FARM & RANCH ESTATE/SUCCESSION PLANNING

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FARM & RANCH ESTATE/SUCCESSION PLANNING

Succession planning is a process for identifying and developing new leaders who can replace old leaders when they leave, retire, become disabled or die. In a family business, it entails mentoring the next generation with the potential to fill key business leadership positions in the operation and help them understand the why!

Why is this so important?

2 million farms cover

America’s landscape1

About 99% Only 29% 62% of U.S.

of U.S. farms are of family farms have farm operators are over

operated by families2 transition plans in place2 the age of 551

1 2017 USDA Census

2 2016 US Farm succession plans and the process of transferring land ownership. Agriculture & Applied Economics Assoc. Annual Meeting

Only 30% of family-owned businesses

pass to the next generation

And even fewer (12%) to the third*

* Family Business Alliance

http://www.fbagr.org/index.php?option=com_content&view=article&id=117&Itemid=75

“Failing to plan is planning to fail” Primary reasons farm and ranch transition plans fail? ◦1. No current estate/succession plan ◦2. Inadequate estate/succession plan ◦3. Insufficient capitalization ◦4. Failure to prepare the next generation properly ◦5. Failure to communicate the why?

Components of the Business Succession Plan Establishing Goals and Objectives Family Involvement in the Process Identify Successors Estate Planning Contingency Planning Entity Structure and Taxes Business Valuation Exit Strategy Implement and Follow Up

Who has a transition plan?

Nebraska Intestacy Laws

Intestate Succession: Spouses & Children

Inheritance Situation Who Inherits Your Property

– If spouse, but no children or parents – Entire estate to spouse

– First $100,000 of the estate to spouse

– If spouse, and all children are of decedent

– 1/2 of the estate’s balance to spouse

and spouse

– Leftover split evenly among children

– If spouse, and some or none of the – 1/2 of the estate to spouse

decedent’s children are of the spouse – 1/2 of the estate split evenly among children

– If children, but no spouse – Entire estate split evenly among children

– First $100,000 of the estate to spouse

– If spouse and parent(s), but no children – 1/2 of the estate’s balance to spouse

– Leftover to parent(s)Estate Planning Goals – While Living Provide for management of assets in the event of disability or incapacity Provide instructions for healthcare decisions Protect assets from long term care costs

Estate Planning Goals – At Death Determine who gets what, how and when after death Maximize estate by reducing expenses and avoid delays Avoid family disputes Minimize estate taxes Provide liquidity

Planning All of Us Should Consider

Will

•Legal Document

– Takes effect at death

– State requirements vary

• Benefits

– Transfer of assets

– Names guardians

– Can establish trusts for beneficiariesDistributing Your Assets

Probate

Court-supervised distribution of assets

Advantages

◦ Distributes assets according to will

◦ Limits time to challenge will

◦ Limits time creditors can make claimsWills & Probate –Avoiding Probate

Can you avoid probate? Own property jointly with rights of

survivorship

Complete beneficiary designation

Yes, an estate plan can be designed to

control which assets pass through

forms for property such as IRAs,

probate, or to avoid probate. retirement plans, and life insurance

Transfer on death deeds

Make lifetime gifts

Use trustsTrusts -- What Is a Trust?

Legal entity that holds property Grantor

Parties to a trust: grantor, trustee, Trust

beneficiary Trust Property

Agreement

Trustee

Living trusts vs. testamentary trusts Manages trust property according to

trust agreement

Revocable trusts vs. irrevocable trusts Beneficiaries

Have rights to trust property

under terms of trust agreement

Control and manage an assetRevocable Trusts

Pros Cons

1. Avoid Probate 1. More Complex

2. Incapacity Planning and 2. More Work Upfront

Asset Management (funding the trust)

3. Protects Privacy 3. Higher Initial Cost

4. Reduces Administrative

Burden on Loved OnesTax Basics

Transfer taxes include:

§Federal gift tax - imposed on transfers you make during your life

§Federal estate tax - imposed on transfers made upon your death

§Federal generation-skipping transfer (GST) tax - imposed on transfers to individuals who are more

than one generation below you (e.g., grandchildren) both during your life and upon your death

§Nebraska Inheritance Tax

◦ Immediate relatives are subject to an inheritance tax of 1%

◦ Exemption amount $40,000.

◦ Remote relatives are subject to an inheritance tax of 13%.

◦ Exemption amount $15,000

◦ Other transferees are subject to an inheritance tax of 18%.

◦ Exemption amount $10,000Transfer Tax Basics Federal

2016 2018 2020

Top rate 40% 40% 40%

Gift and estate tax $5,490,000 $11,180,000 $11,580,000

exemption

equivalent

amount

GST tax exemption $5,490,000 $11,180,000 $11,580,000

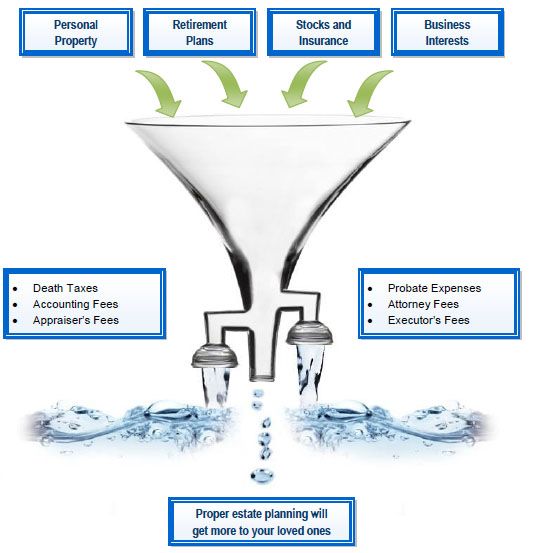

The reversion to a $5 million exemption will occur on schedule on January 1, 2026 if Congress does not act.Taxable Estate The net assets subject to taxation equal the person’s total assets minus liabilities and minus the prescribed tax-deductible portion (charitable donations) of assets left behind by the deceased. Valuation Factors ◦ Lack of Control ◦ Lack of Marketability ◦ Special Use 2032A

Asset Valuation “Basis” Gifted Asset – donee retains donor’s basis Inherited Asset – recipient receives a step up in basis of the assets fair market value at the date of death. To determine if the sale of inherited/gifted property is taxable, you must first determine your basis in the property.

Farm/Ranch Succession Agreements

Buy Sell Agreement

◦Cross Purchase

◦Stock Redemption

Cash Rent or Lease Agreement Structure the terms prior

to the event taking place!

Operating Agreement

Employee BenefitsBuy Sell Agreement Purpose of the buy sell agreement is to create a plan that defines control, value and disposition of the company stock under defined triggering events Triggering Events May Include ◦ Death ◦ Disability ◦ Divorce ◦ Disagreement ◦ Bankruptcy ◦ Felony ◦ Retirement The valuation factor can vary for different triggering events

Cash rent or crop share agreement

Active Children: Inactive Children:

Right to farm the ground Right to an income stream

◦ For a period of years

Right to use and enjoy the property

◦ Or for lifetime

First right of refusal if active child does

Establish a cash rental rate or crop share % exercise right.

◦ Can be based on UNL market study

◦ Local FSA office information

◦ Predetermined by family members

First right of refusal/Put Option

◦ Predetermined price

◦ Tax assessed value

◦ Discount on market valueCommon family scenarios

Active Farming Non-Active Farming

Children Children

Can the operation support Is there a role for a non-

multiple families in the next active child? Concept of Fair

generation? Does everyone vs. Equal

know their role?

Active Farming Family Non-Family Members

Is there a brother or sister Is there a key person or

you farm with today? What property that the operation

are their plans? needs to retain? Are there

ex-family members that could

affect the operation?Building your team

Property /

casualty

agent

Banker / Real estate

lender agent

You and your

quarterback

Accountant Attorney

OthersLeave a Legacy A family owned or closely held business will endure or die depending upon on how effectively they plan for the future. Those who survive will have managed to re-create the energy and wonder that fueled the original entrepreneurial spirit.

Presented By:

Brandon Dirkschneider CFP® FSC, CLTC®

Brandon@insdm.com

(402) 672-8173You can also read