DISTRICT OF OA19!'BAY - Oak Bay

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DISTRICT OF

OA19!‘BAY

REPORT TO: Council

FROM: Christopher Paine, Director of Financial Services

MEETING DATE: April 23, 2020

RE: COVlD—19Financial Plan Risk and Financial Hardship

Mitigation Measures

STAFF RECOMMENDATIONS

THAT Staff be directed to establish an Alternative Tax Collection Scheme Bylaw, should direction

for financial hardship mitigation measures and associated deadline adjustments not be

forthcoming from the Provincial Government, to extend the payment due date for property taxes

to August 4, 2020 to align with the date the District is required to pay property taxes levied on

behalf of the Capital Regional District, the Capital Regional Hospital District, BC Assessment, the

Transit Authority and the Municipal Finance Authority;

THAT Staff be directed to amend the draft 2020-2024 Financial Plan as presented at the March

12, 2020 Committee of the Whole meeting to reduce the tax funded portion of the proposed 2020

budget increase by 1.2% through:

1) deferring the funding for, and hiring of, the Manager of Infrastructure and Facilities position

until 2021,

2) using New Development Taxation revenue to offset infrastructure funding, and

3) incorporating all other budget deliberation direction provided from the Committee of the Whole

as of March 12, 2020 including increasing efforts to renew infrastructure particularly in water,

waste water, transportation and facilities, in order to achieve sustainable service delivery for

the next 50 to 75 years;

AND FURTHER, THAT the Mayor, on behalf of Council, advocate to the Provincial Government

to:

1) increase amounts for Homeowner Grants, and create a new category of grant applicable to

persons who have lost income due to the pandemic, and

2) reinstate the Financial Hardship Deferment Program and extend the program to commercial

properties as well as residential home owners.

EXECUTIVE SUMMARY

This report recommends a number of strategies to Council that the District may undertake in order

to assist ratepayers who are experiencing financial hardship as a result of COVlD-19, while

maintaining local government business continuity and reserve balances as currently considered

in the draft Five Year Financial Plan. This report also highlights current budget risks and potential

mitigation strategies for Counci|’s consideration during these uncertain times resulting from the

pandemic.

Staff consider the recommended focus on financial hardship mitigation measures to be consistent

with the approach that the Provincial and Federal governments are seen to be taking in response

to COV|D—19, by directing financial hardship mitigation measures to those who are in need in the

shorter term.

Staff are recommending that Council consider reducing the tax funded portion of the proposed

budget by 1.2% (from 8.1% to 6.9%), from the direction provided at the March 12, 2020 Committee

of the Whole meeting. This reduction can be achieved by deferring the funding for, and hiring of,

COVID-19 Financial Plan Risk and Financial Hardship Mitigation Measures Page 1 of 12

the Manager of Infrastructure and Facilities until 2021 and by using New Development Taxation

revenue to offset infrastructure funding.

Further, staff are recommending that Council consider “staying the course” with the other

initiatives and funding endorsed by Council on March 12, 2020. This recommendation

proposed

is linked to consideration of business recovery and continuity once the pandemic has passed.

Additionally, this approach creates resiliency in the operating budget for potential responses to the

pandemic that may be required in the future but that are not currently anticipated.

While some capital projects currently scheduled for initiation/completion in 2020 may not be

achieved given staffs focus on COVlD—19response, deferring these projects is not likely to result

in a reduction in 2020 taxation because the majority of these projects are funded from existing

reserves established for such undertakings. For example, the Municipal Hall renovation is fully

funded from a project specific reserve, so a deferral of this project would not have any impact on

2020 taxation.

Throughout the changing conditions associated with the pandemic, the District is committed to

recovering in an operationally enhanced status. Opportunities to achieve this status include

technology and ef?ciency implementations, development of shelf ready projects for potential

stimulus packages that other levels of government may provide, consideration of borrowing at

historically low rates for some capital projects, and more. District staff will stay vigilant for

opportunities that Council may wish to consider in support of the endorsed “better than before

pandemic” approach that the District is adopting.

The tax increase options contained in this report for Council’s consideration are as follows:

Tax increase 8.1% 6.9% 5.4% 3.9%

Average monthly cost to median $20.00 $17.00 $13.00 $10.00

household (rounded)

BACKGROUND

Staff have provided the recommendations contained in this report founded on the principles that

Council:

o wishes to mitigate the financial hardship that municipal taxation may represent to some citizens

and businesses (as permitted under legislation) during this time of pandemic through a variety

of possible means;

0 wishes to continue with infrastructure replacement, striving for sustainable service levels,

maintaining reserve balances over the longer term, and delivering on the numerous other

services and priorities detailed in the 2020 budget process and the draft Five Year Financial

Plan;

0 wishes staff to continue with significantly increasing efforts to renew infrastructure (particularly

in water, waste water, transportation and facilities), in order to achieve sustainable service

delivery for the next 50 to 75 years;

c supports the proposed staffing levels contained in Appendix A to this report, in order to better

facilitate an expeditious return to the course of normal business for the District once the

Provincial State of Emergency ends and the District’s Emergency Operations Centre (EOC) is

deactivated;

o intends to have the District recover from COVlD—19at an operationally enhanced status, once

demobilization of the EOC occurs and recovery from the pandemic is complete by maximizing

opportunities within approved budget that may present during the EOC planning stages; and

o acknowledges that the current pandemic, while having profound and wide spread impacts,

may be a relatively shorter term challenge when considered in the context of the overall Five

Year Financial Plan.

COVlD~19 Financial Plan Risk and Financial Hardship Mitigation Measures Page 2 of 12

Staff are requesting Council provide alternate direction, should any of the premises above not be

reflective of Council’s position.

Staff consider the recommended focus on ?nancial hardship mitigation measures contained in this

report to be consistent with the approach that the Provincial and Federal governments are seen

to be taking in response to COVlD-19, by directing financial hardship mitigation measures to those

who are in need in the shorter term. At time of this report writing, local governments are awaiting

potential direction from the Provincial government on financial hardship mitigation measures and

associated deadline adjustments. Should the Provincial government not provide such measures

over the coming weeks, Council has some authority to undertake District initiated financial

hardship mitigation measures and deadline adjustments as detailed below.

Staff recognize that while some local governments are reducing or negating tax increases for 2020

in response to the uncertainties associated with the pandemic, the economic realities across the

region vary greatly. Some unique attributes of the District include:

1) The District’s tax base is primarily residential (94%). This provides a stable tax base but means

there is very little non-residential tax base available to mitigate costs to residents.

2) The District is already an overly lean organization, in terms of staf?ng numbers, for the levels

of service that the District provides.

3) The District has an older demographic and a higher percentage of residents employed in

sectors not currently experiencing significant job losses when compared to the Provincial

average (Source 2016 Census).

—

4) The District operates a high quality Parks, Recreation and Culture department. The size and

scope of this department is unique for a municipality of the District’s size. The high quality

services provided by this department are supported by high cost recovery ratios. This means

that in economically difficult times, recreational revenues can fall sharply.

5) The District is a ‘built-out’ community, meaning that there is very little undeveloped land. This

fact, combined with the low rate of development, means the District does not have signi?cant

New Development Taxation revenue available to reduce the impact of annual taxation

increases. Many other communities in the region benefit in the short term from fast growth and

associated significant New Development Taxation revenue.

6) Oak Bay was incorporated in 1906 and much of its infrastructure is aging. A significant

inventory of infrastructure is under the District’s care including over 270km of pipe. The amount

and age of infrastructure is unusual for a municipality of the District’s size in the Capital Region.

7) The District’s pace of achieving funding for, and sustainably delivering on, infrastructure

replacement is unique. Few communities in B.C. are increasing infrastructure funding at a

pace comparable to the Districts, as per Counci|’s Strategic Priority of achieving sustainable

service delivery.

8) The Provincial Government’s Municipal Wastewater Regulation requires all BC municipalities

to have separate storm water and sanitary sewer systems. The District is one of the few BC

municipalities, and the only local government in the Capital Region, to have a combined storm

and sanitary sewer system. This system must be separated as part of the Core Area Liquid

Waste Treatment program. This separation project represents significant cost implications to

the District.

9) The District staffs both a Municipal Police force and a 24/7 career Fire Department. The

District’s protective services are highly respected in the region. There is only one other similar

sized municipality in the region with both a Municipal Police force and a career Fire

Department.

For the reasons noted above, staff observe that a “one size fits all” approach to local government

tax rate adjustments resulting from the pandemic is unworkable. The District is recognized as

being unique from other local governments in the region by its challenges, amenities, assets and

service levels.

COVlD—19Financial Plan Risk and Financial Hardship Mitigation Measures Page 3 of 12

HISTORIC CONTEXT

On March 11, 2020 the World Health Organization declared COV|D—19 as a pandemic. On March

12, 2020 the District concluded 2020 budget deliberations pending adoption of the annual

Financial Plan Bylaw.

On March 4, 2020 the Bank of Canada (BoC) cut its benchmark interest rate by 50 basis points

to 1.25% as a result of COVlD—19’smaterial negative shock to the Canadian and global outlooks.

Shortly thereafter, the BoC cut its benchmark rate to 0.75% and then to 0.25% on March 13 and

27 respectively.

Since March 17, municipal facilities have been closed to the public and senior staff work has

focused on the COV|D—19 response, including facilitating delivery of core municipal services by

Departments within a changing/evolving business model. While some core services have been

altered or slowed (e.g. advancement of land use applications which require Advisory Body review

or public input), staff continue to undertake meaningful work for the benefit of the District in

alignment with Council’s Strategic Priorities (ensuring access to diverse housing options within the

built environment; achieving sustainable service delivery; providing service excellence; enhancing

and promoting quality of life and sense of place; and demonstrating leadership in fostering

community health and resilience).

02/29 03/11 03/13 03/20

8 confirmed WHO OB EOC

03/Z8

Parksand 884 confirmed

Cases of declares activated; P[3YB"0U”d5 Cases of

COVID-19 in COV|D—19 a

closed COVI13-19 in

BC pandemic BoC cuts

BC

rate to

0.75%

02/29 03/15 03/30

03/04 03/122020 03/27

BoC cuts rate budget talks 3°C CW5 rate

to 1.25% conclude to 015%

ANALYSIS

In response to the COV|D—19 pandemic, senior levels of government, utilities and banks have

undertaken significant measures with an approach focusing on mitigation of financial hardship for

those in need.

Staff have considered the current economic conditions and are recommending that Council

consider reducing the tax funded portion of the proposed budget by 1.2%. The following rationale

for staffs recommendation is respectfully provided for Council’s consideration:

1. Budget risks and mitigation strategies

Staff have analysed the Districts draft 2020 Financial Plan in the context of the pandemic and

identi?ed the following areas of significant risk:

Parks, Recreation and Culture (PRC) revenue;

Investment income;

Building Permit revenue;

Lease revenue; and

Property tax penalties and interest.

COV|D—19 Financial Plan Risk and Financial Hardship Mitigation Measures Page 4 of 12

The District’scurrent strategy to mitigate the impact of these risks is to: defer hiring of 250 auxiliary

staff; to defer the funding for, and hiring of, 1 full time equivalent employee (FTE); to defer the

hiring of a number of existing vacancies in departments with reduced service levels; to use the

2019 surplus; and, to reduce current year transfers to reserve. Should revenue decline into

subsequent ?nancial periods, the budget gap would need to be addressed through increased

taxation or decreased services. Staff commits to bringing financial risks, resulting from changing

circumstances as the pandemic evolves, to Council for their consideration and direction.

2. Reduction of Tax increase

Staff have considered the current economic conditions and are recommending that Council

consider reducing the tax funded portion of the proposed 2020 budget increase by 1.2%.

2.1 Effectiveness of Tax Increase Reduction

it is anticipated that a substantial tax decrease in the municipal portion of the tax billwill not likely

have a signi?cant impact on many taxpayers in Oak Bay; staff estimate that municipal property

taxes account for approximately 0.3% and 0.43%1 of household expenditures. For example,

reducing the proposed 8.1% tax increase to 0% would save the median residential property

approximately $20 per month in the short term but would negatively impact the District’s long term

financial sustainability and future tax rates. Staff are instead recommending a more effective,

focused approach for those experiencing ?nancial hardship.

Approximately 44% of the municipal tax bill represents taxes collected on behalf of other taxing

authorities. None of these taxing authorities have indicated there will be a deferral in due dates or

reduction in tax rates (except the school tax rate business and industry class properties).

The response to COVID-19 includes numerous ?nancial hardship relief mechanisms to address

the more significant components of household expenditures and income loss. Some of these

mechanisms are noted in the table below:

Income Support - The Federal government has implemented the Canada Emergency

Response Bene?t which provides $2,000 a month for workers who have

stopped working due to COVID-19.

0 Additionally, the Federal government is providing a 75% wage subsidy to

qualifying businesses.

Shelter o Most financial institutions are providing mortgage deferral options.

- The Office of the Superintendent of Financial Institutions announced that it

will not count mortgage deferrals as arrears for banks.

o The Province of BC has introduced a new rental supplement program.

- Utilitybilldeferral programs and credits are available for those experiencing

financial hardship.

TFanSP0l't8’ii0n Gas prices have fallen approximately 25% since COVID-19 was declared a

0

pandemic by the World Health Organization.

- lCBC has introduced a 90-day payment deferral program.

c Free bus fare has been implemented by BC Transit.

2.2 Long Term Ratepayer impact of Tax increase Reduction:

A municipal tax decrease in response to COVlD-19 would not reduce the overall long—termtax

impact to a ratepayer in the District, if Council stillwished to achieve its goals as stated throughout

the 2020 budget deliberations. if the District was, for example, to implement a 0% tax increase for

1

Based on: (1) “Living Wage for BC’s Capital Region” published by the Community Social Planning

Council and (2) the Survey of Household Spending published by the Province of British Columbia.

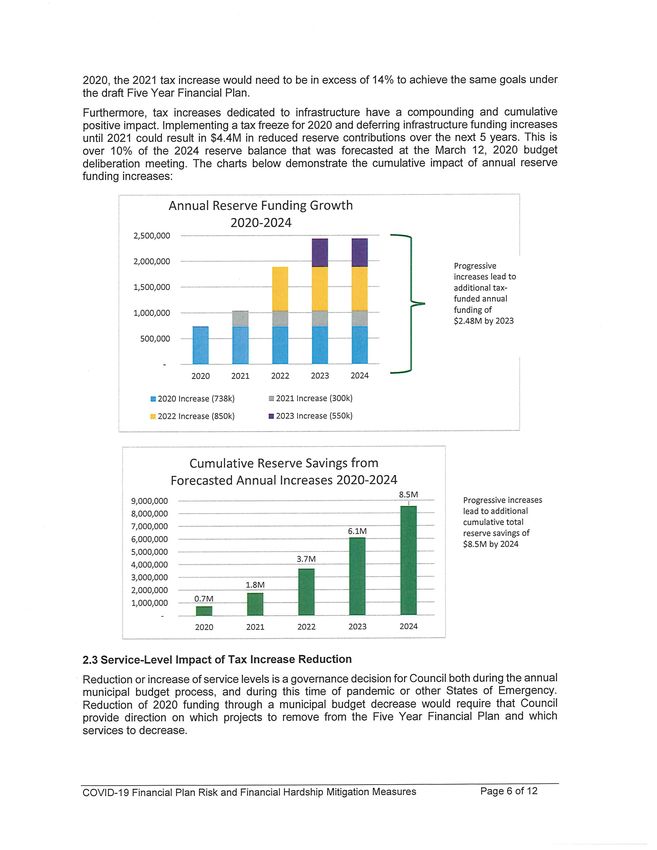

COVID-19 Financial Plan Risk and Financial Hardship Mitigation Measures Page 5 of 122020, the 2021 tax increase would need to be in excess of 14% to achieve the same goals under

the draft Five Year Financial Plan.

Furthermore, tax increases dedicated to infrastructure have a compounding and cumulative

positive impact. Implementing a tax freeze for 2020 and deferring infrastructure funding increases

until 2021 could result in $4.4M in reduced reserve contributions over the next 5 years. This is

over 10% of the 2024 reserve balance that was forecasted at the March 12, 2020 budget

deliberation meeting. The charts below demonstrate the cumulative impact of annual reserve

funding increases:

if if

22

charisma‘.riegerv;.;:.;;.diiagémi

2020-2024

..,,._ ,..,_ _. 2...

..._ - _.

...,.__ .2.

__ ......2__.,..

...._ .. _. ._

2,000,000 v

— —— —~—— -«

.

Progressive

increases lead to

1,500,000 additional tax-

funded annual

1,000,000 —--~—-~—

V ~

funding of

$2.48M by 2023

2020 2021 2022 2023 2024

I 2020 Increase (738k) E 2021 Increase (300k)

I 2022 Increase (8S0k) I 2023 Increase (550k)

Cumulative Reserve Savings from

Forecasted Annual Increases 2020-2024

~—~§'~iV|———~

9,000,000 —~——~——————~—v ~—~~———~~—-—~»~——~—«—~—-r—~~~-~—--~——~

——

Progressive increases

3,000,000 lead to additional

cumulativetotal

reserve f savings 0

6'0o0'000 $8.5M by 2024

$000300

QOOODOO

&OOQ00O

LOOQ000

LOOQOOO

2020 2021 2022 2023

2.3 Service-Level Impact of Tax Increase Reduction

Reduction or increase of service levels is a governance decision for Council both during the annual

municipal budget process, and during this time of pandemic or other States of Emergency.

Reduction of 2020 funding through a municipal budget decrease would require that Council

provide direction on which projects to remove from the Five Year Financial Plan and which

services to decrease.

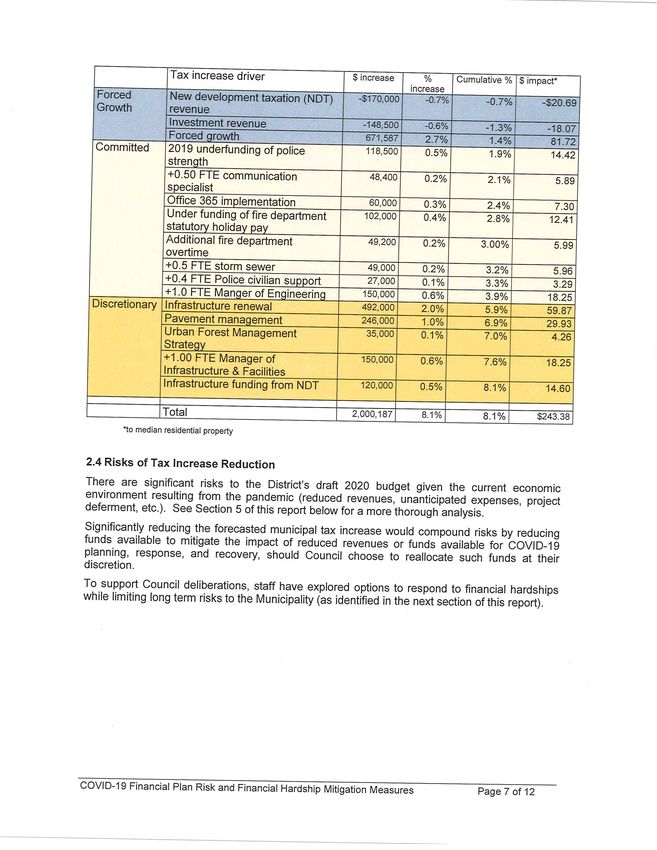

COVID-19 Financial Plan Risk and Financial Hardship Mitigation Measures Page 6 of 12Tax increase driver $ increase % TCumulative

% $ impact*

increase 4

Forced New development taxation (NDT) -$170,000 -0.7%

L

-0.7% -$20.69

Growth revenue

Investment revenue 448,500

Forced growth 671,587 2.7% 1.4% 81.72

Committed 2019 underfunding of police 118,500 0.5% 1.9% 14_42

stre_n_g?1

+0.50 FTE communication 48,400 0.2%‘ 2.1% 5.89

specialist

~_Of?ce 365 implementation 60,000 0.3% 2.4% 7.30

A

Under funding of fire department 102.000 0.4% 2.8% 12.41

statuto_ry_holicl3y_pay _

Additional?re department 49,200 0.2% 3.00% 5.95

overtime

+0.5 FTE storm sewer 49,000 0.2% Jr 3.2%T 5.96

_+o.4 FTE Police civilian supgart ”

27,000 0.1% 3.3%; 3.29

.0 FTE Mner of Enineerin 150,0000.697 7

Total 2,000,187 8.1% 8.1% $243.38

*to median residential property

2.4 Risks of Tax Increase Reduction

There are significant risks to the District’s draft 2020 budget given the

current economic

environment resulting from the pandemic (reduced revenues, unanticipated expenses, project

deferment, etc.). See Section 5 of this report below for a more thorough analysis.

Signi?cantly reducing the forecasted municipal tax increase would compound risks by

reducing

funds available to mitigate the impact of reduced revenues or funds available

for COVID-19

planning, response, and recovery, should Council choose to reallocate such

funds at their

discretion.

To support Council deliberations, staff have explored options to respond to

?nancial hardships

while limitinglong term risks to the Municipality(as identifiedin the next section

of this report).

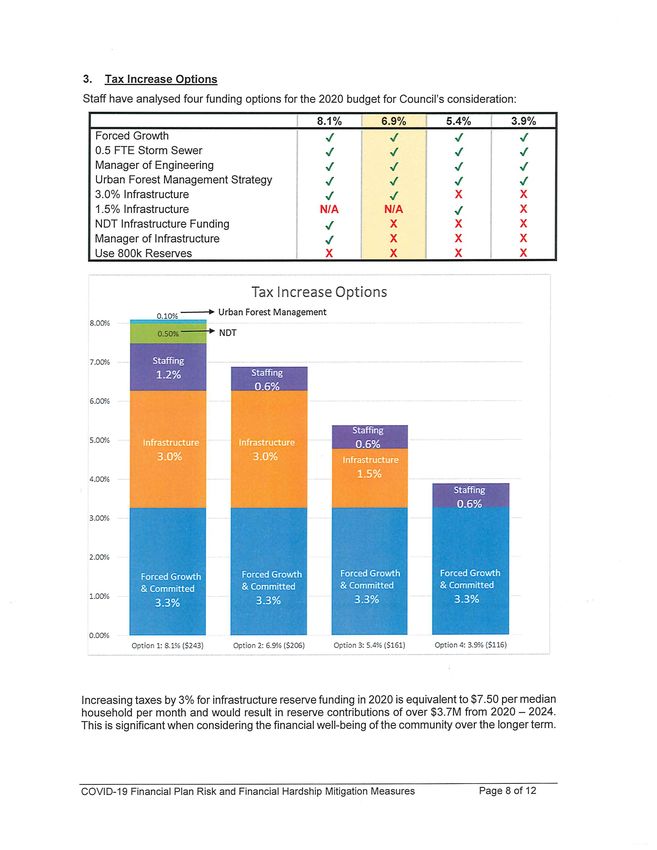

COVID-19Financial Plan Risk and Financial Hardship Mitigation Measures Page 7 of 123. Tax Increase Options

Staff have analysed four funding options for the 2020 budget for Council’s consideration:

Forced Growth

0.5 FTE Storm Sewer

Manager of Engineering

Urban Forest Management Strategy

3.0% Infrastructure

1.5% Infrastructure

NDT Infrastructure Funding

Manager of Infrastructure

Use 800k Reserves

Tax Increase Options

———> Urban Forest Management

8.00‘/o

NDT

7.00% — — —

Staffing

0.6%

6.00%

Staf?ng

5-00% Infrastructure Infrastructure 0.6%

3.0% 3 .O% Infrastructure

4.00%

1.5%

3.00%

2.00%

Forced Growth Forced Growth Forced Growth Forced Growth

& Committed & Committed & Committed & Committed

1.00%

3.3% 3.3% 3.3% 3.3%

Option 1: 8.1% ($243) Option 2: 6.9% ($206) Option 3: 5.4% ($161) Option 4: 3.9% (5116)

Increasing taxes by 3% for infrastructure reserve funding in 2020 is equivalent to $7.50 per median

household per month and would result in reserve contributions of over $3.7M from 2020 2024. -

This is signi?cant when considering the ?nancial well-being of the community over the longer term.

COVID-19 Financial Plan Risk and Financial Hardship Mitigation Measures Page 8 of 124. Financial Hardship Mitigation Strategies for District Residents in Need

a. UtilityBilling Penalty Abatement

At the March 16, 2020 Special Council meeting, Council passed the following resolution: “That

Staff be directed to prepare bylaw amendments such that penalties and interest on utility bills

are indefinitely suspended for bills due on or after March 16, 2020”. Staff have prepared a

draft Amendment Bylaw that is included in the agenda for the April 23 Special Council meeting

and are requesting three Readings and adoption of the Amendment Bylaw.

b. Property Tax Deferral —

Alternative Tax Collection Scheme

Section 235 of the Community Charter empowers the District to establish an Alternative Tax

Scheme Collection Bylaw. Such a bylaw may establish tax due dates, penalties and set terms

and conditions in relation to payments. Should Council wish to consider extending the property

tax due date, staff recommend an August 4 due date.

As noted above, the Provincial Government has indicated they are working on a financial

package for local governments and are awaiting potential direction on financial hardship

mitigation measures and associated deadline adjustments. Should the Provincial

Government not provide such measures over the coming weeks, Council has some authority

to undertake District initiated financial hardship mitigation measures and deadline

adjustments.

Extending beyond August 4 carries significant risk unless other taxing authorities also adjust

their due dates. The District is responsible for collecting taxes for a variety of taxing

authorities: Provincial School Tax, Capital Regional District, Capital Regional Hospital District,

BC Transit Authority, BC Assessment and the Municipal Finance Authority. Collections for

these authorities exceeded $20M in 2019. The District must in most cases remit funds to

these taxing authorities on the first day of business in August each year. If the District was to

implement a tax due date after August 4 in 2020, the District would need additional cash flow

to remit these taxes while waiting for payments from Oak Bay taxpayers.

Under normal circumstances, using the current established due dates and penalties, the

District has the financial capacity and cash flow to maintain operations and advance capital

projects without borrowing short—term. While the possibility of short-term borrowing exists

through the Municipal Finance Authority if a revenue anticipation bylaw is enacted in this time

of pandemic, the Municipal Finance Authority has indicated that they are unable to lend to

every municipality in BC who may need short term loans to cover property taxes.

Deferring the property tax due date beyond August 4, or reducing the penalty for late payment,

would likely significantly impact District cash flow. Impacts to cash flow must be considered

during this time of pandemic when the District is experiencing decreased recreation revenues;

a significant portion of the District’s annual budget.

c. Solid Waste Billing Deferral

Historically, the solid waste user fee has been billed on the annual property tax bill and is a

charge that does not qualify for the deferral program. Staff are recommending that the solid

waste user fee be billed on the utility bill instead of the usual practice and be deferred until

the fourth (4th) quarter of 2020, with the potential for further assessment at that time. This

approach would help ratepayers defer approximately $275 in payments until the Fall of 2020;

an expense that would normally be collected in July. This approach does not significantly

impact cash ?ow for the District.

d. Parking Enforcement Focus

Parking patterns have changed significantly as a result of government mandated isolation,

physical distancing measures and business closures. The District is currently focusing efforts

COVlD—19Financial Plan Risk and Financial Hardship Mitigation Measures Page 9 of 12on education and compliance around parking regulations, with a reduced focus on fines.

Ticketing with financial penalties (?nes) will still be used for repeat offenders to encourage

long term compliance with parking regulations. Note beyond this general approach, “no

—

parking” restrictions in the area of Willows Beach will be enforced through ticketing given the

need to reduce congestion and better enable physical separation on the beach.

Advocate to the Provincial Government

Staff are recommending that the Mayor advocate, on behalf of Council, to the Provincial

Government to:

0 increase amounts for Homeowner Grants, and create a new category of grant applicable

to persons who have lost income due to the pandemic, and

o reinstate the Financial Hardship Deferment Program and extend the program to

commercial properties as well as residential home owners.

The Provincial tax deferment program is a low interest loan program that allows taxpayers to

defer paying all or part of their annual property taxes (excluding utilities that are included on

the tax bill or outstanding balances from previous years). The loan is registered as a lien on

the property. The Province has been building a new online tax deferment portal for launch in

2020. This portal will allow customers to apply for property tax deferral online. This program

may be a solution for individuals who are experiencing a temporary reduction in income and

who also maintain the required minimum equity in their home.

Currently this deferral program is only offered to owners who are at least 55 years of age or

to owners who ?nancially support children under the age of 18. The Province previously

offered a financial hardship deferment program which has since been eliminated.

Deposits & Securities

The District collects deposits and securities from developers for various reasons. These

securities ensure that required works and services are completed to the appropriate standard.

Under normal circumstances, the District would not refund these securities until works and

services are completed in their entirety. However, the District has changed its practice in the

short term to provide partial refunds as work is completed in phases in order to better enable

customers to have quicker access to needed cash ?ow during the COV|D—1 9 pandemic.

5. 2020 Budget Risks and Mitigation Strategies

Staff have analysed the Districts draft 2020 Financial Plan in consideration of the COVlD—19

pandemic, and identified areas of significant risk. Moving fon/vard, staff will continue to monitor

economic conditions and recommend Financial Plan amendments as necessary for Counci|’s

decision making. Revenues that will likely be detrimentally impacted as a result of the pandemic

are identified as follows:

a. Parks, Recreation and Culture (PRC) revenue —

The District’s Parks, Rec and Culture

operating budget is approximately $13.6M in 2020. This budget is funded by $8.9M in

program revenues and $4.7M in taxation. A significant decrease in program revenues would

increase the need for tax funding.

Note PRC has experienced a significant revenue decrease as a result of the pandemic, with

—

facilities continuing to be closed to the public. Much of this revenue decrease is mitigated by

a corresponding decrease in variable program costs. |t’s dif?cult to forecast the impact to the

2020 budget without knowing the duration of the current COVID-19 crisis, but ?nancial

forecasts until the end of August anticipate a $2M net revenue loss.

Building Permit revenue -Forecasted Building Permit revenue in the draft 2020 Five Year

Financial Plan is $750,000. Staff expect a signi?cant decrease in revenues while economic

conditions associated with the pandemic remain.

COVID-19 Financial Plan Risk and Financial Hardship Mitigation Measures Page 10 of 12c. Investment income The Bank of Canada has dropped

-

its benchmark interest rate by 1.50%

since 2020 Financial Plan deliberations began. Staff

anticipate a

Guaranteed Investment Certificates and Money Market Fund returns. corresponding fall in

have not yet dropped proportionately. Furthermore, Yields, though volatile,

portfolio is invested in Guaranteed Investment

approximately 20% of the District’s

Certi?cates with a rate of return exceeding

2019’s investment performance.

cl. Lease revenue Approximately$50,000 in the

—

District’slease revenue is linked to the ?nancial

performance of one of our tenants. This tenant has

recently closed their doors in response to

ProvincialOrders related to the pandemic.

e. Property tax penalties and interest -Should Council implement the financial hardship

measures that staff are recommending, there will be a measurable impact

to the District’s

penalty revenue. The District’sinterest revenue is also expected

to fall by 20% based on the

Bank of Canada benchmark rate reductions.

Should revenue decline into subsequent financial periods, the budget

gap would need to be

addressed through increased taxation or decreased services. At a

minimum, staff will prepare

quarterly budget reports and bring forward Financial Plan Bylaw

amendments as necessary for

Council’s consideration and direction.

STRATEGIC PRIORITYSUPPORTED

Recommendationsin this report mainly support two strategic priorities: (1) achieving sustainable

service by integrating the asset management program within a long—termfinancial plan, and (2)

providing service excellence by optimizing effectiveness and fostering public

public engagement

engagement. Note —

would be “consult” as per lAP2 noted below.

IAP2 FRAMEWORKENGAGEMENT(INDICATE WITH X)

INFORM X CONSULT INVOLVE COLLABORATE

In addition to the public engagement conducted throughout the 2020 strategic

planning and budget

process, the public is being provided with this report 10 days in advance

of the electronic Special

Council meeting scheduled to be held April 23, 2020 in order to allow time

for comments to be

submitted to the District via email, letter or phone.

TIMELINE/PROCESSINEXT

STEPS

Staff will bring fon/vard a number of bylaws for adoption based on Council

direction:

1) Five Year Financial Plan Bylaw 4) Tax Rates Bylaw

2) Boulevard Frontage Tax Bylaw 5) Water Rates Amendment Bylaw

3) Refuse Collection and Disposal Bylaw 6) Sewer User Charges Amendment Bylaw

7) Alternative Tax Collection Scheme

Bylaw

COVID-19 Financial Plan Risk and Financial Hardship Mitigation Measures

Page 11 of 12OPTIONS & FINANCIAL IMPACT

Property Tax Due Date Deferrall Property Tax Penalty Abatement

Council may wish to consider the following options with respect to the property tax deferral or

penalty abatement:

Option Penalty revenue Investment revenue Difference from status quo

No deferral $155,000 $825,000 $0

August 4 $135,000 $787,500 —57,500

September 30 $60,000 $600,000 -$320,000

Tax increase

Council may wish to consider the following options with respect to the 2020 tax increase:

Option $ lnc. Median 2021 tax Impact to 2024 Impact to 5 year

Res. Property increase‘ reserve balancez investment returns?’

Status Quo: 8.1% $244 5.7% $0 $0

NDT4& 1 FTE staffing deferral: $206 7.6% -$600,000 —$10,800

6.9% (Recommended)

NDT4& 1 FTE staffing deferral $161 9.1% —$2,700,000 —$48,000

& 1.50% infrastructure: 5.4%

Forced Growth & 1 FTE $116 10.7% —$3,050,000 -$54,000

staffing deferral: 3.9%

1: required tax increase to put ?nancial plan back on same pace as current draft 2020-2024 Financial Plan

2: assumes infrastructure funding progress shifts one year behind current draft 2020-2024 Financial Plan

3: assumes infrastructure funding progress shifts one year behind current draft 2020-2024 Financial Plan and investment return is

1.80%

4: NDT revenue is New Development Taxation revenue. This is revenue on new properties that were not subject to taxation in the

previous taxation year.

Staff remain vigilant in monitoring the financial impacts of COVID-19 and are committed to

providing Council with information and recommendations to position the District to respond and

recover effectively, while being sensitive to the financial hardship being experienced within the

community.

Respectfully submitted,

0

/as

/

Christopher Paine, CPA, CGA,

Director of Financial Services

I concur with the staff recommendation.

Lou Varéla,

Chief Administrative Of?cer

ATTACHMENT(S): APPENDIX A —

STAFFING PLAN

COVID-19 Financial Plan Risk and Financial Hardship Mitigation Measures Page 12 of 12Appendix A —

COVlD-19FinancialPlan Risk and FinancialHardship Mitigation

Measures

STAFFING PLAN

Position Status Risk Note

Deputy Director

of Corporate

SeWlCeS

.

0 Currently posted

Posting closes

April 9

Essential to

business

No impact to 2020

budget as the general

continuity and consulting budget was

- Hiring anticipated in recovery proportionately

the immediate short reduced

term

Deputy Director 0 Posting for this

Essential to

of Engineering Currently approved in

position is business principle for full

& Public Works anticipated prior to continuity and funding in core budget

Summer 2020 recovery $150,000

o if the position is not

filled in 2020, the

Director proposes to

use the allocated

funding for short

term engineering

consulting support

as required

Manager of 0 Based on the above Though risks Funding for this

Asset hires and current related to facilities position will be

Management & workloads, staff do remain as briefed delayed in the

Facilities not have the during the 2020 Financial Plan until

additional capacity Financial Plan 2021, unless Council

to manage the hiring process, delaying provides direction to

process for this the hiring of this establish the position

position. Therefore, position until 2021 funding in 2020

it is recommended is considered

that this hiring be manageable

delayed until 2021

Water & Sewer o Posting for these Essential to Currently approved in

positions is achieving principle for full

anticipated prior to necessary funding in core budget

Summer 2020 infrastructure Total FTE 4.0

maintenance in ~/ 3.5 FTE

order to ensure utility funded

sustainable $500,000

service levels for J 0.5 FTE taxation

water and sewer funded

$49,000

Building & Vacancies not being Not essential to Currently part of core

Planning filled in 2020 unless existing business budget

Department the current service continuity during , _

Currently 2

levels change pandemic N°t.r.'mngthese

vacant

The Department focus _ will

positions create

will be on the Housing Further review of flexibilitywithin the

positions: Plans these positions will

Framework and current year’s

Examiner and form part of operational budget

related initiatives,

Building & recovery planning without reducing 2020

while addressing a

Planning Clerk taxation

reduced number of

applicationsYou can also read