INVESTMENT MARKET COMMENTARY - For the Period 1 October - 31 December 2020 PRIVATE & CONFIDENTIAL - APAM

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INVESTMENT MARKET COMMENTARY

For the Period

1 October – 31 December 2020

PRIVATE & CONFIDENTIAL

APAM Ltd 3 Barrett Street London W1U 1AY

T: 0207 963 8858 | E: admin@apamuk.com | W: www.apamuk.com

As at 6 January 2021

EXECUTIVE SUMMARY

On Christmas Eve 2020, the UK and EU agreed a trade deal, ahead of the end of the transition period in January

2021. The deal has been referred to as a framework, with key issues such as financial services, to continue to be

debated in the New Year. Yet, the deal represents a key moment in the UK’s exit from the bloc and assuages any

concerns over the damaging effects of crashing out in a no-deal scenario. In certain areas, such as tax and state

aid, the UK and EU have agreed high level commonality in rules but have not yet fleshed out the details. In other

areas, such as farming, the UK has accepted greater friction in trade with the EU in order to assure the flexibility to

strike deals with the rest of the world. With the conclusion of the EU trade deal and a separate deal with Turkey,

the UK has now signed 62 trade agreements since it left the European Union. The markets have responded positively

to the UK’s progress as it endeavours to redefine itself as a forward-thinking green tech hub in the post-Brexit

world.

After emerging from a month-long lockdown, the UK successfully approved and administered the world’s first

COVID-19 vaccine. Markets rallied on the news with the MSCI All-Country World Index climbing by a record 12.2%

in November, followed by a correction on 21 December after the discovery of a variant strain of the virus and the

imposition of a strict lockdown which is expected to last until February. Returning optimism is balanced by

remaining challenges yet to overcome, and whereas the end may be in sight, unemployment is expected to rise

from 4.9% to 7.4% in 2021, which in turn could trigger a wave of defaults and bad debts. Retail empires have

continued to collapse, but as lockdowns end and consumer confidence rises, those on their last cash reserves may

survive. After a tumultuous four years of Trump, the global economy eagerly awaits a more level-headed Biden

approach. President-elect Joe Biden has promised to reform relationships with allies and take a less reckless

approach to international affairs.

The shopping centre and student sectors are underperforming, while Build-to-Rent, industrial, and retail warehouse

outperform. The office sector paints a mixed picture in which Grade B office markets are struggling, whereas Grade

A space remains in demand. Life sciences and tech generally will be crucial to the post-COVID recovery of offices

as the government endeavours to brand the UK as a global science and tech hub. The industrial sector continues

to be buoyed by strong demand, increasingly in the cold storage sector, although there is nervousness around the

weak retail sector, which in part underpins its demand. The retail sector experienced several high-profile liquidations

and CVAs in the past few months as its retransformation accelerates. Build-to-Rent residential investment is largely

unaffected by COVID-19, but the student sector is marked by rental write-offs, poor occupancy, and striking

students.

Several key phenomena are reshaping and will continue to reshape the UK commercial real estate landscape.

COVID-19 has ushered in a rethinking of shared space, predominantly in offices. The UK government’s efforts to

rebrand itself as a tech hub and champion of life sciences and green energy will also transform the real estate

landscape, whether it be through heavy investment into technology parks or an ‘eco-friendly’ redesigning of cities.

2

Other factors could increase or decrease the flow of foreign capital to the UK. The management of Brexit is crucial

and will define the UK economic landscape for decades, especially in terms of the future tax and competition status

of the UK. Early trade deals with Singapore and Taiwan are promising signs. Finally, the degradation of East/West

tensions and how Biden may approach them are integral to future global political and economic stability, which in

turn influences investor willingness to place capital in perceived safe havens such as the UK.

POLITICAL OVERVIEW

The UK has agreed a trade deal with the EU, setting out the framework for cooperation and divergence over the

coming decades. Although the finer details have not been finalised, a no-deal Brexit has been avoided and

compromise has been reached, contrary to significant media commentary over the past few years. There remain

key questions to answer, such as on financial services and Northern Ireland, but the agreement provides the

momentum to tackle these issues head on. Although the transition period has ended, smaller micro-transition

periods form part of the new deal; car manufacturers benefit from a six-year window before rules of origin change

(rules on how much of a product must come from a particular nation). Important questions have been addressed

by the deal: free movement has ended, except for short term business travel, and the UK and EU have agreed to

diverge in certain respects, such as agriculture, in order to allow the UK to strike deals with the rest of the world.

Over the coming months and years, implementation will be contested, independent bodies created, and legal teams

across the continent will pore over the 1,246-page document.

The government imposed a month-long lockdown in England on 5 November, amid rising COVID-19 cases. This

lockdown was less severe than the first as construction sites remained open and essential work continued from the

outset. High-frequency indicators of economic activity including volumes of people travelling to workplaces and

HGV traffic remained unchanged compared with before the restrictions were imposed. On 2 December, the

lockdown was replaced by a tiered system, which prevented retail and leisure-focused businesses from trading at

full capacity. This was then followed by the discovery of a variant strain of the virus and a Christmas lockdown of

varying regional intensity, causing sterling and the FTSE to dip on 21 December. Finally, on 4 January, the

government introduced a nationwide lockdown, similar to the one experienced in March, which is expected to end

in February. At the time of writing, it is estimated that every 1 in 50 people in England has COVID-19.

However, preliminary vaccine testing results have shown high efficacy in tackling the virus, and the UK was the first

to approve and administer doses. There are three principal vaccine contenders: Oxford-AstraZeneca, Moderna, and

Pfizer-BioNTech. The Oxford vaccine is the cheapest to produce and, crucially, can be stored at standard

temperatures of 2-8C. The other two vaccines have higher efficacy but are more expensive and require specialist

cold temperature storage. Now that there is a vaccine it will be critical to the economic recovery as to how swift

the rollout will be. Equity markets have bounced significantly as the vaccines were announced, although some of

the excitement was dampened by the prospect of a ‘no deal’ Brexit.

Donald Trump lost the US presidential election to Joe Biden by 306 electoral college votes to 232. 67% of the

eligible population voted, which represents the highest turnout since 1900. Biden secured over 80M votes, which

3

is the highest ever for a US president. The markets responded positively to the news, starved of certainty in recent

years and yearning for a more level-headed presidential approach to geopolitics. Biden’s approach to the world

stage will be pivotal in the coming years. His stance on Brexit, China, and Europe will all determine the strength of

the global economy. It is unlikely that a Biden presidency will immediately relax East/West tensions. There will

continue to be global political and economic instability for the foreseeable future. Global uncertainty has historically

benefited UK property, which is perceived as relatively secure. Foreign investment into UK property will furthermore

be amplified as trade deals are signed, especially with the US.

UK ECONOMIC OVERVIEW

TABLE 1: KEY UK ECONOMIC INDICATORS

CPI GDP Halifax HPI

Unemployment FTSE 10-year GBP/ GBP/

Inflation Growth Quarterly

Rate (Oct-20) 100* Gilt Yield* EUR* USD*

(Nov-20) (Oct-20) Change

0.3% 0.4% +3.8% 4.9% 6,787 0.25% 1.11 1.36

*As at 6 January 2021

The UK economy experienced record GDP growth of 15.5% between July-September following the lifting of the

first COVID lockdown restrictions. The second lockdown has dampened the strength of recovery, but it is not as

damaging as the first given that considerable economic activity has continued throughout the period. The W-

shaped recovery now seems a far more likely outcome as periodic tightening and untightening of COVID

restrictions becomes commonplace to keep the virus subdued before vaccines are widespread enough to lift all

restrictions. The OECD forecasts that the UK will be hit hard by the pandemic with an economy 6% smaller by the

end of 2021 than before the COVID crisis. This is the worst outcome of all G7 nations and many others across the

globe and in part results from the UK’s services-focused economy. The OECD has predicted economic growth of -

11.2% in 2020, 4.2% in 2021, and 4.1% in 2022. Yet influential organisations such as Goldman Sachs are advising

their clients to buy British, predicting that the pound could rise to $1.44 in 2021 as the economy recovers faster

than expected and investment into UK business, infrastructure, and real estate continues to defy the gloomy

forecasts.

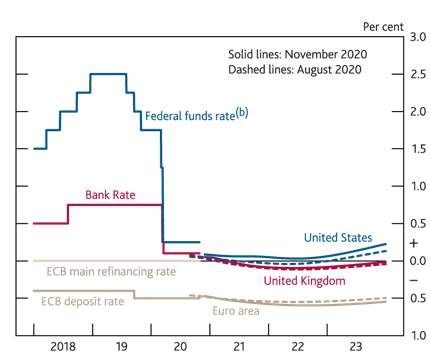

The Bank of England has kept interest rates at a record low of 0.1%, supporting a flat yield curve with negative gilt

yields up to 6-year maturities. The government has provided various support to SMEs, as it seeks to avoid a repeat

of the rise in defaults that occurred following the GFC. To date, analysts have not seen the expected rise in corporate

defaults that were first expected. Before the pre-Christmas correction, Sterling had been strengthening, with the

exchange rate nearing pre-COVID levels until coming under pressure due to December no-deal Brexit concerns.

The Bank of England has increased its buy-back programme, purchasing £300B government bonds to continue to

encourage low rates on mortgages and business loans. UK house prices continue to surge, helped both by the low

interest rate environment as well as Government stimulus reducing stamp duty until end March 2021. Halifax HPI

reported +7.6% annual change in October, while mortgage approvals are at a 13-year high. Lending spreads have

4

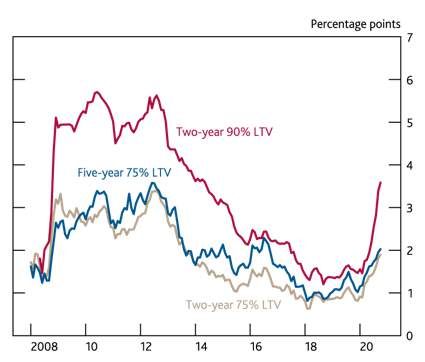

contracted for low credit risk borrowers, while riskier loans with high LTVs have seen a record spike in interest rates.

Banks are reluctant to underwrite riskier loans; currently a 2-year fixed rate mortgage with 90% LTV earns an interest

rate of around 5%.

Figure 1. Market implied path for policy rates Figure 2. Mortgage Spreads

Equity markets have experienced repeated bouts of volatility in 2020 but have risen sharply in November and

December before the pre-Christmas correction. FTSE 100 rose to its highest level since March, but still down from

pre-COVID levels. Equity markets continue to be supported by the low yield environment as well as the less-than-

severe risk of corporate defaults. Dividends have been largely reduced as well as optimism on corporate debt being

affordable, as companies hold on to their cash to offset near-term disruption while maintaining a more defensive

balance sheet. M&A activity has slowed understandably from the record activity over the summer where 36 deals

worth $5B or more transacted, but there is still significant activity such as AstraZeneca’s $39B purchase of Alexion,

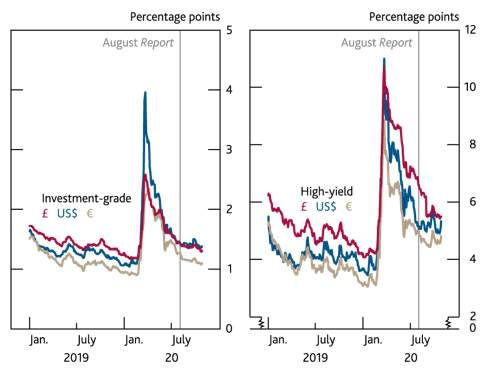

a business that specialises in disease immunology – a sign of the times. Corporate bond yields have fallen to below

pre-COVID levels, stimulated by cheap credit and low borrowing costs. UK credit spreads as of end of October for

AAA are 32bps while BBB are 194bps, representing a tightening of 11.1% and 4% month-on-month, respectively.

Debt markets have also witnessed continued tightening, as investors seek riskier assets to generate strong returns

against the low yields found in an investment grade paper. Active debt buyers expect a large increase in NPLs post-

COVID as more investors enter this space.

Figure 3. Movements in equity prices Figure 4. Investment grade corporate bond spreads

5

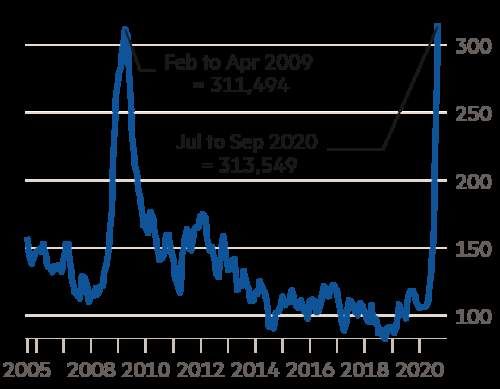

Unemployment, the ‘dark cloud’ looming over the economy, is anticipated to rise to 7.4% in 2021 from a pre-crisis

4%. Debenhams and Arcadia alone announced 25K job cuts on the first day of December. Managing unemployment

will be a key government focus over the next 5-10 years. A rising jobless rate is an important factor which could

risk turning the current health crisis into a long-term financial crisis. People out of work default on their debts and

put banks’ balance sheets under pressure with mounting bad debt liabilities. Concurrently, quantitative easing

programmes inflate asset prices, enriching those with existing holdings and entrenching social and economic

inequality. Whilst growing unemployment collided with the introduction of a new lockdown in November, the

government extended its furlough support scheme. Yet, as the new tiered system phases out and people are

allowed back to work, the government will be forced to wind down support schemes and the true impact of the

jobless dragging on the economy will be felt. Despite the government support, current UK redundancies equal

those at the peak of the global financial crisis in 2008 and are most likely to increase beyond that previous high in

the early part of 2021.

Figure 5. UK Redundancies (total of previous three months)

In order to fund various support schemes, the government has taken on high levels of debt. £215B has been

borrowed since April, and national debt is currently over 100% of GDP. Moody’s has downgraded UK’s long-term

issuer and senior unsecured ratings from Aa2 to Aa3. The effects of indebtedness are not yet being felt as the

government continues to do battle with COVID, and further capital is spent. However, as the government tightens

the purse strings in the years to come, perhaps even reverting to the austerity witnessed post global financial crisis,

investment could fall in other areas. Of particular concern is infrastructure where there are growing calls for HS2

and Crossrail to be scrapped despite the considerable sums already invested. It has even been suggested that

although HS2 may make it to Birmingham, it will not go any further. Yet, if the UK is to define itself in the post-

Brexit era, it will have to be forward-thinking and invest in the future of its cities. The government has committed a

6

further £8B to finishing Crossrail, but even that may not be enough to finally get the Elizabeth line running smoothly

in 2022.

The government has attempted to rebrand itself in the post-Brexit era as a champion of green energy and

technology. There are promises of significant investment into electric car charging, bicycle lanes, and solar farms.

Whether the government will be able to uphold this agenda amid the high debt environment also remains to be

seen; it may come at the cost of other objectives as the UK political sphere attempts to market itself on the

international stage. The shift to green energy will have important ramifications for real estate, whether that be in

tighter regulation on EPCs, a reduced need for car parking, or the complete redesign of urban environments to

become more eco-friendly. The latest announcement to cease production of diesel and petrol cars by 2030 is an

ambitious target and shows real intent but the cost of ensuring that the appropriate infrastructure is in place to

support this mission could be prohibitive.

The UK has received the most tech investment in Europe since 2016 at $50B, which is more than double the next

country, Germany, with $23B. The UK, specifically London and Manchester, has become a breeding ground for start-

ups. Six unicorns (privately held start-up companies valued at over $1B) have been created this year. As the UK

leaves the EU, the government is keen to capitalise on this strong tech performance as a defining feature of the UK

economy in the years to come. The government’s pivot toward the tech sector is facilitated by a strong existing

data centre sector. In Q3 2020, London was the ‘top performing Gigawatt market’ in EMEA with 52MW of take-up.

London data centre take-up reached 139MW in 2020, which is almost double the 77MW recorded in 2019.

PROPERTY OVERVIEW

UK property market headlines are dominated by continuing underperformance in the retail and student sectors

and outperformance in the industrial and residential sectors, with offices occupying the middle ground. The tide of

bankruptcies is beginning to break on the bricks-and-mortar landscape particularly in retail and the food and

beverage component of leisure. On the other hand, industrials continue to be buoyed by high demand for cloud

services and e-commerce coupled with an anticipated reshoring of manufacturing following Brexit. Offices are

anticipated to experience lacklustre or negative growth in 2021, but there has not yet been a significant dampening

in occupier demand or indeed investment into the higher quality end of the market. The Build-to-Rent sector is

also in high demand, but student accommodation is plagued by tenant default and forced rental write-offs.

The listed real estate sector paints an exaggerated picture of the winning and losing sectors of the past few months.

New River REIT, a shopping centre specialist, has scarcely recovered from the depths of its March 2020 fall, whereas

Tritax Big Box REIT is trading 10% higher than pre-COVID. All listed stock has bounced on the vaccine news, but for

some it may be too late. After a year of burning through already weak cash reserves, certain participants in the

listed sector are left with no option except to put themselves up for sale. APAM has identified 11 REITs which have

a high chance of M&A activity; on average these companies are trading at a 62% discount to NAV.

7After a subdued 2020, market activity has picked up at year-end. Manchester Airport Group sold its non-core

Magical Portfolio to Columbia Threadneedle for £370M in Q3 2020. City of London investment volumes rose from

£145M in September to £541M in October. AGC Equity Partners purchased 1 London Wall Place for £472M in

October (3.85% NIY) and Sun Venture bought 1&2 New Ludgate for £552M, reflecting a return to the large

transactions which have been absent in City markets since the beginning of the COVID crisis. Asset management is

also increasingly in demand as the worsening economic situation has begun to materialise in distress. It is glaringly

apparent that much of the UK real estate landscape is no longer fit for purpose, whether it be an oversupply of

retail, a poorly operated private rented sector or simply obsolete buildings that do not meet the modern occupiers’

requirements. Debt default has triggered a surge of activity in shopping centres where lenders have been forced to

take control. In Q3 and Q4 2020, APAM was appointed on £470M of shopping centres, bringing APAM’s total

shopping centre AUM to £750M. 32% of APAM’s AUM now relates to bank workout mandates, whereas 18 months

ago it stood at 0%.

1 & 2 New Ludgate

In March 2021, landlords will once again regain all legal means available to collect rent arrears, a year after the

government intervened to protect tenants. The decision was announced in December and gives landlords and

tenants three months to come to an agreement on unpaid rent. The British Property Federation stated that landlords

and tenants have generally been working constructively together in the past year but that it is the “end of the road

for those well-capitalised businesses who have refused to engage and pay any rent since March 2020”. Since the

beginning of the COVID crisis, APAM has received 248 rent concession requests. 76% of the approved requests

have resulted in a positive or neutral outcome for the landlord, such as a lease extension or break removal. Well

capitalised businesses which have been withholding rent and service charge payments will certainly see a backlash

as 31 March 2021 arrives.

8OFFICE

The office sector has generally weathered the COVID-19 storm. Take-up, investment and development have all

been weakened, but rents are yet to fall, and yields have remained relatively robust. The formerly prevailing view

of ‘the end of the city’ is waning in conviction as occupiers seek a return to normality. It is likely that there will be a

reorganisation of city centre space, and there will surely be a reduction in the density of desk space, but demand

for offices is expected to again pick up in 2021. Offices do not serve solely to improve ease of management, but

they are social spaces of idea sharing, collaboration, and variety. Most occupiers will move to a more flexible

working format, and as a result, the office needs to broaden its appeal, not just as a place of a work, but a place

where talent enjoys deploying its skills and this will require considerable re-organisation and investment in the

‘traditional’ office environment.

Just as happened after the 2008 global financial crisis, there is a growing polarisation of office space. A two-tier

system is emerging whereby the demand for Grade A space is less affected by the crisis, but Grade B has suffered

from an initial drop-off in occupier interest. Grade A occupiers tend to be established businesses, often global

corporates, which can afford to take a long-term view on their business plan. On the other hand, for Grade B

occupiers the COVID-19 pandemic has forced businesses to reassess their need for poorly located and out of date

office space. These types of occupiers have accordingly held off making leasing decisions until there is further

clarity. Yet, on the other side of the pandemic, these are the businesses which will be demanding new space, without

the necessary infrastructure to have all of their staff working from home all of the time.

The most important office trend of the coming years is the expansion of the life sciences sector. There has been

significant growth in the life sciences sector as of late, especially as the government endeavours to rebrand itself

following the Brexit vote. The objective of the government is to style the UK as an R&D hub. The life sciences sector

currently contributes £74B to the UK economy and has placed Britain at the forefront of the COVID-19 vaccine race.

In 2019, £27.6B capital was raised by UK life sciences, amounting to a 135% increase on 2018.

Recently the UK signed a $17.6B trade deal with Singapore following a similar deal with Canada in October. Britain

has now signed 56 trade deals covered by current EU arrangements. Yet UK laboratory and R&D space is drastically

undersupplied. London and Manchester have a combined 459K sq ft of available space, against New York and

Boston’s 16M sq ft. The UK property industry will have to catch up with the likely boom in occupier demand if the

full benefits of these occupiers choosing to relocate to the UK is to be seen.

TABLE 2: CENTRAL LONDON Q3 2020

Take-up Vacancy

Investment Prime

Prime Take-up vs 10- Supply Vacancy Rate 10-

Region Volumes Rent

Yield (M sq ft) year (M sq ft) Rate year

(£M) (£ psf)

Average Average

Central London 3.75% 1,000 117.50 0.94 (47%) 14.3 5.9% 5%

West End 3.75% 452 117.50 0.46 (48%) 5.8 5.9% 4%

City 4% 245 72.50 0.44 (69%) 6 5.1% 5.4%

East London - 380 50 0.04 (69%) 2.5 9.7% 7.3%

9TABLE 3: CENTRAL LONDON Q3 2020 KEY TRANSACTIONS

Leasing

Address Occupier Area (sq ft)

280 Bishopsgate Baker & McKenzie 152,690

30 Berners Street Netflix 87,000

210 Euston Road The Office Group 68,182

76 Turnmill Street J A Kemp 45,273

100 Liverpool Street Storey 45,058

Investment

Address Purchaser Yield Price (£M)

The Cabot Link REIT 4.86% 380

1 New Oxford Street Sun Venture 4.20% 174

7 Soho Square Hines Pan-Euro Core Fund 3.98% 78

103 Mount Street STARS REI 4.06% 78

Wellington Street APG - 76.5

TABLE 4: THE BIG NINE Q3 2020

City

Investment Headline Under

Prime Rent free Centre

City Volumes Rent Construction Pre-let

Yield (months)* Take-up

(£M) (£ psf) (sq ft)

(sq ft)

Birmingham 5% 131 37 24 79,935 748,000 32%

Bristol 5% 64 35.50 18 58,833 403,000 68%

Cardiff 5.75% - 27 18 40,038 109,000 0%

Edinburgh 4.75% 133 37 15 308,656 291,913 23%

Glasgow 5% 82 34.50 15 63,852 1,400,000 80%

Leeds 5.25% - 32 24 88,507 134,000 100%

Liverpool 6% - 22 24 10,000 160,000 44%

Manchester 5% 74 36.50 24 69,106 1,300,000 52%

Newcastle 6% - 26 18 48,015 107,000 0%

*On a 10-year term

TABLE 5: BIG NINE Q3 2020 KEY TRANSACTIONS

Leasing

Area

City Address Occupier

(sq ft)

Bristol 100 Bristol Business Park Babcock 132,000

Newcastle Weymouth House Green Energy Advice 30,479

Manchester The Vic Tech Mahindra 23,580

Glasgow Lightyear Public Sector 22,369

Glasgow Lumina Building NHS 24 13,711

10Investment

Price

City Address Purchaser Yield

(£M)

Edinburgh Lochside Crescent Hyundai Asset Management 5.10% 133

Birmingham 55 Colmore Row Union Investment 4.85% 105

Bristol Bristol Business Park Lime Property Fund 4.60% 55

Glasgow Broomielaw Elite Partners Capital 7.66% 40

Glasgow Queen Street Maya Capital 9.50% 30

RETAIL AND LEISURE

Bricks-and-mortar retail has had its recovery from the first COVID lockdown halted by a second. Weak footfall

between the two lockdowns did not provide enough respite for many retailers to survive the second. Debenhams

has entered into liquidation, Arcadia has announced a CVA, and Bonmarché fell into administration for the second

time in a year. Whereas COVID-19, online retail, and increasing occupational costs have been cited as the reasons

for retailers failing, most of these businesses have suffered from chronic lack of investment whilst poor management

coupled with private equity financing led to inflated salaries and excessive dividends financed by too much cheap

debt. COVID finished off many companies’ remaining cash reserves, but these companies were dying before it

struck. Good retail businesses have weathered the ‘storm,’ with many reporting higher conversion rates and

increased basket size in store, while increasing investment in online platforms and branding. Others such as Primark

and B&M have simply tightened their efficiency model and made adjustments to their supply chain and logistics

costs. These retailers will hit the ground running in 2021, whilst others will continue to fail as management bemoans

the ‘unprecedented times’ rather than adapting to them.

The UK tiered system implemented following the lockdown is another hurdle for the retailers to overcome. However

due to variations in restrictions throughout the country and the increase in working from home, there has been an

increase in local shopping, with a number of retailers reporting strong trade in suburban/local centres at the

expense of the major urban centres and super regional centres, both of which have seen significant reductions in

footfall. Yet rents across the UK continue to fall, and APAM’s data shows that rents fell 11% on lease renewals in

Q3 2020 alone. The Christmas period will provide a boost to the high street but there will be more bumps in the

road with the April 2020 increase in National Living Wage presenting another unwelcome addition to retailers’ cost

bases.

In times of crisis, budget retailers tend to thrive; Aldi and Lidl gained significant market share in the aftermath of

the 2007/08 global financial crisis. The standout performer of the past few months and years has been B&M, which

announced a £37M special dividend in November. This is the second exceptional dividend the discount retailer has

declared this year, notwithstanding the 60% increase in its regular interim dividend. In total, B&M has declared

£500M in dividends in 2020. In September, B&M was promoted to the FTSE 100, and its share price has risen by a

11quarter in 2020 and has doubled since flotation in 2014. This is an outstanding performance given the economic

environment.

Online sales are expected to rise £5.3B in 2020, a 19% increase on 2019. The impact of the significant increase in

online delivery during the pandemic should not be understated, although cracks in this model are likely to be

exposed when the dust settles in January, as demand is expected to outstrip supply not only of products but also

of logistics resources (namely drivers and vans). Online is now suffering increasing delivery and returns costs,

reducing the opportunity for upselling and the attractiveness and frequency of impulse buying.

The leisure sector has been put under considerable strain as many industry operators have been shut since March

2020, unable to open even once lockdowns were eased. Cineworld’s shares have fallen 87% since the pandemic hit

the UK. Yet leisure space has been a robust component of retail schemes in recent years and the leisure operator

has been one of the primary occupiers that landlords have targeted to stem negative cashflow and bring footfall

into struggling shopping centres.

Retail warehouses have been tarnished with the same brush as shopping centres and the high street yet, as the

high street struggles, out-of-town destination shopping has performed better, with open air settings and free car

parking naturally facilitating social distancing and convenience. Value retailers in particular have been taking

advantage of tenant failures in this sector.

Whilst lockdown has curtailed spending on leisure and travel, consumers have increased spending on DIY and

groceries due to the increase in staying and eating at home. Q1 and Q2 2021 are expected to continue to be

challenging for the retail and leisure sectors due to the impact of continuing COVID-19 restrictions and anticipated

tenant failures. Arguably, investors have over-discounted both leisure and out-of-town retail parks, and both

sectors are anticipated to bounce back strongly in 2021.

INDUSTRIAL

The industrial sector maintains its strong growth. Since 2007, the average annual new lease take-up has risen from

15M sq ft to 32M sq ft, a 113% rise. This increase results from the evolution of the retail supply chain over the past

three decades, which is increasingly concentrated in the Midlands Golden Triangle, from which 90% of the UK

population is reachable within four hours. Increasingly, last mile hubs have been spiderwebbing away from the

Golden Triangle, allowing e-commerce operators to deliver goods to consumers by the next or same day.

Brexit and COVID are shifting the focus away from the Golden Triangle to port towns. Brexit and COVID have

encouraged processes of ‘near-shoring’, whereby companies with global manufacturing operations relocate their

overseas operations back to the UK, sometimes incentivised by the government. Near-shoring has grown in

popularity as current affairs have laid bare the fragility of global supply chains, and 95% of all goods leaving and

entering the UK do so via seaports. As goods enter via seaports, it makes sense to begin basing distribution hubs

there, as Tesco and Asda have done, to reduce road congestion and pollution.

12Cold storage has been in the spotlight in recent months. Cold storage has in part been repopularised by stockpiling,

on the one hand of food as COVID and Brexit threaten supply chains, but also for storing doses of vaccines.

Moreover, cold storage has grown in popularity as society has become more conscious of climate change in so far

as it purportedly minimises food waste and over-production. Cold storage currently accounts for 12% of total UK

warehouse space with a further 16.7M sq ft under construction, of which 75% will be occupied by retailers and 23%

by 3PLs. There are 678 cold storage warehouse units in the UK over 50K sq ft, equating to 134M sq ft of space.

There has been growing investment into cold storage due to its growing popularity, and Newcold purchased 23

acres in Corby in Q2 2020 to further expand its footprint.

There had been fears of a distribution space oversupply at the beginning of the year as rapid construction

threatened to outstrip demand, but the events of 2020 have pushed the sector back to undersupply. A record

quarter of 16.6M sq ft of take-up in Q3 2020 reduced availability by 11% to 66M sq ft, which is the same as a year

ago and 30% below its post-GFC peak. Amazon accounted for a third of take-up in the first three quarters of the

year, and e-commerce is at an all-time high of 40% of the total. Rental growth is 2.8% pa, and prime yields have

sharpened to between 4-5.5% based on the UK region. The true test for the UK industrial sector will be whether

demand remains strong once the dust settles on COVID and Brexit and when Amazon reaches full capacity,

whenever that may be.

RESIDENTIAL

Q3 2020 was the strongest quarter on record for UK Build-to-Rent (BTR) investment, with £1.84B transacted. There

has been a 160% year-on-year increase in new equity targeting the sector. The BTR sector is increasingly attractive

for investors as the UK institutionalises its private rental product to more closely resemble the US and German

models. The sector is nascent amid a UK landscape of non-institutional Buy-to-Let landlords. Thus, there is fierce

activity as investors, both UK and overseas, attempt to get an early foot in the door and secure attractive returns

before yields drop to institutional levels. The BTR sector has scarcely been affected by COVID-19, despite concerns

that co-living models would no longer be attractive during a pandemic. In fact, the inverse has been true, and

although there was an initial fall in occupational demand as uncertainty weighed on the country in March, it has

picked up again and residents of existing schemes have praised the community aspect of assets as helping them

get through long isolation periods. There is little doubt that the UK is going through a ‘social transformation’ where

generation X and Y, and Z for that matter, have decided that ‘ownership’ is a constraint on life choices, and it is no

longer an ambition to buy a house or ‘get on the property ladder.’

The student sector continues to be constrained by COVID-19. Operators have managed to secure moderate

occupancy for the 2020/21 academic year. Unite has secured 88% occupancy (98% 2019/20) and Empiric 70% (94%

2019/20). However, operators are having to offer flexible lease terms which allow students to cancel their

commitments at short notice. Moreover, tenants in certain universities, such as in Manchester, have successfully

lobbied to have their rents reduced as they are forced to stay inside and are barred from socialising under lockdown

rules. Unite wrote off between £90-125M in rent for the 2019/2020 academic year. Accordingly, prospective sales

have been pulled from the market as vendors do not believe their aspirations will be met in the current market.

13Investment is stagnant and there are one or two early signs of distress not dissimilar to those that were evident in

the retail markets in 2015/2016.

CONCLUSION

The UK has battled through another quarter of lockdowns and restrictions on economic activity. The retail and

leisure sectors have borne the brunt and whilst the vaccine rollout offers some hope. The recent rise in infection

rate, due to the spread of a more virulent strain of the virus, ensure that the next six months at least will see further

stringent measures imposed to attempt to get the virus under control, culminating in further disruption to the UK

economy.

Beyond this next challenging period there are plenty of reasons to be more optimistic with the UK and EU trade

deal being agreed, along with 61 other trade deals, and the UK charting a new path towards tech, life sciences,

data, and green energy, all supported by substantial infrastructure investment. In 2020, despite COVID-19, UK tech

start-ups received £15B of new investment, marginally ahead of 2019 and nearly twice as much as Germany and

France combined. The impact on the buildings will be significant. Obsolete buildings in all sectors will need to be

repurposed to meet modern occupational demand. Post COVID-19, the way we shop, work, live, and play will all

change. This shift combined with a new and improved attitude to sustainability, will change the look and feel of

buildings, and ultimately the configuration of the urban environment.

The burgeoning build to rent residential sector will become integral in reimaging the city of the future as a talented

and mobile workforce demands to live in close proximity to both a place of work but also to a place to shop and

enjoy limited leisure time. The private rented sector will expand further to the family market and residential

investment will become a mainstream investment class for institutions in the UK as it is across Europe and the US.

Change is unavoidable and the speed of change will continue to accelerate. In order to accommodate modern

businesses and their workforces the property industry must work out a more flexible and integrated built

environment where all services interact efficiently and sustainably.

14Contact Details:

Simon Cooke

scooke@apamuk.com

+44(0)20 7963 8850

Nick Phillips

nphillips@apamuk.com

+44(0)20 7963 8855

The contents of this report or document (“Report”) are confidential. If you use or accept this Report, you are bound

by strict confidentiality obligations which could lead to liability if any disclosure is made to third parties or

unauthorised persons.

You acknowledge this Report may contain personal data and that at all times you shall be in compliance with the

General Data Protection Regulation and other applicable laws. APAM has provided personal data to the extent and

in such manner as is necessary for the provision of the Report.

APAM and its affiliates accept no liability whatsoever for any direct, consequential or indirect loss of any kind arising

out of the use of this document or any part of its contents.

15You can also read