A Tale of Two Markets: Gulf Coast & the Rest - S&P Global Platts

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Bradley Olsen

bolsen@tudorpickering.com

(713) 333-7693

A Tale of Two Markets: Gulf Coast & the Rest

Northeast, Canadian Markets Cut Off From Export Boom

Platts NGL Conference: September 29, 2014 – Houston, TX

**IMPORTANT DISCLOSURES BEGIN ON PAGE 18 OF THIS REPORT**

After 2011-2013 NGL Tidal Wave…

Belvieu prices set to improve: With LPG exports ramping,

Belvieu prices improve steadily through 2018. Ethane cracking

& exports improve price through 2020 and beyond.

Northeast, Canadian markets lack access to Gulf: Pricing will

be weak. East and West Coasts need a different escape hatch

— export projects, pipes will take longer.

Currently waiting on long-haul pipes: Liquid USGC NGL

markets more attractive to petchems vs. Canadian and

Northeast markets. E&Ps are nervous about oversupplying

USGC, so are slow to subscribe to large-scale projects.

USGC pricing will improve steadily 2014-17: NGLs hit 50%

before ethane exports drag Belvieu pricing to 55% of WTI by

2020. Meanwhile, Northeast NGLs likely to remain around 20-

25% of WTI until pipes arrive, if they arrive.

2

With Oil at $90/bbl, US NGL Supply Growth is Inelastic

Gas Price Required for 10% ATROR with NGL Sensitivity

$6.00

$6.00

NGLs from gas stream:

2.9 MMBPD April 2014

$5.00

$5.00

4.3 MMBPD TPHe 2020

$4.00

$4.00

+1,800 MBPD growth

through 2020

$/mcf

$/mcf

$3.00

$3.00

~1,650 rigs, active ~250 marginal rigs active

with gas >$3/mcf

$2.00

$2.00

~400 MBPD declines

$1.00

$1.00 through 2020

$0.00

$0.00

NGL Assumption

*Economics assume $87/bbl WTI

30% WTI 40% WTI

Source: TPH Research

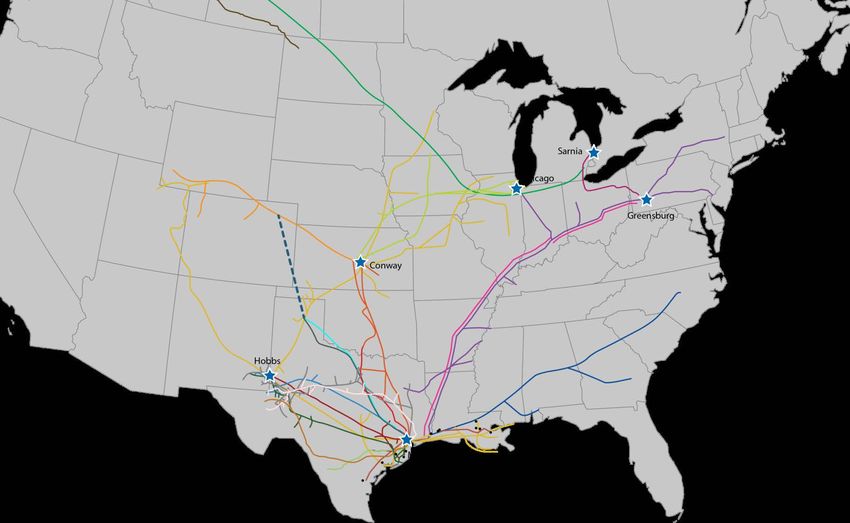

Distance, Economics have cut off NE & Canada from Belvieu

Edmonton

~200 MBPD proposed LPG

Canada’s main C3 export Exports (vs. >400 supply)

line has been reversed. ~140 MBPD proposed C2

Exports

Philadelphia

EPD - ATEX (TE Prods Reversal)

EPD - TE Products (Belvieu-Chicago-Northeast)

EPD – MAPL (Rockies-Permian-Conway-Midwest)

Pipes to Gulf are

EPD – Dixie (Belvieu-Southeast)

EPD – Various NGL Pipes (S. TX-E. LA)

EPD – Seminole (Permian-Belvieu)

ethane only, offering

EPD – Chaparral (Permian-Belvieu)

EPD – Skelly-Belvieu (TX Panhandle-Belvieu) poor netbacks.

EPD/EEP/APC/DCP – Texas Express* (TX Panhandle-Belvieu)

OKS – Bakken Pipeline (Bakken-Rockies)

OKS – Overland Pass (Rockies-Midcon)

OKS – Sterling (Midcon-Belvieu)

OKS – Arbuckle (Midcon-Belvieu)

All roads lead to the

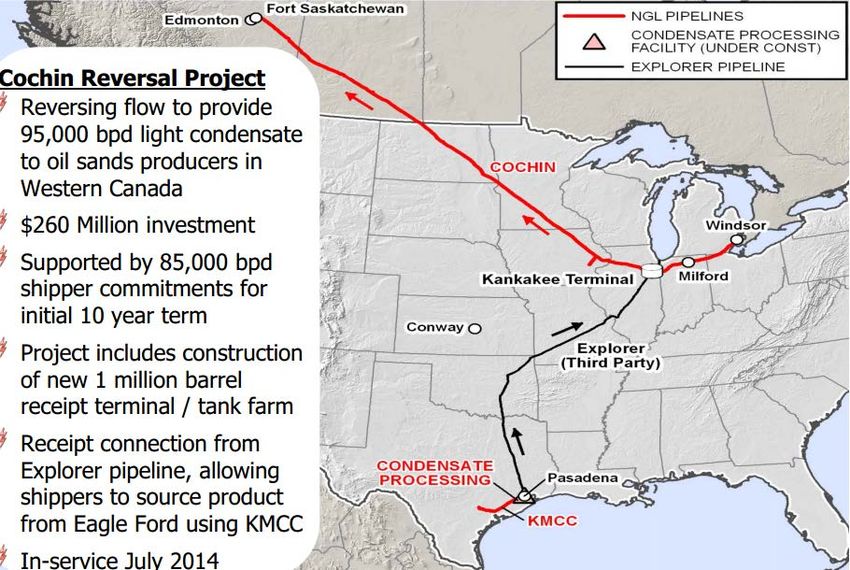

KMP – Cochin (Edmonton-Midwest-Sarnia)

EPD – Eagle Ford (Eagle Ford-Belvieu) Gulf Coast…pending

OKS – North (Conway-Midwest-Chicago)

COP – Line EZ (Permian-Belvieu)

CVX – W. Texas LPG (Permian-Barnett-Belvieu)

Northeast &

ETP/RGP – Lone Star NGL (Permian-E. Texas-Belvieu)

ETP/RGP – W. TX Gateway (Permian-Eagle Ford-Belvieu)

SXL/MWE – Mariner West (Marcellus-Sarnia)

Canadian exports.

PBA – Vantage Pipeline (Bakken-Alberta)

EPD/APC/DCP - Front Range* (DJ Basin-TX Panhandle)

DCP – Southern Hills (Midcon-Belvieu)

DCP - Wattenberg Pipeline (Rockies-Midcon) ~1,140 MBPD Proposed LPG Exports

DCP – Sand Hills (Permian-Eagle Ford-Belvieu)

DCP – Black Lake (E. LA-Belvieu)

SXL – Mariner South (Belvieu-Nederland)

~ 800 MBPD Petchem Demand for C2 & C3

SXL – Mariner East (Marcellus-Marcus Hook Export)

ETP – Justice NGl (S. TX-Belvieu) ~67% Demand Growth By 2020 4

Northbound Diluent Strands Canadian NGLs

Canada— cut off by

pipe conversions to

diluent.

Only outlets for

Canadian NGLs are

export projects on

West Coast.

Canadian/Pac NW LPG Export Projects

In absence of pipe to Project Operator Startup LPG (MBPD)

Idemitsu/Altagas Ferndale, WA Petrogas 2015 20

West Coast, Longview, WA Sage Q4 2016 45

Canadian projects Portland, OR Pembina 2018 37

rely on high-cost rail Total NGL/LPG Exports 102

% of Total NAM LPG Capacity 7%

transportation.

5

Source: Company Presentation

NORTHEAST OVERSUPPLY

PIPELINE SCARCITY ENSURES RAIL &

TRUCKING SET MARGINAL PRICE FOR

FORSEEABLE FUTURE

6

Battle for NE C3+: ~700 MBPD Proposed, 40 Committed

3-4 Projects Compete for Heavy NGL Volumes

2-3 pipes to USGC: 2 y-grade, 1 propane Philadelphia

1 pipe to Philly: purity NGLs/other Pro: Cheaper pipe cost, less LPG traffic

Con: Likely higher cost fractionation

capacity, higher cost to Asia

What’s at stake?

Projects still leave NE long NGls, price

set by cost of shipping to USGC.

With >600MBPD of future ethane and

US Gulf Coast >500MBPD future C3+ production,

Pro: Liquidity, storage, world-scale docks market will require multiple C3+

Con: limited ex-ethane LPG demand growth solutions; today none are finalized.

7

Never say never but…

Ethane in Northeast Will Never be Economic

ATEX Contracting

ATEX ethane netback has

been

While Waiting for Takeaway, NE NGL Discounts Will Widen

Northeast NGL markets will see discounts of $20 or netbacks of>10 bcf/d Processing Produces ~1.1 MMBPD of NGLs by 2017…

Northeast wet gas processing capacity will nearly double from beginning of 2014 to

YE 2015 to approximately 10 bcf/d based on announced newbuild and expansion

projects.

12

1 Bcf/d of incremental

processing capacity announced

10

YTD in the Utica, with 0.6

Bcf/d in the Marcellus

Processing Capacity (mmcf/d)

8

6

4

2

0

Dec 13 Dec 14 Dec 15 Dec 16

MWE Marcellus WMB Caiman Blue Racer/DOM XTO Marcellus

MWE/EMG Utica M3/Access Utica NI Utica KMP Utica

Source: Company Presentations, Public Filings, TPH Estimates 10GULF COAST DEMAND

>$100B OF MEGAPROJECTS ON GULF

COAST DRIVES DEMAND FROM PETCHEMS &

EXPORTS THROUGH END OF DECADE

11~800 MBPD Growth in US Ethane Cracker, PDH Demand by 2020

1,400

PDH Projects Tentative projects

1,200 could add additional

Cracker Newbuilds ~400MBPD of demand

Ethane/Propane Demand (MBPD)

1,000 near end of decade.

Cracker Expansions

800 Potential Newbuilds

600

400

200

0

2013 2014 2015 2016 2017 2018 2019 2020 2021

WMB Geismar LYB Midcon LYB Corpus Christi

LYB La Porte DOW Freeport 7 WLK Lake Charles/Calvert City

INEOS Chocolate Bayou DOW Plaquemine BASF Port Arthur

Formosa DOW Freeport 8 XOM Baytown

OXY Ingleside CPC Texas DOW Freeport Newbuild

SSL Louisiana Ascend TX- PDH 2015 EPD - PDH 2016

DOW - PDH 2015 DOW - PDH 2018 Formosa TX - PDH 2017

Potential Demand

*Potential demand includes estimates for Axiall/Lotte, Shell, Odebrecht, Shin-Etsu, & 12

Williams projects.LPG Exports Set to Increase >1MMBPD through 2020

LPG Export Capacity (MBPD)

1,600

1,400

Total Arabian Gulf

1,200 Exports

1,000

800

Qatar, world’s

600 current #1 exporter

400

200

0

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Dec-18

EPD Targa EPD 2013 Expansion Targa Sept 2013 Expansion

Targa Q3 2014 Mariner East I EPD 2015 Expansion Mariner South

OXY Corpus EPD Phase 2: OTI PSX Sweeny Terminal Mariner East II

Gulf Coast Blue Northeast Red

13

Source: Company Releases>$100B in Gulf Coast export projects before 2020

Project Invest. ($B) Capacity Labor In-service Project Invest. ($B) Capacity Labor In-service

Golden Pass 10.0 2.6Bcfd 3,500 2018 Trunkline LNG 11.0 2.4Bcfd 4,000 2019

Sabine Pass LNG Terminal 6.0 2.6Bcfd 3,500 2015

Cameron LNG 9.5 1.7Bcfd 3,500 2019

Mariner S. PL & Terminal 0.4 200MBPD 750 2015

Various Fractionators 0.5 200MBPD 400 2014

Huntsman EO Exp. 0.1 132.5MTPA 325 2015

Total $16.5 8,075 Beaumont Axiall/Lotte Cracker

Sasol Cracker

3.0 1000MTPA

6.0 1500MTPA

2,500

7,000

2018

2017

$17B Total $30.0 17,400

8,100 Lake

Houston Jobs Charles

$40B $27B

17,400 Jobs

39,000 Jobs

Corpus Christi Project Invest. ($B) Capacity Labor In-service

$16B Freeport LNG 14.0 2Bcfd 3,500 2018

Targa Terminal Exp. 0.3 100MBPD 188 2014

9,200 Jobs Enterprise LPG Export 0.6 264MBPD 300 2015

Enterprise Ethane Export 1.0 240 MBPD 400 2016

PSX Sweeny Hub 3.0 100MBPD 350 2015

Dow Cracker 1.7 1650MTPA 4,800 2017

Kinder Condensate Hub 0.4 100MBPD 300 2015

Project Invest. ($B) Capacity Labor In-service

Exxon Cracker 6.0 1500MTPA 10,000 2017

OxyChem Cracker 1.0 600MTPA 1,700 2015

Lyondell Cracker Exp. 0.4 363MTPA 667 2015

Formosa Cracker 2.0 1600MTPA 2,500 2016

Dow PDH 1.3 800MTPA 2,000 2015

Lyondell Cracker Exp. 0.4 363MTPA 731 2015

Enterprise PDH 1.3 800MTPA 2,000 2016

Various Fractionators 1.0 260MBPD 400 2015 Various Fractionators 4.0 800MBPD 2,500 2015

Oxy NGL Export 1.0 110MBPD 350 2015 Ascend PDH 1.2 1000MBPD 2,000 2015

Cheniere NGL 10.5 2.6Bcfd 3,500 2018 CP Chemical Cracker 6.0 1650MTPA 10,000 2017

Total $15.9 9,181 Total $41.2 39,005

14

Source: Company Presentations, Public Filings, TPH Estimates, Press ReleasesExports cheaper, shorter lead time vs. petchems

PDH Facility LPG Export Dock Ethane Cracker C2 Export Dock

Total Capital Cost ($mm) Total Capital Cost ($mm)

Low End $1,100 $250 Low End $5,000 $750

High End $1,700 $550 High End $7,000 $1,250

Capital Cost/MBPD of Propane ($mm) Capital Cost/MBPD of Ethane ($mm)

Low End $44.5 $2.5 Low End $58.8 $3.8

High End $55.8 $3.0 High End $73.7 $5.0

Range of IRRs Range of IRRs

Low End 24.2% 16.5% Low End 9.4% 8.4%

High End 37.4% 42.0% High End 29.7% 14.3%

Time for Approvals/Construction (Months) Time for Approvals/Construction (Months)

Low End 42 18 Low End 48 24

High End 60 24 High End 72 30

Export facilities offer comparable economics to petchem

new-builds while requiring less than half of the allotted time

to progress through approvals and construction.

Reduced lead time gives export projects advantage in

capitalizing on arbitrage opportunity between US & global

prices.

15Ethane exports always made sense… on paper. Why now?

TPHe Ethylene Gross Margin by Feedstock, Cents/Lb

65

Cents per Lb of Ethylene Produced

60

55.2

55

50 46.6

45

44.0

40.0 Potential 20-25¢ uplift

40

for foreign petchems

35

(ex-capital cost)

30

25

20.9 20.3

20

15

MB Ethane MB Propane US Export Ethane US Export Propane AG Propane Naphtha

(27c/gal, $200/t) (110c/gal, $550/t) (54c/gal, $396/t) (137c/gal, $684/t) (153c/gal, $765/t) (257c/gal, $917/t)

Why the delay?: Ethane docks are more expensive than propane docks, while ethane-

importing facilities are relatively scarce. SXL and EPD made clear that ethane exports are a

“when” not an “if”, leading more global facilities to declare interest in US ethane. Margins

look similar for exported ethane and exported propane. In reality, consumers may find it

easier to secure US ethane on commercial terms. Producers are willing to sell price-indexed

ethane over lengthy terms, while propane sales have reflected AG, rather than MB pricing.

16NE, Canada Left out as Belvieu Recovers…

Multi-year NGL price improvement starts this winter

with LPG exports, while ethane exports tighten the

market in 2017 and beyond.

Northeast and Canadian NGL markets lack pipe

access to the Gulf.

Rail provides export access for Canadian NGL

producers.

Northeast NGL producers have yet to commit to a

large-scale takeaway solution; 3 major projects

have been proposed.

Gulf Coast price advantage is likely to persist as the

location of more than 90% of proposed NGL

export/consumption projects.

17Price Target Methodology:

Analyst Certification: In valuing midstream companies, we use a variety of valuation methods to derive our

I, Brad Olsen do hereby certify that, to the best of my knowledge, the views and price target, including sum-of-the-parts (SOTP) valuations based on comparable

opinions in this research report accurately reflect my personal views about the publicly traded companies, discounted cash flow (DCF) models and dividend discount

company and its securities. I have not nor will not receive direct or indirect models. We use dividend discount models to value more income-oriented vehicles,

compensation in return for expressing specific recommendations or viewpoints in this such as MLPs. Dividend discount rates can vary from 7% to 12% depending on our

report. perception of business risk. We will typically use SOTP and DCF to value C-corporation

structures. We will also use dividend discount models as a secondary methodology for

Important Disclosure: valuing C-corporations, generally using lower dividend discount rates than we use for

The analysts above (or members of their households) have a long stock position in our MLP price targets, given C-corps’ lower payout ratios and lower reliance on

Anadarko Petroleum, Arch Coal Inc., EQT Corp., Huntsman Corporation, Phillips 66, outside capital markets.

Potash Corporation, Teekay Corporation, Teekay LNG Partners, and Teekay Offshore

Partners. John E. Lowe, Senior Executive Advisor at Tudor, Pickering, Holt & Co., also OTHER DISCLOSURES:

serves as a member of the board of directors of Phillips 66 and Apache Corporation.

Trade Name

Ratings: B = buy, A = accumulate, H = hold, T = trim, S = sell, NR = not rated Tudor, Pickering, Holt & Co. is the global brand name for Tudor, Pickering, Holt & Co.

Securities, Inc. (TPHCSI) and its non-US affiliates worldwide.

For detailed rating information, distribution of ratings, price charts and other

important disclosures, please visit our website at www.tudorpickering.com. To Legal Entities Disclosures

request a written copy of the disclosures please call 800-507-2400 or write to Tudor,

Pickering, Holt & Co. Securities, Inc. 1111 Bagby, Suite 5000, Houston, TX 77002. U.S.: TPHCSI is a member of FINRA and SIPC. U.K.: Tudor, Pickering, Holt & Co.

International, LLP is authorised and regulated by the Financial Conduct

Buy – The stock should be purchased aggressively at current prices. The stock has Authority. Registered in England & Wales, Financial Services Register number

among the best combination of risk/reward and positive company specific catalysts OC349535. Registered Office is 5th Floor, 6 St. Andrew Street, London EC4A 3AE

within the sector. Stock is expected to trade higher on an absolute basis and be a top

performer relative to peer stocks over the next 12 months. Canada

Accumulate – The stock should be purchased consistently at current prices. The stock The information contained herein is not, and under no circumstances is to be

has above average risk/reward and is expected to outperform peer stocks over the construed as, a prospectus, an advertisement, a public offering, an offer to sell

next 12 months. securities described herein, or solicitation of an offer to buy securities described

Hold – Do nothing with the stock at current prices. The stock has average risk/reward herein, in Canada or any province or territory thereof. Any offer or sale of the

and is expected to perform in line with peer stocks over the next 12 months. securities described herein in Canada will be made only under an exemption from the

requirements to file a prospectus with the relevant Canadian securities regulators and

Trim – The stock should be sold consistently at current prices. The stock has below only in the relevant province or territory of Canada in which such offer or sale is

average risk/reward and is expected to under perform peer stocks over the next 12 made. The information contained herein is under no circumstances to be construed as

months. investment advice in any province or territory of Canada and is not tailored to the

Sell – The stock should be sold aggressively at current prices. The stock's risk/reward needs of the recipient. To the extent that the information contained herein

is skewed to the downside with possible negative company specific catalysts or references securities of an issuer incorporated, formed or created under the laws of

excessive valuation. The stock is expected to trade lower on an absolute basis and be Canada or a province or territory of Canada, any trades in such securities must be

among the worst performers relative to peer stocks over the next 12 months. conducted through a dealer registered in Canada. No securities commission or similar

regulatory authority has reviewed or in any way passed judgment upon these

materials, the information contained herein or the merits of the securities described

herein and any representation to the contrary is an offense.

18United Kingdom

Tudor, Pickering, Holt & Co. International, LLP is a limited liability partnership

Tudor, Pickering, Holt & Co International LLP does not provide accounting, tax or legal registered in England and Wales (registered number OC349535). Its registered office is

advice. In addition, we mutually agree that, subject to applicable law, you (and your 5th Floor, 6 St. Andrew Street, London EC4A 3AE. Tudor, Pickering, Holt & Co.

employees, representatives and other agents) may disclose any aspects of any International, LLP (TPH International) is authorised and regulated by the Financial

potential transaction or structure described herein that are necessary to support any Conduct Authority, and is a separate but affiliated entity of Tudor, Pickering, Holt &

UK income tax benefits, and all materials of any kind (including tax opinions and other Co. Securities, Inc. (TPH Securities). TPH Securities is a member of FINRA and

tax analyses) related to those benefits, with no limitations imposed by Tudor, SIPC. Unless governing law permits otherwise, you must contact the Tudor, Pickering,

Pickering, Holt & Co International LLP or its affiliates. Holt & Co. entity in your home jurisdiction if you want to use our services in effecting a

The information contained herein is confidential (except for information relating to transaction.

tax issues) and may not be reproduced in whole or in part. Tudor, Pickering, Holt & Co

International LLP assumes no responsibility for independent verification of third-party Tudor, Pickering, Holt & Co. International, LLP is a limited liability partnership

information and has relied on such information being complete and accurate in all registered in England and Wales (Financial Services Register number OC349535). Its

material respects. To the extent such information includes estimates and forecasts of registered office is 5th Floor, 6 St. Andrew Street, London EC4A 3AE. Tudor, Pickering,

future financial performance (including estimates of potential cost savings and Holt & Co. International, LLP (TPH International) is authorised and regulated by the

synergies) prepared by, reviewed or discussed with the managements of your company Financial Conduct Authority, and is a separate but affiliated entity of Tudor, Pickering,

and/ or other potential transaction participants or obtained from public sources, we Holt & Co. Securities, Inc. (TPH Securities). TPH Securities is a member of FINRA and

have assumed that such estimates and forecasts have been reasonably prepared on SIPC. Unless governing law permits otherwise, you must contact the Tudor, Pickering,

bases reflecting the best currently available estimates and judgments of such Holt & Co. entity in your home jurisdiction if you want to use our services in effecting a

managements (or, with respect to estimates and forecasts obtained from public transaction.

sources, represent reasonable estimates). These materials were designed for use by

specific persons familiar with the business and the affairs of your company and Tudor, See http://www.tudorpickering.com/Disclosure/ for further information on regulatory

Pickering, Holt & Co International LLP materials. disclosures including disclosures relating to potential conflicts of interest.

This information is intended only for the use of professional clients and eligible

counterparties or persons who would fall into these categories if they were clients of

Tudor, Pickering, Holt & Co International, LLP, or any of its affiliates. Retail clients

must not rely on this document and should note that the services of Tudor, Pickering,

Holt & Co International, LLP, are not available to them.

Under no circumstances is this presentation to be used or considered as an offer to Copyright 2014, Tudor, Pickering, Holt & Co. This information is confidential and is

sell or a solicitation of any offer to buy, any security. Prior to making any trade, you intended only for the individual named. This information may not be disclosed, copied

should discuss with your professional tax, accounting, or regulatory advisers how such or disseminated, in whole or in part, without the prior written permission of Tudor,

particular trade(s) affect you. This brief statement does not disclose all of the risks Pickering, Holt & Co. This communication is based on information which Tudor,

and other significant aspects of entering into any particular transaction. Pickering, Holt & Co. believes is reliable. However, Tudor, Pickering, Holt & Co. does

not represent or warrant its accuracy. The viewpoints and opinions expressed in this

Notice to UK Investors: This publication is produced by Tudor, Pickering, Holt & Co. communication represent the views of TPH as of the date of this report. These

Securities, Inc. which is regulated in the United States by FINRA. It is to be viewpoints and opinions may be subject to change without notice and TPH will not be

communicated only to persons of a kind described in Articles 19 and 49 of the Financial responsible for any consequences associated with reliance on any statement or opinion

Services and Markets Act 2000 (Financial Promotion) Order 2005. It must not be contained in this communication. The viewpoints and opinions herein do not take into

further transmitted to any other person without our consent. Any other person should consideration individual client circumstances, objectives, or needs and are not

not rely on or act upon the content of this publication. intended as recommendations of particular securities, financial instruments or

Persons falling within Article 19 include authorised or exempt investment firms, UK or strategies to particular clients. Past performance is not indicative of future results.

overseas governments, UK or overseas local authorities or international organisations. This message should not be considered as an offer or solicitation to buy or sell any

Person falling within Article 49 include companies or unincorporated associations with securities. Institutional Communication Only. Under FINRA Rule 2210, this

net assets or called-up share capital of £5 million or subsidiary companies of the same communication is deemed institutional sales material and it is not meant for

that have net assets or called-up share capital of £500,000. distribution to retail investors. Recipients should not forward this communication to

a retail investor.

19RESEARCH SALES TRADING

Oil Service / E&C E&P Macro Houston Denver Houston - (800) 507-2400

Jeff Tillery Matt Portillo Dave Pursell Clay Coneley Win Oberlin Scott McGarvey

713-333-2964 713-333-2995 713-333-2962 713-333-2979 303-300-1919 smcgarvey@TPHco.com

jtillery@TPHco.com mportillo@TPHco.com dpursell@TPHco.com cconeley@TPHco.com woberlin@TPHco.com

Seth Williams

Byron Pope Michael Rowe Brandon Blossman Mike Bradley Jason Foxen swilliams@TPHco.com

713-333-7690 713-333-3983 713-333-2994 713-333-2968 303-300-1960

bpope@TPHco.com mrowe@TPHco.com bblossman@TPHco.com mbradley@TPHco.com jfoxen@TPHco.com New York - (800) 507-2400

George O’Leary Jeoffrey Lambujon Mike Davis Todd Wood

713-333-2973 713-333-7549 Midstream 713-333-2971 New York twood@TPHco.com

goleary@TPHco.com jlambujon@TPHco.com Brad Olsen mdavis@TPHco.com Ken Johnson

713-333-7693 212-610-1650 London

Klayton Kovac Henry Wyche bolsen@TPHco.com Oliver Doolin kjohnson@TPHco.com

713-333-3866 713-333-2993 713-333-2989 Harry Grist**

kkovac@TPHco.com hwyche@TPHco.com odoolin@TPHco.com Craig Webster hgrist@TPHco.com

Coal / Power 212-610-1652 +44 20 3427 5832

Shola Labinjo** Jamaal Dardar Brandon Blossman John Hurd cwebster@TPHco.com

+44 20 3008 6437 713-333-3926 713-333-2994 713-333-2951 Richard Heggs**

slabinjo@TPHco.com jdardar@TPHco.com bblossman@TPHco.com jhurd@TPHco.com rheggs@TPHco.com

London +44 20 3427 5833

Aly McCaffrey Jonathan Wright**

Integrated Oils E&P International Utilities / Power 713-333-2983 +44 20 3008 6436

Dave Pursell Anish Kapadia** Neel Mitra amccaffrey@TPHco.com jwright@TPHco.com

713-333-2962 +44 20 3008 6433 713-333-3896

dpursell@TPHco.com akapadia@TPHco.com nmitra@TPHco.com

Anish Kapadia** Shola Labinjo** Ryan Caylor

+44 20 3008 6433 +44 20 3008 6437 713-333-7694

akapadia@TPHco.com slabinjo@TPHco.com rcaylor@TPHco.com

David Gamboa**

Refiners +44 20 3427 5896

Dave Pursell davidgamboa@TPHco.com

713-333-2962

dpursell@TPHco.com

**Office of Tudor, Pickering, Holt & Co. International, LLP. Employed by Tudor, Pickering, Holt & Co. International, LLP in the United Kingdom and is not registered/qualified with FINRA and is not an

associated person of Tudor, Pickering, Holt & Co. Securities, Inc.

Anish Kapadia, Shola Labinjo, and David Gamboa are employed by Tudor, Pickering, Holt & Co. International, LLP in the United Kingdom and are not registered/qualified as research analysts with FINRA. Mr.

Kapadia, Mr. Labinjo, and Mr. Gamboa are not associated persons of Tudor, Pickering, Holt & Co. Securities, Inc. and as such are not subject to NASD Rule 2711 restrictions on communications with subject

companies, public appearances and trading securities held by a research analyst account.You can also read