European Business Administraion - UNYP eLearning

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

European Business Administraion

How does technology impact human workforce in banking?

The influence of automatization on labor market,

requalification and professional development within the

banking sector.

By

Marco Flaugnatti

2018 Mentor: Michael Williams

Statement of originality

I, Marco Flaugnatti declare that this submitted thesis including all used material is performed

by myself. The only guidance was provided by mentor, Michael Williams. Any research done

by others within the thesis is sourced in the reference list. I also confirm that this thesis was

not previously submitted as final degree project or in similar form at any other university.

Marco Flaugnatti, December 7, 2018

1

Acknowledgements

I chose my topic due to positive interest regarding finance, particularly banking industry

combined with the actual worldwide phenomena, technology.

Moreover I would like to thank to my mentor Mr. Michael Williams, who guided me through

all thesis and Dr. Neal Harold, who advised me about formatting and sources research.

Important piece of this thesis belong to Mgr. Henrieta Makovicová, who gladly answered my

questionnaire, guided me through banking environment and explained chronological changes.

The second interviewed person was Matúš Gedaj, the financial advisor in Partners Group.

2

Literature review

The future predictions are, according to most sources, negative, however we do not see the

reflection in unemployment rates.

Anderson (2017) in his publication called: THE INTRODUCTORY GUIDE TO

CRYPTOCURRENCIES offers explanations and the characteristics of virtual currencies,

which gain popularity.

Arjunwadkar (2018) in his publication named: Fintech have described the chronological

development of technology implementation in finance and banking. Each important

invention, which changed the banking procedures was widely presented. Moreover the author

also examined and evaluated the role of Fintech revolution, since the beginning and new

related startups.

Bennett (2017) published a book named: A guide to understanding blockchain, offers a guide

to blockchain, including the historical development. The author provides a deep analysis of

the blockchain technology development since the beginning. Analysis are supported by detail

explanation about the basis of blockchain technology.

King (2018) in the publication named: Banking everywhere, never at a bank, explains the

current banking environment, which is full of technology. Banks are trying to get to clients as

close as possible via computers, smartphones or any online electronical devices in order to

determine customer needs and set up suitable service.

Nicoletti (2014) in book, called: Mobile Banking: Evolution or Revolution, states the

procedure of how banks and financial companies try to make their services available

everywhere and anytime. The author explains the chronological connection of technology and

banking.

3

Wolfe (2015) in publication called: The industrial revolution, explains the process of

transition from agriculture to industry with the machine assistance. His examples are mainly

focused on agriculture and the impact of technology in this industry. The author also

compares the number of substituted employees by machine and the impact on unemployment

rate.

4

Research methodology

Secondary research

External sources

Secondary gained information were collected from books, articles, journals, newspapers and

also from related blogs, studies.

In order to achieve main goals of this thesis, the analysis of employment in commercial banks

are provided and compared. Moreover the comparison of unemployment rates were also

helpful to support the argument.

Primary research

Information for the primary research were collected by personal interview with employees

from commercial banks or financial intermediary firms.

5

Table of contents

1. Abstract............................................................................................................................. 7

2. Introduction ....................................................................................................................... 8

2.1 Background ................................................................................................................. 9

3. History of industrial revolution ........................................................................................... 9

4. Fourth industrial revolution - Fintech revolution ............................................................... 13

4.1 Automatic teller machines .......................................................................................... 14

4.2 Computers and internet ............................................................................................. 15

5. Regtech .......................................................................................................................... 19

6. Current situation .............................................................................................................. 20

6.1 Employment in the financial sector ............................................................................ 22

7. Blockchain ...................................................................................................................... 24

7.1 Crypto currencies ...................................................................................................... 24

8. Customer experience ...................................................................................................... 25

9. Future Fintech and banking jobs predictions ................................................................... 26

9. 1 Fintech employment ................................................................................................. 28

9. 2 Traditional banking professions ................................................................................ 29

9. 3 New banking/Fintech jobs ......................................................................................... 31

9. 4 Retraining costs of required skills ............................................................................. 32

10. Technological benefits for bank ..................................................................................... 33

10. 1 Benefits for customers ............................................................................................ 34

10. 2 Famous Fintech Startups ........................................................................................ 34

11. Comparison to traditional banking ................................................................................. 40

12. The future of banking .................................................................................................... 40

13. Traditional banks response ........................................................................................... 42

14. Inside the bank (practical interview) .............................................................................. 42

14. 1 Interview evaluation ................................................................................................ 48

15. Suggested solutions ...................................................................................................... 49

15.1 Retraining ................................................................................................................ 49

16. Conclusion .................................................................................................................... 49

17. Work Cited .................................................................................................................... 51

18. List of figures................................................................................................................. 57

6

1. Abstract

The first part of this paper illustrates the background and characteristics of industrial

revolution, which has developed to Fintech revolution. Moreover the chronological

involvement of automatization is analyzed throughout the entire thesis.

The main goal of this thesis is to consider the positive or negative impact of technology on

human labor force within banking. This work seeks to investigate the following questions

with the hope of shedding light on the implications of technology on the workforce in the

banking field.

1. How does the implementation of technology effect human workforce in banking over

time?

2. Which technology effects particular positions in detail?

3. Does Fintech and artificial intelligence remove jobs within banking?

4. How does the effected employees reeducate?

5. What is the future situation of human labor within banking?

The main goal of this paper is to investigate the chronological implementation of

technology and determine if automatization reduces jobs in the finance sector, particularly in

banking, or if the technology is able to create new positions in suitable time and wage level.

Furthermore the analysis of required profession retraining are provided. Aims mentioned

above are analyzed globally and locally by an interview with Tatra Banka, a. s.

representative, Mgr. Henrieta Makovicová, with over x years of experience in one of the

major Slovakian banks. Matúš Gedaj a financial advisor at Partners Group having the

majority of Slovak commercial banks in portfolio and advising final clients the best possible

solution for financial services. According to the answers in the questionnaire, this thesis will

provide the practical picture about the banking environment. The last part of this thesis

focuses on the future predictions based on sources and collected information.

7

2. Introduction

Nowadays the impact of technology is felt almost everywhere. Humans interact with

computers or smartphones on a daily bases. The working environment is an area, where

automatization is felt the most, due to cost savings for the company. Majority of companies

try to substitute employees with computers or machines. Banking industry is no exception. In

current online world, banks try to offer their services through internet. On one hand internet

and technological devices save our time, provide more efficiency and effectiveness. On the

other computers and artificial intelligence is able to do the work faster, more efficiently and

do not retire, compared to humans, which changes the working conditions.

This research analysis will focus on the financial industry, particularly on banking, which is

analyzed from the beginning of machine implementation, until present day. Furthermore this

thesis will provide future predictions of banking industry, technological development and Its

impact on human workforce. Since the beginning of financial technology revolution the fear

of unemployment increased. Throughout the development of technology have been replacing

different professions, creating distance between personal interaction of clients and

employees. However the technology is able to create new jobs, where the humans are

necessary. The solution lies on retraining. Are the employees able to retrain themselves in

order to sustain in the banking industry?

This thesis will also present a comparison of the most machine substituted industries, the

agriculture, where technology removed almost all human labor force and the influence on the

unemployment rate.

8

2.1 Background

The history of traditional banking has the origins in ancient times. The basic services were

the deposit of valuables and later loans offering. First European banks in 12th century created

first invention, the exchange bills, which facilitated the exchange. The valuable paper served

as subsidiary for valuable metals and was considered as exchange currency (BNP Paribas).

Small paper was much easier and safer than heavy coins made of valuable metals. Similarly

to other industries like agriculture, manufacturing, the technology has helped to enlarge the

industry.

The banking industry was a multi-billion monopoly for over 600 years with very few big

players. However, the smart phone era created an opportunity for smaller businesses to

compete in financial market (Arjunwadkar, 2018). The current technological era will change

business banking. Since the industrial revolution, one of the key elements to remain

competitive depends on the level of technological development in particular firm. On one

hand the progress of automatization reduces costs, time and makes the process more efficient.

Nonetheless the velocity of machine replacement is usually not approachable by creating new

jobs. Furthermore new jobs often require retraining, which has its costs and do not guarantee

the same earnings.

3. History of industrial revolution

The Industrial revolution is known as transformation from agriculture handicraft environment

to automatic industrial and machine manufacture. This change had begun in 18th century,

England and spread to the entire World (Wolfe, 2015). There were concerns about huge

increases of unemployment due to the tech revolution in agriculture. At the beginning of the

20th century, the agriculture industry started to use the latest technology for cultivating plants,

feeding plants and animals faster, killing pets efficiently and removing diseases (Mason,

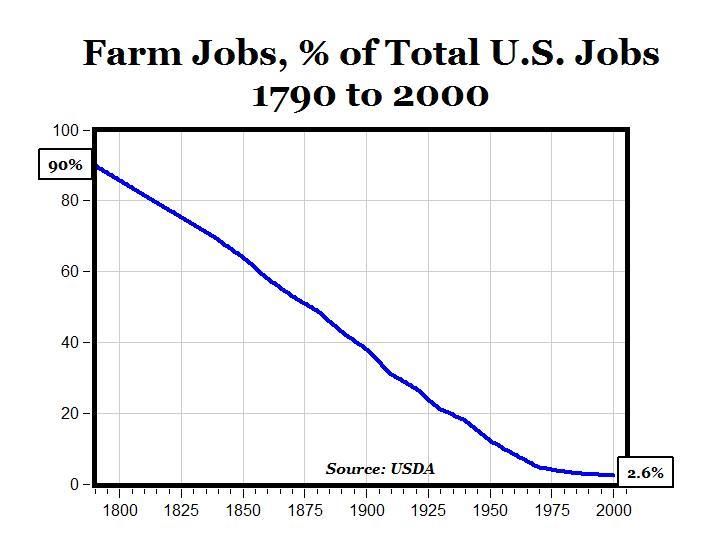

92003). Most of the work was done by humans, as can be seen in the following graph. I have

mentioned the agricultural sector, due to its highest automatization so far.

Figure 1: Percentage of farm jobs out of total amount of jobs in US

Source: http://4.bp.blogspot.com/_otfwl2zc6Qc/S7v_t

YLdiI/AAAAAAAANL4/mvqKtxmrbg8/s1600/farmjobs.jpg

After the industrial revolution in agriculture, majority of jobs included machines, thus it

created the threat of huge unemployment increase. In 1 900, 40% of the workforce were in

agriculture. Today, agriculture industry employs around 1% of US workforce, due to

automatization. (Dorfman, 2015). However the mentioned 1% of workforce is able to

produce enough food for the whole country. Moreover one quarter of production goes on

export (Dorfman, 2015). What happened to all those ex-agriculture workers? Machines

increased productivity, which means higher income leading to higher spending (Dorfman,

2015). Higher spending creates more or new jobs and services. For instance the mentioned

machine productions, service, etc. had created positions which did not exist before agriculture

10automatization. Example mentioned serves as a proof that machinery is able to create new

jobs, which fills the gap, such as jobs in harvesters factory, fertilizers production, etc.

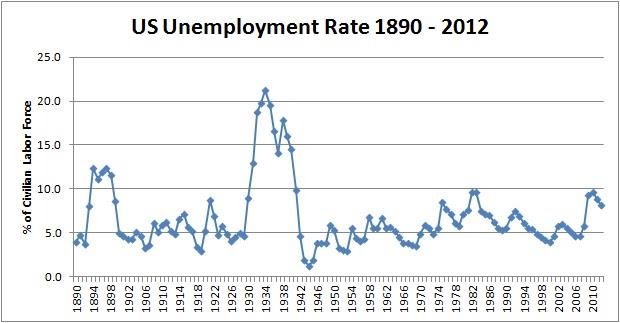

Figure 2: US Unemployment Rate from 1890 until 2012

Source: http://mindandmarket.blogspot.com/2012/10/historical-us-unemployment-data.html

As shown at the Figure 2 the US unemployment rate did not experience big fluctuations.

However in 1930s, a bigger increase can be seen, but it is a consequence of Great Depression

(Amadeo, 2018). As can be seen from the comparison of two showed graphs, we can

conclude that implementation of robots in agriculture did not cause mass unemployment.

Furthermore the industrial revolution hit all economic sectors, including finance and banking.

Traditional banks had been providing three basic activities, generating the majority of their

income, safe value storage, money transfer and loans (King, 2018). Each activity was done by

human workers. As the competition and number of customers were growing, managers were

trying to find a way to decrease costs in order to increase profits. Results ended in machine

investments, which replace employees. Within the first wave of automatization mostly

administrative and customer care services were targeted. However, as a result of

technological development, banks tend to increase automatization investments, in order to

11decrease its costs. As Noonan (2018) have stated that 90% of banks on US market use

artificial intelligence in front office for majority of actions, such as Facebook messenger chat

bot or Alexa, artificial intelligence tool created by Amazon, dealing with customer care

service. With this in mind, what happens to employees replaced by artificial intelligence?

According to Berutti, Ross and Weinberg (2017), the bank can utilize those employees on

higher valuable projects. Hence, the question is, what are the current employees doing in

order to learn new skills. Most of the companies do not cover training which can be used on

the labor market due to inefficient investment in workers who will use the knowledge in

another company.

124. Fourth industrial revolution - Fintech revolution

The Financial Technology revolution is nowadays usually connected with mobile

applications and internet banking. Moreover it is linked to recent technological development.

However the Fintech had started in USA, then expanded to UK and the rest of the World.

Generally the big boom of Fintech firms occurred after the post financial crisis in 2008

(Arjunwadkar, 2018). Authorities imposed demanding restrictions on banking industry

(Reavis, 2012). Higher bank restrictions changes created a niche market gap for startups

offering financial services.

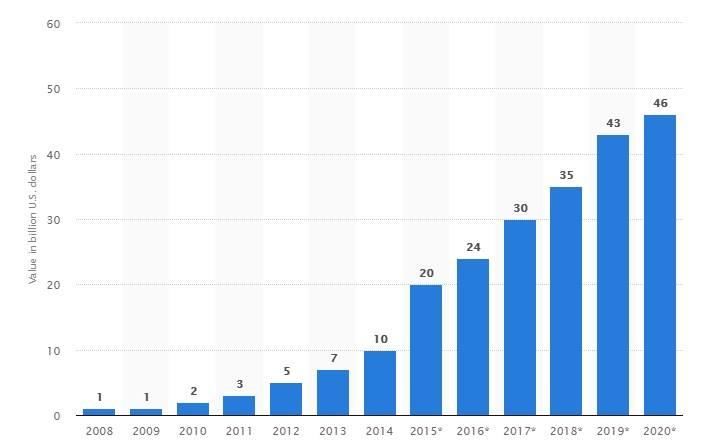

Figure 3: Total value of Fintech investments worldwide from 2008 to 2020.

Source: https://www.statista.com/statistics/502378/value-of-fintech-investments-

globally/?fbclid=IwAR1cCxHX0FO7svB4XBR8WNsVzFNQvwA4jQm77fmanMddSUEf5UCLkL5IbPU

The investments in Fintech grows every year from 2008. Currently the global value of

investments reached 35 billion USD. The graph also provide future predictions.

Within the financial industry, the Fintech started in 1950s by replacing cash with credit cards.

In 1960s the ATMs were initiated to facilitate cash operations, 1970s stand for electronic

13stock exchange and in 1990s the e-commerce and internet have expanded (Desai, 2016). In

other words, each decade the financial World experience a significant and efficient step

forward, which also impacts particular jobs.

Arjunwadkar (2018) explains that for a substantial period of time, the book keeping in

banking was done by voluminous registers1. Hence even the simple operations, like money

withdrawing and depositing was time consuming, risky of manual errors and blackmailing.

For this reason, in 1960, mostly IBM computers were introduced in banking industry. The

new systems computerized the majority of card and banking transactions. This was the

beginning of the punch card machine. The client´s bank account information, and direct

access to the central banking system. The punch card machine was mainly used to validate

checks. The confirmation of check originality was determined within seconds and first

machine series could handle up to 1 500 checks per hour (The Automation of personal

banking). The main advantage was the increased speed of processing the banking transactions

and security. The technology mentioned required trained staff, but fortunately did not have

fundamental impact on the occupation, as can be seen from the Figure 2.

4.1 Automatic teller machines

One of the most important waves of machinery implementation within banking hit the tellers,

who were replaced by ATM (automatic teller machines) in 1967 (Bátiz-Lazo, 2015).

However in the United States, the first ATM was introduced in 1969 in San Franscisco at the

Stonestown branch by Bank of America (The birth of Automated teller machines, 2014).

ATMs were firstly designed to serve as cash withdrawal machine, but more and more

services were left on these devices over time (Arjunwadkar, 2018). In 1977 the ATM

manufacturer, NCR launched model 770 was able to operate 24/7, which included controller,

cash dispenser and depository with PIN access hence an all in one machine unit. Other

1 Voluminous registers – large notes, where banks kept internal information often in hand written form

14important innovation came in 2012 allowing cash withdrawal using a code sent to mobile

phone. Gordon (2017) believes that future ATMs will have functions like money transfer

between accounts, purchasing train or gift cards, etc. In other words future ATMs are going

to handle the whole scale of bank account operations. Therefore bank tellers had more and

more new work, due to ATMs development. Currently, ATMs are able to manage the

majority of personal account activities, such as actual balance, cash deposit, change

password, charging phone credit, etc. Around 85% of the teller´s work can be done by ATMs,

today (Wasserman, 2014). According to Worstall (2011) machines are created for two

purposes, to destroy jobs and to reduce costs. In 1970s the popularity of ATMs grew with

over 1 000 units around the world, to offer convenience to clients. Moreover, Autor (2015)

claims that ATMs were introduced in 1970s, since then the number of them quadrupled from

100 000 up to approximately 400 000 in US economy. The author also argues that tellers

working positions in banking have risen from 500 000 up to 550 000 (10% increase) since

1970, until 2010. Considering the fact of the industry growth since 1970, we can assume that

bank tellers are rarely needed. Although a 50 000 employment growth throughout 40 years in

the whole US banking market cannot be considered an employment increase. This statement

is also supported by Autor (2015), because he states that the number of branches within the

same time period rose by 40%. Banks argue that Fintech will create more jobs, than it

destroys, which is partly true, due to market spread, but I believe that this situation cannot

last forever.

4.2 Computers and internet

The third essential change in banking came in 1990s with the desktop computers and internet.

From the beginning the use of online platforms was limited to employees, but then banks

took advantage of online network to develop website application through which clients

provide transactions while sitting at home or work (Arjunwadkar, 2018). With this

15convenient form of bank accession, the personal interaction between client and banker started

to decrease. However on Figure 2 we cannot see the increased unemployment rate, which

increased from 5% to 10% in US. It seems that in online network, banks have started to offer

larger scale of services, like internet banking information exchange, electronic payment and

investments, which can be one of the factors that caused growth of bank branches in US.

Hannan and Hanweck (2007) state that the amount of branches grew by approximately 27%

from 1994 to 2006. In 1994 banks were equipped by 16 employees on average. Also at the

beginning of 21st century the internet only banks started to penetrate the financial market.

With the minimum amount of branches, customers were able to access banks services, like

money transferring, applying for loan, accessing account, etc. online (Berger, 2003).

Together with computers ATMs served as substitutes for services offered in branches.

However in 2004 banks were employing around 12 workers per branch, which is less than in

1994 (Hannan & Hanweck, 2007). In similar matter, the electronic payment also gained

popularity, where consumers started to use electronic payment cards instead of checks or

cash, which decreased the work volume of bank tellers. In fact statistics show a decline of

checks payments from 49.5 billion in 1995 to 42.5 billion in 2000, which represents 3%

annual rate (Berger, 2003). The last important banking online service is the exchange of

information. This term means collecting information about companies or individuals from

financial institutions, public record, business creditors and other sources and exchanging

them with other institutions to determinate the risk of loan seekers (Berger, 2003). Study

done by Jappeli, Tulio and Pagano (1999) found that amount of provided loans in countries

where banks exchange information are higher and interests are lower. There is no doubt that

internet and computers enriched the portfolio of banking services, which sustained or

enlarged number of needed employees.

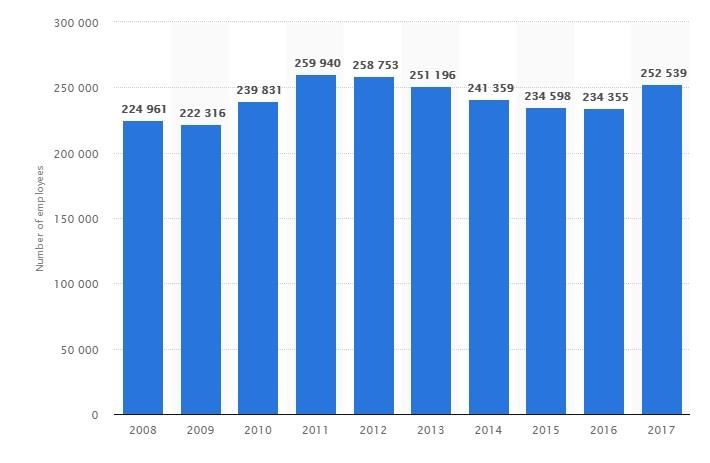

16In similar matter, one of the largest traditional banking institutions, JP Morgan Chase with

over 250 000 current employees had the net income 24.44 billion USD in 2007 (Nasdaq). The

market capitalization of JP Morgan Chase has risen to 364.35 billion USD in May 2018,

which makes the bank most valuable in terms of actual shares value (Worlds largest banks by

market cap 2018 - Statista). Bank of this size admittedly involve automatization, however

does not dismiss employees, as can be seen in the Figure 3.

Figure 4: Number of employees of JPMorgan Chase from 2008 to 2017

Source: https://www.statista.com/statistics/270610/employees-of-jp-morgan-since-2008/

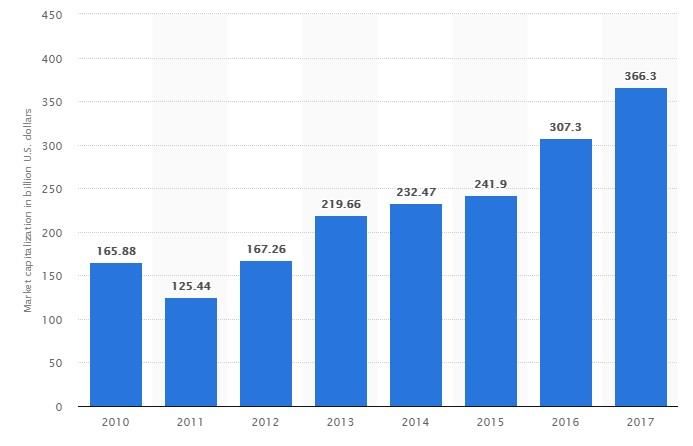

17Figure 5: Market capitalization of JPMorgan Chase from 2010 to 2017 (in billion U.S. dollars)

Source: https://www.statista.com/statistics/422930/market-capitalization-jpmorgan-chase/

By comparing Figure 3 and Figure 4, we are able to say that in Figure 4 the actual market

value of JP Morgan Chase is 366.3 billion dollars and kept increasing since 2012. The value

of the bank rises, but the number of employees is relatively stable. According to these facts,

we can conclude that the same amount of employees have more job responsibilities to handle.

The bank invests in technology, rather than training new workers.

185. Regtech

The European Union started to regulate Fintech companies and the whole financial industry

in March 2018 (European Commission, 2018). For instance by restrictions like GDPR in

Europe, MiFID II – new legislations about investor protection and financial market (ESMA)2,

KYC3 – the clients verification process (Dunn, 2018) and AML4 – regulations preventing

money laundering and financing terrorism, particularly after the last economic crisis, are

difficulties for many financial institutions. (Blaafalk, 2018). The rules and regulations are

often difficult and expensive for the banks and companies to adapt. Moreover the increasing

amount of regulations becomes more challenging for affected companies, particularly in the

process of adaptation, implementing and understanding (Kehoe, Dalton, Smith, Elst,

Mackenzie & Chollet, 2016). Furthermore the legislations usually tend to change. This

situation opens opportunity for so called “Regtech” firms, which large financial entities

outsource to take care of complex operations. Deloitte conducted a research by Kehoe et. al.

(2016), which gives examples of Regtech firms in Irish market, “FundRecs (Reconciliation

software for the Funds Industry); Silverfinch (creates connectivity between asset managers

and insurers through a fund data utility in a secure and controlled environment); Trustev

(online fraud prevention by scanning transactions in real time to determine whether they are

real or not); TradeFlow (trade data tracking and risk alert based technology); Vizor (software

provider that enables the supervision of companies by a supervisory authority, such as a

central bank, financial regulator or tax authority); Corlytics (software that analyses

compliance risks in banks and financial firms)“ (p.7). In brief the Regtech startups help

finance companies to follow laws and regulations issued by state authorities. However

according to Blaafalk (2018) the artificial intelligence used within Regtech is able to detect

2 ESMA – European Securities and Markets Authority

3 KYC – Knowing your customer

4 AML – Anti-money laundering

19fraud transactions and uses the algorithm to improve itself, which would take more time and

effort when done by human, but the employees can focus on more elaborate issues.

6. Current situation

Navaretti et al. (2017) state that modern Fintech firms will not replace the key functions

provided by traditional banks. These companies offer efficient way of popular financial

services. Smith (2017) thinks that the boom of Fintech firms is due to highest amount of

international online transactions since the beginning of banking and freelance restrictions free

economy. The actual trend of providing financial services is the mobile banking, where

customers can access their accounts anytime. Smartphone applications fully replace internet

banking and provide higher security like fingerprints or face recognition. Internet and

smartphones had brought the bank accession everywhere. The actual number of employees in

a bank branch is around 12 – branch manager, loan and mortgage advisor, financial advisors

and tellers.

Furthermore, recently we experience the boom of Fintech firms, supported by the last global

financial crisis in 2008. Commercial banks had to follow new regulations containing different

approach to risk taking and storing higher amount of liquid assets (Desai, 2015). This

situation created a suitable gap, which the startups immediately have used. As a result the

growth is continuous. Desai (2015) states that there are approximately 2 000 new Fintech

startups in Asia and around 4 000 in USA and UK. Moreover more than 24 billion USD was

invested in startups since 2010. Around 11 billion USD come from 2015.

One of the main business trends, finance is not an exception, is the rising computer usage to

substitute humans, especially within Fintech companies, which operate with the latest

technology (Mortlock, 2015). According to Schifrin (2018) more than 27.4 billion USD was

invested in Fintech companies in 2017. Thus Fintech firms will need to hire more workers, as

the “boom” trend continues.

20Massive amount of technology will be brought to banking and will delete big number of

traditional banking positions such as customers support, insurance management, insurance

assistant predictive analysis, etc. (Smith, 2018). For instance commercial banks dispose with

higher amount of capital. In 2017, Citi Group has invested over 1 billion USD to technology

(Citi Annual Report, 2017). British banking sector currently employs approximately 460 000

workers, in 1989, approximately 460 000 people were employed in the sector (Hamilton,

1995).

With the current situation in mind, the British banking industry will cut another 75 000 jobs,

according to Sir Brian Pitman, chief executive of Lloyds Bank (Hamilton, 1995). As I

mentioned earlier, banks offer other services besides traditional banking, like investments,

wealth management, insurance and so on.

216.1 Employment in the financial sector

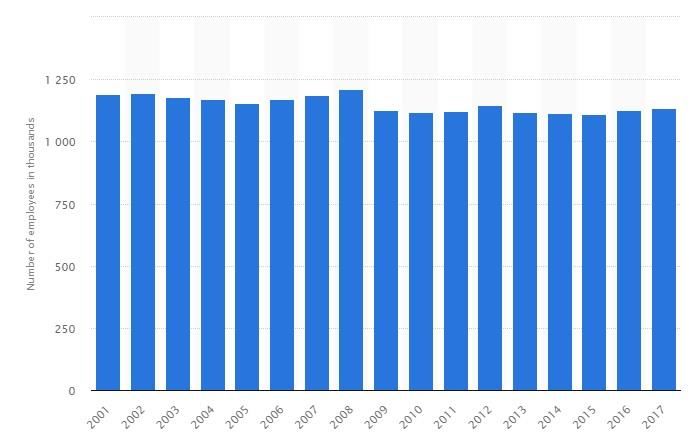

Figure 6: Number of employees in the financial services sector in the United Kingdom (UK) from 2001 to 2017

(in 1,000s)

Source: https://www.statista.com/statistics/298370/uk-financial-sector-total-financial-services-employment/

On the other hand this graph shows us almost no difference in employment rate within

financial sector. Thus we need to believe that technology creates enough jobs, because we

cannot see big unemployment fluctuations and UK is one of the most technologically

involved countries with one of the largest banking industry. According to UK Parliament

report by Rhodes (2018), the financial sector is responsible for 119 billion GPB (153.51

billion USD), which represents around 6.5% of total British economic output in 2017.

Moreover in 2016 the British financial sector was the eighth largest in OECD5 with the

proportion to annual economic value output. In 2017, there were around 1.1 million financial

services jobs, which represents 3.2% of UK jobs. I believe that massive layoffs would effect

5 OECD – Organization for Economic Cooperation and Development

22more percentage of workers, due to connected industries like information technology in case

of technological unemployment, but we cannot see big fluctuations in the unemployment rate.

The recent technological trend effects banking everywhere and is called Artificial

Intelligence. At the banking summit 2018 – The digital future, global finance conference,

Rohit Talwar stated that we should invest time to encourage our skills, abilities, creative

thinking and innovation in order to sustain employed, due to technology replacement mainly

in administrative and customer care areas (TASR, 2018). Citi Bank already uses the artificial

intelligence for the whole front office, from Facebook chat bot, until virtual software Alexa

for customer service. In other words the client mostly interacts with computer, without

human interaction. Moreover some banks use artificial intelligence in middle, front, back

office and for data analytics (Noonan, 2018). Actual bank branches try to leave all cash

operations on ATMs, account management and money transaction to clients via internet and

mobile banking (Jaques, Maxwell, Patiath & Stephents, 2017). Employees available at the

branch serve as helpers, when clients cannot manage the technology. The personal bank visit

is also more expensive due to costs like employees wages. On the other hand services like

loan application, investments require a human being, due to low trust in technology. Another

example would be the situation of Equity Bank in Kenya, where 660 employees were fired

due to new technology adoption. 63% of transactions are done by computers and just 7,4% go

through branches (The Independent Kampala, 2017). Philip Charsley (2017) believes that the

job removals will mostly touch back office positions, where technology can bring more

efficiency. Therefore, creative jobs, like product development, marketing and machine

control will be the only left for humans. In addition, Crosman (2018) states that some jobs

will disappear, but others will transform to something different, such as bot supervisor, bot

designer and others. Artificial intelligence will just do the work which nobody wants. In fact

the artificial intelligence is limited by what we teach it to do. In other words, the self-

23development of artificial intelligence is impossible, as of yet. Fortunately, machines cannot

be as inventive as humans, so far. Moreover, according to Independent Kampala (2017)

sectors like marketing, product development, investment banking and sales are hardly

replaced by computers. Large number of Fin Tech startups have for instance a smart phone

application, which needs development, configuration and management. Thus the inquiry for

application developers and managers increases. However, Matúš Gedaj from Partners Group,

believes that financial firms take care about employees´ education and provide regular

trainings in order to keep employees skilled and increase efficiency.

7. Blockchain

Blockchain is characterized as extended online decentralized database. In case of Bitcoin

blockchain, the network consists of many miners, thanks to which the database does not

depend on one computer or data center. In other words the blockchain cannot be destroyed by

shutting down the datacenter, or one computer. Moreover each transaction is encrypted by its

unique hash, recorded and needs to be confirmed by majority of members in the network

(Matuszynski, 2018). According to Bennett (2017) the blockchain is reliable and have

worked without any fault so far. The blockchain technology cannot be manipulated and

record all digital transactions virtually. Due to this advantage blockchain does not depend on

any states regulations, which increased the trust of its users (Navaretti et al., 2017). Thanks to

the advantages the blockchain gained quick popularity. Crypto currencies are often connected

to blockchain, due to its famous exploitation. However blockchain offers a wider usage in

exchanging information with high security. For instance modern hospitals give patients

prescription drugs recipe via blockchain (Williams, 2018).

7.1 Crypto currencies

The virtual currencies has also an effect on banking and its related jobs and are part of

Fintech. The first cryptocurrency, Bitcoin was introduced in 2009 with less than one USD

24value per one Bitcoin. With this independent crypto currency, anyone can trade anonymously

online without any regulations like banks or state. Each transaction is stored on block-chain

ledger and is verified by decentralized computer system. Steele (2018) believes that the

blockchain is the future of banking, due to its reliability, velocity, lower cost and safety.

However all transactions are not reversible, due to absence of controlling authority or third

participant, like banks. The transactions are set of codes and are sent almost immediately.

Controllers of blockchains and increasers of the amount of Bitcoins on the market are called

Miners (Anderson, 2017). Considering the fact that the whole procedure is done online and

by set algorithms, no human effort is needed. The blockchain technology can take bankers

jobs. As Huynh (2018) states that Deutsche Bank had 146 million USD profit in the first

quarter 2018 with approximately 97 000 employees. However in the same time period,

Bilance, cryptocurrency exchange provider published its 200 million USD net profits with

only 200 employees. I believe that the big banks will feel these new blockchain providing

firms as competitors and will need to react. In fact since 2009 the number of trading crypto

currencies had rapidly increased as well as their market value. Although the value depends on

the demand. The fear of banks can be felt even today by increasing the pressure for

cryptocurrencies regulations.

8. Customer experience

However from the customer´s point of view, banking services are becoming cheaper, faster

and more accessible. Recently, less than 5% of transactions are done by branches, others are

done by ATMs or other technology. The Independent Kampala (2017) journal published that

digital banking uses devices like phones, tablets, computers to make transactions with no

need to visit bank (The Independent Kampala, 2017). Clients are one of the few ones, who

will benefit the automatization almost instantly. As a matter of fact customers expect to

access the services of financial institutions anytime and everywhere by any portable devices.

25In addition the technological development is aiming to hands free voice control commands

(Nicoletti, 2014). The great example is the Ally Bank by Amazon. The device is activated by

voice and is able to track transactions, access the bank account and even suggest the amount

of working hours in order to afford a new bike. The more information client gives to Ally

Bank, the better suggestions (Wisnievski, 2017). With this upcoming trend, clients will have

almost no need to physically visit the bank branch.

9. Future Fintech and banking jobs predictions

PWC (2016) consultants predicts the future banking successful elements like data analysis of

customers, which will forecast profitability and revenue, digital mainstream use for

everything from basic banking to wealth management to smarter adapt clients´ needs.

Financial technology will interact, record and evaluate every customers activity.

Modifications mentioned above will provide lower costs, better service and deployment.

According to Vives & Xavier (2017), new technologies will automate the majority of

financial activities, such as portfolio advice, asset management, payment system etc.

Deutsche Bank chair executive, Mr. Cryan stated that more than half of current 98 000

employees can be replaced by robots, due to artificial intelligence adaption. Similar message

was published by Citigtoup chief officer Mr. Pandit, about 30% banking jobs reduction will

be due to automatization (Noonan, 2018). In general, jobs dealing with data and jobs

involving same processes are the ones in danger (Mortlock, 2015). The future banking will

try to adapt to personal clients´ needs and offer the best solution. As Nicoletti (2014) stated,

that future financial institutions will be tailor-made and more personal. Crosman (2018)

predict that 70% of front office professions will be removed, specifically tellers, loan

interviewers, customer service providers and clerks. Most of mentioned jobs will be done by

computers. According to Nicoletti (2014) the front office positions are one of the main ones

in danger. Clients will be able to manage their accounts directly from electronical devices and

26there will be no need for another person between bank and customer. In fact actions like

small loans and money transfer can be done via internet banking or applications even today.

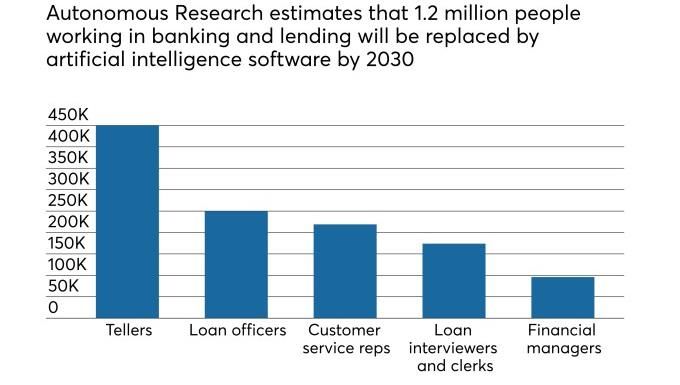

Figure 7: Estimation of jobs lost due to bots

Source: Crosman, P. (2018, May 07). Losing their jobs to bots [Digital image]. Retrieved from

https://www.americanbanker.com/news/how-artificial-intelligence-is-reshaping-jobs-in-banking

According to the graph, most effected occupation will be the tellers, who mostly interact with

customers, were firstly replaced by ATMs and currently with artificial intelligence. In

contrast the Fintech will bring colossal number of new companies on the market. Crosman

(2018) states that companies implementing artificial intelligence will increase employment by

14%, due to revenues raise by 34% by 2022.

On the other hand, Kessler (2017) believes that labor displacement caused by automatization

should be measured and education programs should be provided to those who lost a job.

However Navaretti, Barba, Calzolari, Giacomo, Pazzolo & Franco (2017) state that the

important questions is whether and how much does Fintech replace financial institutions , if it

does so, Fintech should expect stricter regulations. These conditions are unfair towards

traditional commercial banks, which have to obey regulations and laws of state and central

bank. Furthermore commercial banks have to regulate their interests rates set by national

27bank, which is one of their main source of income. As Freixas & Rochet (2008) state, the

bank´s operations consist of providing loans and taking deposits from clients. According to

my practical interview with Matúš Gedaj, financial advisor from Partners Group, I was told

that the upcoming trend is to fully digitalize bank branches and reduce employment to one,

maximum two employees per branch. However brick and mortar branches will be available

only for financial providers, who will substitute interpersonal meetings with bankers. The

complete banking service portfolio will be provided through financial advisors. Matúš

believes that the client will not have a need to personally visit a bank branch, because client

will manage the personal or firms account through web or application.

9. 1 Fintech employment

Smith (2017) publish that in United Kingdom around 100 000 jobs will be created by the end

of 2020, due to estimated 8 billion USD investments is Fintech industry. The UK was again

chosen due to its importance in financial industry.

28Figure 8: UK unemployment rate Source:

https://www.ons.gov.uk/employmentandlabourmarket/peoplenotinwork/unemployment/timeseries/mgsx/lms/lin

echartimage

According to the graph the current unemployment rate in UK is around 4%, which is one of

the lowest level since 1983. However the technological unemployment does not have an

important impact on global UK unemployment rate.

Figure 9: Number of employees in the financial services sector in the United Kingdom from 2001 to 2017

Source: https://www.statista.com/statistics/298370/uk-financial-sector-total-financial-services-employment/

9. 2 Traditional banking professions

Traditional bank branch consists of several main employees, such as:

Bank Teller is usually the first person who meets clients after their entrance in the bank

branch. This position does not usually have any special requirements. Majority of banks train

their new employees internally. The essential part of their job is to offer basic bank services,

like cashing checks, receiving deposits, loan payments, manipulation with client´s bank

account, etc. In the past, tellers did not have computers, so they had to do most of their

29activities manually, from cash calculation until documents storage (Zamosky, 2007).

Currently the average salary of bank teller is around 27 260 USD per year (Campbell, 2018).

Loan officer is in charge of tailoring loans and mortgages according to client´s needs.

The substantial part of his/her work includes matching the banks offer with client´s needs and

providing advisory services (Projobs).

Branch manager is responsible for the whole bank branch unit. The position includes

supervising over all branch employees and reporting results to headquarters. The average

number of employees at each branch is around 6 (Deaton, 2015).

However, before the technological implementation, banking services were limited to basic

activities like money deposit and providing loans. With the technology upcoming, banks have

expanded offered services with providing worldwide investments, personal financial advice

and so on. Therefore new jobs were created. The current digital age allows the accession to

bank services practically everywhere, which is more popular and comfortable to clients, than

visiting a bank branch. Dallerup, Jayantial, Konov, Legradi and Stockmeier (2018) state that

there are far more transactions provided electronically than even before, moreover since the

last financial recession, more than 10 000 branches have been closed in US. Considering the

evidence above, bank branches may reduce number of employees or change their job duties.

Majority of customer contacting will be replaced by computers and their working duty will

change. Dallerup, et.al (2018) show that according to their McKinsey study, future bank

branches include three main areas. The first is the self-service zone equipped with ATMs,

service terminals, robot greeters and video conferencing room available 27/7. The second

area is called the standing zone furnished with bankers, who can by approached with assisted

and sales services. Priority lounge is the last area in the bank branch offering premium private

banking advisory and support services. Authors also estimate that 85% of branches will have

30up to 4 employees. To sum up, approximately two employees from each bank branch need to

be retrained or fired.

Figure 10: Number of establishments and employees in commercial banking businesses in the United States in

2010, 2014 and 2015 (in 1,000s)

Source: https://www.statista.com/statistics/188895/us-commercial-banks-number-of-establishments-and-

employees/

9. 3 New banking/Fintech jobs

The new technology have also brought new job duties, which created the demand for

different positions. M-Pesa, money transaction provider, is a new startup in Kenya and has

potential to grow, thus will need more employees. The traditional banks will not reduce

employment, because M-Pesa just filled in the market gap (King, 2018). In general machines

can take our jobs, but machines are not able to take the jobs which has not been invented.

Only humans are inventive so far (Dorfman, 2015).

Generally, Fintech technology and companies have created new positions, which did not exist

before. I will list the top 11.

311. Blockchain developer – the position requires programming and coding in order to keep the

flow of crypto currencies.

2 Applications developer – the increasing demand for applications increased the need for

creating more application.

3. Financial analyst – is responsible for managing budget and creates income forecast.

Furthermore financial analyst can also advise about investment opportunities and create

pension plan (Campbell, 2018).

4. Product Manager – handles the overall Fintech product. For example the product manager

is in charge of designing, developing the blockchain until the successful end.

5. Compliance expert – is making sure that the company follows the law and regulations on a

particular market in order to prevent complications.

6. Cybersecurity analyst – discovers the threat of being the target of hackers.

7. Quantitative analyst – are behind the data driving, big investments, analyzing the security

and risk.

8. Culture champions – basically make the professional environment comfortable for

employees.

10. Business development manager – generate new income, search the ways how to access

new markets or look for new strategies for existing markets.

11. Data specialist – designing databases according to the needs of company.

(Gaskin, 2018)

9. 4 Retraining costs of required skills

Majority of Fintech jobs require skills in particular programming language or software, such

as Java, Business Analysis, C#, Murex and Python (Clarke, 2015). Java is a programming

32language used for software production for multiple platforms. It is also used for creating web

applications (Christesson, 2012). Java skills are required for banking technology positions.

The average price for Java programming course is around 2 850 USD (Certstaffix, 2018). On

the other hand, average salary of Java developer is around 57 500 GPB (74 750 USD) per

year (CW jobs, 2018). Business Analyst requires skills of risk level in for example

implementing new IT projects. These employees get paid approximately 77 712 USD per

year. Usually companies do retrain employees by themselves. C# developers create

applications which run on desktop computers. The course in visual studio costs around 2 950

USD (Certstaffix, 2018). Murex is a software managing the integrated trading, risk

management and post – trade solutions (Murex, n.d.). Murex is a widely used software with

over 45 000 daily users in over 60 countries (International Fintech, 2017). Courses for Murex

are provided by individual companies which use the software. Python is a programming

language working on most operating systems. Python is open source (Python, n.d.). The

course for Python costs around 2 700 USD (Certstaffix, 2018). The average salary for Python

developer is approximately 116 379 USD per year (Daxx Nearshore IT). To sum up,

automatization create popular jobs mentioned above directly However there are more jobs

created as a consequence of increased productivity.

10. Technological benefits for bank

The adoption of new technology brings more control over the offering services, increased

revenues and cost efficiency (Nicoletti, 2014). The customer care is often related with angry

customers. In case of client in debt or unexpected penalties calls the bank, mostly the anger

takes its role. However the computer does not have emotions and is able to find the suitable

offer faster than a human. Moreover machine does not misbehave by other side behavior

(Crosman, 2018). The other advantage of chat bots is the data management. The software is

able to find for instance previous clients problems, financial details are retrieved much faster

33than by human. Furthermore bots are equipped with self-learning algorithm, which get

enriched from previous experience and is able to adapt to customer needs (Arjunwadkar,

2018).

10. 1 Benefits for customers

Increasing number of Fintech companies enlarge the competition on the market. Traditional

banks and other financial institutions have to react either by lowering prices or offering

additional services. From the clients point of view the choice of financial services providers

will be wider, cheaper and available everywhere and every time.

10. 2 Famous Fintech Startups

Fintech startups mainly penetrate the current market with wealth management, payment and

loan services (Arjunwadkar, 2018). The application or software will replace financial

advisors. Major wealth management sector consists of management of clients liquid assets

from 100 000 USD up to 1 million USD, where the online platform does all the job instead of

financial advisor. Current leaders in robo-advising Wealthfront and Betterment manage

around 2.3 billion USD (Mortlock, 2015).

E-commerce and mobile banking had brought an important change to banking industry.

Arjunwadkar (2018) mentions that current applications provide wallet services, personal

financial planning, mobile banking, peer-to-peer landing and much more. In fact, Mortlock

(2015) believes that Fintech companies will bring more efficiency and effectiveness to

banking by reliance on machines than humans. The most popular ones are online payments

platforms, which are available to everyone, who wants to proceed payments via internet.

My Bank - Alibaba

Alibaba introduces online bank, mainly for small customers, not rich. The bank will be able

to offer smaller loans and lower interest rates to small enterprises also located in rural areas

thanks to smaller operational costs than a physical bank (Millward, 2018). Despite the fact

34that Alibaba is one of the fastest grown trading companies, they came up with a support for

smaller manufacturers.

Apple Pay

Apple is a service provided by Apple Corporation to receive and send payments right through

messages or by asking Siri. Moreover the service is available on number of Apple devices,

such as laptops or watches. In other words, Apple provides money transactions via messages

(Apple, 2018). There is no need to remember password, Apple touch ID serve as verification

by your fingerprint. The credit or debit card is simply registered into the apple device, thus

there is no need to carry it anymore. Moreover, in case of paying via terminal, the Apple

iWatch can serve as a payment method through NFC – near field communication chip. At the

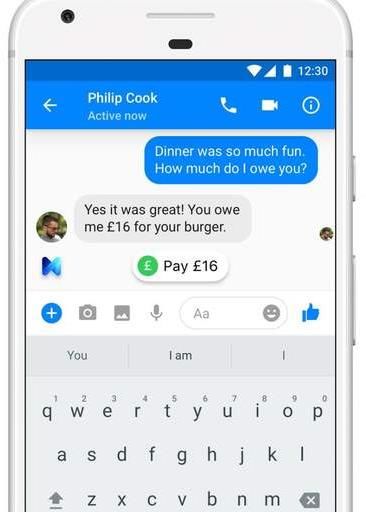

end of transaction the bill will automatically be saved to your iPhone (Rogowsky, 2014).

Saved bill database in smartphone provides an easy access to personal spending, plus in case

of goods return the bill can be found immediately (see figure 9).

35Figure 11: Apple Pay on iPhone

Source: https://www.mobilmania.cz/clanky/zivesk-prichod-apple-pay-do-ceska-a-na-slovensko-je-na-

spadnuti/sc-3-a-1342347/default.aspx

Google Wallet

An Android application Google Wallet serves as a payment method in the smartphone also

using Near Field Communication – NFC (Handa, Maheshwari & Saraf). I believe that every

transactions is recorded and the company can tailor targeted advertisement based on what,

where and when was the user purchasing goods. Obviously Google will have Android Pay

application pre-installed in every smartphone with NFC chip and Android operation system

(Marks, 2015).

Zonky

Another example is Czech startup Zonky.cz, which deposits money from investors for a

higher interest than banks and borrows money to lenders for a lower interest than commercial

banks. Therefore the whole process is transparent and both sides can see where the money are

and what provision does Zonky take. The firm acts as a provider (Zonky, 2018). Zonky.cz is

36an online Czech peer-to-peer financial platform established in 2015. The main offered service

is money deposit and lending. Zonky basically finds investors who want to invest their capital

and borrowers at better interest rate for both sides (Zonky, 2018). What I see as a big

advantage is the independency from state and the national bank. Thus, Zonky is able to create

own interest rates for deposits and loans. The website or application collects loan enquiries,

where borrowers have to state exact sum, purpose and annual personal financial record. The

whole process takes up to two days. After the confirmation, Zonky publishes loan enquiry on

their portal. Investors can decide to whom their money will go. The whole process is

transparent and both sides can see each payment. Zonky charges two percent from the loan

(Kudrnová, 2018). In summary Zonky works as a connection platform between investors and

borrowers, which I see as a benefit, because there are not three participants as in commercial

banks, borrower, lender and the bank.

PayPal

Usually described as online platform service. As Arjunwadkar (2018) expresses PayPal had

started in 1998 and simplify the online payment method. Customers do not need to take out

their credit cards and copy details. PayPal does the job instead of them, including the

shipping details. PayPal is considered as the first online wallet service.

The beginning of 21st century was hit by broad – spectrum digitalization within banking, such

as payment applications (Google Pay, Apple Pay), mobile wallets, robo – advisors, online

lending platforms (Zonky.cz), etc. (Desai, 2016).

Stripe

The online payment platform, Stripe has its origins in Ireland and was founded in 2011. The

main offered service is software, which enables to receive online payments by individuals or

companies. Stripe provides payment service as final product including technical and security

37You can also read