UNIVERSITY OF CANTERBURY STUDENT ACCOMMODATION DISCUSSION DOCUMENT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UNIVERSITY OF CANTERBURY

STUDENT ACCOMMODATION

DISCUSSION DOCUMENT

Date: 25 February 2014

Status: DRAFT

NOT UNIVERSITY OF CANTERBURY POLICY

WELLINGTON Level 20, 125 The Terrace, PO Box 3531, Wellington 6140, New Zealand. Phone +64 4 471 0665

AUCKLAND Level 12, 55 Shortland Street, PO Box 105-673, Auckland 1143, New Zealand. Phone +64 9 379 5753

SYDNEY Suite 3, Level 5, 66 Hunter Street, Sydney NSW 2000, GPO Box 254, Sydney NSW 2001, Australia. Phone +61 2 8031 7781

TABLE OF CONTENTS

1.0 EXECUTIVE SUMMARY 4

ABOUT THIS DISCUSSION DOCUMENT 8

1.1 IMPLEMENTATION 10

2.0 INTRODUCTION 11

2.1 THE UNIVERSITY OF CANTERBURY 11

3.0 STUDENT ACCOMMODATION AT UC 13

3.1 REVIEW OF EXISTING STOCK 13

Bishop Julius Hall 15

College House 16

Rochester and Rutherford Hall 18

University Hall (Retro & Ritz) 19

Sonoda Apartments 21

Ilam Apartments 23

Existing Stock - Capital Expenditure 24

3.2 2014 - STOCK UNDER CONSIDERATION OR SECURED 24

3.3 2015 - STOCK UNDER CONSIDERATION 25

4.0 UC DEMOGRAPHICS AND FORECAST FOR STUDENT ACCOMMODATION 27

4.1 UC DEMOGRAPHIC FORECAST 2014 - 2023 27

4.2 FORECAST FOR STUDENT ACCOMMODATION 32

5.0 CHRISTCHURCH POST EARTHQUAKE ACCOMMODATION ENVIRONMENT 38

5.1 ON-CAMPUS 38

5.2 OFF-CAMPUS - HOUSING PRESSURES IN CHRISTCHURCH 40

6.0 TRENDS IN STUDENT ACCOMMODATION 45

6.1 INTERNATIONAL TRENDS 45

6.2 NATIONAL TRENDS 48

7.0 LOCATION & STYLE OF ACCOMMODATION 52

7.1 LOCATION 52

7.2 DISTRICT PLAN 54

7.3 DRAFT UC DEVELOPMENT CORPORATION INVESTMENT OPPORTUNITY

FLYER (8 JULY 2013) 55

7.4 STYLE OF ACCOMMODATION 56

APPENDIX 1

Page 2 of 65

Postgraduate Survey on Student Experience – May 2013 61

APPENDIX 2

New Accommodation Lettings and Rental Values 64

Page 3 of 65

1.0 Executive Summary

The Christchurch earthquakes of September 2010 and February 2011 have

significantly changed Christchurch and The University of Canterbury (UC). UC has had

to adjust its business operation to cater for students in the post-earthquake

environment. Student accommodation has become a critical component of the student

experience and a key factor in a student’s decision as to attend UC.

Since the earthquakes UC has seen student numbers decrease by more than 3,000

EFTS1 (2013 versus 2010) and they are not forecast to return to pre-earthquake

numbers until 2020. The decline in EFTS does not provide a direct correlation to

demand for accommodation as the earthquakes have put significant pressure on

housing city-wide. The demand for housing is nowhere more evident than in the lower

to middle price range.

Post-earthquake, anecdotal evidence indicates a higher demand for UC

accommodation. There has also been more volatility in the student application and

acceptance process.

To address immediate 2014 requirements, UC has added in excess of 330 beds to its

portfolio for 2014. These are a mix of owned beds not previously used by UC, and

recently leased properties.

The UCSA student surveys in 2012 and 2013 demonstrate that the majority of students

are finding accommodation within 2km of UC and that rental costs have not increased

markedly over the last two years. A minority, however, have recorded more difficulty

finding suitable accommodation in 2013.

This document discusses the long term requirement for beds at UC based on its EFTS

growth forecasts. EFTS is equivalent full time students which has a flow on effect to

headcount numbers at the University.

Due to the lumpy nature of construction, new accommodation at UC could be occupied

over the medium term by groups affected by the earthquake as EFTS numbers

improve.

The Canterbury Earthquake Recovery Authority (CERA), the Canterbury Development

Corporation and the Ministry of Business, Innovation and Employment have each

provided statistics and forecasts relevant to the housing market in Christchurch. This

document is cognisant of the broader Christchurch housing market pressures, however

also recognises that the market will return to equilibrium at some time in the future.

1

Although a disproportionate number has been from the College of Arts whom we are advised are often

older or part-time students with less demand for UC student accommodation.

Page 4 of 65

More detail is presented in the next section. The three key findings providing guidance

are:

1. There is little quantitative evidence to support a significant new accommodation

requirement for current students. A decline in FTE’s post-earthquake has

increased the ratio of beds to students at UC. This ratio has been further

enhanced with the addition of 330+ beds in February 2014.

Anecdotal evidence, however, suggests demand for additional accommodation at

UC.

2. Strong growth forecasts of “Full Fee” paying Undergraduate students supports

circa 600 additional new beds for this sector. This requirement is not

immediate.

If development occurred ahead of demand from this sector the beds could be

occupied by domestic students in the interim. Building design would need to

accommodate both groups.

3. Strong growth forecasts for postgraduate students supports circa 200 additional

new beds for this sector. This requirement is not immediate.

If development occurred ahead of demand from this sector the beds could be

occupied by domestic students in the interim. Building design would need to

accommodate both groups.

A staged build program allows regular re-assessment of demand, and also the ability to

modify design to suit changes in the target market or accommodation trends.

Oversupply risk is further mitigated by the ability to exit leased accommodation as

leases expire.

The following table demonstrates forecasts for growth in equivalent full time students

(EFTS) for the different student groups.

Table 1: UC Equivalent Full Time Student Forecasts

Student Type Actual Forecast

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Domestic - under-graduate 10,256 9,407 9,357 9,346 9,622 10,044 10,482 10,870 11,179 11,427 11,636 11,841

Domestic - post-graduate 2,078 1,979 1,968 2,011 2,074 2,128 2,190 2,242 2,295 2,345 2,394 2,441

Sub-total Domestic 12,334 11,386 11,325 11,357 11,696 12,172 12,672 13,112 13,474 13,773 14,030 14,283

Full Fee - Under-graduate - Navitas - - - 80 194 304 398 498 600 703 805 907

Full Fee - Under-graduate - Non Navitas 770 728 690 694 732 788 855 939 1,038 1,153 1,288 1,391

Full Fee - Post-graduate 67 68 81 84 88 92 98 104 111 119 128 132

Sub-total Full Fee 837 796 770 858 1,015 1,184 1,351 1,541 1,749 1,975 2,220 2,431

TOTAL UC 13,171 12,182 12,095 12,216 12,711 13,356 14,023 14,653 15,223 15,748 16,250 16,713

Source: 10 Year Forecast Model, UC Financial Services

Page 5 of 65

Total UC EFTS were 15,500 in 2010. 2013 EFTS were 21% lower than 2010, however

UC is forecast to return to pre-earthquake EFTS numbers by 2020.

The following table demonstrates the forecast annual average growth in EFTS for each

student type between 2013 and 2023..

Table 2: Annual Average Forecast Growth in EFTS, 2013 to 2023

Student Group Annual Average Growth

2013 / 2023

Domestic - Undergraduate (local) 2%

Domestic - Undergraduate (non local) 3%

Domestic - Postgraduate 2%

Full Fee - Undergraduate (Navitas) 2014 first year

Full Fee - Undergraduate (non Navitas) 7%

Full Fee - Postgraduate 7%

TOTAL UC 3%

Source: 10 Year Forecast Model, UC Financial Services

The following themes are also reflected:

+ New first-year beds to be built near the centre of campus

+ Flexibility in design to cater for changes in demand over time (for example,

dislocated Christchurch students and domestic students in the short term and

international students over the longer term)

+ New accommodation to reflect latest international trends in living-learning

environments and provision of technology

+ Acknowledgement of UC’s policy of upgrading buildings to a minimum of 67% of

New Building Standard where economically and physically feasible.

A process to address positive or negative changes in EFTS forecasts is also

presented.

Whilst UC has a comprehensive understanding of the international student sector,

Navitas is a new market for UC. Further research into the needs of this cohort prior to

committing to any design or commercial arrangement for new accommodation may be

required. Key areas of research should include accommodation styles and pastoral

care requirements. These issues are discussed within the body of the report.

Providing new, purpose-built, on-campus accommodation will provide UC with a unique

opportunity to provide world class accommodation that will provide a competitive

Page 6 of 65

advantage in its endeavours to attract New Zealand’s best students, international

undergraduate students, and post-graduate and research students.

Success will be measured by the delivery of positive student experiences and higher

student retention, not just simply the provision of more beds. Pastoral care, student

management, living environments and catering (where provided) are all critical to the

student experience.

This report also sets out a flexible implementation programme.

Regular review and update will be needed to reflect changes in the student

accommodation business, changes in demand, and changes in the Christchurch

housing market. Regular review is more important in this instance due to the pace of

change in the Christchurch market following the Canterbury earthquakes.

Page 7 of 65

About this discussion document

The discussion document is presented under five key headings.

1. Increase supply of on-campus accommodation

The following table demonstrates EFTS forecasts for the groups identified as

requiring additional accommodation. A 40%2 ‘take-up’ of accommodation has

been assumed, and from that an indicative build programme is presented.

Table 3: Additional Student Accommodation Required, Type and Timing

Student Type Forecast

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 TOTAL

EFTS Forecast

Domestic - Postgraduate 1,979 1,968 2,011 2,074 2,128 2,190 2,242 2,295 2,345 2,394 2,441

Full Fee - Undergraduate (Navitas) - - 80 194 304 398 498 600 703 805 907

Full Fee - Undergraduate (non Navitas) 728 690 694 732 788 855 939 1,038 1,153 1,288 1,391

Full Fee - Postgraduate 68 81 84 88 92 98 104 111 119 128 132

Increase - Undergraduate (Full Fee) - 38 84 153 165 161 184 201 218 236 206

Increase - Postgraduate (Domestic & Full Fee) 2 47 67 58 68 58 60 58 57 52

Additional Accommodation Requirement Forecast (40% take-up assumption)

Domestic - Postgraduate - 17 25 22 25 21 21 20 19 19 189

Full Fee - Undergraduate (Navitas) - 32 46 44 38 40 41 41 41 41 363

Full Fee - Undergraduate (non Navitas) - 2 15 22 27 34 40 46 54 41 281

Full Fee - Postgraduate 5 1 2 2 2 3 3 3 3 2 26

Sub-total Undergraduate (Full Fee) - 34 61 66 64 74 80 87 95 82 643

Sub-total Postgraduate (Domestic & Full Fee) 5 19 27 23 27 23 24 23 23 21 215

Indicative Build Programme

Undergraduate (Full Fee) 100 125 150 200 575

Postgraduate (Domestic & Full Fee) 50 50 50 50 200

Source: 10 Year Forecast Model, UC Financial Services (EFTS data only)

The style of accommodation and to a lesser degree the timing of delivery of new

accommodation is subject to confirming a design brief. The following steps are

required:

- Complete research into target user group requirements.

- Prepare a design brief following engagement with the target markets.

Whilst EFTS numbers for Full Fee Undergraduates and Postgraduates grow relatively

smoothly over the forecast period the construction and delivery of student

accommodation is lumpy. The delivery of beds outlined above may need to be varied

to accommodation commercial terms with providers or the practicality of delivering a

number of smaller buildings versus fewer larger buildings. Clever design may allow

staged development over a period of years to match demand.

2. Location of new accommodation

2

The 40% take-up remains subject to review.

Page 8 of 65

o Undergraduate Accommodation

- Preferred locations are (in no particular order):

Dovedale campus

Montana Avenue

Ilam Stage 2 (behind Blocks K & L on Waimairi Road)

Independent Hall – College House

Independent Hall – Bishop Julius

- Aim to house first-year students closer to the “campus heart”.

o Postgraduate Accommodation

- Preferred locations are (in no particular order):

Dovedale campus

Waimairi Village and adjacent land

- Aim to locate these groups to the campus periphery.

3. Refurbishment of existing stock

o Confirm a minimum structural condition target for refurbished (owned)

student accommodation buildings of 67% of New Building Standard (NBS)

where technically and financially feasible.

o Undertake a detailed assessment to confirm the accommodation within the

Campus Living Villages (CLV) portfolio that requires refurbishment.

Schedule this refurbishment to occur as funds are available from the

refurbishment fund that CLV contributes to annually.

o Technology – see below.

4. Technology

o All new accommodation to be wireless throughout.

o Provide wireless internet access across the CLV managed portfolio within

five years - by academic year 2019.

Page 9 of 65

5. Monitor and measure

o Commence an annual survey of hall residents, consistent across all halls.

Survey to include an assessment of pastoral care, catering, technology,

facilities and student experience.

o Support the continuation of the UCSA annual student accommodation

report. Report to be refined to clearly identify UC hall residents.

The approach outlined above is predicated on UC’s forecasts of the student population

(EFTS) over the next ten years. The forecasts will either be exceeded or not met.

Should the increase or decrease in EFTS be such that more or less student

accommodation is needed, the approach could be revised as follows:

EFTS Numbers Exceeded

1. Consider further development at Dovedale campus for non first year students.

Low-rise housing can be constructed relatively quickly if site and consenting can

be addressed.

2. Expand Sonoda Hall on the adjacent tennis court for post-graduate and senior

student housing if this is the cohort demonstrating further demand. Low-rise

housing can be constructed relatively quickly if site and consenting issues have

been previously considered.

EFTS Numbers Not Met

1. Do not proceed with any of the independent hall options

2. Exit Innes Road and other leased premises as leases allow

3. Accommodation developed for post-graduate students could be used for

undergraduate students if flexibility in design allows.

1.1 IMPLEMENTATION

Implementation will need to remain fluid as commercial negotiations, consenting,

construction contracts, management arrangements, and funding options are all

complex and subject to change. The implementation approach will need to be

amended as appropriate over time.

Page 10 of 652.0 Introduction

2.1 THE UNIVERSITY OF CANTERBURY

UC is not described in detail as it should be well known to the target audience.

We note the following key metrics as at 31 July 2013:

+ Student headcount = 14,872 (13,238 domestic, 1,634 international)

+ Total EFTS = 12,180 (10,119 undergraduate (83%), 2,061 postgraduate (17%))

+ Land area = 87 hectares

In the months following the earthquake, the University lost 25% of its first year students

and 8% of continuing students. The number of international students, who pay

significantly higher fees and are a major source of revenue, dropped by 30%. By 2013,

the University had lost 22% of its students.

UC considers it is experiencing a significant increase in demand for student

accommodation in 2014, as measured by3

+ Applications for places in halls of residence have increased 31%, from 1,534

applications in 2012 to 2,012 applications in 2013 (for accommodation in 2014)

+ Applications from domestic students are up 15%, and for international students

are up 61% when compared to 2012

+ Study Abroad numbers have recovered to pre-earthquake levels

+ Campus Living Villages (CLV) has approximately 100 Christchurch Polytech

Institute of Technology (CPIT) and Lincoln students seeking accommodation.

The UC Investment Plan 2013 – 2015 provides the following summary of the UC

strategy.

3

As at October 2013. Project Brief.

Page 11 of 65Figure 1: UC Strategy

While UC strategy details a clear focus on research and postgraduate students, UC

has a medium term goal of recovering first year student EFTS to pre-earthquake levels.

UC has recently concluded an agreement with Navitas, an internationally recognised

education provider, to develop New Zealand’s first Affiliated College at the UC campus.

This college provides intensive teaching for specified first-year programmes to

international students, with successful completion allowing entry into second-year

courses at UC4. Navitas students are full fee-paying.

The management of student accommodation at UC has been predominately

outsourced, with CLV as a key partner managing 77% of all beds offered by UC. The

remaining 23% comprises three independent halls.

4

UC Investment Plan 2013 – 2015, 7 September 2012.

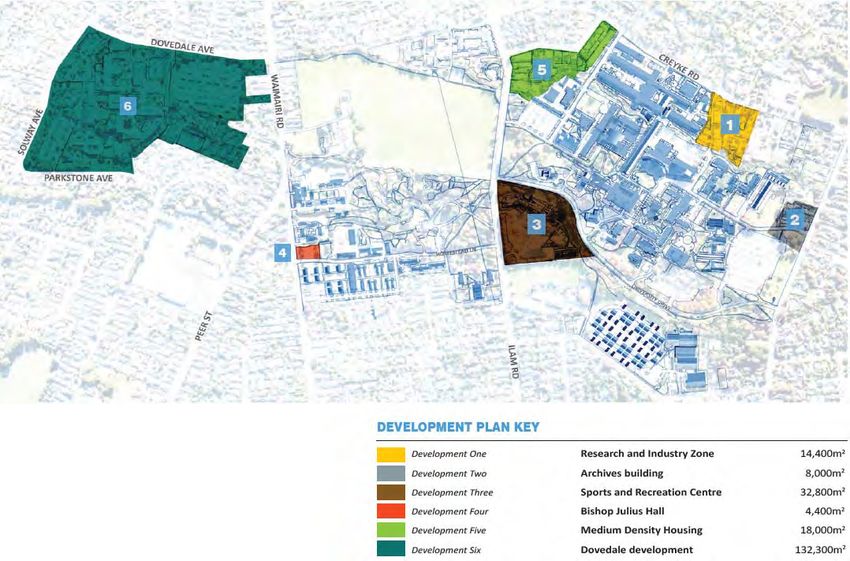

Page 12 of 653.0 Student Accommodation at UC

UC currently has access to approximately 1,950 student accommodation beds. It has

also secured additional beds for the 2014 year as Christchurch wide demand is

impacting on students’ ability to secure affordable accommodation.

This section provides a review of UC’s existing stock, and also provides a brief

summary of stock under consideration or secured for 2014.

UC is also considering progressing plans for a new student accommodation hall at

Dovedale Avenue, near the Sonoda accommodation facility. It is possible that this

development would be funded and managed by CLV.

The following figure demonstrates the location of existing student accommodation halls

at UC.

Figure 2: Student Accommodation at UC

3.1 REVIEW OF EXISTING STOCK

The following table demonstrates the current student accommodation halls offering at

UC.

Page 13 of 65Table 4: Existing Student Accommodation at UC

Single One Semester Annual Fees

Hall Type Primary User Meals $ / week**

Rooms Applications (2013)*

Bishop Julius Hall Dormitory 1st year 109 3 per day No $14,340 $299

Independent Halls

(some 2nd year)

College House Dormitory 1st year and 2nd 152 3 per day No $15,800 $329

year

Rochester and Dormitory 1st year 178 3 per day No $13,650 $284

Rutherford Hall

University Hall (Retro) Dormitory 1st year 296 3 per day Yes (pending $11,600 $242

availability)

UC Accommodation Student Village

University Hall (Ritz) Dormitory and 1st year 259 3 per day Yes (pending $13,600 $283

Apartment availability)

Sonoda Christchurch Apartment 2nd year and older, 110 Meal plan Yes (pending $8,880 $185

Campus International available availability)

Ilam Apartments Apartment 2nd year and older, 144 Meal plan Yes (pending $8,880 $185

(Manuka: 6 bedrooms) International available availability)

Ilam Apartments Apartment 2nd year and older, 683 Meal plan Yes (pending $8,880 $185

(Kowhai: 6 bedrooms; International available availability)

Hinau: 3, 4, 5 bedrooms)

Ilam Apartments Apartment 2nd year and older, 18 Meal plan Yes (pending $10,560 $220

(Hinau: 2 bedrooms) International available availability)

TOTAL 1,949

Standard contract length = Feb - Nov with no vacation fee***.

* Reviewed annually.

** Based on a 48 week academic year. Figures provided for comparative purposes only.

*** A vacation fee is the fee charged to stay in your hall during the term and semester breaks. Meals are not provided during this time

and all students are requred to self-cater.

Source: UC Accommodation Office

The following section provides a brief overview of the existing UC halls of

accommodation.

Page 14 of 65Bishop Julius Hall

Bed Style: Dorm Style

Number of Beds: 109

Catered: Yes

Development Opportunity: 60 – 120 beds

Bishop Julius Hall (BJH) is independently managed by “Bishop Julius Hall” and

provides 109 fully furnished single bedrooms in three separate accommodation blocks.

It is fully catered.

BJH provides both wireless and cabled internet access, and a telephone to each

bedroom. Wireless internet access is also provided to a range of common areas.

Common facilities include a music room, computer suite, TV room and general

common rooms. These spaces are all in average condition.

One building is currently being strengthened to 67% of New Building Standard (NBS).

The BJH site could accommodate an additional 60 to 120 beds; however the

management board’s preference is for circa 70 beds. Wilkie & Bruce Architects has

provided a scheme plan for additional beds. Further development of the site would

leverage off the existing infrastructure.

UC is supporting the development of this site by providing BJH with independent

technical advice and contacts.

Page 15 of 65College House

Bed Style: Dorm Style

Number of Beds: 152

Catered: Yes

Development Opportunity: circa 48 beds

College House is independently owned and managed by “College House”, and is New

Zealand’s oldest and “most traditional college”. It was founded in 1850.

The hall provides 152 single bedrooms in ten separate houses, and is fully catered.

Residents are a mix of first year students (circa 60%) and second year students (40%).

The buildings were predominantly constructed around 1966; with another two being

constructed in 1990. The condition is generally reflective of the buildings’ age although

interiors appear to have been upgraded over time, as required.

Both wired and wireless data connection is available throughout the facility.

The buildings are three-level and walk-up; no lifts are provided. The Chapel is currently

closed due to structural concerns.

Bedrooms are typically 12 – 13m2 which is generous by modern standards.

As a result of the Christchurch earthquakes, the central dining hall is currently

accommodated in a marquee. A new main block including new House with

Page 16 of 65accommodation for 15 students (new total = 159 students) and a new dining hall for

seating 200 will be completed in time for the 2015 academic year.

College House site could accommodate a total of circa 200 beds, an increase of 48

beds. Further development of the site would leverage off the existing infrastructure and

the new (to be constructed) 200 seat dining hall. Modern dining halls often have

student to seating ratio of 2:1.

Further development at College House may be complicated due to possible

encroachment onto the adjacent heritage garden.

Page 17 of 65Rochester and Rutherford Hall

Bed Style: Single bedrooms + Motel Units

Number of Beds: 178

Catered: Yes

Development Opportunity: UC land adjacent.

Rochester and Rutherford Hall is independently managed by “Rochester and

Rutherford Hall”.

The Hall provides 178 single bedrooms for predominantly first-year students. This hall

also provides two motel units for parents visiting residents.

The bedrooms are dated but are being progressively upgraded. Wireless data

connection is provided to all bedroom and common areas.

Catering is provided by Alliance Catering.

There is land adjacent to Rochester and Rutherford Hall that could be used to expand

the hall however management has advised UC that it would like to retain the hall size

at 178 beds.

Page 18 of 65University Hall (Retro & Ritz)

Bed Style: Dorm Style

Number of Beds: 550

Catered: Yes

Development Opportunity: 150 beds

University Hall is managed by CLV and provides 550 single bedrooms. The halls are

fully catered, and from 2014 CLV will be managing catering in-house, having employed

its own catering staff.

The facility comprises an older hall – The Retro that was originally built to house

Commonwealth Games athletes in 1974, and The Ritz, a facility built in the 1990’s.

The Retro, being the older facility is somewhat dated. Whilst some refurbishment

should be considered (bathrooms, carpets and wall linings), the annual rental at the

Retro is $2,000 per annum less than the nearby Ritz due to the lower quality facility.

We are advised (by CLV) that the lower price point ensures strong demand for the

Retro.

The Ritz provides more modern dorm style rooms and apartments with a shared

kitchen (up to six bedrooms per kitchen). Previously self-catered, we understand that

from 2014 a meal plan is mandatory.

Page 19 of 65The condition of The Ritz accommodation is acceptable, and comparable to similar

accommodation at other New Zealand universities.

Cabled data connection is available in the bedrooms and wireless is provided to

common areas.

University Hall benefits from The Hub, a social hall, library and computer lab facility.

Wireless internet access is provided to this area.

Page 20 of 65Sonoda Apartments

Bed Style: Apartment Style

Number of Beds: 140

Catered: Optional meal plan available

Development Opportunity: Tennis courts are being considered for

further development

UC is an academic partner university to Sonoda Women’s University in Japan. Sonoda

Apartments are a group of Japanese inspired buildings and landscaped grounds.

Sonoda is managed by CLV and is part of UC Accommodation Student Village. This

facility is approximately a 10 minute walk from the main campus.

Page 21 of 65The hall was opened in 1993 and provides 140 beds of which 110 beds are available

for general release to UC students. The balance of 30 beds are held for visiting

academics, postgraduate students and short-term student groups from Sonoda

Women’s University.

The apartments are arranged in a series of five-bedroom self-catered apartments and

are provided to residents fully furnished. Kitchens include a hob and a convection

microwave, but no oven.

A central common room and computer room is provided and these are furnished as

would be expected of a student accommodation facility. Tennis and netball courts are

adjacent to the hall.

A central laundry (coin operated) and car parking facilities are provided.

Cabled data connection is available in the bedrooms and wireless is provided to

common areas.

Page 22 of 65Ilam Apartments

Bed Style: Apartment Style

Number of Beds: 845

Catered: Optional meal plan available

Development Opportunity: Up to 150 beds

Ilam Apartments comprise 845 bedrooms in a mix of 2, 3, 4, 5 and 6 bedroom

apartments. The original part of Ilam Apartments was constructed in 1972 for the 1974

Commonwealth Games. Between 1999 and 2007 a further 542 rooms were added.

Whilst full kitchens are provided in each of the apartments, meal plans are available at

the nearby University Hall.

Cabled data connection is available in the bedrooms and wireless is provided to

common areas.

Interiors of the new apartments are in good condition however interiors of some of the

older units, such as Manuka are in poor condition and in need of upgrade.

Ilam Apartments benefit from a large common room.

Page 23 of 65Existing Stock - Capital Expenditure

UC has no forecast capital commitments for its Halls of Residence.

The independent halls (Bishop Julius, College Hall and Rochester & Rutherford) do not

currently receive any capital expenditure funding from UC, and CLV has built its own

residences (which UC has a reversionary interest in). CLV also leases some

accommodation from UC, however CLV meets all capital expenditure requirements5.

UC does provide support services in some areas to both CLV and Rochester &

Rutherford which covers grounds and controls technicians and emergency support for

most trades. CLV also ‘piggy-backs’ on UC’s contracts for bulk electricity purchases

and MTHW (medium temperature hot water) from the central boiler plant6.

3.2 2014 - STOCK UNDER CONSIDERATION OR SECURED

Innes Road – leased

Innes Road provides 80 beds. UC has leased this facility for a term of six years (no

rights of renewal were available).

The facility is approximately seven kilometres from the campus.

Waimairi Village – owned

Waimairi Village is a new on-campus complex. Hawkins Construction was engaged in

December 2013 to construct this village. Waimairi Village provides 15 x 4-bedroom

houses (60 beds) on UC land next to College House.

These houses will be available for occupation by late February 2014, and can be

relocated at a later date.

The business case for these houses assumes a student mix of 50% international and

50% domestic, a 48 week per year “in use” period and a 95% occupancy rate.

Head leases and Owned Property

UC has added the following accommodation to its student accommodation portfolio for

2014

5

Adrian Hayes – Financial Controller

6

Rob Oudshoorn – Group Manager Engineering

Page 24 of 65Table 5: Head Leased and Owned Accommodation

Address Beds Bed Type Comments

32 Jennifer St 7 5 x Dbl Head lease property

2 x Single

27 Newnham 18 15 x Dbl Head lease property

Terrace 3 x Single

63 Parkstone 8 6 x Dbl Head lease property

Cres 2 x Single

75 Clyde Rd 5 2 x Dbl UC owned property

3 x Single

39 Creyke Rd 6 2 x Dbl UC owned property

4 x Single

118 Ilam Rd 4 4 x Dbl UC owned property

TOTAL 48

3.3 2015 - STOCK UNDER CONSIDERATION

Dovedale and Ilam

UC is currently considering two on-campus development options with CLV.

Key points include:

+ Circa 250 beds at South-west Dovedale

+ Up to 150 beds at Ilam Stage 2 (we understand development on this site has

been re-assessed to circa 80 beds)

+ Could open in semester 1, 2015 (as advised on 10 December 2013, but unlikely

as at the date of this report)

+ 35 year build-own-operate-transfer (“BOOT”) arrangement with CLV managing

the halls.

Independent Halls

The independent halls are (as the name suggests) independent. UC acknowledges

that it cannot direct these halls with respect to further development. The independent

halls and UC do however have strong working relationships and work closely to meet

each parties respective objectives.

Page 25 of 65As discussed above, the independent halls have the capacity to add 100+ beds as

follows:

+ BJH - circa 70 beds

+ College House - circa 30 beds

UC is already providing technical advice to BJH and BJH has provided a scheme plan

for additional beds. There is an opportunity to extend these discussions to College

House and Rochester & Rutherford.

Other Options

UC continues to explore other lease options for 2014 and beyond.

Page 26 of 654.0 UC Demographics and Forecast

for Student Accommodation

4.1 UC DEMOGRAPHIC FORECAST 2014 - 2023

UC has forecast student numbers out to 2023. This forecast is presented in the

following table.

Table 6: Actual and Forecast Student Numbers, 2012 – 2023

Student Type Actual Forecast

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Domestic - Undergraduate (local) 5,785 5,394 5,344 5,292 5,419 5,644 5,894 6,120 6,302 6,449 6,574 6,694

Domestic - Undergraduate (non local) 4,471 4,013 4,013 4,055 4,204 4,400 4,588 4,750 4,877 4,978 5,063 5,147

Domestic - Postgraduate 2,078 1,979 1,968 2,011 2,074 2,128 2,190 2,242 2,295 2,345 2,394 2,441

Sub-total domestic 12,334 11,386 11,325 11,357 11,696 12,172 12,672 13,112 13,474 13,773 14,030 14,283

Full Fee - Undergraduate (Navitas) - - - 80 194 304 398 498 600 703 805 907

Full Fee - Undergraduate (non Navitas) 770 728 690 694 732 788 855 939 1,038 1,153 1,288 1,391

Full Fee - Postgraduate 67 68 81 84 88 92 98 104 111 119 128 132

Sub-total full fee 837 796 770 858 1,015 1,184 1,351 1,541 1,749 1,975 2,220 2,431

TOTAL UC 13,171 12,182 12,095 12,216 12,711 13,356 14,023 14,653 15,223 15,748 16,250 16,713

Source: 10 Year Forecast Model, UC Financial Services

The data from Table 6 has been indexed (December 2012 = 100) and is displayed in

the following figure.

Page 27 of 65Figure 3: Forecast Growth in Total EFTS by Type

Source: UC data

Full Fee EFTS demonstrate the highest forecast growth, increasing from 6% of total

EFTS in 2012 to 16% in 2023. The forecast for this cohort demonstrates annual

average growth of 11.2%, compared to 2.2% for total EFTS.

Full Fee EFTS is categorised by UC as: non-degree, undergraduate, postgraduate

taught, or postgraduate research. The following figure demonstrates the forecast

growth for these four categories. The statistics are indexed to 2010, demonstrating

historic (pre-earthquake) EFTS at UC.

Page 28 of 65Figure 4: Full Fee EFTS (Index 2010 = 100)

Source: UC Financial Services

Figure 4 demonstrates that for Full Fee EFTS the Undergraduate and Postgraduate

Research categories are forecast to exceed 2010 levels during the forecast period to

2023. The forecast increase for these two groups is as follows:

+ Undergraduate – an increase of 1,539 EFTS (963 in 2010 to 2,502 in 2023).

Undergraduate EFTS is not forecast to return to the year 2010 level until 2017.

+ Postgraduate Research – an increase of 20 EFTS (27 in 2010 to 47 in 2023).

Postgraduate Research EFTS is not forecast to return to the year 2010 level until

2015.

The following table demonstrates the forecast for Full Fee students (EFTS) to 2023.

Table 7: Full Fee EFTS by Type

Forecast

Type 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Undergrad - Navitas - - - 80 194 304 398 498 600 703 805 907

Undergrad - Non Navitas 770 728 690 694 732 788 855 939 1,038 1,153 1,288 1,391

Postgraduate 67 68 81 84 88 92 98 104 111 119 128 132

TOTAL FULL FEE EFTS 837 796 770 858 1,015 1,184 1,351 1,541 1,749 1,975 2,220 2,431

Source: 10 Year Forecast Model, UC Financial Services

Page 29 of 65The following table demonstrates forecasts for Navitas EFTS at UC.

Table 8: Navitas EFTS Forecast

Forecast

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Navitas ‐ First Yr - - - 80 122 162 210 259 308 357 406 454

Navitas ‐ Non First Yr - - - - 72 142 188 239 292 346 399 453

Navitas ‐ Total - - - 80 194 304 398 498 600 703 805 907

Source: 10 Year Forecast Model, UC Financial Services

Table 8 above demonstrates that a minimum of 50% of Navitas students will be first-

year students.

With respect to international students UC guarantees an offer of accommodation to any

international student who applies for a full academic year (48-week contract) in a self-

catered apartment by 1 December of the prior year. This offer is reviewed annually by

UC. If it is going to continue to provide this guarantee it is likely UC will need to provide

additional student accommodation suitable to this cohort.

The following table presents the EFTS forecast for all post-graduate students.

Table 9: Total Post-graduate EFTS Forecast

Total post-graduate EFTS in 2013 were near pre-earthquake numbers (down 31

EFTS). Table 9 demonstrates strong growth in EFTS over the strategy period.

Page 30 of 65The following table demonstrates the compilation of students in the 2012 year. We

understand this to be the most up to date data available.

Table 10: Demographic of 2012 Students

Fee Type Gender Age

< 18 18‐19 20‐24 25‐34 35‐44 45‐54 55‐64 Over 64 TOTAL

Domestic Female 44 1,506 3,006 929 513 297 84 6 6,384

Male 54 1,605 2,966 894 260 122 35 14 5,950

Full Fee Female 7 64 293 41 9 1 1 ‐ 417

Male 5 67 264 75 9 2 ‐ ‐ 421

TOTAL 111 3,241 6,528 1,940 790 422 121 20 13,171

Age Group % 1% 25% 50% 15% 6% 3% 1% 0% 100%

Female 47% 48% 51% 50% 66% 71% 71% 30% 52%

Male 53% 52% 49% 50% 34% 29% 29% 70% 48%

Source: Student Accommodation Strategy Project Brief

There is little differentiation in gender split in students under the age of 35, thus no

impact is forecast for the student accommodation strategy.

The following figure demonstrates the age group spread at UC in 2012.

Figure 5: Age Group Spread, 2012

Source: Student Accommodation Strategy Project Brief

Page 31 of 65In 2012, 75% of UC’s students were less than 25 years of age.

New Zealand universities have historically focused on providing accommodation to

first-year students, thus typically younger students who have preferred fully catered

accommodation with a high level of pastoral care.

This trend is changing with New Zealand universities starting to adopt the international

model of providing some accommodation to senior students. The most recent New

Zealand example is Carlaw Student Village at The University of Auckland.

The following figure demonstrates total applications received by UC for accommodation

as at 1 October each year between 2008 and 2013 (for the 2014 academic year).

Figure 6: Applications for Student Accommodation (as at 1 October)

Source: Student Services and Communications

Applications for accommodation in October 2013 (for 2014) were 11% higher than

2010, and have grown significantly when compared to 2011 and 2012. Half of all UC

students are from outside Christchurch.

4.2 FORECAST FOR STUDENT ACCOMMODATION

Student accommodation is typically designed to cater for specific groups of students.

Following is a list of accommodation types.

Page 32 of 65+ Domestic under-graduate first-year (local / non local)

+ Domestic under-graduate non first year (local / non local)

+ Domestic post-graduate (local / non local)

+ International undergraduate

+ International post-graduate

+ Family

Within these groups are various sub-groups. Accessible housing, for example, may be

specifically addressed.

Masters and post-graduate student intakes are not consistent with the under-graduate

year. There are multiple Masters intakes, and post-graduate students have the option

of starting at any time.

Providing accommodation mid-year can be difficult financially due to an accompanying

vacancy period pre-occupation.

UC is a Navitas partner university (from 2014), thus will also be accommodating

international undergraduate students. This group should be specifically considered as

the students are both first-year and international. International students often prefer to

integrate into a hall with local (NZ) residents rather than an internationally focused hall.

The Navitas academic year is longer than UC’s standard year.

UC also accommodates a number of students attending block courses and

conferences. Prior to the earthquakes approximately 400 Study Abroad single

semester students attended UC.

Current Demand for Student Accommodation

At present UC does not comprehensively survey students about their accommodation

experiences and requirements, although the halls undertake their own surveys. UCSA

has undertaken an annual survey of student accommodation experiences in 2012 and

2013. The respondents are a cross-section of the UC student body thus include

students in private accommodation.

A comprehensive survey of students, including both UC halls residents and those in

the private market would, over time, provide UC with a valuable benchmark to ensure it

is meeting the needs of its students.

Page 33 of 65International Students

More than 78,000 international students were approved to study in New Zealand in the

year to October 2013. While slightly down from the 80,743 approval over the same

period in 2012, the 2013 approvals are 9,500 higher than the 2011-2012 year. China

provided 24,178, or 31% of international students in the 2013 year.

The Government has announced a package of new initiatives to encourage further

growth in New Zealand's international education sector.

Changes will make it easier for some international students to work during their studies

and allow streamlined visa processing in partnership with selected high quality

education providers.

Under the changes, students studying full-time will be allowed to work during all their

scheduled course breaks (rather than just summer); doctoral and research masters

students will be able to work full-time; and English-language students will be allowed to

work part-time during their study.

UC undertakes the following obligation to provide accommodation to international

students:

+ “The UC Accommodation Student Village (managed by Campus Living Villages

NZ Ltd) guarantees an offer of place to any international student who applies for

a full academic year (48-week contract) in a self-catered apartment by 1

December. This offer is reviewed annually in July by the Accommodation Office

and CLV. The only other University to guarantee a place for international

students is Lincoln University with a due date of 10 December. International

students are not required to provide a reference as part of their accommodation

application.”

Source: UC Accommodation Office

International students often demonstrate sensitivity to accommodation pricing at a

lower price-point than local students. UC undertook a postgraduate survey of student

experience in May 2013. A summary of anecdotal evidence from that survey is

included as Appendix 1.

Another issue often raised by international students is the poor quality of insulation in

New Zealand housing compared to overseas. Purpose-built student accommodation

can address this issue.

UC is a signatory to the Ministry of Education’s Code of Practice for the Pastoral Care

of International Students. UC needs to ensure that its accommodation facilities comply

with the requirements of this code of practice.

Page 34 of 65With respect to applications from international students at UC the following graph

provides a comparison of applications received, as at 30 January, in 2013 and 2014.

Figure 7: International Applications for Accommodation at UC (as at 30 January)

Source: UC Accommodation Office

Figure 7 shows an increase of 41 applications, or 10% in 2014 when compared to

2013. This improvement most likely reflects a return to Christchurch post-earthquake.

Anecdotally, international students expect universities to provide accommodation

inclusive of all furniture. If the accommodation is privately owned they tend to expect

the university to manage, or assist in managing, the application process. This

expectation is often not understood by New Zealand universities and leads to

dissatisfied international students shortly after their arrival in New Zealand.

Page 35 of 65Options for Additional International Student Accommodation

International students have a preference for university provided accommodation with

the following key attributes:

+ Stress-free application process

+ all furniture provided

+ Utilities including wireless internet included in rental price

+ Integration with New Zealand students

+ A strong sense of community

+ Low cost – more relevant to some groups who receive funding for tuition fees but

not accommodation

+ Occasionally shared rooms – can address cost issues

+ Self-catering option – can address cost issues and also diet requirements

Prior to any new development at UC that is geared to cater to the international market

(particularly Navitas students) a comprehensive study of the needs of the target groups

should be undertaken to confirm the above accommodation attributes and other

preferences.

Increasing the Number of Shared Rooms

Providing more shared room accommodation is a possibility for providing more

affordable accommodation. Larger shared rooms are not particularly flexible for a

change of user (i.e. single room) and can lead to other design issues such as

compliance with fire regulations and sizing of dining accommodation and common

areas.

International students are known to lease apartments and share bedrooms with friends.

With respect to shared rooms at UC accommodation, three issues need to be

considered:

1. Building compliance; particularly maximum occupants for fire design

2. General marketability of rooms

3. Change of use at a later date (to single / double rooms, catering capacity, common

area spaces, retaining flexibility)

4. Shared accommodation is often suitable in existing residential housing such as can

be found in the private market in suburbs proximate to UC.

Page 36 of 65The ‘Total Package’ Option and Accommodation Scholarships

Providing suitably priced accommodation is an issue faced by all New Zealand

universities. More expensive building costs and property prices in New Zealand

compared too many other countries lead to comparatively high rental costs.

Some international groups have difficulty paying the weekly accommodation fees

required at New Zealand universities. Often home-country financial assistance is

available for tuition fees, but not accommodation.

There is an opportunity to re-package UC’s offering to groups that include tuition and

accommodation as a single package.

Providing accommodation scholarships is also an option. This option clearly delineates

tuition fees from accommodation fees.

Page 37 of 655.0 Christchurch Post Earthquake

Accommodation Environment

5.1 ON-CAMPUS

In December 2011, UC had 1,800 fewer domestic students and 400 fewer full fee-

paying international students compared with 2010. In October 2013, Government

announced a cash grant of up to $260m to UC for the purpose of a new science centre

(estimated at $212m) and to expand and upgrade engineering facilities (estimated at

$145m). The total cost of these two projects is circa of $357m. UC is expected to fund

the $100m difference.

With respect to student accommodation, there has been only minor reduction in the

number of on-campus beds due to structural remediation work.

Following the Christchurch earthquakes, seismic strength of buildings has become

topical, particularly so for educational institutions, and most importantly with respect to

student accommodation. We are aware of institutions setting minimum requirements in

the range of 80% to 100% of NBS for student accommodation facilities, and also

undertaking building stair reviews with respect to the MBIE Practice Advisory 13 (where

relevant) which addresses safety of stairs.

UC has a policy of upgrading buildings to a minimum of 67% of New Building Standard

where economically and physically feasible.

One building at Bishop Julius Hall is currently being upgraded to 67% NBS.

UC may wish to provide some guidance or technical assistance to its accommodation

providers as and when upgrade works are undertaken at the various halls.

The UC Students’ Association has commissioned a “Student Accommodation

Research Report” in both 2012 and 2013. These two reports are the results of surveys

of student experiences with finding accommodation in the post-earthquake rental

market. 1,608 students were surveyed in 2012 and 844 in 2013. This equates to 12%

and 7% of the total student population (EFTS) respectively.

Page 38 of 65The figure below demonstrates on a scale of 0 to 10 how difficult it was for students to

find suitable rental accommodation in 2012 and 2013.

Figure 8: How easy was it to find suitable accommodation in 2012 and 2013

Source: UCSA

Figure 8 demonstrates that in both 2012 and 2013 63% of respondents recorded a

response of 5 or less, stating that finding suitable accommodation was somewhere

between a “piece of cake” and “same as always”.

As the survey respondents may not have been seeking accommodation in the pre-

earthquake years it is impossible to ascertain relativity i.e. the “same as always” may

still be difficult.

The two main responses as to difficulty were:

1. Lack of accommodation available (2012 = 31%, 2013 = 45%)

2. High rent / cost / expensive (2012 = 31%, 2013 = 43%)

The survey noted that in 2012 “Nearly half of flatting students pay between $101 -

$125” (average rental price per rooms). The 2013 survey noted “Around half of

students paid between $101 and $125 per week in rent”.

Page 39 of 65In 2012 35% of students paid $100 or less per week in rental, and in 2013 17% paid

$100 or less indicating the average rental has increased between 2012 and 2013.

The 2013 survey also identified the following key messages:

+ “For most students, finding accommodation in 2013 was no more difficult than in

previous years

+ At the same time a significant minority of students (38%) experienced more

difficulty finding accommodation in 2013 than they had previously

+ 80% of students lived within 2 kilometres of the University

+ 17% of students who found finding accommodation more difficult than in previous

years noted that there was a lack of housing close to the University

+ Students found the lack of accommodation available and the high cost of renting

to be factors that caused the most difficulty in finding rental accommodation in

2013.”

Unfortunately only two years of surveying do not allow issues to be monitored over

time.

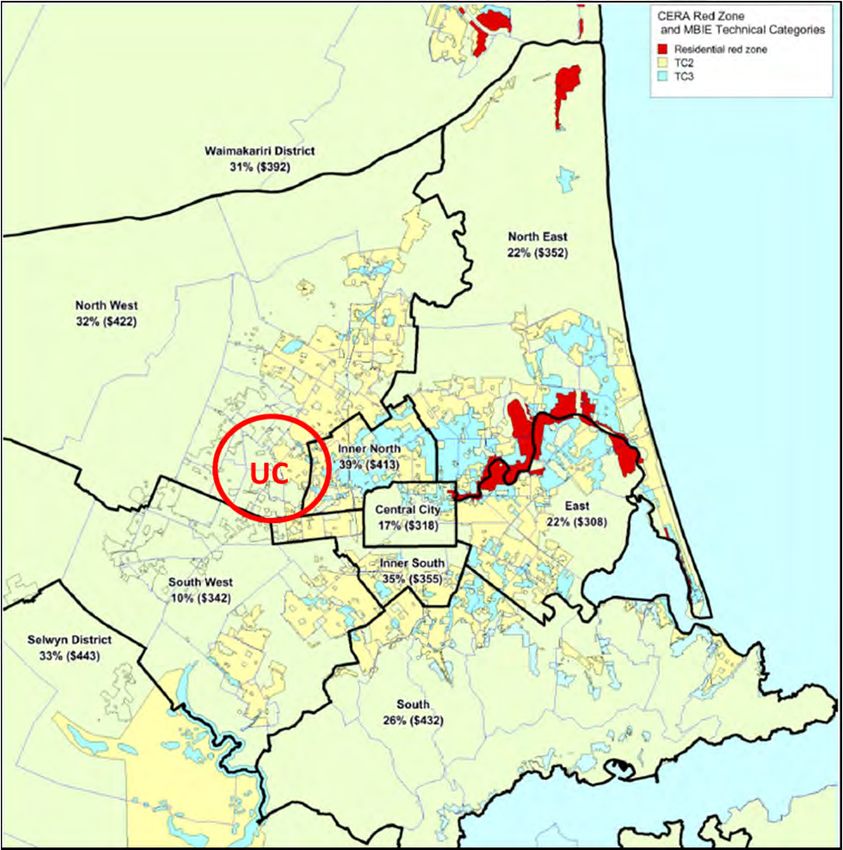

5.2 OFF-CAMPUS - HOUSING PRESSURES IN CHRISTCHURCH

CERA estimates 25,000 houses were lost in the earthquakes of which 7,860 are in the

‘red zone’. Preliminary analysis indicates approximately 7,000 houses have been re-

built however a portion of these will be ‘business as usual’; natural construction growth

that would have occurred.

The ‘red zone’ predominantly lies to the east of the city centre. Some of these ‘red

zone’ suburbs historically provided lower cost housing when compared to the western

suburbs, including those proximate to UC. Residents from the ‘red zone’ suburbs will

now be competing for accommodation elsewhere in the city, including those suburbs

proximate to UC. This will create additional demand pressure.

It has been reported that traditionally 95% of UC students live within a five kilometre

radius of the campus, but now they are living as far away as Halswell (circa 10km).

7,860 houses have been deemed uninhabitable and classified as ‘red zone’. It has also

been estimated that an additional 9,100 properties were uninhabitable due to requiring

major repairs or rebuilds.

After taking into account new houses being built it has been estimated that the total

housing stock has been reduced by a net 11,500 (6.2% of the previous housing stock)

between the fourth quarter of 2010 and the fourth quarter of 2012.

Page 40 of 65Whilst new housing has gone some way to alleviating the housing shortage, students

typically do not occupy new housing.

The number of rentals in the private market held static7 during 2011 and 2012, against

an historic trend of annual growth of circa 1,500 rental properties prior to 2010. Since

the earthquakes, the total number of rental bonds lodged with MBIE has fallen from

20,500 in the year to December 2010 to 16,600 in the year to December 2012 (the

lowest annual number since 1998).

The following figure illustrates the decrease in new rental tenancies between 2010 and

2012 by area based on tenancy bonds lodged in the private market. UC’s approximate

location is highlighted. A decrease in bond lodgements indicates people are staying for

longer periods in rented housing.

Figure 9: Decrease in Number of New Bonds Lodged Between 2010 and 2012

December

Source: MBIE

7

As measured by the number of active tenancy bonds.

Page 41 of 65Appendix 2 illustrates new accommodation lettings (1 May 2013 to 31 October 2013)

and rental values for a range of Christchurch suburbs proximate to UC.

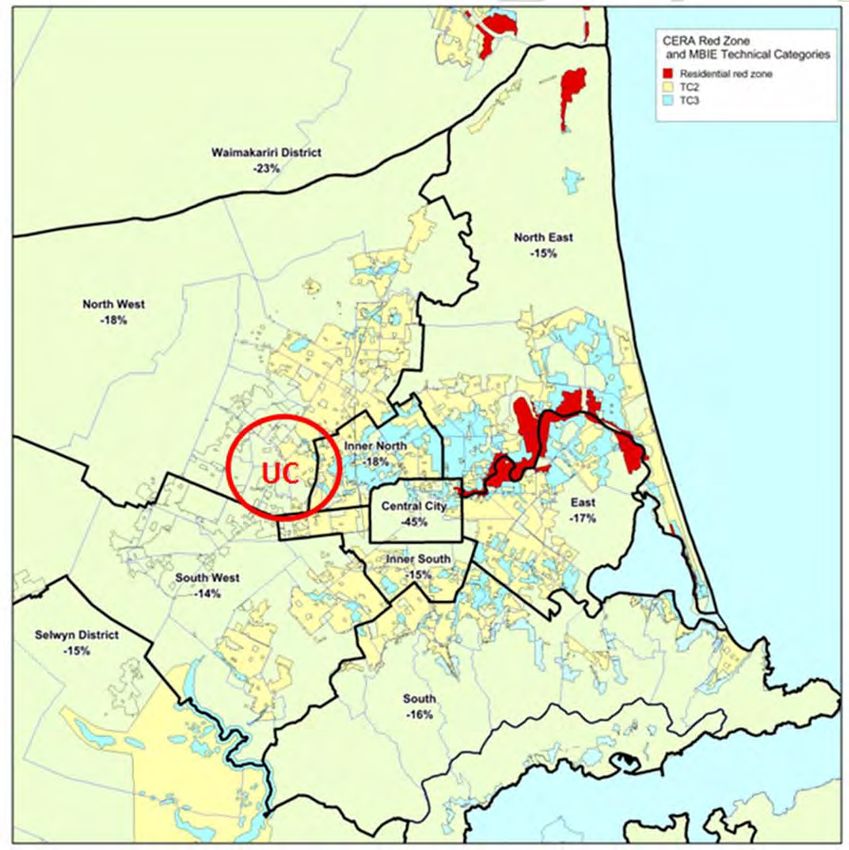

The price for new weekly rentals within the greater Christchurch region has risen faster

than in other New Zealand regions including Auckland since the earthquakes. The

average weekly rental in the greater Christchurch region in the month of February 2013

was $384. This compares to $293 in August 2010, a 31% increase or annual average

increase of 11.40%.

The following figure illustrates the increase in average rentals between the three

months to August 2010 and the three months to February 2013.

Figure 10: Percentage Increase in Average Rental, February 2013 vs August 2010

Source: MBIE

A 2012 MBIE report identifies a significant decline in the availability of low-rent

properties. Pre-earthquake approximately 900 bonds were lodged each month for

Page 42 of 65rentals of less than $300 per week. In the six months to February 2013 the number of

these ‘affordable’ rentals averaged 362 per month, a 60% decrease. Whilst this

analysis is now dated we expect the situation not to have improved.

The report identifies three sources of medium term (2013 – 2016) demand for housing:

1. Increase in residential population growth

Statistics New Zealand has projected that the region’s residential population will

increase to 474,900 by 2016, an increase of 20,200 or 4.4% on its June 2012

estimate. If the greater Christchurch average of 2.5 people per dwelling from the

2006 census is adopted, then an additional 8,100 houses will be required to keep

pace with population growth by 2016.

2. Temporary accommodation for residential repairs and rebuilds

It is difficult to estimate when this demand will peak, however most repair /

rebuild work on residential properties is likely to take place over the next three

years. At the end of June 2012, EQC had repaired 18,000 properties, with about

80,000 or 80% of repairs still to take place. IAG, the biggest insurer in

Christchurch, has stated that it aims to complete its repair / rebuild programme by

the end of 2015.

3. Accommodation of construction workers

It is expected that anywhere between 15,000 and 25,000 construction workers

will arrive in the greater Christchurch region for the rebuild. It is probable that the

majority of them will arrive in 2013 and 2014 for work over the 2013 – 2016

period. In 2012 Westpac estimated that earthquake related building activity would

begin to decline from early 20158 while NZIER forecasts that total construction

activity will peak in 20159. If these forecasts are accurate, then the demand for

accommodation from construction workers will begin to ease after 2016.

In October 2013 Statistics New Zealand released business demography information

that confirmed Canterbury had 4,700 more construction workers in February 2013 than

in February 2012. We are unaware of any more up-to-date information on the arrival of

construction workers.

If the forecasts above are accurate there should be an easing in both demand and

rental growth from around 2016. Based on the Statistics New Zealand information it is

likely that construction activity has been slower to proceed than anticipated in the MBIE

report.

8

Westpac, ‘Rebuilding a city: An update on developments in Canterbury’, 16 August 2012, Figure 5

9

NZIER, New Zealand Trends in Property and Construction, Fourth quarter 2012, Figure 3.

Page 43 of 65Any endeavour by UC to address this 2014 – 2016+ spike in demand and rental costs

for its students would have to be via residential style or low-rise accommodation as any

significant development would unlikely be delivered prior to the start of the 2016

academic year.

Due to the speed with which changes are occurring in the Christchurch residential

market UC should continue to monitor statistical data on a regular basis.

The following organisations are currently monitoring housing in Christchurch:

+ MBIE – various research including the New Zealand Housing and Construction

Quarterly and Quarterly Market Rental survey (via bonds received by the

Department of Building and Housing)

+ Canterbury Development Corporation – various research including its monthly

Economic Snapshot

+ Canterbury Earthquake Recovery Authority (CERA) – various research.

Page 44 of 656.0 Trends in Student Accommodation

Trends in student accommodation can be considered from both an international and

national perspective.

This section briefly discusses international trends in accommodation, then provides a

more detailed analysis of national trends.

6.1 INTERNATIONAL TRENDS

The following trends or issues are common discussion points within the student

accommodation sector internationally.

With respect to construction quality and fundamental building design, it is our

experience that New Zealand is delivering new accommodation facilities at least as

good as overseas universities10.

In the USA we note a desire to house a high percentage of students on-campus, not

just first-year students as has historically been the case in New Zealand.

Millennial / Generation Y Students

The Millennial / Generation Y student was born between 1980 and 2000. Significant

research on the millennial student has been undertaken - the following are their

attributes11:

+ Special – a sense of being vital to the future

+ Sheltered – they expect a residence that is safe

+ Pressured – they want space and opportunities outside the classroom

+ Confident – they want to be challenged, hall programming is important

+ Conventional – value tradition and ritual.

Whilst these attributes may be a generalisation of the Gen-Y student, they do provide

some guidance as to the types of issues that should be considered in the delivery of

student accommodation.

10

We have toured a range of universities in the USA and Australia between 2010 and 2013.

11

Millennial attributes from a presentation at Texas Christian University, June 2010.

Page 45 of 65Living-learning Environments

Living-learning environments have been discussed elsewhere in this report.

+ Living-learning programmes – the definition is elusive, but may include:

o A programme with a clear academic objective

o Residents may share a common academic course

o Formal engagement between accommodation hall and faculty

o Faculty offices and teaching spaces within a residential hall

o Provision of multi-function spaces.

Technology

Technology is driving a range of changes in the learning environment. In recent years,

student accommodation has become an extension of university teaching and learning

spaces. Today’s students are internet ‘natives’ and expect seamless technological

delivery between the university campus and home.

Further development of student accommodation at UC should incorporate modern

technology and leverage the traditional benefits of face-to-face interactions between

student residents and faculty. Accommodation facilities can become a cornerstone of

the campus learning environment and enhance the campus experience at UC.

Technology is discussed elsewhere in this report. Key points include:

+ Today’s student is “hardwired to be wireless”, teaching and learning will occur in

every part of the physical campus environment

+ High bandwidth wired and wireless is a requirement throughout campus

+ Integration with living and learning – multi-function spaces

+ Technology-rich study spaces

+ Printing facilities

+ Gaming rooms.

Page 46 of 65You can also read