For the period ending: December 31, 2017

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

For the period ending: December 31, 2017

303 Congress Street

Boston, MA 02210

617.723.6400

www.dalbar.com

CONTENTS Introduction ........................................................................................ 3 Anatomy of Investor Returns .............................................................. 5 Executive Summary........................................................................... 10 2017 Year in Review.......................................................................... 12 Taking a Closer Look ......................................................................... 16 Short-Term Focus and Market Timing ............................................... 18 Behind the Numbers: Investor Psychology… ..................................... 24 Year-by-Year Investor Returns .......................................................... 26 Glossary ............................................................................................ 28 QAIB Products ................................................................................... 31 Investor Return Calculation: An Example… ....................................... 33 Rights of Usage and Sourcing Information ........................................ 35 © 2018 Quantitative Analysis of Investor Behavior 2

Introduction Since 1994, DALBAR’s Quantitative Analysis of Investor Behavior (QAIB) has measured the effects of investor decisions to buy, sell and switch into and out of mutual funds over short and long-term timeframes. These effects are measured from the perspective of the investor and do not represent the performance of the investments themselves. The results consistently show that the average investor earns less – in many cases, much less – than mutual fund performance reports would suggest. The goal of QAIB is to improve performance of both independent investors and financial advisors by managing behaviors that cause investors to act imprudently. QAIB offers guidance on how and where investor behaviors can be improved. QAIB 2018 examines real investor returns in nearly 30 different categories of funds. The analysis covers the 30-year period to December 31, 2017, which encompasses the aftermath of the crash of 1987, the drop at the turn of the millennium, the crash of 2008, plus recovery periods leading up to the most recent bull market. This year’s report examines the results of investor behavior during a booming 2017. About DALBAR, Inc. DALBAR, Inc. is the financial community’s leading independent expert for evaluating, auditing and rating business practices, customer performance, product quality and service. Launched in 1976, DALBAR has earned the recognition for consistent and unbiased evaluations of investment companies, registered investment advisers, insurance companies, broker/dealers, retirement plan providers and financial professionals. DALBAR awards are recognized as marks of excellence in the financial community. Methodology QAIB uses data from the Investment Company Institute (ICI), Standard & Poor’s, Bloomberg Barclays Indices and proprietary sources to compare mutual fund investor returns to an appropriate set of benchmarks. Covering the period from January 1, 1988 to December 31, 2017, the study utilizes mutual fund sales, redemptions and exchanges each month as the measure of investor behavior. These behaviors reflect the “Average Investor.” Based on this behavior, the © 2018 Quantitative Analysis of Investor Behavior 3

analysis calculates the “average investor return” for various periods. These results are then compared to the returns of respective indices. A glossary of terms and examples of how the calculations are performed can be found in the Appendices section of this report. The QAIB Benchmark and Rights of Usage Investor returns, retention and other industry data presented in this report can be used as benchmarks to assess investor performance in specific situations. Among other scenarios, QAIB has been used to compare investor returns in individual mutual funds and variable annuities, as well as for client bases and in retirement plans. Please see the “Rights of Usage” section in the Appendices for more information and appropriate citation language. Visit the QAIB Store! Renowned investor behavior research is now at your fingertips! Visit the QAIB Store at www.QAIB.com for images, infographics and data feeds from the 2018 study. You can find a menu of additional products on page 31 of this report. For questions, please contact Cory Clark at cclark@dalbar.com or 617-624-7100 for additional questions © 2018 Quantitative Analysis of Investor Behavior 4

Anatomy of Investor Returns

…the story of Harry

Investment returns have been simplistically reduced to a single percentage that

disguises the incredibly complex issues that investors experience. This article is

intended to shed some light on these complexities. It shows how deceptive the

most frequently published investment returns are.

These complexities are presented in the form of a narrative of an investor, Harry,

and his adventures with his retirement plan.

What happens to real people: Harry’s Story

A $500 payroll deduction is automatically put into Harry’s 401(k) each month.

Unfortunately, this is $500 less to pay bills and for the essentials and pleasures

of life. But this is worth it because it means a more comfortable retirement for

Harry and his family when that time comes.

Harry’s monthly pay stub holds some good news. It is often

The $500 deduction is a lot less painful because his recommended that one

employer sweetens the deal with an additional $250, should aim to replace

plus there are no taxes withheld! The $500 payroll 75% of their pre-

deduction instantly becomes a $750 contribution to retirement income.

Harry’s retirement, with no taxes taken out.

There is even more good news at the end of the quarter. Harry gets a statement

showing his three monthly investments are now worth $2,350, but

contributions only add up to $2,250! Another $100 appeared as though it was

by magic.

Harry is also delighted to see on the statement

that the markets had gone up by 10% in the

quarter. Compare that to a CD that earned a

measly 0.1%! That would explain the magical

$100.

But wait a minute Harry thought, 10% of $2,250 is

$250. Why did Harry’s $2,250 only go up by $100?

© 2018 Quantitative Analysis of Investor Behavior 5

Harry figured that this difference could amount to a great deal of money in 20

years when he retires so he was not happy and called the number on his

statement for an explanation. Harry learned the important lesson that while the

balance of $2,350 was his, other figures had nothing to do with his account.

The 10% return applied only to investments that were in place from the start of

the quarter to the end of the quarter and since his came in at different times

the magical money was not as much. Harry’s total contribution for the quarter

would have to be made on the first day of the quarter for the entire 10% to

apply. Even if Harry had the money, this day one investment could not be done

due to constraints of the 401(k) plan. Harry concluded that the 10% really did

not apply to his account, even though it was on his statement!

Additionally, Harry found from the friendly representative at the number on his

statement that there were a number of other factors that were not shown,

which also lowered the magical figure. He was totally confused after learning

that his money was allocated and not fully invested, that there were expenses

not shown on his statement and that he was paying trading costs and fees that

were only shown in legal disclosures.

The 10% return on his statement did not reflect the fact that only 65% of his

account was invested in comparable stocks. The remaining 35% was held in low

yielding bonds and in cash. This means that it would be impossible to earn the

10% on over one third of his money! The representative explained that this is

done to limit his losses when the markets went down. Harry saw the benefit but

still felt that the 10% on his statement was misleading. By this time Harry had

been on the phone for half an hour and the representative was becoming less

friendly.

Harry then tried to understand what the expenses were and why they were not

shown on his statement. Harry was comfortable after learning that the

expenses covered items like administrative costs, record keeping, managing

investments, and for the services of an advisor. He remained concerned that

these expenses were not reflected in the 10% return shown on his statement.

He asked the representative,

“Why show the 10% if you know it is wrong?”

The representative’s frustration was growing.

© 2018 Quantitative Analysis of Investor Behavior 6

Harry was not giving up because he wanted to get the whole story so he asked about the trading costs. He immediately understood that there was buying and selling of investments and that commissions had to be paid when transactions occurred. Harry was becoming angry when he realized that these commissions were not reflected in the 10% on his statement! It is all the representative could do to calm Harry down. His concerns had grown to accusations of illegal activity! Harry had to hear the end of this. What additional fees apply to his account that are not included in the elusive 10%? Harry learned that there were fees that apply if he were to take out a loan or had a personal hardship and had to withdraw some funds. Harry thought this unfair, but it would be his choice to take the loan or withdrawal. Harry learned about something else that he thought would answer many of his concerns but there was yet another cost and burden on him. The representative described the self-directed brokerage account. This would mean that Harry need not use the low yielding investments if he chose not to. He could use very low expense investments like ETFs and Index funds. The trading commissions would be lower. Harry was not so happy to find that the self- directed brokerage meant he would have to actually enter every investment himself and if he made a mistake it would be his loss. Furthermore, the cost of this type of account would exceed what Harry was currently paying. By now Harry and the representative had been on the phone for an hour and a half and both were totally stressed out. Harry thanked the representative who had confused him and decided to be thankful for the magical $100 and forget about the possibility of earning any more. Life went on for Harry until one statement showed that his balance was actually less than it was on the previous statement. By now Harry’s balance had grown to $50,000 on the previous statement and the new statement showed only $47,500. How was this possible? Harry had not withdrawn any money. In fact $2,250 was added to his account. To make matters worse, the market had gone down by 4% but Harry’s balance went down by 5%. Harry again called the number on the statement and learned that the expenses, trading costs and fees were being incurred, even when Harry’s account was losing money. © 2018 Quantitative Analysis of Investor Behavior 7

What was Harry to do? By this time he realized that he was not earning as much

as was possible but the taxes and penalties of withdrawing his money made it

impractical… He was trapped!

Harry was now committed to avoiding future surprises. He wanted to

understand what might be in store for him in the future. What if he changes

jobs? What happens when he retires?

By this time Harry had become famous in the phone center. He had won the

contest multiple times for time spent on the phone! But Harry remained

undaunted.

Harry found that changing jobs could cost him money.

First was the “unvested” portion of his account that he would lose. At the time

Harry made the inquiry, his unvested balance was $25,000. Yes, that was a

nasty surprise that changing jobs would cost $25,000. But that’s not all. If Harry

decided to take the money out of the old employer’s plan, he would owe taxes

on that money plus a 10% penalty unless it was reinvested in 60 days.

The taxes and penalties could be avoided if the new employer permitted Harry

to invest the money in the new employer’s plan. This is a great solution if the

new employer’s plan is as good and cost no more than the old plan.

The other option is to shop for a “Rollover IRA”. Harry could transfer his plan

money into this account, avoid the taxes and penalties and never have to worry

about future job changes. The problem here, Harry found out, is that these

“Rollover IRAs” could cost as much as twice as much as the 401(k) plan.

Harry kept wondering,

“When does all this end?” Unfortunately, the answer was:

“Not yet.”

When Harry decides to retire he will face a new set of issues. With some

careful planning beforehand, Harry can avoid some of these.

The first problem Harry will face is taxes. As currently configured (the usual

practice), Harry will owe taxes on every dollar he withdraws from his

retirement plan. This is treated as ordinary income and is subject to

withholding, just like his paycheck is. Ouch!

© 2018 Quantitative Analysis of Investor Behavior 8But there is an alternative that Harry can use to avoid this nasty retirement surprise. Instead of using a regular 401(k), Harry could use a Roth 401(k) if his employer offers it. With the Roth, Harry pays the taxes on the contributions and at retirement can withdraw the contributions and all the appreciation tax free. This is an attractive option if Harry is willing to pay the taxes along the way because all the growth (the magical money) is tax free! The next problem is outliving his retirement funds. Surely, if Harry decides to spend like a drunken sailor after he retires, his funds won’t last very long. But even if Harry controls his spending, he could live to use up his entire account. In addition to controlled spending, two other actions can help. Harry can invest wisely so that his retirement funds continue to grow during his retirement years. This usually requires an investment strategy that is connected with the spending controls. Such an arrangement adjusts spending to what investments can sustain. Another action is for Harry to create his personal pension plan that will continue to pay him for as long as he lives. This is called an annuity and is more expensive than the sustainable spending described above. However, it eliminates the risk of running out of funds. © 2018 Quantitative Analysis of Investor Behavior 9

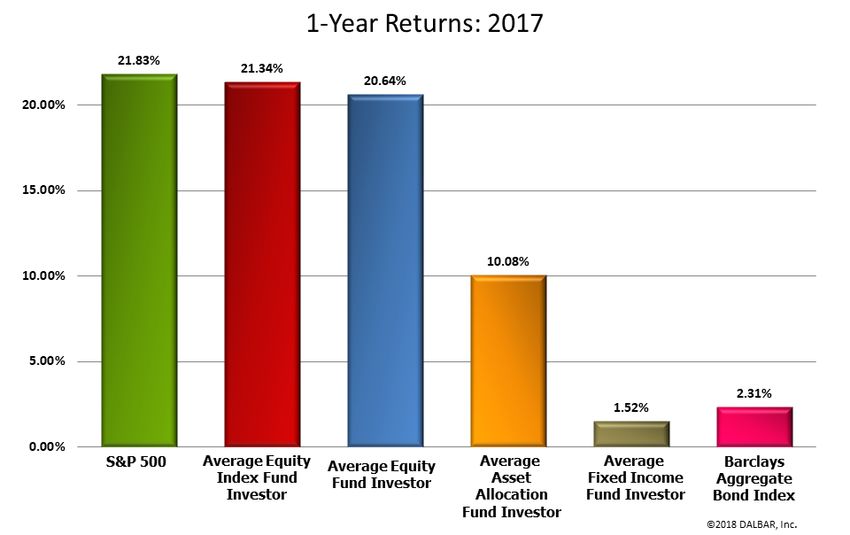

Executive Summary In 2017, the Average Equity Fund Investor underperformed the S&P 500 by 1.19% (20.64% vs. 21.83%). The Average Equity Fund Investor was outperforming the S&P 500 by a slim margin entering the month of October before underperforming the final 3 months of the year. The Average Equity Fund Investor’s underperformance can be entirely attributed to the 4th quarter. Two of the three best performing months for the S&P 500 (October and November) coincided with relatively large net outflows of assets. The Average Equity Index Fund Investor underperformed the S&P 500 by 0.49% (21.34% vs. 21.83%) but outperformed the Average Equity Fund Investor by 0.70% (21.34% vs. 20.64%). In 2017, the Average Fixed Income Fund Investor underperformed the BloombergBarclays Aggregate Bond Index by 0.79 (1.52% vs. 2.31%). The Average Asset Allocation Fund Investor earned a return of 10.08 in 2017. Just about splitting the difference between the Average Equity Fund Investor return (20.64%) and the Average Fixed Income Fund Investor return (1.52%). When examining funds by capitalization and style, the Average Growth Fund Investor emerged as the clear winner. The Average Large Cap Growth Fund Investor earned 29.45%, while the Average Small Cap Growth Fund Investor earned 25.43%, and the Average Mid Cap Growth Investor earned 24.25% for the year. All growth fund investors outperformed all value and blend investors. The Average Small Cap Value Fund Investor was the worst performing capitalization and style fund investor, earning only 10.82% on the year. This performance was only marginally better than the Average Asset Allocation Investor (whose portfolios are comprised of both equity and fixed income). When examining specific sector funds, the Average Technology Fund Investor (35.68%) and the Average Healthcare Fund Investor (23.45%) emerged as the highest performing of all the sector fund investors. Investments traditionally associated with safety were out of favor in 2017 and consequently the Average Natural Resources Fund Investor, Average Utilities Fund Investor and Average Precious Metals Fund Investor were the 3 poorest performing sector fund investors. © 2018 Quantitative Analysis of Investor Behavior 10

The Average Target Date Fund Investor outperformed the Average Asset Allocation

Fund Investor by 6.84% (16.92% vs. 10.08%). This can be explained in part by the

fact that net cash flow for Target Date Funds was decidedly positive throughout the

year while cash flows of asset allocation funds was mostly negative despite the bull

market.

Equity fund Retention Rates rose by almost 3 months, from an average of 3.80 years

in 2016, to an average of 4.03 years in 2017.

Fixed income fund Retention Rates rose over 4 months, from an average of 3.09

years in 2016, to an average of 3.45 years in 2017.

Asset allocation fund Retention Rates rose by over six months in 2017, pushing from

4.09 years to 4.65 years.

Average

Average Average Asset Bloomberg-

Fixed

Equity Fund Allocation Inflation S&P 500 Barclays

Income Fund

Investor Fund Investor Aggregate

Investor

Bond Index

(%) (%) (%) (%) (%)

(%)

20 Year 5.29 0.44 2.58 2.15 7.20 4.60

10 Year 4.88 0.48 2.52 1.64 8.50 3.31

5 Year 10.93 -0.40 5.41 1.48 15.79 1.27

3 Year 8.12 -0.05 3.85 1.71 11.41 1.40

12 Month 20.64 1.52 10.08 2.11 21.83 2.31

© 2018 Quantitative Analysis of Investor Behavior 112017 Year in Review

Q1 – Racing out of the Gate

Investors were greeted to the year 2017 with an S&P return of nearly 2% in January and

then almost 4% in February. As it turned out, the first 2 months of 2017 for investor

returns were a mirror image of the last 2 months of 2016 for the S&P 500. In January, the

S&P 500 was similar to the previous month’s return (only -0.08% lower than December)

but the Average Equity Fund Investor was able to improve its gains by over 2% and

outperform the index and the Average Index Investor.

The previous year, the market rose steadily in November and December despite

uncertainty stemming from the recent presidential election. Equity investors were

burned in the fourth quarter, underperforming the S&P index in all 3 months.

In 2017, the Average Equity Fund Investor was able to outperform the S&P 500 in 2 out

of the 3 months. The markets were calm throughout the 1st quarter, displaying a lull in

volatility that began the previous November and that would extend until the end of the

year.1

1

See CBOE Market Volatility Index (VIX)

© 2018 Quantitative Analysis of Investor Behavior 12Q2 – Slow and Steady The markets would continue to rise in the second quarter without any significant disruptions. Each month saw slow and steady gains of the equity markets while volatility remained low. The Average Equity Fund Investor and the Average Equity Index Fund Investor both outperformed the S&P 500 in April. It would be the second straight month that they would do so. The Average Equity Fund Investor would continue to outperform the S&P for the 3rd month in a row in May while the Average Equity Index Fund Investor would slightly lag the index that month. June was a relatively flat month where the Average Equity Index Fund Investor prevailed slightly over the overall Average Equity Fund Investor and the S&P 500. Q3 – Average Investors Leading the Race The third quarter would see two months where the S&P 500 gained 2.06% and a flat month sandwiched in between. Volatility remained low, so there were very few market swings to help or harm the Average Investor’s return. The Average Equity Fund Investor return was tightly correlated to the S&P 500 during the quarter and by the end of September had not significantly trailed the S&P 500 since February (trailed the S&P 500 by -.04% in June and -0.18% in August and outperformed S&P 500 in March, April, May July and September). © 2018 Quantitative Analysis of Investor Behavior 13

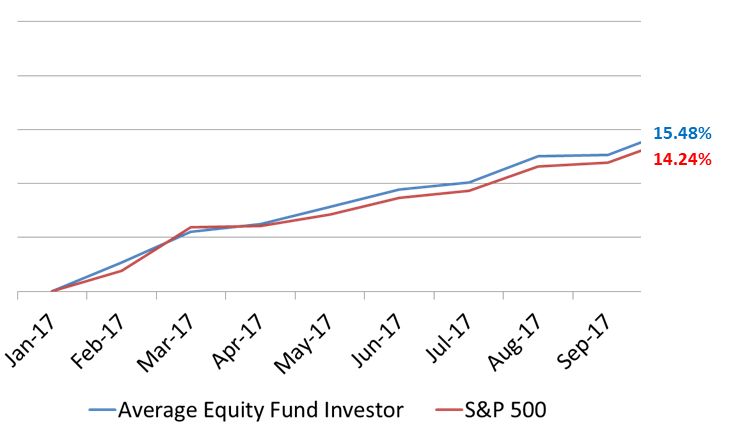

Heading into the 4th quarter, the Average Equity Fund Investor was standing strong with a YTD return of 15.48% vs and S&P 500 YTD return of 14.24%. The Average Equity Fund Investor was on the verge of outperforming the market for a calendar year for the first time since 2009 when the S&P 500 advanced 26.46% and the Average Equity Fund Investor earned a whopping 32.10%. Q4 – Average Investor Can’t Hang on for the Win The fourth quarter of each year has been a historically poor period for the Average Investor. In 2017, the Average Equity Fund Investor struggled in the fourth quarter for the second straight year, underperforming the S&P all 3 months and ultimately underperformed the major equity index for the year. It was a better quarter to be an equity index investor, as the Average Equity Index Fund Investor outperformed the Average Equity Fund Investor in all three months and significantly in December. © 2018 Quantitative Analysis of Investor Behavior 14

The year 2017 was a year friendly to the Average Investor. The trend from the previous year continued and investors had little to shake their confidence along the way. Gains were steady, volatility was low, and the Average Equity Fund Investor left very little on the table in 2017. © 2018 Quantitative Analysis of Investor Behavior 15

Taking a Closer Look

… Examining the Various Average Fund Investors

For years, DALBAR’s QAIB report has

looked at equity and fixed income fund

investors to see how their actual

market gain/loss compares to reported

market returns. In 2008, DALBAR

introduced the Average Asset

Allocation Investor, covering funds

that invest in a mix of equity and fixed

income securities. In 2018, DALBAR is

introducing for the first time Average

Fund Investors for various fund

classifications.

With valuations fair to high2,

anticipation of lowered taxes, and the

market presumably anticipating

economic expansion, growth stocks

ruled the day in 2017. Large cap

growth fund investors earned almost

30% on the year, beating the S&P 500

by a wide margin (29.45% vs. 21.83%).

2

According to YCarts.com, average P/E ratios of the S&P 500 in 2017 were in the range of 23-24.

© 2018 Quantitative Analysis of Investor Behavior 16The average technology fund investor led all investor categories for 2017 and earned 10% more than any other sector fund investor. Sectors associated with safety such as precious metals and natural resources were at the bottom of the list. © 2018 Quantitative Analysis of Investor Behavior 17

Short-Term Focus and Market Timing Irrational investor behavior is typically triggered by some sort of stimulus. A geo- political event, previous market experiences, news stories, or a hot tip from a colleague can distract an investor from his or her long-term goal. But investor underperformance emanates only partially from poor decision-making; other factors such as fees, the need for cash, and the unavailability of funds to invest can all lead to an investor lagging the overall market. For example, if Harry has to withdraw some portion of his investments to cover medical costs. That can hardly be considered irrational investor behavior. Harry may miss a market advance that will plague his portfolio for years to come but it was not due to any of the psychological factors we have discussed over the years. Or perhaps Harry does not have money to invest due to his personal circumstances, but when he gets his Federal tax return he plans to put it all into his IRA. If the market tanks in the first quarter before Harry contributes his tax refund, he looks like a genius. If he misses a 1st quarter bull run, it looks like he timed the market all wrong. The truth was that Harry did what he could do and was at the mercy of Lady Luck. While underperformance is not due entirely to irrational investor behavior, there are two behaviors for which evidence shows time and time again that fall outside of what would be generally accepted as a prudent investment strategy. The behaviors are the tendency to move into and out of investments too frequently and the tendency to time the market. The data shows that the average mutual fund investor has not stayed invested for a long enough period of time to execute a long term strategy. In fact, they typically stay invested for just a fraction of a market cycle. QAIB has also shown numerous instances in which market conditions create a shift in cash flows which run counter to the eventual direction of the market. © 2018 Quantitative Analysis of Investor Behavior 18

Retention Rates Over the past 20 years, equity mutual fund investors have seldom managed to stay invested for more than 4 years. When they have done so, it has generally been during periods of bull markets. Equity fund retention rates surpassed the four year mark from 2004-2006 and would do so again in 2013-2015. In 2016, equity fund retention rates dipped below 4 years to 3.80 years but in 2017 rebounded back over the 4-year mark (4.03 yrs.). After exhibiting retention rates below the 3-year mark 2013-2015, the Average Fixed Income Fund Investor surpassed the 3.0 year mark in 2016 (3.09 yrs.) and continued to forge higher in 2017 to its highest Retention Rate (3.45 yrs.) since 2006. Asset allocation mutual fund investors have generally stayed invested longer than their equity and fixed income investor counterparts. Asset allocation fund retention rates have stood above the four year mark for eight straight years. In 2016, asset allocation fund Retention Rates decreased to 4.09 years, nearly falling below the 4.0 year mark for the first time since 2008. However, in 2017, the © 2018 Quantitative Analysis of Investor Behavior 19

Average Asset Allocation Investor followed the trend of other Average Investors and stayed put. Retention Rates for the 2017 Average Asset Allocation Investor rebounded to the levels before 2016 where fund redemptions accelerated. The market conditions of 2017 caused the expected effect on fund Retention Rates. Investors tend to withdraw funds when markets decline or there is imminent fear of a crash or correction. The effect of the increased withdrawals is to reduce retention rates. The Retention Rates plummeted in 2016 as the Average Investor was not comfortable where they stood. The Average Investor was more comfortable in 2017 and for good reason, the markets gave no reason to be concerned, so investors hung on and made their money right alongside the market indices. © 2018 Quantitative Analysis of Investor Behavior 20

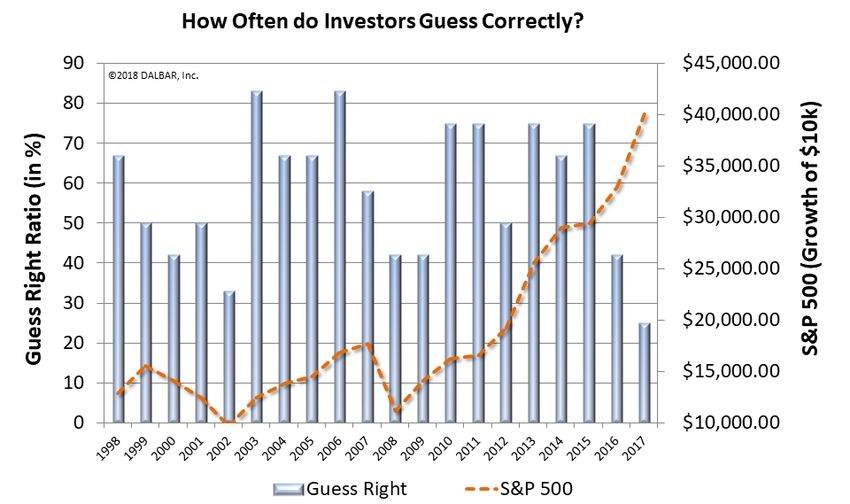

Market Timing The retention rate data for equity, fixed income and asset allocation mutual funds strongly suggests that over the long-term, investors lack the patience to stay invested in any one fund for much more than four years. Even when the markets are in perfect harmony, which is how one might categorize 2017, Retention Rates still do not suggest sufficient holding periods. Investors displayed more patience in 2017, but only from a relative standpoint. Over a quarter of equity funds’ assets are being redeemed and replaced with new purchases each year on average over the last 20 years. Low retention rates are not a result of investors investing their money for a few years and then divesting forever. The growth of overall mutual fund assets over time suggests much of the money being redeemed is moving from one investment to another. It can be theorized that much of the money movement suppressing Retention Rates can be attributed to the Average Investor’s tactical strategies and market timing. DALBAR continues to analyze the investors’ market timing successes and failures through their purchases and sales. This form of analysis, known as the Guess Right Ratio, examines fund inflows and outflows to determine how often investors correctly anticipate the direction of the market the following month. Investors guess right when a net inflow is followed by a market gain, or a net outflow is followed by a decline. Investors have guessed right 50% of the time or more 14 out of the last 20 years, but 2017 was not one of them. Unfortunately for the Average Investor, guessing right did not produce superior gains over the years because the dollar volume of bad guesses exceeds the volume of right guesses. Even one month of wrong guesses can wipe out several months of right ones. In 2017, investors guessed right only 3 out of the 12 months (25%) despite a consistently up-trending market. © 2018 Quantitative Analysis of Investor Behavior 21

While Retention Rates suggest a decrease in redemptions, total redemptions actually outweighed total sales in 8 out of the 12 months. So while investors were less likely to redeem their funds, they were even less likely to add more funds. Perhaps this signifies distrust with the current bull market where investors are unwilling to continue investing at the same rate during all-time market highs. Fortunately for the Average Investor, this ostensible trepidation did not lead to significant underperformance, as the Average Equity Fund Investor only underperformed the S&P 500 by 1.19%. As we examined earlier in this report, the 1.19% underperformance by the Average Equity Fund Investor occurred primarily in the 4th quarter. In October, the S&P was up over 2.3%, the second best month of the year to that point. At that time, net fund flows were at its second lowest level of the year. Money flows and the market direction were uncorrelated. That continued to an even greater extent in November, as net outflows continued to accelerate and the market continued to rise at an even greater pace. For the second straight month, the second best month of the year (November surpassed October for that © 2018 Quantitative Analysis of Investor Behavior 22

title) coincided with the second greatest outflow of the year (November

surpassed October for that title as well).

December was (and typically always is) the month that experiences the largest

net inflow of funds. Unfortunately when investors were piling money back into

mutual funds, the S&P 500 was having an unremarkable month in comparison to

the other months of the year. In December, net inflows were far and away

greater than any other month. December’s +0.29% net inflow was nearly triple

the second largest inflow that took place in June. However the S&P 500 earned

only 1.11%, below its average monthly return of 1.66% in 2017.

Month-by-Month Look at

Equity Fund Investors in 2017

Average

Net Inflow/ Equity Fund S&P 500 Investor

Month

Outflow Investor Return Gap

Return

Jan -0.08% 2.67% 1.90% 0.77%

Feb 0.05% 2.80% 3.97% -1.17%

Mar -0.03% 0.67% 0.12% 0.55%

Apr -0.12% 1.48% 1.03% 0.45%

May 0.04% 1.51% 1.41% 0.10%

Jun 0.10% 0.59% 0.62% -0.03%

Jul -0.12% 2.21% 2.06% 0.15%

Aug -0.16% 0.13% 0.31% -0.18%

Sep -0.05% 2.15% 2.06% 0.09%

Oct -0.14% 1.93% 2.33% -0.40%

Nov -0.15% 2.11% 3.07% -0.96%

Dec 0.29% 0.29% 1.11% -0.82%

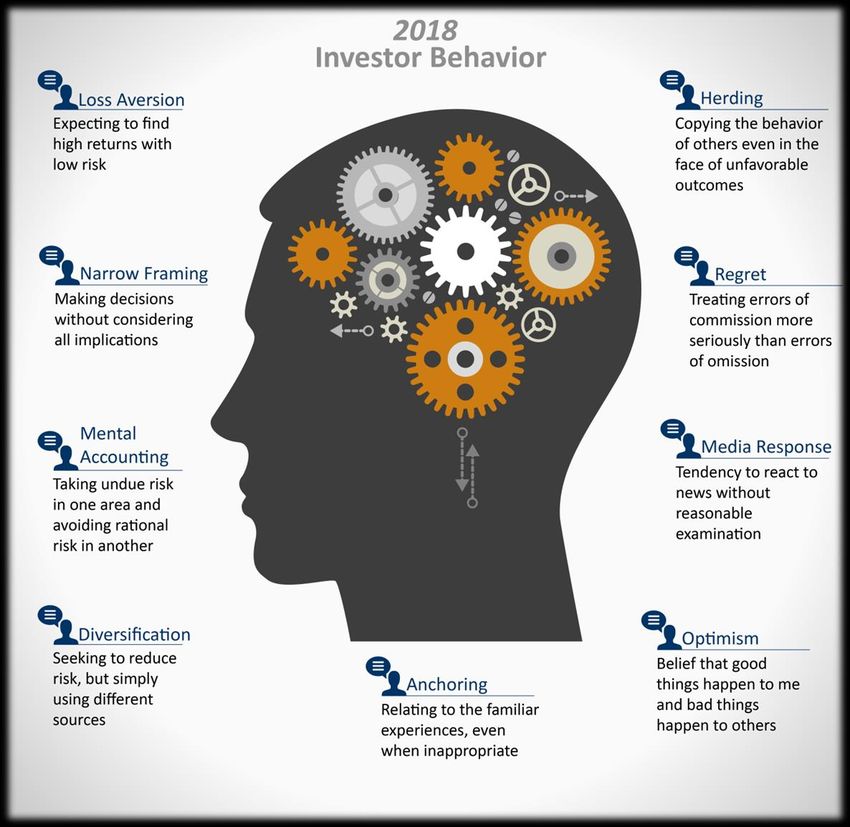

© 2018 Quantitative Analysis of Investor Behavior 23BEHIND THE NUMBERS…

INVESTOR PSYCHOLOGY

When discussing investor behavior it is helpful to first understand the specific

thoughts and actions that lead to poor decision-making. Investor behavior is not

simply buying and selling at the wrong time, it is the psychological traps, triggers

and misconceptions that cause investors to act irrationally. That irrationality leads

to buying and selling at the wrong time, which leads to underperformance.

There are 9 distinct behaviors that tend to plague investors based on their

personal experiences and unique personalities.

© 2018 Quantitative Analysis of Investor Behavior 24APPENDICES 1. Year-by-Year Investor Returns 2. Glossary 3. QAIB Products 4. Investor Return Calculations: An Example 5. Rights of Usage and Sourcing Information © 2018 Quantitative Analysis of Investor Behavior 25

YEAR-BY-YEAR INVESTOR RETURNS

The following table shows the one-year investor return since inception from 1985

to 2017. These calculations assume that investors start investing on January 1 of

each year and withdraw their investments on December 31. The effect of

compounding across years is therefore lost. Additionally, because of the year-by-

year nature of the calculation, returns cannot be asset weighted.

Avg. Avg. Avg.

Year

Equity Fixed Income Asset Allocation

1985 27.79% 11.86% 20.50%

1986 17.53% 7.94% 5.97%

1987 0.51% -0.84% 6.03%

1988 17.88% 4.70% -1.78%

1989 23.51% 6.63% 20.77%

1990 -5.62% 2.18% 6.81%

1991 29.40% 11.94% 17.25%

1992 7.28% 8.60% 1.13%

1993 15.93% 7.87% 16.66%

1994 -0.02% -4.99% -5.48%

1995 26.52% 14.37% 25.36%

1996 17.33% 7.71% 11.51%

1997 20.59% 8.14% 16.02%

1998 34.48% 5.92% 32.40%

1999 26.58% -5.68% 5.47%

2000 -10.20% 4.17% 1.39%

2001 -14.92% -0.75% -5.15%

2002 -21.86% 2.20% -10.56%

2003 30.08% 4.31% 16.80%

2004 12.60% 1.30% 8.01%

2005 8.45% -0.58% 1.95%

2006 14.65% 2.09% 11.12%

© 2018 Quantitative Analysis of Investor Behavior 26Avg. Avg. Avg.

Year

Equity Fixed Income Asset Allocation

2007 7.33% 0.80% 3.47%

2008 -41.77% -11.55% -31.35%

2009 32.10% 9.78% 19.31%

2010 14.11% 3.05% 8.83%

2011 -5.73% 1.84% -2.60%

2012 15.62% 4.70% 8.53%

2013 25.69% -3.47% 13.72%

2014 5.51% 1.19% 2.60%

2015 -2.28% -3.11% -3.48%

2016 7.26% 1.23% 5.48%

2017 20.64 1.52% 10.08%

© 2018 Quantitative Analysis of Investor Behavior 27GLOSSARY Average Investor The average investor refers to the universe of all mutual fund investors whose actions and financial results are restated to represent a single investor. This approach allows the entire universe of mutual fund investors to be used as the statistical sample, ensuring ultimate reliability. [Average] Investor Behavior QAIB quantitatively measures sales, redemptions and exchanges (provided by the Investment Company Institute) and describes these measures as investor behaviors. The measurement of investor behavior is the net dollar volume of these activities that occur in a single month during the period being analyzed. [Average] Investor Return (Performance) QAIB calculates investor returns as the change in assets, after excluding sales, redemptions, and exchanges. This method of calculation captures realized and unrealized capital gains, dividends, interest, trading costs, sales charges, fees, expenses and any other costs. After calculating investor returns in dollar terms (above) two percentages are calculated: Total investor return rate for the period Annualized investor return rate Total return rate is determined by calculating the investor return dollars as a percentage of the net assets, sales, redemptions and exchanges for the period. Annualized return rate is calculated as the uniform rate that can be compounded annually for the period under consideration to produce the investor return dollars. Average Equity Fund Investor The Average Equity Fund Investor is comprised of a universe of both domestic and world equity mutual funds. It includes growth, sector, alternative strategy, value, blend, emerging markets, global equity, international equity, and regional equity funds. © 2018 Quantitative Analysis of Investor Behavior 28

Average Equity Fixed Income Investor The Average Fixed Income Fund Investor is comprised of a universe of fixed income mutual funds, which includes investment grade, high yield, government, municipal, multi-sector, and global bond funds. It does not include money market funds. Average Asset Allocation Investor The Average Asset Allocation Fund Investor is comprised of a universe of funds that invest in a mix of equity and debt securities. Average [Sector] Fund Investor The Average [Sector] Fund Investor is comprised of a universe of funds that invest solely in companies that operate in related fields or specific industries. The following Average Sector Fund Investors were referenced in this report: Consumer, Health, Financial, Tech/Telecom, Real Estate, Precious Metals, Utilities, and Natural Resources. Average [Capitalization and Style] Fund Investor The Average [Capitalization and Style] Fund Investor is comprised of a universe of funds that are categorized by the types of companies in which they invest: Small-cap mutual funds invest primarily in companies with market capitalizations of up to $2-2.5 billion. Mid-cap mutual funds invest primarily in companies with market capitalization that generally ranges from $1 billion to $7 billion or in companies with both small and medium market capitalization. Large-cap mutual funds invest primarily in companies with market capitalizations which are generally more than $5 billion or in companies with both medium and large market capitalizations. Growth mutual funds invest primarily in common stock of growth companies, which are those that exhibit signs of above-average growth, even if the share price is high relative to earnings/intrinsic value. Value mutual funds invest primarily in common stock of value companies, which are those that are out of favor with investors, appear underpriced by the market relative to their earnings/intrinsic value, or have high dividend yields. Blend mutual funds invest primarily in common stock of both growth and value companies or are not limited to the types of companies in which they can invest. Average Equity Index Fund Investor The Average Equity Index Fund Investor is comprised of a universe of funds that are designed to track the performance of a U.S. equity market index. © 2018 Quantitative Analysis of Investor Behavior 29

Average Target Date Fund Investor The Average Target Date Fund Investor is comprised of a universe of funds that follow a predetermined reallocation of assets over time based on a specified target retirement date. Average Alternative Strategies (Alt-) Fund Investor The Average Alternative Strategies (Alt-) Fund Investor is comprised of a universe of funds that employ alternative investment approaches like long/short, market neutral, leveraged, inverse, or commodity strategies to meet their investment objective. The following Average Alternative Strategies Fund Investors were referenced in this report: Alt-Domestic Equity, Alt-World Equity, Alt – Asset Allocation (“AA”), and Alt-Multisector Bond. Guess Right Ratio The Guess Right Ratio is the frequency that the average investor makes a short- term gain. One point is scored each month when the average investor has net inflows and the market (S&P 500) rises in the next month. A point is also scored when the average investor has net outflows and the market declines in the next month. The ratio is the number of points scored as a percentage of the total number of months under consideration. Retention Rate Retention Rate reflects the length of time the average investor holds a fund if the current redemption rate persists. It is the time required to fully redeem the account. Retention rates are expressed in years and fractions of years. Inflation Rate The monthly value of the consumer price index is converted to a monthly rate. The monthly rates are used to compound a “return” for the period under consideration. This result is then annualized to produce the inflation rate for the period. © 2018 Quantitative Analysis of Investor Behavior 30

QAIB Products © 2018 Quantitative Analysis of Investor Behavior 31

© 2018 Quantitative Analysis of Investor Behavior 32

INVESTOR RETURN CALCULATION…

AN EXAMPLE

Investor return is calculated by measuring the actual gains that investors realize.

The following example is hypothetical:

Step 1: Compute Monthly Net Change

1/31 Assets - 12/31 Assets =

The equity assets at the end of 1/31 are subtracted from Change

the assets at 12/31 to determine the change for the month.

The change is the net of investor actions [new investments 5196 – 4940

(which includes the reinvestment of dividends and capital = 256

gain distributions), withdrawals (redemptions), exchanges

(In $ Billions)

in and out], changes in market value, net of loads, fees,

expenses, commissions, etc.

Monthly Change 256 Step 2: Compute Change in Market Value

Minus New Investments -123 The change in assets due to investor actions

Plus Withdrawals +105

Minus Exchanges in -25 are deducted from monthly net change,

Plus Exchanges out +12 resulting in the market value change that is

Equal Net Change in Market net of loads, fees, expenses, commissions, etc.

Value 225 The net change in market value is the return

(In $ Billions)

earned by the investor for the month, after all

fees and expenses are paid. This could be either a gain or loss.

January 225

Step 3: Calculate Total for Period February -28

The calculation is repeated for each month to develop the total for March +106

April +106

the periods for which the investor return is being measured – (1, 3, May -213

5, 10 and 20 years.) June -5

July -20

August +119

September +88

October +195

November +154

December +30

Total for period 757

© 2018 Quantitative Analysis of Investor Behavior 33The example illustrates a one-year period. Note that the average investor

suffered losses in February, May, June and July but these were more than offset

by the gains in the other months.

Step 4: Determine Cost Basis

Opening Assets 4940

The cost basis is the opening balance for the period adjusted by Plus New Investments +1288

the investor actions (new investments, withdrawals, exchanges Minus Withdrawals -1150

in and out). Plus Exchanges in +206

Minus Exchanges out -128

Equal Cost Basis 5156

(In $ Billions)

Investor Return $ / Cost Basis = Step 5: Calculate Investor Return Percentage

% Return

Dividing the investor return dollars

757 / 5156= 15% calculated in Step 3 by the cost basis in

Step 4 gives the total investor return

(In $ Billions)

percentage.

Step 6: Find Annualized Rate of Return

Annualized return is then calculated. This is the single rate that can be

compounded for each year to produce the same effect as the varying monthly

rates.

Since the period in our example is only one year, the annualized investor return is

the same as the total investor return.

The formula used to calculate annualized return is:

Annualized Return =

[% Return ^(1/# of years)]-1

© 2018 Quantitative Analysis of Investor Behavior 34RIGHTS OF USAGE AND SOURCING INFORMATION

When purchasing the Full Study of the Quantitative Analysis of Investor Behavior

(“Document”), DALBAR, Inc. (“Licensor”) grants purchaser (“Licensee”) the rights

to incorporate certain materials contained within the document entitled, in

whole or in part, into other works (“Derivative Works”) on the condition that

Licensee makes required regulatory disclosures and sources QAIB and DALBAR as

appropriate.

1. Licensee shall own the copyright in Derivative Works.

2. Licensee shall not redistribute, provide access to, share or transfer printed or

electronic copies of the Document to anyone outside the Licensee’s

organization.

3. All right, title, and interest in the Document, including without limitation, any

copyright, shall remain with Licensor.

4. These rights are conveyed to purchasers for their own use and are limited to

their own specific publications.

Source example: “Quantitative Analysis of Investor Behavior, 2018,” DALBAR, Inc. www.dalbar.com

Applicable Disclosures Examples:

Equity benchmark performance and systematic equity investing examples are represented by the Standard &

Poor’s 500 Composite Index, an unmanaged index of 500 common stocks generally considered representative

of the U.S. stock market. Indexes do not take into account the fees and expenses associated with investing,

and individuals cannot invest directly in any index. Past performance cannot guarantee future results.

Bond benchmark performance and systematic bond investing examples are represented by the Barclays

Aggregate Bond Index, an unmanaged index of bonds generally considered representative of the bond

market. Indexes do not take into account the fees and expenses associated with investing, and individuals

cannot invest directly in any index. Past performance cannot guarantee future results.

Average stock investor, average bond investor and average asset allocation investor performance results are

based on a DALBAR study, “Quantitative Analysis of Investor Behavior (QAIB), 2016.” DALBAR is an independent,

Boston-based financial research firm. Using monthly fund data supplied by the Investment Company Institute,

QAIB calculates investor returns as the change in assets after excluding sales, redemptions and exchanges.

This method of calculation captures realized and unrealized capital gains, dividends, interest, trading costs,

sales charges, fees, expenses and any other costs. After calculating investor returns in dollar terms, two

percentages are calculated for the period examined: Total investor return rate and annualized investor return

rate. Total return rate is determined by calculating the investor return dollars as a percentage of the net of

the sales, redemptions, and exchanges for the period.

© 2018 Quantitative Analysis of Investor Behavior 35You can also read