INVESTOR PRESENTATION - Mintos

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

I N V E S TO R P R E S E N TAT I O N

MAY 2020

www.getbucks.com

www.getbucks.com | 1

Table of contents

Investor Presentation 2020

1. Executive Summary

2. Market Overview

3. Business Model

4. Growth Strategy

5. Financial Outlook

6. Leadership

7. Conclusion

www.getbucks.com | 2

GetBucks at a glance

Enabling and GetBucks is a digital financial services platform, providing a range of lending and insurance

products to the South African consumer, with a strategic focus on simplicity and ease of use.

empowering. GetBucks South Africa includes the South African lending business, GetBucks Eswatini, GetBucks Namibia and

GetSure South Africa, a registered Financial Services Provider (FSP).

There is a large unbanked and under-banked population in South Africa which does not

use formal banks or semiformal microfinance institutions. This presents an opportunity for us to

offer an innovative range of high-quality, affordable financial products and services.

Through our lending solutions we see ourselves as providers of interim finance and over-

draft solutions for the under-banked and those looking to access and pay for goods and

services.

GBSA Loans granted Outstanding loan book Default

customers to date as of 31/03/2020 rate

177 000 1 145 342 R 153 287 618 11.6%

www.getbucks.com | 3

We have used 2019 to reshape the portfolio

01 Affordability criteria

Tightened our affordability criteria and process,

04 Performing channels

Reduced our exposure to poorly performing

including aligning sales incentives to the quality of channels of business.

As GetBucks in South Africa, we have the originated portfolio. There is exposure more to

spent 2019, positioning the portfolio

05

bank transactional data in the decision process as NPL portfolio

and the business to be able to absorb well as factoring some of the more relevant short- Disposed of a large portion of our NPL portfolio

term characteristics.

any downturn in consumer fortune, as which was a drag on both performance and

collection levels and a detractor of focus on the

well as to be able to make the most of

the opportunity that normally > 02 New loan process

Launched our new loan process which automates

reality of running the business.

emerges in these periods – bearing in affordability calculations directly off the bank

mind that real consumer demand statement and uses our bespoke AI models to assess 06 Rebuilding management

An experienced management team with a strong

and determine risk.

does not diminish while supply lending background and vision for an exceptional

contracts. What becomes more

03 Credit scoring brand implemented in Q4 2018.

important is the ability to accurately Enhanced the credit scoring models to be more

and pragmatically make sound risk

relevant to the current market reality. We have also

raised the credit bureau cut-off scores that act as the

07 Shareholder change

Finclusion 100% shareholder of GetBucks SA since

decisions. initial entry point validation. January 2020.

www.getbucks.com | 4

The impact of these changes is clearly visible

Approval rates over time GBSA Industry

18.1%

CD1 default rates over time

14.8%

H2 H2 H1 H2

11.3%

2017 2018 2019 2019

9.1%

7.8% 7.8%

6.8% 6.9% 6.5%

4.4% 4.6% 4.4% 4.4% 4.6% 4.6%

4.1% 3.8% 3.5% 4.1% 4.2%

52% | 46% 50% | 28% 54% | 35% 51% | 37% 3.9%

Collection rates over time

J A S O N D J F M A M J J A S O N D J F M

2018 2019 2020

Q1 Q2 Q3 Q4

2019 2019 2019 2019 In addition, we have begun the development of a product with self-contained cash

flow support to customers with a lower borrowing cost than they could obtain from

a traditional pay-day lender. Our online focus will also shift towards a broader

financial training and awareness platform, ensuring that customers understand the

73% | 80% 72% | 91% 71% | 91% 72% | 90%

credit purchasing decision they are making and the implications thereof.

www.getbucks.com | 5

MARKET OVERVIEW

www.getbucks.com | 6

A look at the 60%

Age

South African 27% 66%

40%

20%

Population 0%

Unemployed Urban population 0-14 15-24 25-54 55-64 65+

Population 2019: SA's smartphone* penetration

58 892 763 2016 43.5%

2017 74.2%

32,615,165

2018 81.7% Internet users: June 2019

Female Male

50.74% 49.26%

*As at September 2018

GDP - composition, by end use: (2017 est.)

Languages: Household consumption 59.4% Investment in inventories -0.1%

English, Afrikaans, Zulu, Xhosa, Southern Sotho, Government consumption 20.9% Exports of goods and services 29.8%

Tswana, Venda, Northern Sotho, Tsonga, Swati, Investment in fixed capital 18.7% Imports of goods and services -28.4%

Ndebele

www.worldometers.info/world-population/south-africa-population/ | www.indexmundi.com/south_africa/by_end_use_gdp_composition.html

www.itweb.co.za/content/GxwQDM1AYy8MlPVointernetworldstats.com/stats1.htm

www.getbucks.com | 7

State of the South African Consumer

Consumer vulnerability index

The recent results show a sharp deterioration in income and expenditure

H1 2018 vulnerability

H1 2019

Average loan sizes and repayments increase

Driven by higher income borrowers 17%

Average income increase

Income Expenditure Savings Debt

While overall growth in the mortgage and

vehicle debtor’s books were relatively in line % Of unsecured advances > 5 years

with previous years there was a 16.4%

2011 2012 2013 2014 2015 2016 2017 2018 2019

increase in unsecured loans. Short-term

lending continues to play a critical role in the

provision of a financing product for

3,7% 12% 14.4% 11% 5.8% 7.6% 9% 14% 16%

unexpected life events, especially in the

formal credit market where overdraft Unsecured lending continues to repeat the trends seen in the last rapid expansion phase of 2012 to 2014. In 2019, 16% of all

penetration is less than 16%. unsecured disbursements have been on terms of over 5 years (average of c. 78 months).

www.getbucks.com | 8

State of the South African Consumer Consumers having at least one account

at NPL stage (3 months or more in

arrears):

Over the past 24 months there has been a:

21.7% 23.5%

2018 2019

500k Consumers

Growth in Portfolio vs NPL 48.70%

Customers two months in

Book Growth % NPL Growth % arrears on at least one account:

28.80%

17.60% 16.4%

11.8% 12.4%

13.60% 12.30% 2017 2019

4.8% 6.1%

3.8%

0.2%

200k Consumers

Mortgage Vehicle finance Credit facilities Unsecured Short term

www.getbucks.com | 9

The South African market is prepared for digital disruption

Innovation in only one component of the value chain will ultimately fail

Challenges of access

Physical access Financial access Emotional access

Inconvenient or impossible Too expensive Too complex and not trusted

Branch infrastructures offer complex Data-poor markets, often without mature credit Historical oversupply and

processes and bureaucracy bureaus, drive increased credit risk commoditisation of the lending

market

Limited voluntary savings results in need High cost of funding stems misalignment of risk Adoption becomes troublesome due to

for easy access and quick decisions of the market vs actual, demonstrated behaviour a lack of financial and digital literacy

Overcoming the challenges

Disruptive partner model Structural cost advantage Simple, transparent propositions

Powered by our proprietary data science and AI Our technology and operating model makes the Centered on aligning customer needs with

technologies delivery of lending solutions more affordable and solutions

efficient

www.getbucks.com | 10Solving financial access through leading credit risk management

Innovative digital credit products are underpinned by advanced data analytics and use of alternative data

Alternative data usage Advances modelling Behavioural economics Test, Adapt, Refine

Leverage big-data technologies The following advanced Product feature designed to Prudent test and learn approach to

and industry insights to create techniques are used to deliver influence customer behaviour ensure model validation prior to

new attributes from alternative best in class models: Examples include: scale

data suppliers

• Deep learning Vintage-based views of actual

• Personal loan

• Random forest performance versus expectations

Cash-flow support to reduce the

Generate unique credit insights enable faster modification of credit

need for consumers to access

from raw bureau data strategies

expensive, unregulated informal

Our solutions allow for rapid

credit

deployment of advanced models Integrated provisioning modelling

Leverage the inherent value in

with reduced operational risk • Mobile device finance allows for virtual portfolio

transactional information

With first to market soft-lock assessments and immediate view

(including bank statement data)

technology to manage payment of IFRS9 impacts

behaviour

www.getbucks.com | 11BUSINESS MODEL

www.getbucks.com | 12Demographics

Age distribution –

Advances H2 2019

Channel distribution over time Online Payroll PartnersKey product statistics Loan portfolio Online Payroll Portfolio Term Mix

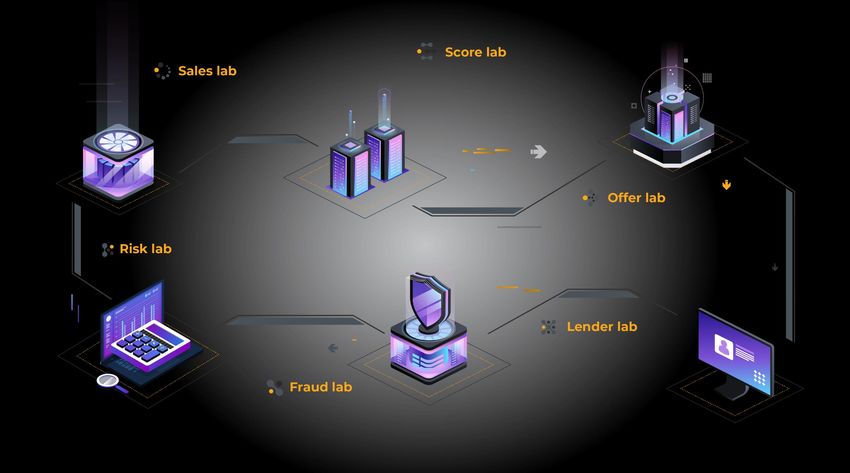

Four pillar credit assessment approach supported by credit scoring using

multiple and alternative data points

Policy rules Scorecards

• Minimum Age • Sequestration • Tailored for markets and partners (e.g. • Personal information

• Maximum Age • Minimum Credit Bureau Scores new/repeat) • Credit bureau information

• Minimum Income • Judgements • Incorporate partner client data where • Bank Transactional data

• Debt Review • Default/Adverse appropriate

• Administration

Affordability

Sector / Employer

• Automated from bank statement data 3 months with 3 salary deposits

• Min no. of employees • Discard highest and average remaining 2

• Min. years of operation • Expenses calculated as outlined above

• Macro sector assessments • Net salary needs to be able to afford 1.25x instalment

Psychometrics Client Acquisition

Worthy Credit by Innovative Assessments (IA) is a psychometric assessment tool • Categorised liabilities – personal and short-term loans, rental assets and

for evaluating creditworthiness based on a client’s personal character. ∫ property or vehicle finance

• Personal character helps to evaluate clients’ willingness to repay their loans, • The gradient of debt acquisition

above and beyond their traditional financial credit scores. • Credit score trends – average score and score transitions

www.getbucks.com | 15AI solutions

Supervised machine learning to make predictions within

seconds. Using financial and psychometric data allows faster

Scrutinisation of clients’ personal data to

more accurate decision making, greatly improving the speed

optimise leads and define quality and well as

of loan application processes as well as user experience.

which clients are more likely qualify and convert

into a sale.

Transactional behaviour modelling creates

opportunity to up-sell, cross sell and identify where

improvements can be made on spending habits with

Seamless provisioning modelling allowing inputs product expansion possibilities.

from all other modules delivering IFRS9 compliant

models with scenario analytics for macro-economic

and SIC-R impact assessments and implementations

Reduce risk, eliminate human error, improve

turnaround time and improve over all

customer experience.

Identify organized groups of fraudsters,

synthetic identities, stolen identities,

compromised networks and hijacked devices.

www.getbucks.com | 16Building unique customer experiences Transparency Transparency equals trust Whether it is pricing, credit eligibility, or business performance, transparency is a top priority at GetBucks. Through transparency we aim to build a trusting relationship with our clients, empowering them to make sound financial decisions. Simplicity Quick and easy online process We eliminate any unnecessary steps, offering a seamless experience any time, anywhere Empowerment GetBucks has established a debt rehabilitation product that assists clients with over indebtedness, backlisting’s, judgement removals and help getting out of debt review. Through debt restructuring, GetBucks helps overindebted clients get the financial stability they need to get back on their feet. Empowering our people to deliver a superior customer experience underpinned by dignity and www.getbucks.com | 17 respect

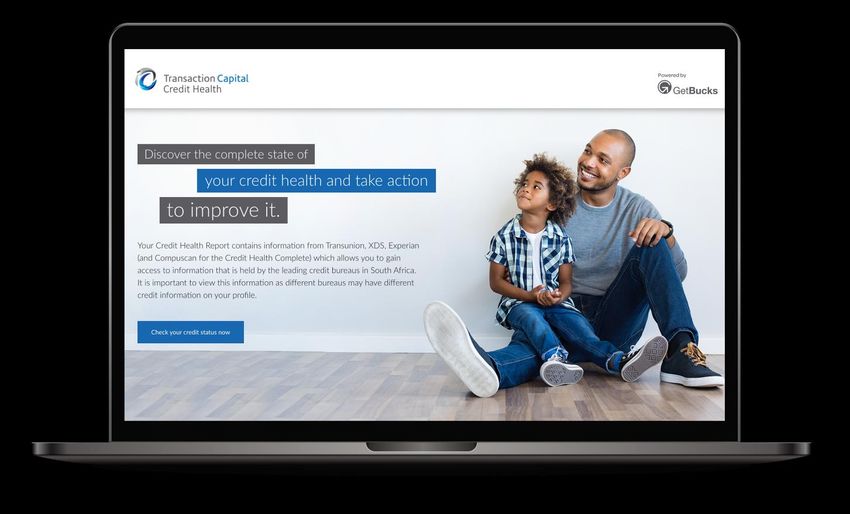

Financial Education & Wellness

GetBucks is a responsible lender that not only assists people when they need a little extra

financial help, but also believes in educating people to make financially sound decisions.

Free Credit Report

• As a value add to our clients, we offer a free monthly credit report for them to get

feedback on credit scores, financial history and spending habits

• Not only is it important for clients to know their financial standing, but GetBucks

tries to assist clients with minor changes that with improve their financial status.

GetBucks Finance Guide

• Available to download from the website or on request, GetBucks clients get

access to a quick and easy to understand guide on finance firsts, as well as a

simple budget to assist in budget management and planning.

Full view of current and historical personal credit data | Accessibility to your credit

profile allows deeper feedback on movement of credit score | Aid financial

understanding and education based on spending habits | Help to financially

rehabilitate blacklisted clients through our partners

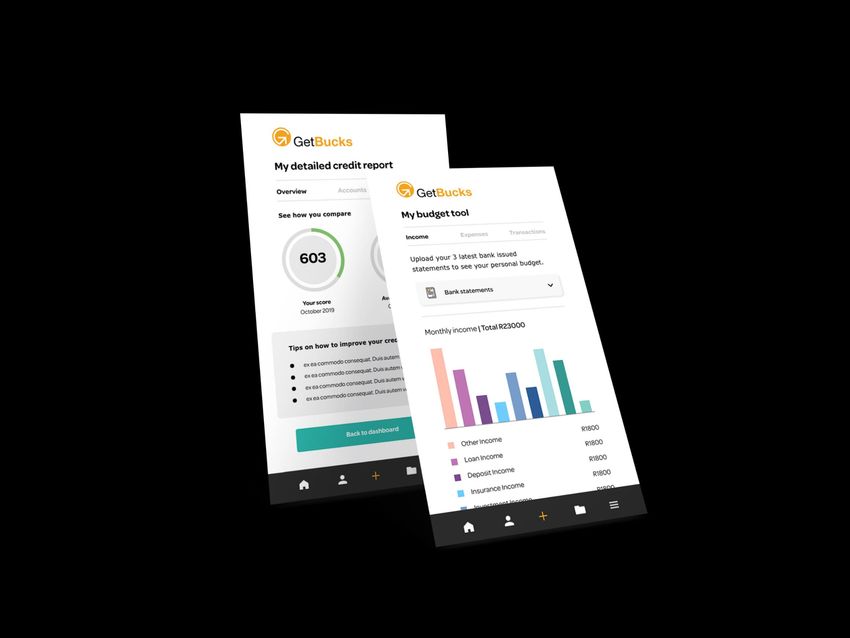

www.getbucks.com | 18Budgeting tool

Customers have the right to their own valuable data.

• Using artificial intelligence and proprietary technology, GetBucks

has developed an easy to use budgeting tool that allows customers

access to their personal financial information.

• The budgeting tool simplifies and displays the customers income,

expenses and transactions to see where they can make

improvements and assist the client on a journey to financial

wellness.

www.getbucks.com | 19Credit Rehabilitation

GetBucks has established a debt rehabilitation product that assists clients with over indebtedness, black listings, judgement removals and help getting out of

debt review. Through debt restructuring, GetBucks helps overindebted clients get the financial stability they need to get back on their feet.

How it works

Sign Up

Sign up on the Platform to reveal your free Credit Score.

Credit Report

It all starts with your Credit Report. See your Credit Report and Scores from three

different Credit Bureaus on your own personalised dashboard.

Recommendations

See recommended financial products based on the outcome of your credit report

to help you with your overall financial health. You can apply for these products

straight from your Dashboard.

Room for Improvement

Learn what affects your credit score and what you can do to improve your credit

status.

www.getbucks.com | 20G R O W T H S T R AT E G Y

www.getbucks.com | 21Gearing for growth

Three pillar business strategy utilising our capabilities and experience with a build once, deploy multiple times solution set.

Grow Sales Improve and maintain quality Deliver meaningful experiences

Partner with leading other financial Strengthen non-traditional data sources and Expand scoring techniques to include

services and technology providers to increase reliance on AI models to grow sales psychometric score offerings to enable entry

enable their new customer propositions without compromising risk into the less traditional credit market

Enablement through the launch of the Run best of breed collections outsource Innovative wallet and payment technologies

online-store and finance solutions for model - champion/challenger on will also enhance the sales and collections

brick-and-mortar and on-line retailers contingency basis only fulcrum

Treating customers as individuals and tailoring

Scale the insurance product offering to Identify timings for book sales to optimise solutions to their need and personal risk profiles

deepen the customer relationship or accelerate potential returns

Ensuring that our customer experience retains

Grow top-end payroll client base Ensure provisions remain realistic but the values of dignity and respect at its core

pragmatic

Loan Book - R480m NPAT Growth - R90m Sales - R600m

www.getbucks.com | 22Growth through partnerships

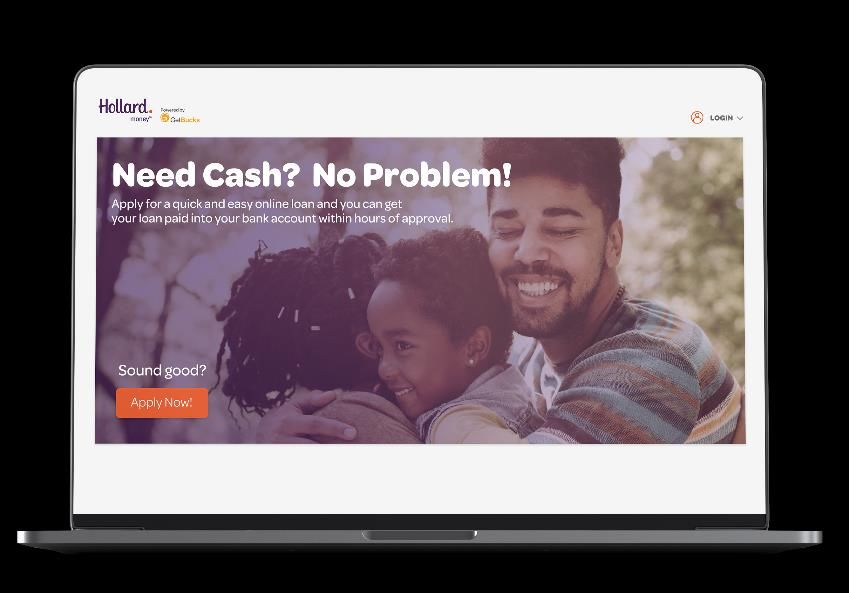

Hollard Money on-line finance solution, powered by GetBucks

• Initially short-term loans up to 6 months with plans to expand as performance is evidenced, paid for on an

origination basis (2% to 3.5% per origination)

• GetBucks risk models and balance sheet at launch, Hollard have signalled an intent to fund after 6 months at a

rate of 10% to 15% per annum

• Also access to retail store for all Hollard customers

• >2m Hollard customers driven through a white-labelled on-line solution

• Also opportunity to discuss Hollard staff payroll

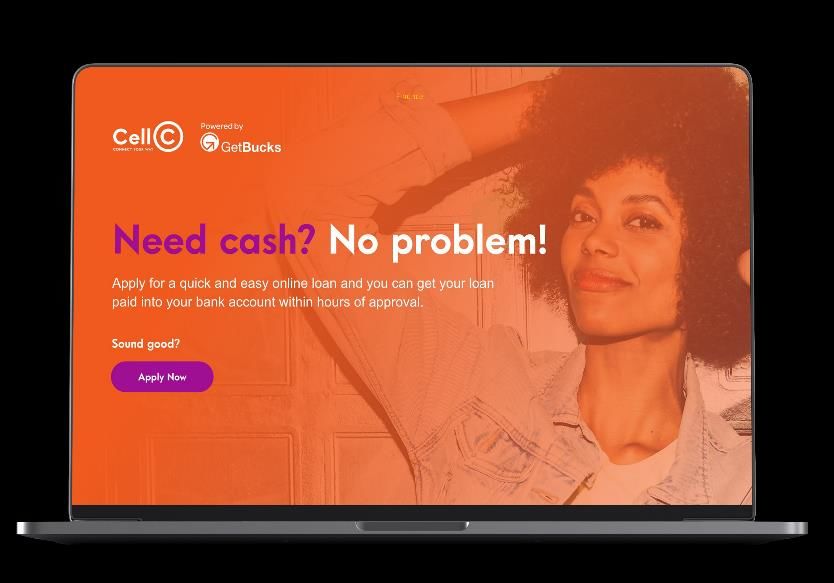

Cell C on-line finance solution, powered by GetBucks

• Cell C on-line finance solution, powered by GetBucks

• Initially short-term loans up to 6 months with plans to expand as performance is evidenced, paid for on an

origination basis (2% to 3.5% per origination)

• GetBucks risk models and balance sheet at launch

• Also access to retail store for all Cell C customers

• >1.5m Cell C customers driven through a white-labelled on-line and mobile solution

• Pre-cursor to device financing for contract and post-paid device agreements

www.getbucks.com | 23Growth through partnerships

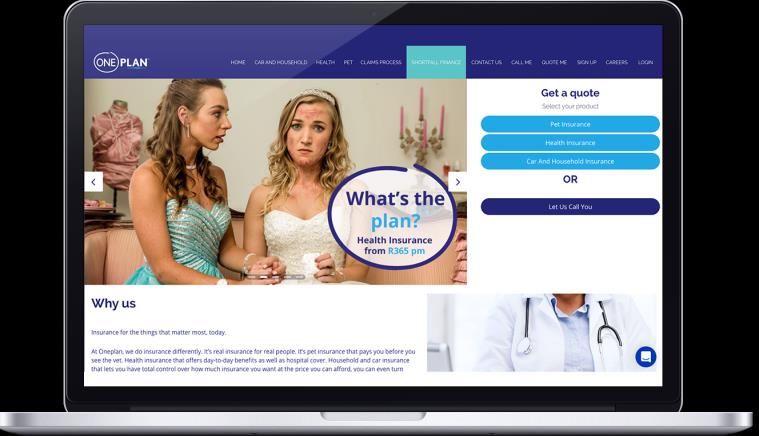

Insurance gap cover powered by GetBucks

• Short-term loans up to 6 months with plans to expand

• Access up to R8000 through an online application extending One Plan Clients the funds for

shortfalls on claims

• GetBucks risk models and balance sheet at launch

• One Plan customers driven through a white-labelled on-line solution

• Also opportunity to discuss One Plan Hollard staff payroll

GetBucks facilitates finance for educational materials

• Students and learning professionals get access up to short term credit up to R8000

over 6 months

• Branch based pilot with application assistance through agent model

• Online application to roll out as phase two.

• Third party payments made directly to Van Schaik book store. Learning goods are

released to students.

• Monthly deductions collected as loan repayment.

www.getbucks.com | 24F I N A N C I A L O U T LO O K

www.getbucks.com | 25Key Ratios Cost to income ratio

101%

Provisions and NPL’s over time 62%

55%

46%

60% 30.0%

50% 25.0%

40% 20.0% 2019 2020 2021 2022

30% 15.0%

Opex breakdown 2019

20% 10.0%

10% 5.0% Sales Expenses

Collection Costs

0% 0.0% Consulting & Professional Fees

2018 2019 2020 2021 2022 Marketing

Salaries

NPLs - LHS Provisions as % of NPV - RHS Other

www.getbucks.com | 26R 600 Loan book and NPAT growth R 120

Profit and revenue metrics R 500 R 480 R 100

R 384 R 96

R 400 R 80

Sales and book growth

R 300 R 260 R 60

700 600 R 58

R 200 R 40

R 110

600 R 100 R 31 R 20

500

R0

R0 R0

500 2019 2020 2021 2022

400

400 Loan Book (ZAR 'm) - LHS NPAT (ZAR'm) - RHS

300

300

Revenue per active loan (ZAR)

200

200

R400

R318 R325 R328 R330

100

100 R300

R200

0 0 R125

H2 2019 H1 2020 H2 2020 H1 2021 H2 2021 H1 2022 H2 2022 R100

R0

Sales (ZAR'm) - RHS Loan Book (ZAR 'm) - LHS

2018 2019 2020 2021 2022

Revenue per active loan (ZAR)

www.getbucks.com | 27Assumptions

31-Dec 2019 31-Dec 2020 31-Dec 2021 31-Dec 2022

Loans and advances to customers 160 910 471 232 075 414 315 517 475 369 850 618

Loan terms allocation 100.0% 100.0% 100.0% 100.0%

X12 Months 57.5% 50.5% 50.5% 50.5%

Loan yield 67.5% 67.9% 67.9% 67.9%

X12 Months 26.5% 27.2% 27.2% 27.2%

Collection rate 92% 92% 92% 92%

Addition funding injected into Loan Book annually* 13 895 811 69 000 000 40 000 000 20 000 000

Marginal cost of funding 12.3% 12.3% 12.3% 12.3%

*Includes funds drawn down from existing facilities, and R30 million raised pursuant to the IPO.

www.getbucks.com | 28Forecast consolidated statement of financial position

Figures in ZAR 31-Dec 2019 31-Dec 2020 31-Dec 2021 31-Dec 2022

6 months 12 months 12 months 12 months

Assets

Current Assets

Cash and cash equivalents 11 438 583 15 370 388 20 474 684 34 019 707

Loans and advances to customers 95 287 079 125 967 388 161 524 807 192 862 091

Other financial assets 15 879 239 12 249 333 12 249 333 12 249 333

Investment in insurance contracts - 2 590 074 3 490 934 4 632 684

122 604 901 156 177 183 197 739 759 243 763 816

Non-current Assets

Loans and advances to customers 45 196 189 59 748 351 76 613 805 91 477 582

Right of use asset - 1 409 582 1 319 531 1 229 480

Property and equipment 993 432 1 297 229 996 102 740 578

Intangible assets and goodwill 18 313 164 13 464 236 12 220 967 10 977 698

Deferred tax 21 673 240 21 673 240 21 673 240 21 673 240

Investment in joint ventures 1 941 748 2 325 820 2 985 820 3 711 820

88 117 773 99 918 458 115 809 465 129 810 397

Non-current assets held for sale 1 282 670 - - -

Total assets 212 005 345 256 095 640 313 549 224 373 574 213

Current liabilities

Other payables and liabilities 31 032 257 24 300 486 28 316 129 32 563 169

Other financial liabilities 49 136 571 21 525 552 32 869 582 38 147 123

80 168 828 45 826 038 61 185 711 70 710 292

Non-current liabilities

Shareholder loan 50 000 000 65 247 390 73 546 293 82 900 745

Other financial liabilities 109 524 31 770 060 49 304 374 57 220 684

50 109 524 97 017 450 122 850 667 140 121 429

Non-current liabilities held for sale 4 884 042 - - -

Equity

Share capital 65 199 525 393 335 959 392 435 488 391 242 922

Reserves 278 264 060 - - -

Retained income -266 124 806 -280 083 807 -262 922 643 -228 500 430

77 338 779 113 252 152 129 512 846 162 742 492

Non-controlling interest -495 829 - - -

Total equity and liabilities 212 005 345 256 095 640 313 549 224 373 574 213

www.getbucks.com | 29Forecast consolidated statement of cash flows

Figures in ZAR 31-Dec 2019 31-Dec 2020 31-Dec 2021 31-Dec 2022

6 months 12 months 12 months 12 months

Cash generated from/ (used in) operations -13 568 494 -32 503 673 -2 383 793 25 746 354

Net interest -2 759 265 -15 322 782 -19 207 389 -22 233 297

Tax paid -289 336 -1 531 211 -1 800 325 -2 751 351

Net cash flows used in operating activities -16 617 095 -49 357 666 -23 391 507 761 706

Cash flows from investing activities

Net investment in tangible non-current assets -60 555 -775 000 -162 500 -210 000

Acquisition of subsidiary net of cash acquired - - - -

Disposal of subsidiary -1 372 608 - - -

Purchase of other intangible assets - - - -

Payment arising from loans to Group companies and related parties -500 000 - - -

Net investment in financial assets - - - -

Net cash flows used in investing activities -1 933 164 -775 000 -162 500 -210 000

Cash flows from financing activities

Payment received from loans to Group companies and related parties 13 895 811 - - -

Addition of new equity - 50 000 000 - -

Net payments from other financial liabilities -969 085 5 581 873 28 658 304 12 993 317

Net cash flows from financing activities 12 926 726 55 581 873 28 658 304 12 993 317

Total cash movement for the year -5 623 533 5 449 208 5 104 297 13 545 023

Cash at the beginning of the year 17 021 636 9 921 180 15 370 388 20 474 684

Total cash and cash equivalents at the end of the year 11 398 103 15 370 388 20 474 684 34 019 707

www.getbucks.com | 30LEADERSHIP

www.getbucks.com | 31Meet the team

Country Executives

Mark Young Dean Crocker Jaco Coetzee

Zandile Dlamini

GetBucks

CEO CFO COO

CEO

Eswatini

Board of Directors

Charmaine Diergaardt

Takuma Mpofu Manuel Koser Matsi Modise Operations Executive,

Non-executive Director Independent non-executive director Independent non-executive director Namibia

www.getbucks.com | 32CONCLUSION

www.getbucks.com | 33Investment opportunity

Cash management / Debt opportunity

Coupon Minimum investment Warrants Rate penalty

R[100,000-500,000] For every R200 invested – you will

have the right to subscribe for 1

If withdrawn within 12

months, rate drops to 8%

(legal viability to be confirmed] Finclusion Group share at US$10

per share for a period equivalent

12% p/a

as your commitment period on

12

the credit line plus [12] months

Interest %

(e.g. one year placement is two year

Monthly / Quarterly payment, monthly warrant, three year placement is four

If withdrawn within 6

investor statements year warrant)

months, rate drops to 6%

Security Liquidity 6

Specific loan-id list to be generated and Minimum ninety days placement,

provided as security over your portfolio max three years (tbc)

www.getbucks.com | 34GetBucks South Africa

Thank you

www.getbucks.com

The Wedge, First floor

43 Garsfontein Road, Waterkloof, Pretoria

Mark Young | CEO Dean Crocker | CFO

marky@mybucks.com | 082 468 9344 dean@mybucks.com | 083 629 5986

www.getbucks.com | 35You can also read