Omicron - the ghost of Christmas past? - Monthly Investment Strategy AXA IM Research December 2021 - AXA IM Netherlands

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Omicron – the ghost of Christmas past? Monthly Investment Strategy AXA IM Research December 2021

Summary: December 2021

Theme of the month: The outlook for US real yields

• US real yields have continued to set fresh lows. Over the past 25 years, real yields and monetary policy have moved lower together. Monetary policy

looks set to present ongoing headwinds for real yields over the coming six months – even if there are questions surrounding the direction of causality.

• Over this period, each fresh crisis has seen yields ratchet lower. Such a ratchet lower is consistent with the decline in the natural rate of interest, r*,

which in turn reflects a number of real economy developments. The outlook for r* should be for a modest rise over the medium-term.

• Credit enjoys an inverse relationship with real yields – spreads tighten as real yields rise. For equities, earnings revisions tend to be lower as real yields

rise. Real yields have also been associated with a rise in growth over value stocks. A modest reversal should materialise as real yields rise.

Macro update: Omicron – the ghost of Christmas past ?

• The Omicron variant presents a new and as yet undefined risk to the growth outlook for 2022. A risk of a highly transmissible, vaccine evading virus that

causes severe illness has been a key downside risk. Omicron appear to have two of those traits, we await evidence on the severity of infections.

• Otherwise, growth more broadly had softened from a robust re-opening pace around mid-year, but most regions saw the promise of above trend growth

for next year, even as supply constraints and real income growth promised to be a challenge in coming quarters.

• Inflation continues to rise, but may be close to a peak in several jurisdictions. Developed economies are seeing medium-term inflation expectations in the

main well anchored. Headline inflation should stabilise in the early months of 2022 and fall sharply from the spring.

• Labour market idiosyncrasies will shape medium-term inflation risks and central bank reactions. Tight labour markets in the UK and Canada make the BoE

and BoC look likely early tighteners. The Fed is tapering more quickly and can tighten earlier in 2022. The ECB has announced its own taper for 2022.

Investment strategy: risky assets shaken but not stirred, amid govie curve bear flattening and Omicron

• FX: The Omicron variant has been a reminder of the importance of monetary policy expectations in driving currency moves, as the dollar’s reaction was to

depreciate against the euro. Beyond short term noise, expectations for the terminal rate to rise may bring additional support to USD early in 2022.

• Rates: US CPI pricing two years forward does not look too aggressive if we account for inflation risk premium that inflation-linked investors demand. This

should be rather comforting for the US Fed, albeit with some caution attached, as survey-based inflation expectations have picked up more notably.

• Credit: Nov spread widening is consistent with the more aggressive Fed pricing, as spreads tend to widen when govie curves bear flatten. Yet the recent

correction hardly registers historically. Unless Omicron derails the recovery, we remain constructive for credit in 2022 amid strong credit fundamentals.

• Equity: The Omicron variant does not alter our constructive longer-term outlook for stocks either. Policy divergence between US and Europe raises the

risk of Fed policy spillover on Europe’s risk premia, but by our estimates this risk appears rather modest as US-Europe implied volatility beta has declined.

1

Central scenario

Summary – Key messages

Monetary policy

Inflation Divergence. Those with supply- Fiscal policy

side issues tighten (UK, Ca), those

“Mostly” transitory inflation without do not (Ez, Jp). US Expect final US package in 2022.

pressures ease visibly from depends on labour market. EMs Support in Europe more gradual.

Spring 2022. Threat from pressured by inflation UK aims at some tightening.

persistent labour supply issues expectations and FX. Omicron risks sharp rise.

and more region specific.

Growth Emerging Markets

Our central scenario:

Rebound continues. Virus and Access to vaccines paramount.

supply risks to recede in H2 Fading virus allows inflation Inflation pressures see further

2022. Supported by excess retracement as recoveries persist monetary tightening, made

saving spending in many DMs. We forecast global growth to rise by worse as Fed starts to tighten.

4.2% in 2022 and 3.6% 2023.

Economic growth persists despite supply FX

Rates pressures. Fading virus sees inflation

Gentle rise in longer-term rates, and supply constraints recede. Fed pricing favours dollar for now.

driven primarily by rising real rates European election uncertainty to

in a what still-expected-to-be weigh H1. Dollar outlook weakened

a gentle tightening cycle. by inflation and politics H2 2022.

Credit Equities

Benign spread regime can Strong earnings surprises in 2021

extend into 2022 favouring are set to diminish in 2022 but

higher beta carry while still above trend growth should prove

problematic for duration risk. supportive of earnings.

2

Alternative scenarios

Summary – Key messages

Persistent recession (probability 40%) Fast recovery (probability 5%)

What could be different? What could be different?

- Coronavirus mutation sees renewed outbreaks - Vaccine rolls out more quickly spurring pent-up demand burst

- Post-pandemic structural changes – labour market withdrawal - Labour market participation recovers, strong income growth

and goods demand – persist. Supply shocks last longer and easing inflation pressures

- Geo-political tensions mount in post-Covid world - Productivity boost following investment rebound and structural

- Nervous households maintain high saving buffers post-pandemic adjustments

What it means What it means

- Growth weaker, employment rebound softer, but inflation - Growth surprises on the upside in most regions

remains more elevated - Inflation fades towards and below central bank targets

- Monetary policy ill-equipped to deal with supply shocks, - Monetary policy proves more patient than expectations

deteriorating inflation credibility forces tighter monetary policy

in DMs

Market implications Market implications

- Risk appetite deteriorates / equities sell off / credit widens - Risk-on environment, equities make further gains, growth retains

lead over value

- Safe-haven rates rally resumes

- UST softens, EUR strengthens

- EM debt to come under pressure

- Spreads grind tighter

3

RISk Radar

Summary – Key messages

Global pandemic – Labour market Climate Change

risk of new variants scarring transition effects

Supply China –hard Global – Trade and

constraints landing currency wars

Global – Liquidity US – Corporate Europe – Sovereign

Financial Risks disruptions leverage debt crisis repeat

Global – financial China – property

conditions tighten inspired financial

abruptly pressures

US – Congressional Italy/Spain/France Global – Rise of populism

gridlock Political risk

Russia / Ukraine N Ire elections, and indy US – China

confrontation refs (Sctld and NI) decoupling persists

Short term Long term

4

Contents

1. Theme of the Month P.07

2. Macro outlook P.13

3. Investment Strategy P.28

4. Forecasts & Calendar P.33

5Theme of the month

The outlook for US real yields

The monetary policy effect on real yields

Monetary policy – rates and QE

- Monetary policy has been comprised of two components in the last decade and more: rates and QE. Theoretically, policy rate

expectations guide the rate outlook and balance sheet size affects term premium although in practice this distinction is not clear. A

combination of the two (and allowing for MEP in 2011) has provided a good model of real yields historically. This outlook suggests

ongoing headwinds for real yields as excess reserves (tapered QE and reverse repo unwind) impacts 2022.

Direction of causality not apparent

- Technically the trends in real yields may not flower from the stance of monetary policy. Growth and broader demographic factors

may reduce r* (influencing real yields), monetary policy will gravitate towards this level (allowing for cyclical variation).

Real yields and monetary policy Monetary policy factors create further head winds for real yields

Real yields and monetary policy Real yields and monetary policy

% %

7.0 -6000.0 4.0

3.0

5.0

2.0

3.0 -1000.0 1.0

1.0 0.0

-1.0

-1.0 Real yields 4000.0

-2.0 Real yields

Fed Funds Rate (LHS)

Excess reserves (QE, RHS rev scale) Combined monetary policy

-3.0 -3.0

1997 2002 2007 2012 2017 2002 2007 2012 2017 2022

Source: FRB, Bloomberg, AXA IM Research, Dec 2021 Source: FRB, Bloomberg, AXA IM Research, Dec 2021

7The outlook for US real yields

Real yields and the interest rate cycle

Tightening cycles have been consistent with modest rise in real yields

- We consider the last three policy tightening cycles. These were of markedly different magnitudes, with the 2004-06 cycle far

greater and sharper than the rise to 2001 or the 2015-18. Yet each different policy cycle yielded a broadly similar 100bp rise over

similar time frames of around three years. Moreover, the rise in real yields materialised as the Fed started hiking – not in advance.

A pleasing consistency

- If real yields begin to rise in 2022 as the Fed begins the next tightening cycle, adding 100bps, as per the last three cycles, onto

current levels (-1.00%), while BEI remains broadly unchanged, then nominal yields would rise from around 1.50% now to around

2.50%. This in turn would be consistent with a rise in FFR to 2.50% the Fed’s current assessment of the longer-run interest rate.

Real yields and the policy cycle Fed’s longer-term rate outlook

Real yields and FFR UST 5y5y and FOMC LR FFR expectation

% %

7.0 5

Real yields

5.0 Fed Funds Rate (LHS) 4

3.0 3

1.0 2

-1.0 1 FOMC LR FFR outlook (mid)

UST 5y/5y

-3.0 0

1997 2002 2007 2012 2017 Q1 2012 Q3 2013 Q1 2015 Q3 2016 Q1 2018 Q3 2019 Q1 2021 Q3 2022

Source: FRB, Bloomberg, AXA IM Research, Dec 2021. Source: FRB, Bloomberg, AXA IM Research, Dec 2021

8The outlook for US real yields

Yields ratchet lower, movements in r*

Yields ratchet lower after crisis, falling r*

- Consistent with the above observation that real yields have fallen sharply after each crisis, to rise only modestly, we can see that

yields have ratcheted lower after each crisis. This process may be associated with the scarring felt after each crisis in terms of

investment, productivity, skills losses and debt accumulation. More broadly, this echoes the overall trends estimated in the natural

rate of interest, r*. Estimates of r* have fallen over the same period.

A poor guide for policy, a good guide for term rates

- A host of economic and demographic factors appear likely to have driven r* lower these past decades. The short-term correlation

with advanced economy growth may point to some rise in r*, particularly if private sector debt expands further and broader

uncertainty fades. That said, trying to ascertain short-term movements to r* has proven a poor guide to policy setting. However,

historically r* has been a good benchmark identifying levels of 10-year yields.

The crisis ratchet – real yields settle lower after each crisis Trends in r* have been difficult to predict, but some signs of a rise

Estimated R* and Trend Global Growth Rates

% %

Advanced economies GDP (7yr ma, LHS)

4 LW r* estimate (RHS) 4

Lubik Mathhes r* est (RHS)

3

3

2

2

1

1

0

0 -1

1986 1991 1996 2001 2006 2011 2016 2021 2026

Source: Bloomberg, AXA IM Research, Dec 2021 Source: FRBSF, FRBR, IMF, AXA IM Research, Dec 2021

9The outlook for US real yields

Credit does not react adversely to rising real yields

The cycles chico, they don’t lie

- Parsing the cycles in US 10y real rates and the accompanying change in US HY spreads reveals an inverse relationship.

- The global financial crisis saw two major widening episodes; one at the start when real rates declined (“Jun07” label on chart) and

one around Lehman, when real rates increased (“Jul08” label on chart).

2008 was an outlier year

- The massive risk off around the Lehman bankruptcy included a material drawdown in US HY returns. At the same time US real

yields spiked, albeit mechanically due to the collapse in inflation expectations.

- Excluding this highly irregular episode from the histogram of USD HY returns vs real rate changes, shows that USD HY returns are

mostly positive, even if modest, during rising real rates.

USD HY spread directionality inverse to real rates USD HY returns skewed by the outlier year 2008

Source: Bloomberg, ICE and AXA IM Research, Dec 2021 Source: Bloomberg, ICE and AXA IM Research, Dec 2021

10The outlook for US real yields

Equity and real rates

Real rates, a potential headwind

- Companies have maintained high profit margins despite rising input costs, but margins may come under threat if pressures persist.

Real rates may also prove a headwind for stocks, as earnings revisions tend to trend lower with rising TIPS yields.

- 2022 consensus forecast for revenue growth at 6.8% is near the long-term trend. Downward revisions could undermine equity

returns in year when policy withdrawal is unlikely to support an expansion in multiples.

Value/Growth rotation and real rates

- The under-performance by Value vs Growth has shadowed the downtrend in real yields over the past couple of decades, although

the relationship has been less clear-cut over certain periods (2010-12, 2013-17). But there has been strong recoupling post Covid.

Rising real rates may penalise earnings expectations USD HY returns skewed by the outlier year 2008

Source: MSCI and AXA IM Research, Nov 2021 Source: : CBO, MSCI and AXA IM Research, Nov 2021

11Macro outlook

Growth outlook solid despite headwinds

US

Beginning to feel a bit like Christmas ?

- As the holiday season rolls on the focus turns to consumer spending. October posted strong retail sales (1.7% m/m) and

consumption (1.3%, or 0.7% in real terms). However, this may have represented a faster start rather than stronger overall season.

November’s outturn was a much softer at 0.3% for retail sales and December could also be soft. We expect consumption to rise by

1.5% q/q in Q4. But are wary of the impact of real income compression and COVID on Q1 spending.

Still strong growth outlook

- We forecast 4.5% (saar) growth for Q4 delivering a 2021 total of 5.5%. Headwinds and supply constraints at the start of the year

may delay an inventory rebound into H2 2022, dampening growth the 2022 average and lifting 2023. We forecast growth of 3.5% in

2022 and 2.7% in 2023 (consensus 3.9% and 2.5%). However, we expect the US to be operating in excess of potential growth – in

excess demand – from 2022, something that should build inflation pressure for the future.

Retail recovery to drive faster Q4 GDP CPI inflation reaches 40-year high

Key drivers of CPI inflation around peak

% yoy % yoy

80

20 CPI - total (LHS)

Owner's equivalent rent of residences (LHS) 60

15 New & used vehicles (LHS)

Motor fuel (RHS) 40

10

20

5

0

0 -20

-5 -40

Jan 15 Jan 16 Jan 17 Jan 18 Jan 19 Jan 20 Jan 21

Source: BEA, US Census Burueu, AXA IM Research, Dec 2021 Source: BLS, AXA IM Research, Dec 2021

13The impact of 40-year high inflation

US

Inflation close to peak

- Inflation rose to 6.8% in November, a 40-year high. On the month, price increases were driven by new & used car prices, rents and

motor fuels. Gasoline should be lower next month, and used car prices in a couple of months, but rents look like rising further.

Headline inflation should be around a peak, albeit that it will likely take until spring before the rate begins to fall sharply. We

forecast inflation to average 4.7%, 4.1% and 2.9% in 2021, 2022 and 2023 – a little ahead of consensus (4.6%, 3.7% and 2.4%).

Fed pivoting to inflation

- The Fed announced a quickening in the pace of asset purchases in December. These are now forecast to finish in March. The Fed’s

December meeting marked a mor hawkish turn. We omicron concerns and a softer growth and employment outlook than the Fed,

as well as signs of inflation retracing, as persuading the Fed to wait until June before tightening – but now expect three hikes in

2022 and three in 2023 to close the year at 1.50-1.75%, with risks skewed to a fourth.

Market expectations have adjusted timing not extent of hikes Inflation has weighed on the dollar

US - Market expectations of Fed policy Trade-weighted US dollar (real and nominal)

FFR estimates Index (Jan

(%)

2.5

1973=100)

31/03/2021 140 Real

30/06/2021 Nominal

2.0 Linear (Real)

30/09/2021

120 Linear (Nominal)

16/12/2021

1.5 AXA IM Outlook

100

1.0

80

0.5

0.0 60

Dec 22 Jun 23 Dec 23 Jun 24 Dec 24 1973 1979 1985 1991 1997 2003 2009 2015

Source: Bloomberg, AXA IM Research, Dec 21 Source: FRB, AXA IM Research, Dec 21

14Seasonally adjusted

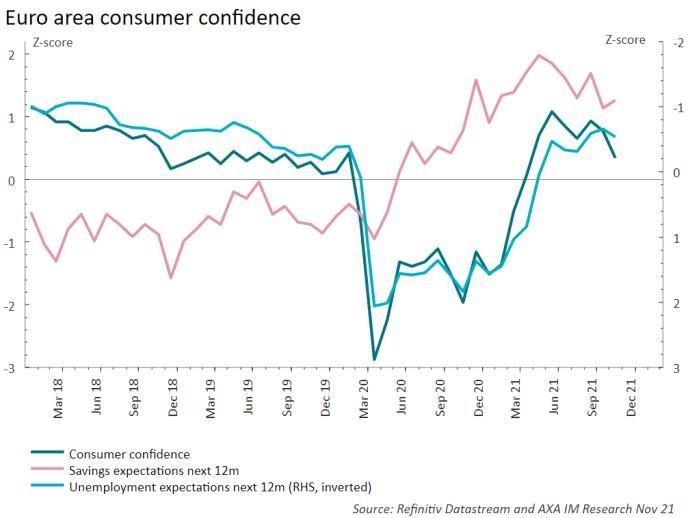

Euro area

Softening demand

- November’s consumer confidence eased again, while October retail sales declined in Germany (-0.3% mom), France (-0.2%) and Spain

(-0.1%) due to rising energy prices and a shift of spending towards services. The latter is now exposed to tougher restrictions from the

Delta COVID-19 wave and uncertainty around the Omicron strain.

Mixed manufacturing data

- German industrial production surprised on the upside, rising 2.8% mom but was strongly biased towards auto production, which

jumped 26% while VDA data pointed to another strong print in November (up 15%) as the sector recovers from extreme weakness

relating to chip supply.

- In the Eurozone, France also saw a 0.9% rise, but Italy and Spain – less exposed to autos – both contracted. However, German orders

fell by 6.9% mom pulled down by external demand (-13%), despite robust domestic demand (+3.4%).

- We continue to expect timorous Q4 GDP growth (+0.4% quarter on quarter), while Q1 should be only slightly better.

Softening consumer outlook Auto sector rebound pushed up industrial production

15Political developments

Euro area

ECB: Time for recalibration!

- The ECB announced the end of the PEPP but maintained some flexibilities in the policy reinvestment and extended it until the end of

2024. The APP will be scaled up to €40bn per month in Q2 (versus €20bn), before declining to €30bn in Q3 and €20bn from October

2022 onwards and this "for as long as necessary". We believe rate hike is very unlikely before 2023.

- The ECB anticipates high inflation will persist in the near term but should ease in the course of 2022 and end below 2% by the end of

2022. Macroeconomic projections showed inflation could reach 3.2% in 2022, and 1.8% in 2023 and 2024.

German government is now in office, focus shifts to Italian and French Presidential elections

- The energy transition, increasing minimum wages and strengthening Europe are the top priorities for the new German government.

Fiscal policy is still cautious, but the door remains open to some changes at both domestic and European level.

- In Italy, Matteo Salvini reiterated his support for Mario Draghi as Prime Minister, lowering the probability of Draghi being proposed as

President. But Parliament may yet fail to agree on a candidate, especially as one is yet to be declared.

- In France, we now have contenders for April’s Presidential Election. Valerie Pecresse will lead Les Republicains and recent polls showed a

strong rebound in voting intentions. We continue to see the re-election of President Emmanuel Macron as the most likely outcome.

Inflation projections Pecresse is now favourite for second round against Macron

Source: EU Commission, OECD ECB, AXA IM Research, as of December 2021

16 Sources: Odoxa, BVA, IPSOS, Elabe, Ifop-Fiducial, Harris-interactive, AXA IM

Research, as of December 2021Omicron likely to weigh on GDP outlook

UK

Fresh social restrictions are put in place to counter Omicron

- The omicron variant’s emergence has challenged the government’s previous approach to mitigate the pandemic. With cases of the

new variant doubling every two to three days, the UK government has implemented Winter ‘Plan B’ mandating mask-wearing in

public places and asking workers to work from home where possible, the latter a risk to ancillary leisure services.

Trend of weak growth continues into October, with omicron uncertainty likely to weigh in further months

- UK growth has been weaker than expected in recent months, up by just 0.1% in October. This softer start to Q4, also raises the

prospect of a softer Q4 in total – not least with Omicron related concerns and additional restrictions threatening to weigh later in

the quarter. We now forecast Q4 GDP coming in below the 1% we had previously forecast. Retail sales rebounded in October by

0.8% after five consecutive months of contraction. We expect retail sales to come under increased pressure over the coming

months reflecting pressure on households real incomes.

COVID related deaths rise, but far less than new cases Momentum from the re-opening rebound fades

UK Cases and Deaths

Thousands Thousands

1.4 New deaths smoothed (2 week lag, LHS) 70

New cases smoothed (RHS)

1.2 60

1 50

0.8 40

0.6 30

0.4 20

0.2 10

0 0

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

Source: Our World in Data, AXA IM Research, Dec 2021 Source: National Statistics, AXA IM Research, Dec 2021

17Labour market remains key to inflation outlook

UK

Recent labour market trends risk more persistent inflationary pressures

- Despite output still being below pre-pandemic levels, the economy has begun to face signs of capacity issues. The latest labour

market report showed that unemployment fell further to 4.2% in the three months to October despite the end of the furlough

scheme. In addition, vacancies were at all time highs in 15 out of 18 sectors. These suggest that UK activity is operating around or

beyond its capacity limit, even while total output is still below its pre-pandemic level – let alone its pre-crisis trend.

MPC begins a cautious hiking cycle

- The MPC voted to increase Bank Rate to 0.25% from 0.1% in December. Despite the uncertainty posed by the omicron variant, the

MPC viewed the threat of elevated inflation and a tight labour market as warranting an increase from the low emergency rates.

The MPC highlighted that any future tightening will depend on the uncertain future developments in the virus. However, it

suggested that further modest tightening was viewed as “likely”. We forecast two hikes in 2022 and one in 2023.

Labour market tightness appears to be widespread Evolution of market pricing of interest rates

Source: National Statistics, AXA IM Research, Dec 2021 Source: National Statistics, AXA IM Research, Dec 2021

18Growth recovers on fading power shortages

China

Property woes exert more persistent pressure than the power crunch

- The power shortages waned following a concerted effort across governments to ensure a stable supply of energy. Given the

priority of preserving near-term growth and social stability, the authorities acted swiftly to remove curbs on coal production and

imports. A sharp decline in the cost of coal gave electricity companies the necessary incentives to plug the supply gap. With power

supply back on-line, the resumption of production saw the Purchasing Manufacturing Index (PMI) recover to expansionary

territory after spending the prior two months below 50

Trade still serves as a cushion against economic headwinds

- Despite the supply chain disruptions and as well as rising uncertainties from the Omicron variant, November’s export growth

surprised to the upside, rising by 22% yoy on the back of tech resilience and higher global demand in advance of the holiday

seasons. Import growth also continued its acceleration due to still strong demand for coal as a source for electricity inputs

Headline PMI edges back above the waterline Trade resilience continues

Source: CEIC, AXA IM Research, Dec 21 Source: CEIC, AXA IM Research, Dec 21

19Policy to turn more growth-supportive

China

Inflation picks up on rising food and energy prices

- Headline CPI increased to 2.3% in November from 1.5% in October. While the gain was partly due to base effects, it was also

because of rising fuel and food prices. In particular, pork prices are finally showing signs of a rebound. In contrast, core CPI

declined, likely impacted by on-and-off COVID outbreaks. Overall, despite the notable rise in CPI, it is still below PBoC’s 3% target.

RRR back on the table

- The PBoC recently announced an RRR cut of 50bps to be effective on 15 December, taking the all-bank weighted average ratio

down from 8.9% to 8.4%. This is estimated to release around RMB 1.2 trillion of liquidity into the banking system. In fact, Beijing

had already started to ramp up policy supports: fine-tuning property policies, more generous liquidity injections and faster local

government bond issuance. However, these piecemeal actions are insufficient to spur activity to hit our growth forecast of 5% next

year. We expect the upcoming Central Economic Working Conference to send a clear dovish policy signal, preparing the local

authorities for more forceful action next year

Inflation continues to rise, but still below PBoC target for now 50bp cut of RRR, effective mid-Dec 2021

Source: CEIC, AXA IM Research, Dec 21 Source: CEIC, AXA IM Research, Dec 21

20Domestic demand and auto sector rebound

Japan

Demand resilient

• Data now confirms a substantial domestic demand increase following the end of the state of emergency. In October, the BoJ’s

consumption index jumped 4.3% on the month, with spending rebounding in durable goods and recovering fast in services. Looking at

consumer confidence, employment prospects rose again and are now above the pre-pandemic level while income expectations are

flat. Willingness to buy durable goods has declined, although this probably reflects a shift of spending towards services.

Auto production rebound

• In the manufacturing sector, output progressed, and the auto sector is gradually recovering. December’s BoJ Tankan surveys for

manufacturing firms were surprisingly unchanged. That said, FY21 profit expectations strengthened considerably and capex plans were

only revised down modestly.

Consumer confidence are close to pre pandemic levels Only large manufacturers were unchanged in last Tankan surveys

21Government and Bank of Japan policies

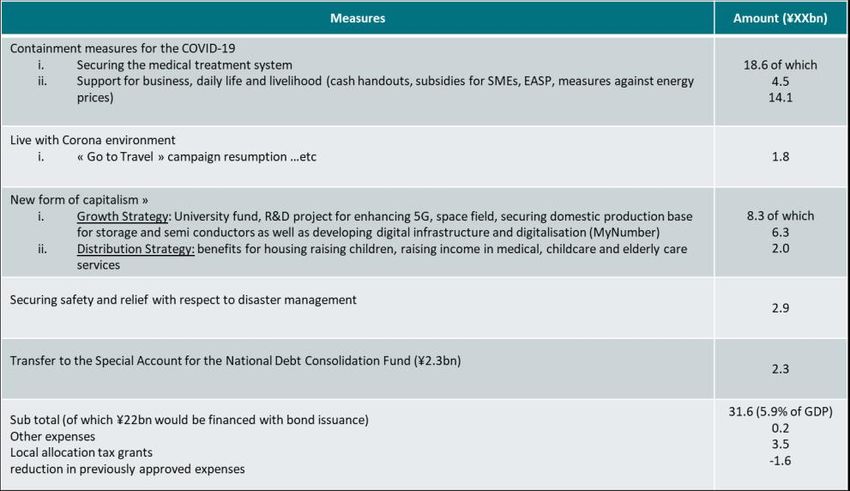

Japan

Cautious assessment on the latest supplementary budget

• Of the ¥56trn announced, only ¥31tn (5.9% of GDP) comes from government spending. Cash handouts, subsidies and vouchers will be

distributed, but excess savings that have already reached around 3.7% of GDP may dampen their take-up. On the investment side, the

package recycles some previous measures, such as digitalisation and strategic sovereignty, while spending should be smoothed over the

coming years.

Despite strong distortions, underlying inflation remains low so the BoJ kept the status quo

• October CPI reached 0.1% yoy but the figure remains significantly distorted by lower mobile phone charges that have decreased by

54%yoy, removing approximately 1.6 percentage points from the index.

• The BoJ decided to extend the termination date of the COVID loan program mainly for SMEs by six months to the end of Sep 2022.

Other measures are broadly unchanged. Contrast with other central banks is still important and Gov Kuroda insisted that inflation

excluding energy prices was subdued, so the very accommodative polices were still justified.

The expected impact of supplementary budget is likely to be lower Mobile phone charges only accounts for 1.7% but decline

reaches -50%yoy

22 Source: Cabinet Office, AXA IM Research, December 2021Growth running into constraints

Canada

Growth swings with virus

- GDP contracted more heavily in Q2 2021 than first estimated (-3.2% saar) during the most recent material COVID spread in Canada.

But it rebounded strongly (+5.4%) in Q3 as the economy re-opened. The new omicron variant poses a risk even to Canada’s highly

vaccinated population. However, Q4 growth is also likely to be impacted by flooding in November. We adjust our GDP outlook

accordingly to 4.4% for 2021 (from 4.9%), 3.7% 2022 (from 3.5%) and 2.6% 2023 (consensus 5.0%, 4.1% and 2.8%).

Labour market tightens sharply

- The labour market shows signs of recovering well. Employment jumped by 154k in November, taking it to pre-pandemic levels.

Labour supply barely rose, but at 65.3% participation is also close to its pre-pandemic 65.5%. And the unemployment rate dropped

to 6.0% from 6.7% - its lowest since February 2020. However, productivity fell by 1.2%qoq in Q3 and looks set to fall again in Q4 –

which would be a sixth consecutive fall (bar +0.1% in Q1 20).

Quarterly GDP impacted by swings in virus and restrictions Strong employment rebound matched by subdued productivity

Economic Growth (actual and first estimate) Productivity and Employment thousands

% qoq % qoq

10 15 1500

8 10 1000

36.0

6

5 500

4

2 0 0

0 -5 -500

-2 *Q4

-10 estimated -1000

-4 value

-6

GDP annualized -44.2 -15 -1500

-8

First Estimate -20 -2000

-10

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 -25 -2500

2019 2019 2019 2019 2020 2020 2020 2020 2021 2021 2021 Q1 2019 Q3 2019 Q1 2020 Q3 2020 Q1 2021 Q3 2021

Source: CANISM, AXA IM Research, Dec 2021 Source: CANISM, AXA IM Research, Dec 2021

23Constraints to spur Bank of Canada from Q2 2022

Canada

CPI inflation to fall from 2022

- CPI inflation reached 4.7% in November, its highest in 30-years. While the supply-chain issues that have helped drive prices higher

are likely persist into H2 2022, headline inflation should start to fall sharply from the start of 2022 – earlier than in most developed

economies. For now we forecast inflation at 3.4% in 2021, 3.1% in 2022 and 2.3% in 2023 (consensus 3.3%, 3.2% and 2.2%).

However, we are monitoring unit labour cost development as a key source of medium-term inflation pressure.

Market to keen on policy tightening ?

- The BoC left its overnight rate target unchanged in December at 0.25% as we and markets expected. However, expectations diverge

from here. The market prices five hikes next year, starting in January, and two in 2023, taking policy to 1.50% end-2022 and 2.00%

end-2023. The BoC has guided to policy tightening from the middle quarters of 2022. We forecast an April lift-off, but now see three

hikes in 2022. For now we forecast one more hike in 2023, but further labour market outperformance could see two to 1.50%.

CPI inflation set a new 30-year high Forecasting fewer hikes than the market

BoC o/n rate target expectations

FFR estimates

(%)

Market

2.0

AXA IM

1.5

1.0

0.5

0.0

Current Jun-22 Dec-22 Dec-23

Source: CANISM, AXA IM Research, Dec 2021 Source: Bloomberg, AXA IM Research

24Diverging recoveries, converging inflation, diverging monetary policies

Emerging Markets

Recovery paths remain Covid-19 dependent, but inflation acceleration is broad-based

- Differences in the timing of coronavirus infection waves and the type of containment policies implemented locally impact the

recovery path. Supply chain limitations have also pressured some countries’ production.

- Q3 GDP growth contracted in Malaysia, Thailand, South Africa, Brazil and Mexico, but came out stronger in Chile, Colombia, Turkey

and CEE region.

Inflation accelerates further. Normalization in monetary policies on diverging trends.

- Inflation further accelerated in EM mainly driven by external factors, domestic demand plays only a limited role in the recent pick-up in

inflation. Still, EM central banks are reacting to higher inflation by delivering hikes and keeping a hawkish rhetoric.

- Year-to-date, 32 EM banks have hiked rates this year and more hikes are likely, although some central banks, such as Russia or Mexico,

have probably already done most of the heavy-lifting ahead of the upcoming Fed lift-off.

Inflation rates are more consistently above targets… … results in monetary tightening (almost) everywhere

Source: Datastream, AXA IM Research, November 2021 Source: Datastream, AXA IM Research, November 2021

25Turkey : playing dangerously

Emerging Markets

Turkey’s inflation expectations de-anchoring

- November’s CPI inflation stood at 21.3% yoy, yet again above consensus expectations. Underlying trends in core CPI show persistent

inflation and an evident FX pass-through. PPI inflation jumped 10% on the month, +54.6% yoy.

Further easing in December likely, but current monetary policy stance becomes increasingly difficult to sustain

- CBRT has cut rates by a cumulative 400bps since September, despite seeing already very high and accelerating inflation rates. Despite

secular deterioration in price dynamics, another cut appears on the cards at the December meeting given political interference.

- A considerably tighter stance is badly needed to anchor expectations and stabilise the currency. Economic dollarisation is accelerating:

64% of Turkish bank deposits are FX-denominated. A U-turn in the monetary policy should occur in 2022: the sooner, the better.

A dissonant easing cycle in Turkey … … accelerating dollarization of the economy

Source: Datastream, AXA IM Research, November 2021 Source: Datastream, AXA IM Research, December 2021

26Investment Strategy

Multi-Asset Investment views

Our key messages and convictions

Positive on equites

#1 Neutral on

Despite a slowdown in Investment Grade

economic activity, #2 Credit

corporate earnings Despite support

continue to rebound from fiscal

initiatives,

valuations are no

longer attractive

due to tight

#3 spreads

Government

Negative on bond yields

Sovereign Bonds expected to rise #4

as Central Banks Slowing Chinese demand,

tighten monetary and increased supply, as Negative on

policy production normalises, Commodities

weighs on commodity

prices

Source: AXA IM as at 15/12/2021

28FX & Rates Strategy The Omicron stress test emerges while inflation still matters • The emergence of the Omicron variant has been a fitting reminder of the importance of monetary policy expectations in driving currency moves, as the dollar’s reaction was to depreciate against the euro upon a partial unwind of Fed policy expectations. As Omicron concerns subsided and the Fed Chair made some hawkish comments on inflation, a more aggressive hiking cycle was priced-in again. Beyond that, the terminal rate seems underpriced; expectations for it to rise may bring additional support to USD early in 2022. • Inflation expectations are a key performance factor for the months to come, as in 2021. US CPI pricing two years forward does not look too aggressive if we account for inflation risk premium that inflation-linked investors demand given uncertainty about future inflation. This should be rather comforting for the US Fed, albeit with some caution, as survey-based inflation expectations have picked up notably. Uni of Michigan survey hints at 3% in five to ten years, while the NY Fed survey indicates inflation expectations above 4% in three years. The delta variant spread in Europe accelerated euro depreciation Inflation risk premium compensating for inflation uncertainty Source: Bloomberg and AXA IM Research, December 2021 Source: Bloomberg and AXA IM Research, December 2021 29

Credit & Equity Strategy

Returns weaker in November as govie curves bear flatten; risky assets are shaken but not stirred

• The credit spread widening in November is consistent with the more aggressive pricing of the US Fed’s rate hiking cycle, as credit spreads tend

to widen when govie curves bear flatten. Sentiment steadied in December, and spreads retraced. The recent correction hardly registers in the

grand scheme of things. Unless Omicron derails the global recovery, we remain constructive for credit in 2022 amid strong credit fundamentals.

• The Omicron variant does not alter our constructive longer-term outlook for stocks either, being a rather short-term catalyst. More aggressive

pricing of US monetary policy was also a headwind, as stocks don’t tend to perform well when the govie curve bear flattens. Global equities

declined by 1.1% over the month; cyclicals outperformance over defensives came to a halt; the value/growth rotation remained stable.

• The current environment of policy divergence between US and Europe as the transitory inflation message appears no longer viable in the US,

raises the risk of Fed policy spillover on European risk premia. Yet by our estimates this risk appears rather modest, as the beta of implied

volatility between European and US equities is currently near historic lows (1st quartile).

November spread widening hardly registers in the grand scheme of things US monetary policy contagion on European stocks appears limited

Source: ICE and AXA IM Research, December 2021 Source: CBOE and AXA IM Research, December 2021

30Asset allocation stance

Positioning across and within asset classes

Asset Allocation Equities Fixed Income

Key asset classes Govies

Developed

Equities Euro core

Euro area

Bonds Euro peripheral

UK

Commodities UK ▼

Switzerland

Cash US

US ▲

Inflation Break-even

Japan

US

Emerging & Equity Sectors

Euro

Emerging Markets

Credit

Europe Cyclical/Value

Euro IG

Euro Opening basket ▼

US IG

Euro Financials

Euro HY

US Financials US HY

US Russell 2000 ▲ EM Debt

EM Bonds HC

Legend Negative Neutral Positive Change ▲ Upgrade ▼ Downgrade

Source: AXA IM as at 15/12/2021

31Forecasts & Calendar

Macro forecast summary

Forecasts

2021* 2022* 2023*

Real GDP growth (%) 2020

AXA IM Consensus AXA IM Consensus AXA IM Consensus

World -3.2 5.7 4.2 3.6

Advanced economies -5.0 4.9 3.8 2.4

US -3.4 5.5 5.5 3.5 4.0 2.7 -

Euro area -6.7 5.0 5.0 3.9 4.3 2.1 -

Germany -4.9 2.6 2.7 3.5 4.3 1.9 -

France -8.0 6.7 6.5 3.6 3.8 2.0 -

Italy -8.9 6.2 6.1 3.7 4.2 1.9 -

Spain -10.8 4.3 5.0 5.5 5.9 3.0 -

Japan -4.9 1.9 2.2 3.5 3.0 1.6 -

UK -10.0 6.8 6.9 5.0 4.7 2.3 -

Switzerland -2.5 3.5 3.4 3.0 3.0 1.6 -

Canada -5.3 4.4 5.0 3.7 4.1 2.6 -

Emerging economies -2.0 6.2 4.4 4.3

Asia -0.8 6.8 5.1 5.1

China 2.3 7.9 8.0 5.0 5.1 5.3 -

South Korea -0.9 4.0 4.0 2.6 3.1 2.1 -

Rest of EM Asia -4.6 5.8 5.5 5.3

LatAm -7.1 6.2 2.6 2.5

Brazil -4.1 5.1 4.9 1.2 1.1 2.0 -

Mexico -8.5 6.0 5.9 2.6 2.9 2.2 -

EM Europe -2.1 5.9 3.8 2.8

Russia -3.0 4.5 4.2 3.2 2.6 2.0 -

Poland -2.7 5.1 5.1 5.0 5.0 3.6 -

Turkey 1.8 9.5 8.9 3.6 3.5 3.0 -

Other EMs -2.4 4.2 4.1 3.9

Source: Datastream, IMF and AXA IM Macro Research − As of 16 December 2021 * Forecast

33Expectations on inflation and central banks

Forecasts

Inflation Forecasts

2021* 2022* 2023*

CPI Inflation (%) 2020

AXA IM Consensus AXA IM Consensus AXA IM Consensus

Advanced economies 0.7 3.1 3.1 2.2

US 1.2 4.7 4.4 4.1 3.7 2.9 -

Euro area 0.3 2.6 2.4 2.7 2.3 1.8 -

Japan 0.0 -0.2 -0.2 0.7 0.7 0.6 -

UK 0.9 2.4 2.4 3.8 3.7 1.9 -

Switzerland -0.7 0.5 0.5 0.6 0.7 0.7 -

Canada 0.7 3.4 3.3 3.1 2.9 2.3 -

Source: Datastream, IMF and AXA IM Macro Research − As of 16 December 2021 * Forecast

Central banks’ policy: meeting dates and expected changes

Central bank policy

Meeting dates and expected changes (Rates in bp / QE in bn)

Current Q4-21 Q1-22 Q2-22 Q3-22

2-3 Nov 25-26 Jan 3-4 May 26-27 July

Dates

United States - Fed 0-0.25 14-15 Dec 15-16 Mar 14-15 June 20-21 Sep

Rates unch (0-0.25) unch (0-0.25) unch (0-0.25) unch (0-0.25)

28 Oct 20 Jan 14 April 21 July

Dates

Euro area - ECB -0.50 16 Dec 10 Mar 9 June 8 Sep

Rates unch (-0.50) unch (-0.50) unch (-0.50) unch (-0.50)

27-28 Oct 17-18 Jan 27-28 April 20-21 July

Dates

Japan - BoJ -0.10 16-17 Dec 17-18 Mar 16-17 June 21-22 Sep

Rates unch (-0.10) unch (-0.10) unch (-0.10) unch (-0.10)

4 Nov 3 Feb 5 May 4 Aug

Dates

UK - BoE 0.10 16 Dec 17 Mar 16 June 15 Sep

Rates +0.15 (0.25) unch (0.25) +0.25 (0.50) unch (0.50)

Source: AXA IM Macro Research - As of 16 December 2021

34Calendar of 2021-2022 events

2021 Date Event Comments

December 31 Dec LIBOR fixings discontinued

2022 Date Event Comments

Q3-Q4 2022 Chilean Constitutional Referendum

Jan Italian Presidential Elections

Jan FOMC to commence taper (expected)

Jan Build Back Better Act passed (expected)

January

1 Jan EU introduces Rules of Origin requirements

20 Jan ECB Meeting Unchanged (-0.5)

25-26 Jan FOMC Meeting Unchanged (0-0.25)

Feb BoE Meeting Unchanged (0.1)

6 Feb Costa Rican General Elections

March FOMC Meeting Unchanged (0-0.25)

March China Annual National People’s Congress

9 March South Korea Presidential Elections

March

13 March Colombian Legislative Elections

31 March UK Business rates relief ends

31 March UK Reduced VAT for hospitality and tourism ends

6 April UK National Insurance contributions increase 1.25ppt

6 April UK Dividend Tax increase by 1.25ppt

April

6 April UK Super-deductibility for UK investment begins

10 & 24 April French Presidential Elections

May Philippines Elections

May 5 May UK Elections in Scotland, Wales, and Northern Ireland and UK Local Elections in England

29 May Colombian Presidential Elections

June 12 & 19 Jun French Legislative Elections

July 1 July UK border checks on EU imports scheduled to resume

August Aug US Federal Reserve Jackson Hole Symposium

Oct China’s 20th National Congress- President Xi to be re-elected (expected)

October

2 Oct Brazil General Elections

November 8 Nov US Midterm Elections

35Latest publications 2022-2023 Macroeconomic Outlook: Pandemic effects to recede, policy starts to tighten 1 December 2021 Tapering, profit and equity prices 15 November 2021 China: Riding the green wave 3 November 2021 Investment management and blockchain: The great reshuffle 22 October 2021 October Global Macro Monthly – Transition costs to net zero: significant but necessary 20 October 2021 The cost of climate change: Action versus inaction 30 September 2021 German elections: The post-Merkel era 23 September 2021 September Global Macro Monthly –Supply constraints add to inflation angst 22 September 2021 Asia: “Made in Vietnam”- Understanding the rise of Vietnam as an export powerhouse 14 September 2021 Fit for 55: A carbon pricing upheaval 27 July 2021 36

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date. All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries. © AXA Investment Managers 2021. All rights reserved 37

You can also read