FRAUD RISK MANAGEMENT IN RELIGIOUS INSTITUTIONS: PRACTICAL CHALLENGES AND SOLUTIONS - icpau

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FRAUD RISK MANAGEMENT IN RELIGIOUS

INSTITUTIONS: PRACTICAL CHALLENGES

AND SOLUTIONS

RELIGIOUS INSTITUTIONS

ICPAU FEBRUARY 2018

PRESENTED BY;

ALEX M.B. TWESIGYE

(MBA, BSC, ACCA, CPA-U, CISA & CGAP

LLB – ON-GOING))

atwesigye@alines.co.ug

twesigye2005@yahoo.com

075/77/71-2470088

PRESENTATION OUTLINE

Agenda 1 Definitions of key terms

2 Is Fraud in Religious Institutions Real?

3 Why Religious Institutions?

4 Challenges and Potential Solutions

5

Conclusion

Definition of key terms o Religious Institution: House of worship plus its controlled activities. Christians, Moslems, Jews, … o Fraud: is any intentional act or omission designed to deceive others, resulting in the victim suffering a loss and/or the perpetrator achieving a gain. o Risk: Exposure to the possibility of loss or injury o Management: Systematic process of minimizing potential loses / maximizing gains

Is Fraud in Religious Institutions

Real?

Brazil: Bishop Edir Macedo, Head of the Universal

Church of the Kingdom of God, and 9 of his

associates were charged with embezzling more than

$2 billion.

Canada: Televangelists Ron and Reynold Mainse

allegedly recruited investors in a Ponzi scheme.

China: A whistleblower goes to jail for speaking out

after donations for earthquake victims were stolen.

Is Fraud in Religious Institutions

Real?

Italy: Police confiscated 23 million euros in a Vatican

bank account as part of an investigation into money

laundering.

Ukraine: Pastor Sunday Adelaja charged with fraud

in promoting a business venture to his congregation

that lost $100 million.

United kingdom: Church treasurer Derek Klein

embezzled funds to pay for a stamp collection.Is Fraud in Religious Institutions

Real?

WHAT ABOUT IN UGANDA ????Why Religious Institutions? Willie Sutton, the depression- era bank robber, was asked why he kept robbing banks and he famously replied, "because that's where the money is." we expect thieves to be attracted to banks. By implication, …… because…

Why Religious Institutions? Anywhere money flows thieves and other financial parasites will gather to siphon some of it off for their own purposes. This means Christians, Jews and Muslims …… have a big challenge of fraud. Practice - most of these crimes are quietly hidden. the losses are written off or never even acknowledged, and the criminals are rarely prosecuted.

Why Religious Institutions? This presents PERFECT COMBINATION: MONEY AND SAFETY. Evolution theory. Parasitism is an inevitable feature of any thriving ecology. if there's a resource that's abundant, some species will inevitably evolve to make use of it and so it is with the social ecology.

Why Religious Institutions? Cultural evolution and sociology tell us the same thing about social resources (that is, money). Any time there is an abundant amount of money, the parasites on society, the thieves and financial leeches, will be drawn to it like flies.

What to do?

Why are Religious Institutions so

Vulnerable?

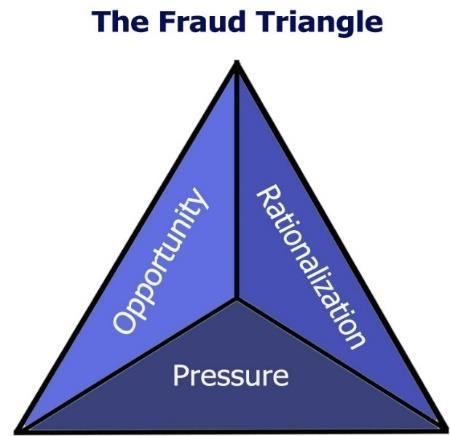

Donald

Cressey’s.

TriangleWhy are Religious Institutions so

Vulnerable?

PRESSURES AND RATIONALIZATION

Ministers, and other staff members in the institutions are

expected to work long hours on paupers’ wages for the

love of a deity, while mingling with the wealthiest of

society. These conditions can result into, desperation and

rationalization, such as “they owed it to me.”

Often, such people may face “non-shareable” financial

problems.Why are Religious Institutions so

Vulnerable?

OPPORTUNITY

ACFE’s reports show that fraud happens most frequently

in small entities with less than 100 employees — a

category that would include most houses of worship.

Because of their small size; Professionals not hired,

Experience not considered, little or no segregate of duties

or independent checks.Why are Religious Institutions so

Vulnerable?

OPPORTUNITY

Secondly, trust among employees and volunteers fuels

“church” engines. Because of the tight-knit culture,

family members and close friends are often hired, which

increases opportunities for collusion.

In most cases, a perception of consequences is not

created which is necessary to deter fraud.What should be on the radar?

FRAUD RISK ASSESSMENT

FRAUD ELEMENTS

People

Theft Act

Tools

Concealment

Processes

Methods

Focus on neutralising fraudster’s toolsPractical Challenges and Solutions Challenge. Trust. Because the work at these organizations centers on missions and philanthropic causes, it is their nature to trust and be forgiving. This creates a twofold problem: (1) these organizations may believe they are immune to fraud, and (2) it may go against religious principles to make accusations of wrongdoing. Possible Solution Possible to build accountability around trusted individuals.

Practical Challenges and Solutions Challenge. Ignoring Base Rates. Simply defined, base rates statistics show how likely an event is to occur. Despite being given the information that fraud is occurring in its industry, the institution chooses to ignore or associate with the group that will not be affected. For example, information that 20 percent of institutions will be a victim of fraud, it associates itself with the 80 percent group. Possible Solution Periodic Fraud Risk Assessments

Practical Challenges and Solutions Challenge. Overconfidence. Overconfidence is a result of two factors; a belief a person is better than others and an overestimation of the controls. There is also a belief that those involved in good deeds and noble causes are of like minds. Possible Solution Honest evaluation of controls

Practical Challenges and Solutions Challenge. Confirming Bias. Result of reliance on confirming evidence. People tend to believe only the information that supports the beliefs they already have and ignore information that contradicts this. An institution may develop complacency and believe that no one will embezzle from them because it never has happened in the past. Possible Solution Honest evaluation of exposures

Practical Challenges and Solutions Challenge. Fear of Prosecution. Religious institutions often have a difficult time accusing an individual of fraud and are particularly reluctant to take the appropriate action against these individuals. These institutions often believe they should show compassion against those who are in a difficult situation. Religious organizations also fear retaliation and possible civil action brought against them by the accused. Possible Solution Provision of adequate information

Practical Challenges and Solutions Challenge. Lack of Segregation of Duties. Lack of segregation is often a result of relying on a single individual to carry out responsibilities of the organization. Many religious organizations either lack the understanding basic concept of internal controls, and that an important control includes separation of duties or, inability to segregate duties is a result of the high level of trust that is given to individuals and the assumption that every individual is assumed to be of high moral character. Possible Solution Maker checker controls

Practical Challenges and Solutions Challenge. Lack of Qualified Individuals. As is typical in small companies, these institutions do not always hire employees with the appropriate experience and expertise. This can be attributed to the problem that the typical religious organization does not budget funds necessary to hire these qualified individuals. Possible Solution Budget and hire competent individuals

Practical Challenges and Solutions Challenge. Lack of Oversight Functions. Most rely on a volunteer board of directors or trustees to run their institution. In these situations it can cause an organization to be particularly vulnerable to fraud. Volunteer board have limitations. Possible Solution Minimal facilitation for boards

Practical Challenges and Solutions Challenge. Lack of Independent Audits. Lack of internal or external audits contribute to religious organizations’ vulnerability to fraud. Audits are more effective at deterring fraud than identifying it. Possible Solution Institute regular audits based on approved plans

Practical Challenges and Solutions Challenge. Moral decay. Society levels for what is acceptable behavior has seriously gone down. Possible Solution Right approval / disapproval

Practical Challenges and Solutions Challenge. Looks like religious institution. When in reality it is not Possible Solution Public scrutiny

Practical Challenges and Solutions Challenge. Lack of Internal Controls. Internal controls include the plans and methods used by an organization to safeguard assets. These controls are often cited as the single most important component to minimize the risk of fraud (Fraud Triangle). Possible Solution Implementation of basic internal controls (oversight, supervision, reporting, monitoring, segregation of duties and risk assessment)

CONCLUSIÓN

Thank you!

You can also read