Recent Issues in Corporate Governance - Practice Law Seminar 2018 Jerry Koh - NUS Law

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Recent Issues in Corporate Governance Practice Law Seminar 2018 Jerry Koh 1 August 2018

KEY THEMES

Introduction

Singapore Code of Corporate Governance

Diversity

Sustainability Reporting

Dual Class Shares

Shareholder Activism

Corporate Governance & M&A

2INTRODUCTION TO CORPORATE

GOVERNANCE IN SINGAPORE

3INTRODUCTION TO CORPORATE GOVERNANCE IN

SINGAPORE

• One of the most transparent and established regimes in Asia Pacific

– Corporate Governance Watch 2016: 1st of 11 countries in the region

• Other countries involved in the ranking:

2. Hong Kong 7. India

3. Japan 8. Korea

4. Taiwan 9. China

5. Thailand 10. Philippines

6. Malaysia 11. Indonesia

– Transparency International’s Corruption Perceptions Index 2017: 6th of 180

countries

• Singapore ranked after:

1. New Zealand

2. Denmark

3. Finland; Norway; and Switzerland (tied)

– World Bank’s Ease of Doing Business Ranking 2018: 2nd of 190 countries

• Singapore ranked after:

1. New Zealand

4INTRODUCTION TO CORPORATE GOVERNANCE IN

SINGAPORE

• Our corporate governance regime comprises a mix of the following rules

and guidelines:

“Comply

Mandatory

or explain”

rules

provisions

Best practice

recommendations

5SINGAPORE CODE OF

CORPORATE GOVERNANCE

6SINGAPORE CODE OF CORPORATE GOVERNANCE

• Aims

– To support corporate performance and innovation

– To strengthen investor confidence in Singapore capital markets

• Timeline:

2018

Consultation

2012

on reviewing

Issuance of a

2006 the Code

second

Issuance of • Anticipating

2003 revised Code

a third

revised Code

The Code revised

2001 Code soon

came into

Introduction of

effect on 1

the Code by

Jan 2003

the Corporate

Governance

Committee

7CG COUNCIL’S PUBLIC CONSULTATION ON THE CG CODE

In Jan 2018, the Corporate Governance Council (the “CG Council”)

launched a public consultation on changes to the Code of Corporate

Governance (the “CG Code”)

• Rationale: To make the “comply or explain” regime under the Code more

effective

• Enhancing corporate governance standards via “three levers”:

1. Focusing on Singapore’s context

2. Strengthening board quality

3. Fostering a supportive eco-system

8CG COUNCIL’S PUBLIC CONSULTATION ON THE CG CODE

Comply-or-explain regime will be further clarified / revised

• The proposed revised CG Code is structured into 13 overarching Principles,

each comprising detailed Provisions

Proposed Framework

Current CG Code

(Multi-tier structure)

Principles:

Principles and Guidelines:

Mandatory compliance

Comply or explain any deviation

Provisions: Comply, or if there is

variation, explain (i) reason for variation;

and (ii) how the practice is consistent with

intent of the relevant Principle

Practice Guidance: Non-binding

guidance and best practices

9CG COUNCIL’S PUBLIC CONSULTATION ON THE CG CODE

Comply-or-explain regime will be further clarified / revised

• 13 Principles – Overarching and non-disputable statements:

1. Effective 3. Clear 4. Formal

2. Appropriate division of and 5. Formal

Board

balance of responsibility transparent annual

responsible

independence process for assessment of

for company’s between

and diversity directors’ performance

long-term Board and

on the Board appointment

success Management

6. Formal, 9. Governance

7. 8.

transparent of risk to

Remuneration Transparent

procedure safeguard

proportionate on

for interests of

to company remuneration

remuneration company and

policies

policy performance shareholders

13. Inclusive

12.

10. AC which 11. Treats approach by

Shareholder

discharges its shareholders considering

communication

duties fairly and needs of

and

objectively equitably material

participation

stakeholders

10CG COUNCIL’S PUBLIC CONSULTATION ON THE CG CODE

Baseline market practices to be shifted to the SGX Listing Manual

• There are Guidelines in the current CG Code which are in effect important

baseline market practices – CG Council has recommended shifting them to

the SGX Listing Manual for mandatory compliance

• Baseline market practices to be mandatorily complied with:

1) Induction for incoming directors

2) Independent directors

3) Identification of independent directors in the annual report

4) Baseline tests of director independence

5) Relationship between Chairman and CEO

6) 9-year rule

7) Board committees

8) Directors’ re-nomination and re-appointment

9) Key information on directors

10) Adequacy and effectiveness of internal controls

11) Internal audit

12) Disclosure of reasons for non-payment of dividends

11DIVERSITY

12DIVERSITY

• The call for diversity

– Increasingly recognised as a feature of corporate governance across countries

• Diversity enhances ability to identify opportunities and manage risk

– Gender Diversity: Female independent directors have a positive direct effect

on companies’ financial performance (NUS’ Centre for Governance, Institutions

and Organisations, 2018)

• Adding one female independent director, on average, is expected to improve financial

performance by 11.8%

– Age Diversity: People from different age groups bring different life experiences

and perspectives to the table

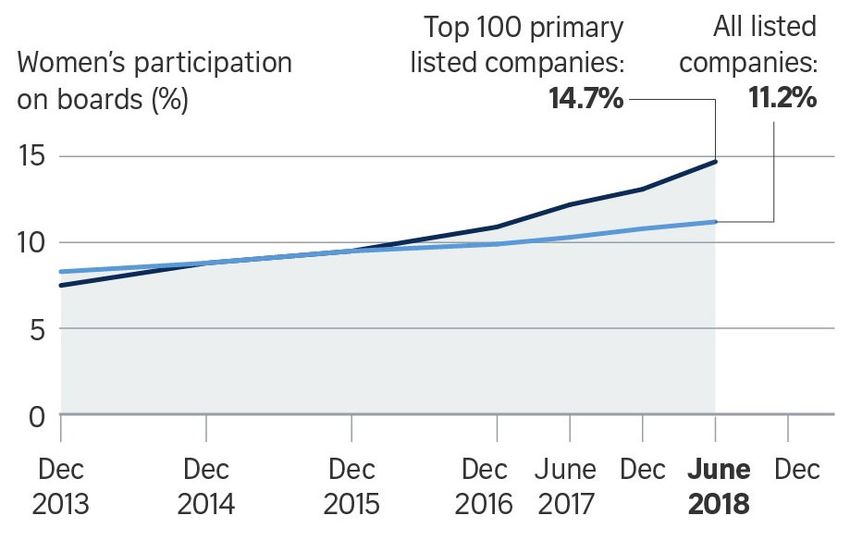

13GENDER DIVERSITY

• Diversity Action Committee (“DAC”)

– Established in 2014 by Mr Chan Chun Sing, then Minister for Social and Family

Development

– Aim: To address the under-representation of women on SGX-listed boards

– “Hop, skip and jump” approach to raise women’s participation: Triple-tier target

of 20% by 2020, 25% by 2025 and 30% by 2030

• Cf Current women representation on boards:

Source: DAC, 2018; Straits Times graphics

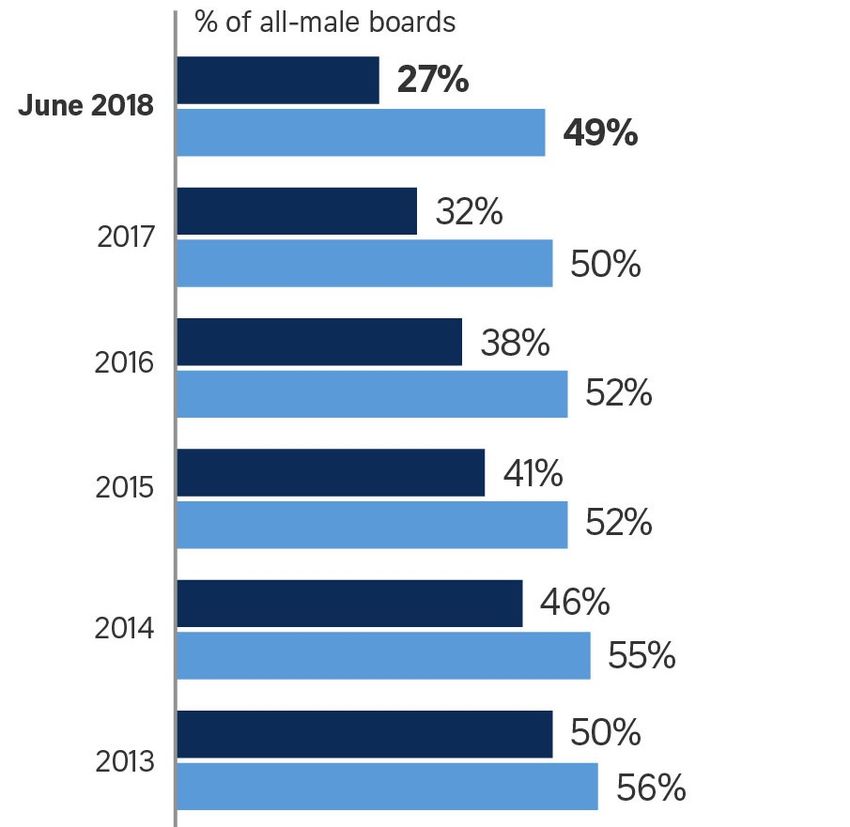

14GENDER DIVERSITY

• Current women representation on boards

– Fewer all-male boards among Singapore-listed companies:

Source: DAC, 2018; Straits Times graphics

15GENDER DIVERSITY

California experience: Proposed board quotas

• In May 2018, the California State Senate passed a bill for board quotas

– If enacted, a public company with shares listed on a major US stock exchange

that has principal executive offices in California would need to have:

• at least one woman on its board by end-2019;

• if company has five directors, at least two female directors by end-2021;

• if company has at least six directors, at least three female directors by end-2021.

– Rationale

• Studies indicate that companies perform better with women on their boards

• More female directors would be beneficial to California’s economy, yet progress towards

gender parity is too slow

• As of June 2017, 26% of California public companies in Russell 3000 had no female

directors, while women made up 15.5% of directors on boards with at least one woman

– Controversy

• California Chamber of Commerce filed an opposition letter arguing that the bill would

violate constitutional law and California civil rights law, on the basis that it may require

male directors to be displaced by female directors

16GENDER DIVERSITY

Singapore experience: No plans for board quotas

• In 2014, the Diversity Task Force regarding Women on Boards did not

recommend board quotas

– Noted that the causes of poor gender diversity are complex and intertwined, e.g.:

• Lack of awareness of importance of gender diversity

• Over-reliance on personal networks to source for directors

• Women who are capable of serving on boards may not wish to do so

– Instead, recommended multi-stakeholder approach to address root causes of

poor gender diversity

• Proposed allowing these measures to run their course before assessing if quotas are

needed

• DAC’s view on board quotas

– Meeting numbers does not guarantee that benefits follow

– DAC is interested in women on boards for the benefits that they would bring

• But DAC and regulators have not closed the door on the possibility of board

quotas

17AGE DIVERSITY

• Age diversity

– Benefits of having Board and Board committees with directors of different ages

• Helps companies to keep pace with fast changing trends and developments in the

preferences and behaviour of different generations of consumers; and

• Helps companies develop capabilities for the future economy

– Proposed CG Code expressly contemplates age diversity:

“The Board and board committees are of an appropriate size, and comprise

directors who as a group provide the appropriate balance and mix of

skills, knowledge, experience, and other aspects of diversity such as gender

and age, so as to avoid groupthink and foster constructive debate.”

18SUSTAINABILITY REPORTING

19SUSTAINABILITY REPORTING

What is sustainability reporting?

• Sustainability reporting: Publication of non-financial information such as

environmental, social and governance (“ESG”) information in a

comprehensive and strategic manner

• Drivers:

– Environmental concerns

– Demand by investors and other stakeholders for more information and

transparency

20SUSTAINABILITY REPORTING

SGX’s introduction of mandatory requirements in mid-2016

• Sustainability reporting required for financial years ending on or after 31

December 2017

– Issuers to disclose any deviation and describe its actual practice, with reasons for

such deviation

– Rule 711B of the SGX Listing Manual requires description of sustainability

practices based on five primary components

• Prior to the SGX’s requirements for mandatory sustainability reporting:

– Out of 502 Mainboard-listed companies on the SGX-ST in 2015, 186 companies

voluntarily communicated sustainability, constituting 37.1% of the companies

(ASEAN CSR Network & Centre for Governance, Institution and Organisations

Report, Oct 2016)

21SUSTAINABILITY REPORTING

SGX’s introduction of mandatory requirements in mid-2016

• Five primary components under the SGX Listing Manual:

Primary Component Disclosures

a) Material ESG factors • Reasons for each material ESG factor and selection process

b) Policies, practices and • Issuer's policies, practices and performance in relation to the

performance material ESG factors (both descriptive and quantitative)

c) Targets • Targets for the forthcoming year

d) Sustainability reporting • Sustainability reporting framework(s) to be selected

framework – Should be suited to issuer’s industry and business model

• Disclose reasons for choosing the framework(s) and the extent

of the issuer's application of the framework(s)

e) Board statement • Board statement, stating that the sustainability report complies

with primary components, or has otherwise explained

alternative practices

22SUSTAINABILITY REPORTING

Board statement and its implications

• Board responsibility

– SGX Listing Manual imposes on the Board “ultimate responsibility for the issuer’s

sustainability reporting”

• Requirement to disclose Board statement under the SGX Listing Manual:

“The sustainability report should contain a statement of the Board on the Board having

considered sustainability issues as part of its strategic formulation, determined the

material ESG factors and overseen the management and monitoring of the

material ESG factors.” (Rule 711B(1)(e) of the SGX Listing Manual)

• Potential liability implications

– Possible for the Board’s statement to result in liability risks under Singapore law

• Especially under Section 199 of the Securities and Futures Act, which prohibits the

making of a statement that is false or misleading in a material particular

– Could potentially enable investors to hold the Board accountable for its failure to

adequately manage sustainability risks

23SUSTAINABILITY REPORTING

Some observations on the practice of SGX-listed issuers

• SGX-listed issuers are still adapting to the new sustainability reporting

requirements

– Cost concerns, especially for smaller companies

– But conscious investment in sustainability efforts could provide long-run benefits

• Operational efficiencies

• Enhanced reputation

– Ultimately, the impact of sustainability reporting here remains to be seen as it is

relatively new

• Common topics / issues

– Corporate governance

– Environment (e.g. energy and water consumption, carbon footprint)

– Social / employment practices

24SUSTAINABILITY REPORTING

Key considerations for Boards on sustainability reporting

• ESG factors should be considered as part of Board’s annual strategy

review

– Identify emerging ESG factors or trends

– Consider how best to allocate resources in managing the most critical ESG risks

• Importance of calibrating the level of constructive disclosure

– Balancing between transparency vs. avoiding immaterial or duplicative

disclosures

25DUAL CLASS SHARES

26SGX’S INTRODUCTION OF DUAL CLASS SHARES

SGX’s introduction of dual class shares

• On 26 Jun 2018, SGX introduced rules on the listing of issuers with dual

class share (“DCS”) structures

– Allows certain shareholders voting rights disproportionate to their shareholding

– The new rules take immediate effect

• Rationale

– Maintain Singapore’s competitiveness and attractiveness as a financial hub

– Draw high-technology companies and family businesses

– In line with Singapore’s strategy to strengthen its innovation ecosystem and

enterprise capabilities

27STRATEGIES TO ATTRACT MORE IPOS

SGX’s recent introduction of dual class shares

• Must show suitability for DCS listing

• Non-exhaustive factors:

Business model Track record

Role and contribution of

Participation by

multiple-vote

sophisticated investors

shareholders

Other features that require DCS structure

(e.g. innovative company, family business)

28SAFEGUARDS TO ADDRESS RISKS

Addressing Addressing

Entrenchment Risks Expropriation Risks

Maximum voting differential of Enhanced voting process – For

10:1 for multi-vote shares constitutional amendments,

variation of class rights,

winding-up, etc.

Minimum 10% voting rights to be

held by one-vote shareholders

Independent directors –

Sunset clause with events Majority of AC, NC, RC

stipulated at IPO

29COMPARISON WITH HKEX

SGX & HKEx DCS regimes

• On the heels of Hong Kong’s launch of its DCS regime, which has attracted

multi-billion dollar IPOs

– E.g. Xiaomi’s DCS IPO in June 2018; Meituan Dianping has filed for DCS IPO

• SGX vs. HKEx

SGX Rules HKEx Rules

• Applicant must be suitable for listing with • Applicant expected to demonstrate:

DCS structure – Necessary characteristics of

• Note: SGX rules are silent as to nature of innovation and growth

the applicant – more flexibility in – Suitable for listing with a weighted

determining suitability of applicant voting rights structure

Food for thought: Does SGX’s DCS regime strike an appropriate balance between

promoting IPOs and mitigating expropriation and entrenchment risks?

30US EXPERIENCE WITH DCS LISTINGS

US experience with DCS

• Nasdaq and NYSE have actively solicited and listed issuers with DCS

– In the US, almost 30% of IPO companies have ≥2 classes of common stock

and unequal voting rights (Davis Polk Survey, 11 July 2018)

• In March 2017, Snap’s IPO was the first in which only non-voting shares

were offered to the public

– Controversy when global index providers announced that they will partially or

fully exclude companies with DCS from their indices

• E.g. Certain S&P Down Jones Indices, FTSE Russell indices

• Role of index providers in shaping governance standards

– Cf Would index exclusion for DCS companies deprive retail investors of

investment exposure to some of the most innovative US companies?

31SHAREHOLDER ACTIVISM

32SHAREHOLDER ACTIVISM

• Increasing shareholder activism in Singapore and other jurisdictions in

recent years

• Controversial process by which shareholders exert their influence by

generating pressure on management

• Spearheaded primarily by two kinds of investors in the past 10 years:

Investors whose motives

Investors whose motives

are to improve corporate

are purely profit driven

social responsibility

33SHAREHOLDER ACTIVISM

Role of proxy advisory firms in corporate governance

• A proxy advisory firm provides advice to institutional and other investors

on how to vote their shares / units at general meetings

– E.g. Institutional Shareholder Services, Inc., which has in the past recommended

institutional investors of SGX-listed issuers against voting in favour of certain

types of resolutions

• E.g. Resolution for share/unit buyback mandate of an issuer

• Institutional investor may, as a matter of internal policy, follow the

recommendation of the proxy advisory firm

34SHAREHOLDER ACTIVISM

Sabana REIT case study (2017)

• Unitholders were unhappy with non-yield accretive acquisitions and

significant discount to rights issue price

• 66 unitholders of Sabana REIT (holding 0.6% of total units in issue)

requisitioned an EGM to, among others, replace the REIT Manager with an

internalised manager

• Activist pressure led the REIT Manager to carry out a strategic review to

improve the REIT’s performance

• Impact of social media and online platforms

– E.g. Facebook, ShareJunction, Hardwarezone Forum

35SHIFT TOWARDS STAKEHOLDER MODEL

• Overall trend towards the stakeholder-centric model of corporate

governance in Singapore and other countries

• BlackRock’s Annual Letter to CEOs (2018):

“The time has come for a new model of shareholder engagement – one that

strengthens and deepens communication between shareholders and the companies

that they own.”

“Society is demanding that companies, both public and private, serve a social

purpose. To prosper over time, every company must not only deliver financial

performance, but also show how it makes a positive contribution to society.”

– Mr Larry Fink (BlackRock’s Founder, Chairman and CEO)

• Importance of investor relations

– To properly articulate long-term business strategies to shareholders/unitholders,

customers, suppliers, regulators and other stakeholders

36SHIFT TOWARDS STAKEHOLDER MODEL

UK & Singapore: Shareholder primacy vs. Stakeholder interests

• The UK framework is traditionally based on shareholder primacy

• Signs of a shift towards stakeholder model

– Section 172 of the UK Companies Act 2006 requires directors to consider the interests

of certain stakeholders:

“A director … must act in the way he considers, in good faith, would be most likely to

promote the success of the company for the benefit of its members as a whole, and in

doing so have regard (amongst other matters) to …

(b) the interests of the company’s employees,

(c) the need to foster the company’s business relationships with suppliers,

customers and others,

(d) the impact of a company’s operations on the community and the environment, …

(f) the need to act fairly as between members of the company.”

37SHIFT TOWARDS STAKEHOLDER MODEL

UK & Singapore: Shareholder primacy vs. Stakeholder interests

• Cf Director’s duty to act in the best interests of the company under Singapore

law

• Section 159 of the Singapore Companies Act does contemplate that directors

can consider the interests of its employees and members

– Unlike Section 172 of the UK Companies Act 2006, Section 159 of the Singapore

Companies Act is permissive, rather than prescriptive

“159. The matters to which the directors of a company are entitled to have regard in exercising

their powers shall include —(a) the interests of the company’s employees generally, as well

as the interests of its members…”

38SHIFT TOWARDS STAKEHOLDER MODEL

UK experience: 2018 Corporate Governance Code

• On 16 July 2018, the revised UK Code was issued

• The slight shift towards the stakeholder model has been highlighted in the

2018 UK Code

“‘The shareholders’ role in governance is to appoint the directors and the auditors and

to satisfy themselves that an appropriate governance structure is in place.’ This remains

true today, but the environment in which companies, their shareholders and wider

stakeholders operate continues to develop rapidly… To succeed in the long-term,

directors and the companies they lead need to build and maintain successful

relationships with a wide range of stakeholders.”

• Concept of “purpose” forms the guiding principle of the 2018 UK Code

“The board should establish the company’s purpose, values and strategy, and satisfy

itself that these and its culture are aligned. All directors must act with integrity, lead by

example and promote the desired culture.”

39SHIFT TOWARDS STAKEHOLDER MODEL

UK experience: 2018 Corporate Governance Code

• Emphasis on employees as stakeholders

• 2018 UK Code requires the Board to promote greater engagement with the

workforce using one, or a combination of the following:

Alternative

engagement

Director

Formal Designated mechanisms

appointed

workforce non-executive which the

from the

advisory panel director Board

workforce

considers

effective

40CORPORATE GOVERNANCE &

M&A

41CORPORATE GOVERNANCE & M&A

M&A as a mechanism for promoting corporate governance

• Hostile takeover as a mechanism for aligning managers’ interests with

shareholders’ interests

• The risk of a hostile takeover poses an external threat which could

incentivise good governance

– Mitigates agency costs which arise from the separation between ownership and

control in a company

Poor corporate governance

Reduces the share price of the company

Could result in the company becoming a ripe takeover target

42SHAREHOLDER PRIMACY VS. MANAGERIAL AUTONOMY

Degree of shareholder primacy in takeover regulation

• Management has more

Managerial autonomy to consider

Autonomy interests of other

stakeholders and pursue

long-term value

• Favours strong

defences against

• Takeover regime should takeovers

maximise shareholders’ Shareholder • E.g. US

interests and minimise Primacy

agency costs

• Favours weak defences

against takeovers

• E.g. UK

Food for thought: To what extent should shareholder primacy prevail under the

Singapore takeover regime?

43SHAREHOLDER PRIMACY VS. MANAGERIAL AUTONOMY

Defensive measures against takeovers

• Examples of defensive measures:

– Poison pill (shareholder rights plans)

– Crown jewel defence (substantial disposals)

– Golden handshakes (payments to key personnel for loss of office)

– Payment of special dividends

• Non-frustration rule has developed in some takeover regimes to limit the extent to

which management can hinder a takeover

– E.g. General Principle 7 of the Singapore Code on Take-overs and Mergers (“Takeover

Code”) – Draws a distinction between pre-bid vs. post-bid steps

“7 Frustration of an offer by offeree board

If the board of an offeree company has received a bona fide offer or has reason to

believe that a bona fide offer is imminent, it must not, without the approval of

its shareholders in general meeting, take any action on the affairs of the offeree

company that could effectively result in any bona fide offer being frustrated or the

shareholders being denied an opportunity to decide on its merits.”

44SHAREHOLDER PRIMACY VS. MANAGERIAL AUTONOMY

Defensive measures against takeovers

• Examples of defensive measures prohibited under Rule 5 of the Takeover Code:

“Such actions include but are not limited to:-

(a) issue any authorised but unissued shares;

(b) issue or grant options in respect of any unissued shares;

(c) create or issue or permit the creation or issue of any securities carrying rights of

conversion into or subscription for shares of the company;

(d) sell, dispose of or acquire or agree to sell, dispose of or acquire assets of material

amount;

(e) enter into contracts, including service contracts, otherwise than in the ordinary course

of business…”

• Cf Counter-argument in favour of managerial autonomy – that Boards and

management should be given sufficient space in which to formulate and implement a

long-term strategy

45SHAREHOLDER PRIMACY VS. MANAGERIAL AUTONOMY

Poison pill defence

• Operates by substantially increasing the cost of acquisition

• Board of directors adopts a shareholder rights plan, which is triggered

once the bidder acquires the target shares beyond a specified percentage

threshold

• Rights or warrants are then distributed to shareholders other than the

bidder, allowing them to purchase shares in the target at a discount – results

in massive dilution of the bidder’s shareholding in the target

46SHAREHOLDER PRIMACY VS. MANAGERIAL AUTONOMY

Poison pill defence

• United States

– Shareholder rights plans recognised as a valid instrument of takeover defence in

Moran v Household International, Inc. (Delaware Supreme Court, 1985)

• Cf Shareholder rights plans are difficult to implement in Singapore

– Section 161 of the Companies Act requires directors to obtain shareholders’

approval in relation to any issuance of shares

– At common law, directors must also ensure they are acting in the interests of the

company in issuing the shares

• Some have argued that poison pills may be detrimental to shareholders’

interests as they entrench incumbent management

47Q&A

48You can also read