56 168 Days to PPP Loan Forgiveness - Ellen M. Sas, CPA Roger A. Jones, CPA Anne Smith, EA ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

56 168 Days to PPP Loan

Forgiveness

Ellen M. Sas, CPA

esas@hauserjonesandsas.com

Roger A. Jones, CPA

rjones@hauserjonesandsas.com

Anne Smith, EA

asmith@hauserjonesandsas.com

Jiyon Han, CPA

jhan@hauserjonesandsas.com

Jennifer Roberts, CPA

jroberts@hauserjonesandsas.com

DISCLAIMER: Please note that the situation surrounding COVID-19 and the PPP Loan

Program is constantly evolving. The subject matter discussed in today’s webinar is

subject to change. Please contact us at Hauser, Jones & Sas for timely advice.

Ellen M. Sas CPA

Managing Partner

Ellen is the managing partner at Hauser Jones & Sas and

one of its founders.

A recognized Banking expert. Ellen has served as the CEO

of two independent community banks, as the VP of Internal

Audit of a $5 billion commercial bank, and as a special

consultant to more than a dozen community banks and

investment bankers.

Ellen is a member of the AICPA and a member of the

Institute of Internal Auditors, serves on the Board and

Finance/Audit Committee Chair of Whistler Twin Peaks,

and has been a member of the governing board of many

different nonprofit organizations in varying capacities for

many years.

A Puget Sound native, Ellen graduated from the University

of Washington with a Bachelor’s degree in Accounting.

Ellen is married and the mother of six kids, the oldest of

eleven siblings and enjoys nine grandkids.

Roger A Jones, CPA

Founding Partner

Roger is one of the founding partners of Hauser Jones &

Sas and emphasizes strategy, business owner succession,

mergers and acquisitions, complex audits, and transactional

tax strategies.

Roger is instrumental in providing the firms Business

Owner Succession Services and leads the firm’s small

business outreach efforts.

Roger is a member of the AICPA, the WSCPA and a

member of the Institute of Internal Auditors.

A Puget Sound native, Roger graduated from the

University of Washington with a Bachelor’s degree in

Accounting.

He is married and the father of six kids, the youngest of 7

siblings and enjoys nine grandkids.

Anne Smith, EA

Client Accounting Services Manager

Anne joined the team in 2015 and has worked in the tax

and accounting industry for 25 years. She has worked in

both public and private accounting, assisting local

business with their accounting, procedures, planning and

reporting.

Anne is experienced in day to day accounting, payroll,

state agency filings, state agency audits, business and

personal tax reporting. She has a wide range of

experience assisting local businesses to develop

accounting systems and procedures, and consulting

businesses throughout all phases from business start-ups to

planning for the sale of closely held businesses.

Anne is an IRS Enrolled Agent and a member of

Washington Society of Certified Public Accountants

Anne graduated from University of Phoenix with a

Master’s Degree in Business and Accounting.

Anne lives with her husband and dogs and enjoys

remodeling her home and training agility.

Jiyon Han, CPA

Senior Tax Manager

Jiyon received her BA from Yonsei University in Korea

before relocating to Seattle.

Her practice encompasses tax and consulting services for

various types of business entities as well as high net worth

individuals.

She represents and supports clients during IRS

examinations. Since starting her career in 2000, she has

built a portfolio of clients in a wide range of industries

including professional service, construction, real estate

investment, restaurant and manufacturing.

Jiyon lives with her husband and two children in

Sammamish and enjoys watching pro sports in addition to

her children’s games.

Jennifer Roberts, CPA

Senior Tax Manager

Jennifer joined Hauser, Jones & Sas in 2017. She has

more than 20 years of experience in the financial industry.

Her favorite part of being a CPA is the ability to work

directly with people and their businesses; helping with

their tax planning and consulting needs.

Jennifer leverages her prior experience as an IRS auditor

by representing her clients throughout the entire IRS audit

process, allowing her to help resolve numerous issues.

She has also worked with several attorneys to assist with

specialized accounting projects required to help resolve

legal cases involving partnerships, estates and trusts.

Jennifer lives in her hometown in Kirkland, WA.

She graduated from the University of Washington with a

Bachelor’s degree in Accounting.

ABOUT HAUSER JONES AND SAS, PLLC

Team of 27 FTE with 2 offices

[Bellevue & Puyallup] We Serve Individuals, Small

Business, and Not-for-Profits

Serving Clients primarily in WA,

CA, OR, AK, ID Ownership succession services

Tax Compliance

Tax Strategy [Planning]

Audits & Reviews

Consulting & Forecasting

Internal Audit & Compliance

Client Acctg. Services (CAS)

Strategic Planning

Executive Services

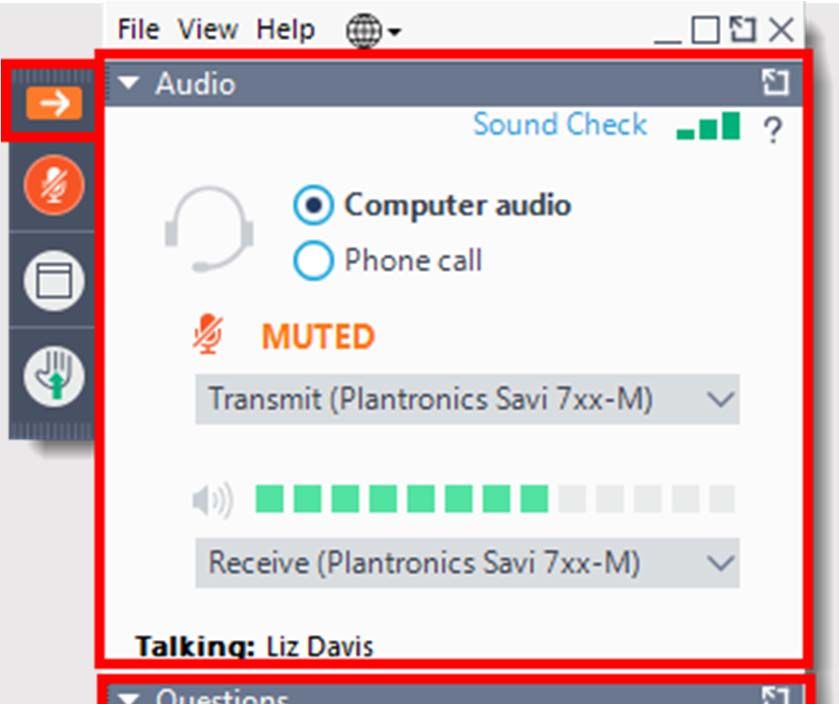

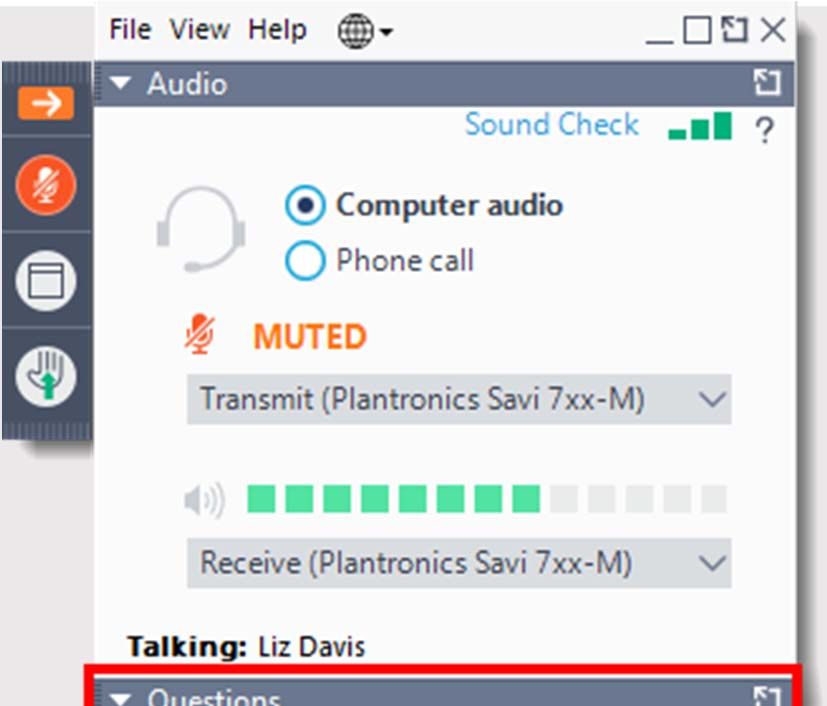

HJS GoToWebinar Housekeeping: Attendee Participation

Your Participation

Open and close your control panel

Click on triangles to expand different

sections on the control panel.

HJS GoToWebinar Housekeeping: Attendee Participation

Your Participation

Join audio:

• Choose Mic & Speakers to use VoIP

• Choose Telephone and dial using the

information provided

HJS GoToWebinar Housekeeping: Attendee Participation

Your Participation

• You can submit questions in writing in

the “Questions” box.

• You are encouraged to submit your

questions throughout the webinar.

• We will collect your questions and

address them in a Q&A session after

the presentation, at the end of this

session.56 Days to PPP Loan Forgiveness - Agenda 1. SBA Loan Forgiveness Application 2. Tips for Use of PPP Funds 3. PPP Loan Forgiveness Limitations 4. Self-Employed Loan Forgiveness 5. Planning and Documentation 6. Unanswered Questions 7. Q&A

56 Days to PPP Loan Forgiveness

IMPORTANT - Know date your PPP loan was funded

• PPP Application – was for 2.5 months or approx. 76 days

• PPP Covered Period = 56 Days 168 Days

• Forgiveness still needs careful planning

• Only 56 168 days starting on loan origination date

• Not based on first date funds were wired/withdrawn

• Example: If your loan was funded on a Wednesday, covered

period will end on a TuesdayNow More Likely that All Will Be Forgiven • PPP Application – was for 2.5 months or approx. 76 working days • “Covered Period” = 56 days Now 168 days • = 26% will be “ Unforgiven”

We’ve Hired Mathematicians on Staff

SBA Loan Forgiveness Application

SBA Loan Forgiveness Application

Reuters Forgiveness Calculator

AICPA Forgiveness Calculator

https://future.aicpa.org/resources/to

olkit/paycheck-protection-program-

resources-for-cpasForecasting to Maximize Loan Forgiveness

• Forecasting will help you understand what strategies you will

need to perform and documentation to track.Forecasting to Maximize Loan Forgiveness

• The PPP forgiveness rules and limitations are complex

• It is very important to forecast how you will spend your PPP

funds prior to the end of your 8-week 24-week covered period

• May need to make adjustments to payroll to meet 75%

60% requirement

• May need to consider rehiring additional employees

• May need to do stub payroll at end of covered period

• Forecasting will help you understand what details you will

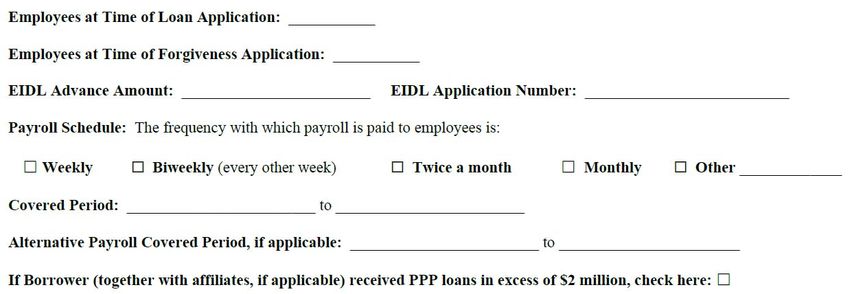

need to track, and what you won’t need to spend time onLoan Forgiveness Application Documentation • Required documentation may vary depending on lender: • PPP loan forgiveness calculation form • PPP Schedule A • FTE • Payroll Costs • Nonpayroll Costs • PPP Schedule A Worksheet (not required to submit) • Required to maintain records for 6 years from date of forgiveness

Loan Forgiveness Application Process

• Application must be submitted by:

• Borrower must submit complete application for forgiveness

• Can apply as soon as you’re ready

• Forgiveness application expires 10/31/2020 10/31/2021?

• Within 10 months after the last day of the covered period

(last possible day for principal and interest pymts to start)

• Lender has 60 days to review and decide on forgiveness

• SBA has 90 days to review forgiveness application

• Borrowers have 30 days to appeal resultsTips for Use of PPP Funds • Must be used for eligible costs • See loan agreement • Payroll costs to retain employees • Non-payroll costs • Business mortgage interest payments • Business rent or lease payments • Business utility payments • Covered period and Alternative payroll covered period • “Paid and/or incurred during the Covered period”

Tips - Qualified Payroll Costs • Maximum gross payroll for any one employee : $15,385 • $46,154? However, owners still limited to prior year - pro rata • Gross wages including: • Salaries & Wages, Commission, Cash tip, Vacation pay • Parental, family, medical, or sick leave, if not used for tax credit • Allowance for dismissal or separation included in gross wages • Provisions for group health care benefits • Retirement benefits for group retirement plan • State or local tax assessed on the compensation of employees

Tips - Qualified Non-Payroll Costs • Obligation or service began prior to February 15, 2020 • Interest on mortgage obligations on real or personal property • Rent and lease payments for real or personal property • Payments on business utilities • Electricity, gas, water • Transportation (interpreted as fuel for business vehicles) • Telephone • Internet

PPP Loan Forgiveness Limitations

• 75% 60% Requirement - At least 75% 60% of the potential

forgiveness amount must be for payroll costs

• Now a cliff? All or none?

• Funds used for non-payroll costs greater than 25% 40% of total

forgiveness amount will have to be paid back.

• Additional limitations apply:

• Full-Time Equivalency (FTE) Reduction

• Salary/Hourly Wage Reduction

• Safe harbors available75% Requirement - Example

• Example: Jeff’s PPP loan was $100,000

• To get full forgiveness, Jeff must spend at least 75% 60% of his

PPP loan on payroll costs ($100,000 x .60 = $60,000)

• Jeff can spend more than 75% 60 of his loan on payroll costs

• Jeff can spend up to 25% 40% of loan on qualified non-payroll

costs

• This is not all or none – if Jeff spends less than 75% 60% of

loan on payroll costs, forgiveness will be limited75% 60% Requirement – Limitation Example

• If Jeff spends less than 75% 60% of PPP loan on payroll costs, the

amount allowed for qualified non-payroll costs will be limited

• Jeff spent $56,000 on payroll costs, $40,000 non non-payroll costs

• Jeff’s non-payroll costs are limited to 40% of loan amount:

• $100,000 Loan Amount

• $ 56,000 Payroll Costs (Minimum required $60k)

• $ 40,000 Non-Payroll Costs (Maxed out at 40% of $100k)

• $ 4,000 Left Over

*IMPORTANT – May not qualify for ANY forgiveness if

cliff requires minimum of 60% for payroll costsHeadcount Compliance

FTE Reduction Calculation • Avg number of hours per week / 40 then round up. • Step 1 - Avg FTEs for 8-week 24-week covered period for PPP loan • Step 2 - Pick lesser FTE’s in two base periods. • Avg FTE 2/15/19 – 6/30/19 • Avg FTE 1/1/20 – 2/29/20 • Step 3 - Calculate FTE % • [ FTEs (8-wk covered period) ÷ FTEs (lesser of 2 base periods)] • Step 4 - Calculate revised debt forgiveness • FTE % x forgivable costs • FTE Reduction Exception & documentation

FTE Reduction Calculation - Example Example – Step 1 Calculate Average FTEs in Base Period: If you had 10 full-time employees (over 40 hours) and 8 part-time employees each with 20 hours, your FTE would be: • 10 + ((8 x 20) / 40) = 10 + 4 = 14 FTEs Example – Step 2 Determine Lesser of FTEs in Two Base Periods: 15 = Average FTE 2/15/19 – 6/30/19 14 = Average FTE 1/1/20 – 2/29/20 • 14 = Selected Lesser FTE from Two Base Periods

FTE Reduction Calculation - Example

Example – Step 3 Calculate FTE Reduction Quotient:

• No FTE Reduction Required:

• If you had 10 FTE in the covered period and 10 FTE in the base

period, there would not be an FTE Reduction in loan forgiveness.

• FTE Reduction Required:

• If you had 10 FTE in the covered period; but had 14 FTE in the base

period, there would be an FTE Reduction in the forgiveness amount

• 10 FTE covered period /14 FTE base period = 71.4%

• 71.4% = FTE Reduction QuotientFTE Reduction Calculation - Example Example – Step 4 Calculate Modified Debt Forgiveness Amount: $30,000 Forgivable Costs 71.4% FTE Reduction Quotient $21,420 Modified Debt Forgiveness

Wage Compliance

Before and After

Wage

ComparisonSalary/Hourly Wage Reduction Calculation • Measured per each employee (only wages under $100K) • Step 1 – Determine if pay was reduced > 25% between two periods • Base period 01/01/20 – 3/31/20 • Avg pay for the covered or APCP • Step 2 – Compare avg pay for three periods – safe harbor a. Avg annual pay as of 2/15/20 b. Avg annual pay between 2/15/20 and 4/26/20 c. Avg annual pay as of 6/30/20 12/31/2020 If b or c is greater than a, safe harbor is met. No reduction. If not, Step 3. • Step 3 – Determine reduction in excess of 25%

Salary/Hourly Wage Reduction Calculation Example – No Wage Reduction: • Employer paid Suzie $50,000 average salary in the prior quarter • Prior quarter is 1/1/2020 – 3/31/2020 • If employer pays Suzie the equivalent salary of at least 75% or $37,500 in the covered period, there will not be a wage reduction • 75% x $50,000 = $37,500

Salary/Hourly Wage Reduction Calculation

Example – Wage Reduction Applies:

• Employer paid Suzie $50,000 average salary in the prior quarter

• Prior quarter is 1/1/2020 – 3/31/2020

• If employer pays Suzie less than 75% of prior wages in the covered

period, the shortage may impact the loan forgiveness amount by the

amount of reduction over 25%.

• Potential reduction on loan forgiveness:

$37,500 75% x $50,000

$30,000 Less Actual wages paid

$ 7,500 Potential reduction in loan forgivenessLimitations Combined

Self-Employed Loan Forgiveness Curveball

• Still many unanswered questions regarding what “other costs” will

qualify for forgiveness.

• Maximum amount for the payroll replacement is $15,385 before

qualified non-payroll cost.

• Example – 56 Day Issue:

$20,833 Loan Amount (Equivalent to $100k max salary)

($15,385) Payroll Replacement (Maximum allowed)

($ 5,129) Other Qualified Costs (Unused portion must be paid back)

$ 319 Curveball – Does Not Qualify for ForgivenessSelf-Employed Loan Forgiveness Home Run! • Still many unanswered questions regarding what “other costs” will qualify for forgiveness. • Maximum amount for the payroll replacement is $15,385 $46,154 before qualified non-payroll cost. • Example – 56 Day Issue: $20,833 Loan Amount (Equivalent to $100k max salary) $46,154 Payroll Replacement (New maximum allowed) *ALL FORGIVEN, NO NEED FOR OTHER COSTS

Self-Employed – the unforgiven

• No Raises Allowed for Self-Employed

• Lower of $15,385

or

• Prorated amount based on 2019 Schedule C line 31

• Example: 2019 Schedule C Line 31 was $80,000

$16,668 Loan Amount (($80k / 12 months) x 2.5 months)

($12,312) Payroll Replacement ($80k / 52 weeks x 8 weeks)

($ 4,104) Allowed for Other Qualified Costs (1/3 of allowed payroll)

$ 252 UnforgivenSelf-Employed – the Forgiven

• No Raises Allowed for Self-Employed…But 24 Weeks Now:

• Lower of $15,385 $46,154

or

• Prorated amount based on 2019 Schedule C line 31

• Example: 2019 Schedule C Line 31 was $80,000

$16,668 Loan Amount (($80k / 12 months) x 2.5 months)

$36,923 Payroll Replacement ($80k / 52 weeks x 24 weeks)

*ALL FORGIVEN, NO NEED FOR OTHER COSTSForecasting to Maximize Loan Forgiveness

• The PPP forgiveness rules and limitations are complex

• It is very important to forecast how you will spend your PPP

funds prior to the end of your 8-week 24-week covered period

• May need to make adjustments to payroll to meet 75% 60%

payroll cost requirement

• We are here to help!Unanswered Questions - PPP Loan Forgiveness What we don’t know for sure: Q: Can I prorate prepaid expenses paid prior to the funding but covers part of the PPP period? Q: How does EIDL grant impact PPP loan forgiveness? Q: What does “Transportation” mean under allowed “Other Costs”?

Unanswered Questions - PPP Loan Forgiveness What we don’t know for sure: Q: Can garbage/trash collection be included in utilities? Q: Do utilities allocated to Schedule C for business use of home count? Q: Can I count lease payments and interest for business vehicle(s)?

Unanswered Questions - PPP Loan Forgiveness What we don’t know for sure: Q: Can I pay employer retirement contribution for 2019 during the covered period and does it count toward payroll costs? If so, 100% or prorated? Q: Can S Corp owner-employee use PPP funds for SEP contribution? Q: Does health insurance for S Corp owner count toward the payroll cost? Q: Will the 8-week covered period be extended? YES!

Attendee Questions

PPP Loan Forgiveness – Q&A Q: Does health insurance for self-employed or partners in a partnership count towards payroll costs? A: No Q: When does Alternative payroll covered period start? A: The first full payroll period after the date of funding. Only applies to weekly and bi-weekly payrolls Q: Do HSA employer payments count toward payroll costs? A: Yes Q: Can I deduct expenses that are eligible for forgiveness on my taxes? A: No

PPP Loan Forgiveness – Q&A Q: How many hours qualify as one FTE? A: 40 hours Q: How are you supposed to round FTE count? A: Round up to the 10th or just use .5 FTE Q: What if an employee won’t come back? A: Does not count towards forgiveness calculation Q: Do bonuses or increases in compensation count as payroll costs? A: Yes

PPP Loan Forgiveness – Q&A

• Q: Will I need to prove that I needed the funds and properly

qualified for the PPP loan?

• A: A safe harbor was put in place by SBA that deemed certification for

loans under $2M, assumed in good faith.

• Q: Will I need to prove that I needed the PPP loan if my loan

amount was greater than $2 million.

• A: Loans > $2M : Borrowers may still have an adequate basis for

making the required good faith certification based on individual

circumstances. Loans greater than $2 million will be audited for need by

the SBA.We Have Answers -

Feel free to contact any of us at HJ&S. Also feel free to

schedule an appointment for individual consultation.

425-889-1778.

More information at our website:

www.hauserjonesandsas.com

Ellen @ 253-370-7524 or esas@hauserjonesandsas.com

Roger @ 425-890-4932 or rjones@hauserjonesandsas.comThe HJ&S Team is Here to Help!

DISCLAIMER: Please note that the situation

surrounding COVID-19 and the PPP Loan Program

is constantly evolving. The subject matter discussed

in today’s webinar is subject to change. Please

contact us at Hauser, Jones & Sas for timely advice.

www.hauserjonesandsas.comThank You!!

Ellen M. Sas, CPA

esas@hauserjonesandsas.com

Jennifer Roberts, CPA

jroberts@hauserjonesandsas.com

Jiyon Han, CPA

jhan@hauserjonesandsas.com

Roger A. Jones, CPA

rjones@hauserjonesandsas.com

Anne Smith, EA

asmith@hauserjonesandsas.comYou can also read