TPG Telecom & Vodafone Hutchison Australia - Merger of equals 30 August 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

TPG Telecom & Vodafone Hutchison Australia Merger of equals 30 August 2018

1) Transaction overview

Recommended merger of equals of TPG

Telecom and Vodafone Hutchison Australia

TPG and VHA have agreed to a merger of equals to create Australia’s leading challenger full-service

telecommunications provider

TPG Telecom (“TPG”) and Vodafone Hutchison Australia (“VHA”) have agreed Illustrative Merged Group shareholder structure

to implement a merger of equals to create Australia’s leading challenger full-

service telecommunications provider

TPG shareholders: 49.90% VHA shareholders: 50.10%

— Merged Group will be owned 49.9% by TPG shareholders and 50.1% by

Ultimate parent HTAL listed

VHA shareholders entity listed on LSE on ASX

— The Board of TPG intends to distribute a fully franked Cash Special

Dividend to TPG shareholders prior to completion of the Merger Other TPG Vodafone Hutchison

David Teoh WHSP

shareholders Group Plc(3) Australia(3)

The Merger will be implemented via a TPG Scheme of Arrangement, following

which the Merged Group will be listed on the ASX and will be named “TPG

Telecom Limited”

The Merged Group’s Net Debt will be ~$4.0bn on completion, representing 17.12% 12.61% 20.17% 25.05% 25.05%

~2.2x Net Debt / PF June 2018 EBITDA of $1,855m, excluding synergies(1)

— VHA will have Net Debt of $1,944m plus a $80m spectrum payment on 31

January 2019 via a recapitalisation by the current VHA Shareholders(2)

— TPG will have Net Debt of $1,672m plus a $352m spectrum payment on 31

January 2019, with the difference relative to TPG’s actual Net Debt ahead Merged

of completion intended to be distributed to TPG shareholders as a fully Group

franked Cash Special Dividend

New ASX listing

— Expected investment grade credit profile with strong cash flow generation To be named “TPG Telecom Limited”

which is anticipated to support an attractive dividend Implied Enterprise Value: $15.0bn(4)

Revenue (PF June 2018 LTM): $6,022m

TPG also intends to separate its Singapore mobile operations by way of an in- EBITDA (PF June 2018 LTM): $1,855m

specie distribution of shares

— The Singapore Separation will occur on or before implementation of the

Merger

Notes: (1) Based on 12 months pro forma EBITDA contribution of TPG and VHA as per unaudited accounts to 30 June 2018 of $1,855m. Leverage of ~2.2x includes TPG’s target Net Debt of $1,672m, VHA’s target Net Debt of

$1,944m and January 2019 700MHz spectrum payments of $352m and $80m respectively. Leverage does not include the January 2020 spectrum payments of $352m and $80m for TPG and VHA’s 700MHz spectrum

respectively, nor any working capital adjustments that may be required. (2) VHA Shareholders include upstream shareholders Vodafone Group Plc and Hutchison Telecom (Australia) Limited. (3) Look-through beneficial ownership

of VHA shareholders. (4) TPG’s equity value based on the last undisturbed share price close of $6.29 as at 21 August 2018, adjusted for the difference between TPG’s current Net Debt of $1,266m and its target Net Debt of

$1,672m. TPG’s Net Debt based on its target Net Debt of $1,672m plus its 700MHz spectrum payment of $352m due January 2019. VHA’s equity value based on the agreed merger ratio with reference to TPG’s adjusted equity

value. VHA’s Net Debt based on target Net Debt of $1,944m plus its 700MHz spectrum payment of $80m due January 2019. Excludes adjustments for Singapore Separation.

PAGE 1

1) Transaction overview

Summary of other key merger terms

TPG and VHA have entered into a Scheme Implementation Deed to effect the merger

Merged Group Board and management TPG Board and shareholder support Key approvals and transaction timing

Merged Group will be led by an experienced TPG’s Board of Directors unanimously Implementation of the Merger is conditional on

Board and senior executive team that will draw recommend TPG shareholders vote in favour regulatory approvals (including ACCC and

on the breadth of both groups’ skills and of the Merger, in the absence of a superior FIRB), TPG shareholder approval, court

expertise proposal and subject to the Independent approval, VHA successfully completing its

Expert concluding that the Merger is in the Restructure and completion of the Merged

— David Teoh (current CEO and Chairman of best interests of TPG shareholders Group’s refinancing

TPG) will be non-executive Chairman of

the Merged Group All TPG Directors intend to vote consistently Subject to when the various conditions are

with their recommendation all their satisfied, the Merger is expected to be

— Iñaki Berroeta (current CEO of VHA) will be shareholdings which they own, control or have implemented next year

CEO and Managing Director of the Merged

a relevant interest in, in favour of the Scheme

Group

in the absence of a superior proposal and

Merged Group Board of Directors will also subject to an independent expert concluding

include existing TPG directors Robert Millner that the merger is in the best interests of TPG

and Shane Teoh, two nominees of the shareholders

Vodafone Group, two nominees of Hutchison

Major shareholders of both TPG and VHA

Australia and two independent directors

remain committed to the long-term value

creation opportunities available to the Merged

Group and will also enter into separate 24

month voluntary escrow arrangements on this

basis(1)

Notes: (1) David Teoh has agreed to a 24 month escrow in relation to 80% of his interest in the Merged Group after Merger implementation. VHA Shareholders have agreed to a 24 month escrow on 100% of their shareholding

after Merger implementation.

PAGE 21) Transaction overview

Side-by-side comparison

Merger will deliver increased scale to support future growth, and an enhanced ability to invest and

innovate in a highly competitive telco market

Merged Group pro forma enterprise value of approximately $15.0bn(1)

Combined PF June 2018 revenue of $6.0bn, EBITDA of over $1.8bn and Operating Free Cash Flow of $0.9bn(2), excluding synergies

Combined market share across key markets of ~20% or more with significant opportunity to win market share from major competitors across mobile & fixed

markets and consumer & enterprise customers

Pro forma Merged Group, excluding synergies Merged Group(3)

Implied Enterprise Value(1) $7.5bn $7.5bn $15.0bn

Implied Equity Value(1) $5.4bn $5.5bn $10.9bn

Merged Group equity ownership 49.9% 50.1% 100%

Target Net Debt (post January 2019 spectrum) / EBITDA(5) 2.4x 2.0x 2.2x

Revenue – PF June 2018 LTM(5) $2,498m $3,569m $6,022m

EBITDA – PF June 2018 LTM(5) $839m $1,008m $1,855m

Operating Free Cash Flow – PF June 2018 LTM(2) $497m $391m $895m

Mobile market share(6) ~1%(7) ~19% ~20%

Mobile subscribers ~0.4m(7) ~6.0m ~6.4m

Fixed line broadband market share(6) ~22% n/a ~22%

Fixed line broadband subscribers(8) ~1.9m n/a ~1.9m

Notes: (1) TPG’s equity value based on the last undisturbed share price close of $6.29 as at 21 August 2018, adjusted for the difference between TPG’s current Net Debt of $1,266m and its target Net Debt of $1,672m. TPG’s Net

Debt based on its target Net Debt of $1,672m plus its 700MHz spectrum payment of $352m due January 2019. VHA’s equity value based on the agreed merger ratio with reference to TPG’s adjusted equity value. VHA’s Net Debt

based on target Net Debt of $1,944m plus its 700MHz spectrum payment of $80m due January 2019. Excludes adjustments for Singapore Separation. (2) Operating Free Cash Flow defined as EBITDA less Capex, before

spectrum payments based on preliminary pro forma twelve months period ending 30 June 2018. Excludes one-off payments of capital creditors and the impact of synergies. (3) Merged Group financials based on preliminary pro

forma merger adjustments including eliminations. (4) Pro forma leverage metrics based on June 2018 LTM EBITDA, TPG target Net Debt of $1,672m, VHA target Net Debt of $1,944m and January 2019 700MHz spectrum

payments of $352m and $80m, respectively. (5) 12 months Revenue and EBITDA for each of TPG and VHA based on unaudited accounts to 30 June 2018. (6) Consumer mobile phone service provider and consumer fixed

broadband services market share for 2016 as per ACCC Communications Sector Market Study Final Report – April 2018. (7) Represents TPG and iiNet MVNO customers. (8) Represents consumer broadband subscribers.

PAGE 31) Transaction overview

Compelling strategic rationale

1 Creating Australia’s leading challenger telecommunications operator

Significant scale across Australia, with complementary fixed line and mobile networks to create a stronger challenger to Telstra and Optus

Well positioned to capitalise on 5G opportunities

Sustained capital investment across both fixed and mobile networks with strategic portfolio of spectrum assets

Highly complementary owned network infrastructure will improve consumer telecommunication services and experience

2 Driving benefits for all customers

Integrated, full-service telecommunications company with a comprehensive portfolio of fixed and mobile products

Scale ensures attractive prices, improved customer interaction and long-term, sustainable consumer choice

Highly complementary product set and distribution channels across all Australian consumer, SME, corporate and government markets

Significantly enhances the customer experience

3 Creating shareholder value

Larger ASX-listed telecommunications operation with an enhanced ability to invest, innovate and compete against the major network operators

Improved returns on capital from increased scale, significant cost synergy potential as well as enhanced revenue cross-sell and upsell opportunities

Strong balance sheet with an expected investment grade credit profile and strong cash flow generation which is expected to support an attractive dividend

Improved returns to all shareholders of both companies

PAGE 42) Overview of the Merged Group

Stronger and more diversified operations

The Merged Group will have an enhanced network with highly complementary assets and a more

diverse earnings base across fixed broadband and mobile

TPG PF June 2018 VHA PF June 2018

Highly complementary owned network infrastructure

LTM EBITDA(1) LTM EBITDA(1)

TPG

Corporate

39%

VHA

2nd largest fixed voice and data Australia-wide mobile network $839m $1,008m Mobile

100%

network with 27,000km+ of with 5,000+ sites

metropolitan and inter-capital fibre

State of the art 4G network

400+ national network points of covering 22 million Australians TPG

presence Consumer

Substantial national low and 61%

Connected to 121 NBN POIs high band spectrum holdings

1,000s of on-net fibre buildings Access to the networks of both

Vodafone and Hutchison Group Merged Group PF June 2018 LTM EBITDA(2)

400+ DSLAM enabled exchanges

including unrivalled global

Wi-Fi networks in 5 major cities roaming and IoT services

TPG Consumer

International links into New Australian firsts: core network 28%

Zealand, Singapore, Hong Kong, virtualisation project and in-field VHA Mobile

Japan and the USA deployment of “4.9G” FDD 54%

massive MIMO $1,855m

TPG Corporate

18%

Notes: (1) PF June 2018 LTM EBITDA based on unaudited LTM accounts to 30 June 2018. (2) Illustrative segments shown prior to segment eliminations. Merged Group PF June 2018 LTM EBITDA of $1,855m includes pro forma

consolidation adjustments.

PAGE 53) Strategic rationale

Merged group will be a stronger

challenger to Telstra and Optus

Merged Group will be a more effective competitor to challenge the major network operators by

integrating fixed line and mobile businesses

Major network Mobile virtual

operators network operators

With an enterprise value of ~$15bn, the

Pro forma Merged Group will have sufficient scale

Merged Others

and scope to effectively compete

Group

against the majors

Enterprise

51.0 58.5 15.0 7.5(4) 7.5 0.3 2.6 n/a Highly complementary product offering

value (A$bn)(1)

across fixed line and mobile will provide

Mobile a complete solution for customers

~41% ~29% ~20% ~19% ~1%(5) MVNOs: ~10%

market share (%)(2)

Significant upside from Merged Group’s

Fixed line ability to win market share from Telstra

~51% ~17% ~22% n/a ~22% n/a ~6% ~4%

market share (%)(3)

and Optus

Estimated Australian spectrum holdings across Sydney & Melbourne (MHz)(6)

400

spectrum holdings (MHz)

334 Combined access to spectrum will

Current Australian

300

better position the Merged Group to

217 compete with the majors across both

196 metro and regional mobile markets

200 156

100

40

0

Optus Telstra Merged Group VHA TPG

Notes: (1) Enterprise values based on last close share prices as at 21 August 2018. TPG’s equity value based on the last undisturbed share price close of $6.29 as at 21 August 2018, adjusted for the difference between TPG’s

current Net Debt of $1,266m and its target Net Debt of $1,672m. TPG’s Net Debt based on its target Net Debt of $1,672m plus its 700MHz spectrum payment of $352m due January 2019. VHA’s equity value based on the agreed

merger ratio with reference to TPG’s adjusted equity value. VHA’s Net Debt based on target Net Debt of $1,944m plus its 700MHz spectrum payment of $80m due January 2019. Excludes adjustments for Singapore Separation.

(2) Consumer mobile phone service provider market share for 2016 as per ACCC Communications Sector Market Study Final Report – April 2018. TPG market share based on company estimates. (3) Overall consumer fixed

broadband market shares by group for 2016 as per ACCC Communications Sector Market Study Final Report – April 2018. (4) Implied enterprise value of VHA based on TPG current valuation and implied merger ratio assuming

VHA target Net Debt of $1,944m plus January 2019 $80m 700MHz spectrum payment, on a pro forma basis. (5) Represents TPG and iiNet MVNO customers. (6) Estimates of spectrum holdings based on public disclosures. For

FDD bands, both Uplink and Downlink spectrum volumes have been added.

PAGE 63) Strategic rationale

Highly complementary owned

network infrastructure

Combines innovative services including complementary fibre, 4G and Wi-Fi networks and allows the

Merged Group to be well positioned to capitalise on 5G

Vertical integration of highly complementary infrastructure assets across the Merged Group

VHA’s mobile network to leverage TPG’s backhaul capacity and 27,000km+ fibre network throughout Australia to rollout 5G services

~$2bn ~$6bn

Capital invested in Spent on network and

the fibre network technology in the last 5 years(1)

Metro &

DSLAMs / POIs International capacity Mobile sites Spectrum licences

inter-capital fibre

7,000km submarine

27,000km+ fibre 400+ DSLAM enabled

cable connecting

network exchanges Early-stage rollout of Recently secured

Sydney to Guam

National voice network 400+ network points of small cell technology in access to 700MHz

Capacity on Southern

Regional HFC & VDSL presence high density areas spectrum

Cross Cable

networks 121 NBN POIs

International links

Australia-wide mobile

network coverage

Long-term spectrum

5,000+ mobile sites

across 700, 850, 1800

91 NBN POIs nationally including

and 2100 MHz bands

n/a n/a

connected 1,200+ new sites and secured until 2028

site upgrades in 2018

Virtualising core

network to be 5G-ready

Notes: (1) Network spend comprises tangible and intangible fixed asset additions (sites, transmission, spectrum, Radio Access Network, software, hardware) and technology operating expenses.

PAGE 73) Strategic rationale

Complementary products and

distribution channels

Merged Group will provide a comprehensive telco product offering, catering to all customers, with

access to TPG’s corporate distribution channels and VHA’s consumer retail presence

Merged Group is expected to significantly enhance the customer experience across all current products and channels

Both TPG and VHA have a long history of driving innovation and challenging the major telco service providers to continually deliver more attractive value

propositions for customers

Combined strength will better position the Merged Group to continue investing in both fixed line and mobile networks to provide customers with an improved

quality of service and network coverage

Merged Group will offer a broader suite of products and services

Improved customer service and interaction via a combined omni-channel strategy, leveraging VHA’s retail storefront network

Consumers / SMEs Corporate / Enterprise

BRAVIN RAGAVAN TO INSERT

PAGE 83) Strategic rationale

Significant synergy potential

Merger is expected to achieve significant synergies

Both TPG and VHA have proven track records in delivering synergies and transformation

Key synergy categories

Leveraging the Highly complementary telecommunications network infrastructure provides opportunity for TPG and VHA to leverage

networks each other’s assets

Cross-sell

Opportunity to cross-sell products across both TPG’s and VHA’s combined corporate and consumer customer bases

opportunities

Rationalisation of

Reduction in costs from duplicated spend including back office and corporate services

duplicated costs

Economies of scale Scale benefits across all procurement including network, IT and marketing

PAGE 93) Strategic rationale

Increased financial scale and balance

sheet strength

Strengthened combined balance sheet with ~2.2x Net Debt / EBITDA, strong cash flow generation

and a combined enterprise value of $15.0bn

Combined revenue of $6.0bn and EBITDA of over $1.8bn on a pro forma June 2018 LTM basis, excluding synergies(1)

— Larger and diversified earnings base across fixed line, broadband and mobile services

Balance sheet flexibility with pro forma leverage of approximately 2.2x Net Debt / PF June 2018 EBITDA(2)

— Increased financial scale and strong combined free cash flow generation to provide an enhanced platform to pursue growth opportunities

— Expected investment grade credit profile

— Strong cash flow generation which is expected to support an attractive dividend and deleveraging profile

— It is intended that MergeCo will pay an attractive dividend of at least 50% of NPAT adjusted for one-off restructuring costs and certain non-cash items(3)

— Medium term target leverage range of 1.5 – 2.0x Net Debt / PF June 2018 EBITDA

Notes: (1) 12 months Revenue and EBITDA of each of TPG and VHA based on unaudited accounts to 30 June 2018. Merged Group financials based on preliminary pro forma merger adjustments including eliminations. (2) Pro

forma leverage metrics based on pro forma June 2018 LTM EBITDA, TPG target Net Debt of $1,672m, VHA target Net Debt of $1,944m and January 2019 700MHz spectrum payments of $352m and $80m, respectively.

(3) Adjustments for one-off restructuring costs and certain material non-cash items to ensure NPAT is more closely aligned to the cash generation of the Merged Group.

PAGE 104) Summary of Merger benefits

Benefits for all shareholders

Merger of equals is expected to deliver significant benefits for all shareholders

Exposure to an enhanced combined business profile with more diversified operations across fixed line, NBN and mobile ✔

Improved ability to invest in Australia’s telecommunications industry including significant investments across both fixed

line and mobile networks to compete with the major network operators ✔

Long-term infrastructure assets including an established nationwide fibre network and secured spectrum licences ✔

✔

Improved financial position and balance sheet strength with an expected investment grade credit profile and an intended

initial dividend payout ratio of 50% of NPAT adjusted for one-off restructuring costs and certain non-cash items(1)

✔

Significant value accretion for both TPG and VHA shareholders due to substantial cost synergies and enhanced revenue

cross-sell and upsell potential across the Merged Group

Notes: (1) Adjustments for one-off restructuring costs and certain material non-cash items to ensure NPAT is more closely aligned to the cash generation of the Merged Group.

PAGE 115) 3.6 GHz Spectrum Auction

Spectrum Joint Venture

TPG and VHA have formed a Joint Venture to secure spectrum and maximise its efficient use

Joint Venture Agreement Scope Purpose

In parallel to the merger agreement, TPG The Government is auctioning To secure long term spectrum for TPG and

and VHA have signed a Joint Venture 125 MHz of 3.6 GHz band spectrum, VHA, by ensuring that TPG and VHA are

Agreement expected in late November 2018 able to:

The incorporated JV (JVCo) will acquire, Scope of the JV is to acquire, hold and negotiate efficient sharing of spectrum

hold and licence spectrum to the licence 3.6 GHz spectrum and mobile/wireless infrastructure,

shareholders particularly for 5G;

The parties will negotiate with the aim

JV is ongoing, and will not terminate if the of expanding the JV’s business in acquire adjacent spectrum (which

merger fails to proceed future, including to acquire future facilitates efficient sharing); and

spectrum licences

have access to sufficient spectrum to

The JV will explore sharing of existing develop one or more 5G Radio Access

infrastructure, assets, facilities and a Networks

shared 5G Radio Access Network

(RAN)

JVCo will register as a participant in the TPG and VHA will participate in the Auction

3.6 GHz Spectrum Auction through JVCo

PAGE 126) Cash Special Dividend

Potential TPG Cash Special Dividend

The Board of TPG intends to distribute a fully franked Cash Special Dividend to TPG shareholders

prior to implementation of the Merger to the extent that TPG’s Net Debt balance is below the target

Net Debt of $2,024m(1) ahead of implementation of the Merger

TPG Cash Special Dividend Illustrative worked formula

As part of the Merger, the parties have agreed that TPG may distribute

a fully franked Cash Special Dividend near implementation of the merger

(1)

provided that TPG’s Net Debt balance at that time is below the agreed (A) TPG target Net Debt at implementation (A$m) 2,024

target Net Debt of $2,024m(1)

(B) Less: TPG’s actual Net Debt at implementation (B)

The TPG Board’s current intention is to declare the Cash Special

Dividend following satisfaction of key conditions precedent (C) Illustrative total Cash Special Dividend = (A) – (B)

The actual size of the Cash Special Dividend will be impacted by TPG’s

cash flows prior to implementation as well as transaction costs and other

customary completion adjustments (S) TPG shares on issue (#m shares on issue) 928

The final Cash Special Dividend will also be reduced by the level of cash Illustrative TPG Cash Special Dividend (A$ / per share) = (C) / (S)

that is used to capitalise TPG Singapore prior to the Singapore

Separation

Notes: (1) TPG’s target Net Debt of $2,024m based on agreed target Net Debt of $1,672m adjusted for upcoming 700MHz spectrum payment of $352m assuming implementation occurs after 31 January 2019.

PAGE 137) Singapore Separation

Singapore mobile business to be separated

Before implementation of the Merger, the Board of TPG Telecom also intends to separate its Singapore

mobile business (“SingaporeCo”) by way of an in-specie distribution of shares to existing TPG Shareholders

Singapore mobile business

In December 2016, TPG successfully bid to acquire spectrum in Singapore and announced its intention to rollout Singapore’s 4th mobile telecommunications

network

TPG remains on track to achieve the milestone of national outdoor service coverage in Singapore by the end of 2018

As announced in March 2018, TPG Singapore’s initial mobile product trials are expected in Q4 2018

Separation of SingaporeCo

TPG Board intends to separate 100% of SingaporeCo by way of an in-specie distribution of shares to existing TPG Shareholders

— Allows TPG shareholders to capture 100% of the upside of TPG Singapore otherwise not valued within the Merger

— TPG Board believes that the strong growth potential and early stage nature of SingaporeCo provides significant upside opportunity

The Singapore Separation will be implemented on or before implementation of the Merger and TPG has commenced engagement with the Singapore

Infocomm Media Development Authority in connection with the separation

The Board intends to capitalise SingaporeCo appropriately as the rollout continues in the near term

Further details regarding the Singapore Separation including timing, process and transaction structure will be provided in due course

PAGE 148) TPG trading performance

TPG preliminary FY18 results

TPG expects to report FY18 revenue of ~$2,490m and EBITDA of ~$840m, ahead of previous

guidance, based on preliminary unaudited accounts to July 2018

FY18 preliminary results(1)

Revenue ~$2,490m

EBITDA ~$840m

Net Debt balance(2) $1,266m

Notes: (1) Preliminary results to July 2018 based on unaudited accounts. (2) Net Debt based on bank debt plus finance leases less cash.

PAGE 15APPENDIX

A Vodafone Hutchison

AustraliaAppendix

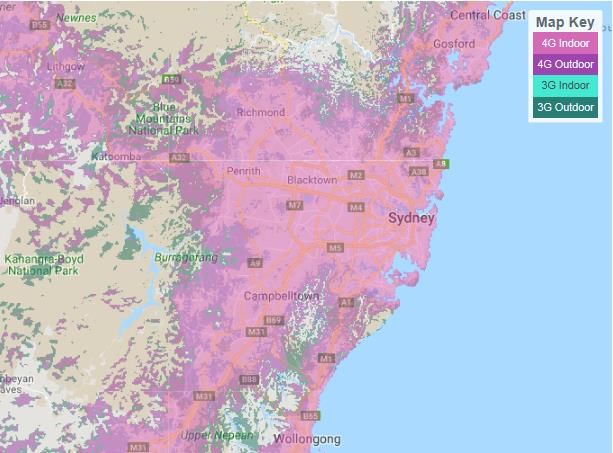

Overview of Vodafone Hutchison Australia

VHA is Australia’s 3rd largest mobile network operator with 6 million customers and

a 4G mobile network covering 22 million Australians

3rd largest Australian mobile network operator

— Mobile customer base of approximately 6 million

— 4G mobile network covers over 22 million Australians

National footprint of retail stores with a focus on metro areas

— 111 company owned stores nationally

— 257 exclusive dealer stores nationally

Coverage profile – Greater Sydney

Offers unique consumer and enterprise initiatives including International

$5 Roaming, no lock-in handset plans for mobile customers, Instant

Connect and 4G back-up for fixed customers

Recently acquired or renewed strategic spectrum holdings across 700,

850, 1800 and 2100 MHz bands

Leading NPS of the major Mobile Network Operators (“MNOs”) and the

lowest rate of customer complaints of MNOs

Employs ~2,500 people at its Sydney, Melbourne, Brisbane, Adelaide

and Perth offices, contact centre in Hobart

PAGE 17Appendix

Vodafone Hutchison Australia’s key metrics

In recent years, VHA has seen continued sustainable growth across its customer base,

growth in EBITDA and has become Australia’s leading major MNO by NPS

Continued growth in mobile network customers Sustained EBITDA growth

Total network customers (‘000) 5,978 EBITDA (A$m) 1,008

5,808

972

5,562

912

CY16 CY17 Jun-18 LTM CY16 CY17 Jun-18 LTM

Significant investment in network and spectrum(1) Leading Australian mobile network operator by NPS

Investment spend (A$m) 1,920

1,204 NPS

1,137

960

751

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 Apr-18 May-18 Jun-18 Jul-18

CY14 CY15 CY16 CY17 Jun-18 LTM Telstra Optus Vodafone

Notes: (1) Network spend comprises tangible and intangible fixed asset additions (sites, transmission, spectrum, Radio Access Network, software, hardware) and technology operating expenses.

PAGE 18Glossary of key terms

Term Definition

ACCC Australian Competition and Consumer Commission

Capex Capital expenditure

The potential cash special dividend by TPG, to the extent that TPG’s actual debt balance is below the agreed target Net Debt

Cash Special Dividend

balance ahead of implementation of the Merger

EBITDA Earnings before interest, tax, depreciation and amortisation

FIRB Foreign Investment Review Board

Hutchison Australia or HTAL Hutchison Telecommunications (Australia) Limited (ASX: HTA)

Hutchison Group CK Hutchison Holdings Limited (HKG: 0001) and its controlled entities

Merged Group The combined entity of both TPG and VHA following completion of the Merger

Merger The proposed merger of equals transaction between TPG and VHA

MVNO Mobile virtual network operator

Net Debt Financial indebtedness less cash

NPS Net promoter score

Restructure The series of transaction steps required by VHA and its shareholders to remove debt in excess of VHA’s target Net Debt figure

SingaporeCo TPG’s Singaporean operations including the rollout of a mobile network

Singapore Separation The separation of SingaporeCo from TPG, to occur on or before implementation of the Merger

TPG Telecom or TPG TPG Telecom Limited (ASX: TPM)

VHA Shareholders Refers to upstream holders of VHA including Vodafone Group plc and Hutchison Telecommunications (Australia) Limited

Vodafone Group or Vodafone Vodafone Group Plc (LSE: VOD)

Vodafone Hutchison Australia or VHA Vodafone Hutchison Australia Pty Limited

WHSP Washington H. Soul Pattinson and Company Limited (ASX: SOL) (a substantial shareholder in TPG)

PAGE 19Important notice and disclaimer

This presentation (Presentation) provides information in summary form and should be read in conjunction with the announcement in relation to the proposed merger of equals transaction between

TPG Telecom Limited (TPG) and Vodafone Hutchison Australia Pty Limited (VHA) (the Merger) that was released today. This Presentation does not purport to contain all the information that investors

may require in order to make a decision in relation to the Merger. It contains selected information only. Further information will be contained in additional documents to be released by TPG.

Neither of TPG nor VHA, nor their respective related bodies corporate, directors, officers, employees, agents, contractors, consultants or advisers makes or gives any representation, warranty or

guarantee, whether express or implied, that the information contained in this Presentation is complete, reliable or accurate or that it has been or will be independently verified. To the maximum extent

permitted by law, TPG, VHA and their respective related bodies corporate, directors, officers, employees, agents, contractors, consultants and advisers expressly disclaim any and all liability for any

loss or damage suffered or incurred by any other person or entity however caused (including by reason of fault or negligence) and whether or not foreseeable, relating to or resulting from the receipt or

use of the information or from any errors in, or omissions from, this Presentation. You should conduct and rely upon your own investigation and analysis of the information in this Presentation and

other matters that may be relevant to it in considering the information in this Presentation.

The information in this Presentation is not investment or financial product advice and is not to be used as the basis for making an investment decision. In this regard, the Presentation has been

prepared without taking into account the investment objectives, financial situation or particular needs of any particular person.

This Presentation only contains information required for a preliminary evaluation of the companies and, in particular, only discloses information by way of summary within the knowledge of TPG, VHA

and their respective directors. Included in this Presentation is data prepared by the management of TPG and/or VHA. This data is included for information purposes only and has not been subject to

the same level of review by TPG or VHA as their respective financial statements, so is merely provided for indicative purposes.

Estimates and forward looking information contained in this Presentation are illustrative and are not representations as to future matters, are based on many assumptions and are subject to significant

uncertainties and contingencies, many (if not all) of which are outside the control of TPG and VHA. Actual events or results may differ significantly from the events or results expressed or implied by

any estimate, forward looking information or other information in this Presentation. No representation is made that any estimate or forward looking information contained in this Presentation will be

achieved and forward looking information will not be warranted. You should make your own independent assessment of any estimates and forward looking information contained in this Presentation.

The forward looking information in this Presentation comprises management projections or estimates only and has not been prepared or verified to prospectus standard. No representation is made

that there is a reasonable basis for that information.

This Presentation does not constitute an offer to sell, or to arrange to sell, securities or other financial products. This Presentation and the information contained in it does not constitute a solicitation,

offer or invitation to buy, subscribe for or sell any securities in the United States. The merged group shares to be issued under the Merger have not been, and will not be, registered under the U.S.

Securities Act of 1993 (the US Securities Act) or the securities laws of any state or other jurisdiction of the United Stated and may not be offered or sold, directly or indirectly, in the United States

unless the securities have been registered under the US Securities Act or are offered and sold in a transaction exempt from, or not subject to, the registration requirements of the US Securities Act

and other applicable securities laws.

The statements in this Presentation are made only as at the date of this Presentation and the information contained in this Presentation has been prepared as of the date of this Presentation. The

statements and the information remain subject to change without notice. The delivery of this Presentation does not imply and should not be relied upon as a representation or warranty that the

information contained in this Presentation remains correct at, or at any time after, that date. No person, including TPG, VHA and their respective related bodies corporate, directors, officers,

employees, agents, contractors, consultants and advisers accepts any obligation to update this Presentation or to correct any inaccuracies or omissions in it which may exist or become apparent.

PAGE 20You can also read