HOW TO FUTURE-PROOF THE GERMAN WIRTSCHAFTSWUNDER - ALLIANZ RESEARCH 23 September 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Photo by khlongwangchao on Shutterstock ALLIANZ RESEARCH HOW TO FUTURE-PROOF THE GERMAN WIRTSCHAFTSWUNDER 23 September 2021 04 Federal election preview: What Germany will get… 08 …what the German economy needs

Allianz Research

Political change is upon Germany, but no major policy overhaul is in the cards.

After the elections on 26 September 2021, Chancellor Angela Merkel will be re-

EXECUTIVE placed after 16 years in power. The transition takes place in a highly fragmented

political context, which will likely see the first three-party coalition emerge at the

federal level and complicate the government-formation process. The significant

SUMMARY dilution of agendas required for an agreement among potentially uneasy political

partners suggests that German politics will see more policy evolution than revoluti-

on over the next four years.

Yet, Germany needs an economic Neustart. Unfortunately, “business as usual” with

at best small, piecemeal reforms are not going to cut it anymore. Germany urgent-

ly needs a major update to ensure that it can master successfully the digital, green

and demographic transitions and in turn safeguard its prosperity.

Making the economy fit for the 21st century. Most parties seem to lack com-

prehensive and concrete plans, though it is high time to finally tackle the well-

known reform „biggies“. These include future-proofing Germany’s institutional

Michaela Grimm backbone (reform and modernization of its federal structure and public admi-

Senior Economist

michaela.grimm@allianz.com nistration), cutting red tape, providing critical (digital) infrastructure,

reforming its education system and fueling the entrepreneurial spirit. Taken

together, these are the pre-requisites for a faster pace of digitization, which in

turn is crucial not only for an effective fight against Covid-19, but also for

achieving climate targets and maintaining an internationally competitive

economy.

Meeting the magic number to limit climate change. The policy targets in al-

Katharina Utermöhl

Senior Economist for Europe most all of the election manifestos are insufficient to limit global warming to

katharina.utermoehl@allianz.com 1.5°C. Carbon prices need to rise and additional policies are required to estab-

lish new technologies and new markets, and to adapt to the already material

damages resulting from climate change. This will affect heating, transport and

food prices and thus particularly burden financially vulnerable households

and businesses, which calls for revenues from carbon-pricing policies to be

used for providing adequate support in the form of transfers and stable

electricity prices.

Markus Zimmer

Senior Expert, ESG

Adapting to demographic change. Most parties shy away from pointing out

the need to adapt Germany’s pension system, promising further increases of

markus.zimmer@allianz.com

benefit levels and freezing the retirement age at 67 instead. However, these

promises will come at the cost of a markedly higher tax-financed state subsidy

of the pension system or a contribution rate of 30% in the long run, which

would mean either curtailing the financial scope for investments in infra-

structure, education and new technologies or undermining Germany’s

competitiveness, not least in the (global) war for talent.

2

23 September 2021

Neustart

Making the economy

fit for the 21st century

3

Allianz Research

FEDERAL ELECTION PREVIEW:

WHAT GERMANY WILL GET...

Political change is upon Germany, but ve been very volatile, with campaigns table coalition partners, namely the

probably not immediately on 26 Sep- marred by sideshow scandals that have right-wing AfD and the Left Party, which

tember and not as far-reaching as nee- seen more emphasis on personality together command around 17% of all

ded for it to master the transformatio- rather than policy substance. As a re- votes. As a result, for the first time in

nal challenges ahead. The federal elec- sult, even a few days before the elec- German post-war history, a three-way

tion on 26 September is bound to bring tions, the race still remains wide open. party coalition is the most likely election

along significant changes to Germany’s In addition, Germany’s political lands- outcome, with a wide array of feasible

political set-up. For one, the vote will cape is becoming increasingly frag- options on the table (cf. Box, opposite).

mark the end of Angela Merkel’s 16- mented, which is bound to complicate .

year chancellorship. Three candidates coalition-building. After all, six parties

stand ready to fill Merkel’s shoes: Olaf are set to enter the Bundestag, of

Scholz for the SPD, Armin Laschet for which none is likely to receive more

the CDU/CSU and Annalena Baerbock than 25% of votes. Moreover, two of the

for the Green Party. However, polls ha- parties are widely viewed as not accep-

4

23 September 2021

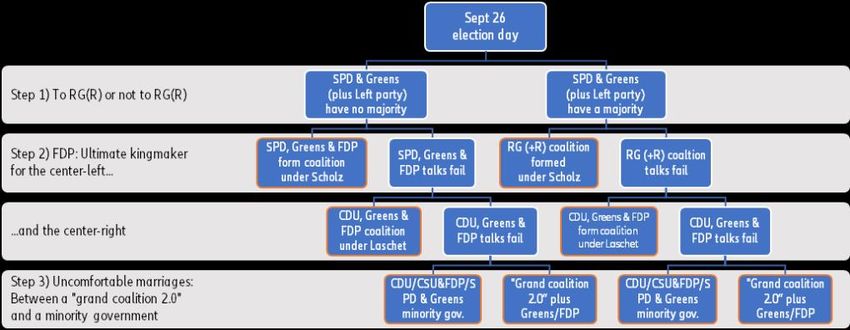

Box: Coalition scenarios

In recent weeks, polls have notably shifted to the left. With the SPD now likely to emerge as the strongest party, it may

dominate the next government coalition. However, the party with the most votes does not necessarily get to decide who takes

the top job, or join the government at all, as seen in the 1976 election, when the CDU under Helmut Kohl won 48.6%

of all votes but lost out against a SPD/FDP coalition. After all, both the CDU/CSU as well as the SPD are unlikely to achieve

a parliamentary majority in their favorite coalition constellation – “Black-Yellow” and “Red-Green” respectively Therefore,

with CDU/CSU, SPD and the Green party all polling at around 20-25%, the focus will be on who can assemble a workable

coalition government (see Figure 1).

Both the “Jamaica” (CDU/CSU, Greens & FDP) as well as the “Traffic light” (SPD, Greens & FDP) coalitions – while only second-

best options – are likely to command a majority in parliament. We think the first option is more likely to materialize since the

FDP in its role as the ultimate kingmaker on both wings of the political spectrum could well demand a high price in return,

such as the finance ministry. In our view, it would prove very difficult to square the “fiscal circle” with the call for a swift return to

pre-crisis government debt levels and no tax hikes on the FDP side and higher investment spending, tax hikes for the top

income bracket and the introduction of a wealth tax on the SPD/Green side.

At this point, even more uncomfortable political pairings such as a Left Alliance (despite differing views on fundamental for-

eign policy issues) as well as a “Grand coalition 2.0” (i.e. “Kenya” (SPD, CDU/CSU & Greens) or “Germany” (SPD, CDU/CSU &

FDP)) should not be ruled out. Yet, the SPD and CDU/CSU are likely to try all alternative combinations before forming another

government coalition together. Even the possibility of a center-left (SPD & Greens) or center-right (CDU/CSU & FDP) minority

government cannot be excluded at this point, though Germany’s only experience in that regard has been at the Länder level

and shelf lives have proved very short.

Figure 1: Coalition combinations—projected seat shares based on opinion polls since end-August (%)

Sources: Various election polls since end-August 2021, Euler Hermes, Allianz Research.

5

Allianz Research

Figure 2: Coalition games cheat sheet

Source: Euler Hermes, Allianz Research

To put it mildly, coalition-building looks government formation process could coalition agreement to emerge among

set to be complicated. Given the more well take until early 2022 and even uneasy political partners likely means

complex task of striking a compromise smash the current record of 172 days that German politics will see more po-

coalition treaty among three parties, that was set in 2017. licy evolution than revolution over the

and in light of notable ideological diffe- In any case, the significant dilution of next four years.

rences (see Figure 4, opposite), the agendas required for a three-party

Figure 3: Government formation process

Sources: Various election polls since end-August 2021, Euler Hermes, Allianz Research.

6

23 September 2021

Figure 4: Overview of key election promises by party

CDU/CSU Green Party SPD FDP Left Party

Taxes Reduce corporate taxes Introduce minimum corporate Tax hikes for top 5% of Reduce corporate taxes to Increase in corporate tax rate

from 30% to 25%, no income tax rate of 25% at EU level, incomes & lower taxes for 25%, no income tax increases, from 15% to 25%, tax hikes

tax increases – tax reduc- tax hikes for top income low and middle incomes, raise top income bracket to for high income households &

tions in line with fiscal earners, introduction of a introduction of a wealth EUR90k. tax cuts for low-income

leeway. wealth tax. tax. earners, one-off wealth levy

(10-20%) introduction of a

wealth tax, boost public

investment.

Public finances Keep debt brake, swift Soften debt brake by exclu- Keep debt brake but take Keep debt brake, limit on Get rid of debt brake.

return to “black” zero and ding investment, EUR50bn of advantage of social expenditures, swift

60% debt ratio public investment per year “constitutional leeway”. return to 60% debt ratio.

over next decade.

Public administration Modernization decade for Anchor digitization in public Organize ambitious politi- Overhaul of the federal struc- Digitize public services,

& federal structure the state: digitizing public administration, boost infra- cal projects in “platforms” ture, modernize and digitize ensure sufficient competent

services, simpler and more structure-planning capacities, that include stakeholders public administration. personnel to maintain/

efficient public administrati- make public administration from across political levels explain digital systems.

on, reform of the federal more innovative, creative and & departments.

structure. inclusive.

Europe No debt union (joint borro- Goal Is a federal European Reform SGP into sustaina- Return to strict SGP rules as Reform SGP, extended EU

wing is a one-off), no wate- republic with a European bility pact, develop EU into soon as possible with reform budget financed by common

ring down of SGP but reform constitution, reform SGP fiscal, social and economic focused on tougher sanctions, debt issuance, ECB to directly

focus on stronger enforce- (more space for investment, union, permanent EU ensure joint borrowing is a one finance public spending,

ment, Banking union (no reduce austerity pressure), recovery fund, European -off, no common deposit financial transaction tax, ESM

common deposit scheme) permanent EU recovery fund, unemployment reinsurance scheme, no common EU taxes. becomes EMF, sovereign debt

and Capital Market Union. common European fiscal scheme, common EU inves- restructuring mechanism.

policy financed by own ting, European banking

resources (digital & carbon union, financial transaction

border tax), ESM becomes tax.

EMF, European banking union

& financial transaction tax.

Labor market Keep HartzIV, no minimum EUR12 minimum wage, EUR12 minimum wage, More flexibility re weekly EUR13 minimum wage, get

basic income, maintain reduction in weekly working abolishing sanctions in working hours. rid of sanctions in unemploy-

social security contributions hours, abolishing sanctions in unemployment benefit ment benefit scheme, boost

at 40%. unemployment benefit scheme. benefits to EUR1200.

scheme.

Climate change 65% reduction in CO2 emissi- 70% reduction in CO2 emissi- Boost investment into Extend emission trading 80% reduction in CO2 emissi-

ons until 2035, climate ons until 2030, national CO2 renewables, mobilize system to all sectors, CO2 ons until 2030, climate neut-

neutrality by 2045, use CO2 price at EUR60 by 2023, CO2 private capital for green revenue rebate for house- rality by 2040, higher contri-

revenues to stabilize electri- revenue rebate for house- projects, shift additional holds, expand emission tra- butions to international

city prices, promote carbon holds, higher contributions to heating costs to landlords, ding and harmonize emission climate finance, free local

capture & storage, CO2 inter-national climate finance, 130km/h on the autobahn, pricing. public transport, nationalize

product labels. shifting additional heating mandatory rooftop solar on railways, coal exit by 2030,

costs from CO2 emissions to public and commercial ban underground carbon

landlords, buildings. capture and storage, shift

2% of land for renewable additional heating costs from

energy, coal exit by 2030, CO2 emissions to landlords,

130km/h on the autobahn, 120km/h on the autobahn,

30km/h in municipalities. 80Km/h outside municipali-

ties, 30km/h in municipalities,

ban short distance flights.

Pension system “Generationenrente” No further increase in retire- No further increase in Flexible retirement age Statutory retirement age of

(publicly financed contributi- ment age beyond 67 years, retirement age beyond 67 (earliest at the age of 60, if 65 years, early retirement at

on to pension fund from stabilization of current pensi- years, guaranteed pension pension entitlements reach at the age of 60 with 40 contri-

birth), state-subsidized on benefit level, publicly benefit level of at least least basic security level), bution years, benefit level of

standard pension product administered pension funds 48%, public pension funds introduction of a capital- 53%, tax-financed minimum

for mandatory private instead of Riester Rente, as vehicle of private pensi- funded pillar into the public pension of EUR1200 per

provision (opt-out), improve- introduction of an employer- on provision (Swedish pension scheme (“Statutory month, higher contribution

ment of cross-border porta- financed minimum contributi- model). Equity Pension”), broader assessment limit and a cap at

bility of occupational pensi- on, guarantee pension of investment opportunities for pension benefits, major share

ons. EUR1000 for people insured pension funds and life insu- of occupational pension

for at least 30 years. rance companies, strengthen- schemes to be solely financed

ing of the demographic factor by employers, abolishment of

in the pension formula, tax deferred compensation.

financing of non-insurance

benefits.

Sources: Various election polls since end-August 2021, Euler Hermes, Allianz Research.

7

Allianz Research

…WHAT THE GERMAN ECONOMY

NEEDS

Unfortunately, “business as usual” with the German economy has lost further Despite various attempts to reform the

at best small, piecemeal reform steps ground since 2018 (cf. Fig. 5, opposite). balance of power, to this day a third of

is not going to cut it anymore. Germany all laws still require the approval from

needs a major update – a Neustart – This is a worrying development since the German Länder. However, in areas

to ensure that it can master successfully updating the German Wirtschafts- where developments have nationwide

the digital, green and demographic wunder is all about speeding up relevance, such as education and pub-

transitions and, in turn, safeguard its digitization, which in turn is key to lic administration, not every German

prosperity. mastering the central challenges of our state should continue to cook its own

time. This is just as true for achieving soup.

Digitalizing the German climate targets as it is for effectively

Wirtschaftswunder combating Covid-19. Looking at the Second, it is high time for Germany

It is no secret that the German econo- parties’ election program, however, to modernize its public administration.

my is facing strong structural head- we see none putting forward the need- The overhaul needs to be comprehen-

winds. Already in late 2019 we raised ed comprehensive approach including sive, from simplifying structures and

the question of whether Germany is a all reform elements required for a procedures to assigning clear responsi-

“stranded” economy1, given its struggle Neustart – and this is before election bilities over moving from paper-based

to keep up with the 21st century tech promises are potentially watered down to digital public services. On the latter

revolution. At the time, Europe’s largest to strike a coalition deal. Germany is a laggard among EU

economy no longer appeared in the countries, taking the 21st place in the

top three of the 2019 World Economic Future-proof Germany’s institutional EU Commission’s 2020 Digital Economy

Forum Global Competitiveness ranking, backbone! and Society Index (cf. Fig. 6, opposite).

falling four places from the year before Before we focus on how to upgrade the

to seventh. If anything, the 2018 German economy’s hard- and software So what do Germany’s political parties

industrial recession should have served let’s start with the reform biggies few promise on this front? FDP and CDU

as a major warning, but it triggered no have dared to address. We see two underline the importance of updating

noticeable policy reaction. Now, with major speedbumps that need to be Germany’s institutional backbone, but

policymakers largely stuck in Covid-19 tackled to make Germany’s institutional for the moment their proposals remain

crisis mode over the past 18 months, backbone fit for the 21st century and vague at times. Meanwhile Green Par-

structural topics appear to have com- set the stage for any major transforma- ty, SPD and Left Party largely focus on

pletely fallen off the government tional process. First, Germany will need digitizing public services but pay little

agenda, despite the pandemic high- to review its federal structure and opt or no attention to modernizing the pub-

lighting Germany’s struggle to adapt to for greater centralization in some core lic administration and reforming the

digital solutions as well as weaknesses areas. While the federal set-up has federal structure.

in public administration. The European many positives, it has proven to be a

Center for Digital Competitiveness’ disadvantage in situations that call for

Digital Riser Index now suggests that swift and unified decision-making, as

highlighted during the pandemic.

1 See our report Is Germany a “stranded” economy?

8

23 September 2021

Figure 5: Digitization progress between 2018-2020 Figure 6: The Digital Economy and Society Index, 2020 Ranking

Source: European Commission.

Sources: Digital Riser Index, European Center for Digital Competitiveness.

9

Allianz Research

Chop down the regulation jungle! the one-in-one-out rule came - if a Governance Report by the Hertie

Taken together, these two reform initia- ministry imposes a new rule on German School of Governance and the OECD2,

tives should already help speed up the businesses, it has to abolish an old one Germany does not do particularly well

German economy’s digitization drive. - with too many exceptions, notably in the planning and implementation of

However, to add further “Wumms” to with EU regulation not covered. A more major infrastructure projects (rank 18

the resulting “simplification shock” calls ambitious approach is needed. One out of 36). Excessive bureaucratic pro-

for a meaningful reduction in the bu- idea could be for each regulation to cedures and demanding legal regulati-

reaucratic, regulatory and legal bur- receive a shelf date, after which it ons are named as the greatest

dens that are usually cited as the big- expires unless the case can be made weaknesses. This does not come as a

gest obstacles to doing business in Ger- for its extension. In terms of priorities, surprise as the number of building re-

many, in particular for Small and Medi- a particular focus should also be put gulations has quadrupled from 5,000 to

um Enterprises (see Figure 7). on the relaxation of reporting require- 20,000 since 1990. Given the urgency to

ments, as well as simplified approval make progress on critical (digital) infra-

Both the CDU and FDP propose some procedures for SMEs – in particular structure projects, such as an upgrade

good ideas to tackle the issue, while in the area of starting a business, of telecommunication infrastructure,

SPD and Greens appear to pay lip ser- where Germany ranks 125th out of special regulatory treatment should be

vice to the cause and the Left Party 190 countries, according to the World given, including fast-track permits.

devotes no airtime at all to the cause in Bank's Ease of Doing Business Survey.

its election program. To put the regula- Moreover, tweaks to Germany’s data Invest in digital hardware…

tion jungle into perspective: In 2015, protection law will be necessary to en- Even on the basic requirements for a

Germany’s Ministry for Economic Affairs sure that it does not stand in the way of successful digital transformation, Ger-

and Energy estimated the annual costs innovation and the adoption of new many is missing the boat. The goal of

to firms from bureaucracy at EUR45 technologies. Furthermore, a notable nationwide coverage with gigabit-

billion – about half the total amount reduction in red tape should also help capable internet connections is still

invested in R&D. Up until now, initiatives tackle Germany’s implementation defi- some way off. Too much copper

to reduce the regulatory burden have cit when it comes to realizing major remains where fiber-optic should be,

proven too timid to leave a notable infrastructure investment projects. particularly in rural areas.

mark. For instance, the introduction of According to the 2016 Infrastructure

Figure 7: Where Germany’s medium-sized firms see risks (share of respondents, in %)

Sources: DZ Bank..

2 Hertie School & OECD, 2016 Governance Report.

1023 September 2021

The results of the World Economic Fo- …and modernize digital software! Furthermore, the proportion of ba-

rum’s Global Competitiveness Ranking The German economy’s digital skill set chelor's degrees in mathematics, sci-

help provide an international context: is in urgent need of an upgrade. ence and engineering is still as high as

With an overall ranking of 72 for fiber- Surveys show that the largest factor it was around 25 years ago, behind that

optic internet connections and 58 for holding back digital competency in of the UK and other countries. A trend

mobile broadband connections when it Germany is a serious lack of adequate towards engineering is not foreseeable.

comes to information technology use, equipment in schools. For instance, Of course, reforming the German edu-

Germany has fallen behind Russia, Chi- according to the IEA's International cation system is a mammoth task and

na, all the Baltic and Nordic countries Computer and Information Literacy solely investing in education will not

and several Gulf countries as well. This Study3 only a quarter of German solve the issue. To make Germany’s

is a problem not simply for households schools has wifi, compared to the inter- education system competitive, a com-

that are unable to stream movies at national average of 64%. In Denmark plete rethink of what is taught and how

home: It also holds back small- and the respective share is 100%. Moreover, it is taught is needed. While the reform

medium-sized businesses in certain in Germany, only 3% of schools equip process needs to take on board local

regions because companies with weak all teachers with their own laptops or and regional best practices,it should be

internet connections work less effec- tablets, compared to 24% for the inter- coordinated at the federal level and

tively. Moreover, fiber is also key for the national average and 91% in Denmark. rolled out nationwide. No political par-

deployment of 5G, which, in turn, is It does not come as a surprise that ty is ambitious enough in its program to

essential for the implementation of German schools struggled to adapt set the stage for a true overhaul of the

major new use cases, such as the Inter- to online teaching during the pandemic education system

net of Things. All parties in favor of when schools were closed. Even more Moreover, to ensure that German firms

more public investment with the Greens worryingly, Germany placed last in the will have adequate access to skilled

even proposing to spend EUR500bn Centre for European Policy Studies’ EU workers, Germany needs to focus much

over the next decade. Yet, without a index of readiness for digital lifelong more on providing incentives for life-

meaningful “simplification shock” that learning.4 The survey concludes that long learning while attracting inter-

aims at speeding up complex planning Germany’s education system is unable national skilled workers at the same

and implementation processes pro- to prepare students with the necessary time.

gress is likely to be limited. digital skills and competencies.

3 IEA ICILS, International Computer and Information Literacy Study (2018).

4 CEPS, Index of Readiness for Digital Lifelong Learning (2019) .

11Allianz Research

Figure 8: Broadband take-up (% households)

Photo by Sigmund on Unsplash

Source: European Commission DESI 2020.

1223 September 2021

Awake the entrepreneurial spirit! were clearly neglected (see Figure 9). programs of CDU and FDP, they don’t

There is arguably a lack of entrepre- Interestingly, while startup activity rose feature in the pamphlets of SPD and

neurial spirit in Germany. In 2018, ac- in the US in 2020, in Germany the num- Left party at all. Meanwhile the Greens

cording to a survey by the German de- ber of startups fell by -12% to 201,000 - mention them once but offer no com-

velopment bank KfW5, only a quarter another record-low. It is high time to go prehensive strategy aimed at grass-

of the German working population on the offensive to awaken the German roots start-ups.

would have liked to be their own boss - entrepreneurial spirit. Again, a compre-

a record low. As recently as 2000, the hensive approach is essential: from

comparable figure was 45%. If any- founder scholarships, government sup-

thing, the Covid-19 economic shock has port for university-affiliated startup fac-

probably further reduced that figure. tories and “innovation clusters” to more

After all, the support measures imple- attractive modalities around employee

mented during the crisis did a good job participation in startups and taxes, as

at getting established companies well bureaucratic relief in the first years

through, but startups - the potential of life. While start-up founders will find

future stars of the German economy - many good reform ideas in the party

Figure 9: Founders’ views on Germany as a start-up location

2018 2019 2020

Free market access 2.4 2.2 2.3

Advisory services* 2.8 2.7 2.6

Business founder image 2.5 2.4 3.1

Protection of IP 2.8 2.7 3.1

Quality of public infrastructure 2.6 2.7 3.2

Financing with promotional loans 3.4 3.1 3.3

Financing with bank loans 3.7 3.7 3.7

Financing with venture capital 3.3 3.1 4.0

Legal regulations* 3.1 3.0 4.3

Tax burden* 3.6 3.5 4.4

Policymakers’ commitment** 3.8 3.4 4.5

Educational system** 3.9 3.9 4.5

Bureaucracy (information & reporting duties) 3.6 3.3 4.6

Source: KfW Entrepreneurship Monitor

Note: * Pertaining to concerns of business founders, self-employed persons and entrepreneurs,

**With respect to the teaching of business knowledge and skills

5 KfW Gründermonitor (2020).

13Allianz Research

Green transition:

Rise to the challenge!

Mastering the green transition is the likely pursue climate targets that are tion until 2030 sounds good but being

make-or-break challenge for the Ger- still not in line with limiting global war- on a 1.5°C path would rather require

man economy. And although there is ming to 1.5°C, the proclaimed aim of reductions of around 65%. The next

broad consensus on the overwhelming the Paris Agreement and the tempera- German government will therefore face

importance of the topic, party pro- ture rise at which the damages from the rare task of being more radical in

grams differ markedly in the ways to climate change are expected to exceed its policymaking than its programming

address it – with only one party fully the economic benefits of fossil fuel usa- and will have to rise to the challenge.

up to the challenge. This is shown in by ge. It is only weak consolation that the But what exactly needs to be done so

Figure 10, which illustrates the range of same must be said for the supposedly that Germany – and the EU – can pivot

ambition using the aspired date of ambitious EU Green Deal measures to the 1.5°C path?

climate neutrality and the coal exit proposed in the “Fit for 55” package,

as well as the 2030 emission target. which would likely result in a long-term

The uncomfortable truth is that the next temperature increase of more than

German government will most 2.0°C. The aspired 55% emission reduc

Figure 10: Climate target comparison

Source: Euler Hermes, Allianz Research and Helmholtz-Klima. Temperature alignment is derived by comparing the targets with complementary analysis and

pathways from Climate Action Tracker, CAN Europe and OXFAM6. * Wants to include CO2-reductions outside of the EU to national reductions. ** Wants to

update targets according to new scientific findings and to refrain from national targets in favor of EU compliance with EU targets. Also wants to include

CO2-reductions outside of the EU to national reductions. *** Wants to abolish neutrality, exit or emission targets. Bars extend further up than shown.

6 https://www.oxfam.org/en/press-releases/fit-55-package-not-fit-tackle-climate-emergency-says-oxfam

https://www.helmholtz-klima.de/aktuelles/klimapolitik-wahlprogramme-bundestagswahl2021

https://climateactiontracker.org/climate-target-update-tracker/eu/

https://caneurope.org/press-release-fit-for-55-climate-energy-eu-commission-package/

https://climateactiontracker.org/publications/germanys-proposed-2030-national-target-not-yet-15c-compatible/

https://climateactiontracker.org/countries/eu/ .

1423 September 2021

Without a carbon price, all is nothing! structure projects require a carbon investment demand for the energy

The policy framework needs to provide price beyond the implemented levels transition at about EUR30bn per year,

financial incentives for a quicker decar- to be competitive versus their fossil which will hardly be met without

bonization while limiting economic fuel-based alternatives, carbon con- private-public partnerships for the

costs for current and future generati- tracts for difference provide an additio- investment needs.

ons. The most effective tool in speeding nal financial benefit that compensates

up the transition is to raise carbon pri- for the difference and makes the Still, the estimated EUR30bn does not

ces and apply them to project attractive for investors. cover another important aspect: As

a broader base of emission sources. climate change is already imminent

Research suggests that to reach clima- Another instrument is a credit-enhance- and damages from floods and droug-

te goals carbon prices in the national ment arrangement between a public hts are accumulating, policymakers will

German emission trading system will player, say, a development bank, and a also have to address adaptation.

need to rise to at least EUR100 in the private investor. The new government Among other measures, this needs to

next five years, thus notably higher must explore and use these public- include a discussion on how to ensure

than the currently aspired EUR55-65 by private partnerships to the greatest the insurability against weather extre-

2026. Although carbon prices are the extent because crowding in private mes. This discussion is not only about

most powerful and effective way to capital is key to the green transition, the introduction of different forms of

advance the green transition there are not least with regard to speed: The mandatory insurances but should also

some cases – for example path depen- secret to opening up markets to new aim at the provision of protection infra-

den-cies resulting from long investment technologies is the quick scaling-up to structure and warning systems.

cycles or the establishment of markets drive costs down. For that, a combinati-

for new technologies – where additio- on of the risk capacity of the public

nal instruments might be required, sector and the knowhow and capital of

namely so-called carbon contracts the private sector is inevitable. AGORA

for differences (CCfD). When infra- Energiewende specifies the additional

7 In principle, carbon prices should reflect the damage caused by greenhouse gas emissions, the so-called social cost of carbon. Scientific estimates of these

damages vary considerable with a median of USD85 (EUR72) in 2020 which is expected to rise to USD145 (EUR123) by 2030 https://www.unepfi.org/

publications/discussion-paper-on-governmental-carbon-pricing/.

8 E.g. https://static.agora-energiewende.de/fileadmin/Projekte/2021/2021_06_DE_100Tage_LP20/A-EW_229_Klimaschutz-Sofortprogramm_WEB.pdf.

15Allianz Research

Save the climate – and the people! The A new harvest – CO2! Agriculture is the emission-intense alternatives. This in-

efficiency of energy use by households often-overlooked piece in the climate cludes the expectations for electricity

has to dramatically increase. policy puzzle, but its role is decisive and price developments. Thus, a credible

But a further tightening of energy manifold: It is supposed to capture regulatory framework is needed that

standards for new buildings can only massive amounts of CO2 and perman- decouples electricity price increases

contribute a little to the climate goals.

ently store it in the ground, to provide from carbon price increases.

What is required is rather a tripling of

large amounts of renewable energy,

the energy renovation of existing The decarbonization of the transport

promote biodiversity and, last but not

buildings. Suggested measures like sector hinges upon the right infrastruc-

mandatory insulation and rooftop least, limit food price increases. This will

ture in place. The new government

photovoltaics installation are cost- require a rethinking of agricultural zon-

should not waste time and should

intensive and will lead to further rent ing with respect to the co-use of land

speed up the roll-out of the necessary

increases. On the other hand, shifting for agriculture, energy production and

infrastructure not only for electric

the costs to landlords reduces the carbon storage. But the essential step

vehicle charging and hydrogen

incentives to invest in the needed addi- would be to create and promote car-

refueling, but also for the complemen-

tional housing space, which will also bon markets that provide sound reve-

tary smart IT solutions, including data

fuel a further rise in rents. Either way, nues to incentivize investments in the

increasing rents are done deal. exchange via 5G networks. As mentio-

co-use activities. Goals for co-use inclu-

Moreover, a reduction in energy ned in the context of the general

de agri-photovoltaics (the combined

consumption needs to be incentivized non-climate-related challenges, the

use of agricultural land for photovoltaic

by raising the price for heating and progress in the energy transition

energy production, e.g. by installing

gasoline. All this can be more than depends on the progress in digitization

challenging for low-income house- solar panels on stilts above meadows)

and the availability of skilled personnel.

holds. Considering the average emissi- as well as agri-forestry (e.g. planting

The roll-out of smart meters and prosu-

ons of a German citizen of around energy wood stripes within fields). In

mer or community electricity models

9 tons of CO2 per year, and a cost pass addition, the agricultural sector is sup-

requires adequate regulatory frame-

-through of EUR50 per ton of CO2, this posed to reduce its emissions from live-

works for data protection, building law

could sum up to EUR1800 per year in a stock and fertilizers, which from a glo-

and zoning regulations; a reduction of

four-person household. It is therefore bal emission perspective will only be-

bureaucracy and the acceleration of

essential to use the revenues from nefit the climate if consumer prefe-

carbon-pricing policies to compensate approval processes.

rences also shift towards eating less

for financial hardships, securing a just meat and more sustainable and pro-

transition. This is the double dividend

bably more expensive food.

of carbon prices, mitigating harmful

greenhouse gas emissions by increa- Spark the electrification! Decarbonizing

sing emission costs and also generating industry means first and fore

revenues that can be used to financially most the electrification of processes,

compensate particularly burdened which has to be leapfrogged. Besides

households. The latter should be the portfolio of support measures,

done in two forms: direct lump-

including subsidies, loans and preferen-

sum transfers like the so-called “Klima-

tial tax write-offs, electricity prices will

prämie” (climate bonus) and a stabi-

play a key role. Investments in electrifi-

lization of electricity prices, which

would also particularly benefit lower cation require electricity prices to

income households. increase much slower than the costs for

1623 September 2021

The emission reduction in hard-to- promotes the integration of electricity structure has to dramatically speed up.

abate sectors such as steel or the che- production and storage capacities This includes tripling the installed pho-

mical industry depends on a sufficient from, say, home storage or electric ve- tovoltaics until 2030 as well as tripling

supply of green hydrogen. This is a hicle batteries and thus technically the tenders for onshore wind develop-

complex task demanding tight coordi- enables the electrification of most of ment. This requires the allocation of

nation between European countries the economy. As already mentioned, to sufficient areas, which will cause land-

and regulations in which carbon keep the necessary investments econo- use conflicts. The potential solutions to

contracts for difference will have a mically sensible, carbon price revenues these conflicts, such as rooftop- photo-

central role. Ramping up the necessary should be used to stabilize electricity voltaics or the above mentioned agri-

infrastructure will also require close prices. To pivot to the 1.5°C path, the photovoltaics, come with additional

cooperation with regions outside of the German coal exit needs to be brought costs. In general, the expansion of rene-

EU as the necessary capacity won’t be forward from 2038 to 2030. As coal wables is exposed to acceptance issu-

available within the EU. This provides profitability and CO2 prices in the EU es, “not in my backyard” mentalities

an opportunity to support economic ETS are directly linked, the best solution and lengthy approval processes. In par-

growth and political stability, for in- would be to reach emission prices in ticular, biodiversity and climate protec-

stance in African countries that have the EU ETS that drive coal power plants tion are often conflicting issues. For a

particularly beneficial conditions for completely out of the EU market and better balance, biodiversity and climate

the expansion of renewable capacities. thus also prevent carbon emission change need to be viewed and asses-

leakage to other EU countries. The se- sed as a joint concept that is not

A happy couple – production and

cond-best option is to strictly coordina- focused on a local assessment but ac-

storage! Electricity is at the core of the

te the coal exit in the EU to prevent counts for the larger national and inter-

energy transition. Electricity production

emission leakage to other, potentially national picture. Decision processes

from renewables is no longer an issue:

more polluting, coal power plants. have to speed up, and the participation

Wind and solar energy are cheaper

of local citizens and communities in the

today than their dirty equivalents from Another challenge is to meet the ex-

financial benefits can increase accep-

coal, gas or oil. Availability and utilizati- pected energy demand: the develop-

tance.

on are the next challenges. The solution ment of photovoltaics and wind as well

is the so-called sector coupling, which as of transmission and storage infra-

17Allianz Research

Demographic transition:

Make aging a boon, not a bane!

An ostrich policy will not prevent demo- in retirement age is set to increase by needed to adapt the pension system

graphic change and its consequences 22%, from 18mn to more than 21mn. but with baby boomers starting to reti-

for the German pension system. With That means that even if 100% of the re, the window of opportunity is getting

respect to pensions, most parties’ elec- population in working age contributes smaller. One possible measure would

tion programs are rather generous, to the pay-as-you-go financed pension be a gradual increase of the retirement

promising that the retirement age will system, there are going to be 46 per- age to 70 years from 2035 onwards. It

not increase above 67 years and the sons in retirement age per 100 persons would not only dampen the increase of

benefit ratio will remain at 48%, obvi- in working age. Today this ratio is at the old-age dependency ratio and sta-

ously ignoring the reality of demogra- 32%. In other words, two people in wor- bilize it in the long run on a level of

phic change. Despite the already ag- king age will be needed to finance the around 37%, but it would also add an

reed upon gradual increase of the pen- pension of one retiree. additional 3mn persons to the labor

sion age to 67 years, Germany’s work- force in 2060 (see Figure 11).

ing age population is expected to Like every pay-as-you-go financed pen-

shrink within the next four decades by sion system, the German one is not im-

15%, from 54mn today to 46mn in mune to the effects of demographic

2060. At the same time, the population change. Further reforms are urgently

Figure 11: Development of working-age population and OADR 2010-2060

Sources: German statistical office, Euler Hermes, Allianz Research.

9 Here from the age of 15 to retirement age.

See Bundesamt für Statistik (2019), 14. Koordinierte Bevölkerungsvorausberechnung, Variante 2.

1823 September 2021

The momentarily favored ostrich policy with measures to enable a higher king and aging while the number of

comes at a price. Keeping the retire- labor market participation of women retirees increases. While in Germany a

ment age and the benefit ratio and older workers and employees: for 10% decrease of the population in

constant would imply in the long example, the provision of nursing care working age is expected, this age

run either a federal subsidy to the facilities for children and elderly family group is set to shrink by 31% in Bulga-

pension system of close to 100% of the members who require care, which ria, 27% in Spain and 25% in Poland

contributions, which amounted to is today in most cases provided by and Romania, for example. Therefore,

EUR247.9bn10 in 2019, or a contribution family members. Furthermore, it needs there will be a competition for high-

rate of around 30% to finance the pen- training offers for a smooth transition qualified specialists in the future and a

sion benefits. Both are inconceivable. into the new work environment that will need for an attractive labor market

Higher subsidies from the general be more and more characterized by environment. Against this background,

budget undermine the state’s capabili- digitization and automation, and espe- to avoid overburdening future genera-

ty to manage the green transition, ad- cially labor market reforms that allow tions, there is an urgent need to be ho-

ding insult to injury to the young gene- people to work longer. Otherwise, any nest about the necessity of further pen-

ration. And higher contributions dent increase of the retirement age would sion reforms. These will imply a combi-

the productivity of German companies be nothing but a hidden cut of the nation of a higher contribution rate, a

– with the same result for the young benefit ratio. further decrease in the benefit ratio

generation. and an adjustment of the retirement

To hope for immigration to be the

age to the development of the further

However, raising the retirement age is remedy for any demographic challen-

life expectancy at retirement age,

not the silver bullet to markedly reduce ge might prove to be in vain. The main

which is expected to increase by more

the financial burden on future generati- sending countries (Romania, Bulgaria

than three years for 65-year-olds until

ons. In our model, the federal subsidy – and Poland), like most other EU count-

2060.

paid out of taxpayers’ money – would ries and many major economies

have to increase above 80% in around around the globe (such as Japan

2040 or the contribution rate would or South Korea) all face the same

reach 26%. It only works in combination challenge: their labor forces are shrin-

10. See Deutsche Rentenversicherung.

11. See UN Population Division, World Population Prospects 2019 Revision.

19Allianz Research

OUR TEAM

2023 September 2021

RECENT PUBLICATIONS

22/09/2021 Climate policy: Time for a "blood, toil, tears and sweat" speech

17/09/2021 Global economy: A cautious back-to-school

15/09/2021 European food retailers: The bitter digital aftertaste of the Covid-19 legacy

09/09/2021 Life after death: The phoenix-like rising of Japan´s life industry

08/09/2021 Export performance in Europe: a sink or swim game

02/09/2021 ECB: Roaring reflation no reason to flinch

01/09/2021 European SMEs: 7-15% at risk of insolvency in the next four years

30/07/2021 Europe´s pent-up demand party is just getting started

28/07/2021 Australia´s pension system: No reform can replace financial literacy

27/07/2021 Chip shortages to boost carmakers´pricing power in Europe

22/07/2021 Corporates need half a trillion of additional working capital requirement financing

21/07/2021 SPACs: Healthy normalization ahead

15/07/2021 EU CBAM: Well intended is not necessarily well done

13/07/2021 Postponed motherhood may help narrow the income and pension gaps

08/07/2021 Global trade: Ship me if you can!

05/07/2021 France vs Germany: No #Euro2020 final but a tie against Covid-19

01/07/2021 This is (Latin) America: The unequal cost of living

30/06/2021 China´s corporate debt: Triaging in progress

24/06/2021 Emerging Markets debt relief

23/06/2021 Allianz Pulse 2021: Old beliefs die hard

17/06/2021 The Covid-19 crisis emphasizes wider fertility challenges

15/06/2021 US yields: Where the music plays

11/06/2021 G7 corporate tax deal: who is winning, who is losing?

09/06/2021 Grand reopening: new opportunities, old risks

02/06/2021 European corporates: It could take 5 years to offload Covid-19 debt

31/05/2021 The flaw in the liquidity paradigm: Lessons from China

27/05/2021 French export barometer: 8 out of 10 companies aim to increase exports in 2021

26/05/2021 Semiconductors realpolitik : A reality check for Europe

20/05/2021 Eurozone government debt - Quo vadis from here?

19/05/2021 Abolishing fuel subsidies in a green and just transition

14/05/2021 Drivers of growth: Property & Casualty insurance

Discover all our publications on our websites: Allianz Research and Euler Hermes Economic Research

21Director of Publications: Ludovic Subran, Chief Economist

Allianz and Euler Hermes

Phone +49 89 3800 7859

Allianz Research Euler Hermes Economic Research

https://www.allianz.com/en/ http://www.eulerhermes.com/economic-

economic_research research

Königinstraße 28 | 80802 Munich | 1 Place des Saisons | 92048 Paris-La-Défense

Germany Cedex | France

allianz.research@allianz.com research@eulerhermes.com

allianz euler-hermes

@allianz @eulerhermes

FORWARD-LOOKING STATEMENTS

The statements contained herein may include prospects, statements of future expectations and other forward -looking

statements that are based on management's current views and assumptions and involve known and unknown risks and

uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such forward

-looking statements.

Such deviations may arise due to, without limitation, (i) changes of the general economic conditions and competitive situ-

ation, particularly in the Allianz Group's core business and core markets, (ii) performance of financial markets

(particularly market volatility, liquidity and credit events), (iii) frequency and severity of insured loss events, including

from natural catastrophes, and the development of loss expenses, (iv) mortality and morbidity levels and trends, (v) per-

sistency levels, (vi) particularly in the banking business, the extent of credit defaults, (vii) interest rate levels, (viii) curren-

cy exchange rates including the EUR/USD exchange rate, (ix) changes in laws and regulations, including tax regulations,

(x) the impact of acquisitions, including related integration issues, and reorganization measures, and (xi) general compet-

itive factors, in each case on a local, regional, national and/or global basis. Many of these factors may be more likely to

occur, or more pronounced, as a result of terrorist activities and their consequences.

NO DUTY TO UPDATE

The company assumes no obligation to update any information or forward -looking statement contained herein, save for

any information required to be disclosed by law.

22You can also read