Electricity Prices & Competition - CER Presentation on - SEAI Conference, July 2010

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CER Presentation on

Electricity Prices &

Competition

SEAI Conference, July 2010

Agenda • Who is the CER and what are our functions? • What are the electricity price drivers? • Recent fuel price trends and SEM prices • Market contracts • End-user retail prices • Retail market price deregulation

Who is the CER? • CER is Ireland‟s independent energy regulator • CER regulates Ireland‟s natural gas and electricity markets in the interests of customers • CER‟s role is to ensure a safe, secure and competitive supply of natural gas and electricity to customers

Who is the CER? • CER is led by 3 Commissioners: – Michael G. Tutty, Chairman – Dermot Nolan, Commissioner – Garrett Blaney, Commissioner • Full details of the CER‟s role at www.cer.ie & www.allislandproject.org

What are our functions? • Regulate the wholesale market with NI - Single Electricity Market (SEM) • Regulate energy networks - set access terms and prices • Regulate end prices - electricity “Roadmap” • Licence and monitor market players • Customer protection and complaints resolution • On-shore and new upstream safety functions

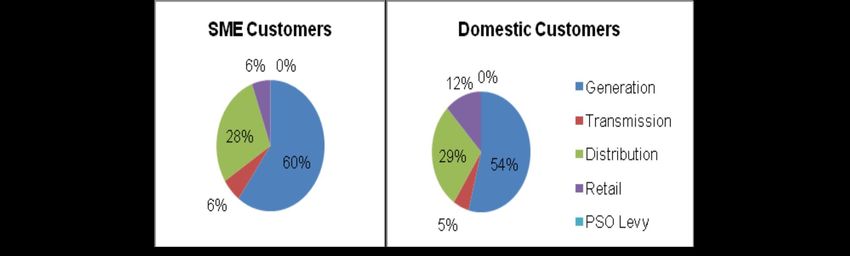

Electricity Price Drivers • Generation is single biggest price driver: over half of a typical customer‟s bill • Networks is 2nd biggest driver: about 1/3 of a customer‟s bill; less for LEUs

Electricity Price Drivers • Over 80% of our generation comes from fossil fuels, with gas the dominant fuel => international fuel price, especially gas, is the key driver of generation costs and therefore Irish electricity prices - much more than in most EU countries

Electricity Price Drivers Gross Electricity Generation % from Fossil Fuels, Eurozone

Electricity Price Drivers

• Generation:

– Main reason why elec prices in Irl are higher than in many European

countries is our fossil fuel dependence - & also why end-prices are lower

than last year

– Fossil fuel prices tend to be volatile: peak in „08 followed by fall followed

by recent rise!

• Networks:

– Capex and low population densities are the cost drivers

– CER published “PR3” proposals last week, with a slight cut in average

network tariffs overall this October

• PSO:

– Govt. scheme, administered by CER, to support primarily wind & peat;

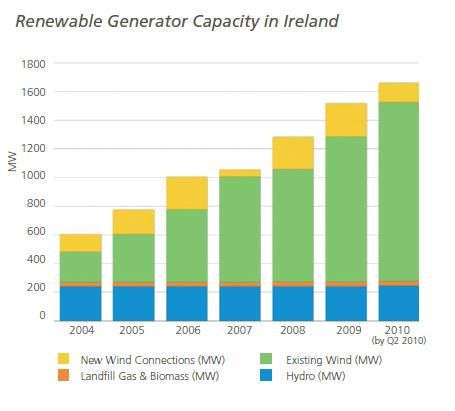

cost estimated as €195m for next tariff yearElectricity Price Drivers • Providing a hedge, renewables are increasing - currently 15% of consumption

Fuel Prices since July „08 Source: Bloomberg

Gas Prices & the SEM • Natural gas accounts for c. 60% of generation and is the prime driver of the SEM wholesale price - the SMP Source: Bloomberg

Carbon • Full cost of carbon emitted is included in the cost of electricity • Due to fuel mix, we pay the cost of carbon on most of our electricity • 2010 carbon spot price has increased as per graph • Gens receive certain number of free carbon credits - Govt. has introduced a carbon levy to recover windfall gain, with intention to pass this on to LEUs • To be administered by CER

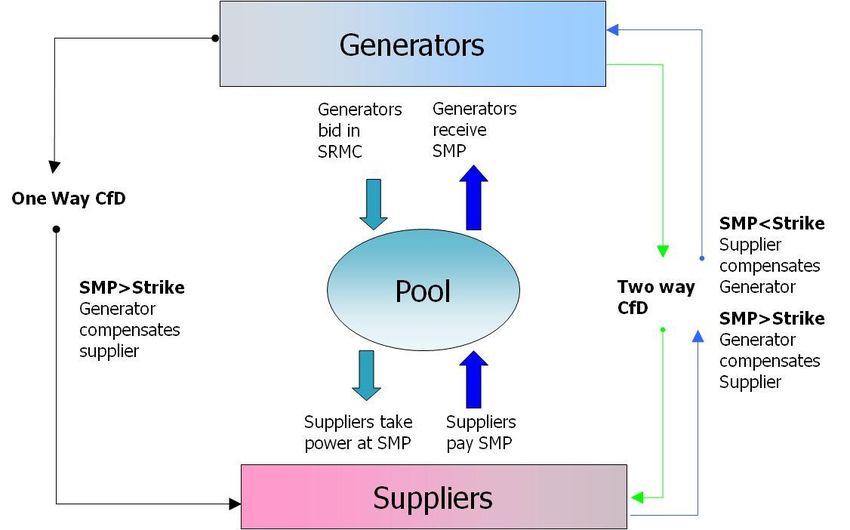

Financial Contracts (1)

Financial Contracts (2) • Directed Contract Prices (€/MWh)

Financial Contracts (3)

• Non-Directed Contracts (NDCs):

– All Financial Contracts other than DCs

– Predominantly sold by ESB PG and NIE PPB to date

– Also PSO-Related Contracts, with reserve price set by RAs

– All sold as 2-way CfDs to date

– Multilateral Trading Facility with competitive auctions

• More flexibility encouraged by RAs:

– Contracts being offered throughout the year, with monthly

contracts being offered for first time: see AIP website

• 2010/11 Tariff Year: higher prices than DCs due to rising fuel

prices; fuel prices putting upward pressure on end-pricesLEU Prices

Electricity & Gas Prices in Ireland

2nd Semester, July - December 2009

• Irish electricity prices remain above the European average, but

moved closer to the average for most consumers

• Prices for business fell for all levels of consumption, ranging

from:

– 5% drop for small business (band IA)

– to a 10% drop for the largest consumers (band IF)

• Medium to large business (bands ID to IF):

– 4% to 6% above the EU average, down from 10% to 13%

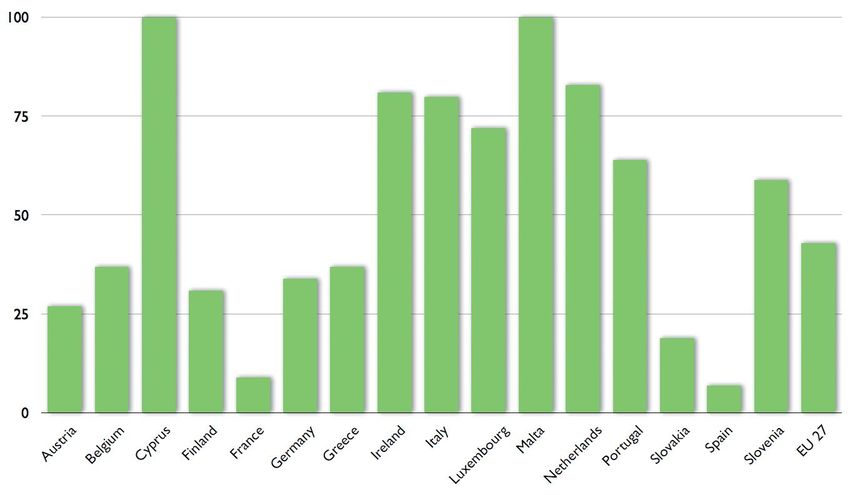

above in the previous semesterLEU Prices - Ireland & EU

Irish Business Electricity Prices Compared to EU 27 - all taxes

included

Based on data from SEAI report on Electricity & Gas Prices in Ireland – May 2010LEU Customer Credits

• 2010/11 Tariff Year:

– Continuation of LEU customer credits

• Financed by alternative means

• At a reduced level, to be phased out further in

2011/12

– Rebalancing of networks charges

• LEU‟s networks charges reduced by €50m per annum

• Permanent measure

– PSO

• LEU Contribution - €36mRetail Market

Deregulation

Big changes in the market place:

• Increased competition in generation & supply in recent years

• Entry of BGES and Airtricity to the domestic market

CER Roadmap consultation paper published Dec ‟09:

• Consulting on the circumstances under which the price control should

be removed from ESB CS

CER Roadmap decision paper published April „10:

• Decided on criteria under which the price controls will be removed

• CER competition review found high level of competition in LEU & all

business markets: to be price de-regulated in October.

• Domestics also seen very high switching rates: if this continues and

ESB re-branding takes place, de-regulation expected next yearDeregulation

LEU Sector

LEU Market Share (Customers) - Q4 2009 LEU Market Share (GWh) - Q4 2009

Criteria for deregulation of LEU market sector

- More than two active suppliers in the market

- Two of which have a consumption market share of 10% or more

- The combined market share (GWh) of ESBIE & ESB PES is 50%.Deregulation

- Next Steps

Competition Reviews:

• Forward looking view of market share, switching rate etc.

• Forecast Deregulation Decision, one month ahead of go-live

• Next review to be published in July

ESB Rebranding - additional requirement for the domestic

price de-regulation

Market Monitoring bi-annual publication to include:

• Number of suppliers

• Market Share (GWhs) for all suppliers

• Switching – total level of switches and switching between competitors

• Revenue – revenue earned for all suppliers to determine profitability

• Range of tariffs on offer and average prices paid by customers by tariffConsumer Survey

Published by CER and the UR on 14th June:

– Research conducted by the Research Perspective

– Covered consumer attitudes to, and awareness of, electricity

supply competition and associated issues

Key Findings For LEU Customers:

– 92% of LEU switchers found the process very easy or easy

– 86% saw their electricity bills reduced as expected;

– Cost of electricity is a significant business challenge for LEUs

– LEUs are interested in more frequent price revisions, and

would consider switching to suppliers who could provide

additional information on usage or dual fuel offeringsConsumer Survey: LEUs

Switching Data

Total Market Switches LEU Switches

200000 160

180000

140

160000

120

140000

100

120000

100000 80

80000 60

60000

40

40000

20

20000

0 0

Q1 Q2 Q3 Q4 Q1 Q2 Q1 Q2 Q3 Q4 Q1 Q2

2009 2009 2009 2009 2010 2010 2009 2009 2009 2009 2010 2010

Total Market switches in 2009 = 454,956 Total LEU switches in 2009 = 267 or 17%Questions and Answers

You can also read