A Year End Update on the LIBOR Transition - Sia Partners

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

R

E

S

E

A

R

C

H

A Year

End Update

on the LIBOR

Transition. jan 20210

0

s i a - p a r t n er s .c o m

@SiaPartners0

0

Project Background and

Acknowledgements.

This report is the last in a series of publications Sia Partners have authored

throughout 2020 relating to industry progress in meeting the LIBOR Transition

deadlines. We are exceptionally appreciative for the assistance and cooperation

from almost 100 institutions who have participated in our initiatives globally. This

year our documents included a pre-pandemic review of efforts as a follow-up to

our 2019 industry report. We also produced a series of short snapshots from the

same group of participants and some new joiners plus webcasts, and webinars on

this topic. We will continue these studies in 2021 as the industry progresses with

their transition investments.

This final effort combines both a policy report on the state of the industry as well

as a series of interviews we conducted in December after the release of the draft

consultative document. Mark Chorazak, a Partner in Shearman & Sterling’s Finan-

cial Institutions and Regulatory Reporting Practice joined us in co-authoring por-

tions of this document. Our colleagues at RISKSPAN provided exceptional depth

and analysis to the section on Risk Modeling and Validation which we believe will

be a looming and expanding area of focus in 2021. Finally, Eigen Technologies pro-

vided valuable contributions on the state of the industries embrace of automation

and natural language processing in their contract review efforts.

These efforts would not be possible without the contributions of many of our ma-

nagers and consultants who have worked long hours to support them. My thanks

to Mark Cheng, Harrison Suttle, Affan Khan, Virginia Sideleva, Asli Ersozoglu, and

Danielle Buttinger for their work throughout the year and to Chris Zachodzki for his

continued efforts in providing essential guidance to all of our initiatives. To all our

Sia colleagues who’ve assisted with these projects while working on their engage-

ments full time; thank you for devoting your time and energy to our industry efforts.

Like everyone, Sia Partners has found this a challenging year at best and, as always

we hope you continue to review our material in a healthy and safe environment.

We have conducted hundreds of conversations virtually, which has mirrored our

commitments to clients in our proprietary work in the LIBOR Transition space. We

would be remiss in not thanking everyone for their patience and helping us to

complete our work successfully.0

0

Table of Contents.

6

• Market Reaction to Recent Announcements

2 A. How has the Release of the Consultative Documents Affected Transition Implementation

Timing?

B. What will be the Impact of the Official Sector in Implementing the Goal of the Consultative

Documents?

C. H

ow has the Release of the Consultative Documents Impacted the Development of SOFR and

other Alternative Reference Rate Products?

•

D. How has the Consultative Announcements Impacted Client Transition Progress?

11

The LIBOR Transition: End of the Year Update on Industry

Progress & Recent Developments

15 A. Background on Research

19 B. Contract Review and Remediation

21 General Observations

19 Coordinated and Consequential November Announcements

21 Prospects for a Legislative Solution

19 Announcement of ISDA Protocol

21 C. Technology and Operational Readiness

21 D. Model Risk Management and Validation Issues

19 E. C

lient Outreach and Communication0

0

Document Overview.

Sia Partners’ divided its following Year End Update on the LIBOR Transition into

two primary sections.

First, we have detailed the industry’s reaction to the announcements made on

November 30 and December 4 by the official sector. We spoke to 25 of our original

participating benchmark firms, which included a balance among foreign banks,

G-SIBs, regional banks, and both financial and corporate end users. We asked for

their feedback on a variety of questions covering both the consultative announ-

cement and year-end feedback on progress for the transition by their peers and

clients. We focused feedback on four related to the impact of the consultative do-

cuments: (a) will the timing of the transition be impacted? (b) the role of the official

sector in interpreting and implementing the consultative recommendations; (c) the

impact on potential delays on the construction of SOFR and other reference rates,

and finally, (d) how have these delays impacted client transition progress?

Second, based on a combination of feedback from research, policy announce-

ments from the ARRC, regulators and fall discussions with participants prior to

the consultative announcements, highlights industry progress and developments

specific to key transition activities. The second section was drafted in conjunction

with Shearman & Sterling.0

0

1. Market Reaction

to Recent

Announcement.

How has the Release of the tives. Study participants agreed the operational progress and product en-

Consultative Documents issues surrounding the actual timing hancements but did not expect that

of the transition from LIBOR to SOFR postponement due to the pandemic

Affected Transition Imple- (or other reference rates) and the ro- related issues. Statements from across

mentation Timing? bustness of the liquidity of those ARR the official sector (FCA, Federal Re-

products were foremost on their mind. serve, FSB, etc.) reiterated the year

Industry regulators continue to empha- We summarize those conclusions end-2021 transition timeline without

size that institutions should not enter below. flexibility. Most of the participants

new US Dollar LIBOR contracts after were surprised by the November 30/

end-2021. Subject to the responses to MIXED REACTIONS December 4 announcements, but not

the IBA consultation, which is open for disappointed. Here is our thinking why

comment until January 25, 2021, lega- First, participants noted that the an- that is the case.

cy contracts referencing certain tenors nouncements have in some meaningful

of US Dollar LIBOR could continue to fashion for some, and far less for others, • Postponement would provide some

mature through June 2023. IBA has affected the broader thinking relating helpful time to implement certain

stated that it intends to publish feed- to the progress of the transition. Insti- operational/vendor upgrades. Larger

back summarizing responses from the tutions noted that the transition was at firms noted that considerable amount

consultation shortly after the consul- an “inflection point” with a broad set of of progress had been made since

tation deadline and regulators are issues ranging from clients’ willingness vendor work was nearing completion;

expected to further consider to what to transition; liquidity growth in SOFR, • Some hesitance on success until ele-

extent they should limit new uses of avoidance of delays in passage of le- ments of SOFR (or another ARR) are

USD LIBOR. gislation to provide legal certainty on finalized that some of those steps

contracts among the topics that nee- likely will be delayed.

Recognizing the impact of these an- ded redress. Others noted that there • S maller and mid-size firms whose

nouncements, we reached out to a has been solid progress on operational systems were internally based would

number of our project participants and topics but reiterated the need for more potentially lag and drag out the pro-

asked them for their input. specificity on the SOFR product roll cess; Firms separately identified the

out (term rate for most, credit spread value of this delay value in the run-off

Over the past two weeks, we have overlay for a smaller group) and most of their agreements and set out their

had several dozen exchanges on the importantly some teeth behind the thinking around these theses:

issues raised in the November 30 and safety and soundness approaches that • Unrelated to the percentage of agree-

December 4 announcements from the banking regulators have identified to ments that firms identified were per-

IBA and the official sector. We also encourage transition progress. tinent to their business lines (40% or

requested input on a year-end as- A significant percentage of the firms we higher) that would get additional time

sessment on the progress on contract spoke with noted that while they were to run-off; the concept of the heighte-

review, operational and vendor efforts ready to meet the original transition ned time was seen as a positive for

to close gaps identified earlier in our deadlines, the delay envisioned would the industry.

studies as well as current challenges be useful. Indeed, our data reflected • For the tougher legacy agreements,

surrounding client outreach and com- mid-year a growing number of firms additional time was helpful to avoid

munications and their transition initia- that wanted additional time for varied negotiation with clients;0

0

• certain clients or business lines with a have been vocal advocates of including the maturity of product growth. Stu-

higher preponderance of (ABS/CMBS, a dynamic credit spread to SOFR. As dy participants shared the view that

etc.,) the deadline loomed, the Credit Sensi- time should provide additional time to

• Easing the negotiations related to tivity Group, sponsored by the Federal build-out growth in cash and derivative

“tough legacy” contracts especially Reserve, considered some alternatives instruments and hopefully a ramp up

as firms articulated the timing asso- but chose not to recommend any of

in issuance as product clarity and legal

ciated with the legislation from either them specifically during the summer.

certainty are enhanced in 2021.Study

the NY State Legislature or Congress Separately, some firms have advocated

participants agreed the additional time

to provide legal clarity and hence the consideration to other approaches in-

should help those in the market that

longer runoff time was seen as an cluding the Bank Yield Index, Ameribor,

asset. had yet to invest or stand up a program.

several under sponsorship by third par-

ties and recommendations put forth by This would include those that were:

IMPACT ON SOFR LIQUIDITY academicians. Individual firms noted • Global but had not invested in their US

that for all the dialogue, the demand Dollar LIBOR efforts;

Not surprisingly, an additional benefit for individual reference rates will be • Firms both financials and corporates

of the extended time from our parti- market driven and liquidity for both the who were aware of the transition but

cipants was the build-out of SOFR to derivatives, cash and lending markets not yet heavily invested;

ensure a higher level of robustness are months off. • M id-size & smaller companies who

and potentially other reference We will address the broader liquidity required additional education and

rates. We have addressed this issue and product issues below. However, persuasion about the necessity for

throughout our papers the past two a majority of our participants agreed

meaningful transition progress.

years and the interest in some alterna- that the additional timing would allow

Institutions noted that the delay would

tive approaches has stayed reasonably a broader liquidity pool to be built for

provide additional time for the legal

consistent among the participants in SOFR emphasizing this was a critical in-

remedies to be passed globally, inclu-

our projects. To be clear, we are not gredient for success. Institutions noted

suggesting that this reflects the broa- ding legislation which would provide

that to date, the SOFR liquidity results

der banking or end user universe, but have been mixed—a pick up after needed clarity that sits before the

rather our research group across those SOFR Discounting but somewhat of a • NY State Legislature

categories. There has been a select flattening thereafter. A few institutions • Congress

group of respondents from the banking felt that derivatives growth was rising • UK/EC equivalents

community---mostly US based—who but most admitted disappointment in

Our initial reaction is that this does not

change what we need to accomplish in 2021.

We still need to complete our application,

model and contract remediation as originally

planned. We plan to be ready to meet the

dates in the ARRC recommendation that were

published in May 2020. U.S. Banking Participant0

0

CONCERNS IDENTIFIED TO DATE so broadly no impact; king groups, timing and best practice

• Many firms noted that “our planned guidelines. A group of firms vocally

Our participants identified some core actions for the transition and timing raised the concern what would be the

concerns about the delay that they stay the same”; outcome of those approaches—would

felt might not be easily calculable im- • They were expecting some relief and those dates be retained/rescued or lost

mediately. These included those that our product enablement, model and to the process?

invested—spent time—to build up their technology work is unchanged; We discussed briefly above the impact

efforts and now were being penalized • Accomplishment benchmarks for 2021 of the announcement on the ability to

by pushing back pieces of the ces- remain unchanged for most firms; and create some global consistency with

sation date, and those firms that saw • Some enhanced thought on client en- regard to the transition. Firms generally

value in their significant organizational gagements and execution times but believed the challenges included:

approaches for contract review, ope- planning unchanged. • a general recognition from the global

rations, and product management and banks that they have been planning on

did not want to surrender that margin. What will be the Impact of a cross currency overlay with different

Second, there was broad concern ex- the Official Sector in Im- implementation dates for a long while.

pressed about the risks of magnifying This did not meaningful change their

global fragmentation. Firms noted that

plementing the Goal of the approach;

this has been a consistent concern gi- Consultative Documents? • an agreement that UK regulators have

ven the earlier start in the UK-EC and been more rigorous in their approach;

The second issue that emerged from

what both banks and buy side firms • other IBORs are further progressed

Sia’s discussions was the role of the

believe has been a more rigorous regu- both for banks and end-users and ins-

“official sector”—regulators—in imple-

latory approach which enhanced pro- titutions believe that this would not be

menting the consultative approaches.

gress. Firms noted that this delay could altered by the announcements;

The views varied and often depended

• participants questioned the impact

upon the intensity of interaction with

• Complicate management of multi-cur- of the announcement affecting the

regulators as part of their LIBOR tran-

rency tenor pairs; and timing related to any fixed dates for

sition. Some firms had begun those

• Lead to inevitable rolling off separate FCA pre-cessation triggers or spread

dialogues at least a year ago and were

currencies in ’21 vs. ’22 and risk ma- rate adjustments or other planned cla-

in contact on a formal, quarterly ba-

naging around that. rifications for the industry.

sis with their supervisors. Others had

dialogues on an informal basis more

Firms also noted a concern about inter- There was extensive dialogue from a

often. Other firms identified a far less

nal progress: group of firms about the ability to align

frequent interaction and did not have

• Loss for client outreach momentum the safety and soundness approaches

a view on the depth of understanding

some pauses until we know the im- for banks with a more robust effort for

on the transition for those who had

pact of the official sector guidelines; less regulated end-users. Participants

oversight. There was some agreement

• Loss of budget commitments and identified a series of challenges:

that the announcements were vague in

risks of re-allocation; • foremost, the structure for the SEC,

what precisely implementation of en-

• Management of whether there is a re- CFTC and others that have oversight

hanced “safety and soundness” efforts

turn to “business as usual” and have responsibilities for corporates, financial

would mean although some felt that

the central program re-focused; end users is meaningfully different and

was transparent and part of the day

• Keeping a team afloat for up to 18 efforts to persuade those they have

to day banking regulator approaches.

more months—funding/resources oversight for quicker action could be

There were some institutions who

• Losing overall management focus— problematic;

clearly wanted greater clarity and a

attention to the transition-some re- • a view that asset managers and some

stronger approach from the regulato-

ferenced seeing this with MiFid and in the ‘alternative space’ could step in

ry sector. These firms have generally

other policy initiatives in the past; and and provide the liquidity for the bank

held similar views throughout our study

• Risk of lowering commitment to risk loan and middle market space is quite

process and have asked for a sturdier

management/model projects and plausible and needs redress if the goal

response from U.S. parties.

digitizing contracts built off the back is to ensure a timely transition away

A number of firms made a separate

of this transition effort at some larger from LIBOR product;

argument—which was embracing the

firms. • a requirement for an FSOC or equi-

ARRC Best Practices as part of the

valent effort across regulators for uni-

“teeth” in the next set of regulatory

Our assessment included a group of formity on goals—standing behind the

commentary. Institutions noted that

clients that did not see at least some hardwire language (as an example) and

for the past several years firms glo-

aspects of this as moving the needle ensuring a clear vocal direction for all

bally (if not primarily in the U.S.) have

in a meaningful way. Clients noted that market participants.

been reliant on ARRC direction, wor-

• There is still no new LIBOR post 20210

0

How has the Release of the were long-discussed challenges of (for example trade financing or any

utilizing SOFR in arrears for a group business that offers discounting).

Consultative Documents Im-

of banks and some end users. Institu- Throughout our summer-fall discus-

pacted the Development of tions identified challenges on the cash sions, a term structure was seen as

SOFR and other Alternative side (vs. derivatives) for using the mul- significantly desirable. The support

Reference Rate Products? ti-step process as well as the timing for for that as we enter 2021 has grown

amendments for options and picking among the firms who did not have

Our third client feedback section fo- conventions for which additional time strong views earlier and certainly in

cuses on the views of the participants would be useful. the strength of that conviction among

related to the consultative paper’s im- those firms who have favored term

pact on SOFR’s maturity as well as the A separate stream of dialogue sur- from the beginning.

creation of other reference rates. Alike rounded the value of giving a dynamic

other themes, this topic arose in every credit solution a chance for fruition. A In summary there was a broad consen-

topical segment we raised related to number of respondents noted that they sus that the growth of SOFR products

the consultative papers role in shaping felt that this option had been more than has been slow and, in many ways, di-

the transition deadlines (section one) sufficiently vetted and that any version sappointing. Institutions agreed that

as well as how SOFR’s development is of either market or operational success discounting provided a short, “large

linked to the official sectors pressure was not likely. However, others (as they boost” but that liquidity was tempo-

on regulated entities to commit to the have throughout our projects) differed. rary. Firms noted that traders did not

transition in a timely manner. The argument from those firms was believe that the discounting switch did

Our participants throughout our stu- built centrally around the market ab- not produce what was hoped for or in-

dies the past several years have voiced sorbing the risk; taking advantage of tended and other mechanisms we have

opinions regarding the value of encou- the “extended runway” and make ad- already discussed above need serious

raging the adoption of alternative refe- ditional attempts to build some support consideration. Several institutions

rence rates to SOFR. Data from our ex- for the credit overlay concept. Some re-emphasized that the liquidity issue

changes have consistently suggested firms noted that building a consensus for SOFR was up to the client demand

that there was limited momentum for around SOFR supplementations (cre- and their appetite and less about the

any one particular alternative—howe- dit, term curve, etc.) would take time actual structure of the product itself.

ver crossing a few alternatives—the and might end up being prioritized as This requires the market and the of-

potential support grew. There was a industry participants choose which ficial sector separately delivering a

broad consensus that the additional aspect is most important to them to strong message both for derivatives

time would provide support for the launch SOFR. Others commented and for syndicated transactions. There

growth for a few alternative rates. A that the challenges of less centralized is a need for strong fallback language

smaller but vocal group of firms have, conventions and greater underlying and hardwire requirements as well as

from the outset been support of consi- data issues made a credit overlay more strong actions by the official sector that

deration of a credit overlay. In our most complex to construct vs. term rates. we have discussed previously. Firms

recent discussions, those firms conti- There was unanimous view on the va- agreed that this was a combined col-

nued to articulate the value of building lue of adding a term rate to the SOFR lective action to achieve the desired

out that choice but also consider for structure. There was a small number of results in building out liquidity in the

their middle market clients additional individuals who felt that a credit overlay SOFR product and other alternative

reference options including Ameribor, was of great comparative importance, reference rates.

Bank Yield index and others being de- but the significant majority did not

veloped. Other firms noted that unless share that view. In no particular order,

there was a meaningful uptick in SOFR firms identified a series of reasons that

post the final release of the consulta- this was valuable:

tive paper in late January/early Februa- • a number of firms generally argued

ry, then the dialogue surrounding op- that a term structure was a pre-re-

tions would build out. And there were quisite for the success of SOFR by

strong views relayed by others that January 2022. The publisher of this

they have been trading and issuing in structure cannot be synthetic; me-

SOFR for a while—they are comfortable thodology preferable ICE driven and

with the progress at multiple tenors of meet pricing and valuation processes

the product build. for accrual calculation;

In the discussions, clients identified • there needs to be a definition end

a variety of reasons that timing could date for issuing to ensure liquidity in

impact SOFR product maturity in va- other products;

rious meaningful ways. First, there • t he value for specific businesses1

1

How has the Consultative by the pandemic. Second, there is a re- to be part of a transition good citizenry.

cognition that simplicity for many of the Finally, we have seen the pace of client

Announcements Impacted

middle market clients will eventually be outreach has increased from our ear-

Client Transition Progress? determinative. Our study participants lier pieces in the spring and summer/

believe that at year end their clients fall of this year. The implications of the

Our last client interview discussant

are either confused by the consultative pandemic on corporate entities was

section will briefly focus on the impact

papers and what the implications are meaningful and clearly impacted their

on end users and clients from the an-

or curious if this allows a time break for progress. Less on financial end users.

nouncements on November 30th and

their own efforts. This feedback com- Client outreach was frozen for the

December 4th. We have in other por-

ports with our own individual client spring for many or limited. That picked

tions of this document addressed what

exchanges the past few weeks. up in the late spring and seemingly

the banks believe will be the impact

Third, there was a broad consensus was a pace through year end until the

on their timeline for implementation,

that there has been close to no engage- issuance of the consultative papers. A

SOFR product development, the role

ment by the official sector with clients. combination of year end activities and

of regulatory bodies in furthering tran-

Larger clients confirmed exchanges the lack of full clarity from the consul-

sition progress and numerous opera-

with some parts of the official sector, tative documents could make further

tional and contractual related topics.

but most had not and were not aware of progress difficult until mid-Q1. Global

The progress of clients in meeting the

particular forthcoming oversight pres- firms could continue to have mixed res-

transition deadlines is tied to every one

sure. Fourth, few buyside institutions ponses—more vigorous commitments

of these topics among others. Separa-

acknowledged what was expressed in their European/APAC offices and

tely, in our policy section, we address

by their dealer peers about the critical less convicted on investment in the US

issues related to client communications

role that end user entities played in the until their US Dollar LIBOR approaches

and outreach. One of the larger provi-

transition. There continued, at year-end are validated by both counterparties

ders in the automation and NLP space

2020 to be a belief that non dealer en- and the official sector. Indeed, some

suggested:

tities were going to be “takers” on ne- financial counterparts in the alternative

Study respondents identified a few

gotiations with their bank counterparts sector will likely await the final outco-

challenges for the end-user commu-

and with few exceptions, did not see me and identify market opportunities

nity. First, participants believed that

themselves as core to the policy dia- that will arise as the transition is fina-

the end user market was bifurcated

logues or negotiations. The potential lized which will enable them portfolio

in their commitment to the transition.

“educational” or “communication” gap enhancements as mismatches occur

Larger financial end users and larger

could be at two levels: the acknowled- across currencies and jurisdictional

corporates appreciate the timeline,

gement of the timing of the transition timings are put in place. In sum, there

have initiated governance and made

and the commitment to complete the is no monolith on the end user side. We

in many cases substantially larger

tasks but also the recognition of the would expect differences in responses

investments. But smaller-mid-size

need for the engagement on the macro across geographies and entity types as

entities have expressed either disin-

side—commitment to trade, willingness the transition progresses through 2021

terest—lack of awareness or focus—or

to partake in risk taking, advance broa- and beyond.

a greater need to focus on clients and

der policy initiatives and best practices

businesses that have been damaged1

1

2. The LIBOR Transi-

tion: End of the Year

Update on Industry

Progress and Recent

Developments.

Background on Research critical steps. In its prior report from and associated costs. Firms with in-

June 2020, Sia Partners had identified house AI/NLP development and delive-

Sia Partners’ research comprised a some sluggishness in progress among ry teams encountered challenges rela-

benchmarking study of over 70 market sections of the industry. While G-SIBs ting to the size and scope of the effort

participants on the progress of their and large non-US financial institutions for LIBOR. For example, the sheer vo-

transition from LIBOR to alternative had made substantial progress across lume of different document types and

overnight risk-free reference rates. the areas of contract review and ex- the variances within required substan-

Representatives from Sia Partners traction and initial remediation, other tial development work, increased mo-

conducted virtual interviews of sub- institutions were at the time, procee- del training time and longer lead times

ject-matter experts from a variety of ding on a markedly slower pace. Based to achieve the necessary data and

functions, including legal, risk ma- on Sia Partners’ most recent set of dis- accuracy rates. Discussions with our

nagement, compliance, operations, cussions with market participants over partner firms and material we separa-

finance and information technology, the course of this fall, a significant up- tely identify in our accompanying docu-

along with those charged with direc- tick among US regional banks and lar- ments highlight both those challenges

ting LIBOR transition efforts at a wide ger financial end-users was identified and how firms have more successfully

range of financial institutions and other with respect to their contract review utilized the technologies. The more

market participants. This report, com- initiatives. Progress entailed a range recent feedback that Sia Partners

pleted in conjunction with Shearman & of steps, from the extraction of key gathered on implementation of key

Sterling, builds upon that research and contractual terms to internal dialogues provisions on the cash and derivatives

supplemental work completed during on fallback terms of criticality. side reflects progress in the industry.

the fall and winter focusing on those The complexity and depth of legacy Many firms have been taking remedial

firms challenges in meeting the requi- contract analysis and remediation re- steps that they had not initiated three-

rements for the global IBOR transition. mains one, if not the most, challenging to-six months earlier. Those that had

Contract Review and Remediation activities firms are facing in completing initiated their efforts earlier—many of

GENERAL OBSERVATIONS a successful and timely LIBOR transi- which had used some form of NLP/AI

Sia Partners’ discussions with financial tion. The use of artificial intelligence solution to expedite that review and

institutions over the past two years in (AI), natural language processing extraction process—have moved on

various studies have highlighted the (NLP) and machine learning (ML) can to recognize that a portion of their

interlinking steps of contract review streamline and speed-up the time as- contracts will not work with conven-

and remediation, as well as the use of sociated with contract analysis, while tional fallback language and will need

automation and natural language pro- increasing efficiency and data quality customized remediation. Some portion

cessing (NLP) to help implement those and reducing resource requirements of those contracts could be beneficia-1

1

ries of the most recent consultative clarity. And indeed, there are still some (ARRC) has published recommended

announcement from the official sector. that would prefer a different reference fallback language for adjustable rate

Among the initial challenges that had rate (outside of SOFR). All these steps mortgages, bilateral business loans,

affected progress on contracts was the impact the core challenges every firm floating rate notes, securitizations,

need for a firm cessation date as well faces: operationalizing the transition, syndicated loans and variable rate pri-

as a determination of a clearer version communicating those changes to vate student loans. The extent to which

of the Secured Overnight Financing clients and helping them effectuate any market participant implements or

Rate (SOFR). Recognition of simple the transition, setting up the appro- adopts any suggested contract lan-

SOFR for some products and more priate risk management tools for new guage is completely voluntary. Each

complex SOFR in arrears for others, reference rates, and ensuring buy-in market participant will make an inde-

such as floating rate notes, continue to from business units to be confident that pendent decision about whether or to

challenge many including some of the the transition will be near flawless. We what extent any suggested contract

most advanced in the industry. address some of those operational and language is adopted.

Some specific lending language on risk issues separately in this document.

CLOs has advanced segments of the Within the cash space, the Alter-

market that had been awaiting industry native Reference Rates Committee

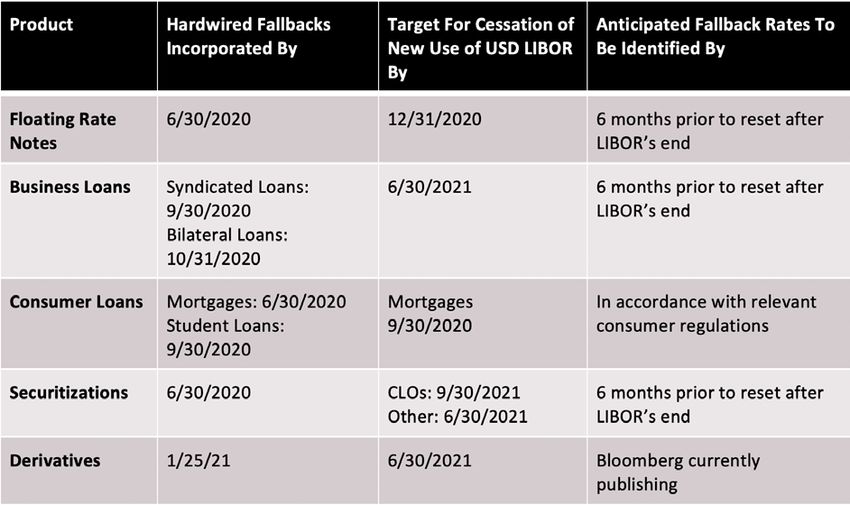

The table below highlights the ARRC’s recommended best practices for newly issued loans.

Notably, ARRC’s set of recommended COORDINATED AND CONSEQUEN- On November 30, 2020, IBA an-

best practices identified June 30, 2021 TIAL NOVEMBER ANNOUNCEMENTS nounced a proposal to extend the pu-

as the target cessation date for new blication of the most commonly used

business loans, derivatives, and non- In November, the industry saw highly USD LIBOR settings (overnight and

CLO securitizations. As discussed coordinated and consequential an- one-, three-, six- and 12-month) until

below, this is six months in advance nouncements from the ICE Benchmark June 30, 2023, with the other settings

of the date—December 31, 2021—by Administration (IBA) (the administrator (one-week and two-month) ceasing af-

which the US banking agencies have of LIBOR) and UK and US banking regu- ter December 31, 2021. IBA’s announ-

encouraged banks to stop entering into lators, which, taken together, provide cement followed an earlier statement

new USD LIBOR contracts. the clearest, most practical framework in which it announced plans to cease

to date on the end of LIBOR. publication of all GBP, EUR, CHF, and1

1

JPY LIBOR setting after December for feedback closes in January 2021. vatives market participants with new

31, 2021. In connection with IBA’s an- • New contracts and instruments that fallbacks, respectively, for legacy deri-

nouncement on November 30, the UK reference USD LIBOR should include vative contracts and for new derivative

Financial Conduct Authority (FCA) and hardwired fallbacks now. contracts. As derivatives represent the

the US Federal Reserve issued state- vast majority of the outstanding LIBOR

ments welcoming IBA’s announcement, The recent announcements, which exposure, ISDA’s announcement was

which the FCA described as “incenti- have been received positively by fi- much-awaited by the industry. It will

vis[ing] swift transition, while allowing nancial and banking trade associations, be an efficient mechanism to amend

time to address a significant proportion signify an important shift from what had derivatives contracts with many coun-

of the legacy contracts that reference been viewed as an inflexible deadline terparties. Broad adherence to the

[USD LIBOR].”1 Concurrently with IBA’s of year-end 2021. With the extra time Protocol is, therefore, important for

latest announcement, the US banking to prepare, market participants should mitigating the financial stability risks

agencies issued a joint statement en- continue taking actionable steps to associated with LIBOR becoming

couraging banks to cease entering into operationalize remediation processes unusable. According to the ARRC’s

new contracts that use USD LIBOR as a in a thoughtful and thorough manner. recommended best practices, market

reference rate “as soon as practicable participants are encouraged to adhere

and in any event by December 31, PROSPECTS FOR A LEGISLATIVE to the Protocol before it takes effect on

2021.” The agencies described this as SOLUTION January 25, 2021.

necessary to facilitate an orderly—and

safe and sound—LIBOR transition. In In March 2020, the ARRC proposed Technology and Operational

particular, “[g]iven consumer protec- legislation for New York that would, Readiness

tion, litigation, and reputation risks, among other things, protect parties

the agencies believe entering into new that adopt SOFR as a replacement Firms have generally identified several

contracts that use USD LIBOR as a re- for LIBOR under financial contracts operational hurdles to the LIBOR tran-

ference rate after December 31, 2021, governed by New York law. ARRC’s sition, including system updates and

would create safety and soundness legislation solution, which specifically product and model construction, based

risks and will examine bank practices addresses LIBOR fallback language, on Sia Partners’ most recent set of

accordingly.”2 was formally introduced in the New interviews. Delays with vendor selec-

York State Senate and is expected to tion have improved in our most recent

In a newly issued guide, ARRC has des- be considered next year. Following the discussions with the industry, with the

cribed these recent announcements as November announcements, the ARRC most progress among the larger firms

being fully aligned with its own work reiterated its support for it. who had begun vendor outreach prior

to date. It has also noted that the time- The New York legislative solution, to the pandemic. Smaller and midsize

lines contained in its recommended together with the November announ- firms have continued some struggles. It

best practices (referenced in the chart cements discussed above, are an es- is evident that firms are either contem-

above) were designed on the basis of sential part of an orderly transition from plating vendor implementation or are

what it considered to be practicable. LIBOR. The additional 18-month time- in the process of testing their own sys-

Therefore, the following take-aways frame during which a substantial por- tems against ARRC guidelines, with the

should be considered by market tion of LIBOR-linked legacy contracts achievement of industry milestones

participants: can run-off will give greater clarity, expected to occur throughout Q1 and

and perhaps urgency, for legislation Q2 of 2021.

• N ew contracts and instruments to address, what Federal Reserve Vice

should stop referencing USD LIBOR Chair Randal Quarles recently descri- We believe firms will need to focus on

by December 31, 2021, but earlier if bed as, the “hard tail.” the following technology and operatio-

practicable. Otherwise, examiners nal areas for 2021:

may determine that a bank is enga- ANNOUNCEMENT OF ISDA

ging in unsafe and unsound banking PROTOCOL Governance

practices.

• Legacy contracts (i.e., those that ma- Finally, a highly positive development • Implement centralized project mana-

ture beyond December 31, 2021) that for contract remediation occurred gement office (PMO) governance to

reference USD LIBOR may have an earlier this fall. On October 23, 2020, oversee all LIBOR Transition Office

additional 18 months—until June 30, ISDA announced its IBOR Fallback (LTO) project timelines and budgets

2023—to mature, be refinanced, or Protocol and IBOR Fallback Supple- • Align PMO timelines to specific LTO

otherwise be remediated, including ment (collectively, the “Protocol”). The vendor solution transition efforts

through a legislative fix, if one were to Protocol, which received widespread • Develop work plans for contract re-

be enacted. For planning purposes, it support from official sector institutions view and remediation

should be assumed that IBA’s propo- worldwide, facilitates the transition Systems

sal is adopted after the consultation away from LIBOR by providing deri- • E nsure technology teams are on

According to recent comments by an FCA official, the FCA believes it is possible to maintain a representative USD LIBOR until June 30, 2023, and it would not be welcoming

1

and supporting IBA’s proposed extension unless it was confident that representativeness thresholds could be maintained in terms of the number of panel banks. Therefore,

the FCA regards an extension as effectively eliminating the risk of so-called “zombie LIBOR” in any currency.

The joint statement clarified that is not to be read as announcing that the LIBOR benchmark has ceased, or will cease, to be provided permanently or indefinitely or that it is

2

not, or no longer will be, representative for the purposes of language adopted by ISDA. For its part, ISDA similarly clarified that it does not view the statements as constituting

an “index cessation event” or triggering fallbacks.1

1

board with end-to-end UAT as aligned MBS, corporate bonds, leveraged as critical both for product develop-

to ARRC recommendations and end- loans for extraction of qualitative and ment and pricing frameworks as well

user requirements quantitative information needed for LI- as emerging regulatory requirements

• P arallel-test beta systems while BOR evaluation on definitions, fallback from examination guidelines by the

running legacy systems to validate provisions, cost of funds, and consent SEC and the banking agencies. Model

readiness for contract parsing and requirements. Furthermore, classifying development is more advanced for

review across in-scope products language for agent determination, some Syndicated Loan or Cash pro-

• Approve new vendor solutions as they arithmetic means and averages tied to ducts, but less so for Derivatives or

pass each phase of UAT towards go- tough legacy contracts are also driving complex structured products. Sensiti-

live dates per PMO action plan and streamlined vendor implementation. vities in hedging ratios with short-term

steering committee Loan accounting systems are pre- vs. long-term RFR instruments are an

Contracts senting some of the most significant ongoing development challenge.

• Perform contract repository scope challenges, (i.e., a legacy loan accoun-

analysis for all in-scope products ting platform) and separate pricing/de- Model Risk Management

• Map gap analysis findings on legacy rivative product transition issues. Such and Validation Issues

contracts vs. revised contracts long-time technology and infrastruc-

ture tools within many impacted organi- The Technology and Operational Rea-

Both EU and US regulatory bodies have zations continue to create obstacles to diness section above identifies key

reiterated the importance of additional a successful transition when updating issues related to execution against es-

focus to these areas for several years to new and different ARR functionality. tablished project plans for performing

or more. To assist in bridging the gap Based on industry feedback, some analyses on how the new alternative

between firms’ current progress and banks are ahead of the curve in certain reference rates will likely impact inco-

regulatory expectations, the following upgrades for particular technologies/ me, funding, liquidity, and capital le-

actions are recommended: systems while others have lagged vels. The PMO must ensure timelines

behind the LIBOR transition timeline in are met, while also being adaptive to

• A s various ARR / LIBOR models affect terms of legacy system upgrades. The possible changes being communicated

different trading scenarios, the LTO need here is to incorporate current from regulators and market activity.

team must be prepared to implement loan accounting calculator modules And critically, those firms without that

dynamic rate-sensitive systems that that can perform simple, term, arrears, governance and infrastructure in place

adjust to market making decisions in compounded, and weighted-average must also diligently implement the es-

real time calculations that match to vanilla, to sential transition steps.

• Business and technology subject mat- complex, to synthetic IBOR, LIBOR,

ter experts should consider all cost SOFR loan structures. On November 20, 2020, the Alternative

and process dependencies along the Reference Rates Committee (ARRC)

design roadmap, which also includes While many loan term variants will go- published its findings and recommen-

clear milestones for each change du- live before the cessation deadline, dations in a memorandum based on

ring the transition from requirements timelines for upgrades are still not in the view that the post-LIBOR cessation

gathering, to beta, to go-live place from a system implementation will cause major sweeping changes to

• B usiness Requirement Documents perspective. Overall, loan accounting stress forecasting scenarios, PPNR,

(BRD), wireframes, and process flows vendors, large and small, are playing ALM, CCAR, RWA, FRTB and other

should be drafted and finalized accor- catch-up, or are in a “wait and see,” applicable treatments to regulatory

ding to the PMO governance model, modality. The continued regulatory capital and control. The ARRC noted

where approved versions clearly guidance should assist in building out that if the transition were to lead to

support all regulatory mandates the number of firms that can transition unintended increases in capital and

pertaining to LTO operational rea- their systems in 2021.In considering liquidity requirements, this would be

diness. Such documentation should the newest upgrades from loan sys- at cross-purposes with the macropru-

be reviewed by IT Audit and Internal tem vendors, some have expressed dential goal of mitigating risk of the fi-

Audit and stored in a user accessible the view that certain rule require- nancial system as a whole. Prior to the

central repository ments are progressing faster than the ARRC release, in June 2020, the Basel

actual development time needed to Committee on Banking Supervision is-

From conversations with vendors of install and test new modules. This is sued its guidance to clarify ES (Expec-

third-party solutions, success is mea- a difficult problem for firms to solve, ted Shortfall) and IMA (Internal Models

sured by the level of effectiveness in and different sectors have expressed Approach) calculations, along with

quantifying basis risk and market risk individual concerns related to Capital FRTB implementation and Counter-

on the portfolio for selected trading Markets, Asset Management, Lending, party Credit Risk Exposure Estimation

dates. Therefore, delays can be expe- Insurance, and Corporates alike. as per international capital and liquidity

rienced by firms gearing up functio- standards in light of the transitions in

nality to identify contracts for CLOs, Model development has been cited different jurisdictions.1

1

From a risk and valuation perspective, Analytic systems and risk processes certain instruments then many insti-

several other areas will also require that do not support negative rates can- tutions will also be required to adjust

attention of market practitioners. Both not effectively analyze SOFR backed complex frameworks around TLAC (To-

VAR (Value-at-Risk) and LCR (Liqui- floaters in mortgage-backed securi- tal Loss-Absorbing Capacity). As SOFR

dity Coverage Ratio) on the whole are tizations. Applying a floor of zero to may become an increasingly important

potentially at stake, or become dys- floating rates causes systems to com- factor for these models, performance

functional, when there is no historical pute a longer duration for such floaters. modelling will be challenging without

pricing for legacy contract fallbacks A proposed GSE transaction included historical proxy data released by the

(e.g., SOFR / LIBOR credit spread, a floating rate bond with a margin of Fed towards MRM application.

SOFR “term” structure, hedged cash / 330 bps and a floor of zero, indicating

derivatives). Another downside risk will that even with a negative SOFR rate the As RiskSpan has noted in a prior blog,

include legacy / fallback assets, which bond would receive interest. This bond, there is multi-layered risk with the

could result in illiquid assets as they be- if run with SOFR floored to zero, would transition away from LIBOR – market,

come too cumbersome to handle ope- effectively behave like a fixed rate se- operational, strategic, reputational,

rationally, or if trading all moves over curity from a duration perspective. compliance, model risk – which im-

to SOFR based assets. Finally, certain pacts any models that are tasked with

contracts will become non-observable A key data vendor in the structured mitigating or assessing these risks.

in terms of their pricing structure, spe- products space has added a feature Model validators will be focused on

cifically, contracts that are locked in to allow end users to define fallback testing of model inputs, benchmarking

legacy LIBOR, interpolated LIBOR, or approaches for legacy securities. Risk performance relative to the inputs, and

synthetic LIBOR credit spreads and systems would have to maintain a da- assessing the selection process across

term. tabase of fallback methods adapted for alternatives. Validators will also need to

each legacy transaction. Inconsisten- be keenly aware of fallback language,

As of November, daily trading volumes cies across systems and vendors can its interpretation and its application

for SOFR futures have now surpassed lead to discrepancies in pricing and to data and model estimation. Docu-

Fed fund futures and are at about 20% affect secondary trading. Banks and mentation and supporting evidence

of euro dollar. SOFR interest curves other regulated institutions would also from the model developers, whether

now have the beginning of sufficient have to validate their approach on a proprietary or vendor created, will

data points to bootstrap a forward deal-by-deal basis for existing holdings be paramount to meeting the typical

curve to calculate floating rate cou- and any future acquisitions. regulatory and model validation best

pons and discount factors. Interest rate practices required for production mo-

derivative trading is still in its infancy. All these factors combined will have dels. Scheduling of model reviews by

Interest rate models used for risk and material impacts on a variant of regu- MRM teams in 2021, if not completed

valuation are calibrated using volatili- latory reporting requirements, such as already with providers should become

ties from the derivatives market. Lack VAR and RWA (Risk-Weighted Assets), a top priority as we close out 2020 and

of SOFR swaption volatility data will FRTB (Fundamental Review of the move into Q1 of 2021.

prevent analytic systems to calibrate Trading Book) capital charges due to

models using SOFR swaptions and NMRF (Non-Modellable Risk Factors).

use LIBOR swaptions as a proxy. Hed-

ging SOFR backed MBS will remain a Additionally, as we interacted with

challenge until the SOFR swaption mar- the Model Risk Management (MRM)

ket is established. leadership at several participants,

the need to review and analyze the

Agency and corporate bond issuers changes being implemented to mo-

have yet to settle on a standard method dels is on their radar, but still requires

for compounding in arrears for SOFR focus as we move into 2021. With in-

backed floating rate notes. Analytic and ternal system/model and vendor sys-

risk systems must provide the flexibility tem/model implementation timelines

for investors to analyze instruments with extending, and a seemingly uncertain

varying compounding methodologies. LIBOR transition date, MRM teams will

Issuers need similar flexibility to be able be squeezed for time to conduct their

to evaluate an optimal approach before risk assessments across a potentially

issuance. Data vendors need to provi- numerous sets of models, depending

de the ability to maintain arrears calcu- on the portfolio composition of the

lations for SOFR floaters. Investment institution. As a specific example, if

firms also need daily accruals and the fallback amendments or replacement

ability to run scenarios to calculate and rate amendments cause future unin-

monitor exposures. tended negative capital treatment to1

1

Client Outreach and nerally found it challenging to engage tion. This is true even at some of the

certain clients on what the LIBOR tran- largest firms and global banks. A lack

Communication

sition means for them until there was of cohesion among different areas of

more specific detail on SOFR and other the business has the potential to sow

Communication, both internal and

reference rates which are being built doubt internally and with clients alike.

external, is integral to a successful

out. Consistency and efficiency should be

LIBOR transition effort. A robust client

Considering the literature from the prime goals for institutions. Having

communication plan requires appro-

ARRC, the current regulatory lands- clear, concrete answers to common

priate diligence and strategy before

cape surrounding the transition and questions will lower the risk of provi-

being properly executed. As contract

what has been learned from Sia ding employees and clients with incor-

remediation ramps up, client com-

Partners’ research, several best prac- rect information.

munication goes hand-in-hand with

tices have emerged as markers of pro- A third significant marker of progress

contract remediation. Pursuant to the

gress among the most well-prepared has been where an institution has used

ARRC’s recommended best practices,

institutions. The first is the develop- client-based focus groups and/or sur-

for contracts specifying that a party will

ment of business and philosophical veys to establish a baseline understan-

select a replacement rate at its discre-

processes to reach out to clients to ding of where client exposures lie. This

tion following a LIBOR transition event,

demonstrate their commitment to has enabled firms to develop more ac-

there will need to be disclosures of the

completing the transition. This more curate approaches for different types

planned selection to the counterparty

specifically includes early reach-outs of clients and prevent the unnecessary

at least six months prior to the date

to targets in individual business units dedication of resources to clients that

that a replacement rate would become

to establish a remediation timeline. The do not require further elaboration on

effective.

development of these processes is a a particular facet of the transition. We

hugely important first step. As men- found additional firms embracing these

Sia Partners has had a series of ex-

tioned, institutions are continuing to approaches in late 2020 as part of their

changes with industry participants

operate with unanswered questions, transition communication efforts.

and, based on interviews conducted

which if full outreach efforts were to These points and others have been dis-

over the summer and fall, found that

begin, would be passed onto clients. cussed by various regulators. For exa-

nearly half of those financial institutions

The biggest advantage institutions can mple, the comprehension of client ex-

interviewed had reached out to their

gain now is to ensure that their inter- posures and risks (and the prioritization

work streams, organized internally and

nal processes are developed and as of certain segments) was discussed by

started high-level client communica-

clear as possible. The establishment of the Financial Stability Board (FSB) in

tions for a single business unit. When

what an institution wants to gain from its “Global Transition Map,” released

asked about the extent of contract re-

discussions with a client, what types of last October. The FSB asserted that to

mediation conducted, less than a third

clients require what level of education remove remaining dependencies on

of that group were actually remediating

and commitment of time, and how and LIBOR come end-2021, firms should

with client segments. Approximately

when these efforts will be implemented fully understand which LIBOR settings

20% of the overall G-SIB group had

across various internal business lines they have a continuing reliance on af-

engaged across all workstreams with

will offer advantages down the line. ter end-2021 (by currency and tenor)

client segments or had been limited to

Many of the largest institutions, both and what fallback arrangements those

due diligence and planning only. The

foreign and domestic, have developed contracts currently have in place. There

follow-up discussions in December of

those approaches through Q4 of 2020 is an added layer of complexity here, as

2020 suggest progress had been made

and are prepared for a more vigorous there is the reliance on the clients to

across most banking groups in rea-

outreach effort leading to remediation understand their risks themselves. The

ching out to their clients. These efforts

in 2021. When the window of oppor- lack of a strong pattern in responses

included a build-out of their internal

tunity opens to have more informa- among various participant segments is

communication capabilities to educate

tive and educative discussions with an indication that there are questions

their relationship managers and others

clients, those that have not begun and as to who internally will lead the charge

with client responsibilities. Clearly,

completed this preparation phase will (relationship managers, internal legal,

the consultative announcements (as

find themselves having to develop and sales etc.) and how to keep messa-

we note above) will likely affect some

implement a plan concurrently. This is ging and education consistent across

of those efforts while clarity is sought

a theme seen in other aspects of tran- the organization. As noted in the FSB

from the official sector in early 2021.

sition efforts. checklist, the biggest concerns are

Based on Sia Partners’ interviews, the

A second closely related marker of legal, conduct and reputational risks;

preponderance of participants indi-

transition-related progress is ongoing each of which will need to be miti-

cated that efforts through the spring

internal educational efforts for sales, gated by a particular workstream. With

into the summer had focused mostly on

traders and relationship managers. the many unanswered questions that

internal communications. For external

A common observation is the lack of remain for participants, it is clear that

communications, institutions have ge-

coherent messaging across an institu- the majority of participants have notYou can also read