ASTIN 2021 Online Colloquium - Renewable Energy Insurance - An Underwriter's Perspective

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ASTIN 2021 Online Colloquium Renewable Energy Insurance – An Underwriter’s Perspective Sam Millard 18.05.2021

Introducing Codan

RSA & Codan has a FTSE100 listed UK & Western Europe, 9 million customers in

strong and well- general insurer and a Canada and more than 100

balanced portfolio leading provider of Scandinavia. territories; approx

13.500 employees.

with major commercial insurance

operations across for more than 300

years.

the globe.

Strong reputation for RSA is financially The first carbon Knowledge and

technical excellence. strong. S&P rated: A neutral insurer. understanding of

customer need tailors

our service.

3

Agenda o Introduction to the business area e.g. what kind of assets / coverages are we talking about o Codan’s expertise o Where & how actuaries are involved o Volume of exposure / claims data and the challenges this presents o How to handle the consistently emerging risk profile

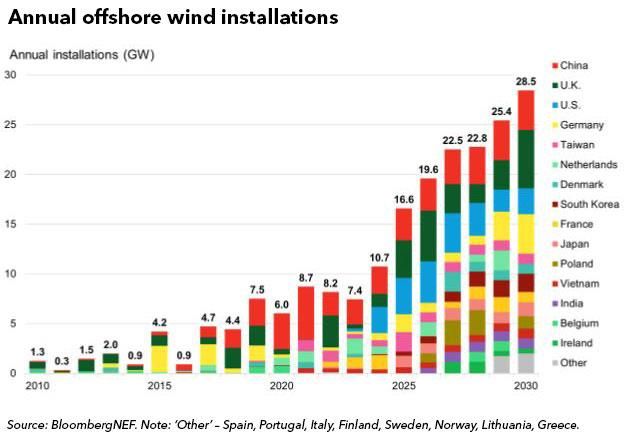

Renewable energy

Different technologies, including: Rapid global growth

5

Renewable energy Offshore wind 6

Products / coverages

There are plenty of available covers e.g.

M&A, TPL, D&O, Cyber, Terrorism,

lack of wind, product efficacy etc etc

Today I will focus on

7

https://www.codan.dk/renewable/bespoke-underwriting-solutions

Providing capacity to more than half of the world’s

offshore wind related construction

1. West of Dudden Sands (389 MW) 20. Horns Rev II (209 MW) 39. Vindeby 58. EirGrid 74. Changhua County 88. Dong Hai 1 –

Phase 2

2. Gwynt Y môr (576 MW) 21. Rhyl Flats (90 MW) 40. Bockstiegen 59. NordLink 75. Greater Changhua

89. Hoah Binh 1 –

3. Global Tech I (400 MW) 22. Provence Grand Large 41. Nysted / Rødsand (166 MW) Phase 2

60. NSN Link 76. Changfang Xidao

4. Dan Tysk (288 MW) 23. Rødsand II (207 MW) 42. North Hoyle (60 MW) 90. Tra Vinh 1-3

61. Nemo Link 77. Southwest Offshore –

5. Baltic II (288 MW) 24. Wave Hub 43. Lynn & Inner Dowsing (194 MW) 91. St Brieuc

Korea

6. Riffgat (108 MW) 25. Samsø 44. Scroby Sands (60 MW) 62. Hohe See 92. Provence Grand

78. Yudean China (portfolio) Large

7. Meerwind (288 MW) 26. Hywind 45. Blyth 63. Merkur Offshore

93. TetraSpar

79. CGN China (portfolio) Demonstrator

8. Butendiek (288MW) 27. Horns Rev I (160 MW) 46. Northwind (272 MW)

64. Albatros

9. Karehamn (48 MW) 28.Lillgrund (110 MW) 47. Amrunbank (288 MW) 80. Akita Noshiro

65. East Anglia 1

10. Humber Gateway (220 MW) 29. Borkum West II (200 MW) 48. Q10 (129 MW) 81. Naert Na Gaoithe

66. Deutsche Bucht

11. Teesside (62 MW) 30. C-Power Phase II+III (295 MW) 49. BorWin 1 & 2

82. Kaskasi

12. Baltic I (48 MW) 31. Alpha Ventus (60 MW) 50. SylWin 1 67. IFA 2

83. Hornsea I

13. Robin Rigg (180 MW) 32. Nordsee Ost (288 MW) 51. HelWin 1 & 2 68. Kincardine

14. Barrow (90 MW) 33. Sheringham Shoal (315 MW) 52. DolWin 1 & 2 84. Fecamp

69. Formosa 1, phase 2

15. Burbo Bank (90 MW) 34. Ormonde (150 MW) 53. Fukushima Recovery Project phase 1 + 3 85. SeaGreen

70. Triton Knoll

16. Kentish Flats (90 MW) 35. London Array Phase I (630 MW) 54. Gemini Offshore Wind Farm (600MW)

86. Beatrice

17. Greater Gabbard (504 MW) 36. Lincs (270 MW) 55. Wikinger 71. WindFloat Atlantic

87. Tra Vinh

18. Thanet (300 MW) 37. Utgrunden 56. Nordsee One 72. Yunlin

8

19. Lillgrund (110 MW) 38. Ytre Stengrund 57. WindFloat

73. Formosa 2

OUR OFFSHORE RENEWABLE ENERGY TEAM

Sales & Underwriting

Brendan Reed, Nordic Director CE&RE

Sam Millard Chief Underwriter Tech Lines

Igor Silence Global Head of Offshore Wind Energy

Tom D. Kristiansen Senior Risk Engineer, BSEE

Lutz Weidtke, Senior UW

Henrik Møller Senior Specialist Underwriter

Jan Petersen Senior UW

Michael Schlüter Senior UW

Jakob Rasmussen Strategic Sales and Business Development

Claims Management Support functions

Torben Larsen, Manager, B.sc. Including:

Claus Hein Senior Large Claims Specialist, B.sc Portfolio Management

Jørn Heintz Senior Claims Handler Pricing

Johan Nissen Senior Claims Handler Reserving

Finn Thyrring Manager, Senior Risk Engineer, B.sc. Reinsurance

Product development

Peter Krarup Senior Risk Engineer

Kasper Kroman Risk Engineer

Mads Nørsøller Senior Risk Engineer

Client team tailored to service our individual clients and brokers

Key components of an offshore wind farm

Wind turbines & Offshore substations Cables

Foundations

10New Technologies from the beginning – “unproven” …..

… but not unknown – a general view:

• Not a new situation for the insurance

industry as we have dealt with this for the

last 30 years

• Projects always include unproven elements

like new suppliers, environment, soil

condition and execution

• Proven technology is considered after of

trouble-free installation, testing and

successful 8000 hours operation

1991 2004 2008 2010 2017 2018 ???

11What has changed beyond NEW technologies from a risk

perspective?

• Bigger projects = larger investments = higher sum insured / higher limits

• New risks/environment = NATCAT, far from shore

• Higher pressure on Lower Cost of Energy = costs to be reduced

• Faster development (no track-record available when risk needs to be bound by insurance)

• Besides fast technical development, also extensions of wordings driven by lenders and developers vs. less

track-record of technology / components and contractors

• Territorial expansion

12Underwriting Considerations

Technology risks

Proven technologies Physical factors

Costs to repair Distance from shore

Vessel costs, long term charter Sea & geography

Water depth

Insurance

Terms and conditions

Deductibles

Defects exclusions Contractors

Series losses Experience

Sublimits Tools and equipment

Delay in startup Installation methodology

Warranties & extended and timeline

maintenance periods

13The role of actuaries

Volume of data

Approximately how many entries are in Codan’s offshore wind claims database (2002 – 2021) – which

I assume is (by far) the largest industry data-set:

a) 120

b) 1,200

c) 12,000

14Approximately how many entries are in Codan’s offshore wind claims database (2002 – 2021) – which

I assume is (by far) the largest industry data-set:

a) 120

b) 1,200

c) 12,000

Average a little over 1 per week during the full period

15Reserving challenges

Case study:

Customer contacts Codan: ”My cable stopped working at 4am – we are trying to establish what

has happened”.

- Is there damage or not? Where has the damage occurred?

- What is the root cause (do any exclusions apply)?

- What kind of set-up will be required for investigation & repair?

- What is the likely downtime?

- Will there be subrogation opportunities?

Case reserve?

Technical reserves

- ‘Medium tail’

- Reporting delays (FNOL)

- Portfolio risk-mix

16Pricing challenges

• Continuously evolving risk profile

• 100+ ‘UW factors’ in pricing tool but relatively limited claims data

• Varied scope of cover

• Rapid industry cost reduction (at least on CAPEX, if not repairs)

• Uncertaintly over correct large-loss funding

- No ‘market standard’ (e.g. Lloyd’s, SwissRe) loss curves

• Vulnerability to particular perils e.g. earthquake, tropical windstorm

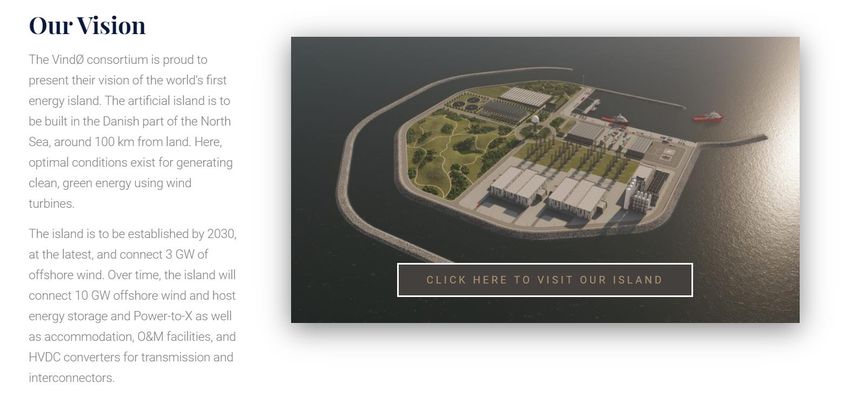

17Future underwriting challenge 18 https://www.windisland.dk/

Closing remarks

• Great to see initiative and technical development in offshore wind

• Strong cross-function collaboration is essential. Pricing & reserving actuaries

cannot operate effectively without input from

- Claims handlers

- Underwriters

- Business leaders

etc

• The specific profile of this sector means that actuaries with a creative, open-

minded approach will add most value

19Thank you,

Any Questions?

20Disclaimer Codan Forsikring A/S This PowerPoint presentation (the “Presentation”) is offered to you by Codan Forsikring A/S (company reg. no. 10 52 96 38) (“Codan”) and is for the exclusive use of the persons to whom it is addressed. The content of the Presentation, including all texts, images and audio fragments, is protected by copyright laws and may not be copied, distributed, published, reproduced or disclosed without Codan’s prior written consent. No changes whatsoever may be made to the content. The Presentation does not purport to be comprehensive or to contain all the information that a recipient may need in relation to the proposed transaction or purpose, for which it was produced. Interested parties should conduct and rely on their own investigation and analysis and not the data contained in the Presentation. Codan endeavours to provide correct and up-to-date information, but Codan makes no representations regarding the correctness, accuracy or completeness of the Presentation. The Presentation may contain forward-looking statements regarding the intentions, expectations, objectives or targets of Codan. Any such forward-looking statements are based on assumptions that Codan believes to be reasonable, but are subject to a wide range of risks and uncertainties and, therefore, there can be no assurance that actual results will meet those expressed or implied by such forward-looking statements. Codan does not accept any liability for any (alleged) damage arising from the Presentation or for any consequences of activities undertaken based on data or information contained therein. By receiving the Presentation, you accept the terms and conditions above. 21

You can also read