Beyond COVID-19: Strategic focus for the board - The Deloitte Academy

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Beyond COVID-19: Strategic focus for the board The Deloitte Academy| 27 May 2020

Agenda

Introductions – William Touche, Deloitte

Key economic indicators and issues to be factored into long term strategy - Ian Stewart, Deloitte

UK Chief Economist.

Strategy Considerations – Alex Curry, Head of Monitor Deloitte

Reflections of a CEO;

- Peter Duffy, Just Eat

- Pano Christou, Pret a Manger

Panel Discussion

The Deloitte Academy www.deloitteacademy.co.uk 2

Ian Stewart

Deloitte

3

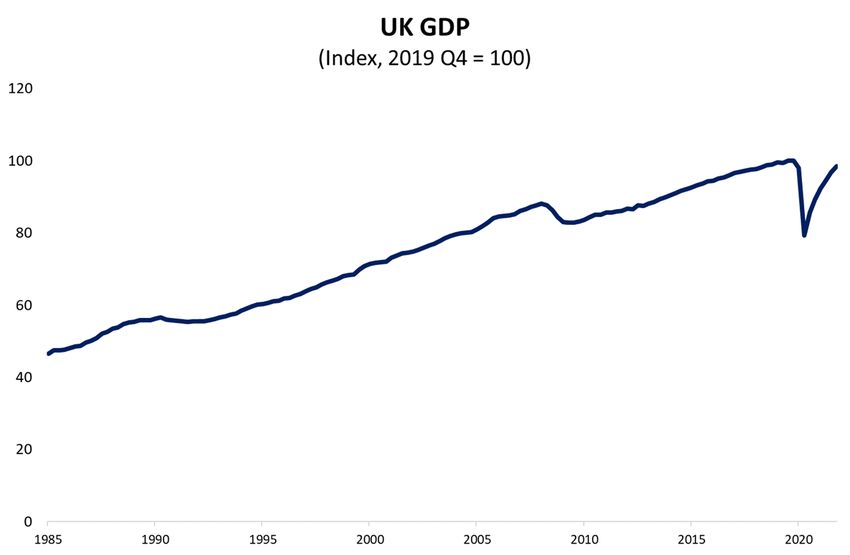

Regaining activity lost in recessions takes years, not months

2020 COVID-19: -21%

2.5 years to regain peak

2008-09 Global Financial Crisis: -6.1%

5 years to regain peak

1990-92 recession: -1.9%

Almost 3 years to regain peak

The Deloitte Academy www.deloitteacademy.co.uk 4

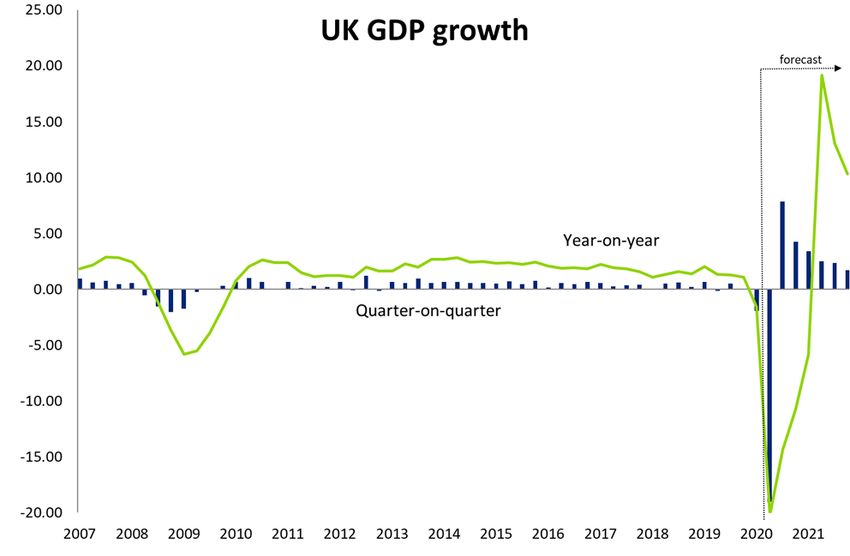

UK GDP forecast: massive volatility ahead

UK GDP forecasts

2020 2021

Deloitte: 18th May -11.7 +8.5

Consensus, 11th May -7.9 +6.1

The Deloitte Academy www.deloitteacademy.co.uk 5The Deloitte Academy www.deloitteacademy.co.uk 6

COVID-19 hit to growth & bounce vary by sector The Deloitte Academy www.deloitteacademy.co.uk 7

Theme 1: Quantitative Easing + debt boom = inflation?

The case for inflation The case for deflation

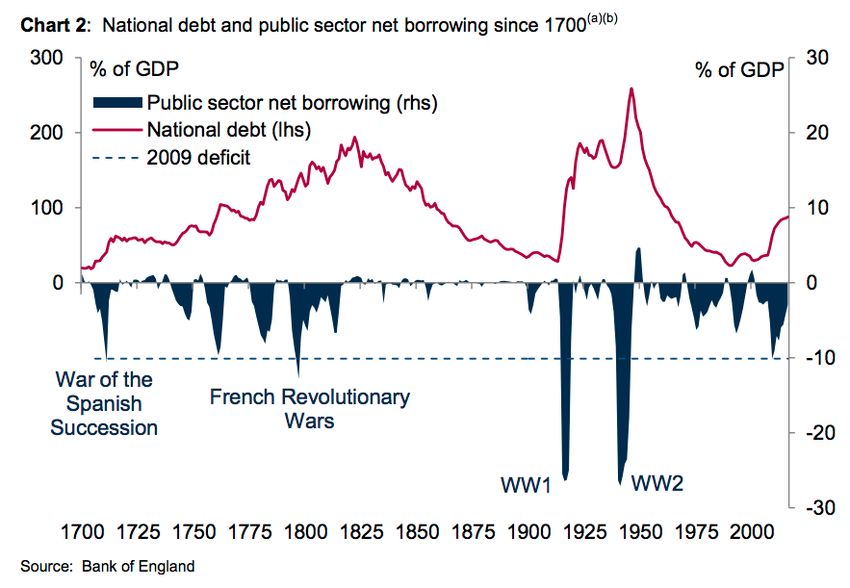

The Deloitte Academy www.deloitteacademy.co.uk 8Theme 2: Soaring Government debt = unsustainable government debt? The Deloitte Academy www.deloitteacademy.co.uk 9

Theme 3: Globalisation in peril? The Deloitte Academy www.deloitteacademy.co.uk 10

Alex Curry

Deloitte

11Looking beyond Covid-19; the Board inbox …

1 Think hard about how your operating environment is changing

2 Identify the areas of impact for your business

3 Challenge the strategy and support that challenge

12The changing operating environment

Government, regulation, and taxation

Financing environment and M&A

Social attitudes, consumer habits, and lifestyle

Technology and data

Climate and sustainability

13Potential areas of impact

The crisis has demonstrated the adaptability of certain enterprises: particularly cloud & platform based, data-rich, multi-

channel ones. Enterprises will need to hasten decision making processes and increase their flexibility and adaptability so

Enterprise

1 as to manage a changing environment and exploit opportunities for growth, as well as increase ROIC and productivity.

Agility Regardless of what immediate decisions enterprises make to navigate the crisis, they will need to ensure that investments

in the future allow them to be as nimble as possible.

This is about strategy.; we believe that many management teams will take this opportunity to question fundamental

aspects of their business which have to date been “too hard” to consider - as a way to boost productivity and profitability

2 Reinvention in the future. In the short-medium term this may result in substantive reworking of operations and overheads so that

enterprises deliberately reshape as they come out of the crisis. As enterprises look towards the future however they will

want to consider how to re-direct investment towards agile business models.

The crisis has highlighted the lack of operational resilience (supply chain, production, technology, go to market) for many

enterprises. We expect Boards to place a renewed emphasis on resilience and be prepared to accept higher costs or

Operational

3 inefficiency to secure it. This could take the form of a combination of ‘shorter’ (less complex, more localised) and ‘wider’

Resilience (more diverse to mitigate reliance on sole suppliers) supply chains, higher levels of stock, and greater use of data and

analytics to understand the full breadth of interactions along their supply chains.

Managing through crisis, either with government assistance or without, is rapidly increasing debt levels. Going forward we

believe that many organisations will struggle with high debt, constraining growth and productivity initiatives. There will

Financial be a surge in refinancing activity, capital raising, equity, restructuring and M&A activity to address these debt levels. We

4

Resilience believe medium sized enterprises will be disproportionately affected by the crisis as they have limited access to capital,

are administratively harder for Government’ to support, lack scale and resilience and are many in number. Yet they’re

politically important as employers, sources of entrepreneurialism and mainstays of many economies.

14Potential areas of impact

Government deficits will increase dramatically (as in the GFC) as will their role in many aspects of national

Relationship life. Governments will face real challenge to reform and increase productivity whilst managing public expectations around

5 with sanctity of key parts of government (Health) and avoiding a return of, or perception of Austerity. This is likely to lead to a

Government higher tax environment. We also expect governments to take a more active role in industrial and M&A policy, and to take

on new responsibilities as business owners, operators and influencers as a result of stimulus measures.

Managing the crisis requires a much greater use of data on population, movements etc. (e.g. contact tracing apps). Whilst

easier in certain countries e.g. China) this will present significant privacy and data management issues in Western Europe.

6 Data & Privacy That said public perceptions – and enablement - of government use of individual and collective data may be changing

which presents huge opportunities in healthcare provision. Additional consideration is evolving relationship between

governments and big tech firms (Google, Facebook etc.).

The way people work has changed considerably, both physically and in the systems they use. This has implications for

Future of property and office space, remote training, talent and resource management and leadership in a remote environment.

7 There may be implications for global workforces and mobility. There is an additional issue around worker protection,

Workforce

future of 0 hours / gig economy and worker protection, which we expect to ascend the political agenda.

During this crisis the trials and tribulations of the EU and US / China have hit the headlines and exposed institutional fault-

lines. This crisis has challenged cooperation within blocs, but also between blocs. Much has been written about the roll-

Global

8 back of globalisation. We don’t anticipate a wholesale retreat from globalisation, but risks will increase. We believe that

Cooperation the crisis will lead to a fresh look at national strategic industries, the impact of foreign ownership of enterprises and the

need for a strong and resilient local footprint and tax contribution.

15The impact on strategy

How is our environment changing?

What are our goals

and aspirations?

Where will we

play?

What is the 5-year How will we

growth ambition? win?

– What metrics Which consumer How will we

will define our segments should configure?

What is our What management

success? we prioritize for

differentiated value systems do we

growth? How do we allocate

What market proposition for the need?

position do we Which needs prioritised segments? financial and non-

aspire to have? should we address? financial resources

What is our product /

What geographies to drive returns? What critical

offer?

should we focus What are the capability gaps exist,

What pricing? and how will we fill

on? capabilities required

What is the cost to capture these them?

structure that will allow growth areas? How do we

us to support sequence our

What networks /

investment in these growth initiatives,

partners should we

growth areas? and where do we

leverage?

In which channels start?

How can digital

should we distribute How do we manage

technologies enable

our products? our initiatives?

our strategy?

16The impact on strategy

1. Define the key 3. Take a view on

2. Take a view on 4. Identify where 5. Decide on actions

assumptions longer term scenarios

nearer term scenarios assumptions have and commit sprint

underpinning your for the post-

and business impact changed the most teams to their pursuit

strategy pandemic world

Make sure short term actions don’t

impact longer term flexibility and

optionality

17An example of scenarios

• Consumer attitudes to how they wish to live • The crisis leads businesses, workers and consumers

and how they wish to work are significantly to realise that legacy ways of working and ways of

changed – attitudes to travel, commuting, doing jobs (broadly defined) are incompatible with

health, leisure and consumption culture are all the needs of 2020s society

impacted leading to a new zeitgeist • This leads to widespread change in the way

New normal

• Traditional businesses, however, do not draw business is done, with a high degree of dialogue

emerges

the same conclusions and retain their pre- 2 4 between businesses of all scales with their

crisis models “New wave “Economy and consumers and with each other

• This dissonance leads to explosive growth in accelerates” society remade” • Sustainability, inclusion and cultural digitisation

alternative business models and an become central features of business models at a

accelerated decline of incumbents in many rapid rate as the economic recovery progresses

sectors

Lifestyle

• As the crisis abates, people and • Businesses discover that outcome-based, data-

Reset to pre-Covid

organisations very rapidly return to pre- centric, machine-assisted and location independent

3

crisis life and work patterns 1 working is more productive as well as more flexible

norms

• Existing ways of working appear to have “Old product, new • This realisation drives accelerated transformation of

“Business as usual”

delivered sufficient business and economic machine” operating models and increased cloud-based

resilience to avoid lasting long-term effects technology investment as the economy recovers

• New (often digital) business models and • Consumer demand, however, has rebounded,

channels played only a minor role in meaning that large-scale reinvention of the value

sustaining people and businesses and thus proposition is not required

continue to play an ‘edge’ role Reset to pre-Covid New normal • Lack of comfort with new ways of working

norms emerges disadvantages a generation of knowledge workers

Productivity who are unable to adapt to the change, increasing

the discomfort of the middle aged, middle class

18These slides have been prepared in general terms and therefore cannot be relied on to cover specific situations. Application of the principles set out will depend upon the particular circumstances

involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise attendees

on how to apply the principles set out in this presentation and the handouts to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person

acting or refraining from action as a result of any material in this presentation and the handouts.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 1 New Street Square, London EC4A 3HQ, United

Kingdom.

Deloitte LLP is the United Kingdom affiliate of Deloitte NSE LLP, a member firm of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee ("DTTL"). DTTL and each of its

member firms are legally separate and independent entities. DTTL and Deloitte NSE LLP do not provide services to clients. Please click here learn more about our global network of member firms.

© 2020 Deloitte LLP. All rights reserved.You can also read