Q1 2019 QUARTERLY LETTER - APRIL 2019 - Keebeck Wealth Management

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

KEEBECK QUARTERLY LETTER

Q1 2019

Q1 2019 QUARTERLY LETTER – APRIL 2019

EASY MONEY, EVOLVING MODERN POPULISM, AND THE POTENTIAL POLICY SHIFT LEFT

In our first quarterly letter of 2019, we highlight the

driver of the sharp bounce in the market during the

first quarter - mainly the Federal Reserve (Fed)

pivot. We look at this in the longer-term context,

explore the growing side effects of easy money, and

culminate with in-depth research on the Left-leaning

proposals coming out of the new Congress and

potential presidential candidates. We dedicate

significant space in this letter to these particular

policies, as even watered-down versions can have

substantial ramifications for long-term wealth

creation and markets moving into 2020 and far beyond.

If you would like to refer back to our previous two quarterly letters, you can find them here and here.

- Mathew Klody, CIO

1

KEEBECK QUARTERLY LETTER

Q1 2019

Introduction

“We have the wolf by the ears, and we can neither hold him nor

safely let him go. Justice is in one scale, self-preservation in the

other.”

“But this momentous question, like a firebell in the night,

awakened and filled me with terror. I considered it at once as the

knell of the Union. It is hushed, indeed, for the moment. But this

is a reprieve only, not a final sentence.”

- Thomas Jefferson in a Letter to John Holms, April 22, 1820 (on

slavery and the Missouri question.)

Thomas Jefferson wrote these words in a letter to John Holms towards the tail end of his life. The issue he

was writing about was slavery and the Missouri Compromise of 1820, which temporarily maintained the

balance of power between north and south. In effect, by not addressing slavery head on, it kicked the can

down the road, calcified the battle lines politically and geographically, let imbalances and discord grow, and

virtually assured the Civil war was the only way to end slavery.

There are a few powerful quotes you hear in life that sear themselves into your permanent memory. As a

student of history, Jefferson’s “Wolf by the Ears” and “Firebell in the Night” are two of those quotes that

stand out in particular to me, as they foretold the coming of the Civil War. While the wolf analogy requires

little elaboration, being startled awake by a firebell in the night, particularly in the early 1800s, must have

been a frightening thing. In densely populated, often primarily wooden towns, a fire not quickly contained

could soon spread and destroy a sizeable part of the community.

Considering what has transpired the past six months regarding the markets, the extreme pivot of the Fed’s

response, and the growing side effects, I can’t help but think of these quotes. Just as the Missouri

Compromise delayed eventual progress culminating in the Civil War, similarly the easy money policies of the

Fed and other global central banks have pushed off true economic and market discovery while increasing

societal disparity. This, combined with changing technology and media consumption, is creating an

environment where perceived crony capitalism is fostering a more direct and aggressive populist evolution

in politics. This trend is significantly increasing the likelihood of far more radical policies which could be

quite unfriendly to capital and growing wealth. As your wealth advisor, we thought this big rock theme

merited sharing our thoughts in the majority of this first quarter letter.

2

KEEBECK QUARTERLY LETTER

Q1 2019

In the following pages we explore some of the proposals coming out of the new Congress and 2020

presidential candidates. Many are more extreme than the nation has seen in quite a while. The bottom

line is that there is a real chance the basic rules may change significantly which merits thought,

preparation, and getting ahead of the curve should the nation choose that path.

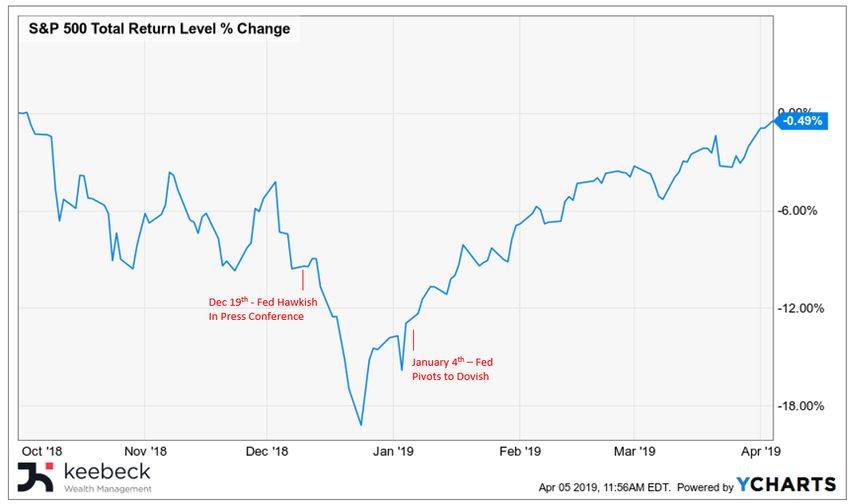

Easy Money

Late in the fourth quarter, with the market in the midst of a rapid and violent

correction, the Jerome Powell led Federal Reserve decided to pivot approximately

180 degrees, creating a ferocious “risk on” rally. This stunning policy shift came

in the form of a less aggressive rate hike pace (or none at all) and signaled an end

to QT (“quantitative tightening”), the effort to restore the Fed’s balance sheet to

a less bloated level following a decade of dramatic expansion.

Source: EL @evan_lorenz - Twitter

S&P 500 Total Return Oct 1st 2018 – April 4th 2019

In our last quarterly letter that was published just three months ago, we wrote the following:

“Along these lines, the Federal Reserve has come under a lot of criticism in recent months. Even the

President himself has publicly criticized the Fed which is rare and considered blasphemy in techno and

plutocratic circles. W e think that for the first tim e in a very long tim e, the Fed is doing w hat

should be its job - to let m arkets function freely and achieve true price discovery. In the

3

KEEBECK QUARTERLY LETTER

Q1 2019

long term , for a free m arket capitalist system to thrive, or even just survive, price

discovery is the single m ost im portant factor. When price discovery is crippled as it has been

over the past decade, efficient allocation of resources cannot occur. When the cost of capital is

severely manipulated, over and underinvestment occurs and in response asset bubbles and crashes,

wealth inequality becomes more extreme, and politics become unstable.” [1]

In contrast to the paragraph above, the Fed once again took the easy route, capitulating to markets and

kicking the can down the road for the umpteenth time. True asset price and economic discovery, providing

long term confidence that the economy and market foundation are not simply built on quicksand (“artificial

markets”, as colleague Bruce Lee calls them) will once again have to be put off indefinitely. Of course, this

policy is not new. The chart below shows the other major instances over the past decade where basically

the same retreat occurred. In addition, there have been a bunch of smaller ones (Bank of Japan QE, Swiss

QE, European negative rates, etc.), but we don’t have enough room on this chart to label them all.

Federal Reserve Market Intervention

4

KEEBECK QUARTERLY LETTER

Q1 2019

A good analyst must ask the following questions. With unemployment at multi-generational lows here in

the US and wage inflation accelerating, what does the Fed know that everyone else does not? Our contacts

in the building sector provide common anecdotes of laborers being poached from job sites on higher wage

offers. Our contacts in the trucking sector describe the continued driver shortage. What massive risks lurk

that warrant this shift with such a robust economy? What sort of tell is this?

Wage Inflation

Source: Goldman Sachs

5

KEEBECK QUARTERLY LETTER

Q1 2019

Maybe the simplest answer is that these policymakers fear that they have the “wolf by the ears” and are so

darn afraid to let go that this “compromise” is what they perceive to be the only option. Is it just me, or

is it slightly concerning that the bull case is simply that central banks must keep easy money flowing

because the downside of letting the wolf’s ears go is unthinkable? The Fed is not acknowledging the

growing side effects of this addiction. So, the compromise endures, and the imbalances and side effects

fester and grow.

Side Effects

A few years ago, I saw an NFL network program called “A Football Life”[2] on Lyle Alzado, the former NFL

star who was one of the first to admit to the use of steroids, which he believed ultimately caused his

inoperable brain cancer and death at the age of 43.

"I started taking anabolic steroids in 1969 and never stopped. It was addicting. I’m sick, and I’m scared. Ninety

percent of the athletes I know are on the stuff. We are not born to be 300 pounds or jump 30 feet…All the time I

was taking steroids, I knew they were making me play better. But I became very violent on the field and off it. I

did things only crazy people do. Once a guy sideswiped my car and I beat the hell out of him...Now look at me.

My hair is gone. I wobble when I walk and I have to hold on to someone for support. I have trouble remembering

things. My last wish? No one should ever die this way." [3]

Side effects are real, and nothing of scale in our modern economy or society happens in a vacuum. There

are few free lunches. Let’s look at what I consider to be the primary side effect of easy money, one that

began small, but is quickly metastasizing into one of the most prevalent and public topics of the day; a

topic that will only gain steam as we move into 2020. The side effect is Populism. Here’s a look at its

evolution.

6

KEEBECK QUARTERLY LETTER

Q1 2019

Easy Money Side Effect = Accelerating Modern Populism

The modern populist movement arose in the early days following the Great Financial Crisis, a response to

early government bailouts and quantitative easing. The Tea Party movement was launched following a

February 19, 2009 on-air call for a “tea party” by CNBC reporter Rick Santelli from the floor of the Chicago

Mercantile Exchange.[4] In response, conservative activists agreed to coalesce against Obama's agenda and

scheduled a series of protests. This movement quickly expanded, calling for smaller government, railing

against government bailouts, crony capitalism, easy money, etc. Many traditional, blue blooded

establishment Republicans were tossed out of office by tea party activists, and the movement helped the

Republicans take back congress in 2010.

This was followed a few years later by "We are the 99%" which became a slogan of the Occupy movement

after a Tumblr blog was launched in late August 2011 by a 28-year-old New York activist. The concept is

said to have been derived from economist Joseph Stiglitz's May 2011 article "Of the 1%, by the 1%, for the

1%" in Vanity Fair, in which he criticized the economic inequality present in the United States.[5] While this

movement was more Left-leaning in nature, what it had in common with the Tea Party movement, and

what gave it legs, was the dissatisfaction with the perception of crony capitalism arising from post-Great

Financial Crisis policies.

In 2015 and 2016, presidential candidate Donald Trump capitalized on the growing dissatisfaction and drew

populist support from both the Right and the Left effectively winning him the presidency. While

campaigning, the sitting Republican president of our country said the following in an economically

depressed former steel town of Monessen in western, PA in 2016. He noted among other things that

“globalization has destroyed the middle class.” “…[Made the] financial elite who donate to politicians very

wealthy… Our politicians took away from the people their means of making a living and supporting their

families. Many Pennsylvania towns once thriving and humming are now in a state despair. The people who

rigged the system for their benefit will do anything - and say anything - to keep things exactly as they

are.” [6] This is the sitting president of the United States, a very wealthy man himself, capitalizing on a

populist platform. He won this region, historically a strongly democratic area, using populism. The growing

undercurrent should not be minimized here.

7

KEEBECK QUARTERLY LETTER

Q1 2019

More than anything, despite political and philosophical differences, the commonality of feeling “pissed off”

and a sense of injustice in policymaker responses to the GFC trumped those traditional Left/Right

differences. This anger has slowly been building for years and strangely comes during a period when the

US economy is robust by most measures. However, it is not simply an economic issue as federal reserve

officials, economists, and policymakers try to base their models on. It is the human element, the moral

compass, and the basic concept of right and wrong which is at play here. Growing populist or even

“Socialist” rhetoric seems to not be a rejection of capitalism, but a rejection of the perceived crony

capitalism that has proliferated over the past decade.

The perception of a corrupt aristocratic

bogeyman pulling the strings of the nation to tilt

it to their advantage has gone mainstream. The

recent college admissions scandal only serves to

further embed that viewpoint. Bloomberg

Businessweek, a business and wealth friendly

publication, wrote in March, “The sweeping

indictment underlined how deeply unfair U.S.

higher education has become. Success in the

modern economy often seems to be more an

accident of birth...than a reward based on

individual ability and achievements. It’s an impression that cuts deep.” [7]

On this topic, the following chart

surprisingly shows that the U.S. is more in line with second and third world nations than modern, advanced

economies when it comes to inter-generational educational and income mobility. The risk here is that higher

inequality typically means lower economic growth over the long term.

8

KEEBECK QUARTERLY LETTER

Q1 2019

Source: Inequality is Holding Economies Back: Education Could Be One Solution – Bloomberg Businessweek

Ray Dalio, head of Bridgewater, one of the world’s largest asset managers, noted in November that

“Today’s debt cycle is most reminiscent of the late 1930s, a time of rising populism and growing disparity

between the rich and poor.” [8] The 1930s is never a good historical reference period when speaking about

economies or politics.

Populism in the current age is much less

about left or right. It is more a call for

correcting a perceived rigged system. (It’s

worth noting and remembering that the

average person today in America lives far

better than the wealthy of Rockefeller’s day

in terms of technology, amenities, and cost of

food as a percentage of income.) Material

progress has been made in advancing the

standard of living, primarily through free

markets and economies and largely without

easy money.

9KEEBECK QUARTERLY LETTER

Q1 2019

However, for today, Trump’s success in getting elected on a populist platform and outflanking the Left on

this issue created a significant political vacuum which opportunistic Left-leaning politicians are now

exploiting and gaining significant traction.

The Left – Reasserting Itself Under A Populist Mantle

Colleague Derek Feilmeier, in researching these topics, writes:

“In a time when wealth inequality is growing, young Americans are looking for ways to fix a system that

they believe has failed them. A recent study by the Federal Reserve Bank of St Louis found millennials who

were born in the 1980s have a net worth 34% below what was expected. According to various polls,

millennial support for socialism is on the rise. An August 2018 Gallup poll suggested that 51% of Americans

between the ages of 18 and 29 have a positive view of socialism compared to only 45% for capitalism. An

October 2018 poll by Buzzfeed News and Maru/Blue found that 48% of millennial Democrats identify

themselves as socialist or democratic socialist.”

This is the current phase of populism, and these concepts are

gaining mainstream attention as evidenced by Democratic Socialist

Alexandria Ocasio-Cortiz (“A.O.C.”). Gaining nationwide acclaim, she

graced the cover of Time Magazine last month under the nickname

“The Phenom.”[9]

She recently proposed The Green New Deal, which is estimated to

cost many trillions, and would be on scale with FDR’s New Deal

during the Great Depression.[10]

Drawing on the example of quantitative easing, many are embracing

MMT or “Modern Monetary Theory” as a way to pay for the plan.

MMT contends that a government that prints its own currency is not

constrained in spending by tax revenue. The logic is that if we can

print money (QE) to boost asset prices, why can’t we use it to boost wages and increase employment?

The major side effect of this line of thinking is a sharp increase in Left-wing populism. We have been

closely following proposals by both the new Democrat-led congress and 2020 presidential candidates and

10KEEBECK QUARTERLY LETTER

Q1 2019

have provided a list below. We have also attached an Appendix outlining many of these proposals along

with links to more in-depth articles.

• Sen. Elizabeth Warren, D-Mass. - 2 percent annual “wealth tax” on Americans who have more

than $50 million in assets, and a 3 percent tax on those with a net worth of more than $1 billion.

That tax would be on top of any income taxes they already pay. She also wants to break up tech

giants like Facebook, Google and Amazon and end the electoral college.

• Sen. Bernie Sanders, I-Vt, - increase the federal estate tax to 77 percent on the wealthiest 0.2

percent of Americans.

• Sen. Kamala Harris, D-Calif., - give middle-income households cash payments of up to $6,000 a

year per family. The payments would be offset by repealing the 2017 GOP tax cuts and creating a

fee on large financial institutions.

• Sen. Cory Booker, D-N.J., - create savings accounts for every American child, paid for by an

increase in the capital gains and estate taxes.

• Sen. Kirsten Gillibrand, D-N.Y., Rep. Tulsi Gabbard, D-Hawaii, and former Maryland

congressman John Delaney - all of these presidential hopefuls have denounced the Republican

tax cuts.

• Julian Castro, a former Obama administration cabinet official, has said he supports raising the

corporate tax rate to make sure companies “pay their fair share.”

• Freshman Rep. Alexandria Ocasio-Cortez, D-N.Y., - top marginal tax rate of 70 percent — a

rate not seen since before President Ronald Reagan implemented a series of tax cuts in the 1980s.

Most of these proposals boil down to much higher taxes on income, capital gains, and wealth and estates.

Markets generally tend to discount six to twelve months out, so that gives investors six to nine months to

position themselves for how 2020 will play out.

Potential Impact

In anticipation of lower personal and

corporate tax rates following Trump’s

election, markets rallied dramatically,

up over 30% in the year following

the election through the passage of

the tax bill, which cut the corporate

rate significantly from 35% to 21%.

The chart to the right shows the

market boost by way of the Russell

2000 which has a higher percentage

of US revenue than the S&P 500.

11KEEBECK QUARTERLY LETTER

Q1 2019

If the tax cuts were to reverse, it would be logical for the opposite to happen over time. There also could

be some positives for high property and personal tax states, if the State and Local Tax (SALT) limitations

are reversed.

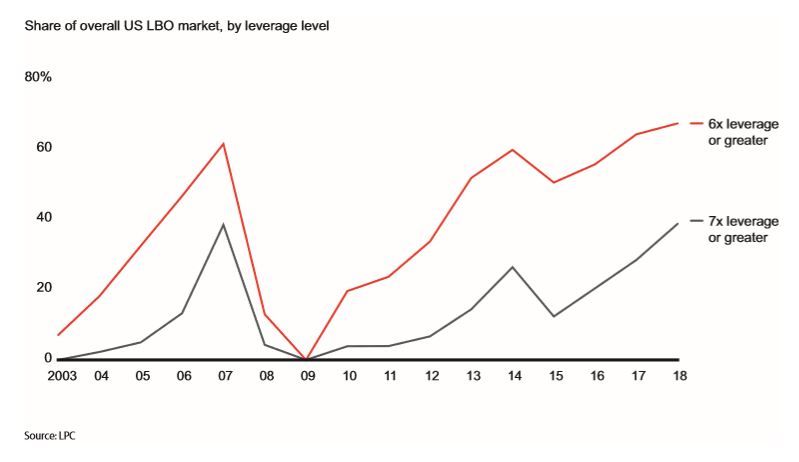

Private equity valuations are currently expensive as we noted in our October letter.

2018 marked the first year that the majority of private equity firms were acquired by other private equity

firms. As one of the strongest performing asset classes in recent decades, it is consequently one of the

most popular. (See page 7 of our 3Q18 letter for more on this.)

12KEEBECK QUARTERLY LETTER

Q1 2019

The carried interest provision of the tax code (which taxes this form of private equity executive

compensation as long-term gains) would be an obvious area of tax reform to be amended under a Left-

leaning administration and congress. In fact, the Trump administration originally tried to get this change

through, but powerful lobbying kept it out of the tax bill.[11] In anticipation of that, it is conceivable that

private equity partners, sitting on significant unrealized gains, would be incentivized to begin to liquidate

existing holdings, even at lower prices. With valuations elevated to start, this wouldn’t be positive.

Another factor aside from valuation keeping us cautious at this stage of the cycle is leverage, which has

overall increased over the past decade. It is worth remembering the amplified downside leveraged

businesses can bring under adverse conditions.

Kraft Heinz, a name that I have followed for years, could go down as a case study for this.

Nearly three years ago, global QE, combined with the onset of Brexit, caused fixed income yields to fall

close to record lows. As a result, consumer staples became richly valued, and low rates had investors piling

into this group as “bond proxies” often paying 25-30x earnings for slow growing or shrinking businesses. At

this time I began searching for short opportunities in this space.

https://www.grantspub.com/userfiles/files/g34n06bz-GADG.pdf

13KEEBECK QUARTERLY LETTER

Q1 2019

In the Applied Private Equity class I taught at the University of Notre Dame last fall, I felt it was important

to drill down on the concept that, despite the recent boom, one can pay too much, take on too much

leverage, and cut too deeply into muscle in short-sighted efforts to boost EBITDA. There can be adverse

long-term consequences.

Investment fads and fashions come and go, but it is important to focus on intrinsic value. Kraft Heinz was

an investment grade corporate credit prior to all this. As we noted in our 4th Quarter letter, there has been

an explosion in investment grade debt, particularly BBB rated debt over the past decade. This serves as a

reminder as to why our current investment philosophy is to underweight US corporate debt at current

values.

There is much potential value to be added through private equity. It enables companies to take a longer-

term view often not possible for public companies. It is often effective at bringing value added solutions

and efficiencies to businesses from specialists who have repeatedly done this. However, excesses develop

in all asset booms, and PE has seen one of the longest booms in history. Bottom line, patience may be

rewarded with better values down the road for both PE and corporate debt.

14KEEBECK QUARTERLY LETTER

Q1 2019

Outlook

Typically, our asset class views won’t change over the very short term, unless there is significant movement

in asset prices or fundamentals. “Staying on our blocks” is usually the best approach long-term. Here are

some of our current views:

• Overweight international and emerging markets and non – dollar securities

• Underweight corporate debt & heavily leveraged securities

• Underweight private equity

• Overweight value vs. growth

• Overweight short duration vs. long duration

• Overweight domestic housing

We think that as this potential shift left continues, the unsustainability of the strong dollar will come to light,

and this calls for additional international exposure. More spending, more printing and a weaker dollar

ultimately is inflationary, and with long-term fixed income yields still hovering near historic lows, little

appears to be gained by having long duration assets. Outperforming with long duration assets from this

point means that the world has slowed down far more than anyone is counting on, and thus equities will

likely be cheaper.

We continue to be tactical, opportunistic, and committed to seeking out unique and differentiated assets

that can add value over the long term.

Conclusion

While this is a less conventional letter, we believe the topics discussed within could be some of the most

important factors when it comes to wealth management in the coming years. We feel it is important to get

ahead of the curve on these topics and be prepared well in advance in terms of both asset class reaction

and suggested structuring. We will continue to research these topics and look forward to discussing these

points further with you.

Sincerely,

Mathew T. Klody, CFA

Chief Investment Officer

Keebeck Wealth Management, LLC

mklody@keebeck.com

15KEEBECK QUARTERLY LETTER

Q1 2019

APPENDIX - Sources

[1]: https://usercontent.vestorly.com/5b2d0969e64b34001babd5f6/1546991934/keebeckquarterlyletter4q18.pdf

[2]: https://www.imdb.com/title/tt4241248/

[3]: https://www.si.com/vault/1991/07/08/124507/im-sick-and-im-scared-the-author-a-former-nfl-star-has-a-dread-disease-

that-he-blames-on-his-use-of-performance-enhancing-drugs

[4]: https://www.cnbc.com/id/29283701

[5]: https://www.vanityfair.com/news/2011/05/top-one-percent-201105

[6]: https://www.politico.com/story/2016/06/full-transcript-trump-job-plan-speech-224891

[7]: https://www.bloomberg.com/news/articles/2019-03-20/if-america-can-t-fix-education-it-won-t-beat-inequality

[8]: https://moneyandmarkets.com/dalio-populism-income-inequality-rates-1930s/

[9]: http://time.com/longform/alexandria-ocasio-cortez-profile/

[10]: https://www.factcheck.org/2019/03/how-much-will-the-green-new-deal-cost/

[11]: https://www.nytimes.com/2017/12/22/business/trump-carried-interest-lobbyists.html

APPENDIX - 2020 Democratic Candidate Headlines

Andrew Yang

- This Presidential Candidate Wants to Give Every Adult $1,000 a Month – Time 02/13/2019

- $1,000 monthly in universal basic income gets put to a test – CBS 02/12/2019

Julian Castro

- (via Twitter): "We’ll work to make the first two years of college, a certification program or an apprenticeship accessible

and affordable, so millions more people get the skills they need to get a good job without drowning in debt." -

@JulianCastro 01/12/2019

- 2020 Democrat Julian Castro wants to abolish the Electoral College, too – The Week 03/20/2019

Kamala Harris

- Kamala Harris pitches big increase in teacher pay – Politico 03/23/2019

- Harris promises family tax credits, free community college in Las Vegas speech – Nevada Current 03/01/2019

- Kamala Harris Wants to Give Middle Class Families $500 Every Month. Her Plan Is Bold, Generous, and Maybe Ill-

Conceived. – Slate 10/22/2018

- Almost all of Sen. Harris’s $2.8 trillion tax plan would help middle and working class, study finds – Washington Post

11/15/2018

- Kamala Harris unveils $315 billion plan to boost teacher pay – NBC 03/26/2019

Cory Booker

- Study: Cory Booker’s baby bonds nearly close the racial wealth gap for young adults – Vox 2/1/2019

- An exclusive look at Cory Booker’s plan to fight wealth inequality: give poor kids money – Vox 10/22/2019

- Cory Booker calls for term limits on the Supreme Court – MSNBC 03/18/2019

- Cory Booker’s new big idea: guaranteeing jobs for everyone who wants one – Vox 04/20/2018

16KEEBECK QUARTERLY LETTER

Q1 2019

Elizabeth Warren

- Elizabeth Warren Proposes Breaking Up Tech Giants Like Amazon and Facebook – NYT 03/08/2019

- Sen. Elizabeth Warren to Propose a Wealth Tax on Those With Assets Over $50 Million – Fortune 01/24/2019

- Elizabeth Warren Urges Universal Child Care, ‘Ultra-Millionaire’ Tax – Newsmax Finance 02/19/2019

- Elizabeth Warren Calls for Ending Electoral College – NYT 03/18/2019

Bernie Sanders

- Bernie Sanders still wants tuition-free college – CNN 04/04/2017

- Bernie Sanders wants to save Social Security by raising taxes on people making more than $250,000 – CNN 02/13/2019

- Bernie Sanders proposes a big hike in the estate tax, including a 77% rate for over $1 billion – CNBC 01/31/2019

- Bernie Sanders: ‘Damn right I will’ raise taxes on the rich - Washington Examiner 02/25/2019

- How Bernie Sanders is turning ‘Medicare for All’ into a major 2020 liberal litmus test – CNN 02/26/2019

Jay Inslee

- 2020 candidate Jay Inslee says he can’t defeat climate change unless filibuster and Electoral College go – Washington

Examiner 03/20/2019

- Jay Inslee Calls for the Nuclear Option to Combat Climate Change – Mother Jones 03/10/2019

John Hickenlooper

- Colorado’s Hickenlooper urges bipartisan tax reform changes: ‘Trickle down economics is a fairytale’ – The Denver

Channel 11/29/2017

Beto O’Rourke

- Beto O’Rourke Joins Calls for Wealth Tax to Avoid ‘Kings and Queens’ – Bloomberg 03/22/2019

- Beto O’Rourke takes moderate path with Medicare for America – CNN 03/23/2019

- Beto calls for nationwide marijuana legalization: ‘Why are we still arresting and jailing people?’ – Washington Times

03/24/2019

- Beto O’Rourke lends support to Green New Deal in Iowa campaign stop: ‘Literally the future of the world depends on us,

right now’ – CNBC 03/14/2019

- ‘I’d take the wall down,’ says Beto O’Rourke of current border barriers – NBC 02/14/2019

Alexandria Ocasio-Cortez (not a candidate)

- Ocasio-Cortez suggests marginal income tax rates as high as 70% - MarketWatch 01/04/2019

- Alexandria Ocasio-Cortez says ‘Medicare for all’ could be paid for by Pentagon waste – Washington Examiner

12/03/2018

- Tech monopolies are killing journalism, Ocasio-Cortez says – CNBC 01/28/2019

- Ocasio-Cortez defends $40 trillion price tag for progressive proposals – CNN 09/16/2018

- Rep. Alexandria Ocasio-Cortez Releases Green New Deal Outline – NPR 02/07/2019

- Alexandria Ocasio-Cortez targets New York’s campaign finance laws – NY Post 02/27/2019

- Alexandria Ocasio-Cortez ‘Biggest Villian’ in Amazon Deal Crash – The Jerusalem Post 03/19/2019

- Alexandria Ocasio-Cortez Wants To Raise Taxes On The Rich – And Americans Agree – FiveThirtyEight 01/18/2019

- Alexandria Ocasio-Cortez Criticizes Capitalism, Political Moderates at SXSW – Rolling Stone 03/10/2019

17KEEBECK QUARTERLY LETTER

Q1 2019

APPENDIX - Biography

Mathew T. Klody, CFA is the Chief Investment Officer at Keebeck Wealth

Management, LLC.

Mathew is also an adjunct professor of finance at the University of Notre Dame.

Prior to joining Keebeck, Mathew was the Founder, Managing Partner and Portfolio

Manager of MCN Capital Management, LLC, the advisor to a private long short

investment partnership.

Mathew was the Senior Vice President and Analyst at Chicago-based Sheffield

Asset Management, a long/short equity hedge fund from 2007-2012. From 2003-

2007, Mathew was an Investment Analyst at the holding company of Alleghany

Corporation (ticker "Y") covering the equity portfolio, corporate development and

the reinsurance portfolio. Mr. Klody began his career as a credit analyst at the Global Corporate and

Investment Bank at Bank of America.

Mathew has been selected to speak at a number of industry events, including the Spring 2017 Grant’s

Interest Rate Observer conference, Invest for Kids - Chicago (Fall of 2017), and the MOI Global - Best Ideas

Conference (2018). He has served as a guest lecturer to the Notre Dame Institute for Global Investing, the

Behavioral Finance and Applied Investment Management programs at the Mendoza College of Business. He

serves as a member of the Parish Council at St. Joan of Arc Church in Lisle, IL.

Mathew graduated summa cum laude from the University of Notre Dame with a degree in finance and

business economics. Mr. Klody is a Chartered Financial Analyst.

18KEEBECK QUARTERLY LETTER

Q1 2019

DISCLOSURES

Hyperlinks or referenced websites are for your reference and convenience, and forward you to third parties’ websites, which generally are

recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not

constitute an endorsement, authorization, sponsorship by or affiliation with Keebeck Wealth Management with respect to any linked site

or its sponsor, unless expressly stated by Keebeck Wealth Management. Any such information, products or sites have not necessarily

been reviewed by Keebeck Wealth Management and are provided or maintained by third parties over whom Keebeck Wealth Management

exercise no control. Keebeck Wealth Management expressly disclaim any responsibility for the content, the accuracy of the information,

and/or quality of products or services provided by or advertised on these third-party sites.

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S.

market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,”

“planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to,

estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All

are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within

certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive,

governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially

from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties

and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking

statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Keebeck Wealth

Management or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking

statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of

the date that they were made.

19You can also read