2018 Outlook Edition - BB&T Perspectives Magazine

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2018 Outlook Edition

bbtperspectives.com/2018-outlook-edition/

January 22, 2018

January 2018

“Forecasts may tell you a great deal about the forecaster; they tell you nothing

about the future.”

Warren Buffett

Each December, Barron’s magazine writes an Outlook edition for the year ahead where

market prognosticators forecast year-end target prices for the S&P 500 Index, similar to

picking the Super Bowl winner. This year’s forecasts predicted the 2018 year-end target price

to land somewhere between 3,100 and 2,675 (2,802 at press time). In this edition of Market

Monthly, we share our 2018 Outlook with you to help navigate the year ahead, but we’ll resist

the temptation to make a market call. We focus on key themes to provide you with objective

guidance to keep your portfolio’s compass true north.

Summary:

1/12

The Economy: Three Rs characterize the economic phases of the past nine years since the

great financial crisis are: Repair, Recovery and Reflation. Global financial systems have been

repaired. Central banking authorities like the Fed have provided a path back to a normal

business cycle and financial recovery. Reflation is a common theme of strong late cycle

recoveries like we have now. Strong global economic growth has continued into 2018 with no

signs of recession. The Federal Reserve remains on their quarterly rate hike path while the

economy is strong to be better prepared for future slowdowns. Tax cuts are expected to add

roughly 0.5 percent to gross domestic product (GDP) growth until rising rates begin to impact

financial asset prices.

Equity Markets: Many of the same factors that led us to favor equities over bonds in 2017

remain in place today. Bulls argue a strong economy and tax reform tailwinds will fuel

corporate earnings and propel global markets. Bears argue high valuations and excessive

optimism may lead to rising risks. We think both are right to a degree and see equities

transitioning from a steep return/flat volatility regime to a modest return/rising volatility regime

as 2018 progresses. We think international markets could lead the way again in 2018.

Bond Markets: Rising inflation expectations have recently nudged Treasury yields higher.

Municipal bonds and investment-grade corporate bonds remain preferred areas with high-yield

corporate bonds and international bonds becoming increasingly unattractive at this late stage

of the cycle. This year is likely to be a “keep your coupon” best case scenario for bond returns.

Currencies: The U.S. dollar sits at a three-year low. Accelerating economic strength of

developed and emerging economies along with growing concerns about the U.S. deficit have

created headwinds for the U.S. dollar. A -10-percent decline in the dollar in 2017 has carried

over into 2018 but has generated significant incremental returns for U.S. investors holding

international stocks, bonds and funds.

Asset Allocation: We continue to favor stocks over bonds in 2018 but expect rising interest

rates to challenge financial asset prices later in the year. Those who have remained invested

since the last recession in 2009 have been richly rewarded. Investors on the sidelines who fear

missing out on a euphoric market melt-up should exercise caution with realistic expectations

prior to entering a race that has largely already been run.

The Economy: The three Rs: Repair, Recovery and Reflation

Repair (2009-2014): The Great Recession from December 2007 to June 2009 was

characterized by the near collapse of global financial systems. Extraordinary monetary policy

responses by the Federal Reserve included Zero Interest Rate Policies, QE1, QE2 and QE3.

These policies and those of other global central banks backstopped the banking systems and

steered global economies down the road to repair with true recovery and a normal business

cycle remaining elusive.

Recovery (2014- ): Though the stock market recovery began from an oversold bottom in

March 2009, we trace the economic recovery back to the end of QE3 in the fall of 2014. The

Fed ceased its QE3 bond buying program in late 2014 nudging the U.S. economy to pull itself

2/12

up by its own bootstraps and stand on its own two feet. With waning Fed support, the recovery

from 2014-2016 was lumpy and marked by an earnings recession and a nominal GDP

recession. Since early 2016, economic growth has become globally synchronized with roughly

90 percent of world economies now experiencing accelerating economic growth. A more

normal business cycle is slowly being restored after years of repair. Though we are past the

mid-point of this cycle, the near term probabilities of recession among leading economies in

the developed world remains quite low as the chart below illustrates.

Reflation (present day): Reflation is a growing theme globally as the table below shows.

Headline inflation has made a broad comeback both in advanced and emerging economies.

3/12

In the U.S., Core Services inflation represents 74 percent of measured inflation and is already

rising in excess of the Fed’s 2-percent target. Core hard goods inflation, however, is actually

deflationary registering price declines of -0.6 percent. Wage growth and commodity prices

continue to slowly build pressure but are not expected to spike. Corporate tax cuts could serve

as a modest inflation headwind as they are expected to increase corporate profit margins by

roughly 0.5 percent potentially giving corporations less incentive to raise prices to make the

same buck.

Bottom Line: Global economic growth remains robust independent of any impact from

corporate tax cuts. Inflation rates remain lower than previous recoveries but are firmly

anchored and supportive of a late cycle reflationary theme. This should be enough to keep the

Fed on course for quarterly rate hikes in 2018.

Fed Update: The Jan. 30-31 Fed meeting will be the last for Janet Yellen’s successful tenure.

This will be a busy year for the Jay Powell led Fed with several FOMC seats yet to be filled by

President Trump. Powell will likely explore more flexible “price level target” frameworks for

future Fed policy during times of economic imbalance as a possible alternative to hard inflation

targets. We anticipate that concerns regarding asset price inflation will become a more

prominent part of Fed discussions. The Fed would rather slowly let air out of economic growth

than be accused of blowing hot air into an asset bubble a year or two from now. Monetary

conditions are actually easier today due to strong economic and earnings growth, a weaker

U.S. dollar and expansionary fiscal policies despite six rate hikes since December 2015. This

gives the Fed the ammunition it needs to continue hiking rates without waiting for a hard 2-

percent inflation target. They do not want to get back into a QE game at the next slowdown,

and they cannot depend on additional fiscal relief from Washington now that tax reforms have

passed so they will continue hiking rates while economic growth is strong.

Bottom Line: The Fed is likely to stay the course with additional rate hikes in 2018 while the

economy continues to grow. There remains a delicate balance between simultaneous

tightening by the Fed and accommodation from Washington’s tax reform. We think the risks for

Fed policy missteps are small in the near term but rising rates eventually impact asset prices.

Washington Update: We expect a busy calendar in Washington during this mid-term election

year but nothing of the magnitude that we saw with health care debates and tax reform last

year. Some of the major items of economic relevance that bear watching include:

Infrastructure Bill: We expect more headlines than headway as it regards a meaningful

infrastructure bill. Tax revenues from repatriation of corporate cash held overseas initially

earmarked to pay for infrastructure are now needed to help pay for the tax cuts. We expect to

hear more about this leading up to the Jan. 30 th State of the Union address but passage of any

meaningful legislation in 2018 is unlikely without funding.

Trade Policy: Montreal will host the next NAFTA negotiations Jan. 23-28th. The Trump

administration may signal its intent to withdraw from NAFTA following round one of these

negotiations but it is more likely this is a negotiation tactic. Also, tariff discussions on Chinese

4/12imports could resurface after being put on hold last year during health care and tax reform

negotiations. Any combination of these two trade events could cause market interference.

Spending and Debt Limits: At this writing the House has passed a temporary spending bill to

keep the government running until Feb. 16th but passage in the Senate will be more difficult. A

shutdown is possible but should not have lasting market impact if it occurs. Likewise the U.S.

must address its debt limit by mid-March, which has been delayed twice in September and

December. Failure on these two fronts could cause near term volatility and make for an even

more difficult midterm election year for Republicans.

Midterm Elections: Since Eisenhower, first term presidents have lost, on average, 19 House

seats in the midterm elections. Unpopular presidents have typically lost more seats (Reagan in

1982 and Obama in 2010) and President Trump’s approval rating is currently the lowest of any

first-term president. The chart below illustrates a 40-percent probability of Republicans

retaining the House and 60-percent chance of retaining the Senate. Current trends suggest the

Republicans are tracking to lose 30 or more House seats in November, which would return the

House to Democratic leadership.

U.S. Equity Update:

As the chart below shows, 2017 was a solid year for U.S. equities. Some trends included:

S&P 500 total returns rose every month for the first time on record

Large Cap beat Mid Cap beat Small Cap

Growth stocks beat value stocks by a wide margin

Cap weighted indices beat equal weighted indices

5/12S&P 500 results were dominated by five big tech leaders (i.e., Facebook, Apple, Amazon,

Microsoft and Google,) which earned a combined 45 percent return. Within the S&P 500 these

five stocks represent:

13 percent of the market value

10 percent of the earnings

6 percent of sales revenue

Also on tap for 2018, are changes to the S&P 500 index as the current Telecom Sector (3

percent of S&P 500) becomes a brand new Communication Services sector (10 percent of

S&P 500). Tech names like Google, Facebook, eBay will join this new sector and no longer be

considered “tech.” Disney, Comcast and Netflix are a few media names that will also join this

new sector. Within the S&P 500, Technology and Consumer Discretionary sectors will see their

index weightings reduced by 4.5 percent and 3 percent respectively. This should not be more

than a game of musical chairs with little if any market impact.

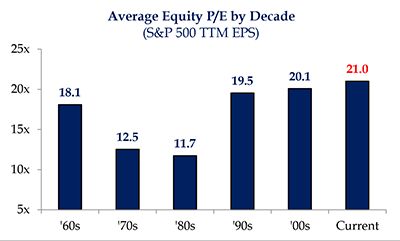

Earnings and Valuations: The charts below illustrate a pattern of earnings growth for the S&P

500 and frame current valuations relative to prior decades based on trailing PE ratios. Four key

points:

1. 2015-16 marks the earnings recession following the end of QE3

2. 2017 reflects a normal business cycle with organic earnings growth

3. 2018 reflects sustained earnings growth of 9 percent with an additional 5-percent tax

reform boost.

4. Valuations remain higher than previous decades making earnings growth necessary in

2018 to support valuations

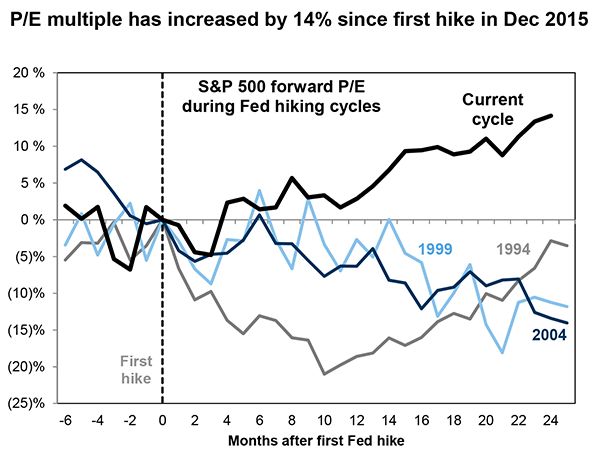

6/12Rising Interest Rates a Key Risk: Historically, rising interest rates threaten stock valuations and

compress PE multiples. As the chart below shows, the current cycle has not followed the path

of prior cycles and is different because this rate hike cycle had 0 percent as its starting point.

To date, rising interest rates have actually been positively correlated with rising stock prices.

This is unusual. Once we see a Fed Funds rate eclipse 2 percent (2 hikes away) and 10-year

Treasury yields pass 2.75 percent we expect rising rates to impact stock prices and compress

PE ratios. This is a late 2018 or early 2019 risk.

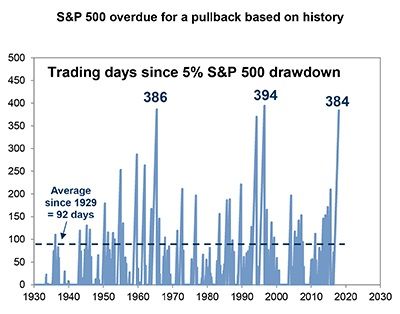

7/12Low Volatility Set to Change: The S&P 500 had the lowest volatility on record in 2017 and the

second smallest drawdown in almost 90 years of market history. This trend extended to global

equities as well. Since 1945, the U.S. has experienced 10 occurrences where the S&P 500

declined by less than 6 percent over the course of a calendar year. These occurrences reveal

that the average:

Drawdown in these low volatility years is just -4 percent (last year was -2.8 percent)

S&P return in those years is 25 percent with all 10 years earning a positive return

Drawdown the following year was -12 percent

Return the following year was 5 percent with negative returns three times

The chart below provides a condensed timeline as of Jan. 4th, 2018, going back to 1930 and

graphs the numbers of days since the S&P 500 last had a 5-percent correction. At press time,

we have officially broken the record for longest period and it has now been 395 days without a

5-percent correction. Our purpose for revisiting this theme is not to talk about broken records

but to caution investors against complacency. In 2018, we expect the increasing levels of

volatility and higher drawdown incidents that typically occur in late stages of a bull market. This

is normal. Stay invested.

8/12Bottom Line: We expect double-digit earnings growth in 2018 with a tailwind from corporate

tax cuts. These tailwinds are expected to drive pro-growth corporate behavior with

corresponding positive economic results. Valuations are currently rich having front run

anticipated EPS growth in 2018 but should be validated with continued strong earnings. We

caution against investor complacency and think 2018 earnings growth could outperform index

returns.

International Equity Update: International equity markets followed the same path of their

underlying economies in 2017 rewarding investors with their best returns in several years. For

U.S. investors the returns were even better due to a -10-percent decline in the U.S. dollar. The

chart below shows the returns of the underlying markets for various regions of the world

without currency effects (local) and with currency effects for U.S. investors (U.S. $). U.S.

investors enjoyed double-barreled returns profiting from good performance in both international

stock markets and their currencies. Both market and currency cycles often last several years,

and so far, in 2018 it has continued, to benefit U.S. investors.

9/12Bottom Line: International economies and their markets are earlier in their recovery cycle

than the U.S., have healthy earnings growth and continuing central bank accommodation.

Even with a stable U.S. dollar, we think international markets will continue to be a bright spot in

investor portfolios.

Bond Update:

Interest rates remained lower than we anticipated in 2017 due to lower-than-anticipated

inflation. We expect the economy to continue growing above trend with a positive impact from

corporate tax cuts as early as the Q2 earnings season. This should apply upside pressure to

inflation and interest rates as 2018 unfolds. Bond markets are only now beginning to price in

rising inflation expectations. Since the end of 2017, bond markets have begun to sniff out

inflation and 10-year Treasury yields have increased 0.25 percent. For now, this has quieted

concerns about a flattening or inverting yield curve as the curve has gotten steeper in the last

month. Markets have only priced in two rate hikes in 2018 despite the Fed’s forecast of three

rate hikes, but that also has begun to change.

Corporate tax reform should benefit investment-grade corporate bonds of companies not

strapped by heavy debt burdens. High-yield corporate bonds could be disadvantaged later in

the year as limitations on their ability to deduct interest expense could hamper financial

performance for highly levered companies at the lowest end of the credit scale. This is not an

imminent risk, but high-yield investors should keep an eye on interest rate spreads between

high yields and high quality as an early warning indicator for signs of late cycle deterioration.

Municipal bonds remain attractive with a supply/demand balance that should support prices

fairly well. Also, TIPs are an area that could gain traction as the year progresses if recent

inflation undercurrents translate into higher top-line inflation numbers.

As the chart below shows, high-yield bonds and international bonds closed 2017 as fixed-

income leaders. Of that return, 100 percent from international bonds was attributable to a

weaker dollar. Aside from currency calculus, international bonds are increasingly unattractive

as other central banks (i.e., ECB) may look to reduce accommodative monetary policies later

this year and into 2019.

10/12Final Thoughts:

The global economic recovery is sustainable, broad based and accelerating

Falling unemployment, rising productivity and higher wages underpin a reflationary

theme

The Fed will hike more than markets imply in 2018 and will evaluate expanding their

policy framework

Currently easy financial conditions will begin to fade into 2019 as rising rates take hold

Corporate tax reform will be a growth tailwind adding as much as 0.5 percent to GDP

growth

Double-digit earnings growth should help support stock prices

S&P 500 performance is being driven more by organic earnings growth rather than PE

expansion (a good thing)

Interest rates have yet to impact financial asset prices, which could change in the second

half of 2018 or early 2019

Any corrections should be shallow and short

Stay invested, focused and true to your compass

Sources: Strategas Research Partners, Evercore ISI, FactSet, Goldman Sachs Global

Investment Research, Morningstar, BCA Research

This piece is produced by BB&T’s Wealth Portfolio Management Team.

The information set forth herein was obtained from sources, which we believe reliable, but we

do not guarantee its accuracy. Neither the information nor any opinion expressed constitutes a

solicitation by us of the purchase or sale of any securities. Diversifying investments does not

ensure against market loss and asset allocation cannot eliminate the risk of fluctuating prices

and uncertain returns. Past performance does not guarantee future results.

11/12Traditional banking services are provided by Branch Banking and Trust Company, Member FDIC. Only deposit

products are FDIC insured. Investment solutions are provided by Branch Banking and Trust Company, BB&T

Investments and BB&T Scott & Stringfellow. BB&T Investments and BB&T Scott & Stringfellow are divisions of BB&T

Securities, LLC, member FINRA/SIPC. BB&T Securities, LLC, is a wholly owned nonbank subsidiary of BB&T

Corporation. Securities and insurance products or annuities sold, offered or recommended are not a deposit, not

FDIC insured, not guaranteed by a bank, not insured by any federal government agency and may lose value.

Services and products featured herein may include some offered by affiliated companies of BB&T Wealth. The fees

for those services and products are in addition to the fees charged by BB&T Wealth. As a result, BB&T Corporation,

as a whole, receives more compensation than would otherwise be received if a non-affiliated service or product was

used. When we offer any service or product to a client, we use the same process to offer both affiliated and non-

affiliated services and products. When we have authority to select any service or product on behalf of a client, if our

process shows affiliated services and products to be competitive with corresponding non-affiliated services and

products, then we may select affiliated products and services. BB&T Wealth expresses no opinion on the use of

BB&T affiliated services and products when the client selects such services and products in a client-directed account.

BB&T and its representatives do not offer tax advice. The information provided should not be considered as tax or

legal advice. Please consult with your tax advisor and/or attorney regarding your individual circumstances.

By clicking any third party links, you will leave BBTPerspectives.com to visit a third-party website where the privacy

and security policies of BB&T do not apply. BB&T is not responsible for the content, products or services that you

may find there.

12/12You can also read