US ECONOMIC OUTLOOK What's ahead for the US economy - Gregory Daco Chief US Economist

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

US ECONOMIC OUTLOOK

What’s ahead for the US economy

Gregory Daco

Chief US Economist

gregorydaco@oxfordeconomics.com

Follow us on Twitter

@GregDaco

@OxfordEconomics

Death and hospitalizations reaching record-highs

US: COVID-19 deaths and hospitalizations

Deaths Hospitalizations

New deaths (7-day MA)

3,500 160,000

Currently hospitalized

3,000 140,000

120,000

2,500

100,000

2,000

80,000

1,500

60,000

1,000

40,000

500 20,000

0 0

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb

Source: Oxford Economics/Haver Analytics

1

Vaccine diffusion will be gradual in 2021 2

Moving to a “delicate” recovery phase

US Recovery Tracker was flat in December

Financial

US: Recovery Tracker Mobility

(31-Jan-20 = 100) Production

Employment

Demand

100 Health

Recovery Tracker

80

60

40

20

0

Jan-20 Mar-20 May-20 Jul-20 Sep-20 Nov-20 Jan-21

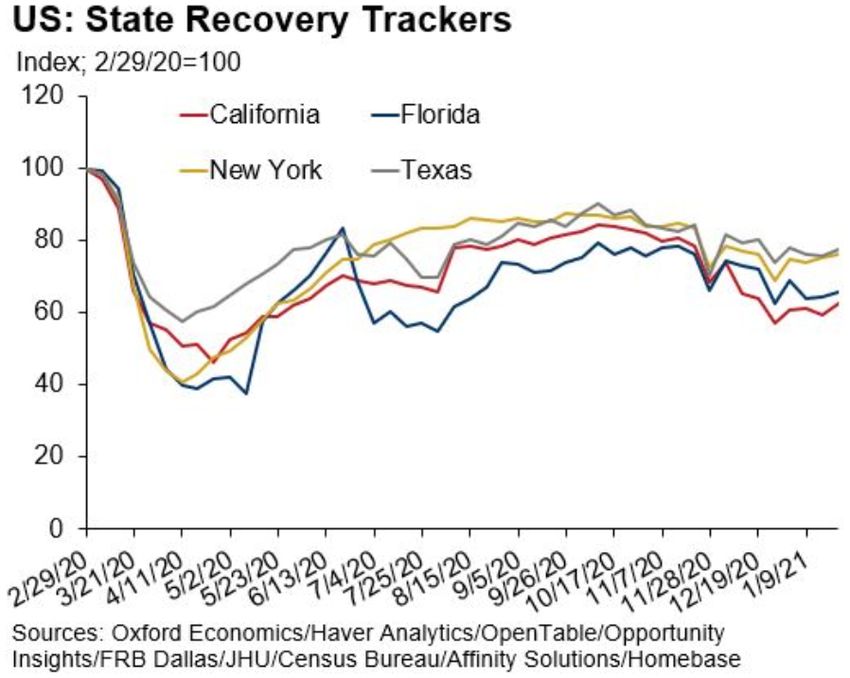

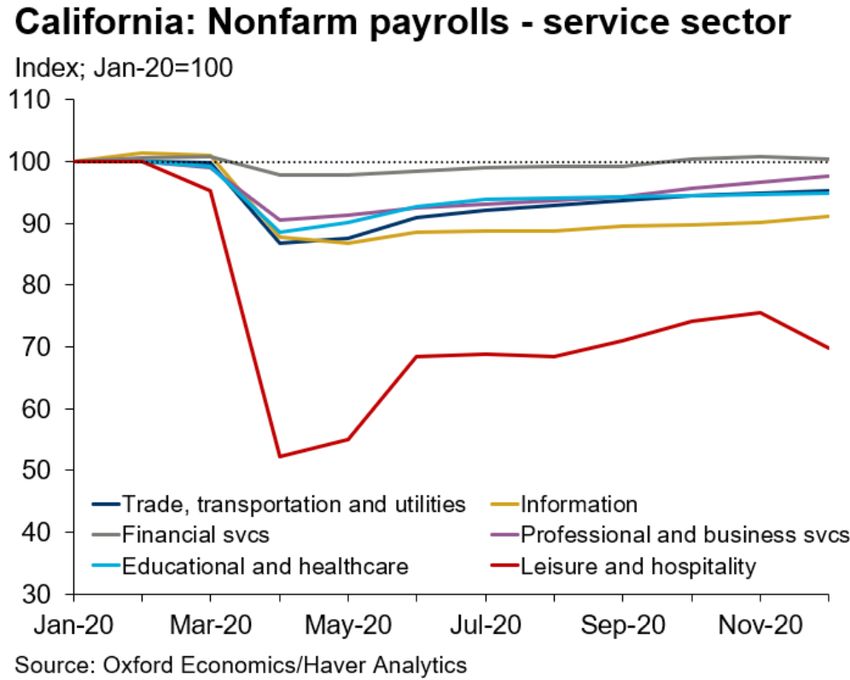

Sources: Oxford EconomicsCalifornia is heating up after cold winter 5

A durable health solution is indispensable 6

Limited US employment momentum at start of 2021 7

A rapid decline in the unemployment rate, but…

US: U3 unemployment rate

%

16 Apr:

14.7%

14

12 10.8%

10.0%

10 9.0%

7.8%

8 7.1%

6.1% 6.3% Dec:

6.7%

6

4

2 Average of 7

prior recessions

0

1960 1970 1980 1990 2000 2010 2020

Source: Oxford Economics/Haver Analytics

8Drop in labor force participation is worrisome 9

Entering a new phase of the recovery

Phase 2: The delicate vaccine rollout phase

GDP Q4 2019 = 100

Phase 1 Phase 2 Phase 3

110

105

Q3*

100

2019Q4 level

Q2*

Q4: Q1*

95 -10.1%

+1.0%

+7.5%

90

85

80

19Q4 20Q1 20Q2 20Q3 20Q4 21Q1 21Q2 21Q3 21Q4 22Q1 22Q2 22Q3 22Q4

Source: Oxford Economics

10Employment should pick up over spring/summer 11

Income support is key to consumer spending

The income paradox is a key feature of the Covid crisis

Household incomes

% q/q in Q2 20202

15

Personal disposable income

10 Compensation of employees

5

0

-5

-10

-15

Canada US Australia Germany France UK Italy

Source : Oxford Economics/Haver Analytics

13Fiscally-stimulated spending driven by low-income families 14

A massive $1.6tn cash stash for households 15

Expecting record-breaking spending this summer 16

With domestic leisure travel leading the rebound

Business and leisure trips Domestic and international trips

Index (2019=100)

Index (2019=100)

120

120

100 106

100 105 108 102

101 100 100 98

100 100 99 96

93

80 90 80 85

85 82

76

60 69

60 66

40 49 40

40 42

20 20 24

0 0

2019 2020 2021 2022 2023 2024 2019 2020 2021 2022 2023 2024

Business Leisure Domestic International

Note: Only domestic trips Source: Tourism Economics

Source: Tourism Economics

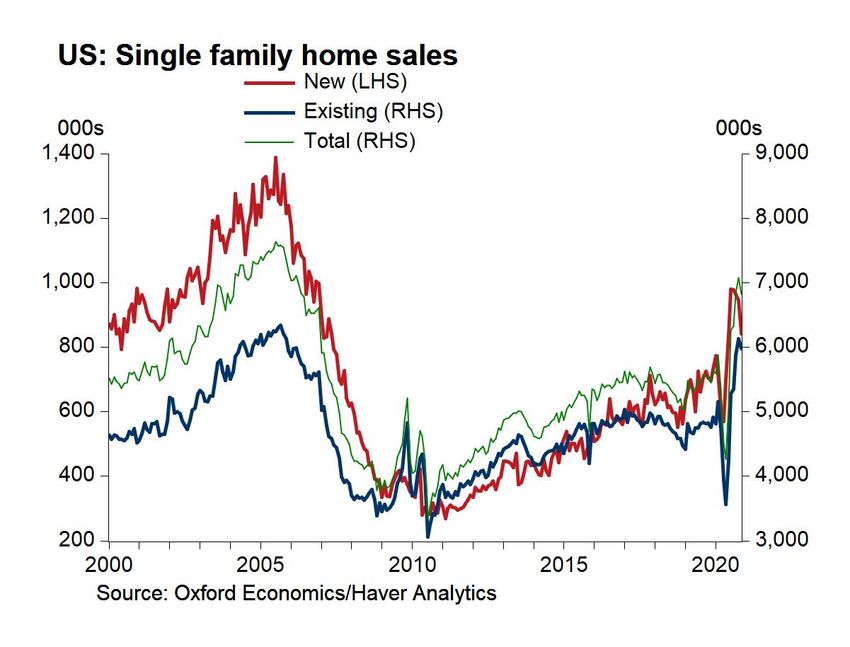

17Strong residential activity

Very strong homes sales and low inventory 19

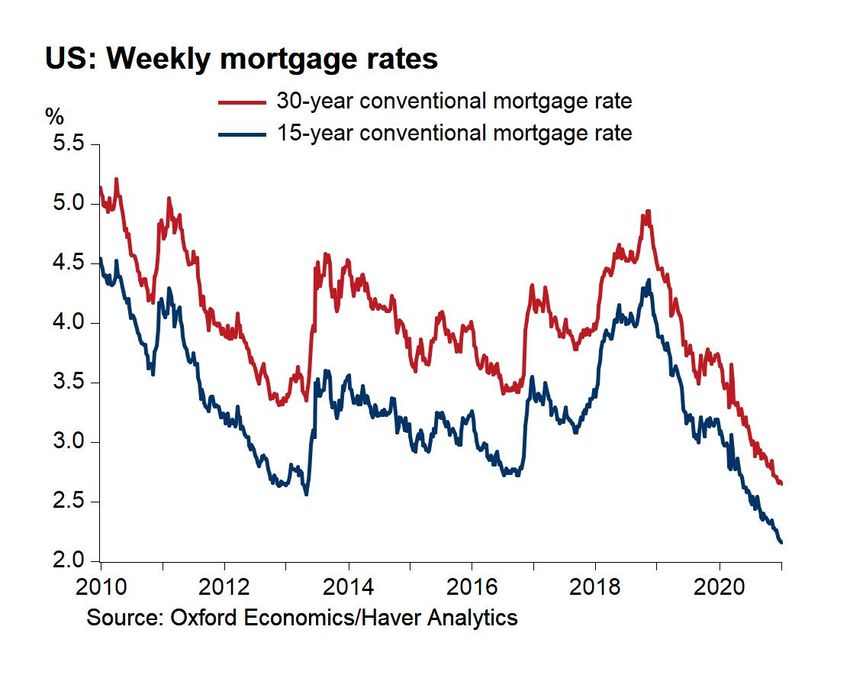

But record low mortgage rates… 20

Business investment remains uncertain

Industrial activity is recovering at a steady pace

US: Industrial activity falls while far below peak

2012=100 / % of capacity

120

IP Manufacturing Capacity Utilization

110

100

90

80

70

60

2005 2006 2008 2010 2011 2013 2015 2016 2018 2020

Source: Oxford Economics/Haver Analytics

22Small businesses remain disproportionately exposed 23

Tech hubs and smaller cities will lead the recovery

US: Medium term metro outlook

24Fed will remain dovish for the foreseeable future

There will be a *transitory* inflation spike this spring

Food contribution

US: CPI inflation

Energy contribution

%, year

Core contribution

4.0 Forecast

Headline CPI

3.0

2.0

1.0

0.0

-1.0

-2.0

2014 2015 2016 2017 2018 2019 2020 2021

Source: Oxford Economics

26But a dovish Fed will maintain low rates 27

Financial conditions remain very accommodative

US: Financial conditions

0 = Average stress Oxford Economics FCI

6.5

5.5

4.5

3.5

2.5

1.5

0.5

-0.5

-1.5

-2.5

2014 2015 2016 2017 2018 2019 2020 2021

Source: Oxford Economics

28A Democrat-controlled Senate will support Biden’s ambitious agenda

Large and rapid fiscal stimulus without precedent

US: Funds authorized by Congress

Since first reported US death from Covid-19 (Feb 28, 2020)

Trillions, $

Since early signs of a financial crisis (Aug. 7th, 2007)

6.00

5.50

5.00

$1.9tn: American Rescue Plan*

4.50 (proposed, not passed)

4.00

3.50 $900bn: Covid relief bill

3.00 $787bn: American Recovery

$480bn: PPP & Healthcare and Reinvestment Act

2.50 (80 weeks after crisis began)

Enhancement Act

2.00 $2.4tn: CARES Act

1.50

$8bn: Preparedness bill

1.00 $190bn: Stimulus bill $700bn: TARP

0.50 $300 bn: Mortgage-guarantee bill

$152bn: Stimulus bill

0.00

0 100 200 300 400 500 Days

Source : Oxford Economics/CBOUpside risks from policy shouldn’t be discounted 31

Conclusions

Conclusions

• While near-term Covid risks are tilted to the downside, gradual vaccine diffusion,

increased fiscal stimulus and warmer weather should ensure stronger economic

activity and employment from early spring onward.

• In Q1, we believe GDP will only advance 1.5% (annualized), constrained by an

uncontrolled health crisis, but supported by the recently passed Covid relief stimulus

package and an expected additional round of $1,400 checks to families. From Q2 on,

broader vaccine diffusion, reduced virus fear, warmer weather, and healthy savings

should bolster the onset of a summer mini boom.

• Real GDP is likely to advance around 3.9% y/y in Q4 2021, versus 3.2% y/y in the

December baseline, on the back of increased fiscal stimulus.

• With Democrats winning Georgia’s runoff races, they will hold a “soft” 50-vote Senate

majority. Control of the Senate will allow President-elect Biden to enact more of his

ambitious fiscal agenda, which boosts prospects for stronger growth in 2021-2022.

• We continue to anticipate QE tapering won’t start until 2023, ahead of rate lift-off in

mid-2024.

33Global headquarters Europe, Middle East Americas Asia Pacific

Oxford Economics Ltd and Africa

Abbey House

Oxford New York Singapore

121 St Aldates

London Philadelphia Hong Kong

Oxford OX1 1HB

Belfast Boston Tokyo

UK

Frankfurt Chicago Sydney

Tel: +44 (0)20 185 268 900

Paris Los Angeles Melbourne

Millan Toronto

London

Stockholm Mexico City

4 Millbank

London SW1P 3JA Cape Town

Dubai

UK

Tel: +44 (0)20 3910 8000

New York Frankfurt:

5 Hanover Square (8th floor) Marienstr. 15, 60329 Frankfurt am Main, Germany

New York NY 10004 Tel: +49 69 96 758 658

USA

Email:

Tel: +1 646 503 3050

mailbox@oxfordeconomics.com

Singapore:

6 Battery Road Website:

# 38-05 www.oxfordeconomics.com

Singapore 049909

Tel: +65 6850 0110

34 Questions: Use the question panel on the rightYou can also read