Text-Based Insights into Stock Market Behavior - Steven J. Davis University of California, Berkeley

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Text-Based Insights into

Stock Market Behavior

Steven J. Davis

University of California, Berkeley

24 April 2018

Text-as-data and text-based methods have

emerged as major tools of analysis in

accounting, finance and economics.

Today’s talk draws on two papers underway to

develop new insights into stock market behavior

• “Diagnosing the Stock Market’s Reaction to Trump’s

Surprise Election Victory,” with Cristhian Seminario

– Automated readings of 61,000 10-K filings

• “What Triggers Stock Market Jumps?” with Scott

Baker, Nick Bloom and Marco Sammon

– Human readings of newspaper articles about a few

thousand jumps in national equity markets across

14 countries, plus a few hundred jumps in U.K. and

U.S. bond markets and US$ currency markets. 2

Diagnosing the Stock Market

Reaction to Trump’s Surprise

Election Victory

Steven J. Davis (Chicago Booth & Hoover)

Cristhian Seminario (U of Chicago)

2018

Noon on Election Day!

Washington (CNN) Hillary Clinton's odds of

winning the presidency rose from 78% last week

to 91% Monday before Election Day, according

to CNN's Political Prediction Market.

But Trump won!!

Initially, stocks fell sharply in after-hours trading From “Markets Sent a Strong Signal on Trump … Then Changed Their Minds,” Justin Wolfers, New York Times, 18 November 2016

But Stocks Boomed on 9 November

Histogram of Daily Market Returns, U.S. Stocks

Sample Period: 8 November 2016 +/- 360 Days

Trump Election

Trump Election

Using

Closing

Prices

… Confounding Prominent Economists Justin Wolfers, New York Times, 18 November 2016: “Throughout the campaign, stocks rose whenever campaign developments made it less likely that Mr. Trump would be elected.” This assessment rests on Wolfers’ pre-election empirical study with Erik Zitzewitz. Their bottom line: “[W]e estimate that market participants believe that a Trump victory would reduce the value of the S&P 500, the UK, and Asian stock markets by 10-15%.”

Our Approach: Examine the Cross- Section of Abnormal Equity Returns in Reaction to Trump’s Victory 1. Trump and Clinton were far apart on many policy issues: regulation, healthcare, trade, etc. Not a Tweedledee vs. Tweedledum election!! 2. Firms differ in their exposures to policy risks. 3. Quantify these risks using Part 1a (“Risk Factors”) of listed firms’ annual 10-K filings. 4. Trump’s surprise victory abruptly shifted the level and structure of important policy risks. 5. We look to the cross-section of firm-level returns to assess the effects of that shift and gain insight into the market’s reaction to Trump’s win.

The Cross-Firm Dispersion of Abnormal Returns

Was Very High in the Wake of Trump’s Victory

Histogram of Cross-Firm St. Dev. of Daily Abnormal Returns

Sample Period: 8 November 2016 +/- 360 Days

Abnormal (CAPM)

Trump Election

Trump Election

returns based on

data for 360 days

before the election.

Histogram of Interquartile Range of

Abnormal Daily Returns Across Firms

Sample Period: 8 November 2016 +/- 360 Days

Trump Election

Trump ElectionAnalysis Sample • Common equity securities (primary issue) traded on AMEX, NYSE and NASDAQ of firms incorporated in the United States, with prices quoted in U.S. Dollars. • Daily closing prices, shares outstanding and shares traded from Compustat North America, with adjustments for stock splits, reverse splits, dividends, etc. Market return data from Ken French’s website. • Sample period: ±360 calendar days from Nov 8, 2016 • 3,606 firms with closing prices on 8 and 9 November. • Matched to 3,383 firms with at least one 10-K filing (with non-empty Part 1a) from January 2006 to July 2016. – Part 1a is not obligatory for all listed firms. • Drop 102 firms with no NAICS code. Drop 20 with fewer than 126 daily return observations in pre-election window. • 3,261 firms in the final sample. – About 1.5 million daily return observations 11

Part 1A of the 10-Ks

• Since 2006 (for FY 2005) the SEC requires most publicly

held firms to include a separate discussion of “Risk Factors”

in Part 1a of their annual 10-K filings.

• In explaining “How to Read a 10-K” at

www.sec.gov/answers/reada10k.htm, the SEC describes

Part 1a as follows:

– Item 1A - “Risk Factors” includes information about the

most significant risks that apply to the company or to its

securities. Companies generally list the risk factors in

order of their importance. In practice, this section focuses

on the risks themselves, not how the company addresses

those risks. Some risks may be true for the entire

economy, some may apply only to the company’s industry

sector or geographic region, and some may be unique to

the company. 12How We Use the 10-Ks

1. Develop term sets that correspond to various policy risk

categories. Examples:

– Healthcare Policy

– Food and Drug Policy

– Environmental and Energy Regulation

– Trade and Exchange Rate Policy

– Various tax policy categories

– Government Spending and Fiscal Stabilization Policy

2. For each 10-K filing – and each term set – calculate the

percentage of sentences in Part 1a with one or more

terms in the set.

3. Average the percentage over available years for each firm

and term set to get our risk exposure measures.

13A Warm-Up Investigation

1. For each 10-K filing with a non-empty Part 1a:

– Calculate the percentage of sentences in Part 1a

that contains “regulation,” “regulate” or “regulatory.”

– Average this percentage over years for each firm.

2. This average value is our measure of Raw Regulation

(Risk) Exposure for the firm.

3. Compute the firm’s daily return as 100 X log change in

the closing price from November 8 to November 9.

4. Obtain the CAPM abnormal return for each firm from

November 8 to 9.

5. Relate Raw Regulation Exposure to abnormal equity

returns in reaction to Trump’s surprise election victory.

6. Plot the firm’s daily return against its Raw Regulation

Exposure.

14Firms with greater exposure to regulatory risks

had higher abnormal returns on 9 November

The estimated cross-sectional effect is large:

Multiplying the slope coefficient by the IQR of

the Raw Regulation Exposure measure (7.6

percentage points) implies a daily return

differential of 1.2 percentage points.

Abnormal Returns from 8-9 Nov:

Mean Firm-Level Daily Return: 1.1%

IQR of Daily Returns: 4.4%Extending the Measurement Method

mean (%) IQR (%)

Variable N % >0 max (%)

All >0 All >0

Raw Regulation 3281 99.6 8.6 8.6 7.6 7.6 57.7

Food and Drug Policy 3281 22.0 1.2 5.6 0.0 7.2 43.3

Trade and Exchange Rate Policy 3281 56.2 0.6 1.1 0.8 1.1 17.1

Government Purchases and Fiscal Policy 3281 28.3 0.1 0.4 0.1 0.3 15.9

Entitlement and Welfare Programs 3281 11.5 0.0 0.2 0.0 0.2 2.1

Government-Sponsored Enterprises 3281 10.7 0.2 1.8 0.0 2.1 18.5

Labor Regulation 3281 37.8 0.2 0.5 0.2 0.5 8.3

Financial Regulation 3281 47.1 1.2 2.6 0.4 2.6 33.5

Intellectual Property Policy 3281 23.9 0.1 0.4 0.0 0.4 6.5

Monetary Policy 3281 23.5 0.3 1.5 0.0 2.0 18.5

Taxes on Business Profits 3281 14.8 0.0 0.3 0.0 0.3 2.9

Business Tax Credits 3281 5.5 0.0 0.2 0.0 0.2 3.0

Sales and Excise Taxes 3281 22.9 0.1 0.5 0.0 0.5 22.4

Generic Tax Terms 3281 92.3 2.2 2.4 2.6 2.5 32.3

Healthcare Policy 3281 31.8 0.8 2.4 0.2 2.5 42.1

Healthcare Industries 453 54.1 2.9 5.4 3.3 6.5 27.4

Other Industries 2828 28.2 0.4 1.5 0.1 1.9 42.1

Energy and Environmental Regulations 3281 24.7 0.6 2.4 0.0 3.0 16.8

Green Sectors (BLS Designations) 810 29.8 0.7 2.4 0.2 2.6 16.8

Brown Sectors 2471 23.1 0.5 2.4 0.0 3.1 16.8Example: The Term Set for

Energy & Environmental Regulation

Energy And Environmental Regulation: {energy policy},

{energy tax, carbon tax}, {cap and trade}, {cap and tax},

{drilling restrictions}, {offshore drilling}, {pollution controls,

environmental restrictions, clean air act, clean water act},

{environmental protection agency, epa}, {wetlands

protection}, {Federal Energy Regulatory Commission,

FERC}, {ethanol subsidy, ethanol tax credit, ethanol credit,

ethanol tax rebate, ethanol mandate, biofuel tax credit,

biofuel producer tax credit}, {corporate average fuel

economy, CAFE standard}, {endangered species},

{Keystone pipeline}, {Alaska oil pipeline, Trans-Alaska

pipeline}, {greenhouse gas regulation, climate change

regulation}, {Nuclear Regulatory Commission}, {Pipeline

and Hazardous Materials Safety Administration}Our Basic Firm-Level Abnormal Return Regression

Dependent Variable: Daily Abnormal Equity Coefficient Times IQR

Return from November 8 to 9 Coeff. (t-stat) IQR|All IQR|Exposure>0

Raw Regulation 8.0 (4.3) 0.6 0.6

Food and Drug Policy 25.5 (5.1) 0.0 1.8

Trade and Exchange Rate Policy -11.8 (-1.9) -0.1 -0.1

Government Purchases and Fiscal Policy 79.2 (4.1) 0.0 0.3

Entitlement and Welfare Programs -156.5 (-1.5) 0.0 -0.3

Government-Sponsored Enterprises -19.9 (-5.3) 0.0 -0.4

Labor Regulation 39.5 (3.2) 0.1 0.2

Financial Regulation 2.7 (1.2) 0.0 0.1

Intellectual Property Policy 68.4 (2.2) 0.0 0.2

Monetary Policy 5.3 (0.7) 0.0 0.1

Taxes on Business Profits 39.6 (1.0) 0.0 0.1

Business Tax Credits -166.2 (-1.7) 0.0 -0.3

Sales and Excise Taxes -26.3 (-1.8) 0.0 -0.1

Generic Tax Terms -10.8 (-3.3) -0.3 -0.3

Healthcare Industries (Dummy) -1.6 (-5.5)

Healthcare Policy # Healthcare Industries -17.3 (-2.3) -0.6 -1.1

Healthcare Policy # Other Industries -0.7 (-0.1) 0.0 0.0

Green Sector (Dummy) -0.8 (-4.0)

Energy & Environ. Regs # Green Sector -35.4 (-5.5) -0.1 -0.9

Energy & Environ Regs # Brown Sector 4.4 (0.9) 0.0 0.1 18

Observations: 3261 Adjusted R-Squared: 11.2%Dependent Variable: Daily Abnormal Dropping Firms Not Russell 3000 +

Equity Return from November 8 to 9 In Russell 3000 Leverage Control

Raw Regulation 8.5 (4.0) 7.9 (3.8)

Food and Drug Policy 32.6 (5.1) 34.5 (5.2)

Trade and Exchange Rate Policy -14.9 (-2.2) -16.0 (-2.3)

Government Purchases and Fiscal Policy 113.5 (5.1) 116.9 (5.3)

Entitlement and Welfare Programs -335.1 (-2.5) -318.2 (-2.7)

Government-Sponsored Enterprises -24.3 (-5.8) -20.8 (-4.7)

Labor Regulation 40.8 (3.4) 43.2 (3.6)

Financial Regulation 0.7 (0.3) -0.4 (-0.2)

Intellectual Property Policy 136.4 (2.6) 123.8 (2.3)

Monetary Policy 11.8 (1.4) 10.0 (1.2)

Taxes on Business Profits 53.8 (1.4) 62.2 (1.6)

Business Tax Credits -183.0 (-2.0) -194.7 (-2.1)

Sales and Excise Taxes -34.0 (-2.3) -36.2 (-2.5)

Generic Tax Terms -17.6 (-4.5) -16.1 (-4.2)

Healthcare Industries (Dummy) -2.0 (-6.9) -2.0 (-6.9)

Healthcare Policy # Healthcare Industries -20.6 (-2.5) -20.9 (-2.6)

Healthcare Policy # Other Industries -5.1 (-0.4) -18.9 (-1.3)

Green Sector (Dummy) -0.9 (-4.2) -1.0 (-4.8)

Energy & Environ. Regs # Green Sector -38.5 (-5.9) -35.5 (-5.6)

Energy & Environ Regs # Brown Sector -6.3 (-0.9) -4.5 (-0.7)

Leverage (long-term debt + short-term liabilities)/Assets in FY 2015 -1.2 (-2.9)

19

Observations (Adjusted R-Squared, %) 2384 (19.5%) 2371 (19.9%)Next Few Slides: Partial Regression Scatter

Plots for Our Basic Specification and Sample

Residualized values, binned on

variable on horizontal axis,

controlling for other regressors.Coefficient (t-stat) on Healthcare Industry Dummy: -1.6 (-5.5)

Coefficient (t-stat) on Green Industry Dummy: -0.8 (-4.0). BLS Green designations.

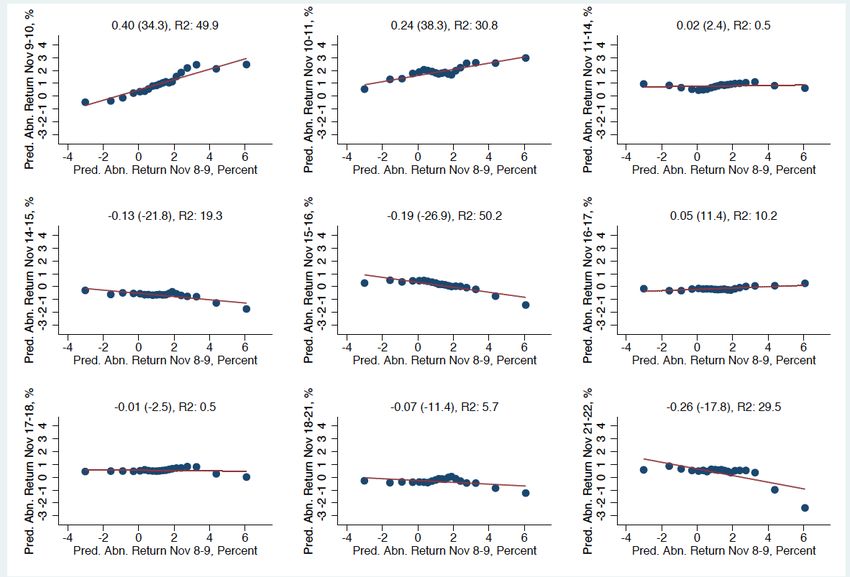

Firm-Level Abnormal Returns Moved Strongly in the Same Direction on November 10, 11 and 14

Russell 3000 Sample Shows a Similar Pattern

A Similar Return Structure on Other Days? No

Our Basic Abnormal Returns Regression, Dropping Firms Not in Russell 3000

Dependent Variable: Daily Average Results For Average Results for Average Results for

9 Nov 2016

Firm-Level Abnormal Return Prior 360 days 3 Largest Gains 3 Largest Drops

Abnormal Return: Mean (IQR) 1.3 (4.4) -0.0 (1.8) -0.0 (2.5) -0.3 (2.8)

Equity Return: Mean (IQR) 3.0 (4.7) 0.0 (1.9) 2.5 (2.7) -3.6 (3.5)

Raw Regulation 8.5 (4.0) -0.1 (-0.1) -0.3 (-0.2) -0.9 (-0.7)

Food and Drug Policy 32.6 (5.1) -1.2 (-0.3) -5.0 (-1.7) -3.9 (-1.0)

Trade & Exch. Rate Policy -14.9 (-2.2) 0.4 (0.1) -3.5 (-1.0) -7.2 (-1.2)

Govt. Purch. & Fiscal Policy 113.5 (5.1) 1.0 (0.1) -10.8 (-0.8) -6.9 (-0.4)

Entitlement & Welfare -335.1 (-2.5) 2.7 (0.1) -1.9 (-0.1) 20.1 (0.4)

GSEs and Related -24.3 (-5.8) 0.4 (0.1) 5.6 (1.3) 4.3 (0.9)

Labor Regulation 40.8 (3.4) -0.7 (-0.0) 1.4 (-0.2) -1.8 (-0.4)

Financial Regulation 0.7 (0.3) 0.1 (0.2) -7.0 (-3.3) -4.3 (-1.8)

Intellectual Property Policy 136.4 (2.6) -2.7 (-0.1) -16.1 (-0.3) -17.2 (-0.5)

Monetary Policy 11.8 (1.4) 0.7 (0.1) -9.6 (-1.8) -3.6 (-0.3)

Taxes on Business Profits 53.8 (1.4) -1.2 (-0.0) 5.9 (0.3) 39.1 (1.9)

Business Tax Credits -183.0 (-2.0) -2.0 (-0.0) -21.1 (-0.4) 19.1 (0.4)

Sales and Excise Taxes -34.0 (-2.3) 2.3 (0.2) 11.0 (1.6) 18.1 (1.6)

Generic Tax Terms -17.6 (-4.5) 0.0 (0.0) 4.0 (1.1) -0.2 (-0.1)

Healthcare Ind. (Dummy) -2.0 (-6.9) 0.0 (0.1) 0.0 (0.2) 0.6 (3.7)

HC Policy # HC Industry -20.6 (-2.5) -0.2 (-0.1) -0.8 (-0.4) -0.9 (-0.6)

HC Policy # Other Industries -5.1 (-0.4) -0.4 (-0.1) 2.3 (0.8) 2.1 (0.6)

Green Sector (Dummy) -0.9 (-4.2) 0.0 (0.1) 0.2 (1.3) -0.1 (-1.1)

E&E Regs # Green Sector -38.5 (-5.9) 0.9 (0.3) 5.6 (1.6) 19.8 (6.3)

E&E Regs # Brown Sector -6.3 (-0.9) 0.4 (-0.1) 13.8 (2.1) 9.3 (1.7)

Observations (Adj-R2) 2384 (19.5) 2380 (6.3) 2376 (4.7) 2380 (7.5)Taking Stock (Tentative)

1. The surprise election outcome triggered a large,

positive stock market response on 9 November 2016,

strongly contradicting pre-election assessments of the

likely market response to a Trump victory.

2. The structure of firm-level equity returns on 9 November

was highly dispersed, highly unusual, and clearly tied to

firm-level policy risk exposures, as derived from 10Ks.

– Firms with high exposures to regulatory risks saw

especially high equity returns on 9 November, except

for those reliant on “green” subsidies.

– Healthcare delivery firms and those with high

exposures to healthcare policy risks fared poorly in

relative terms and, in some case, in absolute terms.– High exposure to risks associated with Trade Policy,

Entitlement and Welfare Programs, and Government-

Sponsored Enterprises involved lower returns.

– High exposure to risks associated with Labor

Regulation, Food and Drug Policy, and IP Policy

involved higher returns.

3. The stock market did not fully digest the implications of the

election outcome by market close on 9 November.

– Instead, (conditional) firm-level abnormal returns over

the next 2-3 days strongly reinforced the initial market

response to the election surprise.

– The shift in the structure of conditional firm-level

abnormal returns over 3-4 days after the election was

about 65% greater than the initial shift from market

close on 8 November to market close on 9 November.4. These results suggest that equity prices do not immediately

and fully adjust to surprise events that (a) involve unusual

shifts in the structure of price-relevant risks and (b) require

large information processing resources to fully assess.

– Human collection and processing of available

information is costly, and it takes time. Thus, the surprise

realization of events that satisfy (a) and (b) need not be

fully and immediately incorporated into equity prices.

– This interpretation calls for study of other major surprise

events that meet conditions (a) and (b).

• Do they also involve a slow-working multi-day

response in the structure of firm-level equity returns?

• When (a) or (b) fails, do we instead see rapid

responses in the structure of firm-level equity returns?5. Asset price responses to prediction-market probability

changes are unreliable guides to the actual price effects

of major surprise outcomes, if they materialize, when

conditions (a) and (b) hold.

– Put more positively, asset price responses to shifts in

the probability of future outcomes are more reliable

when (^a) the prospective event involves a common,

well-understood shift in the structure of price-relevant

risks, and/or (^b) modest information processing

resources are sufficient to assess the pricing

implications of the prospective event.Some Next Steps

1. Improve our term sets and firm-level characterizations:

– Further parse instances of generic Regulation

– Tax policy: develop better term sets and code that

allocates “generic” tax terms

– Trade policy: distinguish among exporters, import-

competing and supply-chain dependent firms.

– Financial regulation: We find little here – a deficiency

in our Financial Regulation term set?

2. Examine firm-level returns on Wolfers-Zitzewitz dates:

– Initial work suggests that “signal” associated with

these episodes is too weak to say much.

3. Compare to Wagner, Zeckhauser and Ziegler papers:

– They take a different approach, consider a smaller

sample, and focus on tax considerations.What Triggers Stock Market Mumps?

Scott R. Baker (Kellogg, Northwestern)

Nick Bloom (Stanford)

Steven J. Davis (Chicago Booth and Hoover)

Marco Sammon (Kellogg, Northwestern)

2018Why does the stock market jump?

• Two broad views on what drives stock market moves:

– Eugene Fama: driven by discount rates, risk, dividends, etc.

– Robert Shiller: Hard to explain fully by fundamentals; narratives

develop and sometimes spread, affecting prices and returns.Why does the stock market jump? • We advance this discussion by considering several thousand large daily moves in national equity markets. • We read next-day newspaper accounts and record the journalist’s characterization of the jump.

How We Characterize Equity Market Jumps

1. Set daily jump threshold: Aim for about 1% of

daily moves à |2.5%| for most countries.

2. Pull dates with market moves > threshold

3. Use newspaper articles to characterize jumps

A. Go to online newspaper archive

B. Enter newspaper, date range (next day) and search

criteria (e.g., “stock market”)

C. Select article

4. One or more humans read the article(s).

5. Record the reason for the jump, its geographic

source, confidence of reporter in explanation,

ease of coding for the reader, etc. 39Jumps by Reason Template

Policy Categories Non-Policy Categories

Government spending Macroeconomic news & outlook

Taxes Corporate earnings & profits

Monetary policy & central banking Commodities

Trade & exchange rate policy Unknown/no explanation

Regulation (other than above) Foreign Stock Markets

Sovereign military & security Terrorist attacks & large-scale

actions violence by non-state actors

Other policy (specify) Other non-policy (specify)

40Preview of Selected Findings 1. Policy news is a major trigger of stock market jumps (according to newspapers) – Journalists attribute 40% of U.S. jumps to policy – More than Macro Outlook (27%) or Corporate Earnings (11%) – Policy share of jump attribution is smaller in most countries – Policy share rises with jump size 2. U.S. developments trigger a huge share of equity market jumps across the globe. – Excluding data for the United States, leading local newspapers attribute 34% of jumps in their national stock markets to developments that originate in the U.S. – The U.S. role in this regard dwarfs the role of Europe, China and other large regions and countries – U.S. role is especially pronounced during the GFC.

Preview of Selected Findings

3. The persistence of national equity

return volatility varies by jump reason.

– Jumps attributed to monetary policy exhibit much less post-

jump return volatility.

4. The clarity of journalist perceptions as

to jump reason varies among jumps

– We quantify perception clarity in several ways.

5. Greater clarity about jump reason à

– Lower intraday market volatility on the jump day

– Lower volume on the jump day

– Greater concentration of jump-day move in a short interval

– Smaller jump-day gain in the VIX100-Page Guidebook for Coders

More on the Coding Process • Coders = authors and RAs • Coders read article and record the jump reason, the geographic source of the jump- triggering news, journalist confidence about jump reason, and more. • RA training process • RA monitoring process • We randomize the order in which RAs review jump days to avoid conflating coder- learning effects and calendar-time effects.

Selected Category Definitions

and Examples from the

Data Construction Guide

The examples on the next several slides give

an indication of how we provide guidance for

coding newspaper articles.

45Taxes

News reports, concerns or events related to current,

planned, or potential tax changes (e.g., income tax hikes,

payroll tax cuts, corporate tax reform, sales tax change,

etc.) and their consequences.

46Taxes, 2

This article is coded as Taxes

because it claims directly that if

anything could be cited as a reason

it would be the tax bill that was

passed. The confidence would be

medium to high because the article

spends some time discussing the

tax bill and claims that the bill was

almost certainly the reason, saying

if any one reason could be cited it

would be that one.

47Government Spending

News reports, forecasts, or concerns about

government spending and its consequences,

including spending matters related to stimulus

programs, publicly funded pensions, social

security, health care, etc.

48Government Spending, 2

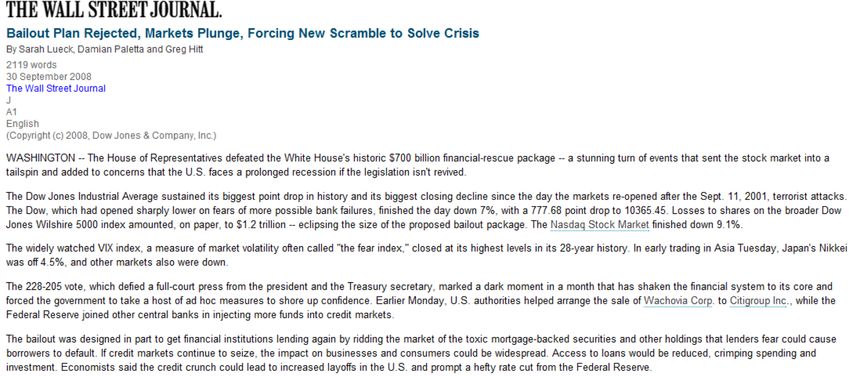

This article is coded as government spending because the first reason

listed for the stock market plunge is the rejection of the government’s

bailout plan. The bailout plan itself involves the government spending

money to help the economy, and even though it is a rejection of the plan, it

is still coded as government spending.

49Macroeconomic News and Outlook

News relating to macroeconomic forecasts or reports such

as inflation, housing prices, unemployment or employment,

personal income, industrial production, manufacturing

activity, etc.

Also included in this category:

• News about financial crisis developments that does not

fall into another category such as Monetary Policy and

Central Banking.

• Trade and exchange rate news NOT attributed to policy

(e.g., news about trade deficits or currency movements)

50Macroeconomic News and Outlook, 2

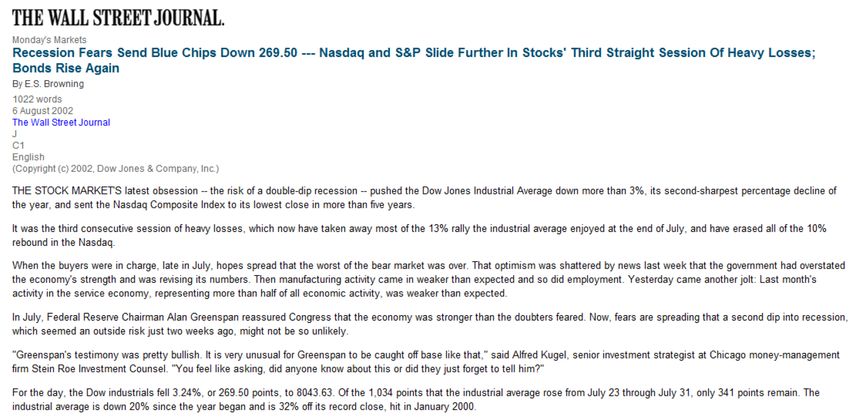

This article claims that the reason for the market move was a fear of a double-dip

recession, a change in the Macroeconomic Outlook. Therefore the article would be

coded as Macroeconomic News and Outlook. The confidence would be high because

the article clearly declares that the fear of recession was the cause for the movement.

51Monetary Policy and Central

Banking

Actions, possible actions, and concerns related to the

conduct and policies of the central bank or other chief

monetary authority. Such actions and policies pertain to

interest rate changes and monetary policy

announcements, inflation control, liquidity injections by the

monetary authority, changes in reserve requirements or

other bank regulations used by the monetary authority to

exercise control over monetary conditions, lender-of-last

resort actions, and extraordinary actions by the monetary

authority in response to bank runs, systemic financial crisis

and threats to the payments system.

52Monetary Policy and Central

Banking 2

This article is coded as Monetary

Policy because it cites the reason for

the market rally as a statement from

the Fed that they will pay less

attention to weekly swings in the

monetary supply, a change in their

policy. The confidence and ease of

coding would also be high because

the article clearly claims the Fed

statement is the reason for the jump.

53Distinguishing Monetary Policy &

Central Banking from Macroeconomic

News & Outlook

Some news articles that discuss market reactions to macro

developments also discuss the Fed’s normal response to the

macro development. Generally, we code an article as Macro

News & Outlook if it attributes the market move to news

about the macro economy. We code it as Monetary Policy &

Central Banking if the article attributes the market move to

(a) news about a change in how the Fed responds to a given

macro development or (b) news about unexpected

consequences of Fed actions.

It is helpful to approach this classification issue from a Taylor

Rule perspective. Consider the following cases:

54Distinguishing Monetary Policy &

Central Banking from Macroeconomic

News & Outlook, 2

1. Macro news: The market moves because it anticipates or

speculates (or sees) that the Fed will respond in its usual

manner to news about the macro economy. That is, the

market anticipates or speculates that the Fed will respond

to macro developments according to a well-understood

description of the Fed's interest-rate setting behavior.

2. Monetary policy: The market moves because of a surprise

change in the policy interest rate -- i.e., a surprise

conditional on the state of the macro economy. From a

Taylor Rule perspective, we can think of this change as a

new value for the innovation term in the Taylor rule.

55Distinguishing Monetary Policy &

Central Banking from Macroeconomic

News & Outlook, 3

3. Monetary policy: The market moves because of an

actual or potential change in the Fed’s policy rule. From

a Taylor Rule perspective, this event corresponds to an

actual or potential change in the form of the Taylor Rule

or a change in specific parameter values. A concrete

example would be a big market response to proposals to

increase the target interest rate.

4. Monetary policy: The market moves because of news

that leads to revised views or concerns about the

consequences of the Fed's actual or anticipated actions.

Articles in category 1 get coded as Macro News & Outlook.

Articles in categories 2, 3 and 4 get coded as Monetary

56

Policy & Central BankingExample 1 (2/8/2018, S&P 500 index return -3.75%): This article would receive a primary category of Macroeconomic News and Outlook (Non- Policy) because the article links rising inflationary pressures to tighter monetary policy. These explanations fit well with Taylor Rule-like conduct by central banks, and therefore would not be classified as monetary policy.

Coding U.S. Jumps • Jumps: Days when CRSP Value-Weighted Index (VWI) has absolute return of at least 2.5%, measured using closing prices. • All jumps coded by 2+ persons for quality control and analysis of agreement rates. • For jumps after WWII, we use five papers (WSJ, NYT, BG, WP & LAT) to compare interpretations and analyze agreement rates.

US Jumps by Year (policy 40%)

Depression Lowest

Growth (1932)

50

Second

Downturn (1937)

Global

Financial

1893 Panic 1901 Crisis

Panic Black

WWI Oil Shock Monday

WWII

0

Banking Tech

Panic of Boom/

1907 Bust

1929

Crash

-50

NY Times and WSJ

1890 1910 1930 1950 1970 1990 2010

Unknown + No Article Non-Policy

Policy

Notes: Each bar shows the number of positive or negative jumps in the year. Shadings indicate the

number of jumps triggered by “Policy” and “Non-Policy” news. The residual category reflects jumps

attributed to unknown causes by the newspaper article and instances in which we found no article about

the jump, which never happens after 1925.Breakdown of US jumps by Category:

Prewar vs. Postwar and Positive vs. Negative

1926-1945 1946-2016 Share of Jumps Within Each Period

Category Negative Positive Negative Positive 1926-1945 1946-2016 Share Negative

Commodities 27 21 6 4 9.2% 2.7% 56.5%

CorporateEarningsandProfit 30 19 26 24 9.2% 12.8% 57.1%

ElectionsandPoliticalTransitions 6 5 7 8 2.0% 3.8% 50.0%

ForeignStockMarkets 5 2 4 1 1.2% 1.2% 77.5%

GovernmentSpending 12 30 11 15 8.1% 6.6% 33.3%

MacroNews 57 61 83 45 22.6% 32.8% 56.8%

MonetaryPolicyCentralBanking 10 27 12 35 7.1% 11.9% 26.3%

NonSovMilitaryTerror 0 1 3 2 0.2% 1.3% 60.4%

OtherNonPolicy 15 6 7 3 4.0% 2.5% 70.9%

OtherPolicy 8 12 3 4 3.8% 1.8% 39.6%

Regulation 18 12 5 5 5.6% 2.4% 57.3%

SovMilitary 40 19 15 9 11.3% 6.1% 66.1%

Taxes 7 5 2 4 2.4% 1.5% 46.6%

TradeandExchangeRatePolicy 4 8 0 4 2.3% 1.0% 28.6%

Unknown 37 20 17 28 11.0% 11.6% 53.2%

Total 274 247 201 190 100.0% 100.0%

Sum Total 912

US jump definition: Days where the CRSP Value-Weighted

Index (VWI) has an absolute return of at least 2.5%.Validation Exercises, 1 1. Industry-Level Jump Responsiveness: For many jumps, the explanation offered in next-day accounts implies an amplified or dampened response of certain industries to the news that moved the overall market. Example 1, Banks: During the GFC, the stock market responded positively to upward revisions in the likelihood or generosity of bank bailouts. For this type of jump, we expect an even more favorable response for Bank stocks. That is, the response of Bank stocks is AMPLIFIED relative to the overall market response. Example 2, Guns: When bad news about the likelihood or duration of the Iraq war generated a negative jump, we expect the response for Guns (Defense firms) to be DAMPENED relative to the overall market response. While a longer war may be bad for the overall U.S. economy, it is less bad (or even good) for the Guns industry.

Validation Exercises, 2

Implementation:

• Obtain daily portfolio returns for 49 industries.

• Review coding detail for U.S. equity market jumps from 1960 to

2016. If the detailed description for jump-date t implicates

industry i, then assign values to !"#$% as follows:

!"#$% = 1, if jump description implies AMPLIFIED response of i.

= -1, if jump description implies DAMPENED response of I;

= 0, OTHERWISE.

• In making these industry assignments, we take a conservative

approach, as follows:

– We typically make industry assignments based on the Primary jump reason

only, not the Secondary Jump reason (if there is a Secondary reason.

– We set !"# to 0 when the detailed explanation for the Jump involved an

overly broad industry group for our purposes. For example,

“Manufacturing,” maps to at least 15 of the 49 industry groups.Validation Exercises, 3

• Most jumps do not map readily to a particular industry.

Sometimes, we assign 2 industries to a given jump. Most, but not

all, of these dual assignments involve Sovereign Military Jumps,

which implicate both Guns and Aerospace.

• Among our 339 jumps from 1960 to 2016, we obtain 115 Jump-

Day X Industry observations with nonzero Tri values, as follows:

– Banks: 38 nonzero values

– Guns: 19

– Aerospace: 16

– Others, all with less than 10 nonzero Tri values: Oil, Coal, Building

Materials, Construction, Autos, Chips, Hardware, Household Goods,

Software, Electrical Equipment

• !"# = the daily return for industry portfolio i on day t.

• %!# = the daily return on market portfolio on day t.Validation Exercises, 4

One-industry-at-a-time approach

Consider daily industry-level returns for i :

89: = < + >?8: + @ABC9: + DABC9: ?8: + E:

Pooled-sample approach

Consider daily industry-level returns for industries

with at least 3 nonzero Tri values:

89: = ∑9 9 ?8: + ∑9 @9 ABC9: + DABC9: ?8: + E:

Under both approaches, the hypothesis of interest is

LM : D = 0, LP : D > 0Validation Exercises, 5

Banks Pooled Sample

All Days Jump Days All Days Jump Days

Coefficient 0.80*** 0.74*** 0.55*** 0.51***

(St. Error) (0.23) (0.24) (0.13) (0.13)

Observations 13,469 339 109,760 4720

R-Squared 0.67 0.83 0.56 0.81

A regression for Guns, yields results similar to the Pooled ones, but the standard

error is large and the coefficient estimate is insignificant. When we set Tri=-1 for

the Aerospace industry for jumps attributed to Sovereign Military Conflict, the

Aerospace regression yields a small, marginally significant coefficient of the wrong

sign. That may reflect the ambiguous nature of Aerospace firms’ responses to

military conflict: (relatively) good news for defense-oriented aerospace firms may,

at the same time, be bad for aerospace firms oriented toward civilian customers.

If we set Tri=1 for Aerospace in these cases, the anomalous Aerospace result

disappears, and the Pooled Sample results get stronger.Validation Exercises, 6

These results confirm that our classification of jumps (based on next-

day newspaper accounts) reflects useful information about actually

triggered the jump.

2. Announcement-Date Responses: We test

whether jumps attributed to:

– Monetary Policy & Central Banking are relatively

likely on FOMC announcement dates (Yes)

– Macroeconomic News & Outlook are relatively likely

on release dates for the Employment Situation

Report and the CPI Report (Yes)

– Elections & Political Transitions are relatively likely

the day after national elections (Yes)Countries, Time Periods, Newspapers and Jump Thresholds

Jump

Country Start End Primary Newspapers

Threshold

United States 1885 2016 Wall Street Journal and NY Times 2.50%

United Kingdom 1930 2011 Financial Times (UK Edition) 2.50%

Australia 1985 2011 Australian Financial Times 2.50%

Canada 1980 2012 The Globe and Mail 2.00%

China (Hong Kong) 1988 2011 South China Morning Post 3.80%

China (Shanghai) 1994 2013 Shanghai Securities Journal 4.00%

Germany 1985 2012 Handelsblat, FAZ 2.50%

Greece 1989 2015 Kathimerini, To Vima 4.00%

Ireland 1987 2012 The Irish Times 2.50%

Japan 1981 2013 Yomiuri and Asahi 3.00%

New Zealand 1996 2011 New Zealand Herald 2.50%

Saudi Arabia 1994 2013 Al Riyadh 2.50%

Singapore 1980 2013 Business Times and Straits Times 2.50%

South Africa 1986 2013 Business Day 2.50%

South Korea 1980 2013 Chosun Ilbo 2.50%

Notes: Jump thresholds vary somewhat across countries to account for

differences in unconditional volatility. We select a jump threshold such that

about 1% of daily moves satisfy the jump criterion.Breakdown of international jumps by category

Category Negative Positive Share Negative

Commodities 84 96 46.7%

CorporateEarningsandProfit 212 143 59.7%

ElectionsandPoliticalTransitions 36 34 51.4%

ForeignStockMarkets 280 221 55.9%

GovernmentSpending 56 93 37.6%

MacroNews 649 356 64.6%

MonetaryPolicyCentralBanking 120 206 36.8%

NonSovMilitaryTerror 39 11 78.0%

OtherNonPolicy 245 206 54.3%

OtherPolicy 67 111 37.6%

Regulation 54 47 53.5%

SovMilitary 55 44 55.6%

Taxes 7 11 38.9%

TradeandExchangeRatePolicy 13 17 43.3%

Unknown 212 243 46.6%

Total 2129 1839

Sum Total 3968

The sample for this table starts in 1980 and ends in 2013 to

maximize sample-period overlap across countries.Count by year for the UK (policy 33%)

Recession and

40

1976 IMF crisis

Global

Financial

Crisis

20

Tech

Great crash

Depression Sterling

Crisis

0

WWII Suez

Crisis Black

Monday

-20

1930 1950 1970 1990 2010

Unknown + No Article Non-Policy

PolicyYearly Count - All Countries (policy 26%)

Global

20

Financial Crisis

Early

1990’s

10

Recession

0

-10

Eurozone

Asian and Crises

Russian

Financial

-20

Crises

-30

1985 1990 1995 2000 2005 2010 2015

Unknown + No Article Non-Policy

Policy

Notes: Each bar is the average number of jumps per year across the following countries: Australia,

Canada, China (HK), China (Shanghai), Germany, Greece, Ireland, Japan, New Zealand, Saudi Arabia,

Singapore, South Africa, South Korea and UKPolicy share rises with jump threshold

Increase Initial

Threshold By # Jumps Policy Share

0.0% 4340 26.4%

0.50% 2933 28.4%

1.00% 2031 29.0%

1.50% 1479 30.9%

2.00% 1134 32.5%

2.50% 812 31.8%

Using our sample of 14 countriesShare of Jumps Attributed to U.S. Developments

.8

Sample excludes Jumps in U.S. stock market

.8

Global

Tech Boom/ Financial

Early 1980’s Bust Crisis

.6

.6

recession

US Share of Global GDP

US Share of Jumps

1987 Crash

.4

Asian/LTCM

.4

crises

Eurozone

.2

Crisis

.2

Gulf War I

0

1980 1990 2000 2010

U.S. Jump Share U.S. GDP Share

0

1980 1990 2000 2010

Notes: Average share of jumps attributed to U.S. developments by year in Australia, Canada,

China (HK), China (Shanghai), Germany, Greece, Ireland, Japan, New Zealand, Saudi Arabia,

Singapore, South Africa, South Korea and UK. Dot size is proportional to the average number of

jumps by country/year. U.S. Share of PPP-adjusted global GDP using IMF data.Geographic Source of Jumps by Country

and Bilateral U.S. Trade Share

North America: US

North America: Canada

Asia: Singapore

Other: South_Africa

Other: Australia

Europe: Ireland

Asia: Japan

Europe: Germany

Asia: Korea

Asia: Hong_Kong

Europe: UK

Other: New_Zealand

Europe: Greece

Other: Saudi_Arabia

Asia: Shanghai

0 .2 .4 .6 .8 1

US Europe

Asia Other

Notes: Red X shows the average bilateral trade share with the United States from

1999 to 2015, measured as (exports + imports) / (Domestic GDP).Jump Shares Attributed to U.S. & Europe

The sample for “US Jump Share” excludes the United States

The sample for “Europe Jump Share” excludes European countries

.8

.6

.4

.2

0

1980 1990 2000 2010

Europe Jump Share US Jump Share

Europe GDP Share US GDP Share

GDP shares computed using contemporaneous exchange rates.Jumps Attributed to Monetary Policy

Exhibit Less Post-Jump Volatility

Using Daily U.S. Data from 1946-2016

Average Cumulative Squared Returns

.01

.008

.006

.004

.002

0

0 5 10 15 20

Days After

No Jump Monetary Policy

Macro News All Other JumpsMonetary Policy Jumps Continue to Show Less Post-Jump

Volatility When We Control for Jump Size and Direction

U.S. Data

(3)

1946-2016

(4)

1990-2016

(5) Daily U.S. Data

Jump 0.83*** 0.43*** 0.29**

(0.13) (0.13) (0.13)

Return 10.36*** 10.96***

Note: The dependent variable is the

(1.42) (2.05) cumulative realized volatility over the

|Return| x Return < 0 25.70*** 30.82*** following 22 trading days. The category

(2.06) (3.07)

Commodities -0.77*** -0.64*** -0.34

variables are dummies equal to one for

(0.24) (0.23) (0.71) a jump of that type. The omitted

Corporate Profits -0.13 -0.08 -0.01 category is Macroeconomic News, the

(0.24) (0.23) (0.25)

Military -0.73*** -0.72*** -0.73***

most common jump category. In

(0.17) (0.16) (0.20) addition to the reported controls, we

Monetary Policy -0.57*** -0.48*** -0.47*** include an NBER recession dummy and

(0.16) (0.15) (0.17)

Other Non-Policy 0.78 0.61 -0.94*** a dummy for return less than zero on

(0.79) (0.82) (0.22) the jump day. Robust standard errors

Fiscal and other policy 0.33 0.32 0.90***

in parenthesis. *** pAre jump codings reliable and consistent?

Two potential concerns about the method:

1. Two persons reading same article may code jumps

differently

2. Results may depend on newspaper consulted

To evaluate these concerns we:

1. Use multiple RAs for same paper - calculate

agreement

2. Use multiple papers - Boston Globe, LA Times, NY

Times, WSJ, Washington Post - calculate agreementAverage Pairwise Agreement Rates

1

Across Coders, Same Paper

1 .8

average 89%

.8 .6

P(Agree)

average 75%

.6 .4

P(Agree)

.4 .2

.2 0

1980 1990 2000 2010

Policy Agreement 16 Category Agreement

0

Notes: Agreement is the share of codings (at the coder-level) that agree, averages are shown for each year.

1980 1990 2000 2010Average Pairwise Agreement Rates Across

Newspapers, Different Coders

1

average 79%

.8

.6

average 49%

P(Agree)

.4

.2

0

1980 1990 2000 2010

16 Categories Policy

Notes: There are 9 coders, across 5 newspapers each day. Agreement is the share of pairs that agree, out of

36 possible pairs. Dots represent an annual average of the share of pairs which agree.Measuring Perceived Jump Clarity

We measure Jump Clarity by averaging five

measures (all on 0-1 scale) for each jump:

1. Pairwise agreement rate among coders as to

jump reason (according to the journalist)

2. Pairwise agreement rate among coders for

same newspaper

3. Journal confidence about jump reason

4. Ease of coding the jump

5. Whether the article said the jump reason was

“Unknown” or offered No Explanation.

We reverse the sign on item 5 before combining

it with the items 1 to 4.Greater Jump Clarity Involves • Lower intraday volatility on jump day (sum of squared 5-minute returns) • Lower market volume on jump day (trades in SPY, largest and most liquid S&P 500 ETF) • Greater concentration of market move on jump day (share of day’s total return in 5-minute window with largest absolute return) • Smaller VIX gain on jump day (change from previous day’s close)

Jump-Day Volatility, Volume, Concentration and VIX Change

Regressed on Clarity Index and Controls

U.S. data from 1996 to 2011. All specifications include controls for day of the week,

month of the year and year.

Volatility Volume Concentration Change in VIX

Clarity [Alternative] -0.11*** -0.05*** 0.04** -0.03*

(0.04) (0.01) (0.02) (0.02)

Return 95.02*** 33.75*** 10.7 -5.19

(21.36) (7.97) (6.85) (5.98)

Return < 0 1.23 0.34 -0.16 1.76***

(0.85) (0.39) (0.46) (0.49)

|Return| x Return < 0 160.44*** 65.30*** 9.61 43.36***

(28.20) (12.11) (12.65) (14.34)

Constant -3.33*** -2.24*** 0.42 -0.82

(0.80) (0.49) (0.55) (0.54)

Observations 235 224 235 223

R-squared 0.587 0.864 0.356 0.753Government Bonds and Exchange Rates We extend our method to U.S. and U.K government bond yields and U.S. exchange rates. 1. Macroeconomic News & Outlook is the main (65%) trigger for jumps in U.S. bond yields. Monetary Policy & Central Banking accounts for another 28%. 2. U.K. bond yields show a muted version of the same pattern: Macro = 43%, Monetary = 23%. 3. Macroeconomic News & Outlook is also the most important trigger for jumps in U.S. exchange rates, with Monetary Policy next.

10-Year U.S. Government Bonds, Jumps Per Year, 1970-2013,

Jump threshold: |relative yield change| > 0.04 OR |yield change| > 0.2

30

20

10

0

-10

Policy-Triggered Increases Other Increases

-20

No Article Found, Increases Policy-Triggered Decreases

Other Decreases No Article Found, Decreases

-30

70

72

74

76

78

80

82

84

86

88

90

92

94

96

98

00

02

04

06

08

10

12

19

19

19

19

19

19

19

19

19

19

19

19

19

19

19

20

20

20

20

20

20

20

8610-Year U.K. Government Bonds, Jumps Per Years, 1979-2013,

Jump threshold: |relative yield change| > 0.04 OR |yield change| > 0.2

20

15

10

5

0

-5

-10

Policy-Triggered Increases Other Increases

-15

No Article Found, Increases Policy-Triggered Decreases

Other Decreases No Article Found, Decreases

-20

79

81

83

85

87

89

91

93

95

97

99

01

03

05

07

09

11

13

19

19

19

19

19

19

19

19

19

19

19

20

20

20

20

20

20

20

87U.S. Trade-Weighted Exchange Rate, Jumps per Year, 1973-2013,

Jump threshold: |relative change| > 0.015

15

10

5

0

-5

Policy-Triggered Appreciation Other Appreciation

Dollar No Article Found, Appreciation Policy-Triggered Depreciation

Depreciation Other Depreciation No Article Found, Depreciation

-10

73

75

77

79

81

83

85

87

89

91

93

95

97

99

01

03

05

07

09

11

13

19

19

19

19

19

19

19

19

19

19

19

19

19

19

20

20

20

20

20

20

20

88USD-GBP Exchange Rate, Jumps per Year, 1972-2013,

Jump threshold: |relative change| > 0.015

20

15

10

5

0

-5

-10

-15

Policy-Triggered Appreciation Other Appreciation

-20 No Article Found, Appreciation Policy-Triggered Depreciation

Dollar

-25

Depreciation Other Depreciation No Article Found, Depreciation

72

74

76

78

80

82

84

86

88

90

92

94

96

98

00

02

04

06

08

10

19

19

19

19

19

19

19

19

19

19

19

19

19

19

20

20

20

20

20

20

89Some Next Steps

1. Code additional jumps and extend sample.

2. Expand analysis of how post-jump market

behavior relates to jump reason.

3. Some (policy-induced) jumps mitigate market

volatility and uncertainty, others amplify it.

– Operationalize and apply this distinction.

4. Improve the Jump Clarity Index

– Relate Clarity to pre-, post- and jump-day outcomes.

– Is there more scope for “narratives” to emerge,

spread and affect asset prices when clarity is low?

5. Automate classifications and extend to smaller

market moves.References

Baker, Scott R., Nicholas Bloom and Steven J. Davis, 2016. “Measuring Economic Policy

Uncertainty,” Quarterly Journal of Economics, 131, no. 4 (November), 1593-1636.

Baker, Scott, Nicholas Bloom, Steven J. Davis and Marco Sammon, 2018. “What Triggers

Stock Market Jumps?” American Economic Association Meetings, January.

Blanchard, Olivier J. Beth Anne Wilson, Mohammad Jahan-Parvar, Juan M. Londono,

Chris Collins and Thomas Pellet, 2018. “Why Has the Stock Market Risen So Much

Since the Election?” Peterson Institute for International Economics Working Paper.

Campbell, John L., Hsinchun Chen, Dan S. Dhaliwal, Hsin-min Lu and Logan B. Steele,

2014. “The Information Content of Mandatory Risk Factor Disclosures in Corporate

Filings,” Review of Accounting Studies, 19, 396-455.

Cutler, David, James M. Poterba and Lawrence H. Summers, 1989. “What Moves Stock

Prices?” Journal of Portfolio Management, 15, no. 3 (Spring), 4-12.

Davis, Steven J., 2017. “Regulatory Complexity and Policy Uncertainty: Headwinds of

Our Own Making.” Prepared for the Hoover Institution Conference on “Restoring

Prosperity: Contemporary and Historical Perspectives” at Stanford University on 9-

10 February 2017. Becker Friedman Institute Working Paper.

Davis, Steven J. and Cristhian Seminario, 2018. “Diagnosing the Stock Market Reaction

to Trump’s Surprise Election Victory,” University of Chicago, in progress.References

Pastor, Lubos and Veronesi, Pietro, 2012. “Uncertainty about government policy and

stock prices,” Journal of Finance, 67, 1219-1264.

Pastor, Lubos and Veronesi, Pietro, 2013. “Political Uncertainty and Risk Premia,”

Journal of Financial Economics, 110, no. 3 (December), 520-545.

Schwert, G. William, 1981. “Using Financial Data to Measure Effects of Regulation,”

Journal of Law and Economics, 24, 121-158.

Shiller, Robert, 2017. “Narrative Economics,” American Economic Review, 107, no.4

(April), 967-1004.

Wagner, Alexander F., Richard J. Zeckhauser and Alexandre Ziegler, 2017. “Company

Stock Price Reactions to the 2016 Election Shock: Trump, Taxes and Trade,” Journal

of Financial Economics, forthcoming.

Wagner, Alexander F., Richard J. Zeckhauser and Alexandre Ziegler, 2018. “Paths to

Convergence: Stock Market Behavior after Donald Trump’s Election,” CEPR

Discussion Paper DP 12657.

Wolfers, Justin and Eric Zitzewitz, 2018. “What Did Financial Markets Think of the

2016 Election?” American Economic Association, Papers & Proceedings,

forthcoming.You can also read