Where we've been to where we're going - Tony Greco, GM Technical Policy, IPA From where we have been to where we are heading to

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Where we’ve been to where

we’re going

Tony Greco,

GM Technical Policy, IPA

1

From where we have been to where we

are heading to

1. Introduction

2. COVID stimulus & Budget measures

3. Possible reforms

4. Headwinds

5. Tax Cases

6. Questions

2

Introduction

• Accounting profession pivotal role

• Government chose in the main to use the tax system to provide

economic support in response to the extraordinary and unprecedented

impact of the COVID pandemic

• ATO acted quickly to implement administrative systems and associated

guidance to facilitate CF & JK

• Compliance not dead

• Trusted role strengthen opportunity to do more

• COVID put a lot of proposed changes& consultation on hold

• Federal Government Macro settings

• No budget repair until unemployment below target figure

• Trillion-dollar debt

• PM recent address to the Nation

3

COVID – Support Package

Safety Blankets

• Cashflow boost

• JK Ver 1 & 2 wage subsidy

• Bank loan repayment deferrals

• Rental concessions

• Temporary moratorium on insolvent trading laws for directors

• Insolvency- viability reviews

• State based grants/payroll tax etc.

4

COVID Stimulus payments

Cashflow Boost

Sole trader – tax free NANE

Partnership – tax free NANE

Company – unfranked dividend if paid out

Discretionary trust – tax free NANE

Unit Trust – tax free NANE (there is an exception to the CGT event E4 for NANE income in s104-

71 so no cost base adjustment

State Business Grants

• Amendment to income tax laws to make regulations to ensure that specified state and territory

COVID-19 business support grant payments are NANE income

• Eligibility for this treatment will be limited to grants announced on or after 13 September 2020

and for payments made between 13 September 2020 and 30 June 2021

ATO guidance – Government grants and payments during COVID-19

5

COVID Stimulus payments

JobKeeper

Do we take into account in determining the entity’s aggregated turnover ?

• ‘ordinary income that the entity derives … in the ordinary course of

carrying on a business’ (s 328-120).

JobKeeper payments (although they are ordinary income they are not

earned in the ordinary course of business)

6

COVID Stimulus payments – strict interpretation

questioned by IGT

Inspector General Report – ATO’s administration of JobKeeper and

Cashflow boost for new businesses

• Legislative framework had some integrity measures to ensure inactive

entities established or revived solely to access JK or CFB would be

excluded

• ATO took narrow interpretation of integrity measures particularly for new

businesses

• Sale or supply by a new business had not been reported in the BAS

before 12 March 2020 even were the businesses were actively trading

prior to this date

7

COVID Stimulus payments – strict interpretation

questioned by IGT

• ATO has accepted that meaning of “taxable supply” as modified by JK and

CFB was broader than normal definition – can include input taxed supplies

and GST-free supplies

• JK and CFB - a taxable supply(modified meaning) includes where an entity

makes or acquires a financial supply i.e. opening a bank account

• Although a taxable supply must be made for consideration, the

consideration might not be received in the same tax period in which the

taxable supply is made

• Notification by requisite time other than the lodgement of a BAS

8

COVID Stimulus payments – strict interpretation

questioned by IGT

Inspector General Report – ATO’s administration of JobKeeper and

Cashflow boost for new businesses (Cont’d)

• ATO will review earlier decisions

• Still need to show that new business was carrying on an enterprise that

made taxable supplies using modified definition and satisfy remaining

eligibility criteria

• Will not identify all potential affected taxpayers

9

COVID Stimulus payments

JobKeeper AAT decision on backdated ABNs

• On 21 December 2020, the Administrative Appeals Tribunal (AAT) handed

down its decision in Apted and Federal Commissioner of Taxation.

AAT decision

• The AAT held that the applicant did meet the requirement to have an ABN

on 12 March 2020, in circumstances where the ABR Registrar decided to

reactivate a previously cancelled Australian business number (ABN) after

12 March 2020 and backdated the reactivation to have effect on or before

12 March 2020.

ATO

• lodged an appeal with the Federal Court of Australia concerning this

decision.

10Federal Budget – full expensing measure

Recent legislative amendments contained in Schedule 1 to the Treasury Laws Amendment

(2020 Measures No. 6) Act 2020 (the amendments).

The amendments provide businesses with flexibility to choose whether to apply the new full

expensing of depreciating assets (FEDA) measure on an asset-by-asset basis.

• However, this flexibility is not available to small business entities (SBE). By the operation of

the law, SBEs are required to fully expense their general small business pool (pool)

balances on 30 June 2021 and cannot choose not to write off the pool balance

• The practical effect of all these rules is that an SBE is required to fully deduct their pool

balance on 30 June 2021, whereas larger businesses have the flexibility to choose not to

apply full expensing on an asset-by-asset basis

• This will be particularly problematic for trusts that are commonly used in the SME sector.

Full expensing may result in a loss being made by a trust, resulting in the trust having no

distributable income

• inability of the trustee to distribute any franking credits attached to dividends received

by the trust to beneficiaries, or fully utilise the franking credits

• FDT if company has paid out dividends during the year

11

Federal Budget – full expensing measure

A similar issue arose when the instant asset write-off (IAW) was increased from $30,000 to

$150,000.

• Broadly, S.328-210 requires a taxpayer that is claiming its depreciation deductions under

Subdivision 328-D of the ITAA 1997 to claim an outright deduction where its general pool

balance as at the end of 30 June 2020 is less than the IAW threshold (i.e., $150,000 for the

year ended 30 June 2020). The change in the IAW threshold is directly linked to outright

deductions for the balance of a general pool (i.e., where the balance is less than the IAW

threshold)

• It can result in some anomalous outcomes that can be detrimental to taxpayers by making

them worse off over time. This can happen as a result of the individual tax-free threshold and

were applicable, the Low Income Tax Offset and the Low and Middle Income Tax Offset. This

can negate any tax ‘saving’ in the 2020 income year.

• Understandably, taxpayers may feel disadvantaged through no fault of their own. This scenario

is commonplace among many SBE taxpayers, where they had no willingness or financial

capacity to acquire any depreciating assets from 12 March 2020 onwards. However, due to the

lifting of the IAW threshold from $30,000 to $150,000, they are forced to claim a significant tax

deduction in respect to their general pool balance in the 2020 income year.

• Without the lifting of the IAW, the deductions would have otherwise been spread over a

number of income years (which could have resulted in a better tax outcome for the taxpayer).

12Federal Budget – $10M to $50M

As part of the 2020–21 Budget, the government announced an extension to certain

small business concessions (which were previously available to small business entities

with an aggregated turnover of $10 million) to those that have an aggregated turnover

of less than $50 million per annum.

• The tax concessions will apply from 1 July 2020 or 1 July 2021, and the Fringe

Benefits Tax (FBT) related exemptions will apply for eligible businesses in respect of

benefits provided on or after 1 April 2021

From 1 April 2021 the following FBT exemptions will be extended to newly eligible

businesses:

• car parking benefits provided to employees will be exempt from FBT if the parking is

not provided in a commercial car park

• multiple work-related portable electronic devices provided to employees will be

exempt from FBT – even if the devices have substantially identical functions.

13

FBT – COVID impacts

Not business as usual 2020 returns

• Entertainment review options – actual versus 50/50

• Car fringe benefits – operating and statutory

• Car parking benefits

• Review COVID support provided to employees and ATO guidance

• Emergency assistance exemption (see next slide)

14FBT – COVID impacts

Emergency assistance exemption if:

• benefit is emergency assistance to provide immediate relief, and

• employee is, or is at risk of being, adversely affected by COVID-19

• Accommodation, food and transport for stranded employees

• Emergency health care to employee affected by COVID-19:

• only applies to health care treatment provided by an employee on your premises at or

adjacent to an employee's worksite

• items provided to employees to protect them from COVID-19

• Work-related preventative health care

• COVID-19 testing

15

COVID-19 and car fringe benefits

Car Park

• If, on a particular day, a business’s office is closed due to COVID-19 and therefore the work car park is

also closed, the employer will not have provided a car parking benefit as there will be no car space

available for use by an employee for more than four hours between 7.00am and 7.00pm on that day.

• The time during which the work car park is closed will not form part of the availability periods used

to calculate the taxable value of a car space under the statutory method.

Closure of nearby commercial parking stations

• If all of the commercial parking stations within a one kilometre radius of a business premises are

closed on a particular day due to COVID-19, there will be no car parking benefits provided.

Reduced rates at commercial parking stations

• May not have provided a car parking fringe benefit (the lowest fee charged by all of the commercial

parking stations within a one kilometre radius of a business premises for all-day parking was less than

$9.15 ). For example, this may occur where all of the commercial parking stations have discounted

their all-day parking rate due to COVID-19.

Cars and Fringe benefits

• During a period of COVID-19 restrictions, a car that has been provided to an employee is not taken to

be available for the employee’s private use if all the following apply:

• the car is returned to the business premises

• the employee cannot gain access to the car

• the employee has relinquished an entitlement to use the car for private purposes.

ATO Factsheet - COVID-19 and car fringe benefits

16PS LA 2001/6: Home office running expenses

What are the acceptable methods of calculating home office expenses:

1. Actual Expenses Method

• Keeping records and written evidence to determine the work-related

portion of actual expenses incurred (Diary actual hours spent/log

book).

2. Fixed Rate Method

• Use a rate of 52 cents per hour (effective from 1 July 2018).

• Noting that this only relates to lighting, heating, cooling, cleaning costs,

and decline in value of home office items such as furniture. (see over)

• The Actual Expenses Method would need to be used for any other

costs (e.g. phone and internet expenses).

17

Home office expenses – fixed rate method

Which expenses are INCLUDED in 52 cent method* Which expense are EXCLUDED from 52 cent method

• Heating/ Cooling • Phone expenses

• Lighting • Internet expenses

• Running electrical items (electricity generally) • Computer consumables

• Cleaning • Stationery

• Decline in value of furniture • Decline in value on computers, laptops or

other equipment

* NB The fixed rate is based on average energy costs and the value of common furniture items used in home

business areas.

18Home office expenses you can and can’t claim

Expenses Home is principal Home not principal You work at home but no

workplace with dedicated workplace but has dedicated work area

work area dedicated work area

1. Running expenses Yes Yes No – see Note 1

(excluding any below)

2. Work-related phone and Yes Yes Yes

internet expenses

3. Decline in value of a Yes Yes Yes

computer

(work related portion)

4. Decline in value of office Yes Yes Yes

equipment

(work related portion)

5. Occupancy expenses Yes No No

Note 1: Generally, an employee who works at home and who does not have a dedicated work area, will not be entitled to claim running expenses, or their claim for running

expenses will be minimal. This is because they can only claim the additional running expenses incurred as a result of working from home.

19

New alternative treatment (temporary now extended

to end of June 2021)

20New shortcut method: PCG 2020/3

TOPIC RESPONSE

Authority: Practical Compliance Guideline PCG 2020/3: Claiming deductions for additional

running expenses incurred whilst working from home due to COVID-19.

1. What is the Rate? 80 cents per hour

2. What is the period? 1 March 2020 to 30 June 2020 (and beyond to 30 June 2021)

3. What running expenses • Electricity (eg lighting, cooling/heating, electronic items used for work) & Gas

does this cover? • Decline in value of capital items such as home office furniture (and repairs)

• Cleaning expenses

• Phone expenses

• Internet expenses

• Computer consumables

• Stationery; and

• Decline in value of a computer, laptop or similar device.

• NB Taxpayers only have to have some of those expense categories to qualify.

21

New shortcut method: PCG 2020/3

TOPIC RESPONSE

4. Who is eligible? • Persons working from home to fulfil their employment duties, or to run their

business during the period from 1 March to 30 June 2020; and

• Incurring additional running expenses due to working from home.

• Covers persons working from home whether as a result of COVID-19 or not.

• Includes any business owner who now carries on their business from their home.

• NB Persons who are on leave or stood down are not eligible during that period.

5. What is the record- • A record of the hours worked at home.

keeping requirements? • Eg timesheets, rosters, a diary or similar document that sets out the hours worked.

6. How to disclose on • Must include the notation ‘COVID-hourly rate’ next to their deduction for home

income tax return? office expenses in their 2019-20 tax return.

22New shortcut method: PCG 2020/3

TOPIC RESPONSE

7. How does it compare to The existing 52 cent per hour fixed rate covers home office electricity, gas, cleaning

the existing methods? and decline in value of home office furniture. It does not cover other expenses; such

as computer consumables, stationery, phone, internet, decline in value of computer,

laptop or similar devices.

As such, a record of the hours worked at home, along with full written evidence to

substantiate those expenses that are not covered by the current fixed rate per hour

must still be kept when using this methodology.

The shortcut method of 80 cents per hour:

• captures all relevant expenses in a simplified manner.

• However, where this method is claimed, a taxpayer cannot claim a further

deduction for any of the listed expenses.

• It does not cover occupancy expenses.

23

New shortcut method: PCG 2020/3

TOPIC RESPONSE

7. How does it compare Multiple people living in the same house can claim this shortcut method rate.

to the existing methods? For example, a couple living together could each individually claim the 80 cents

(Continued) per hour rate, where they are both working from home.

The requirement to have a dedicated work from home area has also been

removed.

This new shortcut arrangement does not prohibit people from making a working

from home claim under existing arrangements.

Claims for working from home expenses prior to 1 March 2020, cannot be

calculated using the shortcut method, and must use the pre-existing working from

home approach and requirements instead for that period.

24Steps – New shortcut method

1. Keep receipts of all expenses.

2. Calculate how many hours you worked from home.

3. Claim a deduction of 80c x number of hours worked from home.

4. Do not claim any further deductions for running expenses or

purchases.

• If you use the shortcut method to claim a deduction for your

additional running expenses, you cannot claim a further deduction

for any of the expenses listed above.

5. Include ‘COVID-hourly rate’ as a notation in your 2020 tax return.

25

Possible Reforms

1. Black Economy Measures

• Limit on cash payments of $10K – not proceeding

• Third party platforms reporting regime – proposed to apply from 1 July

2022 and 1 July 2023

• From 1 July 2021, ABN holders with an income tax return obligation will

be required to lodge an income tax return

• From 1 July 2022, ABN holders will need to confirm the accuracy of their

details on the ABR annually

2. Small Business CGT concessions

3. Expand education deductions

4. Small business tax offset

5. Div 7A – proposed to apply from the first income year commencing on or

after royal assent of enabling legislation

26Expansion of Education Deduction

Should the tax system play a greater role to encourage the retraining and

reskilling of individuals is the question being asked

• The requirement for a tax deduction is limited to expenses in gaining or

producing assessable income.

• This limits deductions to an individual’s current employment activities that

either maintains or improves the specific skills required for that

employment or leads to an increased income in the individual’s current

employment.

27

Expansion of Education Deduction

• We see this proposal working hand in hand with one of the other 2020-21 Federal Budget announcements -

the exemption for FBT employer-provided education

• exempt from FBT, employer-provided retraining and reskilling benefits to redundant, or soon to be

redundant, employees where the benefit may not relate to their current employment

• Regardless of whether the Government proceeds with this proposal, it is an opportunity to remove the current

rule which requires individuals to reduce their self-education deduction by $250

• The concept is outdated and does not serve any useful purpose. Most individuals allocate costs that are

not deductible against this arbitrary threshold, so its removal eliminates some unnecessary compliance

• Safeguarding the tax system – integrity measures required to minimise opportunities for tax misuse

and abuse

• Also need to ensure that individuals do not take advantage of the relaxation of the tax rules to engage in

lifestyle or personal choices subsidised by the taxpayer

• A shared risk approach with the individual who proposes to take advantage of the concession is

warranted

• One option is quarantining half the upfront deduction until the individual earns income from an activity

associated with the retraining. This ensures that taxpayers do not wear the entire cost of education outlay

in cases where the retraining does not result in the furtherance of a new activity

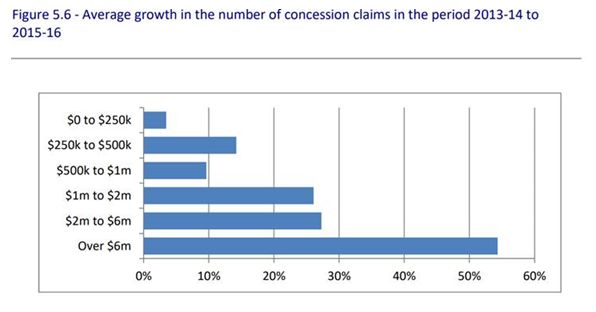

28Small Business CGT concession

Originally meant to provide security in retirement for small-business owners

or encourage growth

• Sheltered capital gains ballooned to $6.2 billion in 2015–16, with some

claims rising to $80 million per claim.

• Claims above $6 million more than doubled between 2013–14 and 2015–

16, with the total value of those claims rising from $180 million to $400

million.

Reform Pathway

• collapsing the 15-year exemption, active asset reduction and retirement

exemption, and replacing them with one CGT exemption subject to a cap.

• eligibility turnover threshold to be raised from $2 million to $10 million,

and to repeal the maximum net asset value test.

29

Small Business CGT concession

30• SMSF Auditor independence revised guidelines – reciprocal audit

arrangements, providing other services

• Retirement incomes review

• Single touch payroll

• Micro employers STP version 1 – exception for micro employers

experiencing exceptional circumstances

• Closely held

• STP stage 2 – January 2022

• TPB Review

• Independence/Governance

• Annual registration

Headwinds • Penalties

• Education requirements

• 120 hours CPD requirement

• Fit and proper tests

• Modernising client verification

• Modernising Business Registers (MBR) Program & Director Identification

Numbers (DINs)

• Tax gaps – ATO to resume focus on high gap sectors – SME’s and

Individuals

• NSW – replace stamp duty with a broad-based property tax

31

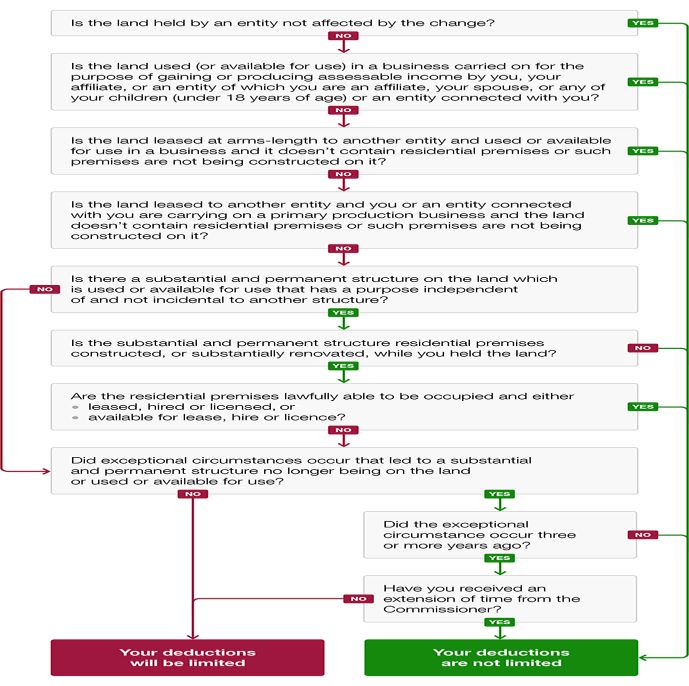

Vacant Land – denial of holding costs

Anecdotally we believe a lot of professionals have not fully understood

these new provisions as the term “vacant land” congers an image that it

will only apply to land without any structures on it, which is unfortunately

not the case.

The new law has far-reaching consequences and catches taxpayers and

circumstances which were not the obvious target

3233

Tax Cases 2020

• Lambourne v FC T - the words “necessarily incurred” under s 8-1(1)(a), to

be entitled to a work-related deduction

• Eichmann v FCT – what constitutes an “active asset” for the small business

CGT concessions (vacant land with a shed sensible outcome)

• Greig v Commissioner Taxation – income versus capital (share trader held

to be on revenue account – applied industry skill and experience)

• FCT v Pike – concept of residency based on ordinary concepts

• San Remo Heights Pty Ltd v FCT - This case illustrates how broad the

enterprise definition can be and that it is harder for a company to prove that

it is not carrying on an enterprise, as opposed to an individual in the same

circumstances

34QUESTIONS? 35

You can also read