Global Investment Weekly 2019.04.22 - CTBC Private Banking

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Investment Weekly

2019.04.22

Market Calendar, 2019/4

W1(4/1-4/5) W2(4/8-4/12) W3(4/15-4/19) W4(4/22-4/26) W5(4/29-5/3)

Composite ECB Meeting(10) U. Of Michigan IFO Outlook(24) Euro Zone Q1

PMIs(1) Confidence(12) BOC Meeting(24) GDP(30)

DM BOJ Tankan(1) Germany ZEW(16) US Durables

RBA Meeting(2) Fed Beige Book(18) Orders(25)

US Nonfarm(5) US Retail Sales(18) BOJ Meeting(25)

US Q1 GDP(26)

Composite

EM China Social China Q1 GDP(17) CBR Meeting(26) China NBS PMI(30)

PMIs(1)

Financing(10~15)

Financials Results Growth Sector Results

Healthcare, Cons. Energy Results

S ector Staple Results Commodities

Results

Utilities, Telecom Iranian

Results Sanction

Waiver Expiry

S ur pr i se Commodity

E vent Price Upgrade

And Its Impacts

M ar ket India Election Indonesia Election

Topic

Source: Compiled by CTBC Bank, 2019/4/19

1

Investment Strategy Summary

Results And Economic Data Outperformed, Risk Asset Rallied

Global Europe: EU Outlook Bottoming Out More Likely, IFO Might Rise For The

Economy 2nd Month

Central BOJ:BOJ Monetary Policy On Hold

JPY:JPY Continued To Be In Range Bound

Bank &

China Bond: Outlook Bottoming, Treasury Yield On The Rise

FX/FI

EM Bond: DM Monetary Policy In Wait-And-See Mode, EM Bonds

Strategy Benefited

Results US: Equity Edged Higher After Posting Better-Than-Expected Earnings

Review & Growth: Fundamentals Bottoming Out To Peak Season Track

Telecom: Clash Of New Setup And Earning Concern, Patient In

Equity

Consolidation

Strategy Resource: 1Q19 Resources Earnings Mostly Fall, 2Q19 Would Recover

Source: Compiled by CTBC Bank, 2019/4/19

2Agenda

Part I Macro and Market Review

Part II Short-Term Focus and Strategy

3Macro Review

Economic Data Release Review(4/12-4/18)

Macro Data: In ZEW Germany Apr data, current situation disappointed with further slide but the more important

expectations jumped from -3.6 to 3.1, back to above 0, indicating optimistic outlook in N6M and confirming the signal of

outlook bottoming out. However, Euro Zone Apr composite PMI released two days later was dragged by France and

Germany to 51.3.Germany manufacturing and services PMIs rose but the former only increased slightly to 44.5 and

missed consensus. Therefore, though both manufacturing and service improved to support Germany composite PMI, it

still stayed at the YTD low of 52.1. The 7-month high Germany service PMI was the bright spot with 4 consecutive

months rise in activity index and accelerating new orders. In contrast, output slid for 3 consecutive months in the weak

manufacturing with falling orders. Export orders, in particular shrank the 2nd fastest in 10 years, dragged by automotives.

Release Date Country Economic Data Period Consensus Actual Prior

04/12/2019 16:00 CN Money Supply M2 YOY Mar 8.20% 8.60% 8.00%

04/12/2019 16:01 CN Aggregate Financing CNY Mar 1850.0b 2860.0b 703.0b

04/15/2019 20:30 US Empire Manufacturing Apr 8 10.1 3.7

04/16/2019 17:00 GE ZEW Survey Current Situation Apr 8.5 5.5 11.1

04/16/2019 17:00 GE ZEW Survey Expectations Apr 0.5 3.1 -3.6

04/17/2019 10:00 CN GDP YOY 1Q 6.30% 6.40% 6.40%

04/18/2019 15:30 GE Markit/BME Germany Manufacturing PMI Apr P 45 44.5 44.1

04/17/2019 16:00 EC Markit Euro Zone Composite PMI Apr P 51.8 51.3 51.6

04/18/2019 16:00 EC Markit Euro Zone Manufacturing PMI Apr P 48 47.8 47.5

04/18/2019 20:30 US Retail Sales Advance MOM Mar 1.00% 1.6% -0.20%

04/18/2019 20:30 US Initial Jobless Claims Apr 13 205k 192K 196k

Source: Bloomberg, Compiled by CTBC Bank, 2019/4/18

4Market Review

Financial Results And Economic Data Fueled Global Equity Rally

Country: Global equity mostly rose last week. China 1Q GDP growth of 6.4% beat consensus, boosting the Chinese A

shares to outperform other EM equities. Rising oil price fueled the rally of Russia equity. In contrast, Brazil equity was

relatively weak as investors waited for further information of reforms. In DM, falling risk aversion demand for JPY eased

the pressure on Japan equity with a bright catch-up rally. US equity financial results and economic data beat

consensus, but the effect of these positive news was marginalized with limited room for further rally in short-term.

Sector: Benefited from improved US/China economic data and better-than-expected corporate financial results,

financials and industrial sectors led the rally in the past week at 2.7% and 2.1% respectively. Healthcare was hit 5.1%

last week by health insurance policy and drug pricing regulations and pessimistic sector view from IBs.

Global Equity Index Change Global Sector Index Change

Source: Bloomberg, past month is for 2018/3/18~2019/4/18, past week is for 2019/4/11~2019/4/18.

Sector indices based on Morgan Stanley Capital International (MSCI) global 11 sectors. 5Market Review

Better Than Expected China Growth Boosted Global HYBs And CNY

FI: China 1Q growth of 6.4% beat market expectation, leading global HYBs higher, especially for Asian and European

HYBs which were highly correlated to Chinese growth. But Germany 10-yr treasury yield returning to positive

depressed overall European bonds. EM bonds mostly fell with local currency bonds falling 0.5% amid stronger dollar.

FX: Better than expected 1Q19 China growth rate boosted both CNY and AUD, rallying 0.2% and 0.4% respectively.

Euro Zone manufacturing PMI disappointed with slightly weaker EUR, boosting DXY by 0.3% in the past week. NZD

and CHF were the weakest performers among DM currencies with CHF depreciating by 1.2% in the past week.

Global Bond Index Change Global FX Change (Against USD)

Source: Bloomberg, past month is for 2018/3/18~2019/4/18, past week is for 2019/4/11~2019/4/18

Note: Bonds take BAML Bond Index price change in the period. FX is against USD. 6Agenda

Part I Macro and Market Review

Part II Short-Term Focus and Strategy

7Macro

EU Outlook Bottoming Out More Likely, IFO Might Rise For The 2nd Month

Real Output Data Returned To Positive Growth: Industrial Production Reversed To Positive

Euro Zone Feb industrial production rose slightly less

at 0.2% MOM but the trend has clearly improved YTD.

The 3.1% average YOY growth of Jan/Feb was much

better than -4.5% in 4Q18.

IFO Might Rise For The 2nd Month Next Week: The

released Sentix and ZEW results both showed more

optimistic correspondents. As recent real data were no

longer weak and shocks from external negative factors

such as Brexit and trade war became mild, business

outlook might rebound further in IFO survey next week.

Investors More Optimistic On Economic Outlook More Optimistic Correspondents

資料來源:(右上)JP Morgan 2019/4/12;(左下)Bloomberg 2013/4~2019/4;(右下)Bloomberg 2007/1~2019/4

8EM Bond Strategy

DM Monetary Policy Wait And See, EM Bonds Benefited

EM Major Currency Sovereign, Corporate, IGB Prefer Major Currency Sovereign In EM: DM central

banks had no urge to tighten. EM central banks

Sovereign: 6.1%

followed with RBI and Banxico might cut rates this year,

Upward Downward 2Q19 Corporate: 6.3%

IGB: 4.4% benefiting EM bonds. Historically sovereign bonds used

to be strong when Fed paused hikes. DXY still

Deviation Realized Quant Voluntary

consolidates at the high. If shocks raise FX volatility,

Reason: Dovish Fed has moderated EM central banks major currency sovereign would be more stable.

policies, positive to EM bonds. But US treasury yield

has overreacted to the easing policy, we would like to To Seek Value Sector In Asia IGBs: EM corporate

caution possible chain reaction of US treasury yield rating deterioration has stabilized though downgrades

retracement. Corporate bonds credit ratings have (mainly in China) were still more than upgrades. Some

stabilized but sliding earning still impacts HYBs so we sectors with weak credit quality (e.g. real estate) have

prefer IGBs among corporate bonds.

their bonds overpriced. Banking, Consumer Goods and

Capital Goods Sector have more opportunities.

EM Bonds Mostly Rally When Fed Pauses Hikes EM Corporate Bond Rating Downgrade Improved

Source: (Left)Bloomberg, ICE Data Indices, denominated in USD, (Right)JPM, 2019/4/3, Compiled by CTBC Bank, 2019/4/12

9Asia Macro

China Outlook Bottoming, Monetary Policy Holds, Treasury Yield To Rise

Timing Mismatch Of CNY Amplified The Effects, But

China 10-yr Treasury Yield

Bottom Is Forming: Recent Chinese economic data

2Q19 3% were impressive with 1Q19 GDP growth of 6.4% on par

Upward Downward

3Q19 3.1% with 4Q18, Mar NBS and Caixin manufacturing PMI

Deviation Realization Quant Voluntary above 50, financing growth rising with medium/long-

Reason: Timing mismatch of Chinese New Year amplified term loans and consumption/production outperform.

the magnitude of improvement but outlook is building Though timing mismatch of CNY might amplify the

the bottom with leading indicator turning better and effects but we expect bottom to form.

medium/long-term loans rising steadily. PBOC 1Q

meeting deleted 4Q18 ‘outlook faces tough challenge’. PBOC 1Q Meeting Wording Conservative: PBOC 1Q

With stable fundamental, China monetary policy would revealed the fundamental has stabilized so monetary

shift from rapid easing to neutral with easing bias, 2-yr policy shifted from rapid easing to neutral with easing

treasury yield might retrace after short-term rally with bias, adjusting with liquidity level. Though 2Q RRR cut

bottom appeared in 1Q. is still possible but total room for 2019 cuts might shrink.

Prior Chinese Credit Expansion Fueled Momentum PBOC 1Q Meeting Wording Compared To 4Q18

Highlights:

• Deleted ‘Outlook faces tough challenge, increase the

extent of counter-cyclical measures’ in 4Q18

• Monetary policy mentioned ‘maintain control over the

floodgates of monetary supply’ again and retained ‘ keep

liquidity at a reasonable and ample level’ since 2Q18.

Source: (L)Credit Suisse, 2013/3~2019/3, (R)Huachuang Securities, 2019/4/16

10BOJ

BOJ Monetary Policy On Hold

Weak Japanese Economic Data But Overseas Outlook Seemed To Improve: Recently released Japanese economic

data continued to be weak with manufacturing outlook as the biggest concern. Japan 1Q Tankan large manufacturing

confidence slid to 12 with outlook falling to 8. Feb core machine tool order shrank further. But as China/US/Europe

economic data sent positive signal, Japan manufacturing outlook might rebound with recovering external demands.

BOJ Has No Urge To Amend Monetary Policy: BOJ Apr meeting would forecast outlook and inflation of 2021, expecting

some downgrades from 2020. But the downgrades were within market expectation. Considering the relative level of JPY

and 10-yr JGB, 4/27~5/6 golden holidays, and recovering external outlook, we believe BOJ Apr meeting would maintain

monetary policy if Japan/US trade talk is not broken apart. Policy rate would be kept at -0.1% and 10-yr JGB target at 0%.

Japan Large Manufacturer Confidence Fell Most Corporate Inflation Expectation Downgraded

Source: (L)Bloomberg, 2000~2019/3, (R)Nomura, 2014/3~2019/4

11JPY Strategy

JPY Continued To Be In Range Bound

JPY Outlook: BOJ easing tools have approached its limit

but JPY could not depreciate too much due to its risk

Japan Economy In Downward Trend

aversion nature. But Japanese economic data were in the

downward trend while the year end consumption tax hike Goldman Sachs Current

could cause some shocks. BOJ would be unlikely to Activity Index - Japan

tighten this year, trapping JPY in a range bound. We

therefore recommend buy on retracement but no chase 6MMA

principle in JPY investment. JPY/TWD might retrace to

range mid of 0.275 in the next month as the possible

entry point.

JPY Futures Speculative Position Net Short To Enter When JPY/TWD Returned To 0.275

CFTC Futures Net

Speculative Position JPY/TWD

Net Long

Net Short

Source: Bloomberg, 2019/4/17

12US Equity Strategy

Better Than Expected Results Boosted US Equity But With Limited Room

US Corporate Results Kick Start, US Equity Near New High:

Mid To Late Apr As Super Reporting Season

81% of the 42 S&P500 companies results beat expectation.

Results better than the downgraded expectation fuel US equity to

new high. But earnings diverged with mixed results in banking.

Global banks such as Goldman Sachs and Citibank were

dragged by revenue with profits missing target. Domestic banks

benefited from Fed rate hikes with rising consumer loan earnings.

US Equity Approaches Fair Value Of 2019, Further Room

Limited: Earnings might bottom out in 1Q19 but investors long

position was still small with conservative sentiment so we think

2Q19 rally still possible. But considering 2019 consensus growth

of 4% and average P/E of 17X, S&P500 fair price falls to 2975,

near its current level, so further rally would be limited.

S&P500 Quarterly Earning Forecast By Sector S&P500 Approaching 2019 Fair Value

S&P 500 @17x

@15x @16x @18x @19x

2019EPS/本益比 (5年平均)

EPS +2% 2565 2736 2907 3078 3249

ESP +3% 2595 2768 2941 3114 3287

ESP +4%

2625 2800 2975 3150 3325

(市場共識)

ESP +5% 2640 2816 2992 3168 3344

ESP+6% 2670 2848 3026 3204 3382

Source: Goldman Sachs, Compiled by CTBC Bank, 2019/4/12

13Sector Strategy - Growth

Fundamentals Bottoming Out To Peak Season Track

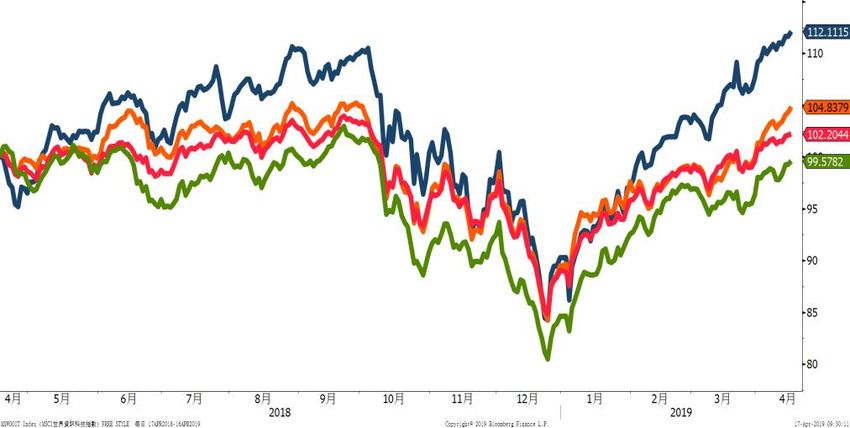

1Q19 Growth Sector Weaker Than Past: Tech has

rallied YTD in 2019 so we think it has correction risk in

Tech Led The Rally YTD In 2019

the reporting season. But central banks stimulus eased (Normalized)

external risks so we think even if it corrects in the short-

term, growth sector could still rebound in 2H19 peak

season with stable and abundant themes.

Market Awaits 2H19 Peak Season Demand:

Economic data slowed YTD in 2019, but it has not Tech

changed the peak/off season demand cycle so far. Consumer Staple

World Index

Therefore, 2H19 demand would still be better than Industrial

1H19 but corporate forecasts were mixed. We caution

possible shocks during the reporting season.

1Q19 Growth Sector Weaker Than Past Tech YOY Positive, Consumer Staple Volatile

公司 日期 QoQ YoY

科 TI 2019/4/23 -11.2% -6.8%

技 INTEL 2019/4/26 -32.0% 0.0%

非

AMAZON 2019/4/25 -22.7% 42.7%

核

心 FORD 2019/4/25 -11.7% -38.4%

3M 2019/4/23 8.4% 0.2%

工

CATERPILLAR 2019/4/24 11.1% 0.5%

業

BOEING 2019/4/24 -23.8% 14.7%

Source:(Top Right)Bloomberg, 2018/4/17-2019/4/16, (Bottom)Bloomberg, 2019/4/2, Compiled by CTBC Bank, 2019/4/16

Note: Sector indices based on Morgan Stanley Capital International (MSCI) global 11 sectors. 14Sector Strategy - Telecom

Clash Of New Setup And Earning Concern, Patient In Consolidation

Telecom Results To Release: Media and entertainment

Market Expectation On Telecom Companies

companies like Tweet, Facebook, Comcast and Google’s parent

company Alphabet and telecom giants Verizon and AT&T would

release their results. From market forecasts, though 1Q19

revenue slowed, growth rate was still double-digit. Profit growth

slowed more profoundly, indicating rising sector saturation as

expenditure squeezed earnings for better contents and network.

Clash Of New Setup And Earnings Concern, Patient In

Consolidation: As market focused on economic growth linked

corporate momentum, telecom might be the first to correct amid

slowing earnings in 1Q19 to reflect the risks. There might be

opportunity of rebound after moderate correction.

Overall Telecom 1Q19 Earnings To Slow

S&P500 Earnings YOY Growth Forecast(%)

Source: (Right)Bloomberg, 2019/4/16, (L)Factset, 2019/4/5, Compiled by CTBC Bank, 2019/4/16

15Sector Strategy - Resource

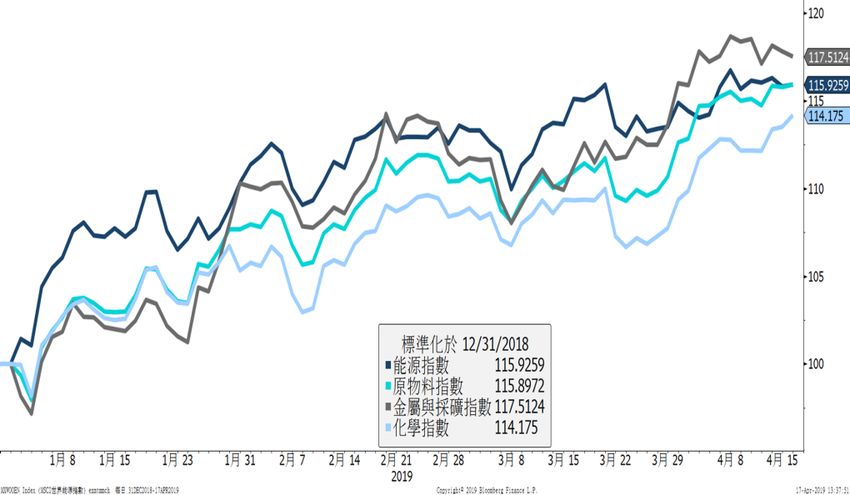

1Q19 Resources Earnings Mostly Fall, 2Q19 Would Recover

1Q19 Energy Results Mostly Contracted: Though 1Q19 Metals And Mining Outperformed YTD In Resource

Brent rebounded due to Jan OPEC+ output cut, base effect

caused 1Q19 energy sector results to contract. We expect

2Q19 oil price to maintain at relative high level with output

growth so 2Q19 earnings could maintain positive but slightly

milder growth. We are positive on 2Q19 MSCI energy index.

Chemicals Contracted: Chemicals 1Q19 sales/margin slid

due to slowing economy, off season and narrow spread. But

2Q19 downstream demand and higher capacity utilization

would boost industrial gas in 1H19. 1Q19 iron ore and

copper prices surged due to supply shock from work safety,

environment protection, improving mining 1H19 earnings.

We are positive on 2Q19 MSCI Commodities.

1Q19 Earning: Mining And Industrial Gas Led 2Q19 Commodity High YOY Growth Due To Mining

Source: Bloomberg, 2019/4/15, Compiled by CTBC Bank, 2019/4/16

16Target Price

Target Price – Rates/FI

spot price 目標價 目標價

第二層 第三層 2019/4/18 2019Q2 2019Q3

美國聯邦基準利率(上緣) 2.50 2.50 2.50

美 美國10Y 2.57 2.70 2.70

巴西利率 6.50 6.75 6.75

歐洲央行再融資利率 0.00 0.00 0.00

德國10Y 0.08 0.35 0.35

英國央行利率 0.75 0.75 0.75

歐 英國10Y 1.24 1.35 1.30

南非政策利率 6.75 6.75 6.75

南非2Y 6.87 7.20 7.35

俄羅斯政策利率 7.75 7.75 7.75

日本央行利率 -0.10 (0.10) (0.10)

日本10Y -0.03 (0.10) (0.12)

中國存準率 13.50 12.5 12.0

亞 中國2Y 2.91 3.00 3.10

台灣央行利率 1.38 1.38 1.38

澳洲目標利率 1.50 1.50 1.25

澳洲10Y 1.95 1.85 1.80

第二層 第三層 2019/4/18 2019Q2 2019Q3

全球投資級債 2.88 3.30 3.14

成熟市場投資級債指數 美國投資級債 3.70 3.99 3.99

歐洲投資級債 0.78 1.20 1.08

全球高收益債 5.83 6.92 6.86

成熟市場高收益債指數 美國高收益債 6.14 6.96 7.13

歐洲高收益債 3.14 4.46 4.14

新興主要貨幣主權債指數 新興主要貨幣主權債 5.78 6.10 6.05

新興主要貨幣企業債 5.71 6.30 6.28

新興主要貨幣企業債指數 新興投資級債 4.07 4.40 4.55

新興高收益債 7.03 8.00 7.70

新興當地貨幣債 6.36 6.65 6.50

新興當地貨幣債指數 人民幣債 3.77 4.05 4.20

亞洲當地貨幣債 4.88 5.30 5.20

Source: Compiled by CTBC Bank, 2019/4/18 : TP Adjustment

17Target Price

Target Price - Equity

spot price 目標價 目標價

第二層 第三層 2019/4/18 2019Q2 2019Q3

成熟市場股 2160.9 2150 2000

美國 2900.5 2900 2600

美

拉丁美洲 2745.8 2800 3000

巴西 93284.8 97000 103000

歐洲 3162.3 2960 3100

英國 4090.6 3800 3920

歐 德國 12153.1 11200 11900

新興歐洲 328.9 292 312

俄羅斯 1259.0 1100 1190

泛太平洋 163.9 160 165

澳洲 6349.9 6200 6500

日本 22090.1 23000 23000

新興市場股 1096.4 1020 1080

新興亞洲 557.8 520 560

中國A 3248.6 2800 3100

亞

中國H 11756.3 11000 12000

香港 29951.0 27500 30000

台灣 10962.0 10500 10650

韓國 2213.8 2300 2350

印度 39165.0 39550 39550

東協 808.7 820 820

科技 265.8 250 260

成長型產業 非核心消費 262.9 253 260

工業 259.4 255 259

金融 117.9 104 107

利率型產業

地產 216.7 205 210

能源 212.5 215 207

天然資源產業

原物料 262.8 265 255

公用事業 135.4 132 130

核心消費 232.9 230 230

防禦型產業

健護 233.1 238 260

電信 71.7 65 69

Source: Compiled by CTBC Bank, 2019/4/18

18Target Price

Target Price – FX/Commodity

spot price 目標價 目標價

第二層 第三層 2019/4/18 2019Q2 2019Q3

美元指數 96.967 96 94

美元兌日圓 111.91 112 110

成熟國家 歐元兌美元 1.1297 1.14 1.17

美元兌瑞郎 1.0098 0.99 0.96

英鎊兌美元 1.3043 1.32 1.32

澳幣兌美元 0.7184 0.69 0.69

商品貨幣 紐幣兌美元 0.6722 0.66 0.65

美元兌加幣 1.3353 1.34 1.35

美元兌台幣 30.836 30.8 30.6

美元兌星幣 1.3536 1.35 1.34

新興貨幣

美元兌人民幣 6.6973 6.85 6.75

美元兌南非幣 14.0309 13.8 13.5

spot price 目標價 目標價

第三層 2019/4/18 2019Q2 2019Q3

布蘭特原油 70.85 75 70

鐵礦砂 92.5 90 85

黃金 1272.08 1330 1350

Source: Compiled by CTBC Bank, 2019/4/18

19GENERAL DISCLAIMERS:

1. This document and the investments and/or products referred to herein are for information only and do not have regard to your specific investment objectives, financial situation or particular needs.

2. This document and the investments and/or products referred to herein should not be construed as any recommendation for you to enter into the investment briefly described above and this document must

be read with CTBC’s General Terms and Conditions including without limitation Risks Disclosure Statements, Supplemental Terms and Conditions and such terms and conditions specified by CTBC from time to

time.

3. You are advised to exercise caution in relation to this document. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice from a licensed or

exempt financial adviser before making your commitment to invest in the investments and/or products referred to herein.

4. If you choose not to seek advice from a licensed or exempt financial adviser or such other independent professional, you should carefully consider whether investment in the investments and/or products

referred to herein is suitable and appropriate for you taking into consideration the risks and associated risks.

5. The final terms and conditions of the proposed investment in the investments and/or products referred to herein will have to be set out in full in the definitive trade confirmation between CTBC and you.

6. CTBC does not guarantee the accuracy or completeness of any information contained herein or otherwise provided by CTBC at any time. All of the information here may change at any time without notice.

7. CTBC is not responsible for any loss or damage suffered arising from this document.

8. CTBC may act as principal or agent in similar transactions or in transactions with respect to the instruments underlying the transaction.

9. Until such time you appoint CTBC, CTBC is not acting in the capacity of your financial adviser or fiduciary.

10. Investments involve risks. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance. Actual performance may differ from the projections in this

document.

11. Any references to a company, financial product etc is used for illustrative purpose and does not represent our recommendation in any way.

12. Any scenario analysis is provided for illustrative purpose only and is no indication as to future performance and it does not reflect a complete analysis of all possible scenarios that may arise under an actual

transaction. All opinions and estimates given in the scenarios are illustrative and do not represent actual transactions.

13. The information in this document must not be reproduced or shared without our written agreement.

14. This document does not identify all the risks or material considerations that may be associated with you entering into of the transaction and the transaction period you wish to consider.

15. This document does not and is not intended to predict actual results and no assurances whatsoever are given with respect thereto. It does not present all possible outcomes or takes into consideration all

factors that may affect or influence the transaction.

16. This document is based on CTBC’s understanding that you have inter alia sufficient knowledge, experience and access to professional advice to make your own evaluation and choices of the merits and risks

of such investments and you are not relying on the CTBC nor any of our representatives or affiliates for information, advice or recommendations of any sort whatsoever.

17. You should have determined without relying on CTBC or any of our representatives or affiliates for information, advice or recommendations of any sort whatsoever, the economic risks and merits as well as

the legal tax and accounting aspects and consequences of the transaction and that you are able to fully assume such risks.

18. CTBC accepts no responsibility or liability whatsoever for any loss of whatsoever nature suffered by you arising from the use of this document or reliance on the information contained herein.

19. CTBC may have alliances with product providers for which CTBC may receive a fee and product providers may also receive fees from your investments.

20. The following exemptions under the Financial Advisers Regulations apply to the CTBC and its representatives:

(1) Regulation 33(1) – Exemption from complying with section 25 of the Financial Advisers Act (“FAA”) when making a recommendation in respect of (a) any designated investment product (within

the meaning of section 25(6) of the FAA) to an accredited investor; (b) any designated investment product (within the meaning of section 25(6) of the FAA) that is a capital market product, to an

expert investor;

(2) Regulation 34(1) – Exemption from complying with section 27 of the FAA when making a recommendation in respect of (a) any investment product to an accredited investor; (b) any capital

markets product to an expert investor or (c) any Government securities;

(3) Regulations 36(1) and (2) – Exemption from complying with sections 25, 26, 27, 28, 29, 32, 34 and 36 of the FAA when providing any financial advisory service to any person outside of Singapore

who is (a) an individual and (i) not a citizen of Singapore; (ii) not a permanent resident of Singapore; and (iii) not wholly or partly dependant on a citizen or permanent resident of Singapore; or (b)

in any other case , a person with no commercial or physical presence in Singapore.

20You can also read