INDEPENDENT POWER PRODUCERS - INFORMATION BRIEF - Squarespace

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INFORMATION BRIEF

INDEPENDENT POWER PRODUCERS

Since 2011, the Renewable Energy Independent Power Producers Programme (REIPPPP) has facilitated private investment in

utility and small-scale wind, solar, hydro and waste to energy generation infrastructure, making a small but critical contribution

to the energy system (1). Independent Power Producers (IPPs) have been the subject of ongoing misinformation and confusion

in South Africa, linked to the role we want the private sector to play in the electricity sector, but there are some basic facts

that must ground this public debate.

1. WHAT ARE IPPS?

IPPs are private sector energy generators. IPPs are a common element of most

electricity sectors around the world. The legislation and policy that controls who may

“An incremental

invest, in what technology, how, and whether the state takes control of infrastructure

at the end of the IPP contract, differs by country. approach allows

decision-makers to

IPPs are a relatively new phenomenon in South Africa, but the private sector has always

played a role in the electricity sector. Currently, most of the power plants in South build consensus on one

Africa are owned by Eskom and run on coal. The coal mines that supply these power step at a time, to take a

stations are privately owned, and the suppliers that provide a range of goods and

country forward. Some

services, including construction of new power plants, such as Medupi and Kusile, are

private companies too. of the benefits of

unbundling could also

In South Africa, the IPP Office in the Department of Energy (DOE) runs several IPP

programmes that enable investment in different kinds of technology: large-scale be realised over a

renewables; small renewables; coal; cogeneration; gas; and the Solar Parks project that shorter period than if a

will focus on large solar projects, specifically. The country’s latest draft Integrated

total overhaul is

Resource Plan (IRP) 2018 does indicate plans for two coal IPPs, for which a request for

proposals (RFQ) was issued in 2014. However, these plans have run into financial issues pursued from the

and other hurdles. This note will focus on renewable energy IPPs, in line with President beginning.”

Ramaphosa’s latest announcements on South Africa’s energy future.

THE RENEWABLE ENERGY INDEPENDENT POWER PRODUCERS

PROGRAMME (REIPPPP)

Functioning since 2011, REIPPPP is the procurement vehicle that the IPP office has used to enable private sector investment

in large (larger than 5MW) and small (1MW-5MW) solar, wind, biomass, biogas, landfill gas, and hydro energy generation (1).

HOW MUCH ENERGY DO WE GET FROM REIPPPP?

Renewable energy IPPs currently contribute approximately 5% of total electricity generated in South Africa. However, given

the recent supply crisis and load-shedding, the President has announced Cabinet’s intention to increase the level of investment

in renewable energy IPPs, and therefore also their contribution to South Africa’s energy mix. More IPP investment does mean

more private sector participation in the sector, but as things stand, there are no plans to privatise any state-owned assets.

Independent Power Producers | Page 12. WHY DO WE HAVE RENEWABLE ENERGY IPPS?

The 1998 White Paper on Energy Policy was the first official national policy that proposed extensive reform of the electricity

sector, which included both the introduction of renewable energy and private sector participation in the electricity sector.

Since then, there have been other policies, programmes and legislation to drive renewable energy generation and private

sector participation.

It is important to note that renewable energy infrastructure can be state-owned or privately owned. Eskom owns the Sere

Wind Farm in the Western Cape, which was commissioned in 2015 and has a 100MW generation capacity. The rationale for

investing in publicly or privately owned renewable energy has two main components:

1. Renewable energy can replace fossil fuels that contribute to global climate change, as well as a range of risks,

including air pollution, water pollution, and human health impact for people working in coal mines, and people living

near power plants.

2. Renewable energy costs are decreasing year on year. Bids awarded in Bid Window 4, shown in Error! Reference

source not found. (awarded in 2015) are the most recent bids to have been awarded for both wind and solar

photovoltaic (PV) energy and are the cheapest to date. The latest local prices achieved are globally competitive,

coming lower than procurement in the same year in India, Brazil and Chile (2). These prices are expected to keep

decreasing.

Table 1: Average tariffs offered by solar PV and onshore wind projects over bid windows expressed in 2018 ZAR/kWh (3).

TITLE ROUND 4 ROUND 4

ROUND 1 ROUND 2 ROUND 3

(A&B) EXPEDITED

Wind (R/kWh) 1.66 1.31 0.96 0.76 0.68

Total reduction

-59%

from round 1 (%)

Solar PV (R/kWh) 4.02 2.40 1.29 0.96 0.68

Total reduction

-83%

from round 1 (%)

Introducing IPPs into South Africa’s electricity sector has introduced competition in energy generation, which was previously

dominated by Eskom, with only a few exceptions of city government ownership, including Cape Town and Johannesburg

owning their own thermal power plants . There are three main aspects to the rationale for allowing the private sector to

participate in energy generationi:

1. Cost-saving: Having more than one service provider for the same service (e.g. different generation companies)

creates an environment where companies compete with each other to provide lower prices and innovative products

(e.g. new technologies), ultimately benefiting the consumer.

2. Risk management and resilience: Horizontal unbundling e.g. different generation companies) also increases the

resilience of an electricity sector. This is because including multiple actors allows for the diversification of power

Independent Power Producers | Page 2sources. If one power company or technology experiences challenges, others continue to operate. This reduces

electricity supply risk.

3. Eskom’s ballooning debt: Eskom is in the grip of a financial crisis, struggling to pay its increasing debt and unable to

secure lending at a reasonable cost. It is currently not financially able to finance the required additional renewable

energy generation infrastructure to support our local energy security.

3. HOW ARE RENEWABLE ENERGY IPPS SELECTED?

REIPPPP run competitive auctions, whereby local and international bidders present plans for infrastructure development that

are assessed on strict criteria. REIPPPP bids are adjudicated on the basis of a 70% weighting for the price (bid tariff), and 30%

for economic development components.

Economic development components are captured in the Balanced Scorecard Evaluation Score Sheet that measures seven

performance areas that are tailored to the renewable energy sector: job creation, local content, enterprise development (ED),

socioeconomic development (SED), ownership, management control, and preferential procurement. This replaces and

expands on Broad-Based Black Economic Empowerment (BBBEE), which usually only accounts for 20% of public procurement

evaluation, in line with the Preferential Procurement Policy Framework Act (2000), the BBBEE Act (2003), and subsequent

regulations (4,5)1. A breakdown of Balanced Scorecard criteria is provided in Table 2.

Table 2: REIPPPP economic development criteria for Round 4 (5,6)

REQUIREMENT %ECONOMIC MINIMUM THRESHOLD AND TARGET

DEVELOPMENT SCORE

1. Job creation in RSA 25% • Citizens: 50% minimum; 80% target

• Black people: 30% minimum; 50% target

• Skilled Black employees: 18% minimum; 30% target

• Citizens from local communities: 12% minimum; 20%

target

2. Local content 25% 40% of total project cost minimum; 60% target

3. Enterprise development 5% No minimum; 0.6% of revenue target

(ED) spend

4. Socioeconomic 15% 1% of total project revenues target minimum; 1.5% target

development (SED) spend

5. Ownership 15% • Shareholding by Black people and enterprises: 12%

minimum; 30% target

• Shareholding by local community: 2.5% minimum; 5%

target

1 There are six elements to BBBEE: ownership, management control, skills development, preferential procurement,

supplier development and enterprise development (ED), and socio-economic development (SED) (encompassing

corporate social investment). Some industries are subject to sector-specific requirements.

Independent Power Producers | Page 3• Shareholding by Black people and enterprises in the

construction contractor: 8% minimum; 20% target

• Shareholding by Black people and enterprises in the

operations contractor: 8% minimum; 20% target

6. Management control 5% No minimum; 60% target

7. Preferential procurement 10% • BBBEE: no minimum; 60% target

• SME and QME: no minimum; 10% target

• Women-owned businesses: no minimum; 5% target

Public procurement can be extremely challenging, as large government contracts have been attractive to corrupt interests

seeking to exploit public resources for private gain. However, to date, REIPPPP has been commended for its good governance,

which is a significant achievement, especially when contrasted with Eskom procurement of private goods and services.

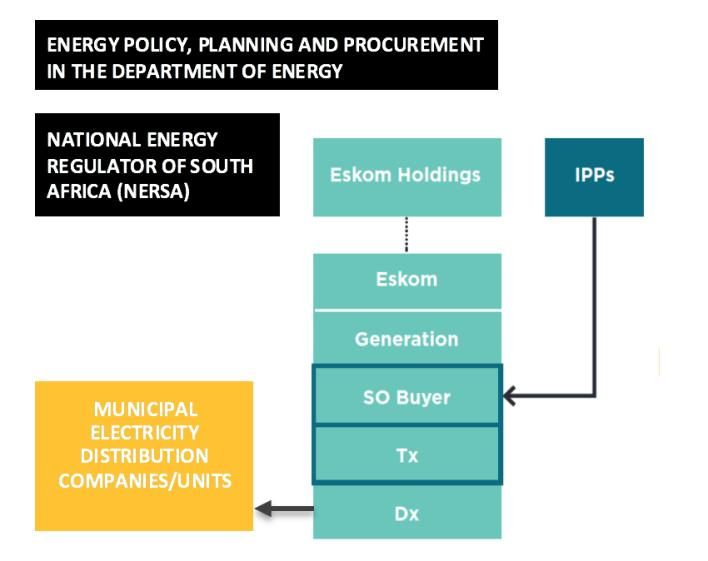

4. HOW DO IPPS FIT INTO THE SOUTH AFRICAN ELECTRCITY

SECTOR?

IPPs contribute to the total amount of electrcity that

the South African government thinks we need to

support our economy. Based on how much electrcity

the DOE thinks we need, the Minister of Energy must

make a determination in terms of Section 34 (1) of

the Electricity Regulation Act, the Minister of Energy,

in consultation with NERSA, to allow for new energy

generation capacity to be built. These Ministerial

Determinations may also make other specifications,

in line with the Electricity Regulations on New

Generation Capacity (published as GNR. 399 in

Government Gazette No. 34262 dated 4 May 2011,

as amended on 19 May 2015) (New Gen Regulations).

Specifications include specifying the buyer (Eskom or

other), and the procurement mechanism, for

example, a bidding process for any new energy Figure 1: South Africa’s current electricity sector structure

capacity (7). Once the Minister makes the determination

for how much energy we need, and from which

technology, a process begins:

1. The IPP Office must arrange a bidding process meeting the Minister’s requirements.

2. Eskom is required to develop a off-take agreement (purchasing contract) with each IPP even before they are allowed

to bid for the right to generate electricity.

3. Companies submit their bids, in line with accepted criteria.

4. Successful bids are selected by the IPP Office.

5. Successful bidders must legally contract with Eskom’s system operator and buyer (SO buyer) at the tariff set out in

the successful bid for an agreed period.

6. When the IPP has successfully been built and commissioned, it sells electricity to Eskom, which transports this

electricity via the national transmission grid (Tx), to local distribution grids (Dx) operated by Eskom and municipal

governments.

Independent Power Producers | Page 4Within the current regulations, IPPs can only sell their electricity directly to Eskom. There are a few exceptions. In 2013, NERSA

awarded PowerX (then Amatola Green Power) an energy trader license, allowing it to buy electricity from IPPs and sell this on

to consumers. Nelson Mandela Bay Municipality (NMBM) signed a 15-year ‘wheeling' agreement with PowerX, allowing it to

play this role within its boundary, using the local distribution grid to transport this electricity (8). The City of Cape Town (CCT)

Mayor Patricia de Lille announced in January 2017 that the City would take the Minister to court over the right to purchase

energy directly from IPPs, without having to go through Eskom (9). Additionally, because Eskom serves as intermediary, the

REIPPPP's cost savings over time have been internalised in its complex accounting system, covering its many different

functions.

5. WHAT ARE THE MAIN CONCERNS ABOUT IPPS?

While REIPPPP has been successful in many ways, there are many concerns that need to be addressed in further rounds of

implementation, which President Ramaphosa has confirmed to be part of South Africa’s energy strategy.

ISSUE EXPLANATION

There is no clear, broadly supported, long-term strategy on the role we would like the private

The role of the private

sector to play in the electricity sector. The private sector is involved in South Africa’s electricity

sector

sector through:

• The provision of finance to Eskom

• The provision of goods and services to Eskom, including increasingly expensive and corrupt

coal contracts,

• Finance, construction, operation and ownership of IPPs

Ownership Because of South Africa’s unequal distribution of wealth and access to resources, there have been

concerns over foreign ownership and a lack of socio-economic transformation in REIPPPP. There

are alternative approaches in IPPs in countries, like Uganda, where IPPs hand ownership of

infrastructure back to the state after their contracts end. These policy options could also be on the

table in South Africa.

The cost of IPPs to There is a lot of misinformation about the cost of IPPs to Eskom. What is true is that the first rounds

Eskom of REIPPPP procurement were not yet competitive with Eskom’s coal-fired power prices. However,

this is not the case anymore. The reason is that the technology and market has evolved, and RE

IPPs are likely to get cheaper.

The success of the Eskom delayed signing contracts with success Round 4 IPPs between 2016 and 2018, which has

REIPPPP was hinged on had negative impacts for the sector, including local manufacturers. An important motivation for

Eskom's willingness and unbundling is to allow Eskom transmission to freely contract with independent power producers

ability to enable (IPPs) and Eskom generation without the conflict of interest that currently exists. This is seen as

connection to the critical, given recent load-shedding, which is partially caused by a shortage of electricity supply.

national transmission

grid.

The IRP is not aligned to The latest draft Integrated Resource Plan 2018 (“IRP 2018”), set to be the first official IRP since

the President’s current 2010, was published for public comment on 28 August 2018 by the Minister of Energy. Planned

position on Eskom, REIPPPP bidding rounds are scheduled for 2019 and then suspended for three years. This stop-

renewable energy and start approach is not ideal for local value chains, including any local manufacturing, and related

IPPs job creation.

Independent Power Producers | Page 5REIPPPPs local Significant funds are invested in local economic development through REIPPPP. For all projects

economic development approved from Round 1 to Round 4, ZAR 20.6 billion has been earmarked for spending on socio-

impacts can be economic development projects over the term of IPP contracts. ZAR16.5 billion is allocated to

improved local communities where projects are built (10). While this is positive, the effectiveness, impact

and monitoring and evaluation of this spending can be improved.

IPP impact on jobs Employment data in South Africa's energy sector is difficult to use because of the inconsistency of

metrics, categorisation and methodologies (11). According to the IPP Programme Office, by June

2018, REIPPPP had created 36 528 direct Job Years, which equates to 41 451 full-time equivalents

(FTEs) (12). Another issue is that the nature of employment in renewable energy value chains is

different from coal mining, in terms of stability, longevity, location, and skills requirements. If the

country is to protect and support workers in the transition from fossil fuels to renewables, many

adjustments and investments will be required.

These concerns are important and will need to be addressed with different stakeholder groups, to achieve the outcomes

that South Africa needs from REIPPPP.

6. WHAT OUTCOMES DO WE WANT IN SOUTH AFRICA?

Whatever the role that the private sector plays in South Africa’s just and sustainable energy transition, it must:

• Allow for least-cost power procurement

• Enable fast-tracking the procurement of additional renewable energy generation capacity being added to the system

within the next two years

• Diversify generation and reduce risks associated with overdependence on Eskom’s current aging coal-fired

generation

• Increase transparency and accountability in the sector

There is an opportunity to look to other countries that have already introduced various forms of private sector energy

generation for innovative solutions that fit our local context.

References

1. Eberhard A, Leigland J, Kolker J. South Africa’s Renewable Energy IPP Procurement Program: Success Factors and Lessons

[Internet]. 2014. Available from: http://www.ee.co.za/article/south-africas-reippp-programme-success-factors-

lessons.html

2. Dobrotkova Z, Surana K, Audinet P. The price of solar energy: Comparing competitive auctions for utility-scale solar PV in

developing countries. Energy Policy [Internet]. 2018;118(January):133–48. Available from:

https://doi.org/10.1016/j.enpol.2018.03.036

3. CSIR. Formal comments on the South African Integrated Resource Plan ( IRP ) Update Assumptions, Base Case and

Observations 2016 [Internet]. Pretoria: CSIR; 2017. Available from:

https://www.csir.co.za/sites/default/files/Documents/CSIR_IRP2016_Comments_1.1.pdf

4. Turley L, Perera O. Implementing Sustainable Public Procurement in South Africa: Where to start [Internet]. Geneva; 2014.

Available from: www.iisd.org/sites/default/files/publications/implementing_spp_south_africa.pdf

5. Eberhard A, Naude R. The South African Renewable Energy IPP Procurement Programme: Review, Lessons Learned and

Proposals to Reduce Transaction Costs [Internet]. 2016. Available from:

https://www.gsb.uct.ac.za/files/EberhardNaude_REIPPPPReview_2017_1_1.pdf

6. Department of Energy, National Treasury, Development Bank of Southern Africa. Independent Power Producers

Procurement Programme (IPPPP): An Overview as at 30 September 2016. 2016.

7. Republic of South Africa Department of Energy. Electricy Regulation Act, 2006 Amendment of the Electricty Regulations on

Independent Power Producers | Page 6New Generation Capacity, 2011. Gov Gaz. 2015;419(38801).

8. ICLEI. Embedded energy generation experience in a South African metropolitan municipality [Internet]. Vol. February, ICLEI

Case Studies. 2015. Available from:

http://www.iclei.org/fileadmin/PUBLICATIONS/Case_Studies/ICLEI_cs_174_NMBM_UrbanLEDS_2014.pdf

9. Evans J. Cape Town draws battle lines over right to buy alternative energy from IPPs. News24 [Internet]. 2016 Jan 26 [cited

2017 Jan 26]; Available from: http://www.news24.com/SouthAfrica/News/cape-town-draws-battle-lines-over-right-to-

buy-alternative-energy-from-ipps-20170126

10. Independent Power Producer Office. Independent Power Producers Procurement Programme (IPPPP): An Overview, as at

March 2018 [Internet]. Pretoria; 2018. Available from: https://www.ipp-

projects.co.za/Publications/GetPublicationFile?fileid=9f9536ed-56e3-e811-9491-2c59e59ac9cd&fileName=20181024_IPP

Office Q1_2018-19 Overview.pdf

11. Tyler E. Briefing paper: An overview of the employment implications of the South African power sector transition

[Internet]. Vol. 2040. Cape Town; 2018. Available from: https://sawea.org.za/wp-content/uploads/2018/07/Employment-

implications-SA-power-sector-transition_final.pdf

12. South African National Department of Energy. Independent Power Producers Procurement Programme (IPPPP): An

Overview, as at 30 June 2018 [Internet]. Pretoria; 2018. Available from: https://www.ipp-

projects.co.za/Publications/GetPublicationFile?fileid=9f9536ed-56e3-e811-9491-2c59e59ac9cd&fileName=20181024_IPP

Office Q1_2018-19 Overview.pdf

Power Futures SA is a platform for inclusive, evidence-based, discussion for a just and transformed South African Energy Sector. For more

information, visit powerfutures.org or email us at info@powerfutures.org. Join the discussion on Twitter by following @PowerFuturesZA and

weighing in on the #NationalGrid #EskomUnbundling #PowerFutures conversation.

iEnergy icon sources: Factory by Creative Stall from the Noun Project ; Biomass Energy by ProSymbols from the Noun Project; solar by Creative

Mahira from the Noun Project; Wind Energy Generation by Symbolon from the Noun Project.

Independent Power Producers | Page 7You can also read