for 1% of the European economy yet attracted 12% of US foreign direct investment.

It must be added that it has benefited more than any European country from profit-shifting by US companies—a point of

some tension with EU partner countries.

For over 30 years, Ireland has promoted itself to American companies as ‘a gateway to Europe’—a pitch that has even

greater resonance since the EU referendum. The government and its agencies have been seeking to capitalise on this

messaging as Brexit nears, promoting the country as even more attractive for investment, and also positing an enhanced

presence in Washington as a close EU partner.”(1)

Dr Ray Bassett is a former Irish ambassador, now a senior fellow (EU Affairs) at Policy Exchange and a regular columnist who

14 Old Queen Street, London SW1H 9HPhas written extensively on the subject of the Anglo-Irish relationship in a Brexit context (see link below to his ‘Options for the

Irish Border’ paper, published in September 2018). While now ex-‘Establishment’, his opinions and writings on this issue are

decidedly opposed to the orthodox political assessment of Ireland’s place in the EU.

His argument is that the Varadkar administration’s slavish adherence to the Barnier/Juncker/Tusk axis is politically motivated

and does not represent what is most beneficial to Ireland from an economic standpoint. He makes the following supportive

points –

• Ireland’s links with the Great Britain are stronger than any other EU member state. It shares a common language, labour

market, culture & sporting links. UK TV and radio are available in the Republic. There is a large Irish diaspora living in

the UK whose travel and residency status pre-date EU membership. In addition to the 1.8m citizens of Northern Ireland

who are all eligible to claim dual nationality, there are an estimated 400,000 from the Republic of Ireland living in the

UK. A further 6m (~10% of total UK population) claim an Irish grandparent. Ireland has no comparable links with any other

mainland European country, with Spain, the second-largest destination for Irish nationals barely coming close (~17,000).

The numbers in the US are significantly larger if assessed by those claiming an Irish heritage.

• In comparison with its established patterns of migration and inward and outward investment, Ireland’s connections to the

Anglosphere are overwhelmingly greater than those to the rest of the EU.

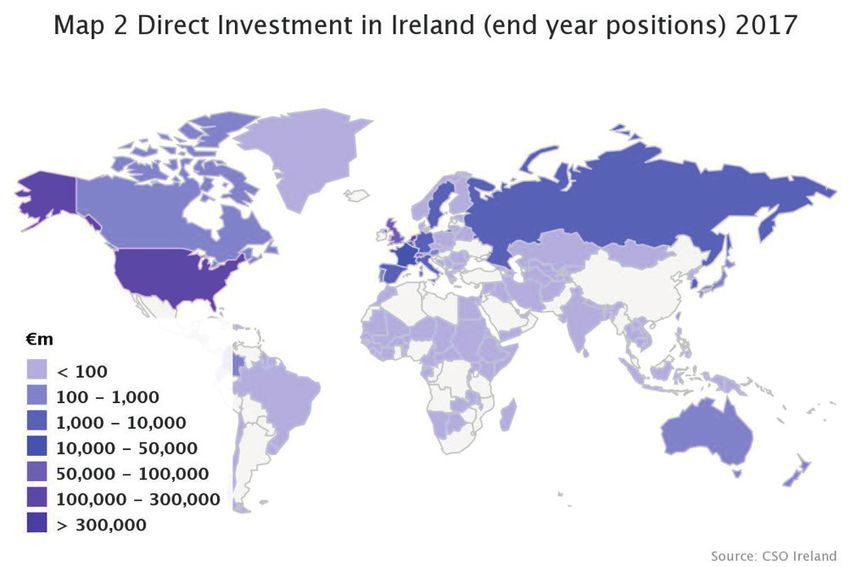

14 Old Queen Street, London SW1H 9HPAs these graphs irrefutably confirm, when it comes to direct inward and outward investment, Ireland is overwhelmingly

tied to the US and the UK. Ireland has €93bn committed to the US, and €88bn to the UK in direct investment abroad; the

comparable numbers for France and Germany are €4.4bn and €3.1bn respectively. The same pattern repeats in terms of

inward direct investment. The US has €179bn, and the UK €58bn invested in Ireland; France has €15bn and Germany €5bn!

While the Netherlands, Luxembourg and Switzerland have a combined €260bn invested in Ireland, the vast majority of this

‘investment’ comprises financial and insurance holding companies located in Ireland for tax purposes.

• The country’s links to the other 26 EU nations are dominated by trade from US multinationals based in Ireland, and is

hugely concentrated in inorganic chemicals, medical products and pharmaceuticals. Ireland’s own indigenous industries

are heavily reliant upon the output from UK SMEs, notably so in the food sector.

• New policies being promoted in the EU are distinctly not in Ireland’s economic interest, notably the Commission’s

suggestion of harmonisation of corporate tax rates which, if invoked, would seriously compromise the attractiveness

of Ireland as an appealing destination for foreign inward investment. Other areas such as defence (a European Army)

are domestically unpopular, while the determination of the EU to curtail US digital corporations, many of whom have

a significant presence in Ireland – Google & Amazon being prime examples – threaten an important growth and

employment component of the economy. A common language and a ready supply of relatively well-educated and tech-

savvy workers may not be able to trump a sharp increase in taxes, particularly if the UK is prepared to fill that void.

• Brexit will leave a massive hole in the EU budget – Ireland’s net contribution will rise steeply; it will also be potentially

more exposed than any other EU member should the UK, US and Canadian trade alignments post-Brexit reach a

productive and mutually agreeable settlement. As shown in the graphics above, the US and the UK are Ireland’s two

largest export markets. Any new trade agreement in the North Atlantic will put significant pressure on Ireland’s relatively

exposed economy.

• The Good Friday Peace Agreement represented a historic and iconic compromise, where all parties negotiated to get

14 Old Queen Street, London SW1H 9HPwhat they needed rather than what they wanted. Brexit has unsurprisingly damaged the goodwill attached to that accord,

but rather than seeking to assist in reinstating the ex-ante status by offering to be the diplomatic bridge between the

UK and the EU, Ireland has actively encouraged the latter to use the Good Friday Agreement as a weapon against the

UK in its withdrawal negotiations, leaving all parties (excepting ironically the EU, who had no figurative dog in the fight

having not been an official signatory to the deal) on worse terms – potentially also giving rise to an upsurge in Republican

activism and violence as recent tragic events have made all too clear.

Appearing as a guest panellist on the BBC’s Question Time, Michael O’Leary, the notoriously combative CEO of Ryanair,

(Europe’s largest airline headquartered in Dublin) made a robust defence of the EU, concentrating on the growth opportunities

afforded to the business he runs by the EU’s eastward expansion. What did not emerge on that programme were details

of Ryanair’s long-running legal battle with the European Commission, which routinely took the side of the (financially

cadaverous) flag-carrying incumbents, for whom Ryanair represented an existential competitive threat; at one point the EC

threatened to sanction any of its employees discovered to have flown Ryanair on official business, even if it represented the

most cost-effective and direct option. It should also be noted that Ryanair’s entire fleet is sourced from American Boeing not

Airbus-the poster child of European industrial collaboration.

In his Politeia article referenced earlier, Dr Bassett makes the following critical observations: “The UK is still Ireland’s most

important trading partner. The Welsh port of Holyhead alone took 425,000 HGV vehicles on the Irish Sea route in 2016

and is now the second busiest ferry port in the UK, second only to Dover. Other Welsh and English ports receive large

volumes of Irish goods on their way to markets around the world.”

“In addition, as Ireland has prospered economically, it has moved away from being a net recipient of EU funds. The

Irish net contribution this year will be around €1bn and rising, soon to top €1.3bn, similar per capita to the UK’s present

contribution. This is even before the EU proposes measures to fill the gap in the budget left by the UK’s departure. These

measures are likely to adversely affect Ireland, as the EU will be seeking larger payments from the present net donors,

as well as cuts to the Common Agricultural Policy (CAP), an area where Ireland gets most of its receipts from the EU

(around two thirds). Norway, a country in EFTA with a similar population to the Irish Republic, pays the EU approx.

€400m pa, for full access to the EU’s Single Market. This figure is less than half the current Irish net contribution.”

Further, he writes “the Irish have always mistakenly looked on the EU as an economic project. As the more grandiose

political schemes of Europhiles like Macron, or the SPD in Germany, become more apparent, then Ireland will have less

enthusiasm for Brussels. In addition, it should be admitted that much of the Euro enthusiasm in Ireland has traditionally

been a form of Anglophobia. With the UK no longer there, the love affair with Brussels will most likely increasingly cool,

as Ireland is forced to give up even more of its sovereignty and elements of its economy are damaged.”

“This will be particularly true when the EU seeks to curb Ireland’s attractiveness to Foreign Direct Investment (FDI),

because of its corporation tax rate of 12.5%. The move to a common consolidated corporation tax (CCCT) would force

even the most Europhile Irish politician to reconsider the country’s continued participation in the Euro project. If Ireland

was outside the EU, then the ability of Brussels to dictate its tax rates would be eliminated. The EFTA type arrangement

would, of course, maintain full and free access to the Single Market.”

“If Ireland were to opt for an EFTA style deal with the EU, this would relieve the UK of the need to solve the thorny issue

of the Irish border, as Ireland could maintain the present customs union with the United Kingdom, thus preserving the

mutually beneficial arrangements between the two islands. The downside for Ireland would be its exclusion from the

decision-making process in Brussels. However, with a voting share of between 1-2% in the Council of Ministers, it is

arguable whether Ireland, at present, has much of a say in EU law making.”

“In addition, there are attractions to the EU for agreeing Ireland’s exit to an EFTA linkage. The usefulness of Ireland in

the negotiations has now passed, with the UK agreeing to a generous financial settlement. To countries on the European

14 Old Queen Street, London SW1H 9HPmainland, such as Germany, France & the Netherlands, it is doubtful whether the huge difficulties in finding a solution

to the Irish border are worth the candle. As the EU showed in its notorious bailout for Ireland, it was more than willing

to dispense with Ireland’s national interests when faced with wider EU considerations. Given the small size of the Irish

economy, relative to the whole EU, it is extremely unlikely that the issue of the Irish border will be allowed [to] scupper

the wider deal.”(2) It is perhaps worth stating that there is no formal or official proposal from mainstream Irish politicians

currently other than for the country to remain firmly in the EU.

In July 2000, Ireland’s then-Enterprise Minister and Tanaiste (Deputy Prime Minister) Mary Harney famously made an

observation about her country to a meeting of the American Bar Association: “Geographically, we are closer to Berlin

than Boston. Spiritually, we are probably a lot closer to Boston than Berlin.”(3) Nearly twenty years on, much of the same

reliance upon familiarity and common purpose could be re-asserted, regardless of what a growing number of people in

Ireland are coming to see as political showboating obstructing Ireland’s national interest.

Even if the initial (and recurring) Irish reaction to the UK’s vote to leave the EU remains one of profound shock, it is typically

tempered by the view that ‘it will never happen’. Theresa May’s seeming preference for ‘BRINO’ – Brexit In Name Only – may

well prove the cynics in Ireland correct. However, it should be absolutely clear that whatever impressions are given by the

political posturing from all sides, the threat to Ireland’s national economic interest is clear and dangerous; whether that threat

is activated by a so-called ‘Hard Brexit’ or a committed movement by the European Commission towards tax harmonisation,

the political priorities in Ireland will shift seismically.

DAVID STANISTREET & FRED HEFFER

david@primaryaccess.co.uk fred@primaryaccess.co.uk

Primary Access & Research Ltd is an appointed representative of Messels Ltd., authorised and regulated by the Financial Conduct Authority

14 Old Queen Street, London SW1H 9HPSources and further reading suggestions

1. https://qz.com/1542757/brexit-could-transform-irelands-relationship-with-the-eu-and-us/

2. http://www.politeia.co.uk/wp-content/Politeia%20Documents/2018/ Ray%20Bassett/’Brexit%20and%20the%20Border’%2 C%20by%20Ray%20Bassett.pdf

3. https://www.herald.ie/opinion/columnists/dan-white/dan-white-harney-was-right-we-are-closer-to-boston-than-berlin-27980646.html

Other sites of interest

https://www.cso.ie/en/index.html

https://www.irishtimes.com/life-and-style/abroad/britain-s-shrinking- ageing-irish- population-1.3817868

https://www.irishexaminer.com/breakingnews/business/eu-as-a-bigger- home-for-irish- exports-than-uk-is-a-pipe-dream-820899.html

https://www.irishtimes.com/news/politics/us-congress-would-oppose-an- eu-trade-deal- that-endangered-ni-peace-neal-says-1.3865160

https://www.dfa.ie/irish-embassy/usa/about-us/ambassador/ambassadors- blog/economic- ties-between-ireland-and-the-us/

Important Disclosure Statement from Primary Access & Research

This document is issued by Primary Access and Research Limited (“Primary”) solely for its clients. It may not be reproduced, redistributed or passed to any

other person in whole or in part for any purpose without written consent of Primary. The material in this document is not intended for distribution or use

outside the United Kingdom. This material is not directed at you if Primary is prohibited or restricted by any legislation or regulation in any jurisdiction from

making it available to you. This document is provided for information purposes only and should not be regarded as an offer, solicitation, invitation, inducement

or recommendation relating to the subscription, purchase or sale of any security or other financial instrument. This document does not constitute, and should

not be interpreted as, investment advice. It is accordingly recommended that you should seek independent advice from a suitably qualified professional

advisor before taking any decisions in relation to the investments detailed herein. All expressions of opinions and estimates constitute a judgement and,

unless otherwise stated, are those of the author and the research department of Primary only, and are subject to change without notice. Primary is under no

obligation to update the information contained herein. Whilst Primary has taken all reasonable care to ensure that the information contained in this document

is not untrue or misleading at the time of publication, Primary cannot guarantee its accuracy or completeness, and you should not act on it without first in-

dependently verifying its contents. This document is not guaranteed to be a complete statement or summary of any securities, markets, reports or develop-

ments referred to herein. No representation or warranty either expressed or implied is made, nor responsibility of any kind is accepted, by Primary or any of

its respective directors, officers, employees or analysts either as to the accuracy or completeness of any information contained in this document nor should

it be relied on as such. No liability whatsoever is accepted by Primary or any of its respective directors, officers, employees or analysts for any loss, whether

direct or consequential, arising whether directly or indirectly as a result of the recipient acting on the content of this document, including, without limitation,

lost profits arising from the use of this document or any of its contents.

This document is provided with the understanding that Primary is not acting in a fiduciary capacity and it is not a personal recommendation to you. Invest-

ing in securities entails risks. Past performance is not necessarily a guide to future performance. The value of and the income produced by products may

fluctuate, so that an investor may get back less than he invested. Investments in the entities and/or the securities or other financial instruments referred to

are not suitable for all investors and this document should not be relied upon in substitution for the exercise of independent judgment in relation to any such

investment. The stated price of any securities mentioned herein will generally be the closing price at the end of any of the three business days immediately

prior to the publication date on this document. This stated price is not a representation that any transaction can be effected at this price.

Primary and its respective analysts are remunerated for providing investment research to professional investors, corporations, other research institutions and

consultancy houses. Primary, or its respective directors, officers, employees and clients may have or take positions in the securities or entities mentioned in

this document. Any of these circumstances could create, or be perceived as creating, conflicts of interest. Primary analysts are not censored in any way and

are free to express their personal opinions. As a result, Primary may have issued other documents that are inconsistent with and reach different conclusions

from, the information contained in this document. Those documents reflect the different assumptions, views and analytical methods of their authors. No

director, officer or employee of Primary is on the board of directors of any company referenced herein and no one at any such referenced company is on the

board of directors of Primary. Residents of the United Kingdom should seek specific professional financial and investment advice from a stockbroker, banker,

solicitor, accountant or other independent professional adviser authorised pursuant to the Financial Services and Markets Act 2000. This report is intended

only for investors who are ‘professional clients’ as defined by the FCA, and may not, therefore, be redistributed to other classes of investors.

Analysts’ Certification

The analysts involved in the production of this document hereby certify that the views expressed in this document accurately reflect their personal views

about the securities mentioned herein. The analysts point out that they may buy, sell or already have taken positions in the securities, and related financial

instruments, mentioned in this document.

14 Old Queen Street, London SW1H 9HPYou can also read