"Avoid" to Suryoday Small Finance Bank - 'Stress appears higher; aggressively priced'

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

“Avoid” to Suryoday Small Finance Bank ‘Stress appears higher; aggressively priced’

16th Mar. 2021

Salient features of the IPO:

Recommendation Avoid

• Suryoday Small Finance Bank Limited (SSFB) started operations as

Price Band Rs303 - Rs305 per share

SFB on Jan 23’ 2017.

Face Value Rs10 per share

• Prior to commencement of operations as a SFB, SSFB operated as an

NBFC – MFI carrying out microfinance operations. Fresh Issue Size Rs2,485.8 mn

Share for Fresh Issue 8.15mn shares

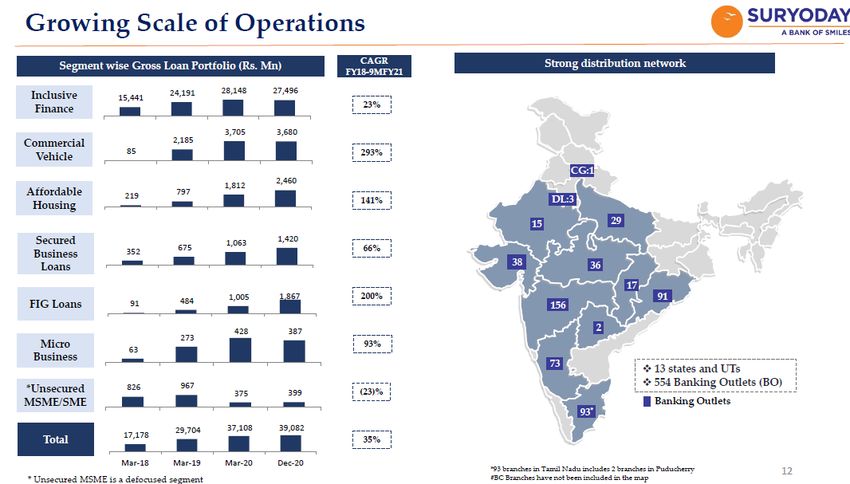

• SSFB has a network of 554 banking outlets across 13 states and UT in

country providing services to 1.44 mn customers OFS Issue Size Rs3,337.6 mn

Valuation: At higher price band of Rs305, the issue is valued at P/BV of Total Issue Size Rs5,823.4 mn

2.0x (on post issue BVPS). Bidding Date Mar 17' 2021 - Mar 19' 2021

MCAP at Higher Price

Below are few key observations of the issue: (continued in next page) Band

Rs32,369.9 mn

• SSFB commenced operations as an SFB on Jan 23’ 2017 pursuant to Axis Capital Limited, ICICI

receipt of RBI’s final approval. Prior to commencement of operations Book Running Lead Securities Limited, IIFL Securities

as a SFB, the company was operated as an NBFC – MFI carrying out Manager Limited, SBI Capital Markets

micro-finance operations. Limited

Registrar Kfin Technologies Private Limited

• Public issue is brought mainly to comply the RBI’s regulation to list

SFB within three years of from reaching the net worth of Rs5,000 mn. Industry Banking

SSFB is required to be listed by Nov 29’ 2020 but due to bank request,

the RBI gave six months extension to May 2020 for listing.

Retail application money at higher cut-off price per lot

• Micro loan categories as inclusive finance constituted 70.4% of gross

loan portfolio in 9MFY21. SSFB disburses micro loans under the joint Number of shares per lot 49

lending group model (JLG) to customers in unbanked and Application Money Rs14,945 per lot

underbanked predominately in urban and semi-urban locations.

Ticket size of unsecured micro loan under JLG ranges between

Rs10,000 and Rs52,500 predominately extended to woman Allocation Detail

customers. Average tenure of loan is up to two years and bank

earned interest between 20.5% - 25.5% per annum on these loans. Qualified Institutional

50%

Buyers (QIB)

• The bank is gradually diversifying the loan portfolio across other

secured categories. Over the past years, SSFB started disbursing Non-Institutional

15%

affordable housing loans, secured business loans to Investors (NII)

SME/MSME/Corporates, CV loans and unsecured business loans to

micro/small enterprises and self-employed individuals. Retail Individual Investors

35%

(RIIs)

• CV loans comprised 9.4%, affordable housing loan at 6.3% and

secured business loans at 3.6% of the gross loan portfolio as on

9MFY21. Shareholding Pattern

Pre-Issue Post Issue

• Coming to distribution front, SSFB has a network of 554 banking

outlets across 13 states and UT in country providing services to 1.44 Promoter & promoter group 30.3% 28.0%

mn customers. Business is largely skewed towards four states namely Public 69.7% 72.0%

Maharashtra, Karnataka, Tamil Nadu and Odisha due to high Total 100.0% 100.0%

presence of banking outlets in the respective states.

• Owing to micro loans to unbanked region and weaker section, SSFB's Source: Choice Broking Research, RHP

average "priority sector" loans, as a percentage of average net

banking credit (ANBC) was 114.1% as on Dec 31’ 2021. Analyst

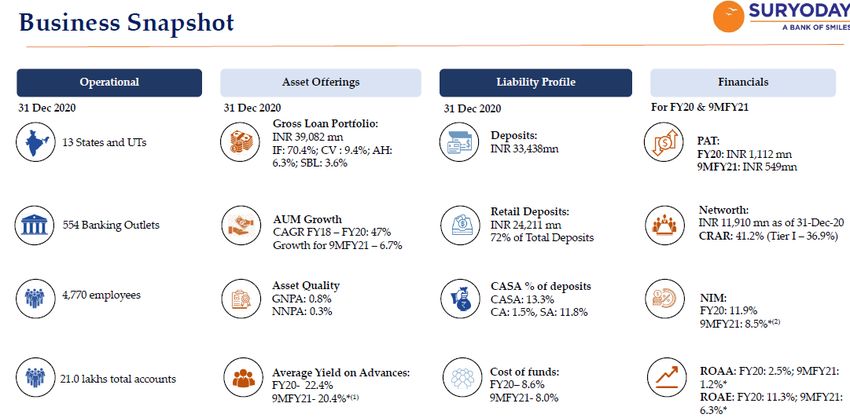

• Gross advances portfolio stood at Rs39,082 mn in 9MFY21 which Satish Kumar

grew at a CAGR of 35% since FY18. The bank is aggressively making (022-67079999; Ext:913,

disbursement in CVs and affordable housing segment, the share of Deskphone

Mob:9167120440

whose rose to 9.4% in 9MFY21 (0.5% in FY18) and 6.3% (1.3% in

FY18). Email satish.kumar@choiceindia.com

1

Continued……

• Average yield on CVs ranges between 10.5% - 19% and affordable housing at 9.7%-16%, which is significantly

lower than micro loan.

• Average NIM stood at ~11% mainly due to higher share of unsecured micro loan. As the bank strategized to

increase share of secured book, NIM is likely to decline in coming fiscals.

• Deposits improved significantly to Rs33,438 mn in 9MFY21 from Rs7,495.2 mn, though credit-to-deposits ratio

stood at 113%. CASA share at 13.3% remained low compared to peers. To fund business growth, SSFB is focusing

on retail customers and include senior citizens, upper middle-class individuals, self-employed and salaried

individuals and HNIs in states Maharashtra, Tamil Nadu and Karnataka where the bank has distribution presence.

• SSFB performance remained strong during FY19-FY20 with average NIM of ~12%, RoE of 12% and robust

profitability. However, during 9MFY21, bank performance has deteriorated as pandemic led lockdown and

economic crises impacted weaker section of society severely. What makes us more concerned is proforma

GNPA at 9.3%, SSFB’s pool of bad loans is the highest among listed peers. While the collection efficiency

improved to above 100% (inclusive finance at 112.5% in Dec), re-surge of Covid cases in key business states

such as Maharashtra and Karnataka to weigh on revival and further weaken assets quality.

• At higher price band of Rs305, demanding valuation of Rs32,370 mn is valued at P/BV of 2x post issue BVPS

which appears expensive given weak assets quality outlook, concentrated business to some states, low CASA

share and small business size. Asked valuation is in line with peers include Equitas/Ujjivan SFB but these banks

are significantly large in business size and has superior fundamentals than SFFB. Post issue, RoE is unlikely to

improve to double digit or FY20 level (RoE:11.4% in FY20) anytime soon. Further, SFFB is well capitalized with

CAR at 41.2% despite this, the company comes with fresh issue of Rs2,486 mn.

Considering all these parameters, we assign ‘Avoid’ rating to issue

Companies CMP 6M 12M P/BV NIM GNPA NNPA Proforma Proforma

M Cap

(Rs mn) (Rs/s) R% R% (x) (%) (%) (%) GNPA (%) NNPA (%)

Suryoday Small Finane Bank 305 - - 32,369.9 2.0 8.5% 0.8% 0.3% 9.3%

Equitas Small Finance Bank 59 - - 67,142.0 2.0 8.5% 2.3% 0.7% 2.2% 0.7%

Ujjivan Small Finance Bank 34 1% -17.0% 66,130.4 2.1 9.7% 1.0% 0.1% 4.8% 2.1%

AU Small Finance Bank 1,255 76.0% 30.0% 3,85,285.0 7.1 5.4% 1.0% 0.2% 3.1% 1.3%

City Union Bank 170 19.4% -4.4% 1,25,528.2 2.2 4.2% 2.9% 1.5% 3.4%

CreditAccess Grameen 713 -2.2% -13.0% 1,10,515.0 3.0 8.7% 0.9% - 6.1%

Companies CAR RoE RoA C/I C/D CASA PAT Net Gross

Deposits

(Rs mn) (%) (%) (%) (%) (%) (%) TTM Worth Advances

Suryoday Small Finane Bank * 41.2% 4.6% 1.1% 55.4% 113.1% 13.3% 732 15,951 39,082 33,438

Equitas Small Finance Bank 21.6% 11.2% 1.4% 60% 110% 25% 3,660 32,800 1,73,730 1,58,620

Ujjivan Small Finance Bank 27% -1.8% -0.3% 58% 117% 18% -550 30,790 1,36,380 1,16,170

AU Small Finance Bank 19% 20.8% 2.4% 49% 112% 22% 11,240 54,030 3,32,220 2,97,080

City Union Bank 17% 6.8% 0.7% 41% 83% 27% 3,860 56,674 3,65,037 4,32,883

CreditAccess Grameen 31% 2.8% 0.8% 44% - - 1,030 37,020 1,23,210

* - Annualized PAT, RoE, ROA are post issue (annualized, PAT), post issue net worth includes impact of pre-ipo

placements

Source: Choice Broking Research, RHP

© CHOICE INSTITUTIONAL RESEARCH

About the issue:

• Suryoday Small Finance Bank Limited (SSFB) is coming with initial public offer (IPO) of Rs5,823.4 mn.

• The issue comprises fresh issue of 8.15 mn shares and offer for sale (OFS) of 10.9 mn shares.

• Price band for issue is fixed at Rs303-Rs305.

• At the higher price band of Rs305, fresh issue size is stood at Rs2,485.8 mn while OFS size derives at Rs3,337.6 mn.

• Issue will open for subscription on Mar 17’ 2021 and close on Mar 19’ 2021

• Not more than 50% of the net offer shall be available for allocation on a proportional basis to a qualified institutional

investors (QIIs).

• Further not less than 15% shall be available for allocation on a proportional to non-institutional investors (NIIs) and

not less than 35% of net offer shall be available for allocation to Retail Institutional Investors (RIIs).

• OFS includes stake sell by private equity players. OFS comprises 4.4 mn shares by IFC, 2.0 mn shares by GAJA Capital

fund 2.02 mn, 1.9 mn shares by DWM Mauritius, 0.75 mn shares by HDFC Holdings, 1.5 mn shares by IDFC First Bank,

0.1 mn by Americorp Ventures, 0.2 mn by Kotak Life Insurance and 0.1 mn by Gaja Capital India AIF.

• Due to post issue equity dilution, promoters’ stake will reduce to 28% from 30.3%.

• Average cost of purchase for major selling shareholder namely IFC is Rs58.8.

• SSFB did pre-IPO placement of 5.2 mn shares at Rs291.75 per share. SBI Life Insurance, Axis Capital, Kiran Vyapar

participated in the pre-IPO placement. Thereby, the size of fresh issue has been reduced by 5.2 mn shares pursuant to

pre-IPO placement.

• Meanwhile SSFL’s board on Mar 2’ 2021 increased the fresh issue size by 1.76 mn equity shares.

• 0.5 mn shares are reserved for employees. Furthermore, employee will get 10% discount for bidding in the

employee reservation portion.

Fresh issue proceed will be utilized to augment bank’s Tier-I capital base to meet bank’s future capital requirements

Indicative IPO process time line:

Unblocking of

Offer Closes on

ASBA Account

19-Mar-2021

24-Mar-2021

Offer Opens on Finalization of Commencement

17-Mar-2021 Basis of Credit to Demat of Trading

Allotment Accounts 30-Mar-2021

24-Mar-2021 25-Mar-2021Company introduction:

Suryoday Small Finance Bank (SSFB) incorporated as Suryoday Micro Finance Private Limited at Chennai, Tamil Nadu on Nov

10, 2008. The bank has been serving the customers over a decade in the unbanked and under banked segments in India and

promoting financial inclusion. Pursuant to receipt of RBI’s final approval, SSFB has started operations as a SFB on Jan 23’

2017. Prior to commencement of operations as an SFB, SSFB operated as an NBFC – MFI carrying out microfinance

operations and operated the joint liability group-lending model for providing collateral-free, small ticket-size loans to

economically active women belonging to weaker sections. SSFB commenced microfinance operations in 2009 and have

expanded operations across 13 states and union territories as of Dec 31’ 2020. With 554 banking outlets including 153

unbanked rural centres, the bank provides services to 1.44 mn customers. SSFB has greater presence in unban and semi-

urban locations and as of Dec 31’ 2020, 37.1%, 27. 8% and 28.8% of gross advances were from metropolitan, urban and

semi-urban areas respectively.

Source: Choice Broking Research, RHPBusiness Overview:

SSFB provides a number of credit products such as commercial vehicle loans, affordable housing loans, micro business loans,

unsecured micro and small enterprise and small and medium enterprise loans, secured business loans, financial intermediary

group loans and other loans. Gross loan portfolio grew at a CAGR of 39% to Rs39,082.3 mn in Dec 31’ 2020 from Rs17,177.8

mn in FY18. Loan portfolio is dominated by inclusive finance which accounted for 70.4% of gross loan portfolio followed by

CV book (9.4% of loans), affordable housing (6.3% of loans) and balance is covered by secured business loans, FIG loans,

micro business and unsecured MSME/SME.

On liability front, deposits grew at CAGR of 72% to Rs33,438.4 mn from Rs7,495.2 mn in FY18. Retail deposits constituted

72.4% of total deposits and CASA share stood at 13.3% as of Dec 31’ 2020. SSFB reported PAT of Rs1,112 mn in FY20 as

compared to Rs904 mn inFY19 and Rs114.9 mn in FY18. Owing to high yielding micro book, NIM margin stood at 11.9% in

FY20 and 8.5% in 9MFY21. Credit to deposits ratio sustained over 100% indicating the bank is fulfilling some portion of credit

growth with borrowings. Cost-to-income ratio improved to 47.1% in FY20 as compared to 64.4% in FY18. In 9MFY21, C/I

stood at 55.4%. The bank is well capitalized with CAR stood at 41.2% as of 9MFY21.

As per the RHP, the bank’s focus will be to grow customer base by providing quality customer service. SSFB will continue to

focus on the use of technology, explore partnerships with fintech companies, undertake data analytics to better understand

the requirements of customers, improve operational efficiency and further reduce costs. As SFFB grows operations, it

strategized to look to selectively expand network of banking outlets across newer geographies and also penetrate further

into existing markets. Further it also intends to engage with BC partners and payment banks to leverage their network to

help expand and increase market share.

Key Financials (Rs mn)

Particulars FY18 FY19 FY20 9MFY21

Net Interest Income 1,658.3 3,403.7 4,909.1 3,532.8

Net Interest Margin 10.4% 12.8% 11.9% 8.5%

Total Income 2,038.7 4,073.0 5,783.6 4,182.0

Growth (%) 99.8% 42.0%

Pre-Prov. Operating Profit 725.0 2,165.5 3,062.4 1,865.7

Adjusted PAT 114.9 904.0 1,112.0 548.7

Growth (%) 686.6% 23.0%

Advances 15,686.8 26,795.8 35,319.4 37,822.6

Deposits 7,495.2 15,934.3 28,487.2 33,438.4

RoA 0.5% 3.1% 2.4% 1.1%

RoE 2.1% 12.7% 11.4% 4.6%

GNPA 3.5% 1.8% 2.8% 0.8%

CAR (Basel III) 43.4% 40.2% 35.4% 41.2%

BVPS 50.7 83.0 100.5 150.3

P/BV (x) 6.0 3.7 3.0 2.0

Source: Choice Broking Research, RHPCompetitive strengths:

• Customer centric approach with a focus on financial inclusion

• Diversified assets portfolio with a focus on retail operations

• Fast evolving granular deposits franchise

• Leveraging emerging technologies to enhance digital footprint

• Strong credit processes and robust risk management framework

• Track record of strong financial performance and cost-efficient operations

• Multiple distribution channels

Business strategy:

• Expand assets portfolio while focusing on secured lending

• Strengthen retail liability franchise

• Expand geographic presence and penetrate further into existing

geographies

Risk and concerns:

• Significant rise in proforma slippages due to Covid led economic

slowdown

• Business skewed to some states like Maharashtra, Karnataka and

Tamil Nadu

• Weak assets quality outlook

• Increased competition in banking industry

© CHOICE INSTITUTIONAL RESEARCHFinancial statements:

Rs mn

Profit And Loss Statement Financial Ratios

Particulars FY18 FY19 FY20 9MFY21 Particulars FY18 FY19 FY20 9MFY21

Interest Earned 2,868.8 5,301.1 7,666.9 6,243.5

Return / Profitability Ratios (%)

Growth (%) 84.8% 44.6%

Net interest margin (NIM) 10.4% 12.8% 11.9% 8.5%

Interest Expended 1,210.5 1,897.3 2,757.8 2,710.7

Growth (%) 56.7% 45.4% Yield on advances 16.4% 23.2% 22.4% 20.4%

Yield on investments 7.2% 6.9% 7.2% 6.9%

Net Interest Income 1,658.3 3,403.7 4,909.1 3,532.8

EPS (Diluted) (Rs) 1.08 8.52 10.48 5.17

Net Interest Margin 10.4% 12.8% 11.9% 8.5% RoA 0.5% 3.1% 2.4% 1.1%

Other Income 380.4 669.2 874.5 649.2 RoE 2.1% 12.7% 11.4% 4.6%

% of Interest Income 13.3% 12.6% 11.4% 10.4%

Cost of Deposits 3.3% 7.1% 8.2% 7.6%

Total Income 2,038.7 4,073.0 5,783.6 4,182.0

Growth (%) 99.8% 42.0%

Operating ratios (%)

Operating & Other expenses 1,313.8 1,907.4 2,721.2 2,316.4 Credit to Deposit (C/D) 209.3% 168.2% 124.0% 113.1%

Pre-Prov. Operating Profit 725.0 2,165.5 3,062.4 1,865.7 Cost-to-income (C/I) 64.4% 46.8% 47.1% 55.4%

Provisions and contigencies 546.6 738.3 1,518.6 1,165.1 CASA (share) 11.0% 11.2% 11.4% 13.3%

P&C % of Advances 3.5% 2.8% 4.3% 3.1% Investment / Deposit (I/D) 41.5% 41.7% 28.4% 45.2%

Operating Profit before Tax 178.4 1,427.2 1,543.8 700.6 Non interest income / Total

Growth (%) 700.2% 8.2% 18.7% 16.4% 15.1% 15.5%

income

Pre-tax Margin % 8.7% 35.0% 26.7% 16.8%

Capitalization Ratios (%)

Tax 63.4 523.3 431.8 151.9

% of PBT 35.6% 36.7% 27.0% 27.0% CET 40.2% 38.7% 34.3% 36.9%

Reported PAT 114.9 904.0 1,112.0 548.7 Tier-1 40.2% 38.7% 34.3% 36.9%

Net Profit Margin % 5.6% 22.2% 19.2% 13.1% Tier-2 3.2% 1.6% 1.1% 4.2%

Extrodinary Income CAR (Basel III) 43.4% 40.2% 35.4% 41.2%

Adjusted PAT 114.9 904.0 1,112.0 548.7 Equity / Assets 25.0% 23.4% 19.9% 18.8%

Growth (%) 686.6% 23.0%

Loans / Assets 72.8% 71.2% 65.8% 59.6%

Balance Sheet

Investments / Assets 14.4% 17.7% 15.1% 23.8%

Particulars FY18 FY19 FY20 9MFY21 Asset Quality ratios (%)

Cash and balance with Reserve GNPA 3.5% 1.8% 2.8% 0.8%

308.2 483.0 605.3 889.0

Bank of India…….. NNPA 1.9% 0.4% 0.6% 0.3%

Balances with banks and money Coverage Ratio 47.5% 75.7% 79.6% 57.7%

1,763.4 2,280.6 7,770.7 7,442.6

at call and short notice Per Share Data (Rs)

Investments 3,113.4 6,643.9 8,082.0 15,114.4

EPS (Diluted) 1.1 8.5 10.5 6.9

Advances 15,686.8 26,795.8 35,319.4 37,822.6

Fixed assets 135.4 189.8 387.3 433.6 BVPS 50.7 83.0 100.5 150.3

Other assets 552.4 1,218.9 1,480.5 1,801.9 Valuation ratios (x)

TOTAL ASSETS 21,559.6 37,612.0 53,645.2 63,504.1 P/E (x) 281.7 35.8 29.1 44.2

P/BV (x) 6.0 3.7 3.0 2.0

Capital 675.0 815.8 865.9 891.9 Growth ratios (%)

Reserves and Surplus 4,709.9 7,987.8 9,796.4 11,017.8 Advances 70.8% 31.8%

Deposits 7,495.2 15,934.3 28,487.2 33,438.4

Deposits 112.6% 78.8%

Borrowings 7,178.3 11,242.3 12,646.2 14,870.8

Other liabilities and provisions 1,501.3 1,631.9 1,849.6 3,285.3 Net interest income 105.3% 44.2%

TOTAL CAPITAL AND Interest Earned 84.8% 44.6%

21,559.6 37,612.0 53,645.2 63,504.1

LIABILITIES…...…… PAT 686.6% 23.0%

Source: Choice Broking Research, RHP

© CHOICE INSTITUTIONAL RESEARCHEquity Research Team

Name Designation Email id

Sundar Sanmukhanis Head of Research - Fundamental sanmukhanis@choiceindia.com

Satish Kumar Research Analyst satish.kumar@choiceindia.com

Rajnath Yadav Research Analyst rajnath.yadav@choiceindia.com

Ankit Pareek Research Associate ankit.pareek@choiceindia.com

Yug Tibrewal Research Intern yug.tibrewal@choiceindia.com

Disclaimer

es

This is solely for information of clients of Choice Broking and does not construe to be an investment advice. It is also not intended as an offer or solicitation

for the purchase and sale of any financial instruments. Any action taken by you on the basis of the information contained herein is your responsibility alone

and Choice Broking its subsidiaries or its employees or associates will not be liable in any manner for the consequences of such action taken by you. We have

exercised due diligence in checking the correctness and authenticity of the information contained in this recommendation, but Choice Broking or any of its

subsidiaries or associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in

the information contained in this recommendation or any action taken on basis of this information. This report is based on the fundamental analysis with a

view to forecast future price. The Research analysts for this report certifies that all of the views expressed in this report accurately reflect his or her personal

views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly

related to specific recommendations or views expressed in this report. Choice Broking has based this document on information obtained from sources it

believes to be reliable but which it has not independently verified; Choice Broking makes no guarantee, representation or warranty and accepts no

responsibility or liability as to its accuracy or completeness. The opinions contained within the report are based upon publicly available information at the

time of publication and are subject to change without notice. The information and any disclosures provided herein are in summary form and have been

prepared for informational purposes. The recommendations and suggested price levels are intended purely for stock market investment purposes. The

recommendations are valid for the day of the report and will remain valid till the target period. The information and any disclosures provided herein may be

considered confidential. Any use, distribution, modification, copying, forwarding or disclosure by any person is strictly prohibited. The information and any

disclosures provided herein do not constitute a solicitation or offer to purchase or sell any security or other financial product or instrument. The current

performance may be unaudited. Past performance does not guarantee future returns. There can be no assurance that investments will achieve any targeted

rates of return, and there is no guarantee against the loss of your entire investment.

POTENTIAL CONFLICT OF INTEREST DISCLOSURE (as on date of report) Disclosure of interest statement – • Analyst interest of the stock /Instrument(s): - No. •

Firm interest of the stock / Instrument (s): - No.

CONNECT US Choice Equity Broking Pvt. Ltd.

Choice House, Shree Shakambhari Corporate Park, Plt No: -156-158,

Any kind of queries on RESEARCH, J.B. Nagar, Andheri (East), Mumbai - 400 099.

You can contact us on: 022 - 6707 9999 +91-022-6707 9999

+91-022-6707 9959

www.choiceindia.com

© CHOICE INSTITUTIONAL RESEARCH

9You can also read