Australia India Institute Volume 20, February 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Australia India Institute Volume 20, February 2021

Fostering Opportunities in Video Games between

Victoria and India

Dr Jens Schroeder

Fostering Opportunities in Video Games between Victoria and India

The Australia India Institute, based at The University of Melbourne, is funded by Australian Government Department of Education, Skills and Employment, the State Government of Victoria and the University of Melbourne.

Summary Video games are booming all over the world, during the COVID-19 pandemic more than

ever. Australia and India are no exceptions. This policy brief focuses on the opportunities

for both Indian and Victorian game developers and educators in the context of the

Victorian government's support for its creative industries. Based on desk research and

discussions at the Victoria-India Video Games Roundtable conducted on 8 December

2020 by the Australia India Institute in collaboration with Creative Victoria and Global

Victoria, this report identified the following avenues for collaboration:

• Access to complementary expertise and talent in both countries

• Joint education programs and exchanges

• Victorian game developers working with Indian partners to adapt their games to the

Indian market and its complexities and challenges

Introduction Video games1 are one of the world's largest and fastest-growing entertainment and media

industries. In Australia, Victoria is the hotspot for game development. With 33% of all

studios and 39% of all industry positions,2 more studios call Victoria home than any

other state in Australia. Meanwhile, India's smartphone penetration has skyrocketed

to the point where the country has become the world's most avid consumer of mobile

gaming apps.

This policy brief sets out to explore how Victoria-based game developers and

educators can take advantage of this emerging market and the opportunities it presents.

It establishes a frame of reference by highlighting the characteristics of both markets:

India, as a highly complex mobile-centric consumer market whose traditional service

approach to games has resulted in unmet demand for certain production skills, stands

opposite a product-centric Australia, where the long engagement with video games

has led to a successful international outlook and track record and the corresponding

acquisition of expertise.

Based on these insights, this policy brief explores three areas of opportunity. First,

joint ventures that can support Indian developers to strive towards more sophisticated

products while Indian talent can support Australian studios in their growth.

Secondly, collaborations between educational providers and other stakeholders

with complementary skills applied to educational activities on a number of levels

(undergraduate, postgraduate, internships, incubators). Thirdly, partnerships where

Australian game developers wanting to enter the highly stratified Indian consumer

market can benefit from the Indian partner’s market insights.

1 Video and digital games are used interchangeably in this report. For purposes of this report, ‘games’ do not include

applications that replicate types of gambling in virtual form. While these games are made in Australia and are popular in India,

IGEA does not represent developers that focus on these kinds of titles. Members’ games can include behaviourist monetisation

techniques, but their core does not revolve around casino-style gameplay.

2 IGEA (2019) Australian Video Game Development Industry Contributes to Exports and Job Opportunities. https://igea.

net/2019/11/australian-video-game-development-industry-contributes-to-exports-and-job-opportunities/

4

Victoria’s Victoria's Creative State strategy highlights the importance of the sector to the state

economy. Creative industries – including digital games along with the visual and

Video Game performing arts, literature and publishing, music, screen production, design and fashion

– contributed $22.7 billion to Victoria’s economy in 2015 and employed 290,000 workers

Strategy

or 8.6% of Victoria’s workforce.3

While the Creative State strategy's original vision has been disrupted by the COVID-19

pandemic and its further development was paused to address the acute and immediate

impacts facing the sector, Victoria’s ongoing support of the creative industries is not

just reflected in temporary relief measures but also the ongoing maintenance of existing

programs. Initiatives include Film Victoria's Games Release Fund and Assigned

Production Investment for games as well as the recently announced allocation of AU$19.2

million to attract international and interstate screen projects to the state. The vast majority

of the investment will be committed prior to 30 June 2021 and will more than double Film

Victoria’s investment in the development of locally generated digital games.4

The Victorian gaming industry is also supported by the Interactive Games &

Entertainment Association (IGEA), the peak industry association representing the voice

of Australian companies in the computer and video games industry. IGEA supports the

business and public policy interests of the games industry, through advocacy, research

and education programs. Its mission is to create an environment that supports and drives

sustainable growth for the interactive games and entertainment industry.

Victoria’s commitment to strengthening the links with India in the digital gaming sector,

including gamification, is recorded in Victoria’s India Strategy. The strategy asserts

that Victoria will continue to promote and support commercial opportunities with

Indian partners,5 an initiative whose potential this policy brief will further explore. The

brevity of this paper and the ever-changing dynamics of the Indian market mean that it

should be treated as a step towards further conversations between the two countries for

exploring opportunities in more detail.

3 Creative Victoria (2020) About. https://creative.vic.gov.au/about

4 Film Victoria (2020) Press Release. Levelling Up Support for Victoria’s Digital Games Sector.

5 Victoria State Government (2018) Victoria’s India Strategy (Melbourne: Victoria State Government), p. 36.

5

Association (IGEA), the peak industry association representing the voice of Australian companies in

the computer and video games industry. IGEA supports the business and public policy interests of

the games industry, through advocacy, research and education programs. Its mission is to create an

environment that supports and drives sustainable growth for the interactive games and

entertainment industry.

Victoria’s commitment to strengthening the links with India in the digital gaming sector, including

gamification, is recorded in Victoria’s India Strategy. The strategy asserts that Victoria will continue

to promote and support commercial opportunities with Indian partners,5 an initiative whose

potential this policy brief will further explore. The brevity of this paper and the ever-changing

dynamics of the Indian market mean that it should be treated as a step towards further

conversations between the two countries for exploring opportunities in more detail.

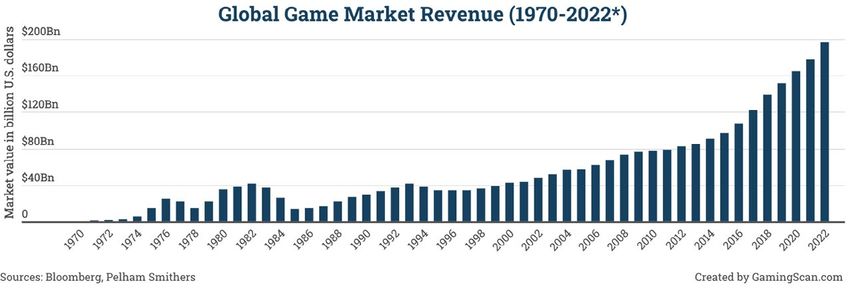

The Global Video Games Market

The Global The interactive games sector is one of the largest and fastest growing entertainment and

media industries

The interactive games in the world.

sector is oneEstimated to be

of the largest andworth

fastestalmost

growingAU$280 billionand

entertainment globally

media by

Video Games 2023 in the1),

(Figure games are bigger

to bebusiness thanAU$280

films, music and books.

6

industries world. Estimated worth almost billion globally by 2023 (Figure 1),6

games are bigger business than films, music and books.

Market Figure

Figure 1:1:Global

Global Game

Game Market

Market Revenue

Revenue (1970-2022)

(1970-2022)

Source: Gamingscan. https://www.gamingscan.com/gaming-statistics/

3

Creative one

Already Victoria

of (2020) About. https://creative.vic.gov.au/about

the world’s largest and fastest-growing entertainment industries before

4

Film Victoria (2020) Press Release. Levelling Up Support for Victoria’s Digital Games Sector.

COVID-19

5 hit, gaming has further expanded during the lockdowns. With the ongoing

Victoria State Government (2018) Victoria’s India Strategy (Melbourne: Victoria State Government), p. 36.

global

6 proliferation

Tom Wijman (2020) TheofWorld’s

smartphones, new monetisation

2.7 Billion Gamers models,

Will Spend $159.3 and

Billion on the in

Games refinement of

2020. Newzoo.

https://newzoo.com/insights/articles/newzoo-games-market-numbers-revenues-and-audience-2020-2023/

revenue streams such as microtransactions, games are increasingly attracting mainstream

consumers. Video games have amongst the largest support base of any creative industry

with over 2 billion gamers globally. The traditional markets of North America and Europe

have seen accelerated growth rates, and the Asia-Pacific region has an estimated 1 billion

gamers and already accounts for more than half of all global game revenue.7

Video Games Gaming in India has grown on the back of smartphone penetration, low data costs,

improved bandwidth, growth in micropayments and the rise in disposable income. The

in India

number of smartphone users in India was expected to reach 530 million by the end of

20208 while the number of all gaming consumers was poised to rise to 628 million within

the same timeframe.9 As a result, the Indian mobile games market alone is expected to

grow to US$1.1 billion.

Traditionally, access to video games in India has been limited; the high cost of hardware

and the need to install games from physical media resulted in a limited appeal of PCs

and consoles as well as a comparatively underdeveloped gaming culture.10 Increased

accessibility came with (Android) smartphones and the ability to download mobile

applications and games over WiFi and mobile networks at low costs (with 1 GB of

data costing AUD 1$ or less). Excluding Chinese third-party app downloads, India

was the leading market for app downloads in Q2 2020, with nearly 7 billion, followed

6 Tom Wijman (2020) The World’s 2.7 Billion Gamers Will Spend $159.3 Billion on Games in 2020. Newzoo. https://newzoo.

com/insights/articles/newzoo-games-market-numbers-revenues-and-audience-2020-2023/

7 Guilherme Fernandes (2019) Navigating the world’s fastest-growing games market: Insights into Southeast Asia NewZoo.

https://newzoo.com/insights/articles/navigating-the-worlds-fastest-growing-games-market-insights-into-southeast-asia/

8 Austrade India (2019) Digital Games Sector Market Insights (Perth: Austrade), p. 2.

9 2020: The up-and-coming year for Indian gaming industry! Hindustan Times. https://www.hindustantimes.com/brand-

stories/2020-the-up-and-coming-year-for-indian-gaming-industry/story-FZdh2XYuCVmXF5DoomuovK.html

10 Austrade India (2019), p. 2.

6by the US with around 3.75 billion.11 Correspondingly, India has also become one of

the top five markets for mobile gaming in terms of number of users.12 In 2019, around

5.6 bn mobile gaming apps were downloaded in India – the highest in the world and

representing nearly 13% of gaming apps globally.13 Between 2016 and 2019, Indian app

downloads grew 190% (Figure 2). In addition, mobile games account for 80-90% of the

overall online gaming segment. KPMG classifies over half of India’s 365 million gaming

consumers as “online gamers.”14

PC and console gaming are projecting muted growth, catering to a limited, albeit

engaged, audience. ‘Hardcore gaming’ in its traditional form demands time and

dedication along with access to PCs or consoles and therefore appeals to a smaller set

of audiences. In contrast, mobile gaming is expected to gain at their expense, given its

inherent flexibility and convenience.

Figure 2: Growth in app downloads by country, 2016-2019 (App Annie)

GLOBAL CHINA INDIA UNITED BRAZIL INDONESIA

45% 80% 190% STATES 40% 70%

5%

Source: Iqbal (2020)

In terms of demographics and user engagement, India is approximating global trends.

In 2018, the average time spent on gaming was close to reaching the global average

(6.92 hours per week for India vs 7.11 hours per week for the rest of the world). While

a younger audience still dominates, older players are increasingly engaging; nearly

one-third of the gaming population in India is now aged over 35 years. Moreover, the

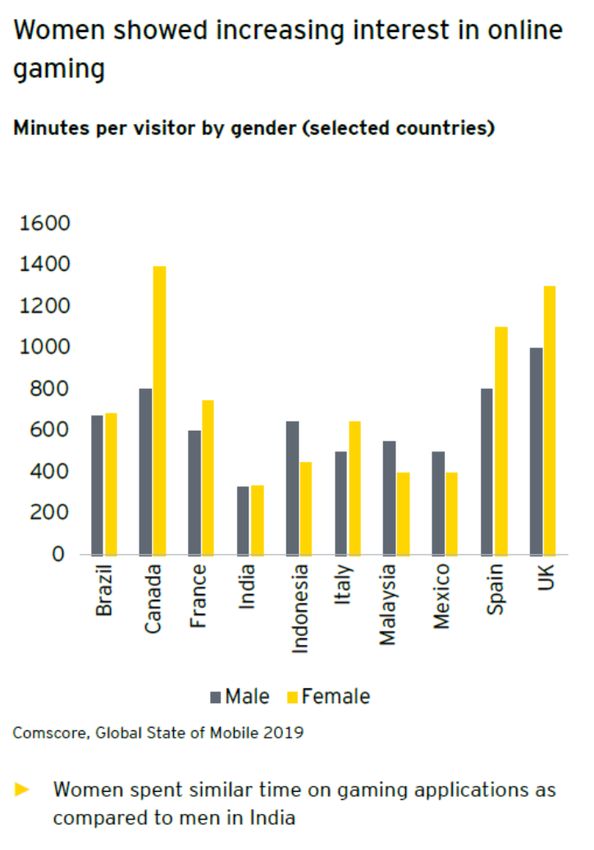

percentage of female gamers has risen to 45%.15 Women in India are showing increased

interest in online gaming and spend similar time on gaming applications compared to

men in India (Figure 3).

11 Mansoor Iqbal (2020) App Download and Usage Statistics (2020) Business of Apps. https://www.businessofapps.com/data/

app-statistics/

12 KPMG (2019) India's Digital Future (India: KPMG), p. 106. https://assets.kpmg/content/dam/kpmg/in/pdf/2019/08/india-

media-entertainment-report-2019.pdf

13 Iqbal (2020).

14 KPMG (2019), p. 106.

15 KPMG (2019), p. 105-106.

7Source: Iqbal (2020).

In terms of demographics and user engagement, India is approximating global trends. In 2018, the

average time spent on gaming was close to reaching the global average (6.92 hours per week for

India vs 7.11 hours per week for the rest of the world). While a younger audience still dominates,

older players are increasingly engaging; nearly one-third of the gaming population in India is now

aged over 35 years. Moreover, the percentage of female gamers has risen to 45%.15 Women in Ind

are showing increased interest in online gaming and spend similar time on gaming applications

compared to men in India (Figure 3).

Figure 3: Minutes per visitor by gender (selected countries)

Figure 3: Minutes per visitor by gender (selected countries)

Source: Global Victoria (2020). Presentation: Session on the Indian Gaming Ecosystem – Overview, Challenges,

Source: GlobalTrends

Victoria (2020). Presentation: Session on the Indian Gaming Ecosystem – Overview,

and Opportunities.

Challenges, Trends

Due toand

theirOpportunities.

free-to-play approach, casual games – including casual ‘real money’ games

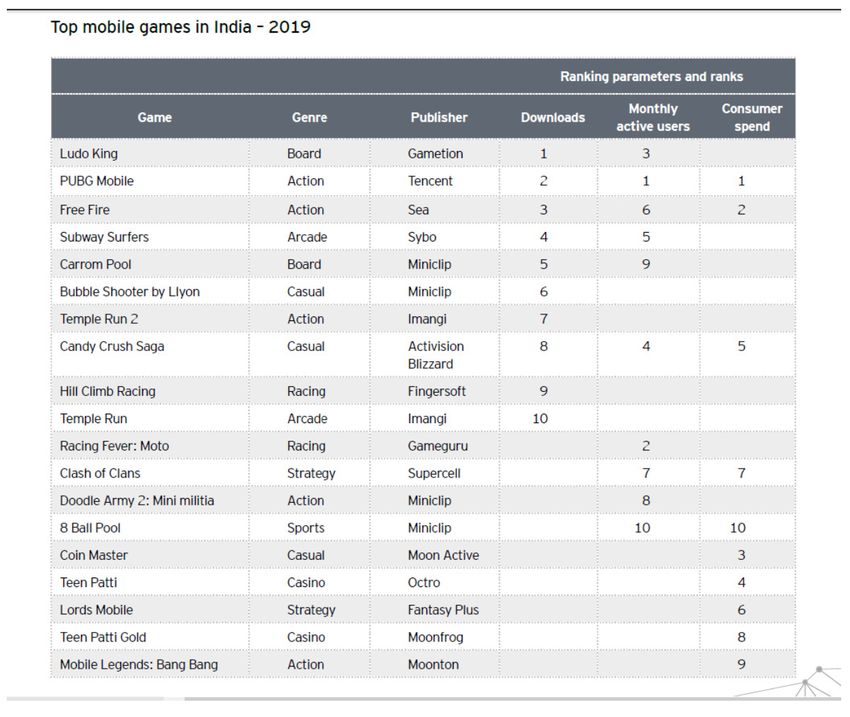

such as rummy, poker, fantasy sports, and quiz games – are the most popular genre in

India (see Table

Due to their free-to-play 1).16 These casual

approach, types of games

gamesare–played by approximately

including 80%money’

casual ‘real of all gamers.

games such as

A successful example of a casual game is Ludo King. Based on the eponymous board

rummy, poker, fantasy sports, and quiz games – are the most popular genre in India (see Table 1).1

game, this locally developed title was the first Indian gaming app to surpass 100 million

These types ofdownloads.

games are By played by approximately

January 2020 80%

it had surpassed 300 of all

million gamers.and

downloads A could

successful

boast 75example of a

casual game ismillion

Ludo King.

monthly Based

active on the

users. eponymous

COVID-19 board

lockdowns game, this

encouraged locally

an even developed

stronger uptake of title was th

first Indian gaming app of

these types togames

surpass 100 million

and attracted downloads.

new users By January

in the process. 2020 itLudo

Correspondingly, hadKing’s

surpassed 300

adoption further accelerated, in the second quarter of 2020 alone it was downloaded over

60 million times, making it the world’s fifth-most popular app.17

15

KPMG (2019), p. 105-106.

KPMG (2019),Likewise,

p. 104. other non-fantasy real money games continued to see “tremendous uptake,”

18

16

with traditional card games such as Teen Patti, Rummy and Poker continuing to lead the

segment due to their potential for social connection, mass appeal, and loyal user base.

16 KPMG (2019), p. 104.

17 Iqbal (2020).

18 KPMG (2019), p. 107.

8million downloads and could boast 75 million monthly active users. COVID-19 lockdowns

encouraged an even stronger uptake of these types of games and attracted new users in the

process. Correspondingly, Ludo King’s adoption further accelerated, in the second quarter of 2020

alone it was downloaded over 60 million times, making it the world’s fifth-most popular app.17

Likewise, other non-fantasy real money games continued to see “tremendous uptake,”18 with

traditional card games such as Teen Patti, Rummy and Poker continuing to lead the segment due t

their potential for social connection, mass appeal, and loyal user base. Over half (55%) of the US$1

billion Indian games market comes from real money gaming; the prospect of earning some money

on the side and ability to show off one’s skills drive annual growth rates between 40% and 50%.

Over half (55%) of the US$1.1 billion Indian games market comes from real money gaming;

Tablethe

1: Top mobile

prospect gamessome

of earning in India 2019

money on the side and ability to show off one’s skills drive

annual growth rates between 40% and 50%.

Table 1: Top mobile games in India 2019

Source: Global Victoria (2020). Presentation: Session on the Indian Gaming Ecosystem – Overview, Challenges,

Trends and Opportunities.

Source: Global Victoria (2020). Presentation: Session on the Indian Gaming Ecosystem – Overview,

Online fantasy sports, meanwhile, suffered a temporary setback. While witnessing strong

Challenges, Trends and Opportunities.

growth on the back of India’s Premier Cricket League in 2019 (Figure 4), these games were

negatively impacted by the cancellation of sports events due to the COVID pandemic.19

Online fantasy sports, meanwhile, suffered a temporary setback. While witnessing strong growth o

the back of India’s Premier Cricket League in 2019 (Figure 4), these games were negatively impact

by the cancellation of sports events due to the COVID pandemic.19

17

Iqbal (2020).

18

KPMG (2019), p. 107.

19

Poonam Mondal (2020) By 2022 gaming sector will witness growth in revenue at 45 per cent CAGR: KPMG

Animation Express. https://www.animationxpress.com/games/by-2022-gaming-sector-will-witness-growth-

revenue-at-45-per-cent-cagr-kpmg/

19 Poonam Mondal (2020) By 2022 gaming sector will witness growth in revenue at 45 per cent CAGR: KPMG. Animation

Express. https://www.animationxpress.com/games/by-2022-gaming-sector-will-witness-growth-in-revenue-at-45-per-cent-

cagr-kpmg/

9Figure 4: Growth in Indian Fantasy Sports

Figure 4: Growth in Indian Fantasy Sports

Source: KPMG (2019), p. 108.

The growth of the Indian games market also highlights how gaming platforms are emerging

as community networks beyond mere entertainment, enabling families and friends to

Source:

connect and share experiences. KPMG

In 2018, Hello(2019), p. 108.

Ludo introduced an in-game voice chat that

resulted in daily active users spending more than 25 minutes in it. Almost half (46%) of

the Indian Player Unknown's BattleGrounds Mobile (PUBG Mobile) players use the in-game

The growth of the Indian games

voice chat featuremarket also

to discuss not onlyhighlights

game tactics buthow gamingtopics

also non-PUBG platforms

at length.20 are emergin

(PUBG is the pioneer of the hugely popular ‘battle royale’ genre, “a large-scale free-for-all

community networks death

beyond mere

match with entertainment,

the goal enabling

to be the last player alive.

”)21 families and friends to connec

share experiences. In What

2018, Hello Ludo introduced an in-game voice chat that resulted in d

all these numbers do not immediately reveal is the diversity of the Indian market.

users spending more than

India is 25

not aminutes in it.butAlmost

monolithic block half (46%)

a highly complex ecosystemof the

with Indian Player Unknow

demographics

extending across the whole range of the socio-economic spectrum and a rapid evolution in

BattleGrounds Mobilegamers’

(PUBG Mobile) players use the in-game voice chat feature to discuss

tastes – even further accelerated by COVID-19 – illustrated in the astronomic rise

game tactics but also ofnon-PUBG topics

battle-royale action at length.

title PUBG Mobile into (PUBG

20

is the pioneer

the charts alongside ofcasino

the casual and the hugely popu

royale’ genre, “a large-scale free-for-all death match with the goal to be the last player aliv

games that have dominated (see Table 1).

In 2019, there were between 33 and 50 million PUBG Mobile players in India. By early

2020, 116 million downloads came from the subcontinent, a number amounting to 21%

What all these numbers do downloads.

of global not immediately

22 reveal

The trend towards moreis the diversity

sophisticated mid-coreof the Indian

to hardcore games market. In

monolithic block but awith

highly complex

multi-player setups isecosystem with

also reflected in the demographics

popularity extending

of Garena Free Fire, which saw across the

a marked increase in downloads after the Indian government banned the Chinese-made

range of the socio-economic

PUBG Mobile spectrum

due to borderand a rapid

tensions evolution

with China. Indian gamersinalso

gamers’

accountedtastes – even furth

for 15% of

accelerated by COVID-19

global – illustrated

downloads of 2020’sin thehitastronomic

global title Among Us. rise of battle-royale action title PU

23

into the charts alongside the casual and casino games that have dominated (see Table 1).

20 KPMG (2019), p. 107.

21 Alessandro Fillari (2019) Battle Royale Games Explained: Fortnite, PUBG, And What Could Be the Next Big Hit.

Gamespot. https://www.gamespot.com/articles/battle-royale-games-explained-fortnite-pubg-and-wh/1100-6459225/

In 2019, there were between 33 and 50 million PUBG Mobile players in India. By early 2020

22 Kayleigh Partleton (2019) PUBG Mobile shoots through $1.5 billion in lifetime revenue Pocket Gamer. https://www.

pocketgamer.biz/asia/news/72145/pubg-mobile-1500000000-lifetime-revenue/

million downloads came from the subcontinent, a number amounting to 21% of global dow

23 Ananya Bhattacharya (2020) Nearly 20% of all mobile game downloads in the world this year were from India. Quartz

India. https://qz.com/india/1937845/pubg-among-us-crazy-indians-downloaded-7-3-billion-games-in-2020

The trend towards more sophisticated mid-core to hardcore games with multi-player setu

10 reflected in the popularity of Garena Free Fire, which saw a marked increase in downloadsThis evolution in taste coincides with a burgeoning e-sports scene. India is ranked number

17 in the US$1.5 billion e-sports industry and is growing rapidly.24 Mobile-based games like

PUBG Mobile and Garena Free Fire helped to overcome latency problems (delays between

user actions and game responses) and the lack of expensive high-end computer hardware,

the traditional platform of choice for e-sports titles. E-sports personalities are emerging, the

prize pools for e-sports tournaments are increasing and, further accelerated by COVID-19,

viewership of streamed e-sports competitions is gaining popularity with the potential to

match the viewership of major sports event over the next five to seven years.

The dominant monetisation strategy, regardless of genre, is free-to-play. The casual segment

is largely supported by in-game advertising although there has been an increase in the

popularity of freemium models (gamers making an in-game-purchase for an additional

boost or to advance quicker in the game), as part of the uptake of mid-core to hardcore

games. In 2019, 28% of gamers were willing to make an in-app purchase for an additional

boost in their gaming experience. While the casual segment relies on in-game advertising,

it is also starting to witness this change in monetisation approaches.25 Expectedly, gamers

from an older demographic have a higher propensity to spend on games due to higher

disposable income. Furthermore, growth in fantasy sports and other real money gaming

platforms is likely to accelerate monetisation even further.

Monetising mobile games represents the biggest opportunity for growth, but it is also the

most vexing barrier. India paints the image of a market whose strength primarily lies in

its sheer size while ongoing claims of its imminent explosion are yet to (fully) materialise.

Ultimately, while the market appears very large from the outside, the number of people

willing to make in-game-purchases is limited to about 40-50 million. That is not to dispute

the industry's tremendous growth in India, but rather to demonstrate the nuance and

complexities of the Indian demographics and cultures.

Monetisation is also curtailed by India’s predominantly cash-based economy. There are only

20 million credit cards in circulation in India, the idea of credit is viewed with a certain

scepticism, and the consumer base is cost conscious.26 In recent commentary on average

revenue per user among newly released games in 2019, mobile analytics company App

Annie stated that India generated “zero” revenue.27 This somewhat exaggerated statement

primarily serves to highlight the disparity between the number of downloads and paying

users, and does not take into consideration real money apps as these are downloaded

outside of Google’s Play Store. Nevertheless, international developers need to be mindful

of the need to find their niche between casual and hyper casual ad-monetised mobile

games with little scope for in-app-purchases outside of the real-money gaming scene, and

the narrow monetisation band of the global phenomena of games like Clash Royale and

PUBG Mobile.28 While in-app-purchases have grown between 70-80% over the last year,

this growth has been very concentrated and mostly confined to the top three or four games.

Revenue drops considerably for titles any lower on the charts.

24 The rise of eSports in India Business Matters. https://bmmagazine.co.uk/business/the-rise-of-esports-in-india/

25 KPMG (2019), p. 107.

26 Haydn Taylor (2019) IGDC: Solving the Monetisation Problem in India Gamesindustry.biz. https://www.gamesindustry.biz/

articles/2019-01-09-solving-the-monetisation-problem-in-india

27 Amit Raja Naik (2020) India Tops the World for App Downloads. But Has ‘Zero’ Gaming Revenue: App Annie. Inc42.

https://inc42.com/buzz/india-tops-the-world-for-app-downloads-but-has-zero-revenue-app-annie/

28 Taylor (2019).

11Another “major roadblock” is the ambiguity around the laws that govern gaming in

India, in particular real money games.29 Under most Indian laws, gambling activities are

referred to as ‘gaming’. Though the Constitution of India gives states the power to pass laws

regulating gambling and betting, there is no clarity regarding online gaming.

Despite these challenges, the Indian market is poised for continued growth. An expanding

user base, advanced monetisation strategies, the growth in e-sports and expanding

infrastructure translate into an estimated compounded growth rate of 32% over the period

between 2020 and 2024.30

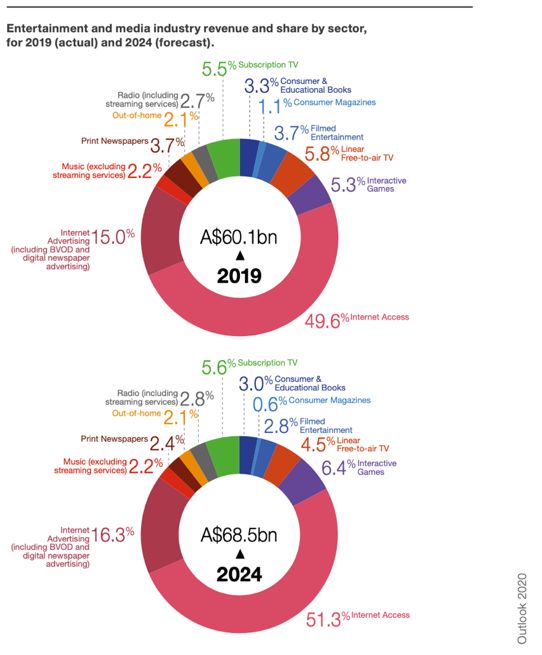

Video Games Australians spent over $4 billion on video games and games hardware in 2018, a 25%

increase from 2017.31 This means Australians spend more on games than they spend on

in Australia

films (three times as much32), streaming services, Pay TV, music, books or likely any other

creative or entertainment activity (Figure 5). Spending dipped below $4 billion in 2019 due

to the 8th console generation (PlayStation 4 and Xbox One) reaching the end of its lifecycle

but is expected to pick up considerably in 2020 with major new hardware and games

releases due and in light of the increase in game play during the COVID-19 pandemic.

A recent PwC report places Australia as one of the highest per capita spenders on video

games in the world.33 This affection for games is also reflected in the demographics of

Australian consumers: two out of every three Australians play games; the average age of

the Australian game player is 34 and video games are almost equally played by males and

females. Over 40% of Australians aged over 65 play games to keep their minds sharp, to stay

active, and to spend time with their grandchildren. Moreover, nine out of ten Australian

households own at least one gaming device.34

Australians’ close relationship with games also translates into a long history of successful

game production. Australian-made games featured heavily on home computers in the

1980s. Beam Software's The Hobbit introduced ground-breaking gameplay and sold over

a million copies while their Way of the Exploding Fist paved the way for ‘beat-em-ups’. In

1986, Beam International sales had ten per cent of the UK market across all formats. The

1990s and early 2000s saw the birth of new studios and the export of titles popular on

the international stage. Australian studios released or worked on such innovative titles as

Dark Reign, Destroy All Humans, LA Noire or BioShock and cemented their reputation as

world-class sources of game content. In a changing industry, Australian studios successfully

rode the wave of mobile games. Flight Control started a trend that saw Fruit Ninja being

downloaded more than a billion times and Crossy Road climb the worldwide app charts.

In recent years, the PC became the dominant platform for game developers and games like

Hacknet, Satellite Reign, Ashes Cricket or Hand of Fate demonstrated Australia's continued

versatility and ability to create internationally successful intellectual property (IP).

29 KPMG (2019), p. 109.

30 KPMG (2019), p. 109.

31 IGEA (2019) Consumer spending breaks through the $4 billion mark. https://igea.net/2019/05/aussies-love-for-video-games-

continues-to-grow

32 Screen Australia (2019) 2019 Snapshot: Cinema Industry Trends. https://www. screenaustralia.gov.au/fact-finders/cinema/

industry-trends/ box-office

33 PwC (2020) Australian Entertainment & Media Outlook 2020-2024 (Sydney: PwC), p. 13.

34 IGEA (2019) Digital Australia (Sydney: IGEA), p. 7.

12Figure 5: Entertainment and media Industry revenue and share by sector for 2019

(actual) and 2024 (forecast)

Source: PwC (2020), p. 3. Source: PwC (2020), p. 3.

A recentAPwC

recent survey

report by IGEA

places found as

Australia that,

oneinofthethe

2018-2019

highest perfinancial

capita year, Australian

spenders studios

on video games in the

world.33generated $143.5for

This affection million

games (see Appendix

is also A).35inThe

reflected thelocal industry employed

demographics 1,275 fulltime

of Australian consumers: two

equivalent

out of every threeemployees

Australians and,

playowing to itsthe

games; small domestic

average agemarket, generated 83%

of the Australian game ofplayer

its is 34 and

revenue

video games areoverseas. There has

almost equally been aby

played marked

malesincrease in focus

and females. on Asian

Over 40% ofmarkets,

Australianswith aged

65% over 65

of respondents

play games to keep theirdeveloping for Asian

minds sharp, markets,

to stay active,up and

fromto37% in 2017.

spend timeOther international

with their grandchildren.

markets

Moreover, nineinclude the US

out of ten and Europe.

Australian Australian

households ownstudios

at leastareone

creative

gamingand device.

focused34with

almost two-thirds (61%) of respondents exclusively developing their own IP. A further

Australians’ close relationship with games also translates into a long history of successful game

production. Australian-made games featured heavily on home computers in the 1980s. Beam

Software's The Hobbit introduced ground-breaking gameplay and sold over a million copies while

35 IGEA (2019) Australian Video Game Development Industry Contributes to Exports and Job Opportunities.

their Way of the Exploding Fist paved the way for ‘beat-em-ups’. In 1986, Beam International sales

had ten per cent of the UK market across all formats. The 1990s and early 2000s saw the birth 13 of

new studios and the export of titles popular on the international stage. Australian studios released28% develop their own IP alongside producing games and services for clients. Australia-

wide, the sector also proved to be largely resilient to the effects of COVID-19. IGEA’s 2020

COVID survey identified that 84% of respondents were not planning to make any staff

cutbacks or redundancies in the immediate term and 44% of surveyed developers reported

stable or increased sales revenues.36

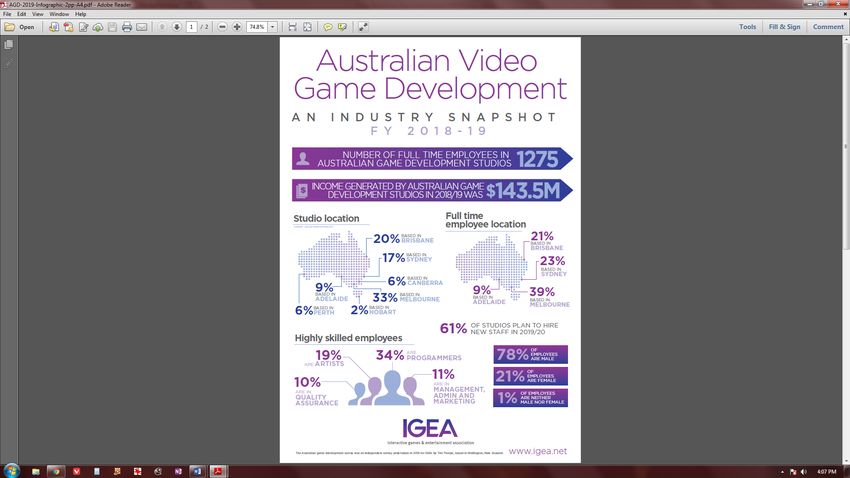

To put the Australian market into perspective, the $143.5 million represents a capture of

only 0.05% of the global market. Australia’s game development industry is world-class

yet underdeveloped. Thanks to expenditure-based tax incentives, other regions were

able to grow their industries into billion-dollar enterprises, Canada and the UK being

prominent examples. Australian Government support will be crucial to the development

of a robust and sizeable Australian industry that is a in a better position to capture global

opportunities, including the opportunities of the Indian market.

The state of Victoria demonstrates what targeted government investment – production

incentives and offsets as well as travel and production grant programs – can achieve. More

Australian game development studios continue to call Victoria home than any other state.37

The majority of the Australian games workforce is based in the state, and there is a steady

supply of graduates from highly-ranked universities and specialised institutions. Victoria

is home to some of Australia’s most significant and successful games titles and studios (see

Appendix B). Victoria is also home to Australia’s biggest e-sports event, the Melbourne

Esports Open, while Melbourne has been recognised as Australia’s top tech city on the

Savills Tech City Index.38

Melbourne's importance as an epicentre for game development and culture is also reflected

in it hosting Melbourne International Games Week (MIGW), Asia Pacific’s largest digital

games celebration which features Game Connect Asia Pacific (GCAP), Australia's premier

conference for game developers, and PAX, Australia's largest consumer expo. MIGW serves

as an event to bring industry stakeholders from various countries together.

36 IGEA (2020) Australian Video Games Industry Resilient Despite COVID-19 Impact. https://igea.net/2020/05/australian-

video-games-industry-resilient-despite-covid-19-impact/

37 Global Victoria. Digital Games. https://global.vic.gov.au/victorias-capabilities/industry-sectors/digital-technologies/digital-games

38 Savills (2019) Tech Cities in Motion. https://www.savills.co.uk/research_articles/229130/274942-0

14Opportunities The SWOT analysis at Appendix C provides the general context for the specific

opportunities listed below that were identified at the roundtable and through the

consultation process.

1. Game Development Collaborations

In line with local preferences, the Indian-made mobile games that dominate the charts

primarily revolve around casino-style or hyper casual gameplay. They do not rely on

elaborate narrative structures, complex economies associated with bigger budget titles,

intricate game design or the continuous enhancement via live operations. Accordingly, there

are gaps in the knowledge of the entire production pipeline of more substantial games and a

corresponding shortage of skills. India is not currently in a position to produce AAA console

or PC titles (games with multimillion-dollar budgets for both production and marketing).

While the industry is catching up rapidly, facilitated by the presence of overseas

studios such as Ubisoft and Zynga and the associated transfer of expertise, a push for

complementary skill sets via joint ventures with studios from mature industries holds

promise. Victorian game developers are particularly well aligned with this opportunity due

to their focus on international markets – 83% of the income of the Australian industry in

2018/19 was generated overseas.

This facilitation of complementary skill sets can go both ways and take the form of joint

ventures or acquisitions in each country. Traditionally, Australia has focused on product

development whereas India has had a service mindset. Indian game developers could

leverage Australian expertise to create more complex games for local and international

markets, while Victorian developers could leverage India's low-cost raw talent pool to scale

and address bottlenecks. Victoria could support India taking a short cut to more advanced

games, while India could support Australia's return to big-budget productions by means of

its workforce.

Lakshya Digital is an example of the latter strategy. Their extension into the US and other

overseas markets completed the production pipeline by adding a managerial/seniority level

which supplemented the art leadership in India (where even today there remains unmet

demand for these skills). This setup, in turn, allowed their clients to take on a greater

number and larger scale productions and facilitated Lakshya Digital's growth from six to

almost 600 staff.

Conversely, there is potential for Australian expertise to collaborate with the Indian

industry to create bigger games that convey Indian stories to local audiences and the

wider world, a strategy that enjoys the support of India's Prime Minister. In August 2020,

Narendra Modi called for India to tap the huge potential of the digital gaming industry and

“lead the international digital gaming sector by developing games that are inspired from

Indian culture and folk tales.”39

39 Press Information Bureau (Government of India) (2020) Press Release. PM convenes meeting to discuss ways to boost toy

manufacturing in India. https://pib.gov.in/PressReleasePage.aspx?PRID=1647971

15While Western games and gameplay mechanics are popular, this is mostly because of the

relative immaturity of the local games industry in a market that highly values local content

on other platforms and is already undergoing a rapid evolution in terms of gaming tastes

moving towards more complex titles. The rewards of this opportunity might not materialise

in the short term and there is the risk of not gaining traction in the marketplace, however,

this path promises exponential rewards in the long run.40

2. Education

The facilitation of expertise also underwrites the possibilities in the educational space.

The skills gaps in the Indian games industry could be addressed through collaborative

efforts between Indian and Victorian universities and specialised vocational education

institutions. Victoria produces over 1,000 graduates a year from 29 games-related courses

and 20 academic institutions and plays an important role in the education of the sector

workforce. The growth of the Indian gaming industry means that games are increasingly

seen as a viable career path, with the field attracting talent across the value chain from

artists, programmers, designers and app developers. Indian education is now catering to

these skills, and there are opportunities for Victorian education providers to supplement

the technical expertise developed under the Indian education system by providing a more

interdisciplinary and holistic outlook that, in addition to practical skills, develops expertise

in advanced game design, narrative psychology and cultural studies.

This could take the form of a finishing school where Indian students complete their studies

overseas to ‘fine-tune’ their craft and facilitate their entry into the (international) industry.

One example of this model is Arena Animation, one of the oldest animation and VFX

training centres in India, which entered into a collaboration with Vancouver's Langara

Centre for Entertainment Arts. Students study a year in India before completing the

remainder of the course in Canada.

This broader approach to education aligns with India's new National Education Policy

(NEP). Launched in July 2020, the NEP posits a liberal education that is multidisciplinary

and holistic, encompassing creativity, collaboration, social responsibility, multilingualism,

and digital learning.41 Video games represent this kind of interdisciplinarity, as the

intersection of all arts, animation, music, sound and even architecture, while being driven

by technology and promoted by advanced marketing and commercialisation techniques.

The opportunities identified in India's National Education Policy also extend to the use

of games in education. The NEP notes the emergence of digital technologies and the

increasing importance of leveraging technology for teaching and learning at all levels from

school to higher education. It plans the establishment of a digital repository of content

including learning games and simulations, augmented reality and virtual reality. It

envisages “fun based” learning using apps and the gamification of Indian art.42

40 This is similar to Naspers Limited, a South African-based consumer Internet company, which invested US$32 million into

Chinese gaming giant Tencent in 2001, a venture that had grown to US$129 billion in 2019. Phoebe Jin (2019) Naspers and

Tencent: the investment case Spaceship. https://www.spaceship.com.au/learn/naspers-tencent-investment-case/

41 Government of India (2020) National Education Policy 2020, p. 5; Craig Jeffrey (2020) A Very Short Policy Brief. India's

National Education Policy (Melbourne: Australia India Institute), p. 5.

42 NEP, p. 59.

16The NEP also envisages online education as a vehicle for increasing access to quality higher

education, which is another avenue of potential collaboration for Victorian education

providers with expertise in online and distance learning. Games have the advantage that

they can be made remotely, something highlighted by collaborative work practices brought

about by the COVID-19 pandemic. In IGEA's COVID survey, 71% of respondents reported

they had successfully transitioned to working from home with another 22% reporting they

were already operating remotely.43

Other forms of potential collaboration include joint coursework where Australian students

engage in prototyping activities with another overseas university, student exchange programs

and study tours, and shared curricula where an Australian university would primarily focus

on the theoretical and philosophical backdrop whereas the production work would be done

locally. Such an arrangement exists between RMIT Vietnam and RMIT Melbourne.

Australian educators could collaborate with their Indian counterparts in developing links

with the games industry, in particular studios operating across both countries, in such areas

as internships. These could be integrated into the curriculum, although this approach needs

to consider the possibility of a lack of direct placements due to the size of the local industry

and the subsequent need to provide alternative work integrated learning options (educational

activities that integrate academic learning of a discipline with its practical application in the

workplace). An example would be the replication of game production within the place of

learning under industry supervision. An alternative model would be fully funded internships

that would allow graduates to embed themselves into a company for three months or other

periods of time, leading to a job offer or take the gained knowledge back home.

Australia could partner with India in the development of research capacity and contribute

to the building of an Australia-India research nexus by means of faculty exchange,

developing post-doctoral networks, and enhancing opportunities for two-way student

mobility. Further opportunities in this context would revolve around complementary

skills and exposing Indian students to international design contexts. Students could also

be introduced to sectors tangentially related to ‘traditional’ games making, such as virtual

reality and games for purposes other than entertainment such as healthcare or education, a

sector that holds immense promise in the Indian market.44

Outside of the academic space, the exchange of knowledge and skills could also take place

within incubators such as IMAGE, India’s first Centre of Excellence (CoE) for gaming, VFX,

computer vision and AI in Hyderabad. Set up by Software Technology Parks of India and

backed by the Telangana government, and industry partners Telangana VFX, Animation

and Gaming Association, with the objective of incubating 25 to 30 start-ups annually for

the next five years, it offers mentoring, technology support, infrastructure, and funding. An

exchange program with Australian partners such as Melbourne’s The Arcade, Australia’s

first, not-for-profit, collaborative workspace created specifically for game developers and

creative companies, could lead to cross-pollination and hone the mutual understanding of

the opportunities each market and games ecosystem has to offer.

43 IGEA (2020) Australian Video Games Industry Resilient Despite COVID-19 Impact.

44 Sindhuja Balaji (2020) How Are India's Biggest EdTech Startups Winning Students? By Treating It Like A Game Forbes.

https://www.forbes.com/sites/sindhujabalaji/2018/03/11/how-are-indias-biggest-edtech-startups-winning-students-by-treating-

it-like-a-game/?sh=149e51c06908; Vibha Chetan, et al. (2018) Gamification: the Next Evolution of Education. Proceeding of the

International Conference on Future of Education 1 (2018), p. 38-49. https://doi.org/10.17501/26307413.2018.1106.

173. Victorian Game Developers Entering the Indian Market

Given the sheer size and growth of the India video games market, it seems obvious

that Victorian studios would attempt to make their games available to these hundreds

of millions of new consumers. Yet market entry into India can be challenging. While

Western games and their art and gameplay are popular, India is a highly complex market

that encompasses a spectrum of socio-economic groups, local cultures and ever-evolving

tastes. The monetisation band is very narrow and dominated by global games that are

able to engage the limited number of gamers with capacity to make in-game-purchases.

Ad-supported casual games rarely pay more than 1-2 cents per user and primarily work

through sheer volume, while real money games remain off limits due to the lack of

legislative clarity.

Victorian developers considering the Indian market need to be realistic about their

expectations. Part of this is the ongoing need to calibrate the product/market fit, and the

tight management of in-game economies to ensure consumers are engaged by positively

responding to their value proposition – and can pay for in-game-purchases via localised

payment systems. This does not just suggest a mere localisation of games by means of

offering it in Indian languages but experimentation with a deeper proactive ‘culturalisation,’

which involves a closer examination of the assumptions to assess the viability of creative

choices in both the global, multicultural marketplace as well as in specific locales.45 In

light of these challenges, Victorian developers seeking market entry should consider

collaborating with a local partner, and preferably one that is willing to shoulder some of the

financial risks associated with market entry (which, according to some Victorian studios

who eyed the Indian market, is not always the case).

One example of a successful Victorian market entry into India is Big Ant's series of cricket

games, with Cricket 19 being heralded as the game that could help to break the ‘beautiful

game’ into e-sports and rival such giants as the FIFA series.46 With this title, Big Ant was able

to take advantage of the unparalleled popularity of cricket in India to promote Cricket 19 as

“the closest to the real thing that a cricket game has ever been.”47 Despite its huge popular

appeal, Cricket 19 also faced challenges. The game is only available for consoles and PC

and, with the PC version selling for as little as US$1, its monetisation relies on volume – but

that volume is constrained by the fact that its operating platforms constitute the smallest

segments in the Indian games market. Improvements in infrastructure offer a potential

solution to this issue. With the proliferation of 5G, India could leapfrog into cloud gaming

whereby remote servers stream games directly to a user's device. This, in turn, would at once

remove the barriers traditional consoles currently face and enable the playing of state-of-the-

art AAA games on low-cost devices (including mobile phones and set-top boxes).

45 Jon Fung and Richard Honeywood (2012) Best Practices for Game Localization (Toronto: International Game Developers

Association), p. 1. http://englobe.com/wp-content/uploads/2012/05/Best-Practices-for-Game-Localization-v21.pdf

46 Raunak Saha (2020) Could India be the Catalyst for Cricket 19 Breaking into eSports? Technosports. https://technosports.

co.in/2020/09/29/could-india-be-the-catalyst-for-cricket-19-breaking-into-esports/

47 Tristan Ogilvie (2019) Cricket 19 Review IGN. https://www.ign.com/articles/2019/05/29/cricket-19-review

18Priority Actions To capture these opportunities requires regular and meaningful exchange between the

industry sectors in both countries. Victoria is already actively promoting such exchanges,

in the form of (virtual and physical) inbound and outbound trade missions, roundtables,

webinars and conferences that inform about the state of the respective markets, promote

the expertise of the Victorian sector and build networks and people-to-people links.

Programs can be further developed to expose Indian stakeholders to the Victorian gaming

landscape and to conduct matchmaking (similar to how MIGW has been used to for

Chinese stakeholders, such as Tencent). Within these initiatives, Global Victoria, Creative

Victoria, and IGEA can all play leading roles.

1. Supported by market intelligence and targeted introductions via Global Victoria,

Victorian and Indian gaming companies should consider joint ventures or other

collaborative efforts that:

• Allow Indian studios better insights into the production pipelines of more

advanced games with international appeal via complementary Victoria-based skills;

• Enable Victorian studios to achieve scale through enhanced production

processes supported by Indian talent; and

• Assist Victorian developers in entering the Indian market by adapting/designing

their games with the help of local partners willing to co-invest.

2. Victorian education providers, with the support of Creative Victoria and Global

Victoria, should be encouraged to explore joint activities with Indian counterparts

aimed at increasing skills and understanding of the respective markets, including:

• Collaborations between education providers to assist Indian students to acquire

skills currently not available in India through overseas finishing schools, joint

coursework, education/industry collaborations and (paid) internships; and

• The development of research capacity and going beyond ‘traditional’ game

making and extending into VR and ‘applied games,’ where games technology is

used for purposes other than entertainment.

The Victorian gaming sector should be aware of the global competition to engage with

India. While Victoria does have the advantage of a long history of gaming culture and local

game developers producing internationally successful IP, a supportive state government,

and other pull factors such as lifestyle and a low Australian dollar, it still faces the challenge

of having to compete with other regions that, due to generous government incentives, may

be in a better position to take advantage of the opportunities on account of their scale,

greater experience with AAA development and the benefits of easier access to capital.

The Indian market has been promising tremendous opportunities for years now, and while

these will materialise eventually, they are open to any mature games industry. Ultimately,

the realisation of opportunities relies on well-informed stakeholders, business partners

aligned in outlook and realistic expectations.

19Appendix A

Australian Video Game Development: An industry snapshot FY 2018-19

Appendix A Australian Video Game Development: An industry snapshot FY 2018-19

Source: IGEA (2019d). Australian Video Game Development: An industry snapshot FY 2018-19.

https://igea.net/wp-content/uploads/2019/11/AGD-2019-Infographic-2pp-A4.pdf

Source: IGEA (2019d). Australian Video Game Development: An industry snapshot FY 2018-19.

20

https://igea.net/wp-content/uploads/2019/11/AGD-2019-Infographic-2pp-A4.pdfAppendix B Some of Victoria’s most significant and successful games studios:

Big Ant A leader of Victoria’s games sector and one of the most

influential studios, Big Ant has created games with a distinctly

Australian character including Rugby League Live 4, Cricket 19

and Big Bash Boom.

House House Makers of the 2019 hit Untitled Goose Game, House House

is also a winner of the Golden Joystick Awards, the Annual

D.I.C.E. Awards, the Game Developers Choice Awards, and the

British Academy Games Awards.

Firemonkeys One of Australia’s largest game studio, Firemonkeys is owned

by the global video games giant Electronic Arts (EA) which

continues to develop and support a range of globally popular

titles, including games for The Sims and Need for Speed franchises.

Wicked Witch A studio with a long history of success over almost two

decades, from original games like Puzzle Wiz to distinctly

Australian rugby, AFL and cricket games.

Hipster Whale One of Australia’s most successful game studios of the past

decade, Hipster Whale’s game Crossy Road has been played by

over 200 million players.

League of Geeks Makers of Armello, a game that combines three styles of play:

the tactics of card games with the strategy of tabletop board

games, combined with a character RPG system. League of Geeks

recently entered a deal with publishing label Private Division.

Mountains Mountains are the makers of Florence, a game that won

international awards for Best Mobile Game, including at the

Game Awards, Game Developers Choice Awards and British

Academy Games Awards.

PlaySide One of Australia’s largest independent game studios, Playside

work on original intellectual property and games developed

in conjunction with studios such as Disney, Warner Bros and

Nickelodeon.

Sledgehammer Games Sledgehammer Games is the Australian satellite studio of the

acclaimed developer of the Call of Duty games, one of the most

successful video games franchises of all time.

Tantalus One of Victoria’s oldest game development studios, Tantalus has

a 25-year history of working with publishers around the world.

Voxel Agents Voxel Agent’s The Gardens Between won Game of The Year

at the Australian Game Developers Awards award, the Apple

Design Award and the Game Changers Award at Google Play’s

Best of 2020 Awards.

21Appendix C Indian Games Industry

SWOT Analysis

Strengths Weaknesses

• Strong, fast-learning workforce with • Comparatively underdeveloped gaming

solid technical skills culture

• Long history of successful servicing • Lack of knowledge of the entire

international game development studios production pipeline of bigger budget /

• Government-driven support initiatives sophisticated games and corresponding

such as incubators shortage of skills

• Market difficult to monetise due to

small monetisation band

Opportunities Threats

• Massive market that is yet to realise its • Losing the status of cost effective

full potential outsourcing destination as countries

• A market that highly values local such as Cambodia catch up

content and culture but is yet to fully • Uncertainties regarding the legal

experience it in game form regulations of games

• Growing e-sports scene

• Growing acceptance of games in

general (including games seen as viable

career paths)

Victorian Games Industry

Strengths Weaknesses

• “Punching above its weight” • Lack of federal government incentives

• Comparatively mature gaming culture puts Australia at a disadvantage compared

and steadily growing industry to other (more) mature industries

• Strong international focus due to small • Australia’s conservative investment

local market and successful history landscape does not lend itself towards

creating globally appealing IP the kind of risk taking that is needed for

• Strong state support of game developers international joint ventures

and gaming culture (including MIGW) • Growth in industry is occurring from

• Talented English-speaking workforce, a comparatively small base and AAA

steady supply of (junior) talent, lifestyle production is only just returning (GFC

(Melbourne being one of the world’s severely diminished Australia’s AAA

most liveable cities), low Australian production as talent and expertise

dollar, advantageous time zone moved overseas)

Opportunities Threats

• Federal government incentives can help to • Without federal government intervention

fully unlock Australia’s / Victoria’s potential the Victorian games industry will

and push the industry towards AU$1 continue to lag behind competing

billion (with all the associated benefits countries, unable to take advantage of

such as a highly skilled innovation-focused international markets as well as more

workforce of 10,000 FTEs) sizeable industries in other regions

22You can also read