"Avoid" to Craftsman Automation - 'High debt level; poor return ratios'

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

“Avoid” to Craftsman Automation ‘High debt level; poor return ratios’

12th Mar. 2021

Salient features of the IPO: Recommendation Avoid

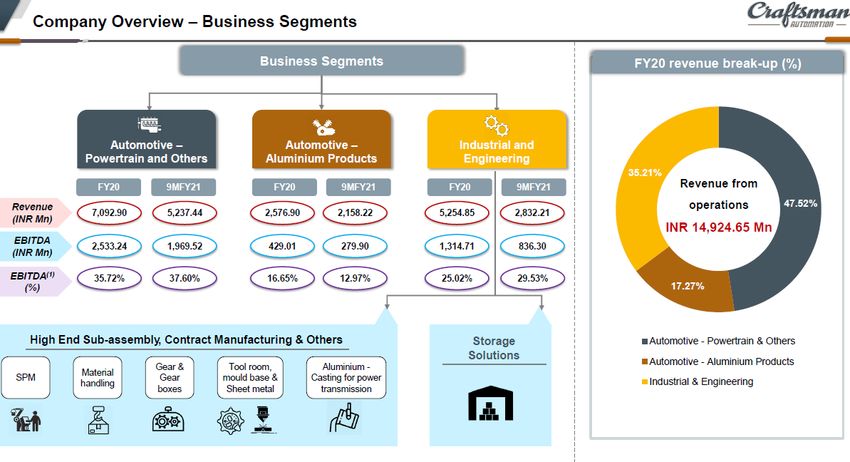

• Craftsman Automation Limited (CAL) is a diversified engineering Price Band Rs1,488 - Rs1,490 per share

company engaged in three business segments include Automotive- Face Value Rs5 per share

powertrain & other products, Automotive-aluminium products and

Fresh Issue Size Rs1,500 mn

industrial & engineering products segment.

Share for Fresh Issue 1.01mn shares

• The company own and operates 12 strategically located

manufacturing facilities across seven cities of India. OFS Issue Size Rs6,737 mn

Total Issue Size Rs8,237 mn

Valuation: At higher price band of Rs1,490, the issue is valued at P/E of

46.6x (on FY21 post issue annualized EPS). Bidding Date Mar 15' 2021 - Mar 17' 2021

MCAP at Higher Price

Below are few key observations of the issue: (continued in next page) Rs31,481.2 mn

Band

• CAL, established in 1986 in Chennai, is a diversified auto ancillary & Book Running Lead Axis Capital Limited

engineering company deals in three key segments include Manager IIFL Securities Limited

automotive-powertrain & other products, automotive-aluminium

products and industrial & engineering products. Registrar Link Intime India Private Limited

• The company manufactures automotive & industrial products from its Industry Auto ancillary

12 strategically located manufacturing facilities across seven cities of

India.

• Business is diversified across end-user industries as CAL caters to the Retail application money at higher cut-off price per lot

needs of heavy commercial vehicles to two wheelers. The company

manufactures cylinders blocks, cylinders heads and transmission parts Number of shares per lot 10

which are required for tractors and trucks as well as crank cases

which are required for two wheelers. Application Money Rs14,900 per lot

• Automotive-powertrain & other products is the major business

segment accounted for 51.2% of CAL’s business as of 9MFY21. The Allocation Detail

segment includes highly engineered products such as cylinder block

and cylinder head, camshafts, transmission parts and bearing caps Qualified Institutional

50%

among others. End users of these products are OEMs producing Buyers (QIB)

commercial vehicles, special utility vehicle, tractors and off-highway

vehicles. Commercial vehicles, SUVs accounts for 30% and 42% of the Non-Institutional

15%

segment’s business, while tractors & construction equipment Investors (NII)

comprises 21% & 7%. End user customers list also include some

marquee OEMs such as Daimler India, Tata Motors, M&M, Escorts, Retail Individual

35%

Ashok Leyland among others. Investors (RIIs)

• The company is present across the entire value chain in the

Shareholding Pattern

automotive aluminium product segment which accounted for 21.1%

of CAL’s revenue as of 9MFY21. Key products under this segment Pre-Issue Post Issue

include crank cases & cylinder blocks for two wheelers, engine & Promoter & promoter

63.4% 59.8%

structural parts for passenger vehicles and gear box housing for heavy group

commercial vehicles. As the company has an entire range of Public 36.6% 40.2%

aluminium casting and product capabilities, increased usages of non- Total 100.0% 100.0%

ferrous metal like aluminium to reduce the weight of vehicles under

BS VI norms has become key growth driver for this segment. Key Source: Choice Broking Research, RHP

customers of company under this segment are Royal Enfield, M&M,

TVS Motors and Daimler India. Analyst

• Industrial & engineering segment accounted for 27.7% of revenue Satish Kumar

during 9MFY21. In this segment, company manufactures high end

(022-67079999; Ext:913,

precision products include aluminium products for power Deskphone

Mob:9167120440

transmission and storage solutions business products such as pallets,

racking, shelving among others. Email satish.kumar@choiceindia.com

1

Continued……

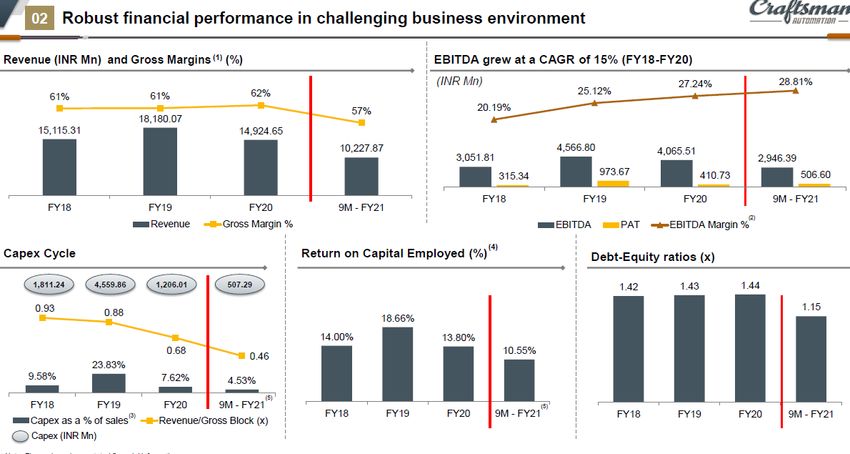

• CAL diversified business across segments as share of automotive - powertrain & other products reduced to 47.5%

in FY20 from 58% in FY18. Top 10 customers accounted for 53.4% of total revenue in FY20 and 59% in 9MFY21.

• CAL operated at 70% capacity utilisation (CU) level in FY20 for powertrain & aluminium segments while CU stood

at 40% for industrial & engineering segment.

• CAL incurred significant capex particularly in FY19 to enhance the installed capacity. Though FY20 remained

challenging due to auto industry slowdown amid events like transition to BS VI norms which impacted business

adversely. Higher capex in FY19 leading to rise in debt level while slowdown in FY20 weighed on business with

increase in interest cost impacting PAT margin. D/E raised to 1.44x in FY20. Profit margin impacted as interest

cost remained high at a rate of ~15% during FY18-FY20 due to lower long term debt rating at BBB+ stable.

• Company will utilize Rs1,200 mn from fresh proceed for the repayment of debt which will modestly help to

improve profit margin (reported debt at Rs8,901 mn and D/E at 1.15x in 9MFY21). Post issue, D/E will reduce to

0.85x which still looks at higher level.

• CAL managed to keep EBIDTA level above 25% in FY20 and 9MFY21, significantly higher than peers. Though,

despite high EBIDTA margin, profitability of the business remained under pressure due to lower profit margin

(NPM) impacting by higher interest cost. Considering the BBB+ rating for long term debt, interest cost is likely

to remain high until the company gets any rating upgrade which is not likely any time soon. We also see

modest positive impact to the tune of Rs120 mn from repayment of debt from fresh issue. Moreover, RoE

remained low at 7.3% (post issue, annualized) and further improvement largely depend upon strong business

growth and NPM movement.

• If we annualize 9MFY21 performance, EPS derives at Rs32. At the higher price of Rs1,490, the issue is valued at

P/E of 46.6x. Peers valuation include Endurance Technologies at P/E of 45x, Mahindra CIE at P/E of 63.4x and

Sundram Fasteners at P/E of 55.8x.

• While CAL maintains strong operating efficiency and has also operating leverage advantage, we are concerned

over high debt level and poor RoE, the improvement on both fronts requires strong business growth and

favourable movement on NPM front. Further, the IPO issue consists a higher amount of OFS of Rs6,737 mn

which also disappoints as contrary to this or higher fresh issue size can be utilized by firm to reduce debt level

significantly.

Considering all these parameters, we assign ‘Avoid’ rating to issue

Peer comparison

CMP 6M 12M M Cap EBIDTA Mar. NPM RoE RoA

Companies

(Rs/s) (R%) (R%) (Rs mn) (%) (%) (%) (%)

Craftsman Automation 1,490 - - 31,481.2 28.1% 5.0% 7.3% 2.8%

Bharat Forge 613 33.0% 48.0% 2,85,045.0 9.3% -6.8% -7.8% -33.7%

Endurance Technologies 1,400 29.6% 44.0% 1,97,400.0 15.7% 7.3% 14.4% 7.9%

Jamna Auto Industries 70 50.0% 130.0% 28,000.0 10.6% 4.3% 7.6% 4.6%

Mahindra CIE 179 43.9% 46.0% 67,841.0 8.3% 1.8% 2.4% 11.2%

Minda Industries 547 61.9% 63.0% 1,47,690.0 10.6% 1.6% 4.0% 1.6%

Sundram Fasteners 726 72.0% 89.0% 1,52,460.0 17.1% 8.5% 13.3% 7.6%

Ramkrishna Forgings 544 144.0% 108.0% 1,740.8 15.1% -2.1% -2.6% -0.9%

P/E P/BV P/S EV/EBIDTA D/E Net

Companies (Rs mn) EV BVPS

(x) (x) (x) (x) (x) Worth

Craftsman Automation 46.6 3.4 2.3 13.3 0.9 40,071.8 9,216.1 436.2

Bharat Forge -70.0 5.5 4.8 59.4 0.9 3,30,740.0 51,960.0 111.7

Endurance Technologies 45.0 6.5 3.3 20.8 0.2 1,96,490.0 30,540 216.6

Jamna Auto Industries 77.8 5.9 3.4 32.0 0.1 28,190.0 4,720 11.8

Mahindra CIE 63.4 1.5 1.1 16.4 0.4 81,941.0 45,290 119.5

Minda Industries 189.3 7.5 2.9 29.3 0.5 1,55,470.0 19,710 73.0

Sundram Fasteners 55.8 7.4 4.8 29.0 0.3 1,58,710.0 20,560 97.9

Ramkrishna Forgings -82.9 2.2 1.7 18.2 1.3 27,698.0 8,030 250.9

*- Craftsman Automation – FY21 annualized EPS : Return ratio annualized basis, margin 9MFY21, Post issue net worth

Source: Choice Broking Research, RHP

© CHOICE INSTITUTIONAL RESEARCH

About the issue:

• Craftsman Automation Limited (CAL) is coming with initial public offering of Rs8,237 mn.

• The issue comprises fresh issue of Rs1,500 mn and offer for sale (OFS) of 4.521 mn shares.

• At the higher price band of Rs1,490, fresh number of shares are stood at 1.007 mn. While OFS size comes at Rs6,737

mn at the higher price band.

• Promoter namely Srinivasan Ravi is selling 0.13 mn shares. Post issue, promoters’ stake will reduce to 59.8% from

63.4% pre issue.

• Other selling shareholders include 1.6 mn shares from Marina III, 1.4 mn shares by IFC and 1.4 mn shares by individual

investor K Gomatheswaran.

• Post issue Marina III stake will reduce to 7.38% from 15.5% and IFC to 6.7% from pre issue stake of 14.1%. While,

individual investors K Gomatheswaran will sell all his stake in the company.

• Issue will open for subscription on Mar 15’ 2021 and close on Mar 17’ 2021

• Not more than 50% of the net offer shall be available for allocation on a proportional basis to a qualified institutional

investors (QIIs).

• Further not less than 15% shall be available for allocation on a proportional to non-institutional investors (NIIs) and

not less than 35% of net offer shall be available for allocation to Retail Institutional Investors (RIIs).

• Average cost of acquisition for selling shareholders is Rs470 for Marina, Rs208 for IFC and Rs1.27 for K.

Gomatheswaran. Average cost of acquisition for selling promoter S. Ravi is Rs1.06.

Objective of Offer

Fresh Issue Rs1,500 mn

Repayment/ pre-payment, in full or part, of certain borrowings

Rs1,200 mn

availed by company

General corporate purposes Rs300 mn

Indicative IPO process time line:

Unblocking of

Offer Closes on

ASBA Account

17-Mar-2021

23-Mar-2021

Offer Opens on Finalization of Commencement

15-Mar-2021 Basis of Credit to Demat of Trading

Allotment Accounts 25-Mar-2021

22-Mar-2021 24-Mar-2021Company introduction:

Craftsman Automation Limited (CAL) is a diversified engineering company with vertically integrated manufacturing

capabilities, engaged in three business segments namely powertrain and other products for automotive segment,

automotive aluminium products and industrial & engineering products segment. The company own and operates 12

strategically located manufacturing facilities across seven cities of India.

CAL is the largest player involved in machining of cylinders blocks and cylinders heads in the intermediate, medium and

heavy commercial vehicles segment as well as in the construction equipment industry in India. CAL is among the top three-

four component players with respect to machining of cylinder block for tractor segment in India. The company is present

across the entire value chain in the automotive aluminium product segment providing diverse products and solutions.

CAL is a significant player in the automotive-powertrain segment with highly engineered products which include engine

parts such as cylinder blocks, cylinder heads, camshafts, transmission parts, gear box housing, turbo chargers, bearing caps

and machining services. End users of these products include OEMs producing commercial vehicles, special utility vehicle,

tractors and off-highway vehicles. Key products under automotive- aluminium product segment include crank case and

cylinder blocks for two wheelers, engine and structural parts for passenger vehicles and gear box housing for heavy

commercial vehicles. Within industrial and engineering segment, CAL developed a diverse product portfolio across two

segments namely 1) storage solution for conventional/automated storage and 2) high end precision products such as

aluminium products for power transmission, material handling equipment such as hoists, crane kits among others.

Source: Choice Broking Research, RHPBusiness Overview:

As per RHP, CAL is considered as a strategic and preferred suppliers by OEM customers and also the single source suppliers

in certain product categories for some key customers. Large portion of the business comprises direct supply to OEM

customers under long term agreements which renewed time to time. Revenue mix include automotive – powertrain &

others accounted for 51.2%, automotive- aluminium products at 21.1% and industrial & engineering segment at 27.7% of

total revenue by 9MFY21. Exports from powertrain segment accounted for 1.6% and exports from industrial & engineering

segment accounted for 9.98% of revenue in 9MFY21. CAL business was impacted in FY20 due to auto industry slowdown

with sales declined to Rs14,924.7 mn in FY20 from Rs18,180 mn in FY19. In 9MFY21, the company posted sales of Rs10,228

mn while EBIDTA margin stood at 28.1% and PAT margin at 5.0%.

Source: Choice Broking Research, RHPCompetitive strengths:

• Diversified business with a focus on providing comprehensive solutions and

manufacturing high quality, intricate and critical products, components and

parts

• Strong in-house process and product design capabilities with ability to

interchange capacity and product mix

• Long term and well-established relationships with marquee domestic and

global OEMs.

• Extensive manufacturing footprint with strategically located manufacturing

facility

• Experienced management team supported by motivated and skilled work

force

Business strategy:

• Leverage vertically integrated manufacturing and engineering capabilities

to tap growing opportunities

• Increase wallet share and acquire new business by leveraging existing

OEM relationship and adding new customers

• Growing opportunities in storage solutions

• Continue to reduce operating costs and improve operational efficiencies

Risk and concerns:

• Risk to business growth if auto industry demand revival slows

• Prevailing economic slowdown

• High commodity prices can impact margin

• High interest cost impacting NPM

© CHOICE INSTITUTIONAL RESEARCHFinancial statements:

Rs mn

Profit & Loss A/c Cash Flow Statement

Particulars FY18 FY19 FY20 9MFY21 Particulars FY18 FY19 FY20 9MFY21

Operating Revenue (OR) 15,115.3 18,180.1 14,924.7 10,227.9

Cash Flow from Operating

Cost of Material Consumed (5,916.9) (7,104.9) (5,717.0) (4,387.3) 2,827.0 3,600.0 3,053.7 2,420.6

Activities

Changes in Inventories of

Cash Flow from Investing

(2,107.4) (3,584.1) (1,370.7) (454.7)

Finished Goods, Work-in- 159.2 70.2 (150.7) 48.1 Activities

Progress

Purchase of fixed assets

(2,038.6) (3,558.1) (1,386.9) (495.0)

Employee Benefit Expenses (1,986.3) (2,168.3) (1,709.9) (1,105.9) and properties

Other Expenses (4,110.8) (4,550.6) (3,367.3) (1,908.4)

Cash Flow from Financing

EBITDA 3,260.5 4,426.4 3,979.8 2,874.4 (603.1) (182.3) (1,279.3) (2,254.0)

Activities

Depreciation and

(1,491.5) (1,761.5) (1,949.9) (1,414.7) Net Cash Flow 116.5 (166.4) 403.7 (288.1)

Amortization Expenses

EBIT 1,768.9 2,664.9 2,029.9 1,459.6 Opening Balance of Cash

244.0 359.4 193.9 598.6

Finance Costs (1,449.3) (1,405.5) (1,484.0) (772.4) and Bank Balances

Other Income 113.3 136.4 85.9 71.2

Closing Balance of Cash

Share of profit from JV 2.5 4.0 (0.2) 0.8 360.4 193.1 597.6 310.5

and Bank Balances

Exceptional Items 0.0 0.0 (57.7) 0.0 Financial Ratios

PBT 435.4 1,399.8 573.9 759.3 Particulars FY18 FY19 FY20 9MFY21

Growth & Margin rations

Tax Expenses (120.1) (426.2) (163.2) (252.7)

Revenue Growth Rate (%) 20.3% -17.9%

PAT 315.3 973.7 410.7 506.6 EBITDA Growth Rate (%) 35.8% -10.1%

EBITDA Margin (%) 21.6% 24.3% 26.7% 28.1%

EBIT Growth Rate (%) 50.7% -23.8%

Balance Sheet EBIT Margin (%) 11.7% 14.7% 13.6% 14.3%

Particulars FY18 FY19 FY20 9MFY21 Adjusted PAT Growth Rate (%) 208.8% -57.8%

Reported PAT Margin (%) 2.1% 5.4% 2.8% 5.0%

Share Capital 100.6 100.6 100.6 100.6 Turnover ratios

Reserves and Surplus 5,866.0 6,732.0 7,088.4 7,615.5 Inventories Turnover Ratio (x) 5.0 5.6 4.6 3.0

Trade Receivable Turnover

Net Worth 5,966.6 6,832.6 7,189.0 7,716.1 7.5 8.7 7.7 4.8

Ratio (x)

Long Term Borrowings 5,746.0 8,502.5 7,963.8 7,334.2 Accounts Payable Turnover

4.2 5.5 5.3 3.4

Ratio (x)

Long Term Provisions 6.8 2.1 Fixed Asset Turnover Ratio (x) 1.2 1.2 1.0 0.7

Short Term Borrowings 2,720.9 1,350.1 2,442.7 1,566.9 Total Asset Turnover Ratio (x) 0.8 0.8 0.6 0.5

Working Capital Turnover

Trades Payables 3,627.3 3,312.1 2,817.8 3,016.2 Ratio (x)

-8.8 -13.7 -22.4

Other Liabilities 1,573.0 2,799.8 2,222.1 2,264.4 Operational ratios

Current Ratio (x) 0.8 0.8 0.8 1.0

Short Term Provisions 40.9 51.5 18.3 28.7

Debt to Equity (x) 1.4 1.4 1.4 1.2

Deferred tax liabilities (Net) 319.7 405.4 370.9 534.3 Total Debt (Rs.) 8,466.8 9,852.6 10,406.5 1,148.25

Net Debt (Rs.) 7,980.1 9,586.8 9,690.1 8,379.4

Other liabilities 0.0 0.0 0.0 0.0

Net Debt to EBITDA (x) 2.4 2.2 2.4 2.9

Total Liabilities 19,994.3 23,254.0 23,031.4 22,462.9 Net Debt to Equity (x) 1.3 1.4 1.3 1.1

Return ratios

RoE (%) 5.3% 14.3% 5.7% 7.3%

Tangible Assets 12,447.4 14,764.5 14,267.0 14,130.7 RoA (%) 1.6% 4.2% 1.8% 2.8%

Intangible Assets 149.6 143.4 106.3 78.7 RoCE (%) 15.1% 17.4% 13.4% 9.7%

RoIC (%) 11.8% 12.9% 10.4% 6.8%

Capital Work In Progress 243.1 906.1 888.2 274.3 EV 39,580.8 41,138.8 41,290.1 40,071.8

Non-current tax assets (net) 44.4 0.0 11.0 0.0 EV/Sales (x) 2.6 2.3 2.8 3.9

EV/EBIDTA (x) 12.1 9.3 10.4 13.9

Other Non Current Assets 1,113.3 1,329.1 1,479.3 1,198.2 Per share ratios

Inventories 3,004.6 3,233.1 3,256.2 3,399.2 EPS 14.9 46.1 19.4 24.0

BVPS 282.4 323.4 340.3 365.2

Trade Receivables 2,016.9 2,100.3 1,943.2 2,142.0 OCF/sh 133.8 170.4 144.5 114.6

Cash and Bank Balances 367.2 195.0 597.6 310.5 FCF/sh 0.0 312.8 217.6 82.7

Valuation ratios

Other bank balances 119.6 70.8 118.8 211.2 P/E (x) 99.8 32.3 76.6 46.6

Other Current Assets 463.4 488.0 349.9 715.1 P/BVPS (x) 5.3 4.6 4.4 3.4

P/S (x) 2.1 1.7 2.1 2.3

Total Assets 19,994.3 23,254.0 23,031.4 22,462.9

EV/EBITDA (x) 12.1 9.3 10.4 13.3

Source: Choice Broking Research, RHP

© CHOICE INSTITUTIONAL RESEARCHEquity Research Team

Name Designation Email id

Sundar Sanmukhanis Head of Research - Fundamental sanmukhanis@choiceindia.com

Satish Kumar Research Analyst satish.kumar@choiceindia.com

Rajnath Yadav Research Analyst rajnath.yadav@choiceindia.com

Ankit Pareek Research Associate ankit.pareek@choiceindia.com

Yug Tibrewal Research Intern yug.tibrewal@choiceindia.com

Disclaimer

es

This is solely for information of clients of Choice Broking and does not construe to be an investment advice. It is also not intended as an offer or solicitation

for the purchase and sale of any financial instruments. Any action taken by you on the basis of the information contained herein is your responsibility alone

and Choice Broking its subsidiaries or its employees or associates will not be liable in any manner for the consequences of such action taken by you. We have

exercised due diligence in checking the correctness and authenticity of the information contained in this recommendation, but Choice Broking or any of its

subsidiaries or associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in

the information contained in this recommendation or any action taken on basis of this information. This report is based on the fundamental analysis with a

view to forecast future price. The Research analysts for this report certifies that all of the views expressed in this report accurately reflect his or her personal

views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly

related to specific recommendations or views expressed in this report. Choice Broking has based this document on information obtained from sources it

believes to be reliable but which it has not independently verified; Choice Broking makes no guarantee, representation or warranty and accepts no

responsibility or liability as to its accuracy or completeness. The opinions contained within the report are based upon publicly available information at the

time of publication and are subject to change without notice. The information and any disclosures provided herein are in summary form and have been

prepared for informational purposes. The recommendations and suggested price levels are intended purely for stock market investment purposes. The

recommendations are valid for the day of the report and will remain valid till the target period. The information and any disclosures provided herein may be

considered confidential. Any use, distribution, modification, copying, forwarding or disclosure by any person is strictly prohibited. The information and any

disclosures provided herein do not constitute a solicitation or offer to purchase or sell any security or other financial product or instrument. The current

performance may be unaudited. Past performance does not guarantee future returns. There can be no assurance that investments will achieve any targeted

rates of return, and there is no guarantee against the loss of your entire investment.

POTENTIAL CONFLICT OF INTEREST DISCLOSURE (as on date of report) Disclosure of interest statement – • Analyst interest of the stock /Instrument(s): - No. •

Firm interest of the stock / Instrument (s): - No.

CONNECT US Choice Equity Broking Pvt. Ltd.

Choice House, Shree Shakambhari Corporate Park, Plt No: -156-158,

Any kind of queries on RESEARCH, J.B. Nagar, Andheri (East), Mumbai - 400 099.

You can contact us on: 022 - 6707 9999 +91-022-6707 9999

+91-022-6707 9959

www.choiceindia.com

© CHOICE INSTITUTIONAL RESEARCH

9You can also read