Exploring cheque use in New Zealand - September 2017 - Innovation Fund

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Exploring cheque use in New Zealand September 2017

Commissioned by the Westpac NZ Government Innovation Fund Project sponsor: IR Working Group: Dave Gillespie, IR Russell Syme, Westpac Shane Spencer, IR Samantha Latham, IR Mondy Jera, ThinkPlace Tarapuhi Bryers-Brown, ThinkPlace Jim Scully, ThinkPlace Visual Designer:Jess Lunnon, ThinkPlace 2 ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund

Introduction

The use of cheques as a mode of payment in New Zealand

has been decreasing over time, but a number of individuals

and organisations continue to use them. Although cheques

are quickly disappearing from common usage there is still

a persistent “tail” of cheque use that needs addressing.

The problem

As cheque use decreases the cost of processing increases. Cheque printers

are being impacted by low-level demand and the technology used to process

cheques in New Zealand is expiring. As a result, support of cheques in New

Zealand for the diminishing “tail” of users would require investment in new

cheque processing technology.

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 3Introduction

Exploring cheque use in New Zealand

Westpac NZ Government Innovation Fund commissioned a project to explore

this issue from a human-centred perspective. The aim of the project was to

produce a base of actionable insights that can be used by banks, businesses

and government agencies to ultimately design cheques out of the system. This

project was considered a “phase one”, whereby this report is an aligned set of

insights and frameworks that can be used prior to deeper concept development.

What we discovered in this project is that the innovation is in the nudge – we found that

although there is worry and resistance about changing on the part of both the issuers

and receivers of cheques, that people are ultimately nudge-able and will change given

the opportunity. However, like most complex issues, a one-size-fits-all, ordered solution

isn’t likely to work; multiple, small nudges towards the goal will shift people towards

cheque elimination (unless of course, someone just decides to mandate against their

use and deal with any repercussions).

This exploration was also an design better, client-centred products

unintentional, mini-intervention; some and services, and ultimately replace

ThinkPlace was commissioned

participants reflected on their payment cheques entirely.

to develop some customer

habits after the interview and said

Westpac Innovation brought insights that can be used

they would make a change. Whilst by banks and government

ThinkPlace, IR (the project sponsor),

not intended, it is also not entirely agencies by investigating the

and the Ministry of Justice together

unexpected given that just a glimpse following:

to design a qualitative approach to

into a complex system can in fact be a

understanding the social, economic,

disruption. It also provides confidence

cultural and regional forces behind Why are some people

to designers that intentional, still using cheques?

payment choices.

empathetic nudges will work towards

solving the problem. ThinkPlace conducted a targeted What would the human

literature review and an ethnographic impact be if cheques

Overall, there is a good, quantitative

study that uncovered a range weren’t an option?

sense of the cheque-user landscape.

of ethical nudges and insights

Westpac and IR in particular provided How can we support

that might empower people and

a robust picture of who is using people to not pay

organisations to use other options.

cheques. But less has been explored by cheque?

A working group from IR, Justice and

about why people use cheques despite

ThinkPlace explored some high-level

other payment options being available.

concepts and the group formed some

The Innovation Fund aimed to

recommendations for the Steering

understand the experience of cheques

Group to consider.

so that agencies and banks could

4 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundSummary of the literature

This section provides a glimpse into

how other countries are managing,

or have managed, the transition to

other payment modes. Cheque use

is declining globally due to products

and processes that replace the key

functions for consumers in each

market. However, there are stark

differences in the rate and the type

of change, and the impact on culture.

The following discussion highlights

the support different users needed

to move to other options.

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 5Summary of literature

Exploring cheque use in New Zealand

Cheque usage

Singapore

South Korea

New Zealand

Sweden China

South Africa Britain Canada

Netherlands Germany Australia USA

Eliminated Rarely used Retention but Relatively popular

rapid reduction payment method

Electronic payments have caused this seven percent of accounts that use

General cheque shift. Kiwis are now completing 67 cheques, only use cheques, and

electronic payments for every cheque these accounts are generally used

use in New Zealand written; an increase of almost 400 infrequently for special payments

percent since 2010. Online, facilitated such as savings or trusts.

PaymentsNZ’s research bill payments continue to play a

Demographically, age and locality

shows that the use of cheques significant role in this.

are key indicators of cheque use.

in New Zealand has halved Overall, a large amount of accounts in The number of cheques deposited

between 2013 and 2016 from the country are issuing a small amount and issued increases with age. The

a monthly total of 4.4 million of cheques. The top 100 issuers were frequency of electronic payments in

mostly organisations who make a high rural and urban areas is the same,

cheques to 2.24 million.

number of irregular payments. however, rural accounts use around

15 percent more cheques per year

Organisations are the largest

than urban accounts. On average

acceptors of cheques, especially

rural accounts deposit 4.4 cheques

utilities, government and retail. Of the

per account, and urban accounts

100 highest cheque acceptors, 37

deposit 3.7 cheques per account.

percent of cheques are accepted by

the utilities industry, many of whom

send invoices in the post and get

cheques posted back to them.

Cheques are rarely the only payment

channel used by individuals and

therefore not many people are solely

reliant on cheques. Even amongst

This summary combines data from a wide range cheque users, EFTPOS is the most

of publically available reports. The authors were

limited to literature available in English and Dutch common payment choice. Only

6 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundInland Revenue cheques can evoke a certain

Government cheque sense of critical reflection on a

use in New Zealand Seven percent of IR payments purchase; some use cheques

are cheques. This equates to to avoid making mistakes; and

Government has a significant 911,000 payments made by finally, unreliable or limited

influence on cheque 150,000 customers annually. reception as a barrier to digital

payment, especially where an

behaviour in New Zealand. Most cheque payments to IR come

authorisation needs to be made.

Inland Revenue and Ministry from customers who are regionally

of Justice process the based and over 50 years old.

Ministry of Justice

Eighty-five percent of customers

most cheques followed by

who pay by cheque are over 50,

Department of Internal Affairs, with 70 percent of these payments

Justice fees, such as filing

then Ministry of Business, made by those over 65. fees, require payment to be

attached. This incentivises

Innovation and Employment.

Ninety percent of cheque

cheque use – as it is the only

payments came from

appropriate way to ‘attach’

customers who had a tax

payment.

agent linked to their account

for the same tax type as the The option for sending

payment was for (although reparations and receiving

payment for jury duty by cheque

it is not clear who made the

is still available. Justice tells

payment).

us that juror cheques are

decreasing, with 59 percent of

payments being made by direct

Seventy-seven percent of all credit; a reduction of 65 percent

cheque payments made in 2017 in the number of payments by

were made by individuals, with cheque since 2014. Justice

50 percent of this group being has also observed a significant

self-employed. uptake in direct credit since jury

correspondence in all areas were

A significant 96.5 percent of

updated to include this as an

customers only use one channel

option.

to pay.

IR research has identified

some key motivations for their

customers’ cheque behaviour.

For example, cheques are often

used by small suppliers; people

find the emotional and tactile

experience of cheques satisfying;

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 7Summary of literature

Exploring cheque use in New Zealand

International trends aimed to improve the efficiency

Even with imaging technology, of superannuation transactions

and insights cheques are still becoming by making it compulsory to make

more expensive and harder to contributions electronically.

In the past, cheques have

use. Cheque use declined 20 Furthermore, the property settlements

been the first port of call for percent in 2016 – the largest industry, who have historically

non-cash, non-card payments decrease ever recorded for the facilitated a high amount of cheque

in many countries. However, county. The rate of declining transactions has also focused on

international changes have cheque use dropped by six going digital through e-Conveyancing.

percent after remaining flat in In early 2016, the electronic

seen other options arise

conveyancing system had processed

preceding years, including no

with a general trend towards over $10 billion property sales.

change in 2015.

electronic payments and

Lastly, to ensure that consumers can

debit cards. The rate of effectively and confidentially transact

decline varies considerably is declining across age brackets, but with government online, work has

is still largely concentrated in older also commenced on formulating

mainly due to the maturity

citizens. approaches to manage online digital

of other options available in

The payments industry has put focus identity.

each country.

on a coordinated and collaborative

approach to managing the decline of

United Kingdom

the cheque system by ensuring that

Australia before any decisions are made about

an end date, that replacements match, After lengthy consultation, in

Australia is noted as our most or exceed, the attributes of cheques. 2009, the UK Payments Council

comparable in experience of Emerging innovative solutions are announced that they would be

cheque use and decline. expected to further accelerate the closing the cheque clearings

decline by providing useful alternatives system if adequate alternatives

to cheques.

The Australian digital economy is were developed by 2018.

booming and correspondingly digital Of most significance is the New

payments and cards are displacing Payments Platform (NPP), an industry Reports show “voucher” payment

cash and cheques, partly enabled by initiative that is expected to be systems were being considered which

a high number of point-of-sale (POS) launched later this year (2017). This would operate like cheques without

devices nationwide. Both the value initiative is developing infrastructure the same sort of clearing facility and

and volume of digital payments are for data-rich, versatile and speedy processing as cheques.

increasing. Whereas cheque use is payments where consumers will

Due to public backlash, especially

declining at an accelerating rate. be able to link accounts to easy to

centred around concern for the

remember information such as a phone

The Australian payments industry elderly and charities, the Council

number or email address. Users will

changed to digital cheque clearing cancelled this target in 2011,

be able to provide this PayID to people

in 2015. Images of cheques are concluding that cheques would

or organisations they want to receive

now captured at branches and stay for as long as customers

payments from. One of the services

processing centres to be exchanged needed them. Currently, the decline

that the NPP will enable is BPay’s real-

electronically, cutting the need for of cheques in New Zealand and

time mobile payments.

physical exchange and storage. Australia is much further advanced

The Superannuation industry has than when this issue was considered

Today, cheques are often used for

seen a decrease in cheques due to the in the UK.

larger expenditures and dictated by

SuperStream reforms. These changes

merchant requirements. Cheque use

8 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundEuropean Union The Netherlands

In 2015, 55 percent of UK businesses In the EU, there has been a The Netherlands successfully

were still writing cheques. They are steady decline in the use of eliminated the use of cheques

still relatively widely used today, with cheques since the early 1990s, through an increase in the

nearly a half a billion cheques issued with the arrival of the Euro in processing charges and a

in 2016. Sixty-eight percent of people 1999 speeding up that process. reduction in the supply of free

over 65 still use cheques (in contrast

Today, cheques are rarely used cheques.

to 88 percent of 16 to 34-year-olds who

and are no longer accepted as a

never write them). They are a popular

payment in many EU countries. The Dutch public opinion was

choice in certain situations such as

supportive of the move – electronic

when the payer does not know the

means of payments had been

bank account number of the payee,

introduced several years previously,

or the sort code. There is also a small Across the EU, policies were

with the first means of electronic

number of businesses (especially implemented to discourage

payments introduced into shops in

smaller service providers) who do the use of cheques, due to

1985.

not want to share their bank account their considerable costs and

details and/or to become accredited risks. However, not all of In the EU, Norway and the Netherlands

receivers of direct debits. these policies were equally showed the most rapid adoption of

electronic payments, which during

A legislative change then enabled the successful, and the decline in

the nineties largely replaced cheques

introduction of cheque imaging. The cheque use was not uniform

(and cash) as forms of payment.

Image Clearing System will transform across member states

It can be argued that, apart from

the system by allowing cheques to be

minimal fixed start-up fees, the fact

cleared using a digital image rather

that transaction prices for consumers

than the physical paper, removing In 2012, more than eight cheque are zero in the Netherlands was an

the need for cheques to be physically payments per capita were made, important driver in this development.

moved from bank to bank. This is on average, in France, Cyprus, Fixed fees are sunk costs ex-post

being phased in at the beginning of Malta, Ireland, the United Kingdom that do not vary with usage and thus

October 2017. By late 2018, all the and Portugal. The highest usage have limited behavioural effects, in

UK’s banks and building societies will occurred in France, with around 43 contrast to transaction-based prices

clear all cheques this way. cheque payments per capita in 2012. that significantly affect consumers’

The move is being framed as a path A number of reasons have been given payment decisions.

with more choice, but “nobody has to for this climate including a standard By 2002, banks were no longer

do anything differently if they don’t for putting bank account details on accepting payment by cheque.

want to”. Customers will still write invoices, mature debit card markets,

cheques and physically give them to and standalone paper credits (also

the recipient (by post, at the bank, or in called paper Giros). The paper-

The Netherlands continue to

person). Some banks may also enable based Giro provided an alternative

be ahead of the curve in terms

their customers to pay using a digital to cheques by paying through mail.

image of a cheque through a secure of monetary transactions. In

Bank Giro transfers instruct a bank

app. 2016, almost 30 percent of

to directly transfer funds from one

bank account to another. They transactions took place using

provide more security than cheques mobile phones, with experts

when lost, and are processed more predicting cash and wallets will

efficiently. Bank Giro Transfer, or have completely disappeared

Giro Credit are effective ways for within the next 10 years.

businesses to receive payments from

foreign customers, and have been

digital for over a decade.

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 9Summary of literature

Exploring cheque use in New Zealand

Sweden USA

Between 2010 and 2014 Even though the USA has a large to other payment methods, and

Sweden led the race in cheque appetite for online retail, it is at consumers choosing internet-based

decline with a rate of 98 the top end of the spectrum in bill payment methods.

percent. terms of cheque use. Out of the

18 countries still using cheques, Canada

Sweden is swiftly moving towards the USA accounted for 64

a cashless society, with businesses percent of total cheques issued Although still comparatively

and social institutions such as in 2014. high, cheque use in Canada

churches adopting new ways

is lower than in the USA and

to harness the power of mobile

continues a rapid decline. Fewer

payment. Notably, the Swish

Even millennials continue to cheques are being written but

payment service, developed by

major banks, allows 24/7, real-time

issue and receive cheques in for increasingly higher amounts,

payments between bank accounts. large numbers in the states; mainly due to continued

70 percent issuing cheques commercial cheque use. As a

Another platform that is making

at least once a month, and result, there is strong push to

waves is iZettle. Their small card

14 percent issuing over 30 encourage businesses to move

reader connects to a mobile

cheques per month. from cheques to direct deposit.

device. iZettle gained international

attention when Situation Sthlm,

Cheques continue to be a large

a magazine sold by the homeless Many business-to-business invoices proportion of remote transactions.

or disadvantaged in the streets of still rely on cheques, possible due to Many banks in Canada have enabled

Stockholm, provided their sellers the absence of real-time electronic customers to deposit cheques

with the device, aiming to increase payment systems. remotely using a secure app.

sales by using a trusted payment

portal. In 2004, the USA implemented Check Duplication and fraud are some of

21, a federal law that was designed the issues that are emerging as

to help banks handle more cheques issues particularly associated with

Germany electronically. Nearly all cheques in cheque imaging.

the USA are now cleared electronically.

Germany introduced an Research from the Canadian

Many cheque payments are converted

image-based cheque collection Payments Association demonstrates

into electronic payments through the

procedure in 2007 which made a strong relationship between the

Automated Clearing House including

the process cheaper and more both cheques mailed in (ARC) or decline in cheques and the use of

efficient. presented in person (POP). Automated Funds Transfers (AFTs)

such as electronic direct credit or

The introduction of the debit card Electronic cheques are also becoming direct debit transactions.

and the ban in corporate cheques more utilised. They are marketed as an

(2002) had massive influence with electronic version of a paper cheque,

just 0.4 cheques written per capita in fitting seamlessly into the cheques

2014, leaving only a small number of payment system at the core of many

personal cheques being used. businesses and the banking industry.

They contain the same information and

Many regular payments (like bills) fit within the same legal frameworks

traditionally use direct transfers rather as cheques. Payments are authorised

than cheques, and Überweisungen, by the issuer, for example through a

or pre-printed paper credits that confirmation click.

detail the payee’s account, and the

amount payable. The payer provides The decline of cheque use in the USA

the Überweisungen and invoice at has especially been influenced by a

the bank, and the bank transfers the long-term migration of state benefits

amount to the payee.

10 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundDiscussion

This summary has demonstrated the range of

approaches to managing the decline of cheques

globally. Further research into how other

countries have directly supported older and

rural citizens towards non-cheque payments,

and the short-term impacts on citizens would

provide additional insight into these strategies.

The international experience brings to light some key themes:

• Countries who have been early adopters of non-cash options are

experiencing a smoother transition to eliminating cheques –

New Zealand has a comparatively mature EFTPOS and debit card

culture so is probably in this camp.

• Government ceasing the issuing and receiving of cheques plays a

significant role in the bulk decrease of payments and cultivating a

broader culture change.

• People often stick with cheques because they are the best or only

option. The availability of other non-cash, non-card alternatives

invites people to change. International experience shows that

the key attributes requiring replacement are: real-time transfers

with immediate availability 24/7, the ability to attach data and

documents with payments, and to be able to make payments

without knowing the recipient’s account number.

Two high level approaches have emerged:

Cheque decline management

Leaning on cheque imaging Leaning on cheque replacement

• Like a cheque but not on paper • New ways of paying

• Less change • More change

• Prolonging life of cheques • Cheques less and less attractive

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 11Our approach

Exploring cheque use in New Zealand

Our approach to human-centred exploration

CO CO

E NV E NV

G ER G ER

ER Explore GE ER Explore GE

DIV DIV

Inn

Inn

A current &

future view of

1

ovate

ovate

our customer

experience

2 Eva 4 Eva

lu at e 3 lu at e 5

We spoke in depth with 19 people across The people we talked to lived, ran businesses or

New Zealand to deepen our understanding worked in organisations in the following locations:

of how and why people are still using

cheques. We heard from a range of

individuals and organisations, including Auckland

those who: issue cheques, accept, and/ Waikato

or deposit cheques and one organisation

who has recently stopped writing cheques. Wairoa

Wainuiomata

Participants were initially approached for permission Lower Hutt

to participate by either Westpac, IR or Justice. The Johnsonville

participants were chosen from the respective three Wellington City

databases due to their high cheque usage. A wide- Dunedin

range was sought in order to explore the breadth of

Clutha

experience.

ThinkPlace then contacted the participants to set

up an interview time. We experienced some minimal

The sample was comprised of:

attrition between the initial permission granting over

the phone by the three agencies and the attempts to

schedule an interview (we had three such cases, two Tax agents Rural and Sport club

of which from Councils). and their urban older treasurer

clients persons

We were unable to speak with end-users of Justice

(participants were not approached by Justice).

Another gap is persons with disabilities. Several Accountants Law firms Council

organisations were contacted but none came

forward to participate.

Other businesses (confidential)

12 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundAnalysis

The participant was given a choice whether they We captured field notes during each

wanted a face-to-face interview or would prefer interview, and also captured our initial

a phone interview. For phone conversations, we

thinking on debrief templates after each

emailed an information sheet, consent form and

research kit in advance.

interview. This aided analysis and ensured

nuances from the interviews were not lost.

We conducted semi-structured interviews using a

set of prompting questions and card sorts. We used

two sets of cards to elicit meaningful reflection from The transcripts were then read and re-read thoroughly

the participants. A “payment channel” card set asked along with the field notes and debrief capture sheets.

participants to pick out the payment channels they Then a framework for capturing key insights was created.

use from a wide range of examples. People were then The analysis framework included: significant quotes,

asked to put their choices in a hierarchy of use. what would get the participant to shift payment modes,

The second set was used with customers who what would be good for them, and any new experiences

mainly used cheques for personal payments rather or observations that added to our understanding.

than business. These card sorts asked the people to From there, we were able to extract key patterns and

discuss the payment method they use for a range of salient points. The next section provides the detail of

activities. those insights.

The main reason for the card sorts was just to

get participants talking about how and why they

pay for things – not all participants chose to put

them in hierarchies and not all cards applied to all

interviewees.

With permission, the interviews were audio recorded

and then transcribed verbatim. Participants were

offered a copy of the transcript if they wanted one.

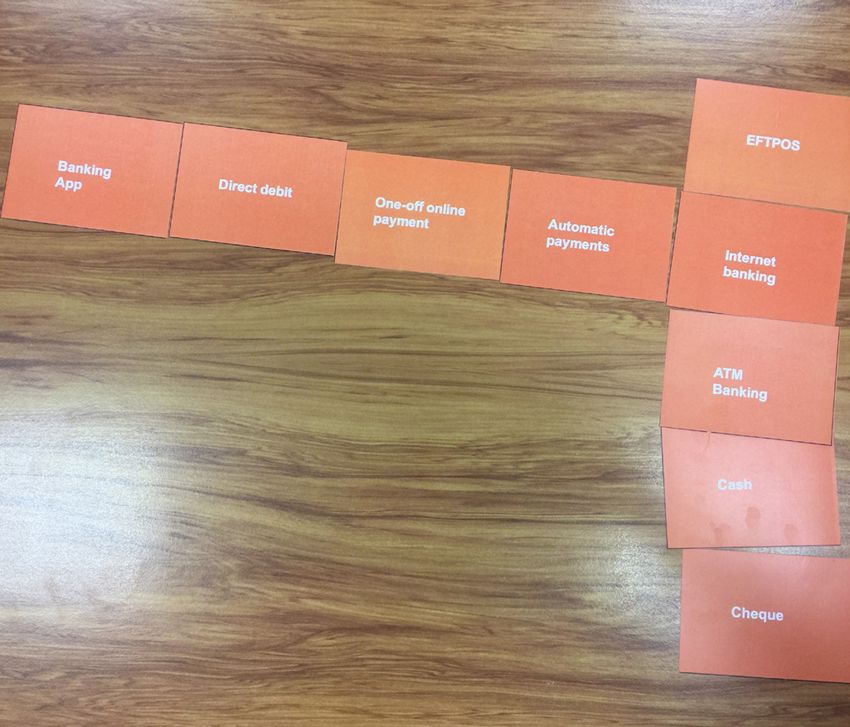

Participants who were not working for government Images

Left: List of the card sort

agencies were provided with a voucher in exchange

Right: Photo of the card sort in action

for their time.

Cheque Credit card PayPal Cash

Internet banking Voucher ATM Banking

EFTPOS One-off online payment

Banking App Direct debit Apple Pay

Automatic payments In person, at the bank

Phone banking Pre-loaded cards Txt

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 13A summary of the reasons the people we

spoke with are writing or receiving cheques.

• Using an outdated payment • School fees

processing system (about to

be upgraded) • Gifts

• The difficulty (or not knowing • Koha

how) to get two signatures for • Perceived as a possible tax

an online payment process workaround

• Fees for other options • Fear of giving bank details

pushing people to cheques for online payments

• Court fees must be paid • Lack of trust that provisional

via cheque tax will be paid properly

• Don’t know how to use online without the paper trail

payments/no digital access/ which shows all the correct

not interested in digital means reference numbers, etc.

• Client demand for using • Paying staff bonuses

them/fear of reprisal to • Paying people who won’t

remove the option accept online payments

• IR deadlines for PAYE and necessitates cheque writing

GST being close together – • When it’s difficult or

having a client’s cheque in impossible to find customer

hand in advance is easier than bank accounts for payments

chasing them down to make

a payment. The payments • No seamless option for

being close together puts too online IR batch payments

much stress on the business

• They like having a paper

to change.

record of when what, why,

• Entrenched business and/or and who they paid

personal processes around

• Because it’s an easy option

cheques (habit)

• Receiving a free cheque book

automatically from the bank

14 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundThe following key insights were derived from

analysis of the conversations. We extracted

the central themes and the salient points.

Insight

The magical window of 10-15 years in the

future when it will be easier for people to In 10 years’ time, I think we’d be in a better

stop writing cheques. position because the new generation will

have taken over all the businesses and stuff,

and they’re much more prepared, sort of, to

For those resistant to, or concerned about, the take that on...

stopping of cheques, they offered up the idea that

Participant WI-01

10 or 15 years into the future would be a better

time to eliminate cheques. These commenters

were concerned about the “older generation” not

being able to transition to online or other payment

channels and an assumption was made that

either they would be retired from their current

Interviewer: What makes you say that,

professional posts or gone altogether (deceased).

waiting 15 years?

The idea that the older generation wouldn’t cope

Because you know everybody like me will

with losing cheques was a strong assumption be gone, and there’ll be, everybody new

throughout the conversations, and thus the will be used to it, or will accept it.

assumption that delaying cheque elimination

would avoid the pain of transition seemed a Participant WI-13

logical solution to them.

HIGH-LEVEL OPPORTUNITY AREA

“Phase out” plans that promote the

message of a supported transition that

leaves no one behind.

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 15Key insights

Exploring cheque use in New Zealand

Insight

There is still fear that providing a bank I know it sounds probably a

account number is unsafe for both direct

little bit funny but, it’s just

debits and credits.

the way I think, and so yeah

that’s what I do, but that’s

For debits, we heard about this lack of trust directly

the only direct debit I’ve got

from citizens, but also from organisations who hear

this from their client base as a reason that they is my household insurance.

use cheques (or other forms of payment that don’t Participant WI-11

involve providing bank details).

Paradoxically, some clients of tax agents felt On the other side, organisations who need to pay

comfortable leaving signed cheques and various people don’t often have bank account details so they

other personal details, but not their bank account. resort to writing cheques. Anecdotally, this is because

There is something specifically about the ability to people are afraid to provide their bank account

remove money from one’s account that seems to numbers rather than a preference for a cheque. For

be the barrier, as opposed to just having personal some organisations we spoke to, hunting down those

details in general. account numbers and putting them into their online

Even more confounding, people pay particular bills systems was just more burdensome than cheque

via cheque or counter payments, and others via writing.

direct debit. When questioned, they were sometimes Some organisations told us there are vendors who still

unsure about their own habits around who and won’t accept direct credit or have trouble with their

why they trust to pay via direct debit. It wasn’t internal accounting systems with direct credits so

always about predictable amounts being paid, they’re forced to pay by cheque.

but that was part of the story (a quarterly, stable

insurance payment versus fluctuating power bills,

for example).

I would have to give them

[accountants] my bank details

basically and for me that would

be a bridge too far in terms of

… but I don’t know from a client’s perspective trust goes. I can sign a cheque

whether there is a perception that they

don’t feel comfortable with IRD just taking

so unless someone forges my

money from my account. Sometimes people signature and stuff.

are a bit funny with that concept.

Participant WI-09

Participant WI-06

16 ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund…yeah they’re [cheques] probably open to fraud

just like anything else, same with direct credit,

someone could send you a new bank account

that’s not technically the company’s bank

account…

Participant WI-14

HIGH-LEVEL OPPORTUNITY AREA

Strengthen messages to consumers and

businesses about the safety of direct

debits and credits. Publish a comparison

of cheques versus direct debits/credits

and their relative safety and accuracy.

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 17Key insights

Exploring cheque use in New Zealand

Insight

People hates fees

It seems that if people can avoid paying fees, they will. While we didn’t fact-check, we heard that some

On principle, some will go out of their way to avoid banks are charging fees that are more expensive

paying even a small fee. While we did not focus on fees than cheques for setting up types of direct credits.

per se, we heard how people felt about them and what This may require further investigation.

they do to avoid them.

Here’s a conversation about potential fees with a

participant who writes cheques out to cash at the bank:

About a counter payment fee:

It’s about, I don’t know how much it is, it’s not

terribly much, 25-cents I think, it’s a matter

of principle to me, I know they put that on

Interviewer: If the bank charged you at the

fairly recently, it used to be that you could just

time to cash a cheque, what would you do?

go and pay anything at the counter and that

“Yeah I’d still use cash, but I’d just see you know was fine, but then all these agencies came in

what’s a cheaper way of getting it out.” and decided they were going to get their cut,

Interviewer: Okay so you might shift if it was because this is probably some of what’s going

like all of a sudden, a big fee or something, you on now, to put people off. So, I thought no I’ve

might start using an ATM instead? got all these cheques, I’m just going to send

a cheque away, so I don’t have to worry about

“No, I’d look for another bank first who wouldn’t that silly little amount.

charge, they’re all down here on Lambton Quay,

I would look for another bank…” Participant WI-11

Participant WI-13

HIGH-LEVEL OPPORTUNITY AREA

The stories we heard about fee avoidance weren’t

necessarily “rational” choices. The participant quoted This issue of avoiding fees probably

above pays a flat $5 monthly bank fee for use of comes as no surprise to the banks.

cheques, and she writes very few cheques, so in fact, However, it seems there may be a role

the 25-cent fee was cheaper, and she was already to play for behavioural economists

paying other bills at the same time at the Paper Plus who can design fee structures that

counter. nudge people away from cheques by

simply communicating the true costs

If there is a fee attached to setting up a process,

of each payment mode in a way that

people will default to using a cheque instead (in spite

helps people make “rational” choices

of cheque fees). Perhaps the “flat fee” model for

and banks could use cheque fees as

cheque usage feels invisible to customers whereas if

a more powerful deterrent.

they are prompted to pay a fee they switch payment

modes without exploring the real costs.

18 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundInsight

HIGH-LEVEL OPPORTUNITY AREA

The ceremony of cheques (and paper)

High-level opportunity area: create clever

alternatives to cheques that still have

We expected to hear more about the romantic side of the ceremony of paper but that have an

using cheques, such as the feel of paper, the ritual of easy digital payment mode for actual

writing them, etc. However, what we heard was more money transfer. This may have particular

around habits, preference, ease, fee avoidance and significance for how things function at

mistrust of other options. marae so could be tested with iwi.

One outlier was a paper-loving participant who

realised at the end of the interview that her worries

weren’t so much about cheque removal. She said,

Insight

If they said, ‘there’s going to be The staunch cheque users admitted

no more post’ and everything they would adapt, but others are worried

had to be emailed to you, and about the impacts on their organisation

you’d never get anything in the

post, I think I’d be more upset There was a noteworthy pattern to the interviews

with some participants who claimed to love the

than if they said, ‘you can’t use of cheques. When prompted whether cheque

write a cheque anymore. elimination would produce a small/medium/large

Participant WI-10

impact on them, even the most ardent cheque fans

admitted the impact would in fact be quite low.

One participant at a government department told

us about using cheques as koha for visiting marae.

Cash would be a good substitute, he said, but the

issue of getting cash to staff who were out in the

Well you know given that in my

field was too risky and difficult. Thus, cheques were case I’ve got my daughter who’s

the best for koha payments. got complete control of those

Older persons we spoke with liked the freedom to be sort of things I’d say, ‘here you

able to write cheques to their grandkids and others

do it’.

as gifts without leaving the home. There was some

Participant WI-04

ceremony attached to handing over the cheque

that was somehow different in nuance to cash (or

probably just easier).

One organisation told us that they pay staff bonuses

by cheques because that creates a more special

feeling than just popping the extra pay into their

accounts.

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 19Key insights

Exploring cheque use in New Zealand

Well, I’d just toddle on, just pay

at the counter and stuff like that,

So I mean if there are other options [through

you know. I wouldn’t have an accountant], I am happy to use them, but we

issue with it. have never been informed of others. We have

just been told to do this, we have the cheque

Participant WI-11 and like okay, it works. So, we have never

queried or questioned.

On the other hand, for some within organisations

Participant WI-08

(who are not necessarily attached to cheques the

way individuals might be) the impact would be bigger

due to the necessary changes in office procedures

and/or fear of customer reprisal should they not be

allowed to accept cheques.

The two sides of the argument suggest there is …but honestly, if they had to go, if the cheques

perhaps more fear from organisations than is had to go, then I would manage. I’m not going

necessary – the die-hard cheque users we spoke to be thinking, I would write into the editor

moaning and groaning that the cheques were

with might not be happy, but they’d find a way.

going or anything

Participant WI-11

Well because we know, we know there’d be a

huge kick up [if we didn’t accept cheques] ...we If we turned off cheques, we’d

get enough of a bad rap as it is, you know it’s

good if everything is good but as soon as you have a queue of [employees] up

make one wee mistake…you know so yeah don’t the stairs to talk to the Board.

want to sort of rock the boat too much, you just

need to get their money without inconveniencing Participant WI-17

people too much.

HIGH-LEVEL OPPORTUNITY AREA

Participant WI-01

Demonstrate clearly to organisations

and businesses that customers may be

mildly annoyed, but are ultimately willing

to change with the right supports and

nudges.

First of all [if cheques were eliminated] there is

nothing I could do, and the other thing is, you

Support organisations with opportunities

know, I’ve got a business to run so I would find for best practice without cheques. Offer

a way. a pool of money for investing in updated

technology.

Participant WI-13

20 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundFramework for thinking

about how to shift away

from cheques

Listening to the reasons behind

cheque usage, we realised there

are those who “can’t” shift easily

or those who “won’t” shift easily

(but will with a nudge).

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 21Those who “can’t” Those who “won’t”

• Lack of digital access entirely

(but will with a nudge)

• Disabilities • Preference for other channels

• Frail elderly • Habit

• Digitally left behind (just didn’t • Easier options available

learn) • Afraid/resistant

• Bound by rules/regulations

(e.g. courts only accepting

cheques, various vendors

requirements)

• Isolated socially, culturally or

geographically

• Low literacy, low understanding

• Can’t pay someone online

when don’t have bank details

The two types require different solutions.

“Can’t” types need “Won’t” types need

support for a transition. cleverly designed nudges.

For example: For example:

• Digital training or non-digital • Remove the option to pay

solutions by cheque

• Just do it for people via family • Make it universally more

support or approved social expensive to pay by cheque

service or private agents

• Promote existing options with

• Social service support for more intent

frail elderly and persons with

• Provide a higher level of

disability if required

confidence that sharing a bank

• Government department and account isn’t tantamount to free

other business commitment to account access

change/streamline procedures

• Make it easy to pay without

giving bank account details

• Design a paper substitute for

time of ceremony or gift-giving

22 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundHēnare Tae

Can’t because it’s difficult to Mix of can’t and won’t

pay other ways due to having because he doesn’t have

frail health, low mobility and online skills, has no time, but

isolation. is also a bit stuck in his ways.

Won’t

Can’t

Can’t because she doesn’t Doesn’t see the need for

always have bank details change and doesn’t want

to pay online. She would if to. He wouldn’t move

it was frictionless. without a good fight.

Suzanne William

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 23Scenarios

Exploring cheque use in New Zealand

The following are some hypothetical, amalgamated scenarios based upon the stories we

heard. These characters can be useful for thinking about client need and for humanising

the issues. The quotes are also hypothetical but represent some of the challenges expressed

by the participants. The scenarios can be plotted on a continuum which helps when

thinking about the solutions they may need based on the “can’t” or “won’t” extremes.

Hēnare Tae

Elderly man Low income Non-digital farmer Lives rurally

Lives rurally No family No internet

Doesn’t trust Doesn’t own No internet

access

direct debits a computer access

No mobile Can’t drive Uses a

phone anymore walker The systems and processes of the

farm are set up for using cheques

Doesn’t own a and he doesn’t have the business

smart phone capability to change confidently

His nearest neighbours Pays bills by posting

look after him by delivering cheques – has flag drop

groceries and taking him at house for postal pick

into town now and again and they come each day I’ve got a system that works for me. I

don’t have time to learn anything new –

I’m a farmer, my time is determined by

the demands on the farm. I find people

I can’t do many things by myself anymore. that I trust to do all my accounts – I can’t

Not being able to pay bills would take be bothered dealing with finances and

away my dignity. I’m already feeling quite money. I have never in my life found the

dependent on a few nice people to help. time to sit in front of a computer.

24 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundSuzanne CFO in a William

medium-sized

organisation Successful small Doesn’t like

business owner to change

Makes a lot of She often can’t pay Has always done Emotional connection

one-off and regular people online because things a certain way to cheques and paper

payments, both online she doesn’t have their processes

and with cheques bank account details

so she finds no other

option but cheque

Doesn’t like emails, Loves the social aspect of

thinks they’re sending letters and going

impersonal into the bank

Until everything is She likes to pay staff

easier online, she will Christmas bonuses with

write cheques cheques to make it feel

more like a gift

Likes the traceability Doesn’t like being told

and control paper what to do – hates

processes enable limited choices

Efficiency is Would like to improve

her main driver efficiency but cheques are

sometimes easier than

a whole system change If my bank took away cheques, I would

within her organisation swap banks. They are legal tender – I will

keep using them and I would complain

to my local MP if they tried to stop them

I really don’t like cheques, but if it’s a altogether. It wouldn’t be fair at all. The

hassle to do it online I won’t bother and government should just wait 10-15 years to

just quickly write out a cheque. eliminate cheques for the next generation

– it would make it easier for everyone.

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 25Frameworks

Exploring cheque use in New Zealand

Initial concept and framework

development Here’s an example of what one group

came up with:

After learning about the insights, the They looked at the reason: Fear of giving bank details

working group came together to test some for online payments. They turned it into the need for

early concepts and frameworks in a half- reassurance and increased trust.

day brainstorming session. This day was Their concept was entitled ‘Assurance of protection’

not designed to be an intensive design

An invitation to change:

experience, but rather a session to develop

ways to think about the issue going forward. • Education about the safety of direct debit

options

• Organisations signing up to and publishing a

To test the process, the group broke code of practice that’s visible to customers

into two and:

• Invitations to change to existing electronic

1. looked at the reasons why people are still platforms – always telling people about them

writing cheques,

Persuasion to change:

2. then thought about what customer need that

• For payments into accounts, ask people,

reason represented, then

do you want to be paid today (direct payment)

3. they developed a high-level concept as a or in two weeks (cheque payment with an

possible solution. exaggerated, intentional delay)?

• Offer a card for payment if they don’t want

The other group then gave their reasons it would not

to give a bank account, but charge a fee for

work in a ‘ritual dissent’ style. They then went back

that card

to the drawing board to strengthen their concept and

• Create alternatives (e.g. pay to a mobile

thought about what style of nudge(s) would help.

phone instead)

The framework for thinking about the nudges

• Non-identifying payments into customer

was initially called “nudge, prod or shove” which account (e.g. generic message on statement

were then turned into three types of nudges with so as not to arouse suspicion by others who

more definition: can see the account – particularly true for

Justice and other complex social events)

Forced to change:

An invitation to change

• All card or other costs go to the individual,

(gentle nudge) many other options are in place

• Must pay/accept payment by these other

Persuasion to change means as we do not use or accept cheques

any more

(the prod, more active nudge)

Both the ‘nudge’ framework and the matrix are useful

Forced to change tools that agencies could use when designing their own

(the shove, making people shift concepts. Ideally, future concepts would be developed

to other modes permanently) and tested with the end users of each agency or bank,

given the wide-range of customer needs and the

special requirements in each department.

26 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundThe working group then decided to think about some

of their concepts for change against a matrix.

Biggest impact

Mandate all payments

Bulk payment to Task from tax agents to be

IR from Tax Agent force electronic

Verify bank account Cheque

with each customer amnesty

phone call program

Direct debit Saying the Industry

Banks stop from 3rd final date Group with

remittance parties to be in public Commerce

processing made easier Commission

Card for

Program of

Easiest payment instead Hardest

communication of having to give

bank details

Education IR to stop Pay to an

accepting alias

post-dated -Facebook

cheques -Email

-Phone Sanctions

with cost

increases

Key

Stop New customers Give incentives

automatic with no cheque when people

An invitation to change

cheque book books log-in

re-issing Persuasion to change

Forced to change

Smallest impact

ThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 27Recommended next steps

Exploring cheque use in New Zealand

Recommended next steps

The working group concluded the brainstorm

session by discussing the recommendations

they would like to take forward.

A re-invigorated focus on Develop champions in each

educating customers government agency

This insight project revealed that Government agencies may require some

customers may not know what is specific changes internally, but will need

available to them, do not understand strategic direction and someone to drive

the safety of online transactions and the initiatives. It was assumed that the

do not understand the expense of Better Public Services Result 10 would

processing cheques. provide the best fit for the strategic

direction and targets, with someone

being the champion who understands the

Exploit and enhance existing insights work and how to coordinate and

communication channels action the nudges.

The working group pointed out Form a benevolent cheque-

that there are already many touch ending industry group

points with customers, but we need

a renewed focus on messaging and The working group recognises the issues

education through those existing for banks if there is not a genuine end

contact moments. date and agreement across the banking

sector. In order to avoid collusion issues,

an industry group or similar could be

Develop a task force to work formed and appeal to the Commerce

with big cheque users Commission with a plan to end cheques

collaboratively.

This is particularly appropriate for Establish a cheque elimination

businesses. The task force would date and then make it public

work more intensively to help design

good solutions for these big cheque

users. The working group suspects The working group agreed that in order

it’s more about habit and minor to initiate the nudges, a genuine end date

tweaks (and education as above) when cheques are to become obsolete

rather than major banking product is critical to success. Otherwise, it will

development. However, the task force simply not be taken seriously. This may

would certainly uncover service or involve investment in public awareness

product gaps in the system from the campaigns to assist with a general

user perspective. culture shift.

28 ThinkPlace in collaboration with the Westpac NZ Government Innovation FundThinkPlace in collaboration with the Westpac NZ Government Innovation Fund 29

You can also read