Creative Resources Leadership - Corporate Presentation October 2017 - Mines and Money Americas

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Corporate Presentation

October 2017

Creative Resources Leadership

Important Notice

This presentation has been prepared by the management of Lepidico Ltd (the 'Company') for the benefit of brokers, analysts and investors and not

as specific advice to any particular party or person.

The information is based on publicly available information, internally developed data and other external sources. No independent verification of

those sources has been undertaken and where any opinion is expressed in this document it is based on the assumptions and limitations

mentioned herein and is an expression of present opinion only. No warranties or representations can be made as to the origin, validity, accuracy,

completeness, currency or reliability of the information. The Company disclaims and excludes all liability (to the extent permitted by law), for

losses, claims, damages, demands, costs and expenses of whatever nature arising in any way out of or in connection with the information, its

accuracy, completeness or by reason of reliance by any person on any of it.

Where the Company expresses or implies an expectation or belief as to the success of future exploration and the economic viability of future

projects, such expectation or belief is based on management’s current predictions, assumptions and projections. However, such forecasts are

subject to risks, uncertainties and other factors which could cause actual results to differ materially from future results expressed, projected or

implied by such forecasts. Such risks include, but are not limited to, exploration success, commodity price volatility, future changes to mineral

resource estimates, changes to assumptions for capital and operating costs as well as political and operational risks and governmental regulation

outcomes. For more detail of risks and other factors, refer to the Company's other Australian Securities Exchange announcements and filings. The

Company does not have any obligation to advise any person if it becomes aware of any inaccuracy in, or omission from, any forecast or to update

such forecast.

Competent Person Statement

The information in this report that relates to Exploration Results is based on information compiled by Mr Tom Dukovcic, who is an employee of the

Company and a member of the Australian Institute of Geoscientists and who has sufficient experience relevant to the styles of mineralisation and

the types of deposit under consideration, and to the activity that has been undertaken, to qualify as a Competent Person as defined in the 2012

edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves.” Mr Dukovcic consents to the

inclusion in this report of information compiled by him in the form and context in which it appears.

2

Overview

Lepidico (ASX: LPD) is an ASX-listed lithium exploration and development

company with a management team experienced in project and business

development - market capitalisation A$25M*

Lepidico’s strategic objective is to become a fully integrated lithium

business from mine to battery grade lithium chemical

Lepidico is differentiated by its L-Max® process technology that extracts

lithium salts from less contested lithium-mica minerals

L-Max® is a clean-tech process with competitive capital intensity and low

operating costs after eco-friendly by-product credits

Phase 1 Plant Project located in Eastern Canada; currently in Full Feasibility

Study – first production target late 2019

Quality lithium-mica mine feed will be sourced from Canada, Portugal and

Australia

At 30 June 2017 Lepidico had A$3.3M in cash and no debt

3

*Reference share price 1.2c

Asset Overview

Separation Rapids lithium

deposit 9.6Mt @ 1.31% Li2O

Lepidolite offtake LOI with

owner Avalon Advanced

Materials

Phase 1

L-Max® Plant

Eastern Canada,

In Feasibility Study Moriarty JV

LPD 75% Farm-in

Lepidolite Target

Exploration

Alvarrões Lepidolite Mine Pioneer Dome JV

Resource pending LPD 75% Earn-in on Peg9,

Ore offtake agreement with Lepidolite rich pegmatite

Grupo Mota Permitting to drill 4

Mineral Resource Development

Alvarrões Lepidolite Mine*

Ore access agreement with Grupo Mota over the operating Alvarrões lepidolite

mine, Portugal

Multiple stacked lepidolite mineralised pegmatite sills 1m to 4m thick exposed

over a strike of more than 1km in two open pits

25-hole drill program commenced May 2017; inaugural Mineral Resource estimate

due October 2017; mineralized system open down dip and along strike

Drilling has extended mineralisation 300m down dip. Target Resource estimates:

Block 1: 0.5 Mt – 1.4 Mt @ 1.0% - 1.5% Li2O in lithium mica

Block 3: 1.0 Mt – 2.6 Mt @ 1.0% - 1.5% Li2O in lithium mica

Current mining operation produces a lepidolite concentrate grading ~1.8% Li2O for

use in the ceramics industry

Mining rates may be increased materially to 50,000 tonne to 75,000 tonne per

annum sufficient to feed the planned Phase 1 L-Max® Plant in Sudbury, Canada

*Reference: ASX Announcement, Alvarrões Lepidolite Mine Ore Access Agreement, 9 March 2017

5

Mineral Resource Development

Separation Rapids*

Separation Rapids is one of the largest “complex-type” lithium pegmatite

deposits in the world, owned 100% by Avalon Advanced Materials Inc.

NI43-101 PEA completed on the Petalite Mineral Resource (opposite)

Excellent recoveries and high-specification, 99.88% battery grade lithium

carbonate produced in L-Max® testwork programme

L-Max® to maximize lithium mineral Resource potential (plus by-products)

Outcropping Lepidolite zone largely un-tested – Resource drilling

completed May 2017 for revised estimate second-half 2017 Tonnes Li2O# Ta2O5 Cs2O Rb2O

Class

(Mt) (%) (ppm) (%) (%)

Latest work indicates >20% of the lithium content of the existing Mineral Measured 4.03 1.32 60 0.017 0.343

Resource is present in lithium micas Indicated 3.97 1.26 70 0.025 0.362

Letter of Intent between Lepidico and Avalon Advanced Materials Inc. (TSX: Measured plus

8.00 1.29 60 0.021 0.352

Indicated

AVL and OTCQX: AVLNF) for an integrated Lepidolite mining and lithium

carbonate production partnership in Canada Inferred 1.63 1.42 80 0.016 0.360

*Reference: ASX Announcement, Lithium Alliance with Avalon Advanced Materials Inc, 6 February 2017 TOTAL 9.63 1.31 63 0.020 0.353

# Note: Li2O is total lithium oxide without distinction between contributions by petalite, Li-mica or lepidolite

6

Mineral Resource Context

3.00%

Lepidolite

Target

Li2O equivalent

after by-

2.50% Greenbushes

products

120

5-15M t @

2.40%

2.0-2.6%

2.00% Lepidolite

Rio - Jadar

Target Nemaska Lithium 136

5-15M t Birimian 37 1.86%

33 1.48% Critical

@

Grade (%Li2O)

1.37% Elements Kidman Resources

1.0-1.5% 37 128

1.50% 1.25% 1.44%

Tawana NeoMetals

13 78

RB

1.18% 1.37% Mineral Resources

Sayona Energy

198

14 33 Prospect

1.18%

1.07% 1.19% 57

1.00% 1.13% Pilbara

Dakota - Sepeda Minerals

Altura

10 Galaxy - Mt 156

Mining

1.00% Caitlin 1.25%

40

16 1.00%

1.08% Galaxy - James Bay

0.50% 23

Cinovec

1.20% 657

Milbra 0.43%

19

0.35%

0.00%

0 50 100 150 200 250

Resources Tonnes (MT)

Source: Company data, Lepidico targets

7

Positive Phase 1 L-Max® Plant PFS*

PFS highlights economic potential to construct a strategically located Product Recoveries

L-Max® Feed Recovery to

Phase 1 L-Max® process facility in Eastern Canada due to: Element

Grade Product

- Close proximity to abundant, low-cost sources of bulk consumables Lithium 2.10% 94%

- Location adjacent to markets for bulk by-products (particularly SOP Potassium 6.77% 85%

and sodium silicate) Silicon 23.10% 85%

- Established infrastructure (particularly road, rail and port Caesium 0.05% 81%

infrastructure)

Tantalum 0.03% 70%

- Close proximity to a skilled labour force with competitive labour

rates Expected Construction Costs

Item US$M

Feasibility Study and Mineral Resource delineation program Feasibility Study and 2017 Owners Costs 5.0

commenced April 2017 L-Max® plant direct costs 16.2

L-Max® plant services 4.6

- A$3.7 million raised April/May 2017 via pro-rata non-renounceable

Infrastructure 2.6

Rights Issue Indirect costs 6.7

Contingency at 20% 6.0

*Refer to ASX Announcement, Positive Phase 1 L-Max® Plant Pre-Feasibility Study”” dated 27 February 2017

for further details Total 41.1

8

Phase 1 L-Max® Plant Project Progressing to DFS

Key metrics for the Feasibility Study scope* will be:

Project Planning Key Metrics

Key Parameter Key Metric

- Plant throughput rate 3.6tph of lithium-mica concentrate

Lithium Carbonate (>99.5%) Production 3,000 tpa

(annualised rate of 29,000tpa – 91.4% operating time)

SOP (>95% K2SO4) Production 3,000-4,000 tpa

- Battery grade lithium carbonate equivalent (LCE) Sodium Silicate (40wt% solution at SiO2:Na2O ratio of 2.0)

40,000-50,000 tpa

Production

production of c. 3,000tpa

Caesium (as metal contained in formate) Production 10-100 tpa

- Average C1 Costs nil to negative after by-products Tantalite Con (30% Ta2O5) Production 20-25 tpa

Li-Carbonate C1 cost after by-products credits

The L-Max® Advantage

L-Max® leaches lithium from certain micas and phosphates without

roasting – conventional processing of spodumene requires capital and

energy intensive roasters to extract lithium, often with no by-products

L-Max® reagents and operation have straightforward health, safety and Lepidolite Zinnwaldite Ambygonite

environmental characteristics K(Li,Al,Rb)3(Al,Si)4O10(F,OH)2 KLiFeAl(AlSi3)O10(OH,F)2 (Li,Na)AlPO4(F,OH)

L-Max® utilises common use, inexpensive reagents & is energy efficient

100

L-Max® is novel but utilises conventional equipment and straightforward 80

Metal extraction (%)

processes – a series of agitated tanks, crystallisers and filters

60

Lithium

By-products include potassium sulphate fertiliser (SOP), sodium silicate, 40

Cesium

gypsum and potentially caesium and rubidium formates 20

Potassium

Fast leach kinetics, high recoveries and moderate process cost estimates 0

0 2 4 6 8 10 12 14 16 18 20 22 24

make for compelling economics

Time (hrs)

Element leach curves under L-Max® - PFS sample

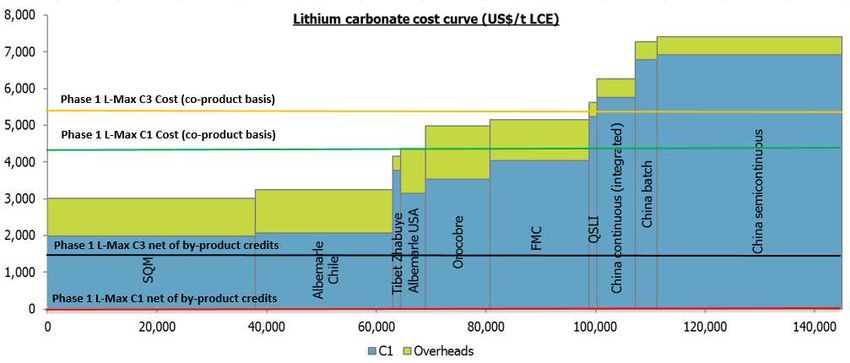

10Peer Analysis

Phase 1 L-Max® Plant is Favourably Placed on the Global Cost Curve*

*Lithium Carbonate Cost Curve 2016 co-product basis (Source: Roskill). Ref: ASX Announcement “Positive Phase 1 L-Max® Plant Pre-Feasibility Study”, 27 February 2017

11Business Model

Operating Business Royalty Business

L-Max® process plant

(wholly owned/JV)

L-Max®

Integrated with third-party

concentrator licences

Third-party

concentrate feed

and mines

Third-party mine ore feed

12Opportunities

Mining and processing sustainably for 21st century products

2017 2018 2019 2020 2021

Phase 1 L-Max® Plant

Phase 1 L-Max® Plant Mini-plant trial & due diligence

PFS c.3,000t pa LCE

DFS

Permits & Approvals FID H2SO4 ~50,000t pa

Early Works/FEED DFS ~US$5M

Implementation

Operation Development ~US$40M

Full Scale L-Max® Plant

Scoping Study Full Scale 1 L-Max® Plant

PFS @ c. 20,000t pa LCE

DFS

Permits & Approvals FID H2SO4 ~400,000t pa

Early Works/FEED

Implementation

Studies ~US$10M

Operation Construction ~$Pending

13Directors and Senior Management Team

Mr. Gary Johnson Mr. Joe Walsh Mr. Tom Dukovcic Mr. Mark Rodda Ms. Shontel Norgate Mr. Gavin Becker

ARSM, BSc (Eng), MBA,

MAusIMM, MAICD BEng, MSc BSc (Hons), MAIG, MAICD BA, LLB B.Bus FAusIMM, CP(Met), GAICD

Chairman Managing Director Director Exploration Non-Executive Director Chief Financial Officer Business Development

Gary has over 30 years Joe is a resources industry Tom is a geologist with over Mark is a lawyer with 20 years Shontel is a finance executive Gavin is a metallurgist with

experience in the mining executive and mining 25 years experience in experience in the resources with over 20 years commercial 40 years industry experience.

industry as a metallurgist, engineer with over 25 years exploration and sector including the experience in the resources During that time he has

manager, owner, director and experience working for development. He has worked management of local and industry including debt and worked in senior operational,

managing director possessing mining companies and in diverse regions throughout international mergers and equity finance, financial R&D, feasibility study and

broad technical and practical investment banks. Joe also Australia, including the acquisitions, divestments, reporting, project management, consulting roles on lead/zinc,

experience of the workings has extensive equity market Yilgarn, Kimberley, central exploration and project joint corporate governance, gold, uranium, copper and

and strategies required by experience and has been Australia and northeast ventures, strategic alliances, commercial negotiations and nickel/cobalt/scandium

successful mining companies. involved with the technical Queensland. Tom is a corporate and project financing business analysis mines and/or projects.

and economic evaluation of Member of the Australian transactions and corporate

many mining assets and Institute of Geoscientists and restructuring initiatives.

companies around the world. a Member of the Australian

Institute of Company

Directors.

14Lepidico Strategy

To become a fully integrated lithium business through the value chain

from mine to battery grade lithium chemical

by leveraging its registered L-Max® technology to process concentrate

from high-quality lithium mica Resources

via high-return, strategically located developments in low risk jurisdictions.

15Q&A

16Creative Resources Leadership

Website: www.lepidico.com

Contact us: info@lepidico.comYou can also read