Monthly World Energy Market Review - Release Date: January 8, 2019 - NUS Consulting

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Monthly World Energy Market Review Release Date: January 8, 2019

International Pricing Information

US Current price M/M (%) Y/Y (%)

Europe Current price M/M (%) Y/Y (%)

Baseload Power (MWh) – Month Ahead

Power (MWh) Rotterdam Coal

Germany € 55.38 - 6.50 % + 75.80 %

Avg. price ind users $69.7 +2.70 % + 0.40 % (US$/t)

C: $81.25 France € 61.49 + 3.10 % + 80.80 %

PJM region weekday $36.69 - 42.90 % - 26.10 %

Palo Verde weekday $21.98 - 27.60 % - 7.00 % M/M: - 5.10 % Spain € 62.40 - 2.80 % + 14.70 %

Y/Y: - 14.20 % Swiss € 60.02 - 3.40 % + 35.40 %

Natural Gas (Dth) per Dth.

UK £ 60.64 - 5.30 % + 15.60 %

Henry Hub $2.944 - 32.20 % - 2.10 %

Italy € 70.90 - 2.60 % + 41.50 %

Natural Gas (MWh)

NL (TTF) € 21.53 - 11.90 % + 12.00 %

WTI UK (NBP) £ 20.87 - 3.50 % + 11.20 %

(US$/bbl)

C: $48.52

M/M: - 9.00 %

Y/Y: - 21.30 %

Venezuela Oil Basket Japan LNG

(US$/bbl) (US$/ Dth.)

C: $56.43 C: $ 8,83

M/M - 6.90 % M/M - 9.90 %

Y/Y - 13.3 % Y/Y: - 21.00 %

Singapore Fuel Oil

(US$/ Ton)

Brazil CEPEA Hydrous C: $362.37

Ethanol (US$/l) M/M: -7.80%

C: $0.4875 Y/Y: - 4.20 % Australia Current price M/M (%) Y/Y (%)

M/M: + 16.20 %

Baseload Power (MWh)

Y/Y: - 8.90 %

Queensland $76.71 - 0.6 % - 0.70 %

Global Energy Review – International Markets

International Energy Markets - Review

• Nordic forward power prices rose on Tuesday, supported by drier, colder weather forecasts in the hydropower-dependent

region and stronger carbon rates.

• President Vladimir Putin opened Russia’s first liquefied natural gas (LNG) floating storage and regasification unit (FSRU) on

Tuesday, saying it bolsters the country’s energy security. Moscow’s decision to set up the FSRU was in part to reduce gas

transit risks to Kaliningrad, home to a Baltic Fleet base, as the EU steps up efforts to reduce its dependency on Russia.

Gazprom CEO Alexei Miller told the Interfax news agency that supplies to Kaliningrad from Lithuania had been completely

halted on Tuesday and replaced with natural gas from the FSRU. The FSRU, the first of its kind in Russia which arrived from

Singapore last month with a cargo on board to commission the LNG import facility, can provide Kaliningrad with 2.7 billion cubic

meters (bcm) of gas a year. LNG is delivered by tankers, meaning it can be supplied to many markets.

• Libyan authorities issued arrest warrants for 37 suspects over attacks on key oil ports in the east of the country and a military

base in the south, a source in the attorney general’s office said. The warrants showed that 31 members of the Chadian and

Sudanese opposition based in Libya, along with six Libyan nationals, are wanted for attacks on the oil ‘crescent’ in the east of

the country and on the Tamanhint military base as well as for their participation in fighting between Libyan rivals.

• Asian spot prices for LNG fell last week although few cargoes were heard to swap hands in a well supplied market with some

traders still on their NY’s break.

Global Energy Review – US Markets

United States Energy Markets - Review

• For the week ending 28 December 2018, US natural gas inventories declined by 20 Bcf, compared with the five-year average

withdrawal of 107 Bcf and last year’s withdrawal of 193 Bcf for the same reporting week. Overall, natural gas inventories remain

substantially below both the 5-year average and prior year’s levels – down 450 against last year and 560 against the 5-year average.

However, over the past two weeks the gap between current inventories and the prior year has declined substantially – roughly 250 Bcf.

This is the result of two consecutive weeks of minimal withdrawals due to milder weather. As one would expect, two weeks of

unusually light withdrawals have had a dramatic impact on 2019 NYMEX Strip Pricing. Two weeks ago, the 2019 Strip (including

January) averaged $3.28. Presently, the 2019 Strip (excluding January) is trading at $2.74. With more mild weather forecasted for the

next 6-10 days, it’s expected that the market might see a few more bearish withdrawals that could add some additional downside

pressure on pricing. However, longer-dated forecasts seem to suggest that colder air will eventually move back into the major

consuming regions.

• If seasonally cold weather returns, expectations are that price volatility and NYMEX futures will move upward, particularly the near

months (Feb, March and April). We continue to view the recent pull back in pricing as an opportunity for consumers with open

positions (in the remaining winter months) to layer additional hedges and limit their exposure to further price volatility being driven by

low inventories and short-term weather forecasts. Moreover, backwardation in market continues to support proactive hedging of

natural gas requirements extending through 2020 and 2021.

• For years, FirstEnergy has been seeking a bailout for its uneconomic coal and nuclear plants. The Ohio-based utility finally got its wish

in late 2016, when the Public Utilities Commission of Ohio (PUCO) approved more than $600 million in customer-funded subsidies.

The money was intended to help improve the credit ratings of FirstEnergy and its parent company, FirstEnergy Corp. But the parent

company’s supposed financial hardship is not the responsibility of the utility’s customers, nor is it under the PUCO’s purview.

Global Energy Review – European Markets

European Energy Markets - Review

• Poland: The European Commission expects Poland to submit its new law cutting tax on electricity for scrutiny to see if it complies with

EU laws prohibiting illegal state aid to companies. Poland’s lower house of parliament passed on 28 December legislation to cut tax on

electricity as the ruling Law and Justice (PiS) party looks to prevent a jump in energy bills ahead of a parliamentary election this year.

State-run utilities have proposed raising household bills by more than 30% next year to claw back revenue hit by a 65% jump in

wholesale electricity prices and a 400% leap in carbon prices this year.

• Greece: Greece has given investors another week to 15 January to submit binding bids for three coal-fired power plants and a licence

to build another one. Public Power Corp. (PPC) is selling the plants in northern Greece and on the southern Peloponnese under the

terms of Athens’ latest international bailout after an EU court ruled that PPC had abused its dominant position in the coal market. deal”

on energy pricing in heavy industry. The bid deadline has been repeatedly pushed back since the tender was launched last year for

different reasons. PPC has shortlisted six investors but a source familiar with the matter, who declined to be named, said only three

may submit binding bids.

• Germany: With the European Parliament backing a net zero emissions target for 2050, EU member states will need to further develop

their biogas markets to continue to reduce emissions from waste, energy, and transport. In Germany, the biogas market has a special

history. It began with the building of around 100 farm waste and food waste plants in the early 1990s, with this number increasing

steadily over the next 15 years. 2008, however, was when the biogas boom really started: the number of plants nearly doubled within

two years. Following the first tranche of funding for biogas in Germany, production of flexible power will be the most sustainable market

moving forward There is also strong growth potential for separation and processing technology for fermentation residues and manure.

Global Energy Review – Asia/Pac Markets

Asia-Pac Energy Markets - Review

• Australia: Clean Energy Finance Group (CEFC) invested $71.82m (A$100m) in the Australian Renewables Income Fund

(ARIF), a fund managed by asset manager Infrastructure Capital Group (ICG), marking its largest equity investment to date.

The fund focuses on large-scale wind and solar as well as energy-from-waste and battery storage. The investment is almost a

40% increase in the CEFC’s renewables equity portfolio, which now stands at A$355m. ARIF will focus on proven large-scale

wind and solar technologies, as well as emerging opportunities in energy-from-waste, large-scale battery storage, and pumped

hydro.

• China: The growth of coal-fired generation outpaced hydropower and solar due to unfavorable weather. China’s power

generation grew 6.9% in the first 11 months of 2018 (January to November) compared to the same period last year. According

to an announcement, this pace of growth is slower than the 7.2% rate in 10M2018. In November, power generation rose by

3.6%. Coal-fired electricity generation expanded at a faster pace in November, rising 3.9% YoY, whilst the generation of

hydroelectricity and solar power both posted a slower growth rate due to unfavorable weather. Wind-generated power output

fell 9.5% YoY last month, compared with a rise of 4.2% in October, because of a high comparative base from November of last

year and low wind speed last month.

• Japan: Royal Dutch Shell Plc has set up a small desk to trade electricity in Japan. The firm sees opportunities to balance the

grid when there are supply-demand mismatches driven by intermittent wind and solar power. More volatility in the power

system is expected in the future and this would increase the opportunities. Shell will be the first major foreign company to enter

the market that fully deregulated in 2016, after being dominated for decades by regional monopolies. It is possible others could

follow as the liberalized market may allow traders to take on risk Japanese firms want to hedge.

Global Energy Review – LATAM Markets LATAM Energy Markets - Review • Mexico: Contour Global plc has announced it has reached an agreement with Alpek S.A.B. de C.V. to acquire Alpek’s portfolio of two natural gas-fired combined heat and power (CHP) plants, together with development rights and permits for a third plant, for US$724 million in cash. The portfolio being acquired consists of 932 MW of potential capacity, located on Alpek’s petrochemical sites in the Mexican states of Veracruz and Tamaulipas. 518 MW will be operational by closing, with around 90% of their power plus all steam revenues under long-term contracts. ContourGlobal’s obligation to complete the acquisition is conditional upon this plant successfully completing its commissioning tests and entering into commercial operations. The facility will provide steam production and power output to the adjacent petrochemical plant under a 20-year contract. • Venezuela: France’s Maurel & Prom will invest $400 million to acquire a 40 percent stake in a Venezuela oilfield joint venture called Petroregional del Lago. Maurel & Prom said in a December statement it had agreed to pay 70 million euros ($80.5 million) to buy the stake from Royal Dutch Shell Plc and that it would invest 350 million euros ($402.5 million) in boosting output. The field in 2018 produced around 15,500 barrels per day, Maurel and Prom said in December. Shell in an emailed statement confirmed the sale of its stake to Maurel and Prom. The Lake Maracaibo area has been plagued by frequent theft of equipment and chronic power cuts as Venezuela remains mired in deep recession, hyperinflation and chronic shortages of food and medicine. The Venezuelan Parliament, where the political opposition has an overwhelming majority, has asked foreign companies not to sign agreements with the Maduro government without the approval of the legislature. The government has ignored lawmakers’ warnings since the country’s Supreme Court declared the Parliament to be in contempt and, as a result, the legislature’s decisions are not taken into account by the other government branches, which back Maduro and the country’s leftwing Chavismo political model and ideology.

Appendix – Commodity Pricing Data Brent Crude - month ahead contract (US$ per barrel) Foreign Exchange (Euro/USD)

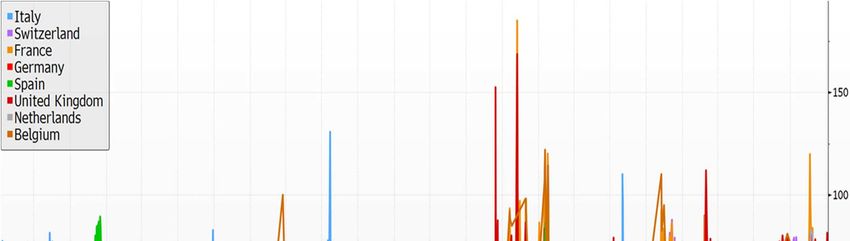

Appendix – Commodity Pricing Data Coal CIF ARA 2019 delivery ($/T) Natural gas prices, “Calendar year 2019” (NBP in £p/therm & TTF in €/MW/h)

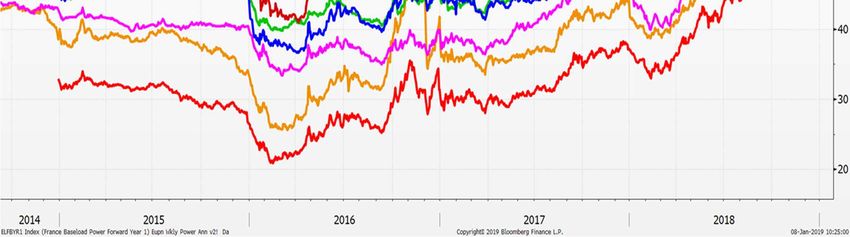

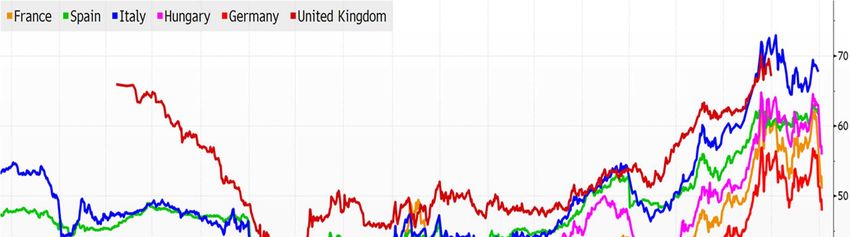

Appendix – Commodity Pricing Data European electricity prices for “Calendar Year 2020” (€/MWh)

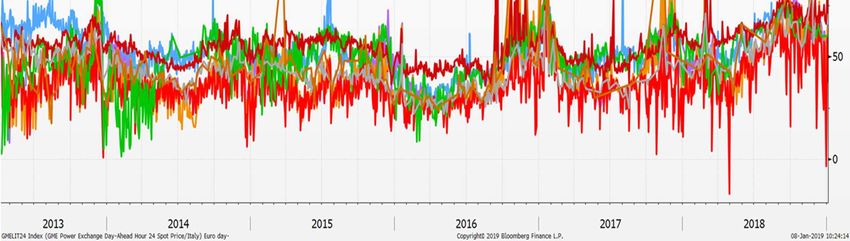

Appendix – Commodity Pricing Data European day ahead electricity prices (€/MWh)

Glossary

Term Definition

Latest unit cost for electricity consumed by industrial users as reported by the U.S. Energy Information

Avg Price Industrial Users

Administration (EIA). The EIA usually publishes the data 4 months after the month of consumption.

The Henry hub in Erath, Louisiana serves as the pricing point for natural gas futures traded on the New

Henry Hub Natural Gas

York Mercantile Exchange (NYMEX).

The reported WTI light crude oil future price is the market determined value of next month’s contract to

either buy or sell in multiples of 1,000 barrels West Texas Intermediate or other light sweet crude oil. WTI

WTI Crude Oil

light crude oil contracts are only executed for physical delivery in relatively few cases but nevertheless they

serve as an important pricing mechanism for contracts that are actually executed for physical delivery.

The Pennsylvania-New Jersey-Maryland (PJM) interconnection functions as a power pool for all or parts of

Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania,

PJM Region Weekday

Tennessee, Virginia, West Virginia and the District of Columbia. The PJM power pool is currently the largest

competitive wholesale electricity market. The price reported here is the price during weekdays.

The Palo Verde switchyard located in Tonopah, Arizona is a key point in the western states power grid and

is used as a pricing point for electricity across the southwest United States. The price reported here is the

Palo Verde Weekday

average market price for peak electricity to be consumed on the next day. Peak hours under this contract

are from Mon – Sat between 0700 – 2200 hours local time.

The market price for a next month delivery of 1liter of ethanol at the mill gate in Sao Palo state as

Brazilian Ethanol

calculated by Cepea.

The market price for a next month delivery of coal in the Amsterdam – Rotterdam – Antwerp (ARA) port

Rotterdam Coal

area.

The market price for one MWh of baseload electricity to be delivered next month as traded on the EPEX

Germany

Spot Market www.epexspot.com.

The market price for one MWh of baseload electricity to be delivered next month as traded on the EPEX

France

Spot Market www.epexspot.com.Glossary

Term Definition

The market price for one MWh of baseload electricity to be delivered next month as traded on the

Spain

trading platform belonging to the Operador do Mercado Iberico de Energia (OMIP).

The market price for one MWh of baseload electricity to be delivered next month as traded on the

Swiss

European Energy Exchange (EEX).

The market price for one MWh of baseload electricity to be delivered next EFA month as traded on the

UK Intercontinental Exchange (ICE). EFA month stands for the specific calendar in use under the Electricity

Forwards Agreement that breaks up the year in equal blocks of 4 and 5 weeks so as to simplify trading.

The Title Transfer Facility (TTF) is a virtual hub that serves as a pricing point for natural gas contracts

TTF within the Dutch gas network. The actual contracts are traded on the European Energy Derivatives

Exchange (ENDEX).

The National Balancing Point (NBP) is a virtual hub that serves as a pricing point for natural gas contracts

NBP

within the United Kingdown. The actual contracts are traded on the Intercontinental exchange (ICE).

The market price for Free on Board (FOB) 180 Centistoke (CST) fuel oil in Singapore port to be delivered

Singapore Fuel Oil

next month.

The reported price for LNG in Japan is derived from the price of West Texas Intermediate (WTI) crude oil

Japan LNG

by means of an index formula and is reported in US Dollar per decatherm.

The market price for one MWh of baseload electricity to be delivered next month in Queensland as

Queensland Baseload Power

traded on the Australian Securities Exchange (ASX).

Brent crude oil is a combination of light crude oil from 15 different oil fields located in the North Sea. Due

Brent Crude Oil to the high quality of Brent crude, it is ideal for making gasoline and middle distillates. As such, Brent

crude forms the pricing benchmark in Europe and Africa.Glossary

Term Definition

The blue line in the graph presents the daily exchange rates Euro to USD while the red line represents the

Foreign Exchange

moving average over the last 14 trading days.

Coal is an important input fuel for electricity generation. The coal price reported in appendix 3 is inclusive

Coal CIF ARA 20XX Delivery of commodity Cost, Insurance and Freight (CIF) from its origin to the ports of Amsterdam – Rotterdam –

Antwerp (ARA) to be delivered next month.

The featured contracts in this graph are for the delivery of natural gas in the UK (NBP), Dutch (TTF) and

German (EEX) markets in the next Calendar year. The benefit of the annual contract is that the buyer has

Natural Gas Price for

an average price throughout the year rather than individual prices for each month that are priced

Calendar 20XX according to market conditions and can show great variances between winter and summer prices. For

further information on the specific country contracts, please refer to the glossary for the world report.

The featured contracts represent the current market price for one MWh of baseload electricity to be

European Electricity Prices delivered next calendar year (except UK) as traded on each of the respective exchanges mentioned as

for Calendar Year 20XX source. The electricity market in the UK features the season contract as its longest contract. As a result,

the reported market price is the average of the nearest summer and winter contracts.

Next to future contracts, each electricity exchange also features a day ahead contract. The day ahead

European Day Ahead contracts are characterized by greater volatility than the monthly and longer period future contracts as

Electricity Prices they are more susceptible to actual supply and demand on the day as well as the other factors

influencing the longer contract prices.Confidential This presentation and the information contained herein is confidential and intended for NUS Consulting Group clients. The material contained herein represents the opinion and views of NUS Consulting Group and is provided to discuss general market activity, industry and sector trends, as well as other broad-based economic, market and political conditions. This information should not be construed as research or investment/purchasing advice. Persons responsible for the purchase of energy for an organisation must consider their organisation’s own objectives, risk tolerance and market forecast when undertaking energy purchasing decisions. The circulation or distribution of this presentation or the information contained herein to persons other than the Intended Entity or its employees is strictly prohibited

You can also read