Duff & Phelps Select Energy MLP Fund Inc - NYSE: DSE

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INVESTOR GUIDE

Duff & Phelps Select Energy MLP Fund Inc.

NYSE: DSE*

This document must be preceded or accompanied by a DSE: A New Closed-End Fund Offering

preliminary prospectus for Duff & Phelps Select Energy

MLP Fund Inc. The information in this document and in the > A portfolio invested in select energy Master

preliminary prospectus is not complete and may be changed.

A registration statement relating to these securities has Limited Partnerships (MLPs)

been filed with the United States Securities and Exchange

Commission, but has not yet become effective. We may not > Potential for attractive tax-deferred distributions

sell these securities until the registration statement filed with

the Securities and Exchange Commission is effective. Neither and capital appreciation

this document nor the preliminary prospectus is an offer to

sell these securities and the Fund is not soliciting an offer to > Exposure to the energy renaissance and the

buy these securities in any jurisdiction where the offer or sale

is not permitted. reshaping of the U.S. energy economy

Investors should carefully consider the Fund’s investment

objective, risks, charges, and expenses before investing. The > Simplified tax reporting; Form 1099, no K-1

preliminary prospectus contains this and other information

about the Fund. Read it carefully before investing. Once the > A seasoned closed-end fund manager, with

Fund’s registration statement becomes effective, investors

should carefully read the final prospectus, which includes over 30 years of experience managing income-

the information described above. To obtain a preliminary

prospectus, and a final prospectus when available, please producing securities

call Virtus Investment Partners at 1-800-243-4361 or visit

www.Virtus.com/DSE.

Investing in common stock of the Fund involves substantial

risks that are described in the “Principal Risks Factors”

The MLP Advantage

section beginning on page 6. Risks are also described in the

preliminary prospectus.

> Potential for attractive risk-adjusted returns

Shares of closed-end funds frequently trade at a discount

from their net asset value. An investment in the Fund is

> Potential hedge against inflation and rising

not appropriate for all investors and is not designed to be interest rates

a complete investment program. The Fund is designed as a

long-term investment and not as a trading vehicle. > Low correlation and low beta** compared to

*It is anticipated that the Fund’s shares of common stock will

be approved for listing under the ticker symbol “DSE” on the traditional income-generating asset classes

New York Stock Exchange, subject to notice of issuance.

**Beta is a quantitative measure of the volatility of a given portfolio to a benchmark.

Higher beta suggests higher volatility.

Morgan Stanley & Co. LLC is acting as the lead underwriter in connection with the proposed offering. Member FINRA, SIPC.

Not FDIC Insured | May Lose Value | No Bank GuaranteeMLPs – An Alternative Investment

What is an MLP? A Master Limited Partnership is a publicly-traded limited partnership that operates primarily in the

exploration, development, production, processing, mining, refining, marketing, and transportation of energy-related

natural resources, including oil and natural gas.

MLPS HAVE GENERATED VISIBLE DISTRIBUTION GROWTH

> MLPs have generated an annual distribution 10.3%

Distribu

on Growth Average Infla

on Rate

9.8%

growth rate of 7.3%, on average since 2006, which 8.6%

is more than three times the rate of inflation. 7.6%

6.7% 6.8%

> Duff & Phelps has seen continued distribution 5.9%

growth as MLPs have capitalized on the

resurgence of U.S. energy production and the

3.0%

build-out of the necessary infrastructure.

2%

2006 2007 2008 2009 2010 2011 2012 2013

Source: Bloomberg Finance L.P. Average inflation rate based on 10-year average, actual from 2006-2013. Over different time periods, MLP distribution growth may

have been lower. If MLP distributions do not grow as projected, the Fund may suffer losses. There can be no assurance that MLP distributions will continue to grow and

they may decline. Past performance is not indicative of future results.

TOTAL RETURN HAS THREE DRIVERS

> MLPs have generated attractive total returns 29%

42% 46%

through a combination of distributions,

10%

distribution growth, and valuations.

Distribuon 41%

61% 42%

Distribuon Growth

Valuaon 16% 11%

3 Year 5 Year

7 Year

10.3% Average Infla

on

Distribu

on Growth Rate

Annualized Total Return 9.8% 15.04% 29.55%

14.59%

8.6%

7.6%

6.7% 6.8%

Source: Alerian Capital, Barclays Research estimates. As of 12/31/13. Bars depict the contribution to annualized total return of the Alerian MLP Index by each of the three factors:

5.9%

distribution, distribution growth, and valuation. Distribution is defined as average implied distribution at year end. Distribution growth is defined as percentage of price change not

3.0%

explained by change in valuation. Valuation is defined as percentage of price change explained by change in valuation multiples. Past performance is not indicative of future results.

2%

POTENTIAL FOR ATTRACTIVE RISK-ADJUSTED RETURNS2006

AND LOW CORRELATIONS

2007 2008 2009 2010 2011 2012 2013

>O

ver the past seven years, MLPs have produced 10

MORE RETURN MORE RETURN

attractive risk-adjusted returns, as compared LESS RISK Alerian MLP Index MORE RISK

Excess Return Over S&P 500® Index

to global indexes and traditional income-

generating asset classes. 5

Barclays U.S. Corporate High-Yield 2% Issuer Capped Index

>M

LPs have shown low or negative correlations

S&P 500® Index

with these asset classes as well. The correlation 0

with the S&P 500® Index has been 0.53 over the S&P 500 Ulies Index

MSCI MSCI U.S. REIT Index

past seven years.

World Index

-5

LESS RETURN S&P GSCI All Crude LESS RETURN

-10 LESS RISK MORE RISK

0.0 0.5 1.0 1.5 2.0

Beta

Source: eVestment. Data is for the 7 year period ended 4/30/14. Correlation is a measure that determines the degree to which two variables’ movements are

associated. Correlation will vary from -1 to +1. A -1 indicates perfect negative correlation and a +1 indicates perfect positive correlation. Beta is a quantitative measure

29%

of the volatility of a given portfolio to a benchmark. Higher beta suggests higher volatility. Over different periods,

42% correlation, beta, and return may have been46% different.

Past performance is not indicative of future results. 10%

Distribuon

Index information is shown for illustrative purposes only. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct

investment. Each index discussed above is comprised of different securities and asset classes.

Distribuon Additional information

Growth 41% regarding the different types of securities42%

and asset

classes that make up each index in the chart above is provided on page 8 of this brochure. 61%

Valuaon

10 16% 11%

500® Index

2 MORE RETURN performance

There is no assurance that any historical Alerian3 MLP Index illustrated5will

or trend

Year Yearbe repeated MORE

in the7RETURN

future.

Year

LESS RISK

Annualized Total Return 15.04% 29.55% MORE14.59%RISK

5The U.S. Energy Renaissance and the Pursuit of Energy Independence

DUFF & PHELPS INVESTMENT MANAGEMENT CO.’S OBSERVATIONS OF INDUSTRY TRENDS

Duff & Phelps believes we are still in the early innings of the energy investment cycle. The shale revolution and U.S. energy

renaissance are leading to significant infrastructure investment that is likely to continue for a decade or more. Recent investment

has been focused on achieving U.S. energy independence. Future investment will be driven by the U.S. becoming a major energy

exporter. MLPs are positioned to benefit from the need for expanded infrastructure.

> Sociopolitical and environmental issues in the rest of the world > Many MLPs have had very visible distribution growth that has

will continue to drive U.S. energy demand. been driven by both listed organic projects and acquisitions of

> U.S. shale formations have decades of reserves and many new general partner assets.

levels of shale to tap.

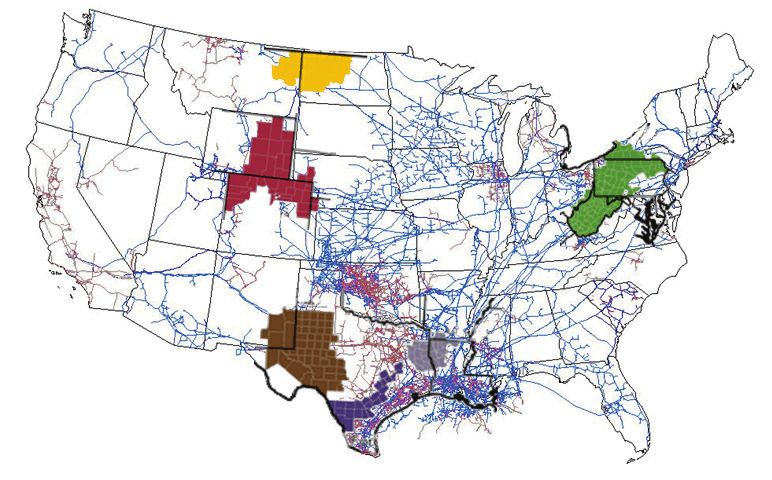

FUELING DOMESTIC PRODUCTION

>D

rilling efficiencies and advanced

technologies are fueling growing domestic

production of natural gas, crude oil, and

natural gas liquids.

> The U.S. is now the largest producer

of natural gas in the world, and the

global leader in crude oil production

capacity growth.

> Duff & Phelps believes ongoing oil and gas

production will continue to create logistics

opportunities for MLPs as producers look

Bakken

to move the oil and gas in new directions

Niobrara

across the U.S. Permian

> Meanwhile, it sees liquefied natural gas Eagle Ford

Haynesville

(LNG), liquefied petroleum gas (LPG), and Marcellus

ethane export facility development over Interstate Gas Pipelines

the next decade as providing an important Intrastate Gas Pipelines

release valve for supply bottlenecks in key

domestic shale plays.

Source: Energy Information Administration, Office of Oil & Gas, Natural Gas Division, Gas Transportation Information System.

CAPITAL SPENDING ESTIMATES REMAIN ATTRACTIVE

> New infrastructure demand points to the

$60,000 60 Large-Cap Pipeline Propane

potential for continued midstream pipeline Small-Cap Midstream Marine

and energy infrastructure growth.50,000 50

Oil Field Services Coal

40,000 40 Gathering & Processing Other

> Midstream MLPs spent a record $30 billion

$ billions

Upstream

in 2013 on logistics and infrastructure,

30,000 30

keeping pace with producer well

20,000 20

completions. This spending is expected to

increase even further in 2014. 10,000 10

> In a recent study, IHS estimates that a0 total 0

2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015E

of $890 billion will be spent on oil and

gas infrastructure over the next 12 years, Source: IHS “Oil & Natural Gas Transportation & Storage Infrastructure: Status, Trends, & Economic

Benefits” Report, December, 2013, for oil and gas infrastructure spending estimates from 2014-

with Duff & Phelps estimating roughly half 2015; Bloomberg Finance L.P. for MLP capital spending 2006-2015. It can be expected that some

being spent by energy MLPs. or all of the assumptions underlying any forward-looking estimates will not materialize or will vary

significantly from actual results or outcomes. Past performance is not indicative of future results.

Duff and Phelps’ observations of industry trends are the result of research conducted by the portfolio management/research team. These observations reflect their industry

expertise and have been prepared using sources of information generally believed to be reliable; however, their accuracy is not guaranteed. Opinions represented are

subject to change and should not be considered investment advice.

There is no assurance that any historical performance or trend illustrated will be repeated in the future. 3DSE Overview

Fund Investment Objective

Duff & Phelps Select Energy MLP Fund Inc. (DSE) is a newly organized, non-diversified closed-end management investment

company. The Fund will be treated as a “C” corporation for U.S. federal income tax purposes. The Fund’s investment

objective is to seek a high level of total return resulting from a combination of current tax-deferred distributions and capital

appreciation. We cannot assure you that the Fund will achieve its investment objective.

INVESTMENT APPROACH INVESTMENT PROCESS

> Apply a long-term strategic view to evaluate the energy sector > Fundamental, bottom-up approach focused on stock selection

and underlying sub-sectors of the energy MLP industry. relative to sub-sector peers.

> Examine supply and demand trends across the energy > Rigorous analysis of management track record, geographic

value chain. location, commodity exposure, distribution growth and

> Strive to minimize exposure to sectors with weak sustainability, valuation, and regulatory dynamics.

fundamentals. > Low turnover with a long-term investment horizon.

> Focus on trends in drilling productivity and rig count > Seeks to enhance the level of cash distributions to common

across multiple basins, and identify early application of stockholders through the use of leverage.*

new technologies.

ASSET ALLOCATION

> Investments focus on midstream services consisting of > No more than 20% of Managed Assets in securities of issuers

gathering, processing, transporting, producing, shipping, either: (i) in the energy sector that are not MLPs or (ii) that

and storing of natural gas, natural gas liquids, crude oil, and produce products that are primarily for the use of companies

refined products. in the energy sector.

> At least 80% of Managed Assets will be invested in energy MLPs. > Target 30% leverage* (based on Managed Assets) through

borrowings.

*The use of leverage involves risks. See “Leverage Risk” on page 8 of this brochure.

MODEL PORTFOLIO AS OF 4/30/14

> Actively managed initial model portfolio of MLP investments (approximately 25-35 holdings)

25.5% Gathering/Processing 8.5% Upstream

19.0% Diversified 8.5% Shipping

17.5% Petroleum Transportaon and Storage 4.5% Other

16.5% Natural Gas Pipelines

The model portfolio is a hypothetical example representing the views of Duff & Phelps on how the Fund would have been invested as of 4/30/14. Sub-sector

classification assignments based on internal methodology. Percentages may not equal 100% due to rounding. The Fund will be actively managed and its initial and

future portfolio may be different than the model portfolio.

Other

4 There is no assurance that any historical performance or trend illustrated will be repeated in the future.

ShippingExperienced and Proven Management

THE MLP CLOSED-END FUND ADVANTAGE

Using a closed-end fund to invest in MLPs presents a series of potential advantages for investors:

> Opportunity for attractive total returns with capital appreciation > Simplified tax reporting compared to direct MLP investments;

> Exposure to U.S. energy renaissance investors receive one Form 1099 at year-end; no K-1s

> Tax-deferred and tax-advantaged distributions > Maintains a stable pool of assets, which may alleviate the need

to hold cash or liquidate assets to meet redemption requests

> A portfolio of MLPs to assist in more complete diversification of

an overall investment portfolio > Qualified account eligible; no unrelated business income

tax (UBIT)

> Actively manage leverage to seek to enhance the level of cash

distributions to common stockholders

> Established manager of utility and infrastructure companies > Deep closed-end fund management experience, with

since 1979 with $9.9 billion in assets under management.1 $5.6 billion1 in closed-end assets under management including

> Wholly-owned subsidiary of Virtus Investment Partners, Inc., over $1 billion in MLP and MLP-related securities.3

a publicly-traded asset management firm with $58.0 billion in > Investment team includes three dedicated MLP investment

assets under management.2 professionals with average industry experience of more than

18 years.

1

As of 4/30/14.

2

As of 3/31/14.

3

MLPs and securities of entities holding primarily general partner or managing member interests in MLPs.

INVESTMENT TEAM Industry Experience INVESTMENT TEAM Industry Experience

David D. Grumhaus, Jr. Nathan I. Partain, CFA

21 years 33 years

Lead Portfolio Manager, Senior Vice President Utilities Team Head, President,

Director and Chief Investment Officer

Charles J. Georgas, CFA Deborah A. Jansen, CFA

26 years

Portfolio Manager, Senior MLP Analyst DPG Portfolio Manager, Senior Analyst, 33 years

Senior Vice President

Kyle West, CFA

8 years

MLP Analyst

Key Facts *The Fund’s stock price will fluctuate and, at the time of sale, shares of common

stock may be worth more or less than the original investment or the Fund’s then-

Offering Period: June 2014 current net asset value. The Fund cannot predict whether its shares of common

stock will trade at, above, or below net asset value. The net amount invested will

Offering Terms be reduced by a 4.5% sales load. Offering expenses (other than the sales load)

Initial Stock Price* $20.00 will be paid by the Fund up to $0.04 per common share. The Adviser will pay all

offering costs that exceed $0.04 per share.

Share Minimum 100

**The Fund expects to declare its initial common stock distribution approximately

Sales Load 4.5% 45 days after the completion of the offering and pay approximately 60 days after

Selling Concession 3.0% the completion of the offering, depending on market conditions. Thereafter,

distributions are expected to be declared quarterly depending on market

Lead Underwriter Morgan Stanley & Co. LLC conditions. Distributions from the Fund will generally be predominantly a return

Distributions** Quarterly of capital until an investor’s basis has been reduced to below zero, i.e., until the

value of an investor’s original investment has been returned.

Fees ***The Fund will pay an annual management fee in an amount equal to 1.00%

of the Fund’s Managed Assets (including leverage). Assuming the use of leverage

Management Fees*** 1.00% in an amount equal to 30% of the Fund’s Managed Assets at an interest rate of

Estimated Other Expenses 0.35% 0.96%, management fees and total annual expenses are estimated to be 1.43%

and 2.25% of the Fund’s net assets attributable to common shares, respectively.

Estimated Total Annual Expenses (before leverage) 1.35% Please refer to the “Summary of Fund Expenses” section of the preliminary

Actual “Other Expenses” may be higher or lower. prospectus for information on the fees, charges, and expenses associated with

investing in the Fund.

“Managed Assets” means net assets plus the amount of any borrowings and any

preferred stock that may be outstanding.

5Principal Risk Factors

An investment in the Fund’s Common Stock involves paid by the Fund will reduce the amount available to pay particular circumstances and performance of particular

various material risks. The following is a summary of distributions to Common Stockholders, and therefore companies whose securities the Fund holds. The price of

certain of these risks. It is not complete and you should investors in the Fund will likely receive lower distributions an equity security of an issuer may be particularly sensitive

read and consider carefully the more complete list of risks than if they invested directly in MLPs. to general movements in the stock market, and a drop in

described under “Risks” in the preliminary prospectus To the extent that the Fund invests in the equity securities the stock market may depress the price of most or all of the

before purchasing Common Stock in this offering. of an MLP, the Fund will be a partner in such MLP. equity securities held by the Fund. In addition, MLP units

No History of Operations. The Fund is a newly organized, Accordingly, the Fund will be required to include in its or other equity securities held by the Fund may decline in

non-diversified, closed-end management investment taxable income the Fund’s allocable share of the income, price if the issuer fails to make anticipated distributions

company with no history of operations or public trading. gains, losses, deductions and expenses recognized by each or dividend payments because, among other reasons, the

such MLP, regardless of whether the MLP distributes cash issuer experiences a decline in its financial condition.

Investment and Market Risk. An investment in the Fund is

subject to investment risk, including the possible loss of the to the Fund. Historically, MLPs have been able to offset a MLP subordinated units typically are convertible to MLP

entire amount that you invest. Your investment in Common significant portion of their income with tax deductions. common units at a one-to-one ratio. The price of MLP

Stock represents an indirect investment in MLPs and The Fund will incur a current tax liability on its allocable subordinated units is typically tied to the price of the

other securities owned by the Fund, most of which could share of an MLP’s income and gains that is not offset by corresponding MLP common unit, less a discount. The size

be purchased directly. The value of the Fund’s portfolio the MLP’s tax deductions, losses and credits, or its net of the discount depends upon a variety of factors, including

securities may move up or down, sometimes rapidly and operating loss carryforwards, if any. The portion, if any, the likelihood of conversion, the length of time remaining

unpredictably. At any point in time, your Common Stock of a distribution received by the Fund from an MLP that until conversion and the size of the block of subordinated

may be worth less than your original investment. is offset by the MLP’s tax deductions, losses or credits is units being purchased or sold.

essentially treated as a return of capital. However, those I-Shares represent an indirect investment in MLP I-units.

Risks of Investing in MLP Units. An investment in MLP distributions will reduce the Fund’s adjusted tax basis in

units involves risks that differ from a similar investment in Prices and volatilities of I-Shares tend to correlate to the

the equity securities of the MLP, which will result in an price of common units. Holders of I-Shares are subject

equity securities, such as common stock, of a corporation. increase in the amount of gain (or decrease in the amount

Holders of MLP units have the rights typically afforded to to the same risks as holders of MLP common units. In

of loss) that will be recognized by the Fund for United addition, I-Shares may trade less frequently, particularly

limited partners in a limited partnership. As compared States federal income tax purposes upon the sale of any

to common stockholders of a corporation, holders of those of issuers with smaller capitalizations. Given their

such equity securities or upon subsequent distributions potential for limited trading volume, I-Shares may display

MLP units have more limited control and limited rights in respect of such equity securities. The percentage of an

to vote on matters affecting the partnership. Holders of volatile or erratic price movements.

MLP’s income and gains that is offset by tax deductions,

MLP units are also exposed to the risk that they will be losses and credits will fluctuate over time for various Energy Sector Risks. MLPs and other entities operating

required to repay amounts to the MLP that are wrongfully reasons. A significant slowdown in acquisition activity or in the energy sector are subject to many operating

distributed to them. There are also certain tax risks capital spending by MLPs held in the Fund’s portfolio could risks, including: equipment failure causing outages;

associated with an investment in MLP units (described result in a reduction of accelerated depreciation generated structural, maintenance, impairment and safety problems;

further below). Additionally, conflicts of interest may by new acquisitions, which may result in increased current transmission or transportation constraints, inoperability

exist among common unit holders, subordinated unit tax liability for the Fund. or inefficiencies; dependence on a specified fuel source;

holders and the general partner or managing member of changes in electricity and fuel usage; availability of

an MLP; for example a conflict may arise as a result of The Fund will accrue deferred income taxes for its future competitively priced alternative energy sources; changes

incentive distribution payments. tax liability associated with the difference between the in generation efficiency and market heat rates; lack of

Fund’s tax basis in an MLP security and the fair market sufficient capital to maintain facilities; significant capital

Tax Risks of Investing in Equity Securities of MLPs. A value of the MLP security. Upon the Fund’s sale of an MLP

part of the benefit the Fund derives from its investment expenditures to keep older assets operating efficiently;

security, the Fund may be liable for previously deferred seasonality; changes in supply and demand for energy;

in equity securities of MLPs is a result of MLPs generally taxes. The Fund will rely to some extent on information

being treated as partnerships for United States federal catastrophic and/or weather-related events such as spills,

provided by MLPs, which may not necessarily be timely, to leaks, well blowouts, uncontrollable flows, ruptures, fires,

income tax purposes. Partnerships do not pay United estimate its deferred tax liability for purposes of financial

States federal income tax at the partnership level. explosions, floods, earthquakes, hurricanes, discharges

statement reporting and determining its net asset value. of toxic gases and similar occurrences; storage, handling,

Rather, each partner of a partnership, in computing its From time to time, the Fund will modify its estimates or

United States federal income tax liability, will include its disposal and decommissioning costs; and environmental

assumptions regarding its deferred tax liability as new compliance. Breakdown or failure of an energy company’s

allocable share of the partnership’s income, gains, losses, information becomes available.

deductions and expenses. A change in current tax law, a assets may prevent it from performing under applicable

change in the business of a given MLP or a change in the Because of the Fund’s status as a corporation for United sales agreements, which in certain situations, could result

types of income earned by a given MLP could result in States federal income tax purposes (as opposed to in termination of the agreement or incurring a liability

an MLP being treated as a corporation for United States a partnership or other pass-through entity) and its for liquidated damages. As a result of the above risks and

federal income tax purposes, which would result in such investments in equity securities of MLPs, the Fund’s other potential hazards associated with energy companies,

MLP being required to pay United States federal income earnings and profits may be calculated using accounting certain companies may become exposed to significant

tax on its taxable income. The classification of an MLP methods that are different from those used for calculating liabilities for which they may not have adequate insurance

as a corporation for United States federal income tax taxable income. Because of these differences, the Fund coverage. Any of the aforementioned risks could have a

purposes would have the effect of reducing the amount may make distributions out of its current or accumulated material adverse effect on the business, financial condition,

of cash available for distribution by the MLP and causing earnings and profits, which will be treated as dividends, results of operations and cash flows of energy companies.

any such distributions received by the Fund to be taxed in excess of its taxable income. See “Certain United States Because the Fund will invest at least 80% of its Managed

as dividend income to the extent of the MLP’s current Federal Income Tax Considerations” in the preliminary Assets in energy MLPs, concentration in the energy sector

or accumulated earnings and profits. Thus, if any of the prospectus. may present more risks than if the Fund were broadly

MLPs owned by the Fund were treated as corporations In addition, changes in tax laws or regulations, or future diversified over numerous sectors of the economy. A

for United States federal income tax purposes, the value interpretations of such laws or regulations, could adversely downturn in the energy sector of the economy, adverse

and after-tax return to the Fund with respect to its affect the Fund or the MLP investments in which the Fund political, legislative or regulatory developments or other

investment in such MLPs would be materially reduced, invests. In particular, certain recent proposals have called events could have a larger impact on the Fund than on

which could cause a substantial decline in the value of for the elimination of tax incentives widely used by oil, an investment company that does not concentrate in

the Common Stock. gas and coal companies and the imposition of new fees the sector. At times, the performance of securities of

In addition, the potential tax benefit to the Fund of on certain energy producers. The elimination of such tax companies in the energy sector may lag the performance

investing in MLPs will depend in part on the particular incentives and imposition of such fees could materially of other sectors or the broader market as a whole. In

MLP securities selected, and whether any distributions adversely affect MLPs in which the Fund invests and the addition, there are several specific risks associated with

paid by such MLPs will be treated as a return of capital energy sector generally. investments in the energy sector, including the following.

(as opposed to currently taxable income). Generally, Duff Lack of Diversification of MLP Customers and Suppliers. Commodity Price Risk. MLPs and other entities operating

& Phelps Investment Management Co. (“DPIM”) will Certain MLPs in which the Fund may invest depend upon in the energy sector may be affected by fluctuations

seek to select MLP securities that provide distributions in a limited number of customers for substantially all of in the prices of energy commodities, including, for

excess of allocable taxable income. If DPIM fails to do so, their revenue. Similarly, certain MLPs in which the Fund example, natural gas, natural gas liquids, crude oil and

a greater portion of the distributions received by the Fund may invest depend upon a limited number of suppliers coal, in the short- and long-term. Fluctuations in energy

may be comprised of taxable income (which would reduce of goods or services to continue their operations. The commodity prices would directly impact companies

the ability of the Fund to make distributions to Common loss of any such customers or suppliers could materially that own such energy commodities and could indirectly

Stockholders that are treated as a return of capital for adversely affect such MLPs’ results of operations and impact companies that engage in transportation, storage,

United States federal income tax purposes). In such case, cash flow, and their ability to make distributions to unit processing, distribution or marketing of such energy

the Fund may have a larger corporate income tax expense, holders, such as the Fund, would therefore be materially commodities. Fluctuations in energy commodity prices

which would result in less cash available to distribute to adversely affected. can result from changes in general economic conditions

Common Stockholders. Also, in connection with managing Equity Securities Risk. A substantial percentage of or political circumstances (especially of key energy

the Fund’s portfolio in order to seek to maximize the the Fund’s assets will be invested in equity securities, producing and consuming countries); market conditions;

potential tax benefits discussed above, DPIM may consider including MLP common units, MLP subordinated units, weather patterns; domestic production levels; volume

selling securities at times or prices that may otherwise be MLP preferred units, equity securities of MLP affiliates, of imports; energy conservation; domestic and foreign

disadvantageous to the Fund. including I-Shares, and common stocks of other issuers. governmental regulation; international politics; policies

The Fund will be treated as a regular corporation, or Equity risk is the risk that the value of MLP units or other of the Organization of Petroleum Exporting Countries

a “C” corporation, for United States federal income equity securities held by the Fund will fall due to general (“OPEC”); taxation; tariffs; and the availability and costs

tax purposes and, as a result, unlike most investment market or economic conditions, perceptions regarding of local, intrastate and interstate transportation methods.

companies, is subject to corporate income tax to the the industries in which the issuers of securities held by The energy sector as a whole may also be impacted by

extent the Fund recognizes taxable income. Any taxes the Fund participate, changes in interest rates, and the the perception that the performance of energy sector

6Principal Risk Factors

companies is directly linked to commodity prices. High could significantly increase the compliance costs of MLPs. properties are subject to royalty interests, liens and other

commodity prices may drive further energy conservation For example, hydraulic fracturing, a technique used in burdens, encumbrances, easements or restrictions, all of

efforts, and a slowing economy may adversely impact the completion of certain oil and gas wells, has become a which could impact the production of a particular MLP. Oil

energy consumption, which may adversely affect the subject of increasing regulatory scrutiny and may be subject and gas MLPs operate in a highly competitive and cyclical

performance of MLPs and other companies operating in in the future to more stringent, and more costly to comply industry, with intense price competition. A significant

the energy sector. Recent economic and market events with, requirements. Similarly, the implementation of more portion of their revenues may depend on a relatively

have fueled concerns regarding potential liquidations of stringent environmental requirements could significantly small number of customers, including governmental

options positions. increase the cost of any remediation that may become entities and utilities.

Depletion Risk. MLPs and other entities engaged in the necessary. MLPs may not be able to recover these costs Catastrophic Event Risk. MLPs and other entities operating

exploration, development, management or production of from insurance. in the energy sector are subject to many dangers inherent in

energy commodities face the risk that commodity reserves Voluntary initiatives and mandatory controls have been the production, exploration, management, transportation,

are depleted over time. Such companies seek to increase adopted or are being discussed both in the United States processing and distribution of natural gas, natural gas

their reserves through expansion of their current businesses, and worldwide to reduce emissions of “greenhouse gases” liquids, crude oil, refined petroleum and petroleum

acquisitions, further development of their existing sources such as carbon dioxide, a by-product of burning fossil products and other hydrocarbons. These dangers include

of energy commodities, exploration of new sources of fuels, and methane, the major constituent of natural leaks, fires, explosions, damage to facilities and equipment

energy commodities or by entering into long-term contracts gas, which many scientists and policymakers believe resulting from natural disasters, inadvertent damage

for additional reserves; however, there are risks associated contribute to global climate change. These measures and to facilities and equipment and terrorist acts. Since the

with each of these potential strategies. If such companies future measures could result in increased costs to certain September 11th terrorist attacks, the U.S. government

fail to acquire additional reserves in a cost-effective manner companies in which the Fund may invest to operate has issued warnings that energy assets, specifically U.S.

and at a rate at least equal to the rate at which their existing and maintain facilities and administer and manage a pipeline infrastructure, may be targeted in future terrorist

reserves decline, their financial performance may suffer. greenhouse gas emissions program, and may reduce attacks. These dangers give rise to risks of substantial

Additionally, failure to replenish reserves could reduce demand for fuels that generate greenhouse gases and that losses as a result of loss or destruction of commodity

the amount and affect the tax characterization of the are managed or produced by companies in which the Fund reserves; damage to or destruction of property, facilities

distributions paid by such companies. may invest. and equipment; pollution and environmental damage;

Regulatory Risk. The energy sector is highly regulated. MLPs In the wake of a Supreme Court decision holding that the and personal injury or loss of life. Any occurrence of

and other entities operating in the energy sector are subject Environmental Protection Agency (“EPA”) has some legal such catastrophic events could bring about a limitation,

to significant regulation of nearly every aspect of their authority to deal with climate change under the Clean suspension or discontinuation of the operations of MLPs

operations by federal, state and local governmental agencies. Air Act, the EPA and the Department of Transportation and other entities operating in the energy sector. MLPs

Such regulation can change rapidly or over time in both scope jointly wrote regulations to cut gasoline use and control and other entities operating in the energy sector may not

and intensity. For example, a particular by-product or process greenhouse gas emissions from cars and trucks. The EPA be fully insured against all risks inherent in their business

may be declared hazardous (sometimes retroactively) by has also taken action to require certain entities to measure operations and therefore accidents and catastrophic

a regulatory agency, which could unexpectedly increase and report greenhouse gas emissions, and certain facilities events could adversely affect such companies’ financial

production costs. Various governmental authorities have may be required to control emissions of greenhouse condition and ability to pay distributions to shareholders.

the power to enforce compliance with these regulations and gases pursuant to EPA air permitting and other regulatory Industry Specific Risks. MLPs and other entities operating

the permits issued under them, and violators are subject programs. These measures, and other programs addressing in the energy sector are also subject to risks that are

to administrative, civil and criminal penalties, including greenhouse gas emissions, could reduce demand for specific to the industry they serve.

civil fines, injunctions or both. Stricter laws, regulations or energy or raise prices, which may adversely affect the total Pipelines. Pipeline companies are subject to the demand

enforcement policies could be enacted in the future which return of certain of the Fund’s investments. for natural gas, natural gas liquids, crude oil or refined

would likely increase compliance costs and may adversely Acquisition Risk. MLP investments owned by the Fund products in the markets they serve, changes in the

affect the financial performance of MLPs. may depend on MLPs’ ability to make acquisitions that availability of products for gathering, transportation,

Specifically, the operations of wells, gathering systems, increase adjusted operating surplus per unit in order to processing or sale due to natural declines in reserves and

pipelines, refineries and other facilities are subject to increase distributions to unit holders. The ability of such production in the supply areas serviced by the companies’

stringent and complex federal, state and local environmental MLPs to make future acquisitions is dependent on their facilities; sharp decreases in crude oil or natural gas

laws and regulations. These include, for example: ability to identify suitable targets, negotiate favorable prices that cause producers to curtail production or

• the federal Clean Air Act and comparable state laws purchase contracts, obtain acceptable financing and reduce capital spending for exploration activities; and

and regulations that impose obligations related to air outbid competing potential acquirers. To the extent environmental regulation. Demand for gasoline, which

emissions; that such MLPs are unable to make future acquisitions, accounts for a substantial portion of refined product

or such future acquisitions fail to increase the adjusted transportation, depends on price, prevailing economic

• the federal Clean Water Act and comparable state laws operating surplus per unit, their growth and ability conditions in the markets served, and demographic

and regulations that impose obligations related to to make distributions to unit holders will be limited. and seasonal factors. Companies that own interstate

discharges of pollutants into regulated bodies of water; There are risks inherent in any acquisition, including pipelines that transport natural gas, natural gas liquids,

• the federal Resource Conservation and Recovery Act erroneous assumptions regarding revenues, acquisition crude oil or refined petroleum products are subject to

(“RCRA”) and comparable state laws and regulations that expenses, operating expenses, cost savings and synergies; regulation by the Federal Energy Regulatory Commission

impose requirements for the handling and disposal of assumption of liabilities; indemnification; customer losses; (“FERC”) with respect to the tariff rates they may charge

waste from facilities; and key employee defections; distraction from other business for transportation services. An adverse determination by

• the federal Comprehensive Environmental Response, operations; and unanticipated difficulties in operating or FERC with respect to the tariff rates of such companies

Compensation and Liability Act of 1980 (“CERCLA”), integrating new product areas and geographic regions. could have a material adverse effect on their business,

also known as “Superfund,” and comparable state laws Weather Risks. Weather plays a role in the seasonality financial condition, results of operations and cash flows

and regulations that regulate the cleanup of hazardous of some MLPs’ cash flows. MLPs in the propane industry, and their ability to pay cash distributions or dividends. In

substances that may have been released at properties for example, rely on the winter season to generate addition, FERC has a tax allowance policy, which permits

currently or previously owned or operated by MLPs or almost all of their earnings. In an unusually warm winter such companies to include in their cost of service an

at locations to which they have sent waste for disposal. season, propane MLPs experience decreased demand income tax allowance to the extent that their owners have

Failure to comply with these laws and regulations may for their product. Although most MLPs can reasonably an actual or potential tax liability on the income generated

trigger a variety of administrative, civil and criminal predict seasonal weather demand based on normal by them. If FERC’s income tax allowance policy were to

enforcement measures, including the assessment weather patterns, extreme weather conditions, such as change in the future to disallow a material portion of the

of monetary penalties, the imposition of remedial the hurricanes that severely damaged cities along the U.S. income tax allowance taken by such interstate pipeline

requirements, and the issuance of orders enjoining future Gulf Coast in recent years, demonstrate that no amount of companies, it would adversely impact the maximum tariff

operations. Certain environmental statutes, including preparation can protect an MLP from the unpredictability rates that such companies are permitted to charge for

RCRA, CERCLA, the federal Oil Pollution Act and analogous of the weather or possible climate change. Further, it their transportation services, which in turn could adversely

state laws and regulations, impose strict, joint and several is possible that future climate change could result in affect such companies’ financial condition and ability to

liability for costs required to clean up and restore sites increases in the frequency and severity of adverse weather pay distributions to shareholders.

where hazardous substances have been disposed of or events. The damage done by extreme weather also may Gathering and processing. Gathering and processing

otherwise released. Moreover, it is not uncommon for serve to increase many MLPs’ insurance premiums and companies are subject to natural declines in the

neighboring landowners and other third parties to file could adversely affect such companies’ financial condition production of oil and natural gas fields, which utilize their

claims for personal injury and property damage allegedly and ability to pay distributions to shareholders. gathering and processing facilities as a way to market their

caused by the release of hazardous substances or other Cyclical Industry Risk. The energy industry is cyclical and production; prolonged declines in the price of natural gas

waste products into the environment. from time to time may experience a shortage of drilling or crude oil, which curtails drilling activity and therefore

There is an inherent risk that MLPs and other entities rigs, equipment, supplies, or qualified personnel, or due production; and declines in the prices of natural gas

operating in the energy sector may incur environmental to significant demand, such services may not be available liquids and refined petroleum products, which cause

costs and liabilities due to the nature of their businesses on commercially reasonable terms. An MLP’s ability to lower processing margins. In addition, some gathering and

and the substances they handle. For example, an accidental successfully and timely complete capital improvements processing contracts subject the gathering or processing

release from wells or gathering pipelines could subject them to existing or other capital projects is contingent upon company to direct commodities price risk.

to substantial liabilities for environmental cleanup and many variables. Should any such efforts be unsuccessful, Exploration and production. Exploration, development

restoration costs, claims made by neighboring landowners an MLP could be subject to additional costs and/or the and production companies are particularly vulnerable to

and other third parties for personal injury and property write-off of its investment in the project or improvement. declines in the demand for and prices of crude oil and

damage, and fines or penalties for related violations of The marketability of oil and gas production depends in natural gas. Reductions in prices for crude oil and natural

environmental laws or regulations. Moreover, the possibility large part on the availability, proximity and capacity gas can cause a given reservoir to become uneconomic for

exists that stricter laws, regulations or enforcement policies of pipeline systems owned by third parties. Oil and gas continued production earlier than it would if prices were

7Principal Risk Factors

higher, resulting in the plugging and abandonment of, and and 50% of the Fund’s total assets through the issuance of INDEXES

cessation of production from, that reservoir. In addition, Preferred Stock. Leverage may result in greater volatility Indexes are unmanaged, do not reflect the deduction of fees

lower commodity prices not only reduce revenues but of the net asset value, distributions on the Common Stock or expenses, and are not available for direct investment.

also can result in substantial downward adjustments in and market price of the Common Stock because changes Each index discussed below is comprised of different

reserve estimates. The accuracy of any reserve estimate in the value of the Fund’s portfolio investments, including securities and asset classes. Different types of securities

is a function of the quality of available data, the accuracy investments purchased with the proceeds from borrowings and asset classes have different characteristics, including

of assumptions regarding future commodity prices and or the issuance of Preferred Stock, if any, are borne entirely with respect to guarantees, fluctuation of principal and/

future exploration and development costs and engineering by Common Stockholders. Common Stock income may or return, and tax features. For example, the U.S. Treasury

and geological interpretations and judgments. Different fall if the interest rate on borrowings or the dividend rate indexes are comprised of securities that are issued by and

reserve engineers may make different estimates of reserve on Preferred Stock rises, and may fluctuate as the interest guaranteed by the U.S. federal government as to principal

quantities and related revenue based on the same data. rate on borrowings or the dividend rate on Preferred Stock and interest payments. These types of securities are less

Actual oil and gas prices, development expenditures varies. So long as the Fund is able to realize a higher net risky than the debt and equity securities, including MLPs,

and operating expenses will vary from those assumed in return on its investment portfolio than the then-current cost that make up the other indexes below. The performance of

reserve estimates, and these variances may be significant. of any leverage together with other related expenses, the the Fund will differ, and may vary materially, from that of

Any significant variance from the assumptions used could effect of the leverage will be to cause Common Stockholders any index. In particular, because the Fund will be treated as

result in the actual quantity of reserves and future net cash to realize higher current net investment income than if the a regular corporation for U.S. federal income tax purposes,

flow being materially different from those estimated in Fund were not so leveraged. On the other hand, the Fund’s it will be subject to corporate income tax to the extent the

reserve reports. In addition, results of drilling, testing and use of leverage will result in increased operating costs. Thus, Fund recognizes taxable income, which the indexes below

production and changes in prices after the date of reserve to the extent that the then-current cost of any leverage, are not subject to.

estimates may result in downward revisions to such together with other related expenses, approaches the net

estimates. Substantial downward adjustments in reserve return on the Fund’s investment portfolio, the benefit of Alerian MLP Index: A composite of the 50 most prominent

estimates could have a material adverse effect on a given leverage to Common Stockholders will be reduced, and if energy master limited partnerships (MLPs) that provides

exploration and production company’s financial position the then-current cost of any leverage together with related investors with an unbiased, comprehensive benchmark

and results of operations. In addition, due to natural expenses were to exceed the net return on the Fund’s for this emerging asset class. The index, which is

declines in reserves and production, exploration and portfolio, the Fund’s leveraged capital structure would result calculated using a float-adjusted, capitalization-weighted

production companies must economically find or acquire in a lower rate of return to Common Stockholders than if the methodology, is disseminated real-time on a price-return

and develop additional reserves in order to maintain and Fund were not so leveraged. There can be no assurance that basis (NYSE: AMZ) and on a total-return basis (NYSE:

grow their revenues and distributions. the Fund’s leveraging strategy will be successful. AMZX).

Propane. Propane MLPs are subject to earnings variability During periods when the Fund is using leverage through The Barclays U.S. Corporate High-Yield 2% Issuer Capped

based upon weather conditions in the markets they serve, borrowings or the issuance of Preferred Stock, the fees Index: An issuer-constrained version of the U.S. Corporate

fluctuating commodity prices, increased use of alternative paid to the Fund’s manager and sub-adviser for advisory High-Yield Index that measures the market of USD-

fuels, increased governmental or environmental regulation, services will be higher than if the Fund did not use leverage denominated, non-investment grade, fixed-rate, taxable

and accidents or catastrophic events, among others. because the fees paid will be calculated on the basis of the corporate bonds.

Coal. MLP entities and other entities with coal assets are Fund’s Managed Assets, which includes the amount of MSCI World Index: A free float-adjusted market

subject to supply and demand fluctuations in the markets borrowings and any assets attributable to Preferred Stock. capitalization-weighted index that is designed to measure

they serve, which may be impacted by a wide range of This means that the Fund’s manager and sub-adviser have the equity market performance of developed markets.

factors including fluctuating commodity prices, the level a financial incentive to increase the Fund’s use of leverage. S&P 500® Index: A free-float capitalization-weighted index

of their customers’ coal stockpiles, weather, increased Any decline in the net asset value of the Fund will be of 500 of the largest U.S. stocks, generally representative

conservation or use of alternative fuel sources, increased borne entirely by Common Stockholders. Therefore, if the of the performance of larger companies in the U.S.

governmental or environmental regulation, depletion, market value of the Fund’s portfolio declines, the Fund’s The S&P 500® Utilities Index: Comprises those companies

rising interest rates, declines in domestic or foreign use of leverage will result in a greater decrease in net asset included in the S&P 500 that are classified as members of

production, mining accidents or catastrophic events, value to Common Stockholders than if the Fund were not the GICS® utilities sector

health claims, and economic conditions, among others. It leveraged. Such greater net asset value decrease will also The MSCI U.S. REIT Index: A free float-adjusted market

has become increasingly difficult to obtain and maintain tend to cause a greater decline in the market price for the capitalization weighted index that is comprised of equity

the permits necessary to mine coal. Further, such permits, Common Stock. REITs that are included in the MSCI US Investable Market

if obtained, have increasingly contained more stringent, Certain types of borrowings may result in the Fund being 2500 Index, with the exception of specialty equity REITs

and more difficult and costly to comply with, provisions subject to covenants in credit agreements relating to asset that do not generate a majority of their revenue and

relating to environmental protection. coverage or portfolio composition or otherwise. In addition, income from real estate rental and leasing operations.

Marine shipping. Marine shipping (or “tanker”) companies the Fund may be subject to certain restrictions imposed by The index represents approximately 85% of the US REIT

are exposed to many of the same risks as other energy guidelines of one or more rating agencies which may issue universe.

companies. In addition, the highly cyclical nature of the ratings for commercial paper, notes or Preferred Stock The S&P GSCI® All Crude Index: A sub-index of the S&P

tanker industry may lead to volatile changes in charter issued by the Fund. Such restrictions may be more stringent GSCI, provides investors with a reliable and publicly

rates and vessel values, which may adversely affect the than those imposed by the 1940 Act. In addition, the terms available benchmark for investment performance in the

earnings of tanker companies. Fluctuations in charter rates of the credit agreements may also require that the Fund crude oil commodity market.

and vessel values result from changes in the supply and pledge some or all of its assets as collateral.

demand for tanker capacity and changes in the supply and These indexes are unmanaged and not available for direct

demand for oil and oil products. Historically, the tanker The Fund may also be subject to the following categories investment.

markets have been volatile because many conditions of risk: Delay in Use of Proceeds Risk, Interest Rate Risk, “Alerian MLP Index,” “Alerian MLP Total Return Index,”

and factors can affect the supply and demand for tanker Inflation/Deflation Risk, Affiliated Party Risk, Competition “AMZ,” and “AMZX” are trademarks of Alerian and their

capacity. Changes in demand for transportation of oil over Risk, Restricted Securities Risk, Capital Markets Risk, use is granted under a license from Alerian. All indexes,

longer distances and supply of tankers to carry that oil may Deferred Taxation Risk, Royalty Trust Risk, Debt Securities trademarks and copyrights are the property of their

materially affect revenues, profitability and cash flows of Risk, Below Investment Grade (High Yield or Junk Bond) respective owners.

tanker companies. The successful operation of vessels in Securities Risk, Foreign Securities and Emerging Markets

the charter market depends upon, among other things, Risk, Currency Risk, Supply and Demand Risk, Derivatives

Risk, Securities Lending Risk, Management Risk and

obtaining profitable spot charters and minimizing time

spent waiting for charters and traveling unladen to pick up Reliance on Key Personnel, Market Price Discount from

Net Asset Value Risk, Portfolio Turnover Risk, Government

For more information,

cargo. The value of tanker vessels may fluctuate and could

adversely affect the value of tanker company securities. Intervention in Financial Markets Risk, Market Disruption

and Geopolitical Risk, Temporary Defensive Strategies

please contact us at

Declining tanker values could affect the ability of tanker

companies to raise cash by limiting their ability to refinance

their vessels, thereby adversely impacting tanker company

Risk, Non-Diversification Risk, Liquidity Risk, Cash Flow

Risk, Small Capitalization Risk, Valuation Risk, Potential 1.800.243.4361

liquidity. Tanker company vessels are at risk of damage or

loss because of events such as mechanical failure, collision,

Conflicts of Interest Risk, Anti-Takeover Provisions, Short

Sales Risk, Legal and Regulatory Risk, Counterparty Risk, or visit

and Privately Held Company Risk. For a complete listing

human error, war, terrorism, piracy, cargo loss and bad

weather. In addition, changing economic, regulatory and of all the Fund’s risks with their full descriptions, please www.Virtus.com/DSE

political conditions in some countries, including political refer to the Fund’s preliminary prospectus.

and military conflicts, have from time to time resulted in

attacks on vessels, mining of waterways, piracy, terrorism,

labor strikes, boycotts and government requisitioning of

vessels. These sorts of events could interfere with shipping

lanes and result in market disruptions and a significant loss

of tanker company earnings.

Leverage Risk. Under current market conditions, the Fund

generally intends to utilize leverage in an amount equal

to approximately 30% of its Managed Assets principally

through borrowings from certain financial institutions. In the

future, the Fund may elect to utilize leverage in an amount

up to 331/3% of the Fund’s total assets through borrowings

6686 (5/14) 8You can also read