FREQUENTLY ASKED QUESTIONS - VALUE ADDED TAX - BAHRAIN 25 DECEMBER 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FREQUENTLY ASKED QUESTIONS VALUE ADDED TAX - BAHRAIN 25 DECEMBER 2018

Contents

Contents

1. VAT eligibility and registration process ................................................... 6

1.1. How do I determine if my business needs to register? ........................................... 6

1.2. How is the registration threshold calculated? ......................................................... 7

1.3. Can I voluntarily register? ...................................................................................... 7

1.4. When calculating my annual supplies, do I include the revenue for each of the

stores / branches that fall under the company? ...................................................... 7

1.5. How do I register for VAT? ..................................................................................... 8

1.6. What information will the NBT require for VAT registration? ................................... 8

1.7. What happens after I have submitted by application to register for VAT to NBT? ... 8

1.8. What is my Tax Registration Number? ................................................................... 8

1.9. When will my VAT registration take effect? ............................................................ 9

1.10. What do I do with my VAT registration certificate? ................................................. 9

1.11. What should I do if there are changes in the registration information? ................... 9

1.12. If I am not established in Bahrain, will the introduction of VAT impact on me and

my business activities? .......................................................................................... 9

1.13. If I make exclusively zero rated supplies above the mandatory VAT registration

threshold do I need to register for VAT? ................................................................. 9

1.14. How do I apply for a registration exception to NBT? ............................................. 10

1.15. What if I fail to register on time? ........................................................................... 10

1.16. Can I register as a Tax Group? ............................................................................ 10

1.17. What are the requirements for mandatory deregistration? .................................... 10

1.18. What are requirements for voluntary deregistration? ............................................ 11

1.19. What documents should I provide in case of deregistration? ................................ 11

1.20. What are my obligations post-deregistration? ...................................................... 11

1.21. Can a VAT-registered business purchase Goods or Services from a business that

is not VAT-registered? ......................................................................................... 11

1.22. Is a sub-CR considered part of the same person or legal entity? ......................... 11

1.23. What is the VAT treatment of transactions between branches of the same legal

entity? .................................................................................................................. 12

1.24. Will I need a separate TRN for each branch under a single person or legal entity?

............................................................................................................................ 12

1.25. How can I register a Joint Venture? ..................................................................... 12

1.26. What if I made a mistake while submitting my VAT registration application? Can I

amend or re-apply? .............................................................................................. 12

2. VAT procedures and filing ....................................................................... 12

2.1. In general, when is Tax due on the supply of Goods and Services? ..................... 12

2.2. What is a Tax Return? ......................................................................................... 13

2.3. What is a Tax Period? .......................................................................................... 13

2.4. Can I change my Tax Period? .............................................................................. 14

2.5. When should I submit the Tax Return? ................................................................ 15

2.6. When shall we pay Tax due for the Taxable Period?............................................ 15

2.7. What should I declare in the Tax Return? ............................................................ 15

© Kingdom of Bahrain | Ministry of Finance

Contents

2.8. What are procedures for submitting the Tax Return? ........................................... 16

2.9. Can a Tax Return be amended? .......................................................................... 16

2.10. What should amended Tax Return include?......................................................... 17

2.11. How soon should submit amended Tax Return when I am become aware of the

error? Will there be fines associated with amendments?...................................... 17

2.12. What are my obligations under VAT invoicing? .................................................... 17

2.13. When should invoices be issued? ........................................................................ 17

2.14. What should a Tax Invoice contain?..................................................................... 17

2.15. How long do photocopies of all Tax Invoices need to be retained? ...................... 18

2.16. Can a bank statement be used as a Tax Invoice? ................................................ 18

2.17. When can a simplified Tax Invoice be issued? ..................................................... 18

2.18. What information should a simplified Tax Invoice include? ................................... 19

2.19. On which items can I recover VAT? ..................................................................... 19

2.20. Do I need to save any documents that are to be used for Input Tax deduction

purposes? ............................................................................................................ 19

2.21. What are the time limits to recover Input Tax? ..................................................... 19

2.22. Can I deduct Input Tax paid that I incurred before I registered for VAT? .............. 20

2.23. What Goods and Services can I not recover VAT on?.......................................... 20

2.24. What is the mechanism for paying Tax?............................................................... 20

2.25. What if I am unable to pay? Can I pay tax in installments? If so, what is the

process? .............................................................................................................. 21

2.26. Currency used on a Tax Invoice ........................................................................... 21

2.27. What should Bahraini businesses do in the absence of the exchange rate

approved by the Central Bank of Bahrain? ........................................................... 21

2.28. How do you calculate the Tax on a Supply if the value includes a fraction of a Fils?

............................................................................................................................ 22

2.29. How will the NBT know the annual taxable income of my company? ................... 22

2.30. Who is permitted to issue and retain electronic documentation? .......................... 22

3. VAT refunds .............................................................................................. 23

3.1. In what cases may I receive a Tax Refund? ......................................................... 23

3.2. Who will be responsible for VAT refunds? ............................................................ 23

3.3. Can VAT payable be offset against refunds? ....................................................... 23

3.4. In case of refund, how long will it take for the Bureau to refund the VAT? ............ 23

4. Imports and exports ................................................................................. 23

4.1. What are the conditions to be met to apply the zero rate for the export of services?

............................................................................................................................ 23

4.2. How is the value of imported Goods determined for VAT purposes?.................... 24

4.3. Are all imports of Goods subject to VAT or are there some exceptions? .............. 24

4.4. What is the VAT rate for re-exports? .................................................................... 25

4.5. Where is VAT collected in case of importation? ................................................... 25

4.6. Is it possible to defer the payment of the import VAT? ......................................... 25

© Kingdom of Bahrain | Ministry of FinanceContents

5. Dealing with discounts and free items ................................................... 25

5.1. How are discounts given to customers treated under the VAT Law? .................... 25

5.2. If I give free items (gift or samples) to my employees or clients, should I charge

VAT on these and declare VAT as sales? ............................................................ 26

5.3. Is there a maximum amount I can give for free without having to declare a sales

and pay VAT? ...................................................................................................... 26

6. Penalties ................................................................................................... 26

6.1. What are VAT administrative penalties?............................................................... 26

6.2. Who is mandated to impose administrative penalties? ......................................... 26

6.3. Can I appeal an administrative penalty?............................................................... 27

6.4. What gives rise to tax evasion and what are the associated penalties? ............... 27

7. Sector specific inquiries .......................................................................... 27

7.1. Financial Services – how is VAT applied to Financial Services? .......................... 27

7.2. Financial Services – what is the VAT treatment of fee-based income, i.e.

commission and margin based income (e.g. interest on loans, deposit) products?

............................................................................................................................ 29

7.3. Financial Services – what is the VAT treatment of Islamic finance products? ....... 29

7.4. Financial Services – will insurance Services be subject to VAT? ......................... 29

7.5. Real estate – what is the VAT treatment of the supply of bare land and buildings?

............................................................................................................................ 29

7.6. Real estate – if I rent an apartment, do I have to pay VAT? ................................. 29

7.7. Real estate – does VAT apply to sales of residential real estate? ........................ 29

7.8. Construction – what is the VAT treatment for the construction sector? ................. 30

7.9. Education – are educational Services subject to VAT? ........................................ 31

7.10. Healthcare – are healthcare Services and related Goods and Services subject to

VAT?.................................................................................................................... 32

7.11. Healthcare – are cosmetic procedures / surgery considered as a qualifying medical

service for VAT purposes? ................................................................................... 33

7.12. Healthcare – what is the VAT treatment of medicines and medical equipment? ... 33

7.13. Healthcare – will equipment for persons with special needs be subject to VAT? .. 33

7.14. Transportation – what is the VAT treatment for the transportation sector? ........... 34

7.15. Oil & gas – what is the VAT treatment for the Oil, Oil derivatives and gas sector?35

7.16. Other – what is the VAT treatment of the supply of gold, silver and platinum? ..... 35

7.17. Other – what is the VAT treatment of pearls and precious stones? ...................... 36

7.18. Other – what VAT rates apply for food items? ...................................................... 36

7.19. Other – are government supplies subject to VAT? ............................................... 36

7.20. Other – can the company apply the VAT on a Government body? ....................... 36

7.21. Other – what is the VAT application on ongoing contracts? ................................. 37

7.22. Other – customer purchased goods in December 2018 and they were delivered to

him on the same day; he is paying by cheque but the date on the cheque is in

January 2019. Will he pay VAT for the transaction? ............................................. 37

© Kingdom of Bahrain | Ministry of FinanceContents © Kingdom of Bahrain | Ministry of Finance

FREQUENTLY ASKED QUESTIONS The FAQs intend to assist Taxpayers in understanding the implementation of VAT in Bahrain. The content is simplified to effectively summarize complex legal content covered in the VAT Law and the VAT Executive Regulations (together referred to as the ‘VAT legislation’). In the event of any conflict between the content of this document and the provisions of the VAT legislation, the VAT legislation shall prevail. 1. VAT eligibility and registration process 1.1. How do I determine if my business needs to register? If the value of your annual supplies exceeds the mandatory VAT registration threshold, you will need to register for VAT. Please note that transitionary phasing applies to registration timelines depending on the size of business. Mandatory registration thresholds and effective dates are: © Kingdom of Bahrain | Ministry of Finance and National Economy 6

Article 33, 44, and 109 of Bahrain VAT Executive Regulations

1.2. How is the registration threshold calculated?

The registration threshold is calculated based on either:

• Annual supplies generated in the past twelve months, or

• Expected annual supplies to be generated in the twelve months to come.

Annual supplies for registration purposes are defined under Article 34 of the

Executive Regulations. Annual supplies mainly cover taxable supplies that are either

standard rated or zero rated. Hence, exempted supplies are not included in the

calculation.

1.3. Can I voluntarily register?

If your annual supplies exceed the voluntary VAT registration threshold of BHD

18,750, you can voluntarily register for VAT.

You must however remain registered for at least two years from the date of

registration unless you completely cease carrying out any business activities prior to

this date. If you completely cease to carry out any business activities, you must

provide sufficient evidence to the NBT.

Article 44 of Bahrain VAT Executive Regulations

1.4. When calculating my annual supplies, do I include the revenue for

each of the stores / branches that fall under the company?

When calculating your annual supplies, you should include the annual supplies for all

stores and branches that fall under the same legal entity.

For completeness, a head office and its branch(es) will be considered as the same

legal entity for the purposes of VAT.

© Kingdom of Bahrain | Ministry of Finance and National Economy 71.5. How do I register for VAT?

Applicants will need to sign up on the webpage and submit the application for

registration. Details around are communicated via NBT’s webpage

(https://www.nbt.gov.bh/vat_registration).

1.6. What information will the NBT require for VAT registration?

The registration application shall require, at a minimum, the following information:

1. The name and address of the applicant.

2. The email address to be used for correspondence with NBT.

3. The commercial registration number.

4. Details regarding the applicant's economic activities.

5. The date of commencing the activity and the date of meeting the conditions

for mandatory registration.

6. Value of actual and expected annual supplies for registration purposes.

7. Reference to the nature of the supplies made and whether they are exempt

from tax or subject to the zero rate.

8. Reference as to whether the applicant is an exporter, showing the ratio of

annual exports to total annual supplies.

9. Details of authorised signatories of the Taxable Person for tax purposes.

Article 37 of Bahrain VAT Executive Regulations and Decree-Law No. 48 of 2018 on

Value Added Tax

1.7. What happens after I have submitted by application to register for VAT

to NBT?

Once you have submitted your registration application for VAT, NBT will review it.

Once approved, NBT will issue the business with a VAT registration certificate. This

will include details of your Tax Registration Number (TRN) and the date your VAT

registration will take effect.

1.8. What is my Tax Registration Number?

Your Tax Registration Number (TRN) will be a unique number that is given to you on

your VAT registration certificate. You should include this on all Tax Invoices that are

issued.

This will be a unique number and will be different to your excise duty number, if

relevant.

© Kingdom of Bahrain | Ministry of Finance and National Economy 81.9. When will my VAT registration take effect?

Your VAT registration certificate issued by the NBT will specify the date that your

VAT registration will take effect.

Article 33 of Bahrain VAT Executive Regulations

1.10. What do I do with my VAT registration certificate?

Your VAT registration certificate should be placed in a visible place in your

establishment.

Article 37 of Bahrain VAT Executive Regulations

1.11. What should I do if there are changes in the registration information?

If there are any changes in the information that you have provided when you

registered for VAT, you should notify NBT within thirty days from the date of the

change. NBT will advise in due course on the process and form for submitting such

information to NBT.

Article 43 of Bahrain VAT Executive Regulations

1.12. If I am not established in Bahrain, will the introduction of VAT impact

on me and my business activities?

The introduction of VAT in Bahrain will impact all businesses that undertake taxable

activities in Bahrain. If you are not established in Bahrain and are carrying out

business activities that will be taxable in Bahrain, you will need to consider whether

you will need to register for VAT or not and the impact of the introduction of VAT on

your business.

You may choose to appoint a Tax Representative to assist you in meeting your VAT

obligations in Bahrain.

Article 36 of Bahrain VAT Executive Regulations

1.13. If I make exclusively zero rated supplies above the mandatory VAT

registration threshold do I need to register for VAT?

If you make exclusively zero rated supplies and the value of your annual supplies

exceeds the mandatory VAT registration threshold, you can apply for a registration

exception to NBT. This means that, if approved, NBT will grant permission for you to

not be required to register for VAT. If you are not registered for VAT, this will also

mean that you cannot recover any VAT that you are charged on purchases and this

VAT will therefore be an additional cost to the business.

Article 35 of Bahrain VAT Executive Regulations

© Kingdom of Bahrain | Ministry of Finance and National Economy 91.14. How do I apply for a registration exception to NBT?

Further details on the process of how to apply for a registration exception from NBT

will be provided in due course. You will however need to provide the following

information to NBT:

1. Name, information and address of place of business in Bahrain.

2. Commercial registration number.

3. Tax Registration Number.

4. Type and description of the Economic Activity conducted, which shows that

the supplies made are subject to Tax at the zero rate.

5. Value of the actual and expected annual Taxable Supplies at the zero rate.

6. A pledge not to deduct Input Tax or claim any Tax Refund during the period in

which the person is exempt from registration, where he has been registered

for Tax purposes at a later date.

Article 35 of Bahrain VAT Executive Regulations

1.15. What if I fail to register on time?

If you do not register on time, you may be subject to penalties that may be up to

BHD 10,000. Please refer to Article 60 of Bahrain VAT Law for more details.

Article 60 of Bahrain VAT Law

1.16. Can I register as a Tax Group?

You cannot register for a Tax Group as of 1 January 2019 and further details on this

will be provided in due course. As such, all legal entities must be separately

registered for VAT where required to do so.

1.17. What are the requirements for mandatory deregistration?

The registrant should apply to NBT for deregistration in any of the following cases:

1. If he stops conducting an Economic Activity.

2. If he stops making Taxable Supplies over a period of 12 consecutive months.

3. If, at the end of any month, the value of the Taxable Supplies made over the

previous 12-month period is less than the voluntary registration threshold, and

he does not anticipate that the value of his supplies or expenses will exceed

the voluntary registration threshold over the next 12 month period.

Article 34 of Bahrain VAT Law

© Kingdom of Bahrain | Ministry of Finance and National Economy 101.18. What are requirements for voluntary deregistration?

The Registrant may apply to NBT for deregistration if the total value of the Taxable

Supplies made over the previous 12-month period is less than the mandatory

registration threshold but exceeds the voluntary registration threshold.

Article 34 of Bahrain VAT Law

1.19. What documents should I provide in case of deregistration?

The deregistration application must include, at a minimum, the following information:

1. The name of the registrant applying for deregistration.

2. The Registration Number of the registrant and the effective date of

deregistration.

3. The reason for applying for deregistration.

4. The date the registrant ceased making Taxable Supplies, if the reason for

deregistration is the cessation of his Economic Activity.

5. The value of annual Taxable Supplies during the previous 24 months.

6. The value of the expected Taxable Supplies for the next 12 months.

Article 46 of Bahrain VAT Executive Regulations

1.20. What are my obligations post-deregistration?

In all cases, the deregistered person must adhere to the following:

1. Refrain from presenting himself as a registrant under any circumstances.

2. Maintain books, records, and invoices related to his Supplies for a period of

five years from the date of his deregistration and allow NBT’s employees to

review them upon their request.

Article 47 of Bahrain VAT Executive Regulations

1.21. Can a VAT-registered business purchase Goods or Services from a

business that is not VAT-registered?

Yes, a VAT-registered business can purchase Goods or Services from a business

that is not VAT-registered. There will be no VAT charged on any purchases from a

business that is not VAT-registered.

1.22. Is a sub-CR considered part of the same person or legal entity?

Generally, a sub-CR is considered part of the same person or legal entity that

owns the main CR and will use the same TRN assigned to the main CR.

© Kingdom of Bahrain | Ministry of Finance and National Economy 111.23. What is the VAT treatment of transactions between branches of the

same legal entity?

Transactions between branches owned by an individual or within the same legal

entity will fall outside the scope of VAT.

1.24. Will I need a separate TRN for each branch under a single person or

legal entity?

An applicant must register one application per legal entity. The applicant must

specify the commercial registration of the branch that he would like to designate for

all communications from NBT for VAT purposes. In addition, the applicant must also

specify the commercial registration numbers of the remaining branches for

compliance purposes. After approval, one VAT certificate will be issued for a legal

entity. The certificate will have details of the designated branch therefore, the

applicant must ensure that relevant branch is classified as the designated branch.

1.25. How can I register a Joint Venture?

If a joint venture has a commercial registration certificate, it can register as a

separate legal entity with NBT using its own commercial registration number.

However, if the joint venture does not have a commercial registration certificate, the

commercial entities constituting the joint venture are responsible to report annual

supplies and purchases of the joint venture in their own returns with due

consideration to the proportion of supplies and purchases that they can account for

in their financial statements which is usually driven by the terms of joint venture

formation.

1.26. What if I made a mistake while submitting my VAT registration

application? Can I amend or re-apply?

Applicants are encouraged to provide correct details at the time of profile creation

request. They will have an opportunity to change select registration application

details at two different instances:

• When NBT’s registration officer reaches out to them for some

clarification.

• When “Change in registration details” process is launched – to be

confirmed by NBT in the future.

2. VAT procedures and filing

2.1. In general, when is Tax due on the supply of Goods and Services?

Tax will be due at the earlier date of:

1. When Goods are delivered or Services are performed.

2. The issuance of a Tax Invoice.

© Kingdom of Bahrain | Ministry of Finance and National Economy 123. When payment, or part payment is received.

Article 12 of Bahrain VAT Law

2.2. What is a Tax Return?

A Tax Return is submitted by each Taxable Person to NBT to mainly declare the

VAT paid on purchases and VAT accounted for on supplies.

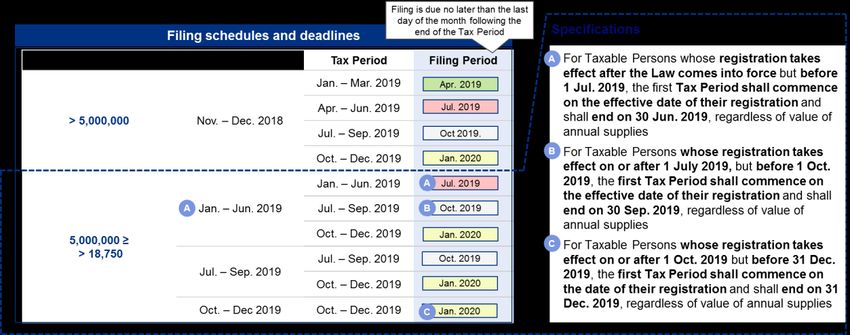

2.3. What is a Tax Period?

Depending on the annual supplies of your business, your Tax Periods will determine

how often you must file a Tax Return to NBT. As per the VAT legislation, Taxable

Persons with annual supplies exceeding BHD 3 M will have monthly Tax Periods and

Taxable Persons with annual supplies less than BHD 3 M will have quarterly Tax

Periods. This is explained in the table below.

Declared Taxable

Supplies Tax Period

> 3 million Dinars Monthly

≤ 3 million Dinars Quarterly, with Tax Periods being as follows:

a) First Tax Period: 1 January to 31 March,

b) Second Tax Period: 1 April to 30 June,

c) Third Tax Period: 1 July to 30 September,

d) Fourth Tax Period: 1 October to 31 December

Or, if requested by the Taxpayer and approved by NBT

monthly

Article 48 of Bahrain VAT Executive Regulations

There will be special rules in place in relation to Tax Periods for the first year of VAT

(i.e. the transitional period). These are set out in the table below:

In the transitional period (1 Jan 2019 to 31 Dec 2019)

Declared

taxable Registration

supplies effective Tax Period

> 5 million 1 Jan 2019 Quarterly, with Tax Periods being as follows:

Dinars a) First Tax Period: 1 January to 31 March

2019,

b) Second Tax Period: 1 April to 30 June

2019,

c) Third Tax Period: 1 July to 30 September

2019,

© Kingdom of Bahrain | Ministry of Finance and National Economy 13d) Fourth Tax Period: 1 October to 31

December 2019

≤ 5 million 1 Jan 2019 One 6-month period, then quarterly, with Tax

Dinars and ≥ Periods being as follows:

18,750 Dinars a) First Tax Period: 1 January to 30 June

2019,

b) Second Tax Period: 1 July to 30

September 2019,

c) Third Tax Period: 1 October to 31

December 2019

Article 109 of Bahrain VAT Executive Regulations

Article 48 of Bahrain VAT Executive Regulations

2.4. Can I change my Tax Period?

Taxpayers with annual supplies ≤ 3 million Dinars can request to change to monthly

Tax Periods. NBT has the authority to approve or reject this request. In case of

© Kingdom of Bahrain | Ministry of Finance and National Economy 14approval, a notice will be issued that states the effective date of the new Tax Period

applying to the Taxpayer.

Article 48 of Bahrain VAT Executive Regulations

2.5. When should I submit the Tax Return?

Tax Returns must be submitted on the last day of the month following the Tax Period

(i.e. for the Tax Period ending 31 March, the return must be submitted by 30 April at

the very latest).

If there is no VAT to be declared for a given Tax Period, for example you have made

no purchases, imports or supplies, you must still submit a nil VAT return.

If a Tax Return is not submitted by the deadline, NBT has the right to estimate the

Tax for the respective period.

Article 49 of Bahrain VAT Executive Regulations

2.6. When shall we pay Tax due for the Taxable Period?

Tax due must be paid at the latest by the last day of the month following the end of

that Tax Period (i.e. taxes due for the filing period ending 31 March must be paid no

later than 30 April).

Where the Taxable Person has not submitted his Tax Return or where his calculation

of Tax proved to be incorrect, the Taxable Person must pay the Tax, Tax differences

and administrative fines due (if imposed) resulting from an assessment issued by

NBT within a period of thirty days from the date of notifying the Taxable Person, or

before the date specified in the assessment.

Article 63 of Bahrain VAT Executive Regulations

2.7. What should I declare in the Tax Return?

Further details on the format of the VAT return will be shared in due course. At a

minimum, the following information will be required:

1. The value of standard rated Taxable Supplies and the amount of Tax due for

the Tax Period for which the Tax Return is submitted.

2. The value of his zero rated Taxable Supplies for the Tax Period for which the

Tax Return is submitted.

3. The value of Goods and Services supplied to the Taxable Person for which he

is liable to pay Tax, and the corresponding amount of Tax due and related to

the Tax Period for which the Tax Return is submitted.

4. The amount of Tax due on import for which payment has been deferred

related to the Tax Period in which the Tax Return is submitted.

5. The value of additional Tax due as a result of adjustment.

© Kingdom of Bahrain | Ministry of Finance and National Economy 156. The total value of Tax due for the Tax Period.

7. The total value of inputs of the Taxable Person and the total value of

deductible Tax from such inputs related to the Tax Period for which the Tax

Return is submitted.

8. The amount of the net refundable Tax from previous periods.

9. The amount of deductible Tax on imports.

10. The value of any excess Tax recovered resulting from an adjustment related

to a discount.

11. The total amount of deductible Tax related to the Tax Period for which the Tax

Return is submitted.

12. The amount of Net Tax due or refundable.

Article 49 of Bahrain VAT Executive Regulations

2.8. What are procedures for submitting the Tax Return?

The steps to submit a Tax Return are as follows:

• The Taxpayer will submit their Tax Return to NBT electronically in a

predefined online tool.

• To access this tool, NBT will provide the Taxpayer with personalised access

data, which will permit them to log onto an individual online account.

• When the Tax Return is submitted online and received by NBT, NBT will send

a receipt to the Taxpayer by email.

• This electronic receipt will be regarded as an official receipt of the Tax Return.

The submission date certified on this receipt will be the official date of

submission of the Tax Return.

• Submitting the Tax Return through NBT’s website will be regarded as an

approval and acknowledgement by the Taxable Person of the validity of the

data contained in the Tax Return and issued on his behalf.

Article 50 of Bahrain VAT Executive Regulations

2.9. Can a Tax Return be amended?

Yes, Tax Returns can be amended if necessary, e.g. in cases of errors on the Tax

Returns. To submit an amended Tax Return, the same mechanism as the

submission of a Tax Return (set out above) can be used.

An amended Tax Return will rescind the original Tax Return and shall be a substitute

to it.

Article 50 of Bahrain VAT Executive Regulations

© Kingdom of Bahrain | Ministry of Finance and National Economy 162.10. What should amended Tax Return include?

The amended Tax Return must include, in addition to the information contained in

the original Tax Return, a description of the amended amounts, the original amounts,

the differences as a result and the reason for the adjustment.

Article 51 of Bahrain VAT Executive Regulations

2.11. How soon should submit amended Tax Return when I am become

aware of the error? Will there be fines associated with amendments?

An amended Tax Return must be submitted within 30 business days from the date

the Taxable Person became aware of the error on his Tax Return and prior to NBT

commencing supervision and inspection procedures.

If the Taxpayer complies with these prerequisites, no administrative fine will be

imposed.

Article 51 of Bahrain VAT Executive Regulations

2.12. What are my obligations under VAT invoicing?

If you are VAT-registered, you must issue an original Tax Invoice when making a

supply of Goods and Services, including a deemed supply, or upon receiving partial

or complete Consideration prior to the date of supply.

Article 38 of Bahrain VAT Law

2.13. When should invoices be issued?

A Taxable Person must issue a Tax Invoice no later than the 15 th day of the month

following the date in which the transaction occurred (e.g. if the transaction happened

at any point in January, the Tax Invoice must be issued at the latest by 15 th

February).

Article 39 of Bahrain VAT Law

2.14. What should a Tax Invoice contain?

A Tax Invoice must contain at least the following:

1. The words “Tax Invoice” clearly stated.

2. The name, address of the Taxable Person and his Registration Number.

3. The name and address of the Customer

4. The date of issue of the Tax Invoice and the date of Supply or date of

payment if these differ from the date of issue.

5. A sequential invoice number.

6. A description of the Goods or Services supplied.

© Kingdom of Bahrain | Ministry of Finance and National Economy 177. The quantity of the Goods supplied.

8. The value of the Supply in Dinars, with the unit price exclusive of Tax in

Dinars.

9. The value of discount, if any, and the net value of the Supply in Dinars.

10. The rate and amount of Tax applicable.

11. The total amount due on the Supply inclusive of Tax in Dinars.

12. The exchange rate applied where a currency other than the Dinar is used.

13. An explicit reference where Tax has been calculated based on the profit

margin mechanism.

14. An explicit reference where the transaction has been exempted from Tax.

Article 52 of Bahrain VAT Executive Regulations

2.15. How long do photocopies of all Tax Invoices need to be retained?

A Taxable Person must retain photocopies of all Tax Invoices issued by him for a

period of five years from the end of the Gregorian year in which such invoices were

issued.

Article 52 of Bahrain VAT Executive Regulations

2.16. Can a bank statement be used as a Tax Invoice?

A bank statement can be treated as a Tax Invoice provided it contains the following

information:

1. The name, address and Registration Number of the bank in Bahrain.

2. The name and address of the Customer.

3. The date of issue of the bank statement.

4. The Tax rate applicable on every Supply.

5. The amount of Tax on every Supply.

Article 52 of Bahrain VAT Executive Regulations

2.17. When can a simplified Tax Invoice be issued?

A simplified Tax Invoice requires less information than a full Tax Invoice and a

Taxable Person may issue a simplified Tax Invoice in either of the following cases:

1. Where the Customer is not registered for Tax purposes in Bahrain.

2. Where the Consideration does not exceed 500 Dinars.

© Kingdom of Bahrain | Ministry of Finance and National Economy 18Article 53 of Bahrain VAT Executive Regulations

2.18. What information should a simplified Tax Invoice include?

A simplified Tax Invoice must contain at least the following:

1. The name, address and Registration Number of the Taxable Person.

2. The date of issue of the simplified Tax Invoice.

3. A description of the Goods or Services supplied.

4. The total value of the Supply in Dinars, inclusive of Tax.

5. The rate and amount of Tax applicable in Dinars.

Article 53 of Bahrain VAT Executive Regulations

2.19. On which items can I recover VAT?

A Taxable Person is entitled to deduct Input Tax paid or payable by him while

carrying out his Economic Activity, mainly for the purposes of making the Taxable

Supplies, including Supplies subject to the zero rate. For further details, please refer

to Article 57 of the Regulations.

Article 57 of Bahrain VAT Executive Regulations

2.20. Do I need to save any documents that are to be used for Input Tax

deduction purposes?

In order for a Taxable Person to be able to deduct Input Tax, the following

documents must be retained:

1. Original Tax Invoices for Goods and Services supplied to him where such

Tax Invoices are valid Tax Invoices as per the VAT legislation.

2. Customs documents relating to imports he has carried out and that prove

that he is the Importer of the Goods in accordance with the Customs Law

for the Cooperation Council for the Arab States of the Gulf.

3. Tax Invoices issued by the taxable Customer on behalf of the Supplier as

per the VAT legislation.

4. Any other commercial documents that evidence that the Taxable Person

has paid the Tax due.

Article 57 of Bahrain VAT Executive Regulations

2.21. What are the time limits to recover Input Tax?

Input Tax cannot be deducted after more than five years after the end of the

Gregorian calendar year in which the right to deduct Input Tax arose.

© Kingdom of Bahrain | Ministry of Finance and National Economy 19Article 57 of Bahrain VAT Executive Regulations

2.22. Can I deduct Input Tax paid that I incurred before I registered for VAT?

A Taxable Person will be entitled to deduct Input Tax incurred on Goods and

Services supplied to him or imported by him prior to the date of registration for Tax

purposes under the following conditions:

1. The Goods have been supplied to him or imported within a period not

exceeding five years prior to the effective date of registration of the Taxable

Person for Tax purposes and are still be in the possession of the Taxable

Person on the effective date of his registration for Tax purposes.

2. The Services have been supplied to him within a period not exceeding six

months prior to the effective date of registration of the Taxable Person for Tax

purposes.

3. They have been supplied to him or imported within the course of his

Economic Activity conferring the right to deduct Input Tax in accordance with

the provisions of the VAT legislation.

Full Input Tax cannot be claimed on capital assets acquired during the pre-

registration period. Please refer to the VAT Executive Regulations for further

details.

Article 61 of Bahrain VAT Executive Regulations

2.23. What Goods and Services can I not recover VAT on?

A Taxable Person cannot deduct Input Tax paid on Goods or Services used for

purposes other than his economic activity or relating to Goods or Services intended

for personal or recreational use. These may include: Input Tax paid on sport,

entertainment, and cultural Services as well as motor vehicles.

For more details, please refer to Article 58 of Bahrain VAT Executive Regulations.

Article 58 of Bahrain VAT Executive Regulations

2.24. What is the mechanism for paying Tax?

VAT, VAT differences and administrative fines due to NBT shall be payable

electronically in accordance with mechanism determined by NBT.

Once the payment of VAT is due, the Taxpayer needs to provide all details related to

his Tax Registration Number and the Tax Period for which VAT is paid.

Each Taxable Person will have an independent Tax account maintained by NBT, in

which the Tax due for each Tax Period, a current balance which relates to the total

Tax payable, the administrative fines, the fees due and any other amounts due will

be recorded.

© Kingdom of Bahrain | Ministry of Finance and National Economy 20The details of the Tax account will be made available to the Taxable Person

electronically, to enable him to access his account in accordance with the

mechanisms set by NBT.

Article 64 of Bahrain VAT Executive Regulations

2.25. What if I am unable to pay? Can I pay tax in installments? If so, what is

the process?

The Taxable Person may apply to NBT for payment of the Net Tax due in

installments for a particular Tax Period, if he can prove that he is unable to pay the

amount of Tax in full within the period specified in the Law.

NBT shall notify the applicant within thirty days from the date of his submission and

the applicant shall be notified of the result, whether it has been accepted or rejected.

Where NBT approves the installment application, the Taxable Person shall pay the

installments within the periods set in the application acceptance. Where the Taxable

Person does not adhere to the payment dates set, all remaining installments shall be

due immediately.

Article 64 of Bahrain VAT Executive Regulations

2.26. Currency used on a Tax Invoice

The currency used on a Tax Invoice must be Bahraini Dinar.

If the supply was made in a currency other than Bahraini Dinar, the amount stated on

the Tax Invoice should be converted into Bahraini Dinar.

Conversion shall be based on the exchange rate approved by the Central Bank of

Bahrain on the date of supply.

Article 40 of Bahrain VAT Law

2.27. What should Bahraini businesses do in the absence of the exchange

rate approved by the Central Bank of Bahrain?

A reliable source of foreign exchange rates should be used, but taxable persons

should use the same source consistently.

Examples of reliable exchange rate sources include, but are not limited to:

• Thomson Reuters.

• Oanda.

• XE.com.

• Bloomberg.

• and the exchange rate published by a Bahraini bank.

© Kingdom of Bahrain | Ministry of Finance and National Economy 212.28. How do you calculate the Tax on a Supply if the value includes a

fraction of a Fils?

Article 55 of the Executive Regulations states that, where a fraction of a Fils is part of

calculating tax on a supply, the taxable person may round the amount to the nearest

Fils in accordance with mathematical rounding.

In practice, as the smallest denomination of Fils in Bahrain is five Fils and, taxable

persons may round to the nearest five Fils accordingly.

Examples:

• If the tax is BHD 50.303, it should be rounded up to BHD 50.305

• If the tax is BHD 50.307, it should be rounded down to BHD 50.305

• If the tax is BHD 50.308, it should be rounded down up to BHD 50.310

Article 55 of Bahrain VAT Executive Regulations

2.29. How will the NBT know the annual taxable income of my company?

A taxable person, or his tax representative (where applicable) must maintain

business records that evidence his supplies. These records may be in Arabic or

English and may be maintained in an electronic form. The following are examples of

records that should be maintained by a taxable person for VAT purposes:

• Accounting books.

• Records of all supplies and imports of goods and services.

• Balance sheet and profit and loss accounts.

• Wage and salary records.

• Fixed asset records.

It is expected that NBT in the near future will start process of inspection and audit for

taxpayers once the Law comes into force. NBT shall have access to the above

records to examine the tax due and verify compliance with VAT Law and

Regulations.

Article 56 and 105 of Bahrain VAT Executive Regulations

2.30. Who is permitted to issue and retain electronic documentation?

Under Article 56 of the Executive Regulations, only taxable persons who have

obtained prior approval from the NBT will be permitted to issue electronic

documentation. Taxable persons who meet the requirements set out in Articles 52

and 54 of the Executive Regulations and whose computer systems are capable of

accounting for VAT on their supplies will be eligible to issue electronic documents

without obtaining prior approval from the NBT.

Article 52, 54, and 56 of Bahrain VAT Executive Regulations

© Kingdom of Bahrain | Ministry of Finance and National Economy 223. VAT refunds

3.1. In what cases may I receive a Tax Refund?

NBT may refund tax paid for any supply or import made by any of the following:

1. A Taxable Person who paid excess VAT.

2. Foreign governments, international organizations, institutions, consular and

military bodies and missions for Goods and Services supplied inside Bahrain.

3. Tourists.

Article 57 of Bahrain VAT Law

3.2. Who will be responsible for VAT refunds?

NBT will have overall responsibility for processing and paying VAT refunds. Further

details on this will be released in due course.

3.3. Can VAT payable be offset against refunds?

NBT may offset refunds against any tax or administrative fines due by the Taxable

Person under the provisions of the Law or any other tax law until the excess is

exhausted.

Article 86 of VAT Executive Regulations

3.4. In case of refund, how long will it take for the Bureau to refund the

VAT?

The Bureau may audit and review the accounts of the Taxable Person in order to

verify the validity of the refund request and, within sixty days from the date of

meeting requirements relating to documentation, shall notify the applicant of its

decision to approve or reject the request.

4. Imports and exports

4.1. What are the conditions to be met to apply the zero rate for the export

of services?

Only supplies of services with a place of supply in Bahrain under the general place of

supply rule in Article 16 of the VAT Law (i.e. the place where the supplier is resident)

can be considered as potentially eligible for the zero rate as an export of services.

Supplies of services with a place of supply in Bahrain as a result of the application of

a special place of supply rule are not eligible to qualify as an export of services. Such

supplies are those which follow the special place of supply rules in Articles 17 and 18

of the VAT Law (e.g. services related to a real estate, restaurant and hotel services,

transport of goods and passengers, telecommunications and electronic services,

etc.).

© Kingdom of Bahrain | Ministry of Finance and National Economy 23Where the place of supply of the services is in a jurisdiction other than Bahrain, the

VAT Law does not apply and the services are to be treated as being outside the

territorial scope of the Bahrain VAT Law (e.g. services related to a real estate

located outside Bahrain, catering services performed outside Bahrain, etc).

In order to apply the zero-rate for the export of services, a taxable person must

ensure that all of the following conditions are met:

1. The customer receiving the service does not have a place of residence in

Bahrain.

2. The customer must not be present in Bahrain at the date the services are

performed.

3. The services do not relate to tangible goods or real estate located in Bahrain

at the time the services are performed.

4. The services are enjoyed outside the territory of the Implementing States.

Where the customer has either a place of residence in Bahrain or a presence in

Bahrain at the time of the supply, the place of residence/presence most closely

connected with the supply will have to be identified so as to determine whether the

services are actually “consumed” in Bahrain. Such assessment must take into

account the nature of the services supplied and the substance of the supply.

The services must not be actually received by and benefit a person, other than the

customer, who is resident in Bahrain.

4.2. How is the value of imported Goods determined for VAT purposes?

Import VAT, where applicable, will be charged on the value of the imported Goods.

The value of imported Goods will be the Cost, Insurance, and Freight (CIF) value

plus excise tax, customs duty and any other charges, excluding Tax.

Article 21 of Bahrain VAT Law

4.3. Are all imports of Goods subject to VAT or are there some

exceptions?

All Goods imported into Bahrain will be subject to VAT, unless they are specifically

exempt from VAT.

The following transactions are exempt from Tax:

1. Import of Goods, if the Supply of such Goods in the state of final

destination is exempt from or subject to Tax at zero rate.

2. The following imports of Goods, that are also exempt from customs duty

Goods:

a. Goods imported for diplomatic purposes.

© Kingdom of Bahrain | Ministry of Finance and National Economy 24b. Goods imported for military purposes.

c. Imports of personal luggage and household appliances used by citizens

residing abroad and foreigners coming to reside in Bahrain for the first

time.

d. Imports of returned Goods.

e. Personal luggage and gifts accompanied with travellers.

f. Goods for people with special needs.

Article 56 of Bahrain VAT Law

4.4. What is the VAT rate for re-exports?

VAT is at the zero rate on the re-export of Goods which are temporarily imported into

Bahrain for repair, conversion, restoration and processing under the conditions

stipulated in the Customs Law.

Article 72 of Bahrain VAT Executive Regulations

4.5. Where is VAT collected in case of importation?

The importer shall pay the tax at the first point of entry to the Customs Affairs in

Bahrain. However, a Taxable Person may apply to the NBT to defer payment of tax

at import until the next Tax Return.

For the first year of VAT, there will be transitional provisions in place for the import of

Goods in Bahrain. Further details will be provided on this in due course.

Article 51 of Bahrain VAT Law

4.6. Is it possible to defer the payment of the import VAT?

NBT may allow the deferral of payment of Tax on import for select registered

taxpayers. The requirements and procedures for import VAT deferral will be

announced by the Bureau in due course. Application window is not open yet.

5. Dealing with discounts and free items

5.1. How are discounts given to customers treated under the VAT Law?

If you give a discount to your customers before you make the supply, you must

calculate VAT on the discounted value of the Goods or Services that you supply. For

example, if a business is selling an item at BHD 100 and gives the customer a 10%

discount, VAT should be accounted for on BHD 90.

Article 24 of Bahrain VAT Law

© Kingdom of Bahrain | Ministry of Finance and National Economy 255.2. If I give free items (gift or samples) to my employees or clients, should

I charge VAT on these and declare VAT as sales?

You should not charge VAT on these gifts (they are free for the recipient) nor declare

VAT on sales provided that their Market Value does not exceed fifty Dinars exclusive

of Tax, per recipient, during a year.

But if you exceed this fifty Dinars per recipient per year, you should declare sales

and related VAT on the excess amount.

Article 8 of VAT Executive Regulations

5.3. Is there a maximum amount I can give for free without having to

declare a sales and pay VAT?

The threshold of annual Supplies of gifts, samples and Goods that a Taxable Person

may provide without Consideration is one thousand Dinars during the year.

Article 8 of VAT Executive Regulations

6. Penalties

6.1. What are VAT administrative penalties?

VAT administrative penalties may be imposed by NBT on a Taxperson for non-

compliance with the VAT Law and the Executive Regulations. They include by way

of example:

For full details, please refer to Article 60 of Bahrain VAT Law

6.2. Who is mandated to impose administrative penalties?

Administrative penalties will be imposed by NBT pursuant to Article 60 of the VAT

Law. In some instances, administrative penalties may be issued by a decision

issued by the Minister or his delegate.

Article 61 of Bahrain VAT Law

© Kingdom of Bahrain | Ministry of Finance and National Economy 266.3. Can I appeal an administrative penalty?

A Taxable Person may appeal a decision to impose an administrative penalty within

thirty days from the date of notification of the decision or procedure, subject to

paying the prescribed fee. For full details regarding the timelines of the process,

please refer to Articles 62 and 66 of the Bahrain VAT Law.

Article 62 of Bahrain VAT Law

6.4. What gives rise to tax evasion and what are the associated penalties?

The table below provides examples of the various cases of tax evasion and the

associated penalties.

For full details, please refer to Articles 63 and 64 of Bahrain VAT Law

7. Sector specific inquiries

7.1. Financial Services – how is VAT applied to Financial Services?

The following Financial Services are exempt from VAT in Bahrain:

1. Financial Services where the remuneration received is not by way of a fee,

commission or commercial discount.

2. The transfer of ownership of an equity security or debt security.

3. The provision of life insurance and life reinsurance Services as well as the

transfer of such contracts.

Examples of Financial Services, include:

© Kingdom of Bahrain | Ministry of Finance and National Economy 271. Depositing money in current accounts, savings accounts or deposits.

2. Granting and transferring loans, borrowings and credit.

3. The issue or cancellation of cheques, debit cards and credit cards.

4. The issue, transfer, receipt or any dealing with money or any financial bond or

any banknotes or money orders.

5. The Supply or issue of financial derivatives or deferred contracts or any

necessary arrangements for them.

6. The Supply or issue of shares, stocks, bonds and securities related to them.

7. Transactions related to ATMs, excluding the Supply, installation or

maintenance of these machines or the Supply of a programme used for their

operation.

8. The conversion of the currency either through the exchange of banknotes or

any related matters.

9. The provision or transfer of financial instruments, sukuks, swaps, options, or

any futures contracts.

10. The issue, allotment, renewal, amendment, rent or transfer of ownership of a

debt or equity security (whether listed or unlisted), credit contract or the like.

11. The provision, or transfer of ownership of a life insurance or reinsurance

contract.

12. The provision of insurance cover or annuities under any investment scheme,

13. The provision, acquisition, amendment or release of a guarantee, indemnity or

security that relates to the performance of obligations arising under a cheque,

credit security, debt security, or similar document.

14. Any Islamic financial products provided in accordance with legally approved

contracts, which are similar to traditional financial products in terms of the

intended objective and materially achieve the same result.

15. Commissions for brokerage Services, or under a mudaraba or wakala

contract.

The VAT treatment applicable to conventional financial products will apply to Islamic

financial products that are Shariah compliant and which are intended to achieve the

same result as conventional financial products.

Article 81 of Bahrain VAT Executive Regulations

© Kingdom of Bahrain | Ministry of Finance and National Economy 287.2. Financial Services – what is the VAT treatment of fee-based income,

i.e. commission and margin based income (e.g. interest on loans,

deposit) products?

Financial Services where the remuneration received is not by way of a fee,

commission or commercial discount is exempt from VAT in Bahrain. Therefore,

margin-based activities are exempt while non-margin based (i.e. fee-based) activities

are standard rated.

7.3. Financial Services – what is the VAT treatment of Islamic finance

products?

Islamic finance products, that are Shariah compliant and which are intended to

achieve the same result as conventional financial products, will be treated in the

same way as the conventional financial products, for VAT purposes.

Article 81 of Bahrain VAT Executive Regulations

7.4. Financial Services – will insurance Services be subject to VAT?

Life insurance, life reinsurance contracts, and transferring ownership of these e are

exempt.

All other insurance Services, for example health insurance and car insurance, will be

taxable at the rate of 5%. In certain circumstances, the zero rate may apply to travel

insurance.

Article 81 of Bahrain VAT Executive Regulations

7.5. Real estate – what is the VAT treatment of the supply of bare land and

buildings?

The Supply of bare land and any buildings by way of sale or rental shall be exempt

from VAT in Bahrain.

Article 55 of Bahrain VAT Law

7.6. Real estate – if I rent an apartment, do I have to pay VAT?

No, the rental of residential real estate, including flats, is exempt from VAT. You

may however be charged VAT on any Services charges relating to your residential

property. VAT may also be chargeable at 5% on furniture rented with an apartment if

a separate charge is made for this.

7.7. Real estate – does VAT apply to sales of residential real estate?

A sale of residential real estate by way of sale or lease is exempt from VAT. You

may however be charged VAT on related Services, such as property agent fees.

© Kingdom of Bahrain | Ministry of Finance and National Economy 29You can also read